Derivatives trading in OTC markets soars

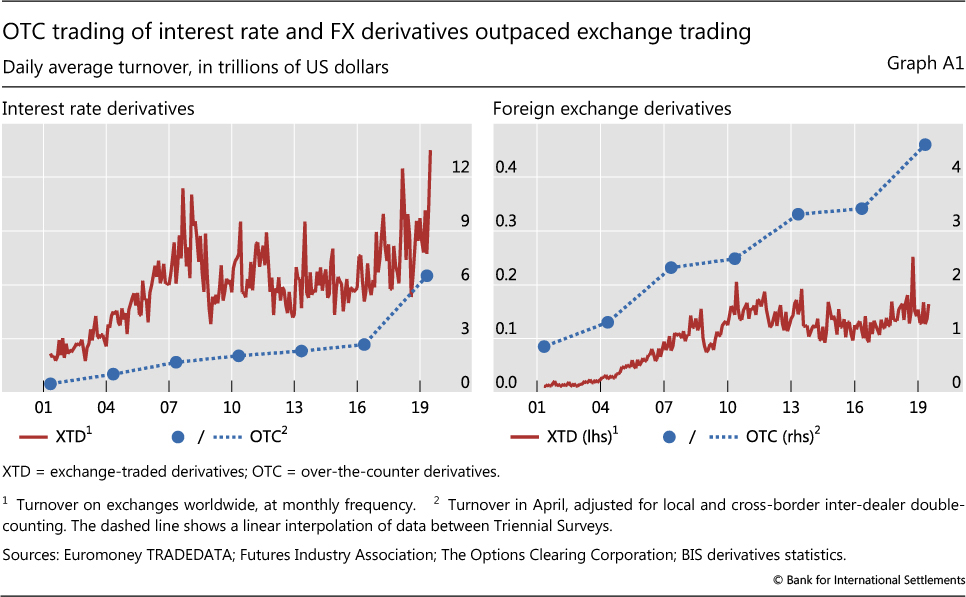

Derivatives trading in over-the-counter (OTC) markets rose even more rapidly than that on exchanges, according to the latest BIS Central Bank Triennial Survey of Foreign Exchange and Over-the-counter Derivatives Markets. The daily average turnover of interest rate and FX derivatives on markets worldwide - on exchanges and OTC - rose from $11.3 trillion in April 2016 to $18.9 trillion in April 2019. OTC trading outpaced exchange trading, continuing the trend that started around 2010 and resulting in exchanges' share falling to a historical low of 41%.

The Triennial Survey is the most comprehensive source of information on the size and structure of OTC markets. Close to 1,300 financial institutions located in 53 countries participated in the latest Survey, which was conducted in April 2019. When the results are combined with the BIS statistics on exchange-traded derivatives, they provide a global (albeit infrequent) snapshot of activity in interest rate and FX derivatives markets.

Close to 1,300 financial institutions located in 53 countries participated in the latest Survey, which was conducted in April 2019. When the results are combined with the BIS statistics on exchange-traded derivatives, they provide a global (albeit infrequent) snapshot of activity in interest rate and FX derivatives markets.

The turnover of interest rate derivatives increased markedly between April 2016 and April 2019, especially in OTC markets, where trading more than doubled from $2.7 trillion per day to $6.5 trillion (Graph A1, left-hand panel). More comprehensive reporting contributed to the increase, yet even after adjusting for this, OTC trading was still up twofold. On exchanges, trading rose by about 50% over this period from $5.1 trillion per day to $7.7 trillion. Consequently, the proportion of interest rate derivatives traded on exchanges fell from 65% in April 2016 to 54% in April 2019. As recently as 2010, this proportion had been close to 80%.

On exchanges, trading rose by about 50% over this period from $5.1 trillion per day to $7.7 trillion. Consequently, the proportion of interest rate derivatives traded on exchanges fell from 65% in April 2016 to 54% in April 2019. As recently as 2010, this proportion had been close to 80%.

A key driver of the rapid growth in interest rate derivatives trading was changing expectations about the path of monetary policy. In the mid-2010s, a sustained period of low and stable policy rates in advanced economies had reduced hedging and positioning. US dollar activity - which accounts for the majority of trading - started to pick up in late 2016, when the US Federal Reserve embarked on a series of rate hikes, and in 2019 dollar turnover surpassed its previous highs, in the context of renewed monetary stimulus. The turnover of interest rate contracts denominated in euros, yen and other major currencies also increased substantially between 2016 and 2019.

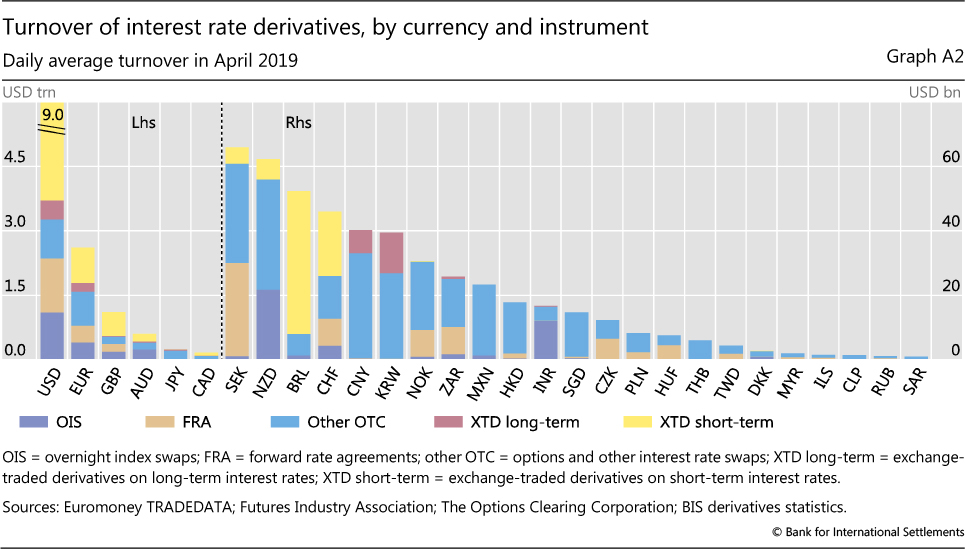

Derivatives referencing short-term interest rates are increasingly traded OTC, though the bulk of activity in such instruments is still on exchanges, in particular for US dollar-denominated contracts. A shift in OTC trading towards short-term instruments would tend to boost turnover because such contracts need to be replaced more often. A maturity breakdown of interest rate derivatives is not collected in the Triennial Survey; nevertheless, it can be approximated from the instrument breakdown because the maturity of overnight index swaps (OIS) - which were collected for the first time in the 2019 Survey - and forward rate agreements (FRAs) is typically less than one year. The instrument breakdown suggests that in April 2019 OTC trading of derivatives on short-term interest rates probably surpassed that on long-term rates. While the share of FRAs in OTC trading has shown no trend since 2010, fluctuating around 30%, the share of OIS appears to have increased, rising above 30% in April 2019 (Graph A2).

OTC trading benefited from innovations that made OTC instruments more attractive. Historically, exchanges had the advantage of centralised trading and, through their use of central counterparties, simpler counterparty risk management. The Great Financial Crisis led to initiatives to strengthen the resilience of OTC markets, such as central clearing, trade compression and swap execution facilities. In effect, these initiatives reformed OTC markets so that they more closely resembled exchanges.

In effect, these initiatives reformed OTC markets so that they more closely resembled exchanges.

In emerging market economies (EMEs) too, the turnover of interest rate derivatives increased significantly, driven by OTC trading. For all EME currencies combined, turnover rose from $182 billion in April 2016 to $280 billion in April 2019. Whereas the turnover of listed derivatives increased by around 10%, that of OTC instruments increased by almost 75%. The most actively traded contracts were denominated in the Brazilian real ($52 billion), Chinese renminbi ($40 billion) and Korean won ($40 billion) (Graph A2). Activity denominated in EME currencies is more concentrated in a few instruments than that of major currencies. Interest rate swaps (including OIS) accounted for the largest share: over 60% of trading in most EME currencies compared with 21% for the US dollar and 35% for the euro. This is partly because there are very few actively traded futures contracts denominated in EME currencies. The real, renminbi and won are the only EME currencies where a significant share of interest rate derivatives are traded on exchanges.

The OTC trading of FX derivatives also rose substantially, according to the latest Triennial Survey. In OTC markets, the daily average turnover of FX derivatives increased from $3.4 trillion to $4.6 trillion between April 2016 and April 2019. By contrast, on exchanges it remained a mere $0.1 trillion (Graph A1, right-hand panel). In only two currencies did exchanges account for a substantial share of FX derivatives activity: the Brazilian real and Indian rupee, where exchanges accounted for 36% and 13% of turnover in April 2019, respectively. OTC markets dominate owing in large part to FX swaps, which accounted for close to 70% of FX derivatives trading. FX swaps are popular as funding instruments because they are collateralised and do not change FX exposures. Furthermore, OTC deals better serve customised demands, such as trading currency pairs not involving the US dollar. Whereas the US dollar was on one side of 99% of trades on exchanges in April 2019, its share in OTC markets was much lower at 90%.

For more about the Triennial Survey, see www.bis.org/publ/rpfx19.htm. The December 2019 BIS Quarterly Review will include several articles that analyse the results of the 2019 survey. BIS, "Triennial Central Bank Survey: OTC interest rate derivatives turnover in April 2019", statistical release, September 2019. See T Ehlers and E Eren, "The changing shape of interest rate derivatives markets", BIS Quarterly Review, December 2016, pp 53-65; and L Kreicher, R McCauley and P Wooldridge, "The bond benchmark continues to tip to swaps", BIS Quarterly Review, March 2017, pp 69-79.