(Why) Is investment weak?

In spite of very easy financing conditions globally, investment has been rather weak in the aftermath of the Great Recession. What explains this apparent disconnect? The evidence suggests that, historically, uncertainty about the future state of the economy and expected profits play a key role in driving investment, and financing conditions less so. As a result, investment after the Great Recession appears to have been broadly in line with what could have been expected based on past relationships. A stronger recovery of investment would seem to depend on a reduction in economic uncertainty and expectations of stronger future growth.

JEL classification: E22, E27, C33.1

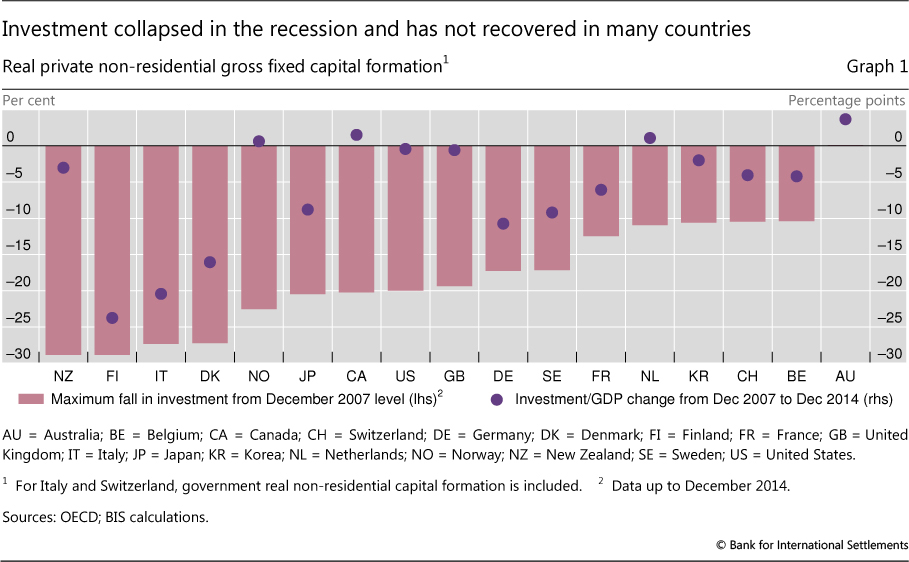

Business investment is not just a key determinant of long-term growth, but also a highly cyclical component of aggregate demand. It is therefore a major contributor to business cycle fluctuations. This has been in evidence over the past decade. The collapse in investment in 2008 accounted for a large part of the contraction in aggregate demand that led many advanced economies to experience their worst recession in decades. Across advanced economies, private non-residential investment fell by 10-25% (Graph 1).2

Since the recession, real investment has recovered in some economies. However, in others its growth has lagged that of real GDP (as shown by the dots in Graph 1).3 Indeed, in some countries - including France, Germany, Italy and Japan - real investment has not even recovered to its pre-recession level. The low level of investment has generated concerns that the average growth of advanced economies may be much weaker in the future.

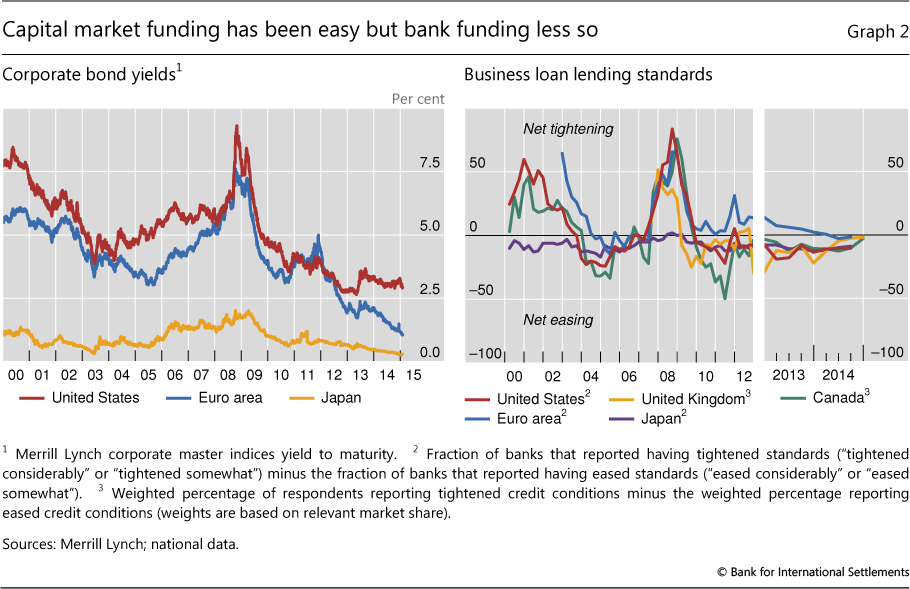

What initially seems puzzling is that business investment has remained low in spite of unusually easy financing conditions globally. Highly expansionary monetary policies have resulted in borrowers facing particularly low interest rates in capital markets, with corporate bond spreads at close to historically low levels in all major financial markets (BIS (2014)). And capital market borrowing has been not only cheap, including for riskier borrowers, but also widely accessible. Equity markets in advanced economies have also risen substantially in an environment of low interest rates and strong risk appetite.

However, as this special feature shows, cheap and readily accessible finance has only provided a small direct stimulus to investment in the recovery. In contrast, in some economies an improvement in expected future economic conditions has boosted investment. These outcomes appear to be broadly in line with the historical relationship these factors have with investment. Overall, the evidence suggests that the recovery in investment has been much as would have been expected given the state of economic and financial conditions.

The first section of this article discusses some of the explanations proposed for weak investment. The second section estimates a model of investment growth for the G7 economies over the past two and a half decades to investigate what factors have historically driven investment and what role these explanations may have had in restraining investment more recently. The last section concludes.

What could explain low business investment?

Two main explanations have been proposed for the weakness in business investment despite low interest rates and widely accessible capital market funding. The first has to do with the apparent mismatch between favourable financial conditions and investment opportunities. In particular, it could be that the firms that have the best investment opportunities do not have sufficient internal funds or easy access to external funding. As discussed below, there are some deficiencies in this explanation. A second, more plausible, explanation is that even if firms do have funds to invest, they are too uncertain about future economic conditions and so whether the possible return on investment will justify its cost. In a stronger form, this second explanation would imply that easy conditions are not the key determinant of investment. This section discusses these two hypotheses in turn.

An inability to fund investment implies that firms have insufficient internal funds and are constrained in borrowing external funds. Firms often use internal funding to finance investment because it can be cheaper than external funds. This has been demonstrated by an extensive research literature starting with Fazzari et al (1988). Aggregate profit growth, and the accumulation of cash balances, has been strong only in the United States but has not been particularly weak in other countries. An extension to this explanation conjectures that cash balances are not available for investment because they are skewed towards only some sectors, such as technology and mining, or reflect a new higher desired degree of liquidity self-insurance.

External funding is readily available and cheap for firms with direct access to capital markets, but is relatively more costly and apparently more difficult to obtain for businesses reliant on bank funding. Low interest rates and high risk appetite have reduced the cost and increased the availability of capital market funding (Graph 2, left-hand panel). However, highly accommodative monetary policy and risk-taking in capital markets have translated to a lesser extent to the cost and availability of bank credit. In most economies, while still very low, the cost of bank credit has declined by less than the cost of capital market funding.4 In addition, in some economies, most notably in the euro area, access to bank credit is more restrictive than it was before the financial crisis, as lending standards have remained tight (Graph 2, right-hand panel). As a result, smaller firms, which rely on bank funding and do not have direct capital market access, face somewhat tighter financing conditions than large firms.

A second, and seemingly more plausible, explanation for slow growth in capital formation is a lack of profitable investment opportunities. More precisely, firms may not expect the returns from expanding their capital stock to exceed their risk-adjusted cost of capital or the returns they may get from more liquid financial assets. This could be because firms are particularly uncertain about future demand, and so are not willing to commit to irreversible physical investments. Firm-level evidence has suggested that increases in uncertainty make firms less willing to undertake investment (see eg Bloom et al (2007) and Guiso and Parigi (1999)). Even if they are relatively confident about future demand conditions, firms may be reluctant to invest if they believe that the returns on additional capital will be low.

Given the strong growth of debt and equity issuance, it is hard to see that a shortage of funding has significantly constrained aggregate investment. Indeed, as van Rixtel and Villegas (2015) note, many companies, especially in the United States, can issue debt on such favourable terms that they have used new debt to finance share buybacks. In addition, while business credit growth is low globally, it is not clear that this is because of a restricted supply of credit rather than weak demand. A lack of demand for credit is surely a large part of weak credit growth, so this is probably a consequence rather than a driver of weak investment.

Other aspects of the funding shortfall explanation also have deficiencies. While small firms are typically most finance-constrained, their contribution to aggregate investment is generally relatively small. In addition, if only small firms had good investment opportunities but only large firms had access to funding, then some form of financing cascade could be expected to develop. This could occur through large firms with capital market access providing funding to smaller firms, say through trade credit, or through large firms buying small firms to access their investment opportunities. However, such a cascade of financing does not appear to be occurring on a large scale.

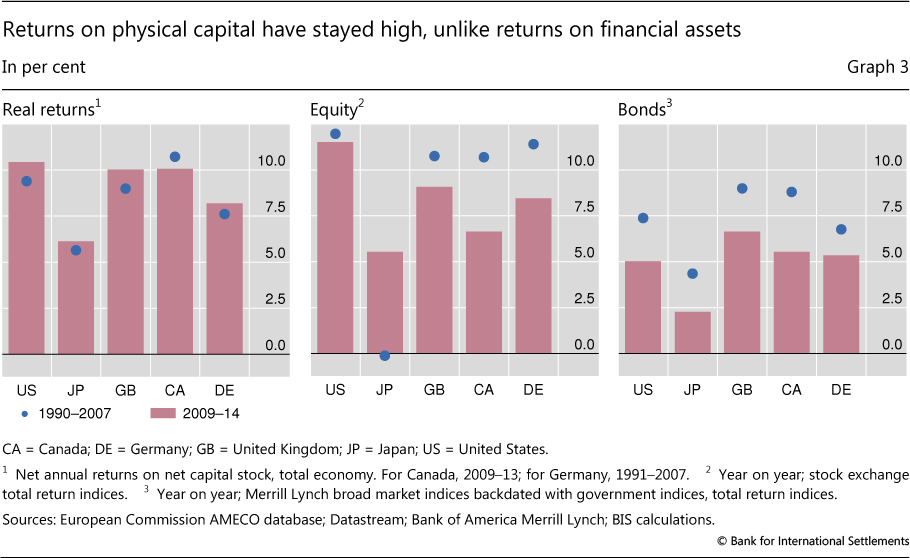

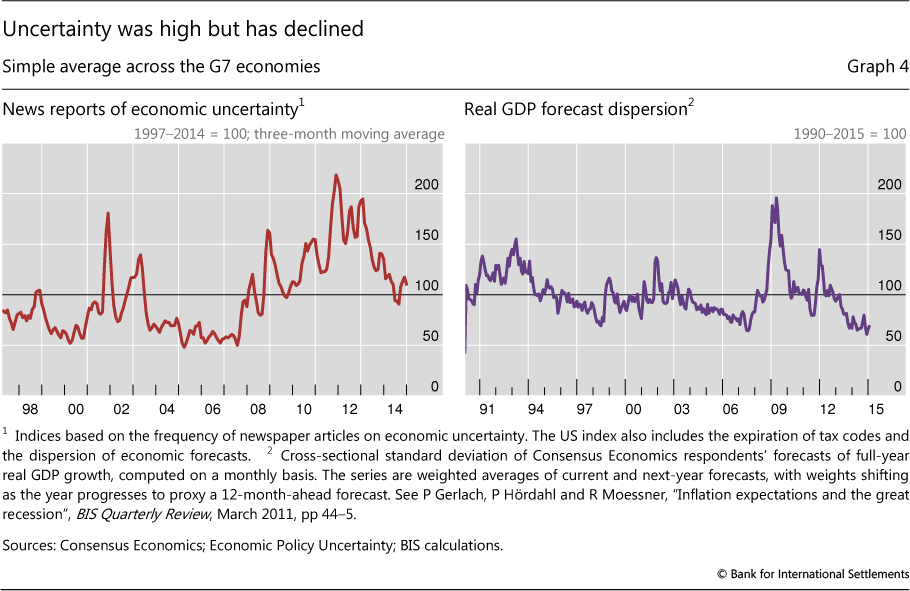

Preliminary evidence suggests that perceived uncertainty about the profitability of investment opportunities is a more plausible explanation for weak investment. There are no direct measures of expected returns on capital investment, although past returns may provide a guide. In the post-recession period, in most advanced economies estimated ex post returns on existing physical assets have actually been higher than historical averages relative to those on financial assets (Graph 3). But while economic growth has recovered in some countries, it remains anaemic in others, and growth prospects remain unclear. Indeed, it could be that firms are more uncertain than usual about the strength of demand and investment returns and so see the risks as being elevated. Again, there are no direct measures of firms' uncertainty about future economic conditions, although some proxies indicate it has been substantial. Indicators based on news reports of economic uncertainty have remained high since the onset of the financial crisis (Graph 4, left-hand panel).5 Similarly, while currently low, the dispersion of forecasts of economic activity, which Bloom (2009) uses to measure uncertainty, was higher in the period 2008-12 than pre-crisis (right-hand panel).6

Overall, the circumstantial evidence suggests that a lack of funding does not seem to have been sufficient to explain weak investment. It seems more plausible that uncertainty about returns on new capital could have played some role in depressing business investment. However, these explanations, either individually or jointly, can probably not explain the full extent of the apparent weakness in business investment. In the light of this, the next section explores these explanations further using a model of investment.

A model of investment

To provide a more rigorous assessment of the roles that funding shortfalls and high uncertainty may have had in depressing investment, this section estimates a simple model of investment for the G7 economies: Canada, France, Germany, Italy, Japan, the United Kingdom and the United States. In recent years investment in these economies has ranged from very weak to levels indicating an almost complete recovery. The estimation covers the period 1990 to 2014. The framework used is flexible, modelling changes in real business investment rather than the level of investment, in order to avoid potentially inappropriate restrictions given the very large changes in investment over the past decade and the disparity of outcomes across countries.7 In particular, the estimation takes the form:

The dependent variable is log changes in investment (which approximate percentage changes) yi,t+h - yi,t+h-1, in in country i calculated over horizons h of zero to five quarters. This variable is regressed on its own lags and a range of explanatory variables, Xi,t.

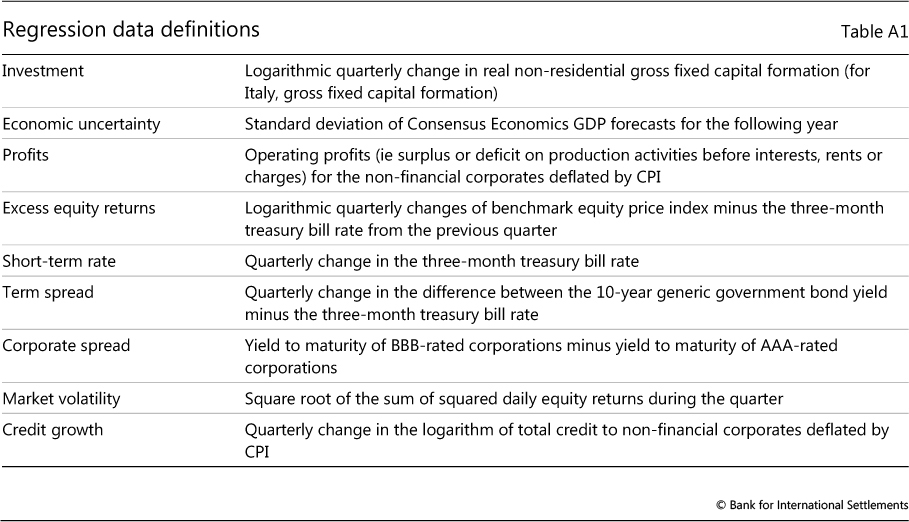

The choice of explanatory variables is motivated by series that conceptually should have a role in determining investment and that empirically have previously been found to have predictive power for investment. In particular, variables are chosen that can provide some insight into the roles of financing conditions and uncertainty in driving business investment. Some of the included variables are financial in nature: the short-term interest rate, the term spread between long-term and short-term government bond yields, the spread between the interest rate on high- and low-rated corporate bonds, the ex post real return on equity in excess of the risk-free interest rate, equity market volatility and the growth of credit from financial institutions. Unfortunately, bank lending conditions and the average interest rate on bank business lending are not available for the full sample and so cannot be included. Real profits in the non-financial corporate sector are also included, measured gross of interest expenses to better aid the identification of an interest rate effect. The final variable included is the standard deviation of GDP forecasts to capture economic uncertainty (the news measure of uncertainty is not available for the full sample of countries).

It is important to note that the individual variables included in the model can have alternative interpretations. Each variable individually may not provide evidence for or against either explanation for weak investment. Rather, they should be interpreted collectively. Indeed, the model simply captures correlations, rather than causal or structural relationships, and so the variable estimates should be interpreted in that light.

Several variables could encompass the availability and costs of funds for investment. Profits should proxy for new internal funds available for investment given that the model is estimated in difference form and profits that are not paid out as dividends add to retained earnings. Because profits are gross of interest, the cash flow effect of lower interest rates boosting cash profits would not be reflected in this variable, and so should be captured by the interest rate variables in the regression. The cost and availability of external funds are represented by the short-term interest rate, the term spread, the corporate spread, excess equity returns and credit growth. As van Rixtel and Villegas (2015) show, rising equity prices occur alongside increased equity issuance. Credit growth is an imperfect measure of the availability and cost of bank credit as it also reflects the demand for credit (which, in turn, could depend on investment intentions), but for the sample period used it is the best available proxy.

The expected profitability of investment opportunities will also be related to a range of variables. The short-term interest rate and profits are likely to co-move with the broader economic cycle. To the extent that aggregate demand is persistent, or at least perceived to be so by firms, these variables could proxy for expected future demand and so investment returns. Excess equity returns should also account for changes in expected future profitability. Finally, the dispersion of forecasts of GDP growth and equity market volatility should represent the uncertainty faced by firms about future demand conditions.

Estimation results

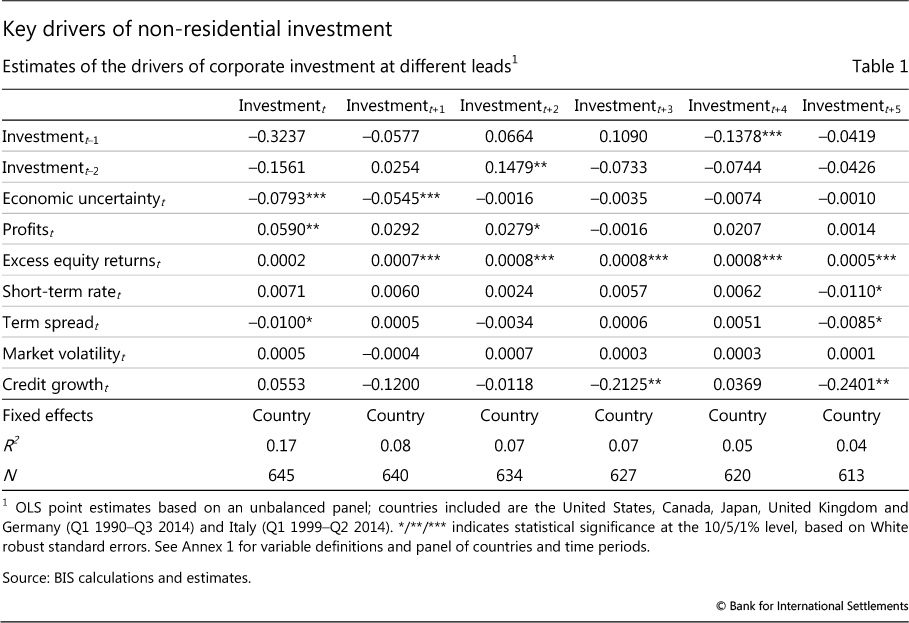

Table 1 presents the results from the estimation of the model.

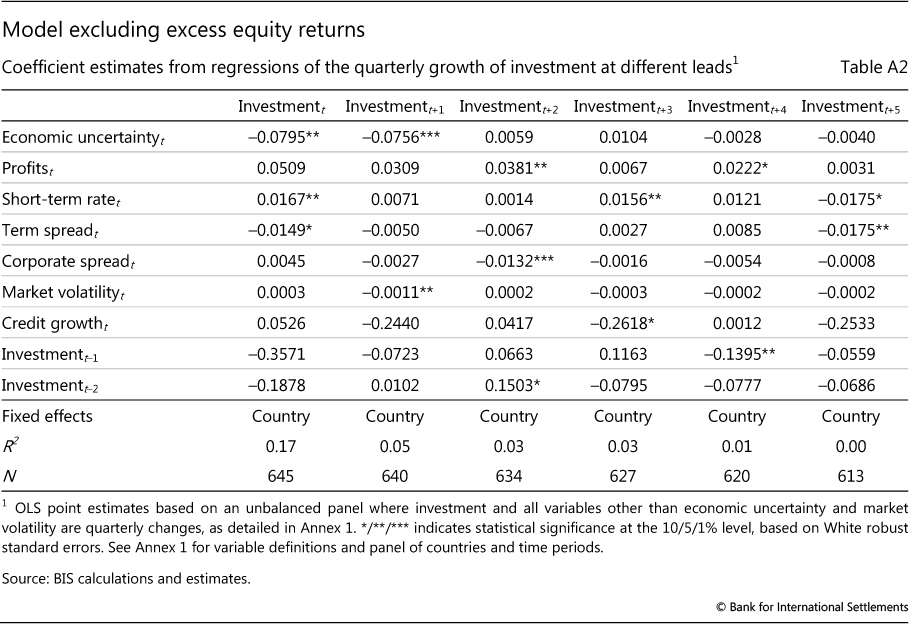

There is some weak evidence that the cost and availability of funding stimulates investment. The term spread is negative at most horizons, indicating that lower long-term interest rates relative to the short rate promote investment, and is statistically significant at two horizons. In addition, the excess equity return is positive and significant, demonstrating that strong equity returns highly correlate with greater future investment. This relationship could indicate that increased investment follows because of cheaper equity funding, a general reduction in risk premia and so availability of other types of funding, or an increase in the value of the firm which reduces financing constraints. In contrast, the coefficient signs on the short-term interest rate and credit growth are not consistent across horizons and when significant generally have the opposite sign to what would be expected. The corporate spread and market volatility are not significant at any horizon. However, when the excess equity return variable is omitted from the model, the corporate spread is generally negative but is significant at only one horizon, suggesting that the excess equity return variable may be capturing broader financing conditions to some extent (Annex Table A2).

There is generally stronger evidence that profitability is a driver of investment. The dispersion of GDP forecasts is negative and significant at the first two horizons, indicating that a reduction in economic uncertainty leads to a quick increase in investment. The profits variable is not statistically significant, but the coefficient on excess equity returns is positive and significant at five horizons. Together these results suggest that future, rather than current, profits drive investment. This interpretation of the excess equity returns variable is supported by the finding that when it is excluded from the regression (Annex Table A2) the coefficient on profits is positive at all horizons and significant at horizons of two and four quarters. A more speculative interpretation of the positive coefficient on excess equity returns could also be that a reduction in the risk premium that investors require to hold risky assets correlates with a greater appetite for firm managers to undertake risky physical investment projects.

Has business investment been weak since the financial crisis?

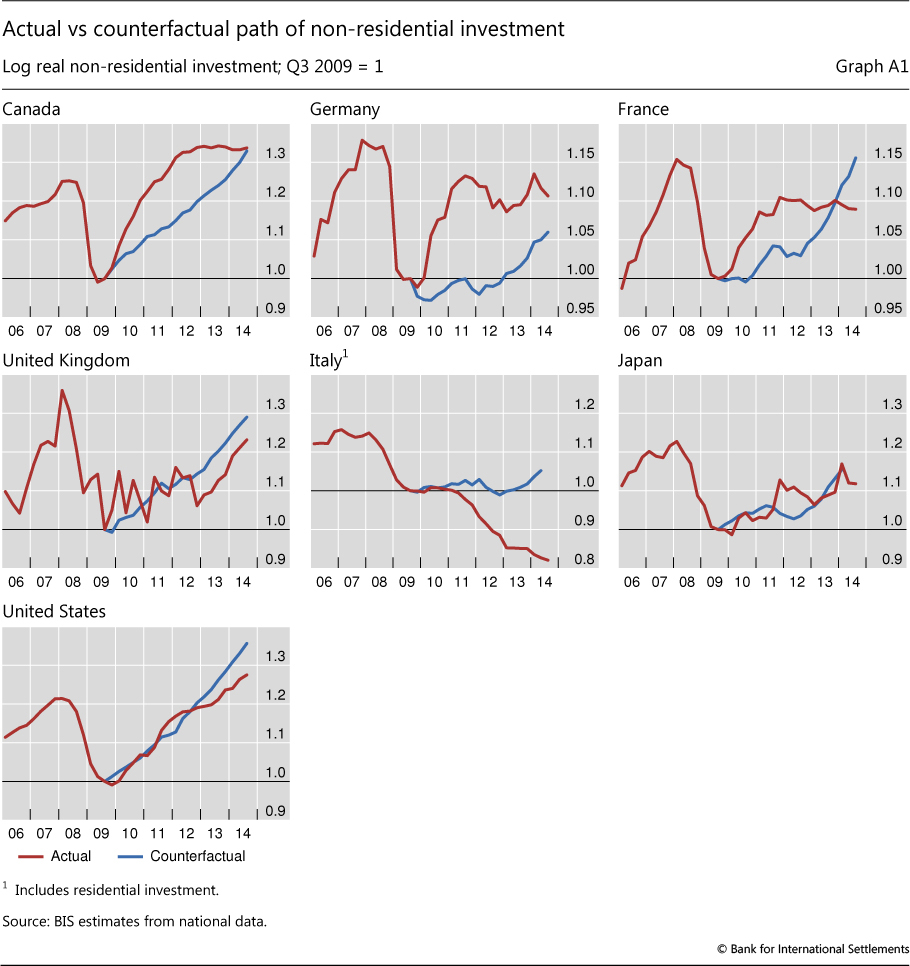

The model can be used to examine whether post-crisis investment has been weak, and, if so, why. This exercise considers whether investment growth has been in line with what would have been expected given the outcomes of the explanatory variables and their past relationship with investment. To do this, the same model specification is re-estimated up to the third quarter of 2009. These model coefficients are then used to perform an out-of-sample counterfactual exercise for investment growth using the realised values of the explanatory variables. Annex Graph A1 shows the counterfactual paths computed by cumulating, from the Q3 2009 trough, the changes in investment predicted by the regression using the realised values of the explanatory variables.8 The merit of this exercise is strengthened by tests for breaks in the coefficient estimates with the onset of the financial crisis. For every variable, except economic uncertainty, and all of them collectively, the test that the coefficients have changed is rejected. The test results imply that the economic uncertainty has had a greater effect since 2007.

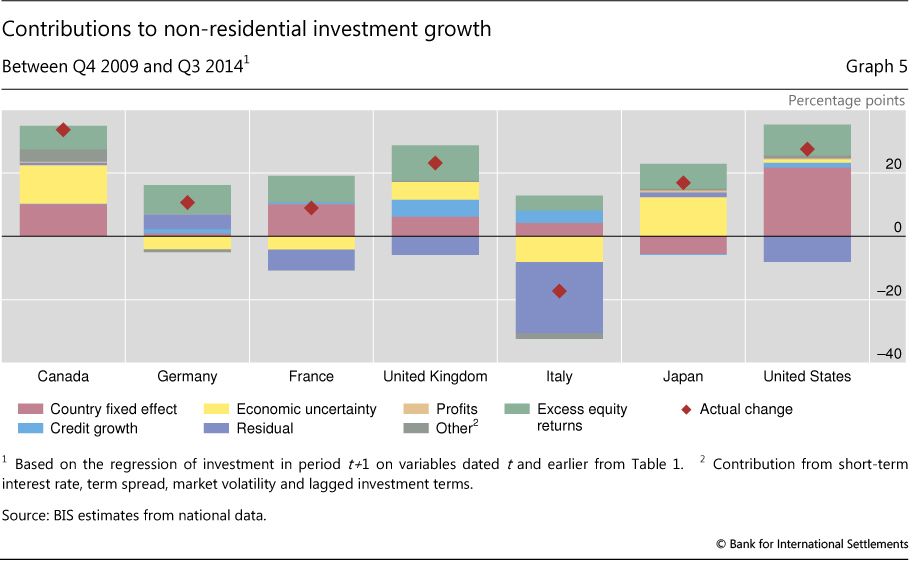

These model-implied contributions to investment growth go some way towards explaining why investment has been stronger in some countries than others. Using the counterfactual investment paths, the bars in Graph 5 show the contribution that each variable has made to investment growth when it has deviated from its historical average value.9 Across all economies, strong excess equity returns since 2009 have boosted investment, by around 8 percentage points on average. The greatest difference in investment growth across the countries that the model can explain comes from economic uncertainty. In Canada, Japan, the United Kingdom, and to a lesser extent the United States, the post-crisis reduction in economic uncertainty has increased investment by almost 8 percentage points on average. And in the euro zone economies, higher economic uncertainty has dragged down investment growth by around 5 percentage points. However, for Italy the large negative residual term shows that a significant share of investment weakness cannot be explained by the model.

Conclusions

Despite the easy financial conditions globally, business investment in recent years has been rather weak in advanced economies. Two leading hypotheses have been proposed to account for weak investment: one that the cost and availability of finance remain restrictive, and another that the expected return is not sufficient to justify the risk of irreversible physical investment.

The evidence appears to confirm that cheap and readily available finance has provided only a small direct stimulus to investment; however, this is not out of line with its historical relationships. Expectations of future economic conditions appear to be more important in driving investment decisions. In most economies, a reduction in uncertainty about future economic conditions has boosted investment, but in Europe uncertainty has seemingly intensified, restraining investment. Overall, the model-based evidence suggests that in most G7 economies, the recovery in investment has been consistent with what would be expected given the evolution of the various determinants of investment.10 Together, the results suggest that the greatest stimulus to investment would come from increased certainty of strong future economic conditions.

References

Bank for International Settlements (2014): 84th Annual Report, June.

Bloom, N (2009): "The impact of uncertainty shocks", Econometrica, vol 77, pp 623-85.

Bloom, N, S Bond and J Van Reenen (2007): "Uncertainty and investment dynamics", Review of Economic Studies, vol 74, pp 391-415.

Connolly, E, J Jääskelä and M van der Merwe (2013): "The performance of resource-exporting economies", Reserve Bank of Australia Bulletin, September.

Fazzari, S, R Hubbard and B Petersen (1988): "Financing constraints and corporate investment", Brookings Papers on Economic Activity, vol 19, pp 141-206.

Guiso, L and G Parigi (1999): "Investment and demand uncertainty", Quarterly Journal of Economics, vol 114, no 1, pp 185-227.

Illes, A and M Lombardi (2013): "Interest rate pass-through since the financial crisis", BIS Quarterly Review, September, pp 57-66.

Kothari, S, J Lewellen and J Warner (2014): "The behavior of aggregate corporate investment", MIT Sloan School of Management Research Papers, no 5112-14.

Pinto, E and S Tevlin (2014): "Perspectives on the recent weakness in investment", FEDS Notes, 21 May.

van Rixtel, A and A Villegas (2015): "Equity issuance and share buybacks", BIS Quarterly Review, March, pp 28-29.

Annex 1: Data

The data set spans Q1 1990-Q3 2014 for Canada, France, Germany, Japan, the United Kingdom and the United States. For Italy, data availability restricts the sample to Q1 1999-Q2 2014.

Annex 2: Investment model

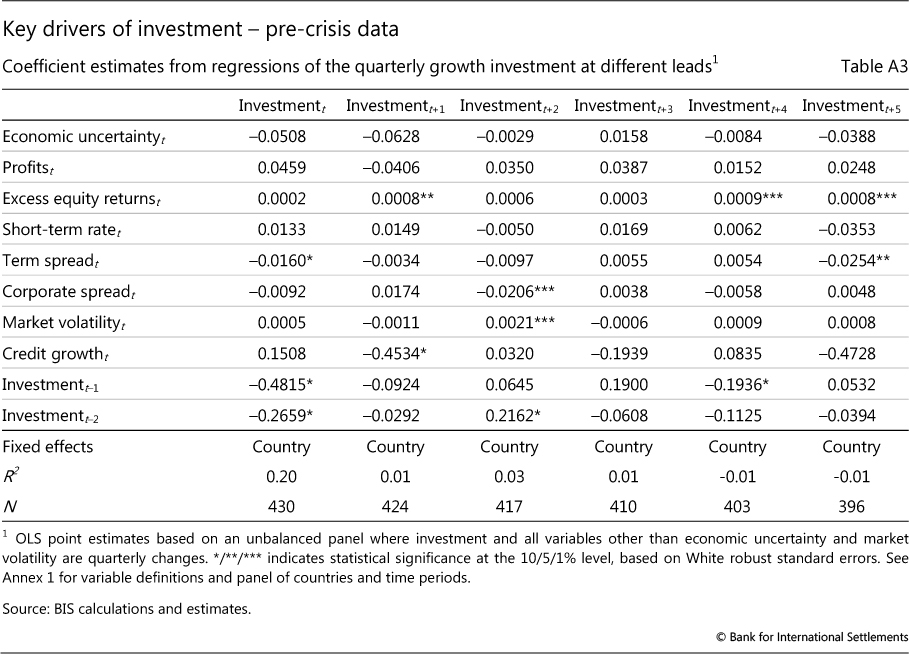

To test the robustness of the baseline results to the sample period, Table A3 reports estimates of equation (1) using pre-crisis data. The results are broadly consistent with the full sample. Real uncertainty remains negatively correlated with investment in the near term, and profits are positively related to investment, with the point estimates being consistently larger over the projection period, suggesting that the relationship between profits and future investment has weakened since the financial crisis. The strong positive relationship between excess equity returns and future investment is virtually unchanged.

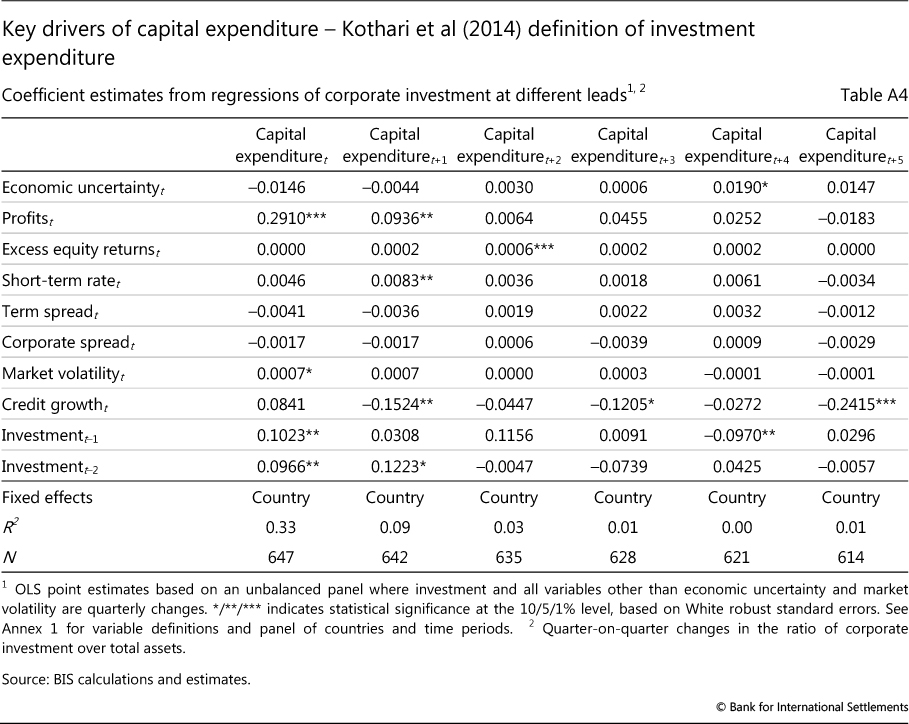

Kothari et al (2014) use an alternative measure of investment based on the change in capital expenditure scaled by lagged total assets of the corporate sectors. Table A4 shows that the results are robust to this alternative definition.

1 We are grateful to Claudio Borio, Dietrich Domanski, Hyun Song Shin and Christian Upper for useful comments and suggestions, and to Giovanni Sgro for excellent research support. The views expressed are those of the authors and do not necessarily reflect those of the BIS.

2 Australia is a notable exception where there was a resource investment boom. However, non-resource investment did fall substantially (Connolly et al (2013)). Investment also did not fall, or fell only slightly, in some emerging market economies.

3 In contrast, real investment grew faster than real GDP in many economies for some years prior to the recession, seemingly reflecting the relative decline in the price of capital goods over time.

4 See, for example, Illes and Lombardi (2013).

5 In 2014, uncertainty remained higher than its historical average in Canada, France, Germany and the United Kingdom, but was below average in Italy, Japan and the United States according to the indices published by Economic Policy Uncertainty. These indices are based on newspaper references to economic uncertainty (the US index also includes forecast dispersion and tax code expirations).

6 Moreover, it is possible that the recent compression may in part be a consequence of low GDP growth.

7 The model used is similar to that used by Kothari et al (2014) for the United States. An alternative approach involves modelling the level of investment, with it returning to some target level that depends on the level of economic activity and other variables (eg the Federal Reserve Bank's FRB/US model). Such an approach has advantages if investment does return to an equilibrium level, but the less prescriptive approach used in this article will be more appropriate if there has been structural change given the large shocks witnessed over the past decade, and so may be more appropriate for a panel of countries with different experiences. The dependent variable of changes in real business investment differs from Kothari et al, who use the ratio of capital expenditure to total assets. This choice is motivated by the availability and quality of data, and because real investment is an important component of real GDP, the main measure of economic growth. Results presented in Annex 2 show that the findings are robust to the alternative specification of investment.

8 In the United States and United Kingdom, and to a slightly lesser extent in Japan, the average growth of investment is broadly in line with the model-implied counterfactual value. In Canada, France and Germany, investment recovered faster between 2010 and 2012 than expected given the evolution of the explanatory variables, but since 2012 has been weaker than predicted. Investment in Italy has been significantly weaker than can be justified by the explanatory variables. This could be in part attributed to the stress in the banking sector and greater reliance on bank funding by Italian corporations that tend to be small, a dynamic that is not well represented in the model.

9 The country-specific growth rate of investment when the dependent variables are at their historical averages is included in the country fixed effects. The large fixed effects for the United States and Canada can be partly attributed to higher population growth rates in these countries.

10 Pinto and Tevlin (2014) also found that investment in the United States had recovered broadly, as would have been expected.