International finance through the lens of BIS statistics: offshore activity

Offshore activity has become an integral part of international finance, with companies increasingly issuing bonds via financial affiliates abroad while banks and other financial firms channel credit through financial centres. This article leverages BIS statistics to look through residence to nationality to show who ultimately borrows and lends offshore. By revealing who borrows and which banking systems hold the exposures, BIS statistics enhance the monitoring of vulnerabilities and international spillovers.1

JEL classification: F23, F36, G15.

The conventional framework for macroeconomic analysis aligns economic and financial activity with residence and country borders. Yet multinational borrowers and creditors often transact through affiliates in financial centres abroad rather than from offices in their home market. Such offshore activity represents a sizeable share of financial activity. While enhancing financial integration, offshore activity also obscures international linkages in conventional residence-based statistics.

This article is a primer on how the BIS international banking and financial statistics can be used to analyse offshore financial activity. Offshore activity is commonly associated with indirect flows between borrowers and savers through complex corporate structures straddling borders. Several BIS data sets, especially the international debt securities (IDS) and international banking statistics (IBS), help to shed light on offshore activity by looking through the sector and residence of an entity to those of its parent, defined by its corporate headquarters. In other words, they provide a nationality view that complements the conventional residence perspective by reallocating the balance sheets of foreign affiliates to their parents.

The nationality view has a long history in BIS statistics and analysis. It had a foundational influence on the design and evolution of BIS international banking and financial statistics (CGFS (2000); Borio (2013)). Reallocation by nationality later formed the basis for broader research efforts to examine who drives economic activity, how corporate groups are interconnected and how financial vulnerabilities and spillovers might arise (Avdjiev et al (2014); Coppola et al (2021); Beck et al (2024)).

Key takeaways

- Offshore activity obscures financial links in residence-based statistics that only become clear from a nationality perspective, like that available in BIS statistics on banking and bond markets.

- Almost a third (nearly $11 trillion) of international debt securities (IDS) are issued by affiliates located outside their home country. Non-financial companies issue nearly half of IDS via non-bank financial affiliates, often in financial centres, with proceeds sometimes repatriated via intercompany loans.

- Banks' offshore affiliates, mainly in financial centres, account for over 40% of global cross-border bank lending. Corresponding statistics for portfolio investment and FDI on a nationality basis are lacking.

This primer extends the residence vs nationality analysis in McGuire et al (2024) by tracing the sectors, instruments and economies through which offshore activity is reallocated in banking and bond markets. It highlights how offshore borrowing can alter assessment of financial vulnerabilities and international spillovers when viewed from a nationality perspective, as they are obscured under the conventional residence view. It shows the extent to which non-financial corporations (NFCs) issue bonds through their foreign financial affiliates – often incorporated in financial centres – and repatriate the proceeds as intercompany loans. The residence view complicates assessments of a debtor's vulnerability to shocks that originate from foreign creditors by masking the nationality of the creditor.

The first section discusses the concept of offshore activity. The second dissects offshore debt securities issuance. The subsequent section turns to offshore lending and investment. The conclusion sketches challenges that offshore activity and related data gaps pose for financial stability analysis.

The concept of offshore activity

Offshore activity refers to financial activity abroad that is unrelated to developments in the economy where the activity takes place.2 Offshore activity takes many forms, from bond issuance in foreign markets to investment funds that pool non-residents' savings and currency trading beyond the reach of regulations that apply to transactions onshore. What these forms have in common is that the activity is ultimately driven by agents that are not residents of the jurisdiction in which it takes place.3 In that sense, offshore activity is inherently cross-border.

Offshore activity concentrates in financial centres. These range from large global centres that provide a full range of financial services, like London and New York, to those specialised in certain services and located in small economies, like the Cayman Islands and Luxembourg (Box A). Economies of scale and scope benefit global centres. At the same time, physical distance, regulation and taxation work against the tendency of financial activity to concentrate (Pogliani et al (2022)). This creates opportunities for multiple financial centres to co-exist even within time zones.

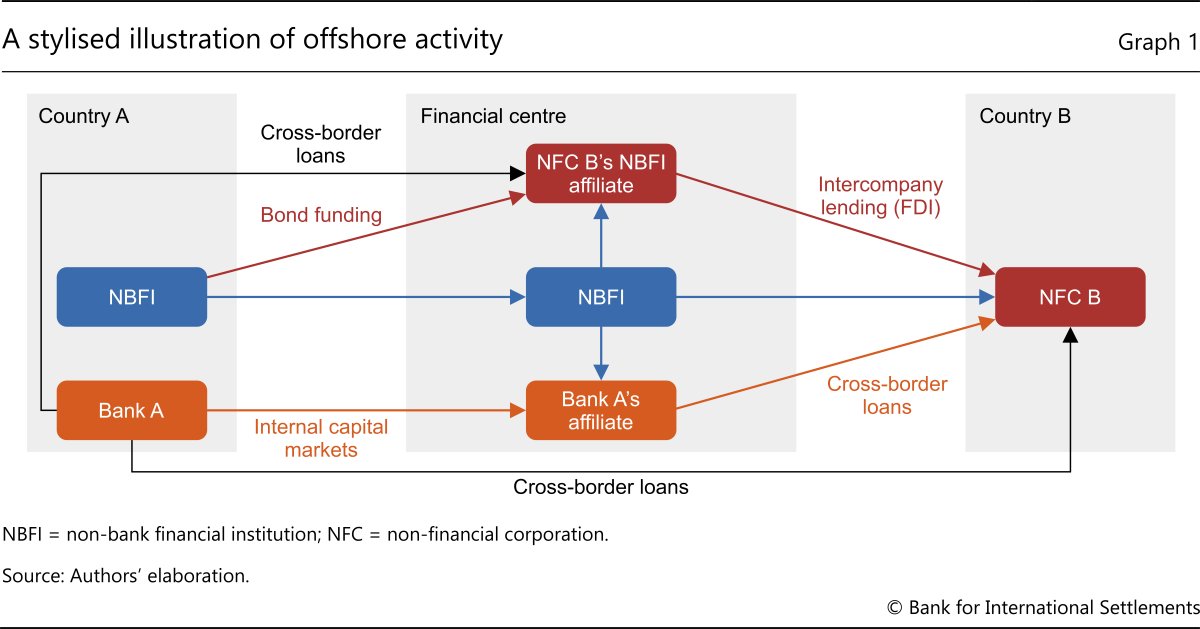

Graph 1 illustrates how offshore activity via financial centres complicates the interpretation of capital flows and external assets and liabilities. Consider a multinational firm that raises funding through an affiliate located in a financial centre. Such affiliates are often set up as special purpose vehicles (SPVs) or other types of non-bank financial institutions (NBFIs) (Graph 1, red boxes). For example, Vale, a Brazilian mining company, issues bonds through an SPV domiciled in the Cayman Islands. The proceeds might finance international operations, or be channelled to Vale's home office via an intercompany loan (red arrows). In the latter case, the issuance would be recorded in conventional balance of payments statistics as debt incurred by residents of the financial centre, while the intercompany loan would be recorded as foreign direct investment (FDI) from the financial centre to the firm's home country (ie from the Cayman Islands to Brazil).

Banks and NBFIs also use financial centres for borrowing and lending. Instead of lending directly to an NFC abroad from its head office in country A (Graph 1, black arrow at the bottom), a bank could lend indirectly via a foreign affiliate, funding the loan from its head office via internal capital markets (purple arrows). Such an indirect loan would be recorded twice: as external debt of the financial centre where the affiliate resides and as external debt of country B where the NFC is based. NBFIs similarly channel funds through and within financial centres (green boxes). For example, many hedge funds domiciled in the Cayman Islands hold US Treasuries to profit from the cash-futures basis trade (Barth et al (2025)), though most are owned or financed by entities in the United States (Bertaut et al (2021)).

The residence perspective on international finance is based on a "triple coincidence": the GDP area, currency area and location of decision-making units (and their balance sheets) are assumed to coincide with country borders (Avdjiev et al (2016)). When these align, financial transactions between residents and non-residents are driven by domestic savings and investment and subject to domestic laws and regulations. However, as Graph 1 illustrates, offshore activity multiplies linkages and distorts observed financial flows. It obscures the underlying drivers of borrowing and lending, and changes the economic interpretation of financial flows – such as FDI that behaves more like debt (Blanchard and Acalin (2016)).

Offshore activity calls for an approach that consolidates activity along lines of ownership and control. The resulting nationality perspective recognises that decision-making units straddle country borders when firms are multinational, breaking the triple coincidence. On the borrower side, linking assets and liabilities to the ultimate parent identifies the country and sector that control them. For example, bonds issued by Vale's subsidiary represent liabilities controlled by its Brazilian parent and have little relation to economic activity in the Cayman Islands. On the lender side, reallocating bank positions by nationality uncovers which institutions ultimately bear credit exposures and funding shortages (McGuire and von Peter (2009)).

The nationality view complements the residence view by providing insights into who drives decisions affecting international assets and liabilities. However, to assess who is ultimately responsible for repaying debts, information about nationality is insufficient. The extent to which a borrower's liabilities are backed by its parent depends on corporate structures and guarantees (Box B).

Offshore activity and the nationality view have a long history in BIS statistics. The initial collection of the locational banking statistics, in the 1960s, was motivated by the growth of "eurocurrency" markets, where banks borrowed and lent foreign currency from outside their home market, mostly in US dollars (McCauley et al (2021)). The expansion of offshore banking later led to the collection of the consolidated banking statistics, which put the nationality of banks at the core. The growth of the "eurobond" market in the 1980s led to the introduction of the IDS. Being compiled from data on individual securities, they have been aggregated from inception by the residence of the immediate issuer as well as the nationality of the issuer's parent (Gruić and Wooldridge (2012)).

Unmasking the offshore activities of bond issuers

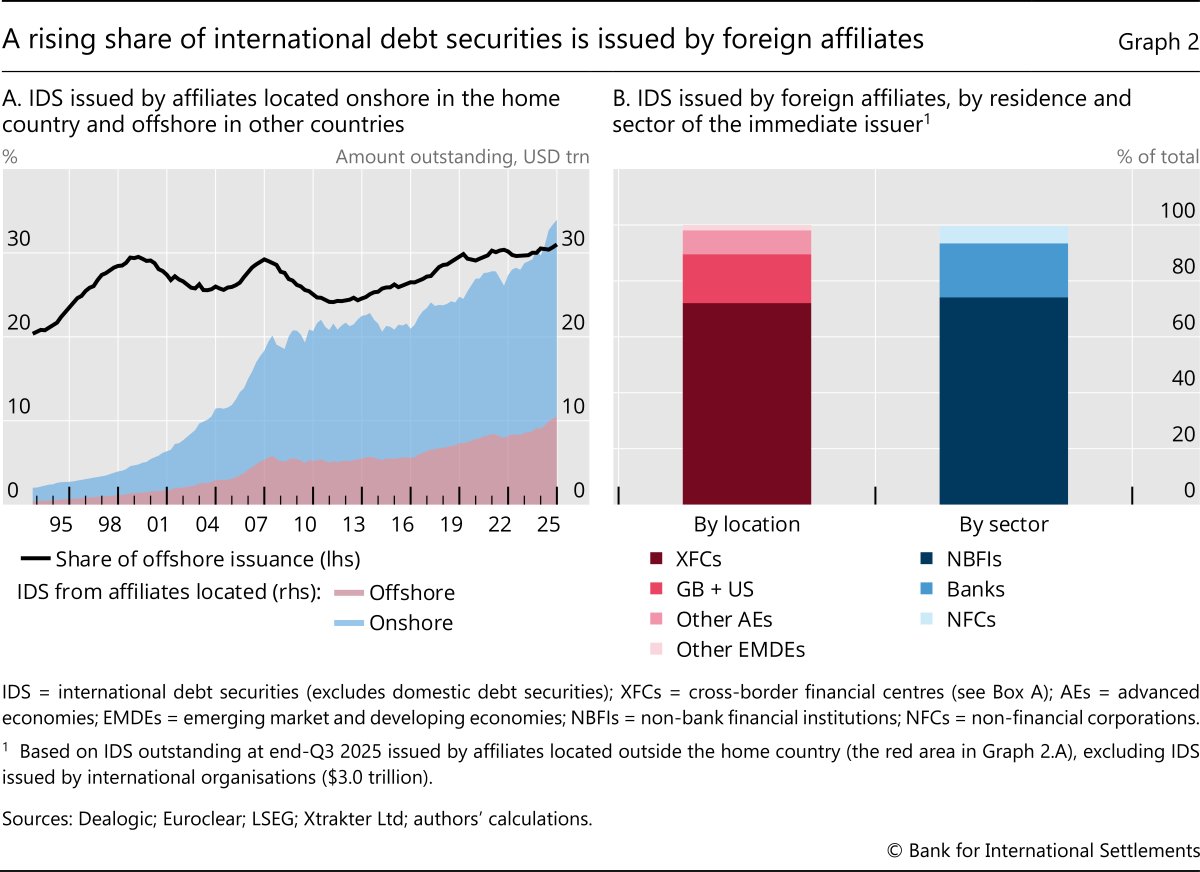

One of the markets shaped by offshore activity is the international bond market. Of the $33 trillion in international bonds outstanding at end-Q3 2025, almost $11 trillion was issued by affiliates located offshore, incorporated in countries other than where their parents were headquartered (Graph 2.A).4 Over the past three decades, issuance by such offshore affiliates has grown faster than aggregate issuance of IDS, with its share rising from around 20% in the mid-1990s to 31% in 2025.

Issuance by offshore affiliates is highly concentrated in financial centres. Global financial centres, notably London and New York, unsurprisingly play a role given their size and markets' liquidity (Graph 2.B). However, issuance is much larger from affiliates in so-called cross-border financial centres (XFCs) that cater to non-residents, like the Cayman Islands, Ireland and Luxembourg (Box A). Issuance by foreign affiliates residing in these centres is considerably larger than that from all other locations combined. Most of these foreign affiliates are NBFIs, although for many the sector of the immediate issuer is different from that of the parent.5

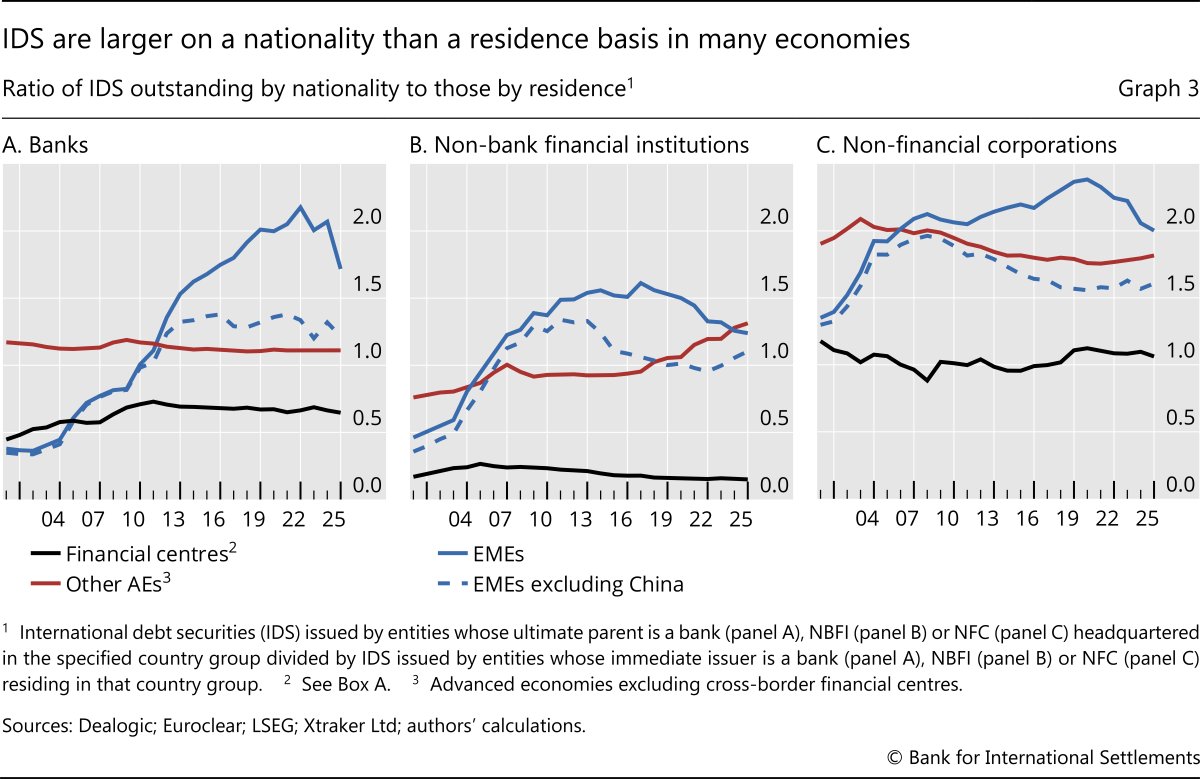

A comparison of IDS aggregated by nationality and sector of the parent versus by residence and sector of the immediate issuer illustrates how offshore activity creates a wedge between residence and nationality statistics. Graph 3 plots, for a given sector and country group, the ratio between IDS amounts outstanding by nationality and by residence. For example, for emerging market economy (EME) banks (Graph 3.A), a ratio of two indicates that IDS issued by banks with parents in EMEs are twice as large as the amounts owed by banks located in EMEs. Conventional residence-based statistics thus underestimate the consolidated debt of EME banks.

Nationality- and residence-based debt measures vary considerably across countries and sectors. For advanced economy (AE) banks, IDS issuance is similar on a nationality and on a residence basis (Graph 3.A, red line close to one). For EMEs, in contrast, the ratio shot up over the past 20 years, with Chinese banks playing a prominent role (solid and dashed blue lines). At the other extreme, for financial centres the ratio is below one, in line with the role they play in offshore activity (black line). The picture is broadly similar, though slightly less pronounced, for NBFIs (Graph 3.B). Notably, the ratio for financial centres is closer to zero than to one, since much of the issuance of NBFIs is by affiliates of foreign entities operating there.

Issuance of debt securities by offshore affiliates is most prevalent among NFCs. In general, NFCs borrow through offshore affiliates to tap deeper, diverse investor bases, raise larger amounts in longer maturities, align funding currencies with revenues and, in some cases, benefit from established international legal and market infrastructures. For AEs, the nationality-to-residence ratio in bond issuance is structurally high (Graph 3.C, red line). For EMEs, it expanded sharply after 2000 (blue lines), driven by Brazil, Russia and especially China. Excluding China, the ratio for EME NFCs is now similar to that of AE NFCs. Chinese NFCs continue to issue more through their offshore affiliates than other EMEs, even as volumes declined recently.

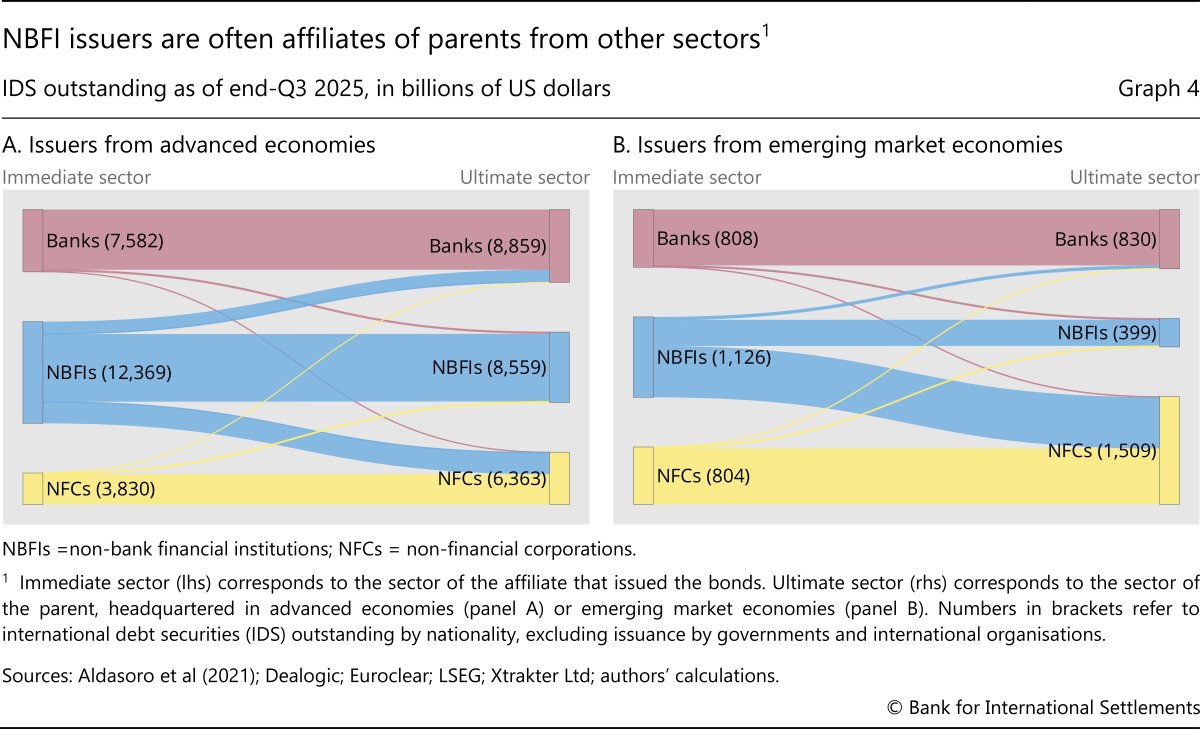

Restating bond issuance on a nationality basis also reveals the sector of the ultimate corporate parent – a reallocation that is particularly sizeable for NFCs. On an ultimate parent basis, NFCs are much more important borrowers than their issuance on an immediate borrower basis suggests. As part of their strategy for optimising funding costs and taxes, NFCs often raise funding through financial affiliates, typically NBFI subsidiaries (eg SPVs) domiciled abroad. This is more common among EME corporates due to capital account restrictions and less developed domestic markets. Of $6.4 trillion in IDS owed by AE-headquartered NFCs at end-Q3 2025, $2.6 trillion (41%) was issued by NBFI affiliates (Graph 4.A). For EME-headquartered NFCs, $0.7 trillion (48%) out of $1.5 trillion was issued by NBFI affiliates (Graph 4.B).

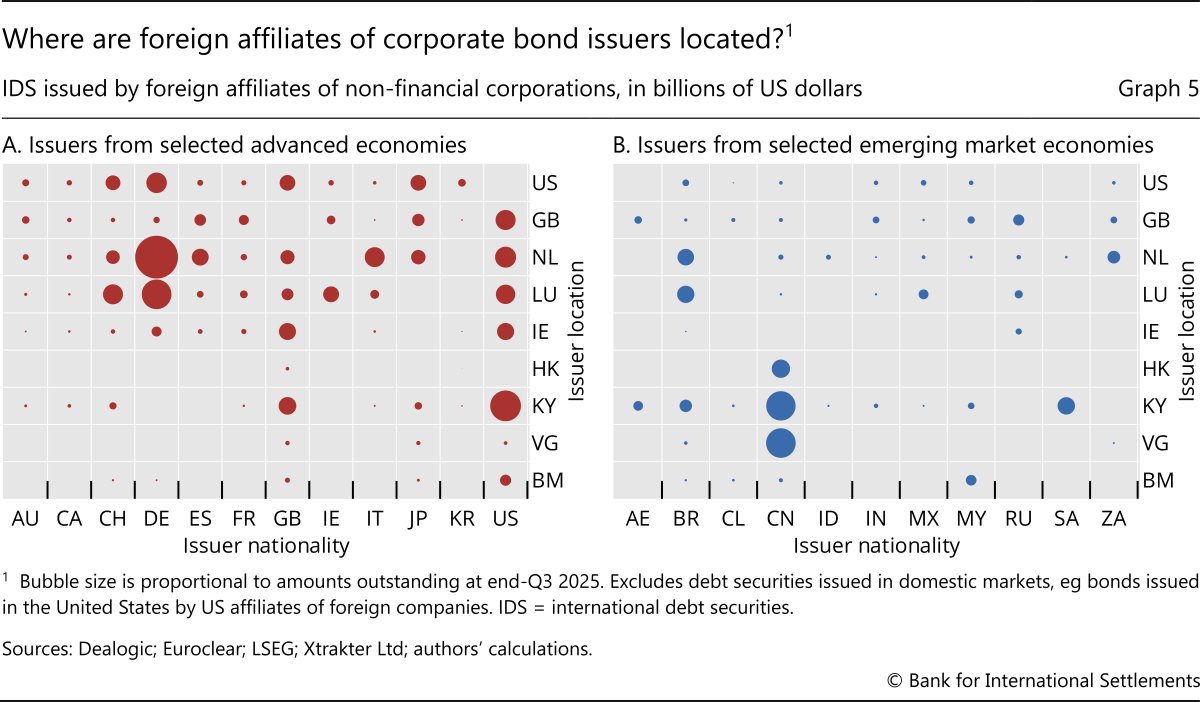

Offshore affiliates of NFCs are located in a handful of financial centres. Euro area NFCs issue relatively more from affiliates in European financial centres such as Luxembourg and the Netherlands (Graph 5.A). US NFCs rely more on affiliates in the Cayman Islands, whereas other AE NFCs (eg Swiss, UK and Japanese) issue through affiliates in a wider set of jurisdictions.

For EME NFCs, the patterns are somewhat starker. Chinese corporates stand out, issuing similar amounts through offshore affiliates as all other EMEs combined (Graph 5.B). Their offshore bond issuance is largely conducted through Caribbean centres, notably the British Virgin Islands and the Cayman Islands. Other EMEs such as Brazil and South Africa, by contrast, tend to borrow through offshore affiliates in European hubs, particularly the Netherlands and Luxembourg.

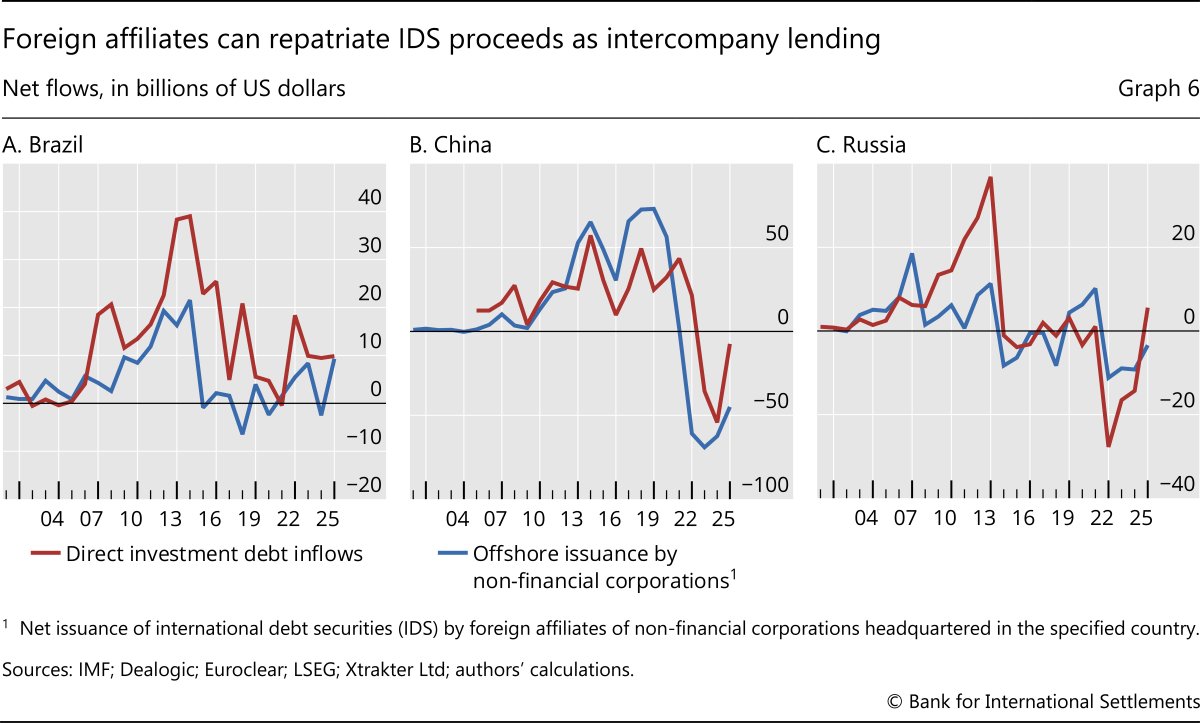

Bond issuance through offshore affiliates obscures the true nature of countries' external accounts in ways that depend on how the funds are deployed across the corporate structure. Evidence of funds from offshore issuance being transferred back to headquarters is most compelling for the largest EMEs (Avdjiev et al (2014)). Comparing offshore issuance with direct investment debt inflows to the home country reveals a strong correlation for Brazil, China and Russia (Graph 6), indicating that intercompany debt inflows tend to rise in periods when more debt is issued by offshore affiliates and fall when new issuance slows. As described in the previous section, this creates two external account entries for one issuance: a portfolio debt liability inflow into the financial centre, and an FDI liability inflow into the home country (with a corresponding FDI asset outflow from the financial centre).

Reallocating offshore lending and investing

Understanding a debtor's vulnerability to shocks originating abroad requires knowing who its creditors are. For example, a shock to the consolidated balance sheet of the lending bank might lead it to reduce lending to borrowers, including unaffected ones, in order to restore its capital adequacy ratio, meet margin calls or adhere to value-at-risk or similar models (Kaminsky and Reinhart (1999)). Data by residence mask the identity of some creditors when lending and investing takes place offshore, routed via intermediaries in financial centres. Residence data thus obscure a debtor's vulnerability to international spillovers via creditors. The nationality perspective in the IBS sheds light on this issue, at least for intermediation via banks.

Further reading

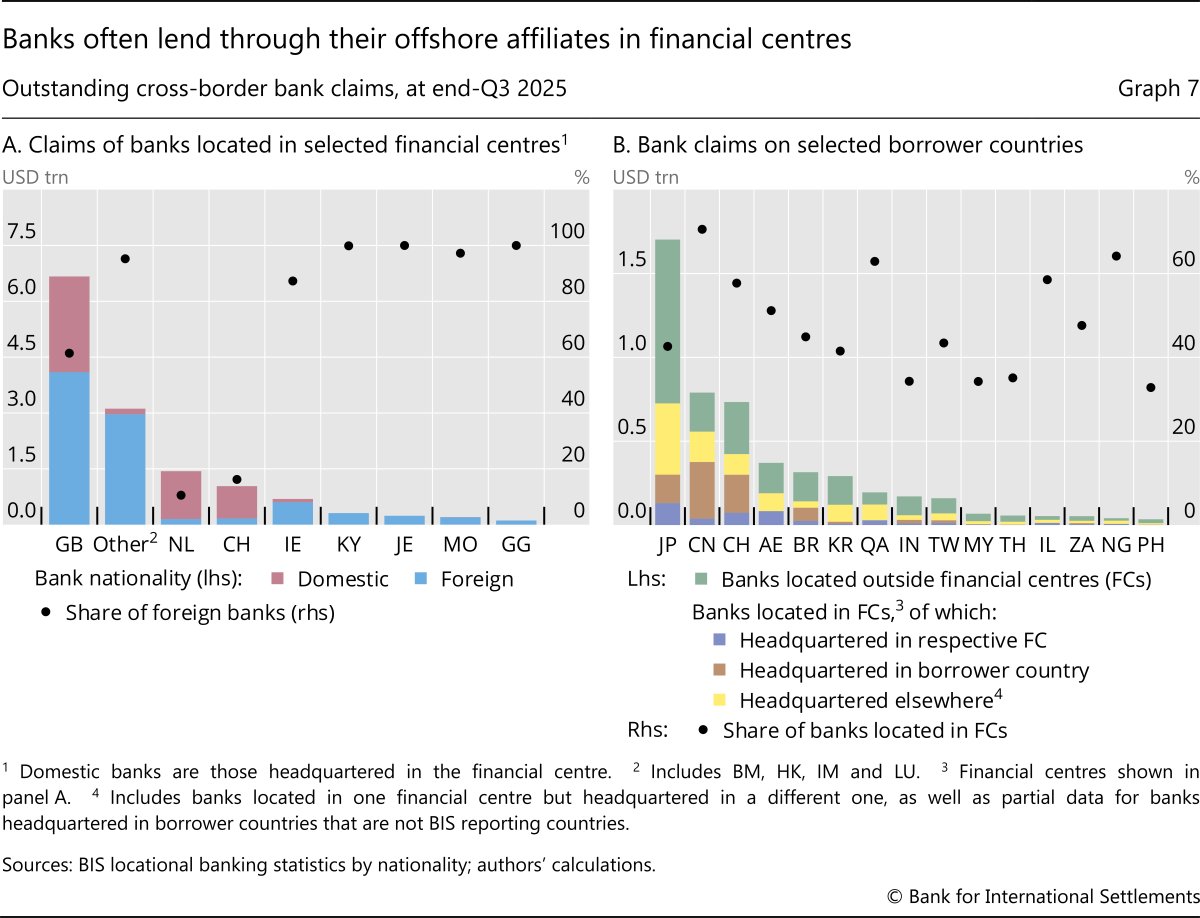

Bank credit intermediated through financial centres represents a large share of overall bank cross-border credit. Credit extended from banks' home offices accounts for less than 60% of their cross-border claims; the remainder is extended via their foreign affiliates, located mainly in financial centres. The United Kingdom is the largest centre for such offshore banking activity, followed by Hong Kong SAR (Graph 7.A, blue bars). Bank business models, as well as differences in regulation and tax treatment, are important factors in banks' choice to operate in financial centres.6

Looking through credit intermediated through financial centres materially changes the source of bank credit for borrower countries. Borrowers in many countries rely on cross-border borrowing from banks located in financial centres (Graph 7.B, black dots), most of which are headquartered elsewhere. For some borrower countries, banks headquartered in the very same country are among the largest cross-border creditors. Over 40% of cross-border bank credit to borrowers in mainland China is extended by the offices of Chinese banks in financial centres outside the mainland, mainly in Hong Kong SAR (brown bars). Similarly, a quarter of cross-border bank credit to Brazil is from Brazilian bank offices in financial centres outside Brazil, mainly in the Cayman Islands and the Bahamas.

Whereas offshore activity (and the attendant distortions in residence-based statistics) was once synonymous with banking activity, over the past few decades NBFIs have expanded their presence offshore. For example, many asset management companies have incorporated funds in financial centres to invest in bonds and equities globally. Unlike for banks, information about who owns and controls the portfolios of NBFIs is not readily available. BIS statistics provide some information about banks' foreign bond holdings, but their share of total foreign bond holdings is small. BIS banking statistics can shed light on the scale and geographical distribution of NBFIs' activities only through their links with banks (Box C). However, these links are recorded on a residence basis and do not identify NBFIs' nationality.

Conclusions

Offshore activity complicates financial stability analysis by obscuring links between related entities because multinational firms and banks borrow and lend through their affiliates worldwide. BIS statistics help to reveal those links by looking through the geography of bond issuance (in IDS) and bank credit (in IBS) to the nationality of the entities involved. Reallocating offshore activity by nationality thus highlights financial vulnerabilities that might not be evident from residence data alone.

Despite the importance of the nationality view, international statistics remain incomplete. In particular, comprehensive statistics on a nationality basis for portfolio investment and other positions are lacking. NBFIs manage vast portfolios through affiliates in financial centres, but identifying ultimate ownership or control requires piecing together various granular data sets (Coppola et al (2021); Beck et al (2024)). Closing these data gaps with official statistics would represent a major public good.

References

Aldasoro, I and T Ehlers (2017): "Risk transfers in international banking", BIS Quarterly Review, December.

Aldasoro, I, W Huang and E Kemp (2020): "Cross-border links between banks and non-bank financial institutions", BIS Quarterly Review, September.

Aldasoro, I, B Hardy and N Tarashev (2021): "Corporate debt: post-GFC through the pandemic", BIS Quarterly Review, June.

Avdjiev, S, M Chui and H S Shin (2014): "Non-financial corporations from emerging market economies and capital flows", BIS Quarterly Review, December.

Avdjiev, S, R McCauley and H S Shin (2016): "Breaking free of the triple coincidence in international finance", Economic Policy, vol 31, issue 87.

Barth, D, D Beltran, M Hoops, J Kahn, E Liu and M Perozek (2025): "The cross-border trail of the Treasury basis trade", FEDS Notes, October.

Beck, R, A Coppola, A Lewis, M Maggiori, M Schmitz and J Schreger (2024): "The geography of capital allocation in the euro area", ECB Working Paper Series, no 3007.

Bertaut, C, B Bressler and S Curcuru (2021): "Globalization and the reach of multinationals: implications for portfolio exposures, capital flows, and home bias", Journal of Accounting and Finance, vol 21, no 5.

Blanchard, O and J Acalin (2016): "What does measured FDI actually measure", PIIE Policy Brief 16-17.

Borio, C (2013): "The Great Financial Crisis: setting priorities for new statistics", BIS Working Papers, no 408.

Committee on the Global Financial System (CGFS) (2000): "Report of the Working Group on the BIS international banking statistics", CGFS Papers, no 15.

Coppola, A, M Maggiori, B Neiman and J Schreger (2021): "Redrawing the map of global capital flows: the role of cross-border financing and tax havens", Quarterly Journal of Economics, vol 136, no 3.

García Luna, P and B Hardy (2019): "Non-bank counterparties in international banking", BIS Quarterly Review, September

Gruić, B and P Wooldridge (2012): "Enhancements to the BIS debt securities statistics", BIS Quarterly Review, December.

Kaminsky, G and C Reinhart (1999): "The twin crises: The causes of banking and balance-of-payments problems", American Economic Review, vol 89, no 3.

Hardy, B, P McGuire and G von Peter (2024): "International finance through the lens of BIS statistics: bank exposures and country risk", BIS Quarterly Review, September.

Lane, P and G M Milesi-Ferretti (2018): "The external wealth of nations revisited: International financial integration in the aftermath of the global financial crisis", IMF Economic Review vol 66.

McCauley, R, P McGuire and P Wooldridge (2021): "Seven decades of international banking", BIS Quarterly Review, September.

McGuire, P and G von Peter (2009): "The US dollar shortage in global banking", BIS Quarterly Review, March.

McGuire, P, G von Peter and S Zhu (2024): "International finance through the lens of BIS statistics: residence vs nationality", BIS Quarterly Review, March.

Milesi-Ferretti, G M (2026): "The external wealth of nations database", the Brookings Institution, 6 February.

Pogliani, P, G von Peter and P Wooldridge (2022): "The outsize role of cross-border financial centres", BIS Quarterly Review, June.

Pogliani, P and P Wooldridge (2022): "Cross-border financial centres", BIS Working Paper, no 1035.

Footnotes

1 The views expressed in this publication are those of the authors and not necessarily those of the BIS or its member central banks. This is the eighth article in a series showcasing the BIS international banking and financial statistics. We thank Stefan Avdjiev, Torsten Ehlers, Jon Frost, Carlos Mallo, Patrick McGuire, Benoît Mojon, Swapan-Kumar Pradhan, Daniel Rees, Andreas Schrimpf, Hyun Song Shin, Frank Smets and Sonya Zhu for helpful comments and Jeemin Son for excellent research assistance.

2 A narrower notion of offshore activity emerged from the rise of eurocurrency markets in the 1950s and 1960s, where the defining characteristic is that activity is denominated in a currency that is foreign to both counterparties (McCauley et al (2021)).

3 That is, offshore activity excludes business driven by the domestic supply of or demand for funds.

4 In order to classify an issue in the IDS statistics, the BIS assesses: (i) the residence of the immediate issuer; (ii) the location of the issue's registration; (iii) the governing law; and (iv) the listing location. When all four characteristics refer to the same country, the issue is classified as a domestic debt security. When at least one points to a different country, it is instead classified as international. See Box A in Aldasoro et al (2021) for further details.

5 Governments, the largest players in the global bond market, do not have offshore affiliates and mostly issue local currency bonds through their domestic debt offices.

6 Banks that adopt a centralised model typically channel a sizeable portion of their international business via financial centres, often through branches. Conversely, banks that follow a decentralised model operate primarily through locally incorporated and capitalised subsidiaries and thus have less of an offshore presence (Hardy et al (2024)).