Non-US banks' global dollar funding grows despite US money market reform

(Extract from pages 22-23 of BIS Quarterly Review, March 2017)

Iñaki Aldasoro, Torsten Ehlers, Egemen Eren and Robert N McCauley

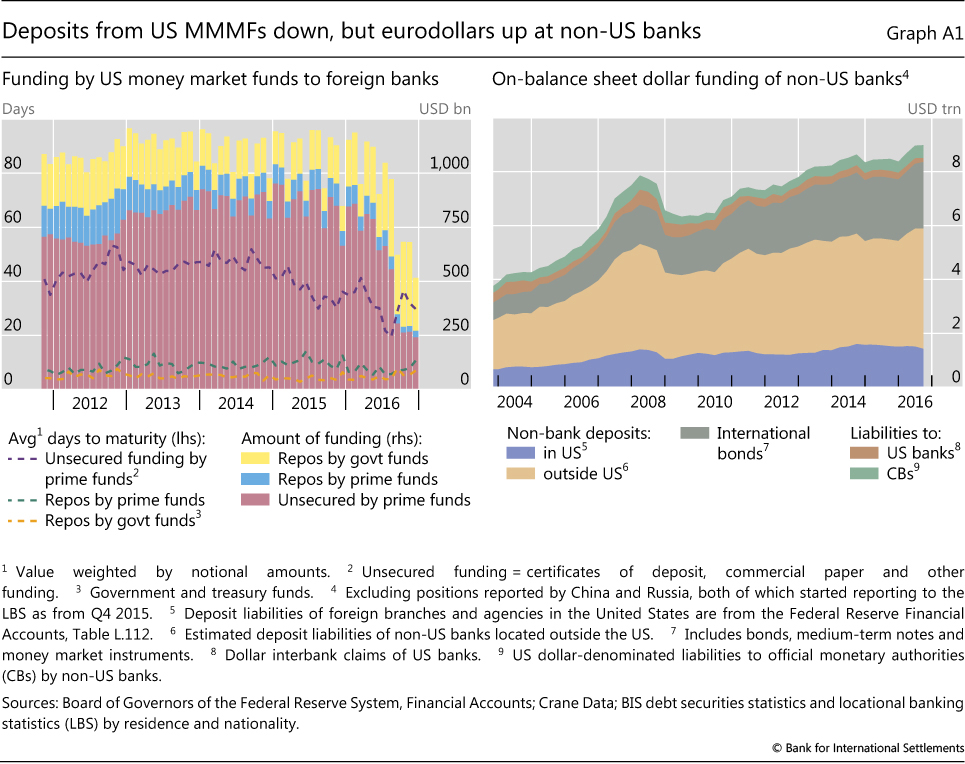

Despite the loss of dollar funding owing to money market mutual fund (MMMF) reform in the United States, non-US banks' aggregate US dollar funding rose to all-time highs in Q3 2016. In particular, deposits outside the United States have risen strongly, offsetting reduced funding from MMMFs. In aggregate at least, non-US banks are not suffering a dollar shortage as in 2008-09.

We estimate that the reform of institutional prime MMMFs, which formally took effect in October 2016, subtracted around $415 billion of dollar funding from non-US banks between September 2015 and December 2016. In some cases, including the largest institutional MMMF, fund sponsors converted such funds into "government-only" funds. In addition, fund investors switched from prime funds to existing government and Treasury-only funds. Both fund conversion and fund switching led to a shrinkage of prime funds' assets by $1.3 trillion over that period. Not all of this came at the expense of non-US banks' funding, given prime funds' investments in US-chartered banks and government paper, and government funds' investment in repos with non-US banks. In the five quarters to end-December 2016, non-US banks lost around $555 billion of US dollar funding from prime MMMFs, but gained approximately $140 billion in repo funding from government MMMFs (Graph A1, left-hand panel). This switch reduced the maturity of non-US banks' MMMF funding.

Not all of this came at the expense of non-US banks' funding, given prime funds' investments in US-chartered banks and government paper, and government funds' investment in repos with non-US banks. In the five quarters to end-December 2016, non-US banks lost around $555 billion of US dollar funding from prime MMMFs, but gained approximately $140 billion in repo funding from government MMMFs (Graph A1, left-hand panel). This switch reduced the maturity of non-US banks' MMMF funding.

Based on this evidence, many analysts have concluded that non-US banks have suffered a shortage of dollar funding. However, taking a global perspective, up until Q3 2016, non-US banks saw a rise in their on-balance sheet dollar funding to $9.0 trillion (Graph A1, right-hand panel). (In addition to on-balance sheet funding, non-US banks also raise dollars by swapping foreign currency for dollars.) Despite the run-off of eurodollar deposits held by US MMMFs, offshore deposits in non-US banks actually rose by $531 billion to $4.5 trillion in the first three quarters of 2016. This is consistent with the $67 billion increase in customer deposits in foreign currency (mostly dollars) reported by Japanese banks in the seven months to end-October 2016. The increase in bids for eurodollars widened both the Treasury-eurodollar and the Libor-OIS spread, raising the cost of floating rate US dollar debt (see Graph 9 in "A paradigm shift in markets?", BIS Quarterly Review, December 2016). In addition, some well rated banks issued more long-term bonds in dollars. No aggregate dollar shortage is evident here.

The increase in bids for eurodollars widened both the Treasury-eurodollar and the Libor-OIS spread, raising the cost of floating rate US dollar debt (see Graph 9 in "A paradigm shift in markets?", BIS Quarterly Review, December 2016). In addition, some well rated banks issued more long-term bonds in dollars. No aggregate dollar shortage is evident here.

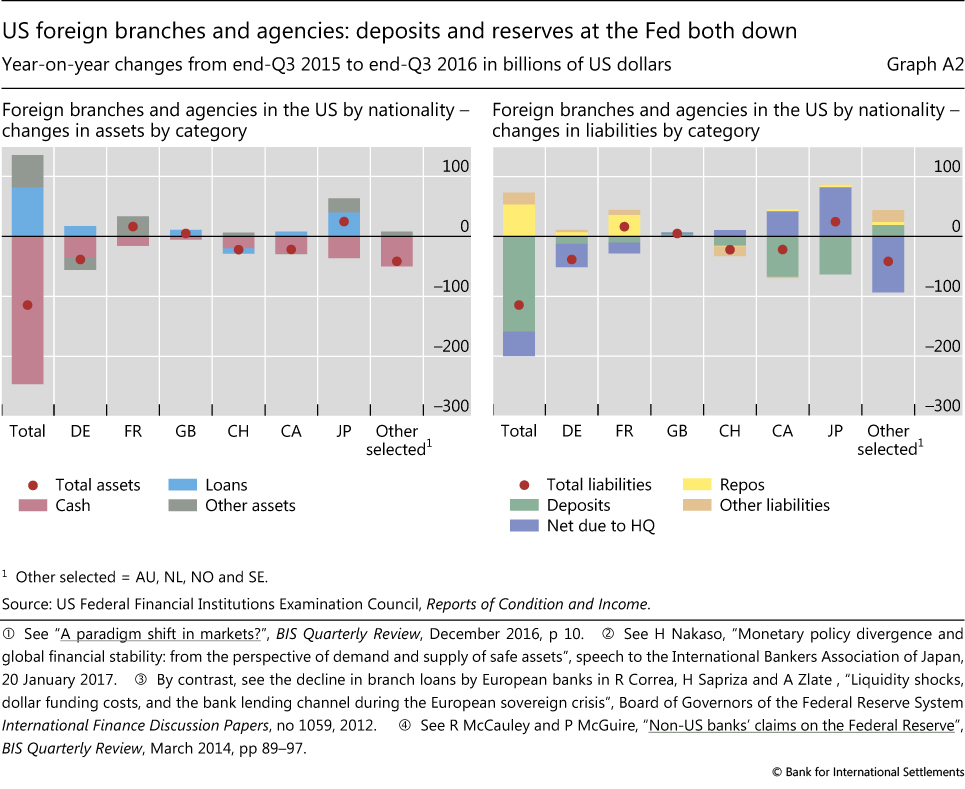

The balance sheets of foreign branches and agencies in the United States shed further light on the adjustment of non-US banks to the funding shock. The loss of funding from US MMMFs shows up in the right-hand panel of Graph A2 as a decline of deposits and the net due to headquarters, the latter reflecting reduced eurodollar deposits by MMMFs in offshore branches, such as in the Cayman Islands. Foreign branches and agencies in the United States have by and large responded by running down their holdings of excess reserves at the Federal Reserve (Graph A2, left-hand panel). While cutting these low-yielding assets, foreign banks increased their more remunerative loans.

As background, recall that non-US banks had built up disproportionately large holdings at the Fed after 2011, when the widening of the FDIC assessment base under the Dodd-Frank legislation imposed a balance sheet charge on US-chartered banks. Consequently, US-chartered banks left it largely to foreign branches to "arbitrage" by taking funds from those unable to earn interest on their Fed balances, such as Fannie Mae and Freddie Mac, and holding these funds as excess reserves at the Fed. Since the return on these transactions was modest, about 15 basis points, it was widely and correctly predicted that holdings at the Fed would feel the brunt of the lost dollar funding.

Since the return on these transactions was modest, about 15 basis points, it was widely and correctly predicted that holdings at the Fed would feel the brunt of the lost dollar funding.

By nationality of bank, the largest losers of deposits were Canadian and Japanese banks (Graph A2, right-hand panel). As "federal funds arbitrageurs", the Canadian banks repaid the money market fund placements by running down their holdings at the Fed and by drawing on funding from affiliates outside the United States. Japanese bank branches added more to their loans and other assets than Canadian banks and drew more funding from their affiliates abroad. As noted above, the consolidated foreign currency balance sheet of Japanese banks suggests that the ultimate source of this affiliate funding was customer deposits.

Overall, we find that non-US banks offset their loss of funding due to US MMMF reform by raising dollar deposits at offices outside the United States and by drawing down excess reserves at the Fed. With less cash, rising loans and the shift to short-term repo funding from MMMFs, foreign branches and agencies in the United States have extended the maturity of their portfolios and taken on more credit risk. However, they collectively still held $630 billion in reserves at the Fed at end-September 2016, a third of the total.

See "A paradigm shift in markets?", BIS Quarterly Review, December 2016, p 10. See H Nakaso, "Monetary policy divergence and global financial stability: from the perspective of demand and supply of safe assets", speech to the International Bankers Association of Japan, 20 January 2017. By contrast, see the decline in branch loans by European banks in R Correa, H Sapriza and A Zlate, "Liquidity shocks, dollar funding costs, and the bank lending channel during the European sovereign crisis", Board of Governors of the Federal Reserve System International Finance Discussion Papers, no 1059, 2012. See R McCauley and P McGuire, "Non-US banks' claims on the Federal Reserve", BIS Quarterly Review, March 2014, pp 89-97.