Risk transfers in international banking

Credit risk transfers shift a bank's country exposures from one counterparty country to another. Risk transfer patterns can shed light on how creditor banking systems assess and manage credit risks across counterparty countries. These patterns are closely linked to the business models and international footprint of global banks and corporates. Global banks have taken on more credit risks vis-à-vis some major emerging market economies - in particular in Asia. This points both to the enlarged international footprint of corporates and banks from these countries, and to the willingness of global banks to retain these country exposures on their balance sheets instead of seeking guarantees or hedging them.1

International risk transfers shift a bank's exposure from one counterparty country to another. They include parent and third-party guarantees, credit derivatives (protection purchased) and collateral.2 Risk transfers are therefore conditional claims, which materialise when an immediate borrower cannot service its debts.3

Risk transfers reallocate banks' exposures from the immediate counterparty country to the country where the ultimate obligor is located. They can be either outward risk transfers, which result in a reduction in banks' risk exposures to a given counterparty country, or inward risk transfers, which increase them. However, the underlying risk does not disappear, but is merely reallocated, since an outward risk transfer vis-à-vis one country is an inward risk transfer vis-à-vis the country that becomes the ultimate obligor. Claims in the BIS consolidated banking statistics (CBS) are reported on both an immediate counterparty (IC) and an ultimate risk (UR) basis.

Net risk transfers (NRTs), defined as the difference between inward risk transfers and outward risk transfers, introduce a wedge between a reporting country's banking system claims on an IC and a UR basis (box).

This feature assesses the size, scope and evolution of international risk transfers. The use of risk transfers by BIS reporting banks is mainly determined by the riskiness of counterparty countries. Therefore, risk transfers can shed light on how creditor banking systems assess and manage credit risks across counterparty countries. This is closely linked to the business models and international footprint of global banks and corporates.

There have been a number of important structural shifts in risk transfers in the past decade. To be sure, some patterns have remained unchanged. Banks have continued to transfer credit risks out of international financial centres and riskier countries, and into advanced economies.4 Even so, there has been a significant change in patterns vis-à-vis emerging market economies (EMEs), as banks have increased credit exposures to emerging Asia. This has been driven in part by the expanding international footprint of EME corporates and banks. It may also reflect creditor banks' growing willingness to retain risk exposures to these countries as their economic strength and creditworthiness have improved.

Interpreting risk transfers in the BIS consolidated banking statistics

The BIS consolidated banking statistics (CBS) record net risk transfers, as well as gross inward and outward risk transfers. Inward risk transfers increase the credit risk exposures vis-à-vis a given counterparty country, whereas outward risk transfers reduce them, by passing them on to another counterparty country. Net risk transfers (NRTs) are defined as inward risk transfers minus outward risk transfers.

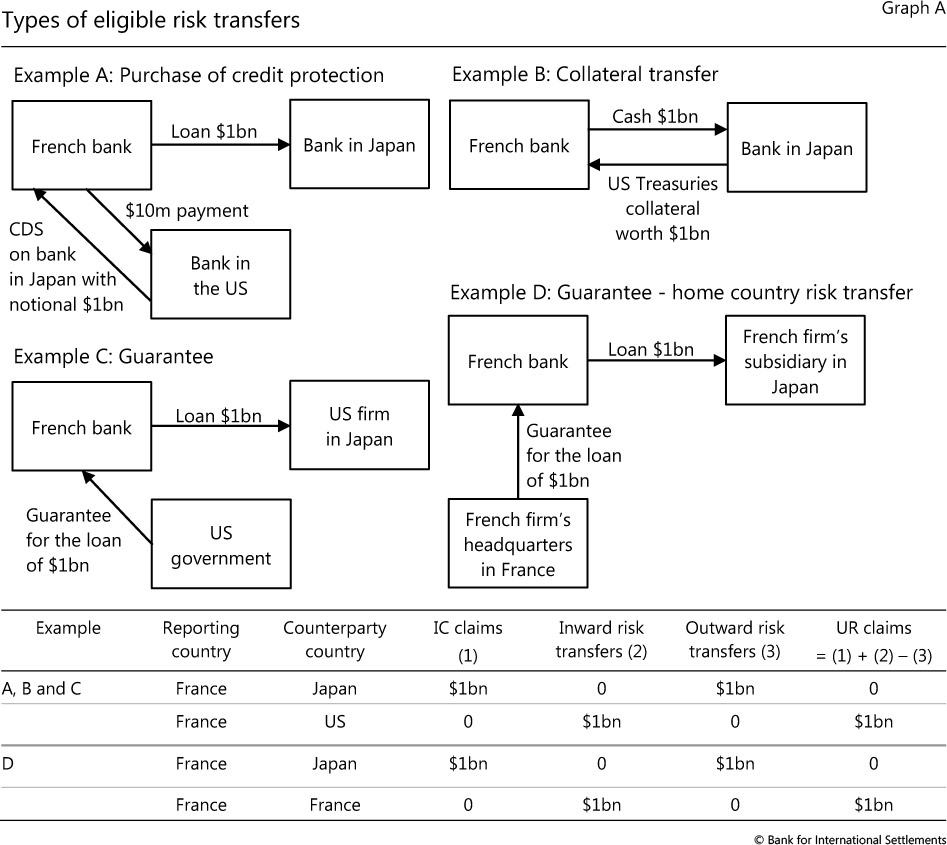

There are three types of eligible risk transfers for a creditor bank: parent and third-party guarantees, credit derivatives (protection purchased) and collateral transfers (see examples A-D in Graph A). A major share of risk transfers occurs either between internationally active banks or between a bank and a non-bank financial institution. For instance, in a collateralised borrowing transaction between banks, such as a repurchase agreement (example B), a creditor bank transacts with another bank to transfer the credit risk exposure vis-à-vis the counterparty country to the country of the collateral issuer (eg the United States in the case of US Treasury collateral).

Internationally active banks and other financial institutions also commonly buy and issue credit derivatives, such as credit default swaps (CDS, example A). If a creditor bank purchases a CDS from an entity located in country A to hedge an exposure to country B, the bank records an inward risk transfer vis-à-vis country A and an outward risk transfer vis-à-vis country B, both equal to the notional amount of protection purchased. Analogously, explicit guarantees transfer risk to the guarantor (example C). A special case in the CBS are credit exposures vis-à-vis foreign branches of banks. Consistent with standards set out by the Basel Committee on Banking Supervision, claims on bank branches are assumed to be guaranteed by the headquarters, even if no explicit guarantees are in place. In all other cases, guarantees need to be explicit.

In all of the above examples, credit exposures vis-à-vis a foreign counterparty may also be transferred to another institution in the home country (home country risk transfer). Home country risk transfers are typically driven by globally active firms in the home country (example D). Another example would be export or foreign direct investment credit guarantees provided by the government of the home country. Risk transfers vis-à-vis the home country therefore provide a measure of the share of foreign credit exposures that are ultimately against counterparties in the home country of the creditor bank. As risk transfers merely reallocate risks, but do not reduce or increase overall credit risk from the point of view of the creditor country, net risk transfers across all counterparty countries sum to zero. Risk transfers vis-à-vis foreign countries and home country risk transfers therefore mirror each other.

Risk transfers vis-à-vis foreign countries and home country risk transfers therefore mirror each other.

The treatment of collateral, however, varies across reporting countries. Risk transfers are likely to be underreported, as some countries do not report risk transfers related to repos or exchanges of collateral. On the other hand, inward and outward risk transfers may overstate cross-border transfers because some reporting countries include risk transfers between counterparties within the same country. The sum of risk transfers vis-à-vis foreign countries and the home country can deviate from zero due to reporting errors and omissions.

The global reallocation of banks' credit risks

The spectrum of banks' credit risk transfers across a wide range of counterparty countries illustrates how differences in global banks' business models, the international footprint of corporates and the riskiness of counterparty countries drive global reallocations of banks' credit risks.

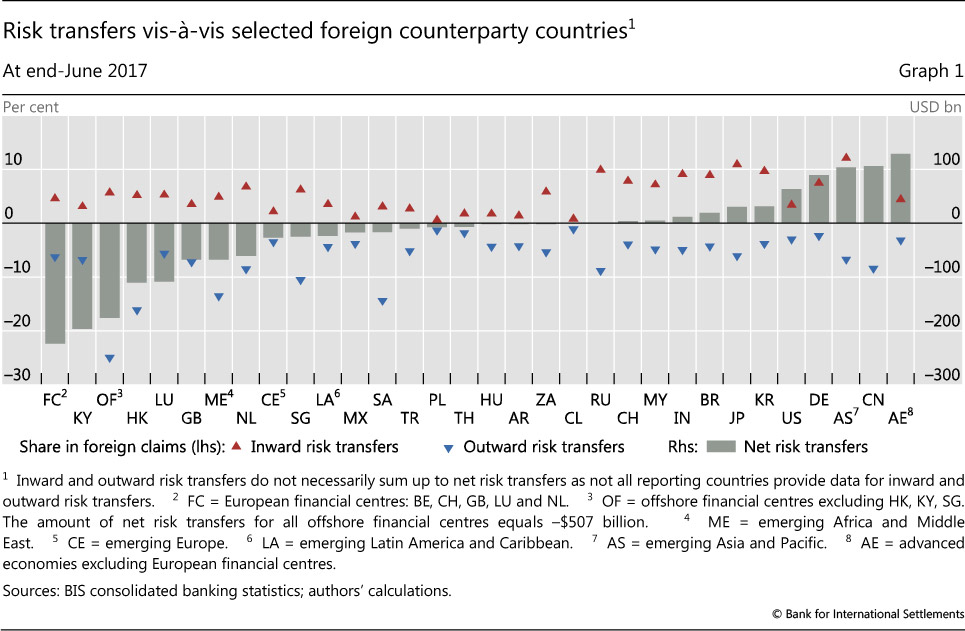

Banks transfer a large amount of credit risk out of financial centres, such as the United Kingdom or the Cayman Islands. This is reflected in large negative NRTs vis-à-vis these jurisdictions (Graph 1, grey bars). Large banks from advanced economies as well as EMEs maintain branches in European and offshore financial centres. Guarantees from the parent bank5 transfer the risk out of the financial centre where the branch is located and into the home country of the parent bank. Analogously, risk is transferred out of an offshore financial centre if a corporate issues bonds through a financial holding company domiciled there, and the parent company guarantees the bonds.6

Risk transfers out of financial centres are the largest negative NRTs globally. For instance, at end-June 2017 credit risks with a notional value of close to $200 billion (16% of foreign claims on an IC basis) were transferred out of the Cayman Islands on a net basis. For European financial centres (including Belgium, Luxembourg, the Netherlands, Switzerland and the United Kingdom) NRTs amounted to around -$220 billion.

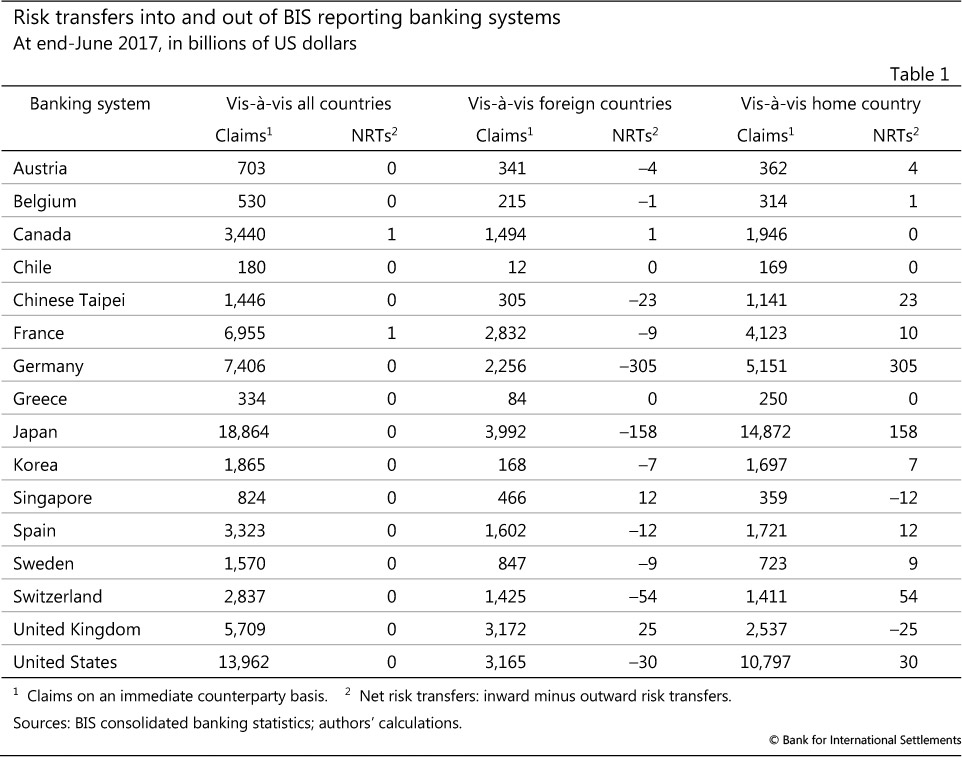

At the other end of the spectrum are those advanced and emerging market economies where international banking business primarily reflects the activity of locally headquartered banks, such as China, Germany, Japan, Korea or the United States. To some extent, this is a mirror image of risk transfers out of financial centres: one driver of the large positive NRTs are advanced economy parent banks' guarantees to their branches located in financial centres. Further, these economies are home to large globally active non-financial firms. If bank claims on the foreign operations of these firms are guaranteed by the parent or third parties in the home country (eg through government export or investment guarantees), banks' credit risks are transferred back into those countries. Indeed, home country risk transfers are also significant for the large economies mentioned above (Table 1). For some major economies, such as the US or Germany, a relevant share of positive (inward) risk transfers results from the use of their government securities as collateral in secured borrowing transactions (Graph A, example B).

The other key determinant of banks' international risk transfers is the perceived riskiness of counterparty countries. For instance, NRTs vis-à-vis countries in the Middle East and Africa, as well as most countries in Latin America, are negative (Graph 1). At the same time, risks are transferred into advanced economies on a global level. The ratio of outward risk transfers to foreign claims on an IC basis (a kind of "hedge ratio") best captures the degree to which global banks hedge risks vis-à-vis certain counterparty countries (Graph 1, blue triangles). Whether these hedges are effective, however, depends on the probability of double default of the borrower and the ultimate obligor.

The evolution of international risk transfers

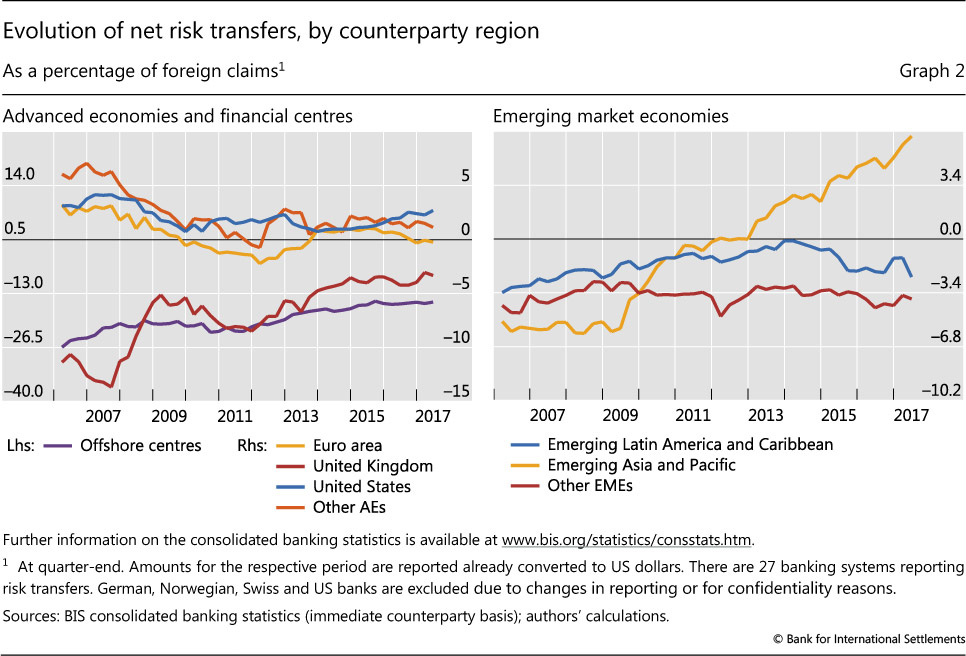

While NRTs vis-à-vis advanced economies and financial centres have been largely stable since the Great Financial Crisis (Graph 2, left-hand panel),7 banks' risk transfers vis-à-vis EMEs - in particular emerging Asia - have changed substantially (right-hand panel). In early 2007, reporting banks transferred around 5.7% of their net exposures out of emerging Asia; by mid-2017, they reported net transfers into the region equalling 6.5% of their foreign IC claims on the region. Underlying the shift in NRTs vis-à-vis emerging Asia is a change in the composition of creditor banking systems. As European banks retreated, banks from Chinese Taipei, Hong Kong SAR, Japan and Singapore increased their exposures to emerging Asia. In Latin America and other emerging market regions, outward risk transfers have continued to exceed inward risk transfers, as reporting banks, in aggregate, choose to offload their exposures vis-à-vis countries in these regions.

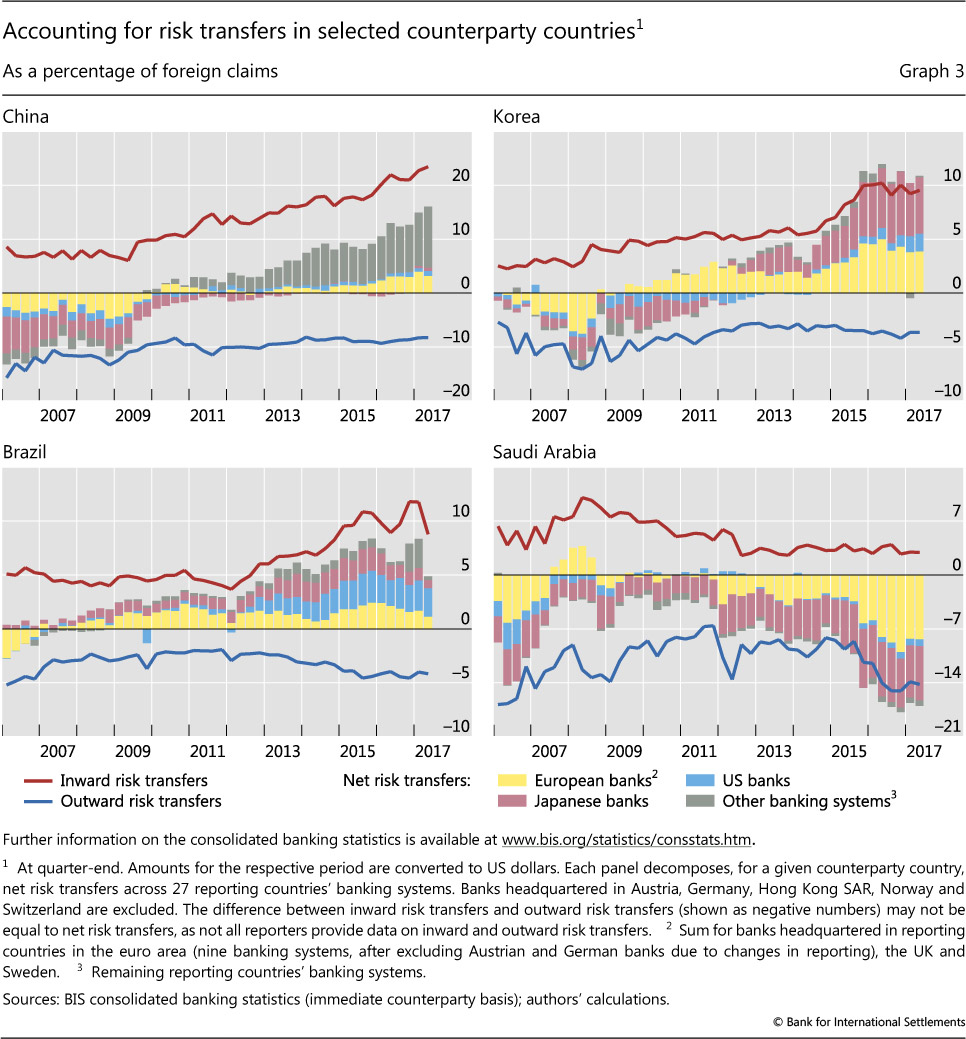

To better understand the drivers of NRTs, Graph 3 decomposes net risk transfers vis-à-vis selected EMEs into the different contributions of BIS reporting banking systems, and plots both outward and inward risk transfers as a percentage of foreign claims on an IC basis.

Different forces have driven these developments in NRTs vis-à-vis EMEs. For countries such as China and Korea, they can be largely explained by the strong rise in inward risk transfers. This probably reflects the increased global footprint and international role of both banks and corporates from these countries.8 The case of Brazil is quite similar, though outward risk transfers have also grown. Most likely this can be attributed to Brazil's recent economic downturn, which led to a deterioration in its sovereign credit rating and thus a search for non-Brazilian entities willing to guarantee exposures to Brazilian borrowers. Finally, the decline in NRTs for Saudi Arabia is largely accounted for by greater outward risk transfers. Given the decline in oil prices since 2014 and the associated economic challenges, such as a weakening of external positions, creditors may have been seeking to lower their risk exposures vis-à-vis oil-exporting countries in the Middle East.9

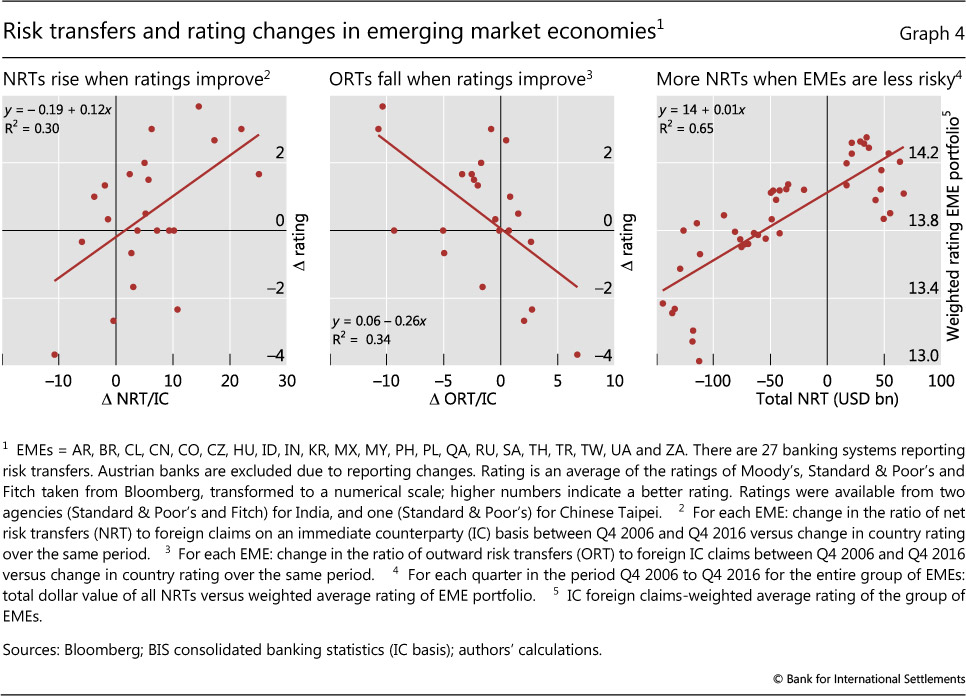

Graph 4 examines in more detail the relationship between banks' risk transfers to EMEs and the creditworthiness of the counterparty country. Changes to the riskiness of the counterparty are proxied by changes in the country's sovereign credit rating. From 2006 to 2016, NRTs as a share of foreign claims on an IC basis tended to increase for major EMEs with improved ratings (Graph 4, left-hand panel). Likewise, outward risk transfers (also as a share of foreign IC claims) decreased vis-à-vis those countries with improved ratings, ie transfers fell as the perceived strength of the country improved (Graph 4, centre panel). The same relationship is apparent when we compare total NRTs vis-à-vis major EMEs with the riskiness of a broad EME portfolio, as measured by a claims-weighted average rating across 22 large EMEs (Graph 4, right-hand panel).

1 Starting with this issue of the BIS Quarterly Review the regular chapter on "Highlights of global financial flows" will be replaced with a short essay on structural or cyclical trends in the global financial system, drawing on the BIS international banking, derivatives and securities statistics. Commentary on quarter-to- quarter changes in the statistics can be found in the statistical releases posted on the BIS website at www.bis.org/statistics/index.htm. Statistical support was provided by Zuzana Filkova. The views expressed in this article are those of the authors and do not necessarily reflect those of the BIS.

2 For examples of how different risk transfers are recorded in the BIS consolidated banking statistics, see the box and "Highlights of the BIS international statistics", BIS Quarterly Review, March 2011, pp 16-17.

3 See BIS, Potential enhancements to the BIS international banking statistics: report submitted by a Study Group established by the BIS, March 2017. The eligibility criteria for risk transfers within the BIS consolidated banking statistics are similar to those in the Basel Committee on Banking Supervision's risk mitigants for calculating risk-weighted exposures. The main difference concerns the treatment of collateral, which under Basel Committee standards is deducted from claims.

4 See Committee on the Global Financial System, Improving the BIS international banking statistics, CGFS Papers, no 47, November 2012; and S Avdjiev, P McGuire and P Wooldridge, "Enhanced data to analyse international banking", BIS Quarterly Review, September 2015, pp 53-68.

5 Claims on branches are assumed to be guaranteed by the parents, generating outward (negative) risk transfers vis-à-vis the country where the branch is located. See also the box.

6 For example, consider a corporate from an EME that issues bonds in an offshore financial centre. If the bonds are held by an advanced economy reporting bank, this will be reflected in an IC claim of the advanced economy's banking system on the offshore centre. However, provided there is a parent guarantee, the ultimate obligor is the EME in which the corporate is headquartered: on a UR basis the claim is vis-à-vis the EME and not the offshore centre.

7 Banks did shift risk out of euro area countries around the time of the European sovereign debt crisis, but this abated towards the end of 2013.

8 For example, if BIS reporting banks have large and growing exposures to the branches and subsidiaries of Chinese banks located all over the world, and if these exposures (as is likely) benefit from a guarantee from the Chinese bank parent, this would show up as gross inward risk transfers to China.

9 See "Highlights of the BIS international statistics", BIS Quarterly Review, June 2017, pp 5-7. Graph 3 presents data for only Saudi Arabia for illustrative purposes. However, a similar pattern emerges in terms of NRTs for other oil-exporting countries such as Egypt, Oman and the United Arab Emirates.