Rise of the central bank digital currencies: drivers, approaches and technologies

Update – March 2024

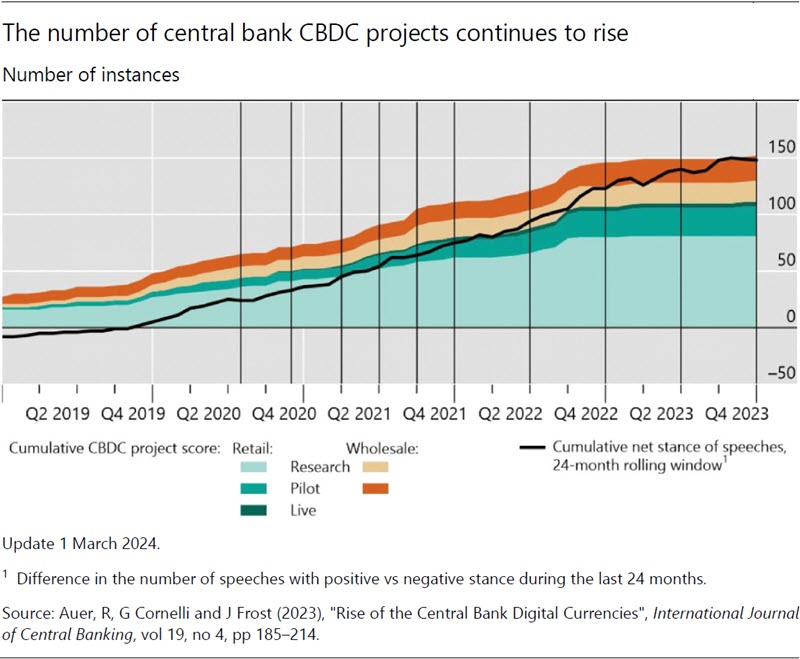

Updated dataset on CBDC projects around the world.

There are four live retail CBDCs in the world – in The Bahamas, the Eastern Caribbean, Nigeria and Jamaica. Pilots of retail CBDCs are now taking place in 24 jurisdictions and 23 jurisdictions have wholesale CBDC pilots.

Summary

Focus

Central bank digital currencies (CBDCs) are in the limelight. But the reasons for issuing them vary between countries, as do the policy approaches and technical designs. This paper looks at the economic and institutional motives behind current CBDC projects and asks how they might shape the design of such currencies.

Contribution

We draw up a database of research and development work, technical approaches and policy stances for the issuance of CBDCs. We assess the policy stance based on a database of more than 16,000 central bank speeches. We also take stock of actual development efforts, providing a taxonomy of technical designs from all relevant policy and analytical publications published by central banks worldwide. Next we look at the drivers of CBDC projects by relating development intensity to the economic and institutional differences between countries. Based on public reports and interviews with central bank experts, we set out the policy approaches behind three CBDC projects: China's Digital Currency Electronic Payments (DC/EP), Sweden's e-krona and the Bank of Canada's CBDC contingency plan.

Findings

On the drivers for CBDC development, we find that most projects originate in digitised and innovative economies. Retail CBDC work is more advanced where the informal economy is larger. None of the projects surveyed seeks to replace cash - all aim to offer a digital complement.

On the technical designs, we find that more and more central banks are considering "Hybrid" or "Intermediated" architectures, where the CBDC is a cash-like direct claim on the central bank but the private sector manages all customer-facing activity. Only a few jurisdictions are considering "Direct" designs, in which the central bank takes on some or all of the customer-facing side of payments. At present, no central bank reports that it is pursuing a "Synthetic" or "Indirect" CBDC design.

While central banks are considering various technical infrastructures, current proofs-of-concept tend to be based on distributed ledger technology rather than a conventional infrastructure. Access frameworks tend to be based on account identification rather than allowing for token-based anonymity. Most retail CBDC projects have a domestic focus.

Abstract

Central bank digital currencies (CBDCs) are receiving more attention than ever before. Yet the motivations for issuance vary across countries, as do the policy approaches and technical designs. We investigate the economic and institutional drivers of CBDC development and take stock of design efforts. We set out a comprehensive database of technical approaches and policy stances on issuance, relying on central bank speeches and technical reports. Most projects are found in digitised economies with a high capacity for innovation. Work on retail CBDCs is more advanced where the informal economy is larger. We next take stock of the technical design options. More and more central banks are considering retail CBDC architectures in which the CBDC is a direct cash-like claim on the central bank, but where the private sector handles all customer-facing activity. We conclude with an in-depth description of three distinct CBDC approaches by the central banks of China, Sweden and Canada.

Online annex (pdf)

- as of March 2024

- as of July 2023

- as of 13 January 2023

- as of 1 July 2022

- as of 1 January 2022

- as of 1 October 2021

- as of 1 July 2021

- as of 5 April 2021

- as of 1 December 2020

- as of 24 August 2020

JEL classification: E58, G21

Keywords: central bank digital currency, CBDC, central banking, digital currency, digital money, distributed ledger technology, blockchain

{kind=link}