II. Monetary policy frameworks in EMEs: inflation targeting, the exchange rate and financial stability

![]() Watch the video (00:01:57)

Watch the video (00:01:57)

with Claudio Borio, Head of the Monetary and Economic Department

Listen to the podcast (00:08:39)

with Claudio Borio

Key takeaways

- Inflation targeting frameworks in emerging market economies (EMEs) have generally been successful. These frameworks have been combined with varying degrees of FX intervention, together with the active use of macroprudential tools.

- This approach reflects EMEs' response to capital flow and associated exchange rate volatility as policymakers seek to design and implement a monetary policy framework for both price and financial stability.

- In this way, practice has moved ahead of theory, much as it did when inflation targeting was adopted in the early 1990s by some advanced economies.

After high inflation and crises in the 1990s, many emerging market economies (EMEs) adopted inflation targeting as their monetary policy framework, catching up with the trend set by advanced economies. The transition has been supported by policies to strengthen economic fundamentals, notably reforms to overcome fiscal dominance, to bolster banking system soundness and to develop domestic financial markets. This regime change has coincided with a widespread reduction of inflation to lower and more stable levels, smoother growth and more stable financial systems.

These achievements have helped EMEs to better integrate themselves into the global financial system and to reap the benefits of financial globalisation. But integration has brought new challenges. EMEs have been exposed to large swings in capital flows and exchange rates, increasingly so since the Great Financial Crisis (GFC) of 2007-09. Near zero policy rates and large- scale asset purchases in the major advanced economies have gone hand in hand with strong capital inflows and exchange rate appreciation in EMEs. In the wake of steps towards monetary policy normalisation by some major advanced economy central banks, phases of significant inflows have alternated with phases of strong capital outflows, reflecting risk-on and risk-off swings in global market sentiment.

To cope with these challenges, most EME inflation targeters have pursued a controlled floating exchange rate regime, using FX intervention to deal with the challenges from excessive capital flow and associated exchange rate volatility. This contrasts with standard textbook prescriptions for inflation targeters, which advocate free floating without recourse to FX intervention. Moreover, in part due to the transmission of easy global financial conditions to domestic financial cycles, policymakers have added macroprudential and, in some cases, capital flow management measures to their monetary policy toolkit. In this light, the practices of EME inflation targeters have moved ahead of theory - as was seen in the advanced open economies when they initially adopted inflation targeting in the early 1990s.

This chapter reviews the challenges that capital flows and the associated exchange rate fluctuations have raised for EME monetary policy frameworks. The first section outlines how EME monetary policy frameworks have evolved over the past two decades. The second discusses how capital flows and exchange rates affect EMEs. The third section looks at how EME monetary policy frameworks have adjusted to cope with these challenges, especially through FX intervention, and at the role of complementary tools, notably macroprudential measures. The chapter concludes by exploring some implications for the design of EMEs' monetary policy frameworks and of their wider macro-financial stability frameworks.

EME monetary policy frameworks: state of play

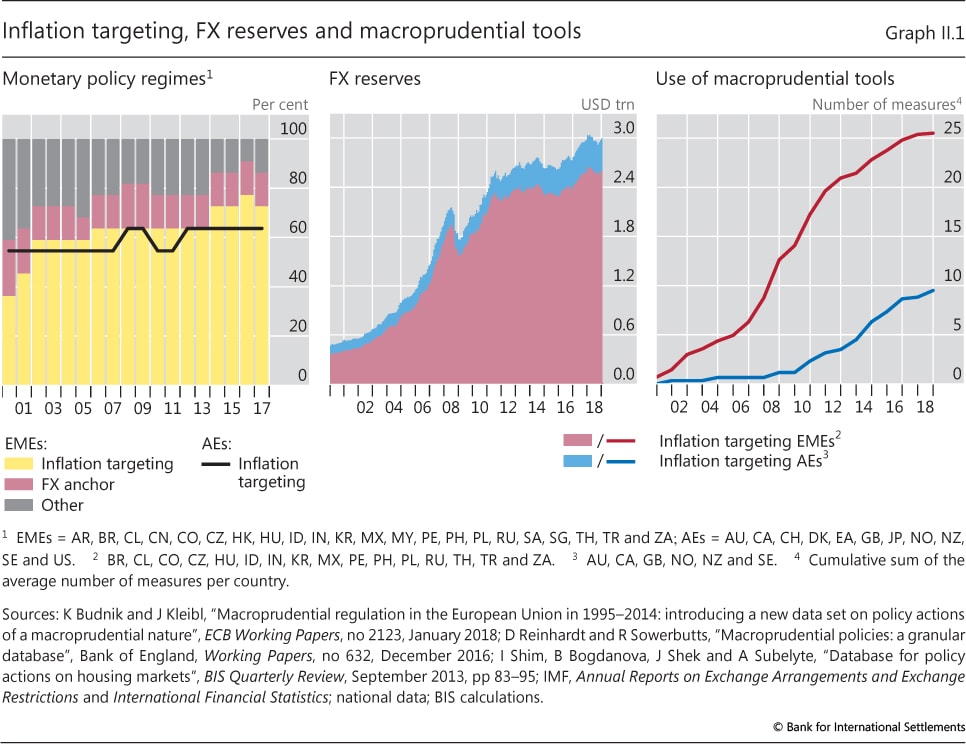

Over the past two decades, EME monetary policy frameworks have increasingly focused on maintaining domestic price stability (Graph II.1, left-hand panel). The number of major EME central banks operating an explicit inflation targeting regime has increased considerably, while the number using an explicit exchange rate anchor has declined.1 Inflation targeting is now the most common framework in major EMEs, catching up with the prevailing practice in advanced economies (black line). This evolution accords with the consensus in the mainstream open economy literature, which has coalesced around the superiority of a monetary policy framework that focuses on domestic inflation while keeping the exchange rate flexible.2

That said, EME inflation targeters have put significant weight on exchange rate considerations, as reflected in the more than sevenfold increase in their foreign exchange reserves over the past two decades, to about $2.6 trillion (Graph II.1, centre panel).3 In relation to GDP, the reserves of inflation targeting EMEs are more than three times larger than those of their advanced economy peers.4 In building up these buffers, mainly after the currency crises of the 1990s, EMEs have sought to self-insure against the risk of sudden outflows and large devaluations. At the same time, changes in FX reserves have often tended to correlate positively with the value of the countries' currencies, suggesting that they have been absorbing exchange rate pressures.5

In addition, EME inflation targeters have resorted to macroprudential measures in order to address financial stability objectives (Graph II.1, right-hand panel). In using such tools, which include reserve requirements, loan-to-value caps and countercyclical capital buffers, they have been considerably more assiduous over the past two decades than inflation targeting advanced economies. While the design and governance structure of macroprudential frameworks varies considerably between countries, many of these tools are at the disposal of the central bank, or the central bank is part of the decision-making process, eg as a member of a financial stability council or committee. Macroprudential tools can thus be considered as part of the wider macro-financial stability framework in which the central bank plays a key role.

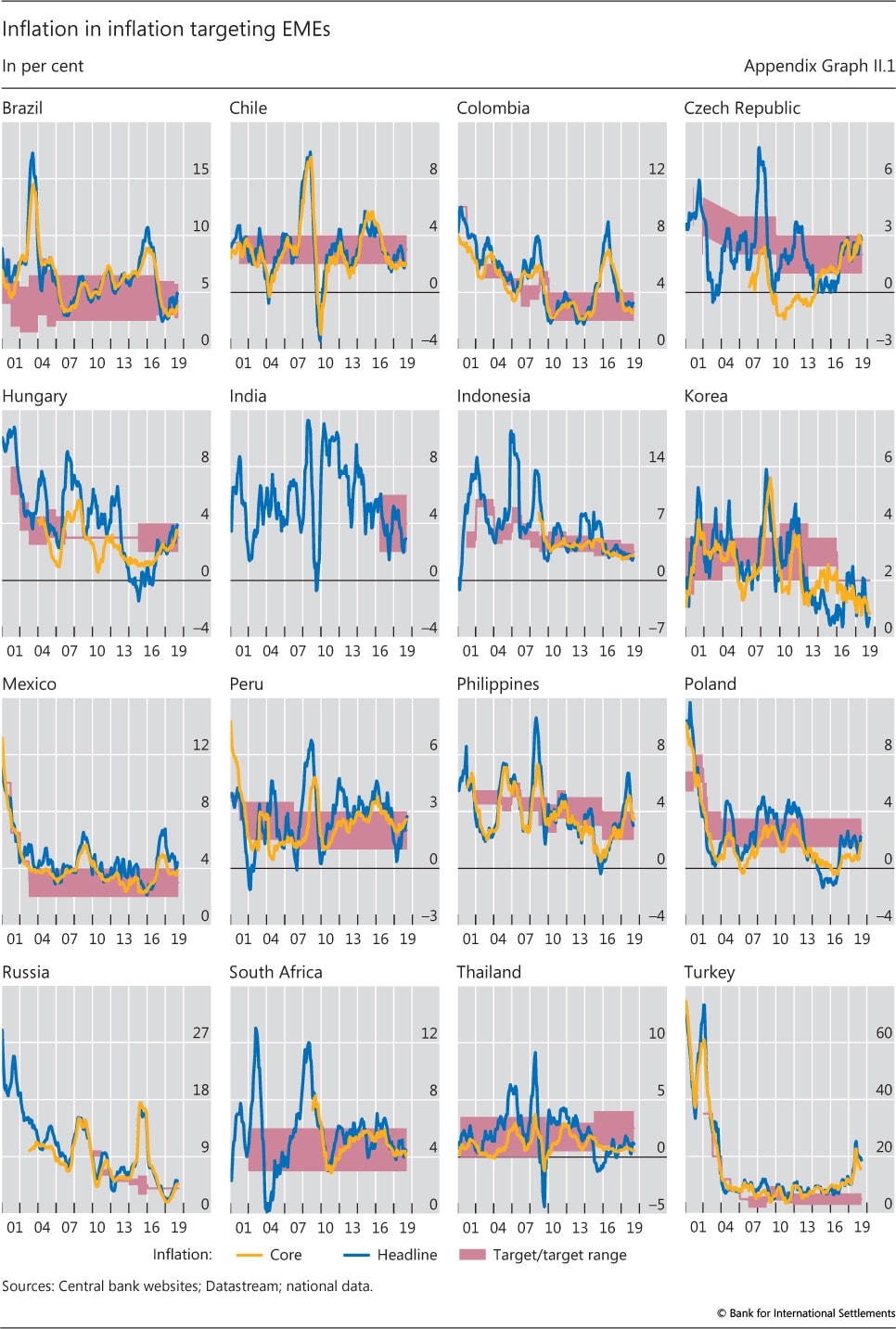

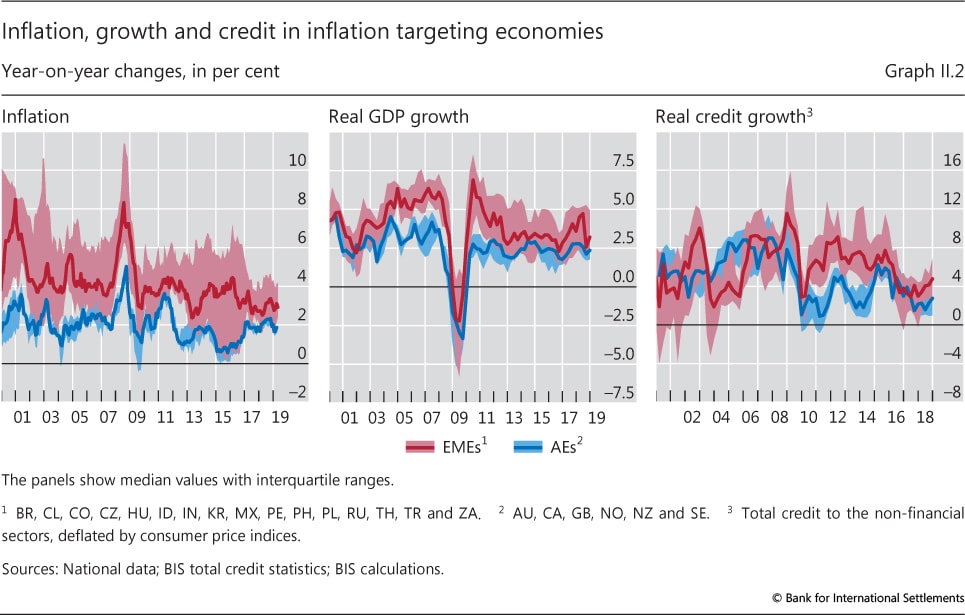

So far, the combination of inflation targeting with FX intervention, complemented by macroprudential policies, has produced favourable macroeconomic outcomes. Inflation rates have fallen (Graph II.2, left-hand panel), notwithstanding some significant differences across countries (Appendix Graph II.1). At the same time, output growth has been relatively solid and stable (centre panel). Specifically, the growth rebound after the GFC was stronger than in advanced economies, not least as EMEs did not experience a financial crisis. However, many EMEs have seen rapid credit growth (right-hand panel), reflecting at least in part the very accommodative financial conditions prevailing globally, and potentially raising risks for financial stability.

Challenges from capital flow and exchange rate swings

The nature of EME inflation targeting frameworks reflects to a significant extent the challenges posed by large swings in capital flows and exchange rates. Over the past two decades, EMEs have integrated themselves more closely into the global financial system, dismantling barriers to free movements of capital.6 As a result, capital inflows increased significantly after the mid-2000s, particularly in the wake of the GFC, although they have slowed markedly since 2013. These fluctuations were driven largely by cross-border credit flows, primarily bank loans before the GFC and increasingly securities thereafter.7 The flows, in turn, reflected global financial conditions. For instance, they first surged after the GFC when short- and long-term interest rates in major advanced economies fell to unprecedentedly low levels and then slowed in the wake of the gradual withdrawal of US monetary accommodation.8

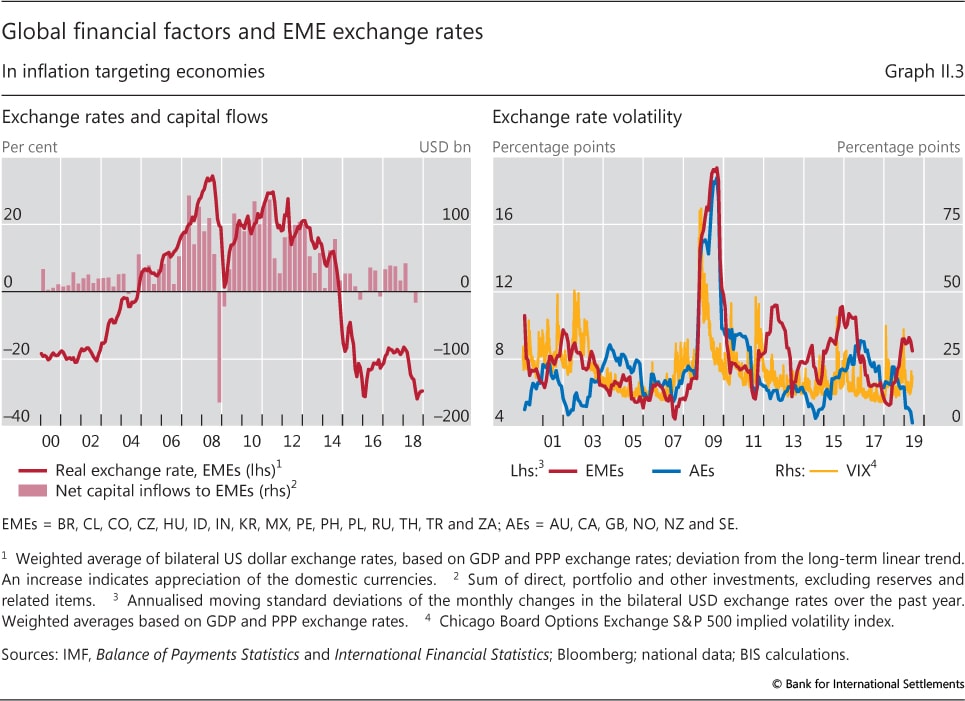

The evolution of capital flows over the past two decades has gone hand in hand with major swings in EME exchange rates, visible in large and persistent movements around their long-run trends (Graph II.3, left-hand panel). Sizeable inflows during the second half of the first decade of the 2000s and in the wake of the GFC coincided with persistent appreciations relative to trend, while the slowdown in inflows since 2013 has proceeded alongside persistent depreciations. At the same time, EME currencies have experienced larger spikes in exchange rate volatility around periods of financial stress that emanated from the advanced economies (Graph II.3, right-hand panel). This has occurred on several occasions over the past two decades, especially since the GFC, reflecting the vulnerability of EMEs to alternating risk-on/risk-off sentiment in global financial markets.

Capital flows and associated exchange rate fluctuations affect macroeconomic and financial stability in EMEs through three main channels: (i) exchange rate pass-through to inflation; (ii) export competitiveness; and (iii) domestic financial conditions. The impact is more significant in EMEs than in advanced economies owing to their economic and financial structures.

Exchange rate pass-through to inflation

Exchange rate swings directly impact domestic inflation through their effect on import prices. This effect is generally larger in EMEs than in advanced economies due to the larger share of tradable goods, in particular food, in the consumption baskets, owing to lower income levels.9

The propagation of exchange rate changes to non-tradable prices and inflation more generally depends on the characteristics of the domestic inflation process. Here the strength of second-round effects through wages is key. The extent of such second-round effects depends in particular on how well inflation expectations are anchored. The anchoring of inflation expectations is, in turn, influenced by the credibility of the monetary policy framework, which also hinges on its ability to mitigate destabilising exchange rate swings.10

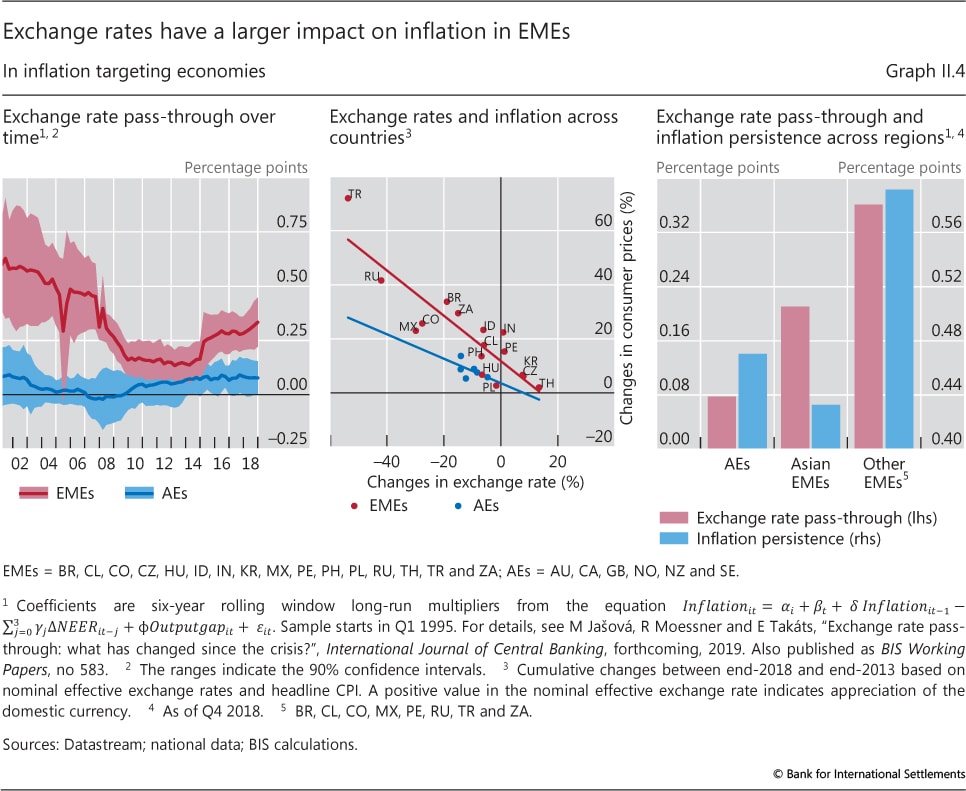

Exchange rate pass-through to inflation in inflation targeting EMEs has on average come down over the past two decades (Graph II.4, left-hand panel). While a sustained 1% depreciation pushed up inflation by 0.6 percentage points in the early 2000s, the long-run effect was just 0.3 percentage points more recently. Yet the effect remains, on average, larger than in inflation targeting advanced economies. The uptick in pass-through over the past few years reflects the impact of large depreciations in a few countries, notably Russia and Turkey (centre panel).

The aggregate evolution of the pass-through conceals important regional differences. In particular, it is lower in Asia than elsewhere (Graph II.4, right-hand panel). Estimates using data over the last six years reveal that a sustained 1% currency depreciation leads to a long-run increase in the inflation rate by 0.2 percentage points in Asian inflation targeting EMEs, still more than double the pass-through estimates for their advanced economy peers. In other inflation targeting EMEs, the same depreciation raises inflation by 0.35 percentage points.

These differences are in part linked to the strength of second-round effects (Graph II.4, right-hand panel). Specifically, inflation persistence, ie the influence of past inflation on current inflation - a rough indicator of the intensity of second-round effects - is relatively low in inflation targeting emerging Asia, even lower than in advanced economies. By contrast, it is considerably higher in other inflation targeting EMEs.

To sum up, exchange rate pass-through in inflation targeting EMEs is lower today than in the past, no doubt in part reflecting better anchored inflation expectations and the more credible anti-inflation credentials of their frameworks. Yet, in many EMEs, inflation dynamics are still less well anchored than in advanced economies.11 In those cases, price stability remains more vulnerable to large currency depreciations.

Exchange rates and export volumes

Exchange rate swings also affect trade and aggregate demand. Many EMEs are highly export-dependent, which amplifies the potential relevance of this channel. From the perspective of the conventional trade channel, a depreciation of the currency improves the exporters' international competitiveness. As a result, exports rise, boosting output, possibly above potential, a level that would create inflationary pressures on top of those from exchange rate pass-through.

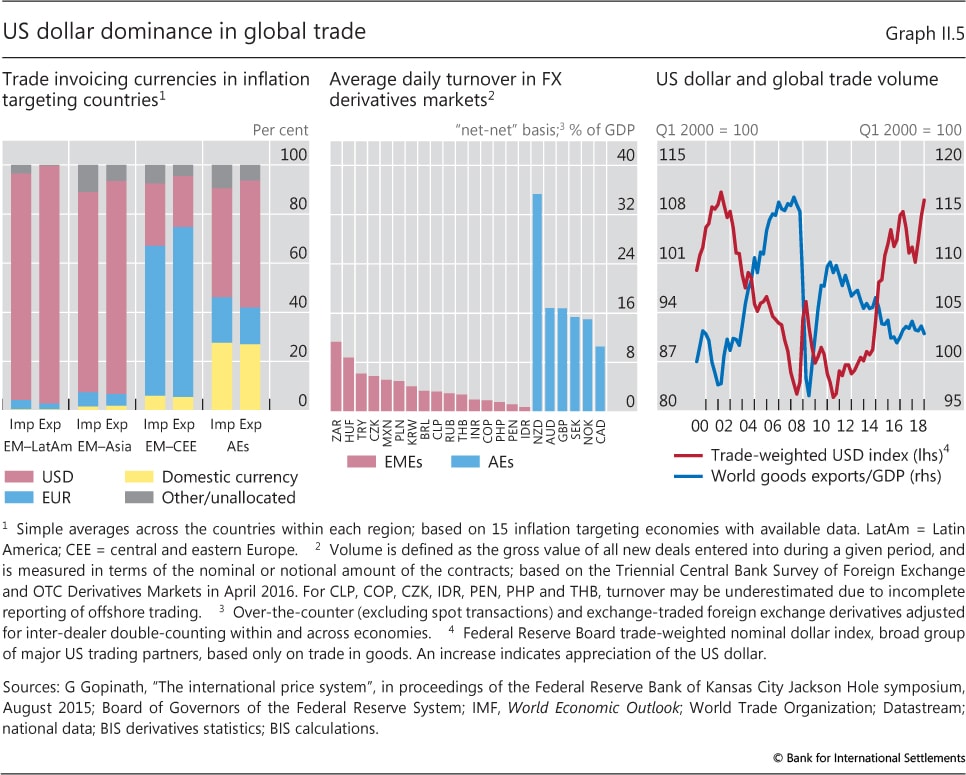

The conventional trade channel rests on the assumption that export prices adjust in response to a change in the country's exchange rate. Over short horizons, however, this may not be the case. This is particularly so in EMEs because their trade is almost entirely invoiced in foreign currency, primarily in US dollars (Graph II.5, left-hand panel). If the invoice price is sticky in US dollar terms, swings in a country's exchange rate against the US dollar would impact imports, but would in the short term have little effect on export competitiveness.12 Instead, export volumes would be affected by changes in import demand from other countries. Thus, a broad-based depreciation of currencies against the US dollar could even reduce EME export volumes, as demand would contract.

That said, exchange rate swings would still have macroeconomic effects by influencing export firms' profits and, through this channel, employment and investment. If export prices are fixed in US dollar terms, a depreciation of the currency would increase the value of exports in domestic currency, boosting firms' profits. This channel is likely to be more pronounced in EMEs, as scope for hedging exchange rate risk through financial derivatives is much more limited. This is illustrated by the much smaller FX derivatives markets in EME currencies, as compared with those of inflation targeting advanced economies (Graph II.5, centre panel).13 As a consequence, EME exporters tend to be largely unhedged against currency fluctuations.14

Widespread US dollar trade invoicing underpins the dominance of the US dollar in global trade financing.15 This, in turn, may influence the effect of exchange rate swings on EME exports in the same direction as that of sticky prices in dollar terms. The role of trade finance has increased as global value chains (GVCs) have lengthened, requiring greater resources to finance them. A stronger US dollar pushes up the value of trade credit in local currency terms, often in parallel with a general tightening of financial conditions in EMEs. This financial dimension weakens the expansionary effect of a currency depreciation on a country's export volumes. In the extreme, currency depreciation could even have a contractionary effect on exports in the short run if GVCs are curtailed due to tighter credit conditions.16

To summarise, the US dollar's dominance in trade invoicing and trade financing weakens the impact of exchange rate changes on export volumes, at least in the short term. Instead, phases of broad US dollar strength would coincide with a broad-based weakness in global trade. This conclusion is consistent with the strong negative correlation between the broad US dollar exchange rate and global export volumes (Graph II.5, right-hand panel).

Capital flows and domestic financial conditions

Capital flows and associated exchange rate fluctuations influence macroeconomic and financial stability in EMEs through domestic financial conditions. Capital flows exert a direct quantity effect on credit and asset markets. In addition, asset prices can move substantially even without significant transactions and, conversely, quantities may change and affect asset prices and the exchange rate without involving capital flows.17 Reflecting such tight links and the associated global arbitrage, asset returns and the yields of bonds denominated in the respective EME currencies have moved closely together with those in advanced economies, despite at times divergent macroeconomic conditions.18

Two structural features make EMEs especially vulnerable. First, EME borrowers rely heavily on foreign currency borrowing, often unhedged. Second, foreign investors have large holdings of EME assets, particularly bonds, on a similar basis. This means that the exchange rate can amplify the impact of capital flows via the so-called financial channel of the exchange rate.

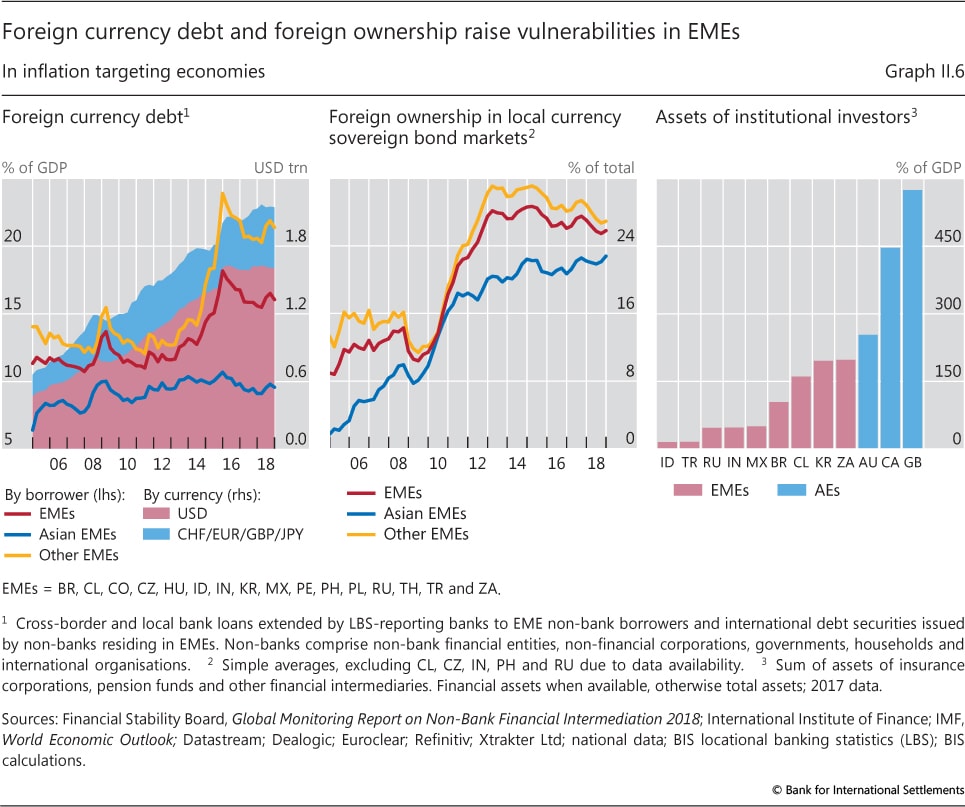

The strong expansion of EMEs' foreign currency debt over the past decade or so makes the financial channel of the exchange rate especially relevant (Graph II.6, left-hand panel). Since 2005, the FX debt of major inflation targeting EMEs has almost tripled, to more than $2 trillion or more than 16% of GDP (up from less than 12% in 2005), mainly driven by corporate sector borrowing in US dollars.19 The incidence of foreign currency borrowing is smaller in Asian EMEs, where it stood at around 10% of GDP in 2018, compared with more than 20% in other EMEs.

Borrowers incur currency mismatches whenever the foreign currency debt is left unhedged by means of FX revenues and assets or derivatives. While widespread US dollar invoicing in trade means that foreign currency debt servicing costs are often matched by export revenues, the private sector's stock of foreign currency debt is, in many EMEs, much larger than that of foreign assets.20 In addition, and as mentioned above, scope for hedging often remains limited. This suggests that currency mismatches are widespread, more so than in advanced economies. As a result, an appreciation, say, of the domestic currency against the funding currency would reduce debt servicing costs and debt burdens, lowering EME borrowers' credit risk, attracting more capital inflows and loosening financial conditions. These mechanisms work in reverse when the currency depreciates, and are then potentially amplified through the higher foreign currency debt burdens accumulated in the appreciation phase.

Just as for borrowers, the strong expansion of foreign investment in local currency securities heightens the relevance of the financial channel of the exchange rate. Foreign investors often hold a large share of EME local currency debt securities. Specifically, in the group of EME inflation targeters, non-residents held, on average, an estimated 26% of local currency sovereign bonds in 2018, up from 11% in 2005 (Graph II.6, centre panel). Here too, emerging Asian inflation targeters are somewhat less exposed. To be sure, local currency securities markets are more developed in EMEs compared with the times when they could only borrow in foreign currency ("original sin"). Even so, the development has not eliminated the vulnerability entirely, not least as EME bond markets have a less developed base of domestic institutional investors (Graph II.6, right-hand panel).21

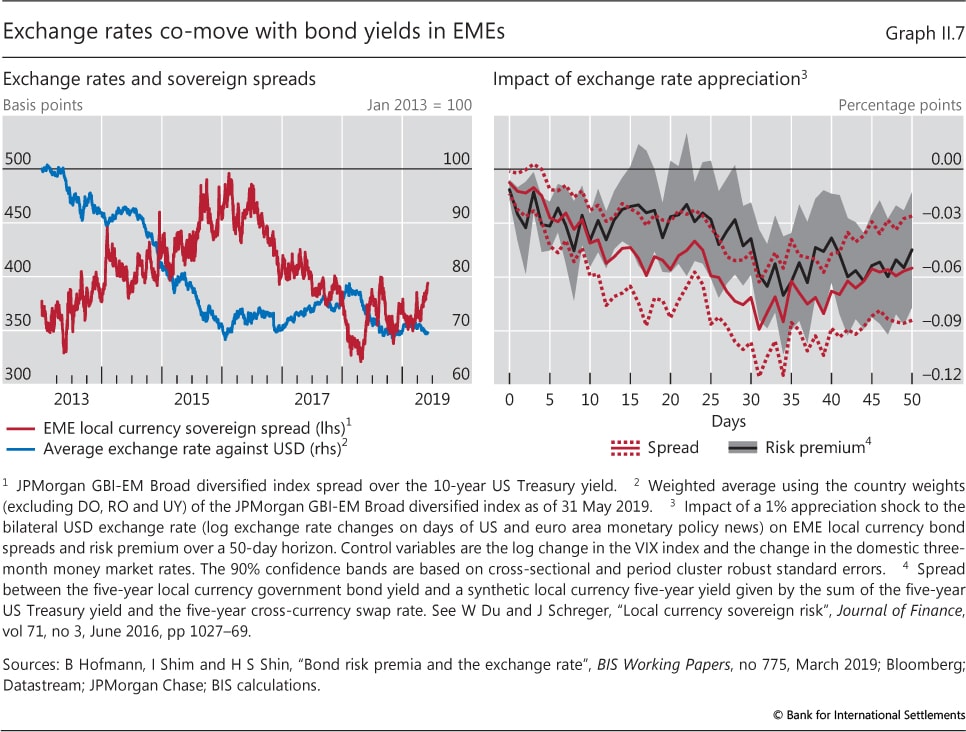

Investors incur currency mismatches whenever they do not hedge the corresponding local currency exposures. In this case, a currency appreciation, say, increases the value of local currency assets in foreign investors' home currency terms, relaxing their value-at-risk constraints. This encourages further investment, pushing down bond yields by compressing the credit risk premium. The same mechanism plays out in reverse when the exchange rate depreciates.22 This mechanism is one reason why EME sovereign spreads move inversely with the exchange rate (Graph II.7, left-hand panel). Indeed, formal empirical analysis for a group of major EMEs finds that exchange rate appreciation leads to lower local currency bond spreads in EMEs, and that this reduction turns out to be driven by lower credit risk premia. This is consistent with the financial channel at work, operating through the risk-taking of global investors (right- hand panel).

Over longer horizons, the impact of capital flow and associated exchange rate swings is greater still. This is because external borrowing, be it through banks or capital markets, interacts with domestic borrowing. There is ample evidence that external borrowing increases relative to domestic borrowing during credit booms,23 and that strong credit expansion coupled with strong exchange rate appreciation has preceded financial crises.24 This way, capital flows, exchange rate swings and domestic financial cycles reinforce each other.

Capital flows, exchange rates and monetary policy in EMEs

The specific ways in which capital flows and associated exchange rate swings affect EMEs give rise to a number of important challenges and trade-offs for monetary policy.

First, while exchange rate pass-through has declined, the inflationary consequences of exchange rate swings have not been vanquished. In many EMEs, exchange rate pass-through to inflation remains significant, although its decline over time is no doubt in part a consequence of central banks' success in containing inflation in the first place. Large swings in the exchange rate, and especially large depreciations, still have the potential to de-anchor inflation.

Second, the effects of global financial conditions transmitted through capital flows tend to weaken the transmission of monetary policy, reducing the central bank's ability to steer the economy through adjustments of its policy rate. If domestic capital market rates and asset prices are tied to swings in global markets, this weakens the effect of changes in domestic monetary policy.25 The strength of these effects depends in part on the economy's financial structure, such as the relevance of long-term rates relative to short-term rates in credit markets, as bank short-term rates tend to be more closely related to the domestic policy rate.

The financial channel of the exchange rate adds to this effect. Under the conventional trade channel, the exchange rate would reinforce monetary transmission. A monetary policy tightening would lead to exchange rate appreciation, lowering inflation through exchange rate pass-through and dampening output through its effect on net exports. But the output effects of the financial channel work in the opposite direction. An appreciation of the exchange rate would tend to ease domestic financial conditions, counteracting the tightening effects of higher policy rates. Thus, the stronger the financial channel is relative to the trade channel, the weaker is monetary transmission through aggregate demand.

Third, the potential weakening of the classical trade channel through US dollar trade invoicing and financing, as well as the significance of capital flows and associated exchange rate swings in shaping domestic financial conditions, may worsen the short-term trade-off between inflation and output stability. A capital outflow accompanied by a depreciation of the domestic currency would push up inflation through exchange rate pass-through, but might have little effect on domestic output through traditional trade channels, at least in the near term. At the same time, domestic financial conditions would tighten, exerting a contractionary effect on the domestic economy. As a result, the central bank may face the combination of rising inflation and a weak economy. The opposite dilemma would emerge when capital flows in and the exchange rate appreciates.

Fourth, the effects of capital flows and concomitant exchange rate fluctuations may give rise to an intertemporal trade-off between stabilising inflation today and the risk of instability tomorrow. This trade-off is best described in the context of persistent capital inflows coupled with an appreciating currency. The appreciation would dampen inflation while loose financial conditions could fuel a domestic financial boom, boosting both credit expansion and increases in asset prices, not least those of real estate, and hence economic activity. However, the corresponding build-up of vulnerabilities, notably through debt accumulation, could result in future economic weakness, a currency depreciation and a probable rise in inflation once the boom turns to bust. That way, lower inflation and stronger economic activity in the short run can give way to higher inflation and depressed activity in the longer run.

Inflation targeting EMEs have met these challenges and trade-offs by augmenting interest rate policy with FX intervention and, in some cases, balance sheet policies in domestic assets. Moreover, macroprudential policies, often with the involvement or even under the lead of the central bank, have complemented monetary policy frameworks.

FX intervention

Intervention in foreign exchange markets can be used to build buffers against future sudden outflows and depreciations, as well as to lean against the domestic consequences of capital flow and exchange rate fluctuations.26 Intervention strategies, tactics and instruments have varied considerably over time and across countries (Box II.A). The most common form remains intervention in spot markets.

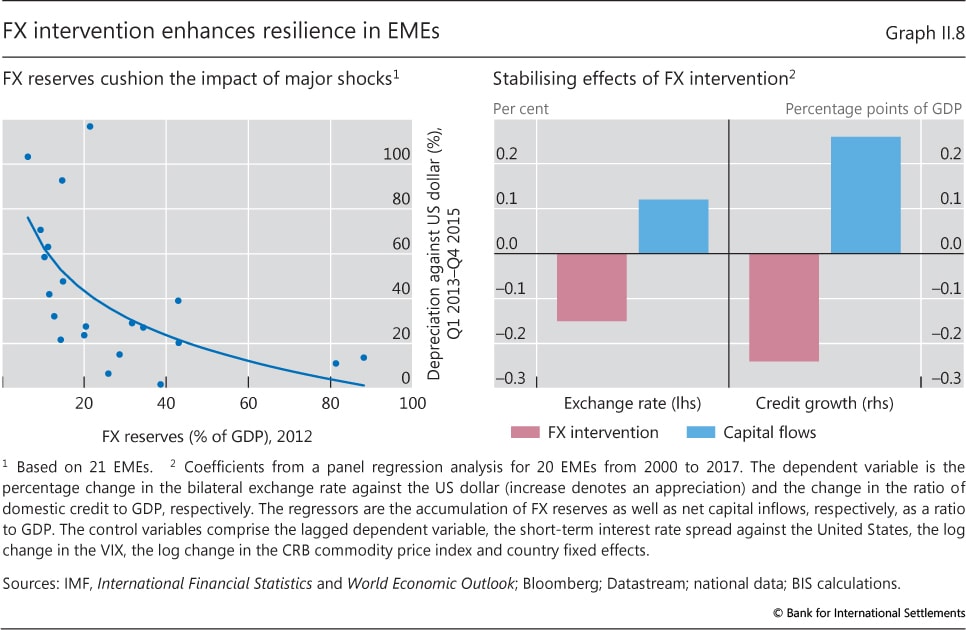

Whether such FX intervention, unaccompanied by policy rate changes, can affect exchange rates at all has long been questioned.27 But recent theoretical contributions have shown it can be effective under realistic assumptions about the functioning of financial markets.28 Empirical evidence is consistent with these results. For instance, Graph II.8 (right-hand panel) reports evidence from a quarterly panel of EMEs. FX purchases depreciate the currency in a way that is statistically and economically significant.29 Quantitatively, the effect is very similar to the appreciating effect of a capital inflow of the same size, suggesting that FX intervention can counterbalance the effects of capital flows on the exchange rate.

FX intervention helps tackle the challenges from exchange rate swings in two main ways. First, through its effect on the exchange rate, it can directly counteract exchange rate swings that would have undesired effects on the inflation rate and on the economy. In doing so, it takes some of the burden off interest rate policy, adding a degree of freedom.

Second, the accumulation of reserves has quasi-macroprudential features. For one, it provides self-insurance against potential large future devaluations, thereby serving as an integral part of a country's financial safety net. Indeed, there are indications that FX reserve buffers helped mitigate the impact of recent episodes of global financial stress on EME exchange rates. For instance, in the wake of the taper tantrum, between 2013 and 2015, EMEs with larger reserve buffers experienced smaller currency depreciations (Graph II.8, left-hand panel).30 For this purpose, the reserve accumulation itself does not even need to influence the exchange rate. In fact, when building up reserves with this objective in mind, central banks often seek to have as little impact as possible on the external value of the currency.

In addition, FX intervention can counteract the impact of exchange rate swings on domestic financial conditions. Working through the financial channel of the exchange rate, FX intervention can break the mutually reinforcing feedback loop between exchange rate appreciation and capital inflows that fuels domestic credit creation. In addition, the sterilisation leg of an FX intervention may help mute domestic credit expansion, to the extent that banks cannot rebalance their asset portfolios so that the sterilisation instruments on their balance sheets "crowd out" other lending.31 In line with these notions, evidence across major EMEs suggests that FX purchases, in addition to slowing exchange rate appreciation, also dampen domestic credit expansion in a way that quantitatively matches the expansionary impact coming from capital inflows (Graph II.8, right-hand panel).32 In other words, FX reserve buffers do not just help to "clean up the mess", once capital flows reverse and stress arises, but their accumulation also "leans" against the build-up of financial imbalances in the first place, reducing the risk, or at least the amplitude, of a possible reversal.

However, central banks also face difficult trade-offs in the use of FX intervention. The fiscal cost of carrying reserves can be considerable. This is especially true when interest rates are very low in reserve currencies, and for countries with high domestic interest rates. Moreover, to the extent that FX intervention reduces exchange rate volatility and possibly even the sense of two-way risk, it may induce further carry trades. And in the longer run, it may encourage currency mismatches, raising the relevance of the financial channel and making economies more vulnerable.33 How far precautionary reserves are accumulated and intervention is used as a stabilisation tool will depend on a cost-benefit analysis, which will vary across countries and over time.

Thus, while FX reserves are an important element of countries' financial safety net, they are quite costly and, also for that reason, will always be limited. In times of large stock adjustments by global investors, outsize capital outflows can overstretch the central bank's FX reserve buffer. In order to mitigate this risk, sound policy frameworks and FX reserve buffers need to be complemented by regional arrangements for financial assistance, such as FX swap lines, and adequate global lending facilities at the IMF.

In addition to intervening in the FX market, EME central banks may also address capital flow and associated exchange rate volatility by using their balance sheet for operations in domestic rather than foreign currency assets. One such policy, implemented by several EME central banks, is to offer foreign exchange protection to investors without affecting the level of international reserves (Box II.A). This is achieved by auctioning non-deliverable forwards (NDFs) that settle in domestic currency. The central bank has a natural hedge for this derivative exposure, ie its international reserves. Thus, offering such protection is equivalent to adjusting the currency composition of the central bank's balance sheet. As a result, such operations can be effective only when backed by a sufficiently large stock of foreign reserves.

FX intervention in EMEs: instruments and tactics

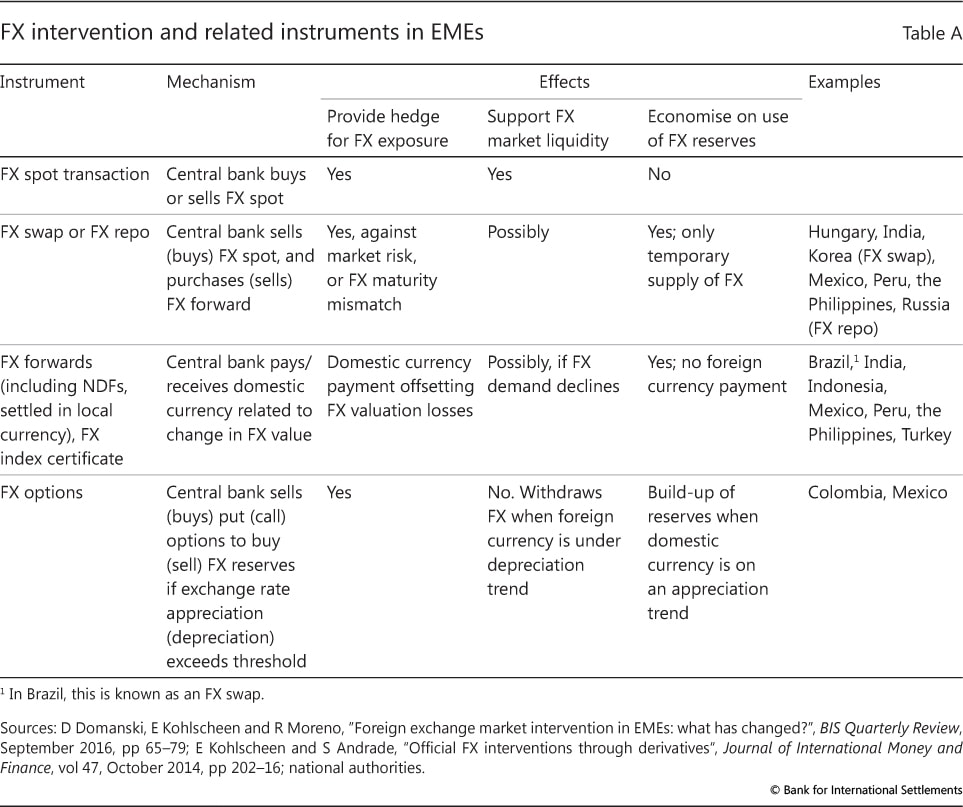

Although spot market interventions remain the most common instrument, the EME FX intervention toolkit has continued to expand. In particular, derivatives are gaining ground (Table A), as they are becoming the most liquid segment of the FX market, and play an increasingly important role in determining prices, even for the spot exchange rate. Two other reasons may be relevant. First is the growing importance of financial stability considerations. With rising FX debt levels and increased foreign asset holdings, the vulnerability to large FX moves has increased. By providing market participants with instruments to self-insure, derivatives may be better suited to mitigating these tail risks. Second, operating in derivatives settled in local currency reduces the risk of having to report unwelcome changes in FX reserves, which might trigger undesirable market dynamics.

Two other reasons may be relevant. First is the growing importance of financial stability considerations. With rising FX debt levels and increased foreign asset holdings, the vulnerability to large FX moves has increased. By providing market participants with instruments to self-insure, derivatives may be better suited to mitigating these tail risks. Second, operating in derivatives settled in local currency reduces the risk of having to report unwelcome changes in FX reserves, which might trigger undesirable market dynamics.

With regard to timing, central banks generally intervene reactively, once the initial bout of market pressure has subsided. This lets them maximise the effectiveness of intervention, instead of falling victim to market forces and depleting reserves significantly without having much impact. Such an approach can also be more flexible. For example, if the pressure on the currency reflects proxy hedging, it is more likely to be self-correcting and may not warrant intervention.

A comprehensive understanding of the functioning of global FX markets is especially valuable. It helps underpin central banks' decision-making on the best timing and place to intervene. For example, if the objective is to influence the exchange rate, operating in locations where and time zones when market liquidity is thin would enhance the impact. On the other hand, if the objective is to adjust the stock of reserves with minimal impact on the exchange rate, intervening in highly liquid markets and during hours when there is a large turnover would be desirable.

Discretionary interventions are the norm in EMEs, and very few central banks have experimented successfully with formal rules-based interventions. Discretion allows central banks to intervene flexibly, limit detection risk, and maximise effectiveness on account of the surprise factor. It also makes it harder for market participants to trade against the central bank, as in the case of precommitted intervention rules.

On communication and transparency, there is a marked difference across regions. Central banks in Latin America have typically opted for more transparency, both in terms of preannouncing their interventions and providing more detailed information after the fact. Central banks in Asian EMEs have been less transparent.

Central banks in Latin America have typically opted for more transparency, both in terms of preannouncing their interventions and providing more detailed information after the fact. Central banks in Asian EMEs have been less transparent.

Central banks have increasingly relied on market-based instruments to sterilise their interventions. As a result, central bank securities have become the most common instrument and reserve requirements have lost ground markedly. While market-based instruments can be more costly, they are instrumental in developing deep and liquid domestic bond markets and a local currency yield curve. Derivatives are quite prominent, and FX swaps in particular have long been used for sterilisation.

See eg T Ehlers and F Packer, "FX and derivatives markets in emerging market economies and the internationalisation of their currencies", BIS Quarterly Review, December 2013, pp 55-67. In particular, they document that the ratio of derivatives to spot market turnover in EMEs increased from 1.6 in 2007 to 2.3 in 2013. As per the IMF's special data dissemination standards (SDDS), only derivatives that are settled in foreign currency are recorded as reserves, while derivatives settled in local currency are reported only as "memo items". Market participants often tend to focus on headline reserve numbers excluding derivative positions. See P Cavallino and N Patel, "FX intervention: goals, strategies and tactics", BIS Papers, forthcoming, 2019.

Central banks could also address capital outflows, and thus exchange rate pressures, by facilitating the adjustment of investor portfolios in times of stress. Advanced economy central banks have provided monetary stimulus by taking duration out of the market through asset purchases, lowering long-term interest rates. EME central banks could follow a similar approach in times of stress. Specifically, when a large amount of foreign capital has been channelled into long-duration public debt and threatens to flow out quickly, the central bank may buy long-term government bonds and sell short-term instruments in order to stabilise bond markets.34

Macroprudential tools

Macroprudential policies complement monetary policy frameworks as an integral element of the wider macro-financial stability framework. They are targeted specifically at addressing risks to financial stability, which arise from domestic financial imbalances.

As discussed in detail in last year's Annual Economic Report,35 such policies rely on a wide set of instruments. These range from tools such as system-wide stress tests, countercyclical capital buffers and dynamic provisions to maximum loan-to-value and debt-to-income ratios. Compared with FX intervention, they target financial vulnerabilities more directly. And, in doing so, they provide an additional degree of freedom for monetary policy too.

Overall, the experience of the past two decades indicates that macroprudential measures do help improve the trade-offs monetary policy faces, including those in connection with capital flow and associated exchange rate fluctuations. They do so by strengthening the resilience of the financial system and by leaning against the build-up of financial imbalances. There is increasing evidence that macroprudential tools can to some extent influence variables such as credit, asset prices and the amplitude of the financial cycle.36 At the same time, because they are largely bank-based, they can leak. And they may be subject to a certain inaction bias,37 because of political economy pressures, among other factors. The evidence suggests that macroprudential measures alone cannot contain the build-up of financial imbalances and that they are best regarded as complements rather than substitutes for monetary policy in the pursuit of macro-financial stability.38

In addition, in some cases, authorities have also relied on capital flow management tools, as these have become less controversial over time.39 That said, evidence for their effectiveness is mixed. For example, while recent empirical studies have generally found that these tools can slow down targeted flows, these effects are typically temporary.40 Moreover, evidence in the post-GFC period suggests that tighter capital inflow restrictions generate spillovers to other countries.41

Sketching a framework

EME inflation targeting frameworks differ in significant respects from textbook inflation targeting frameworks, which prescribe pursuing price stability exclusively through adjustments in policy interest rates combined with freely floating exchange rates. EME central banks have addressed the challenges from capital flow and associated exchange rate swings through the use of complementary policy instruments. This practice has served EMEs well, as indicated by their macroeconomic performance over the past decades and the more specific empirical evidence supporting such a strategy. Yet important challenges remain.

As EME inflation targeters have moved ahead of theory, so the conceptual foundations of their frameworks have lagged behind. In particular, the different elements have been analysed largely in isolation. Box II.B provides a schematic framework that brings the different elements together and suggests how they can rationalise current policies. The analysis shows how the various channels through which capital flows and the exchange rate impact EMEs worsen trade-offs for central bank stabilisation policy and how FX intervention and macroprudential tools can ameliorate these trade-offs. Yet a full-fledged analytical framework that captures EME inflation targeters' full suite of policy practices remains to be developed.

On the practical side, the challenge is how best to design, implement and combine the various tools. Central banks need to decide how to develop and use their toolboxes. These include not only monetary tools proper, such as FX intervention, but also macroprudential tools, if these are under central bank control. The choice of instruments and their exact deployment will depend on country-specific factors, particularly economic and financial structures, as well as on the macro-financial background and policy objectives.

At the same time, authorities have to determine the policy horizon. Under inflation targeting regimes, monetary policy usually aims at stabilising inflation over horizons of up to two years, with policy decisions typically taken at less than a quarterly frequency. Macroprudential measures have a longer horizon, as they aim to mitigate longer-run financial stability risks. Given the slow-moving nature of such risks, these tools are adjusted less frequently, sometimes at yearly frequencies. By contrast, FX intervention often has a very short horizon, especially if it is aimed at stabilising exchange rate volatility, and operations may even be carried out at daily frequencies. However, both FX intervention and macroprudential measures shape the trade-offs involved in interest rate decisions (Box II.B).

This raises the question of the appropriate horizon for monetary policy. There is the enduring question of whether central banks may need to lengthen the horizon of their inflation targets in order to better address the intertemporal trade-off between short-term economic performance and longer-term financial and macroeconomic stability. One way of doing so is to enhance flexibility by lengthening the horizon over which inflation targets are pursued. This would help address the longer-run risks financial imbalances pose to macroeconomic stability. Importantly, the need for flexibility to address this intertemporal trade-off arises only when inflation is below target. This is because the reversal of capital inflows would result in inflationary pressures through its impact on the exchange rate. By implication, a tighter policy during the capital flow surge when inflation is already above target would be called for in response to both short-term and medium-term considerations.

Managing macroeconomic and financial stability with multiple instruments also poses challenges in terms of instrument assignment and coordination, especially as the transmission channels of the different instruments overlap. A common approach for instrument assignment is separation: policy rates respond primarily to domestic price and output developments, FX intervention mainly to unwelcome exchange rate fluctuations, and macroprudential measures to financial stability risks. Instruments are set in sequence, each taking the previous ones as given, and with different policy horizons. A rationale for instrument separation is clarity in the allocation of responsibilities, which could bolster the framework's credibility. The drawback is that each instrument is calibrated in isolation, rather than in a coordinated way, which could in theory yield better results.42

There are major communication challenges as well. Clear communication about policy objectives, frameworks, rules and decisions is generally seen as a key factor boosting the credibility and accountability of monetary policy regimes. This basic insight also applies to frameworks operated with multiple tools (interest rates and FX interventions, complemented by macroprudential tools) and multiple objectives (price, macroeconomic and financial stability). Yet outlining a communication strategy with multiple tools and objectives is particularly challenging. In such cases, authorities could benefit from frequent cross-referencing of decisions and rationalising the context, scope and objective behind each so as to minimise the risk of sending mixed signals. This is especially important in cases where different tools are used to achieve objectives at different horizons, so that they may not always move in the same direction.

In addition to boosting credibility and accountability, clear and active communication about policy rationales and intentions also matters for the effectiveness of specific measures and strategies. The transmission of policy rates to longer-term rates can be enhanced through transparency about the reaction function and the envisaged path of policy rates. For FX intervention, communication strategies will depend on the intermediate objective. If FX intervention serves to accumulate precautionary FX reserve buffers without any intended effect on exchange rates, the central bank might intervene discreetly or alternatively preannounce an intended fixed path for purchases. Rules-based FX intervention might help stabilise the exchange rate as market participants internalise the central bank's reaction to excess volatility, but it may also encourage position-taking against the central bank and reduce the surprise element of the intervention.

In future, EME central banks will need to further develop their toolboxes, frameworks and communications. At a time of large and internationally mobile financial capital and low interest rates, risk-taking and the search for yield acquire greater prominence and can expose EMEs to disruptive stock adjustments by global investors. Thus, central banks may need to reinforce and refine their FX intervention strategies and tactics. They may also need to consider further developing balance sheet policies in the domestic currency to help stabilise conditions in their capital markets at times of stress. In addition, in countries where inflation is low and well anchored, there could be scope for increasing the flexibility of inflation targeting frameworks to better take into account the longer-run risks to macroeconomic stability linked to the build-up of financial imbalances.

Monetary policy in EMEs: a simple analytical model

Capital flow fluctuations affect EMEs' macroeconomic stability through their impact on inflation, exports and domestic financial conditions via various channels. This box highlights the trade-offs that these effects may give rise to for EMEs, drawing on a stylised model. The trade-offs are both immediate, when inflation stabilisation comes at the cost of output stabilisation, and intertemporal, when stabilising inflation today raises macroeconomic vulnerabilities tomorrow. FX intervention and macroprudential tools can improve these trade-offs.

We develop a stylised simple model for the main channels through which capital flows affect EMEs, as discussed in the main text. The model is simply a pedagogical device designed to provide a stylised framework for policy analysis - as a reference point for future research. In the model, a surge in capital inflows appreciates the exchange rate, which, in turn, reduces import prices (pass-through channel) and export competitiveness (trade channel). The impact of the exchange rate on exports depends on trade invoicing and trade financing. Foreign currency invoicing and greater integration in global value chains (GVCs) weaken the trade channel, so that a currency appreciation might not act as a drag on economic activity, at least in the short run. Furthermore, the exchange rate affects domestic expenditure through its impact on domestic financial conditions (financial channel). An exchange rate appreciation improves domestic credit conditions and thus boosts domestic demand. Monetary policy affects the economy through the standard effects of the interest rate on domestic demand and on the exchange rate.

Further reading: online appendix

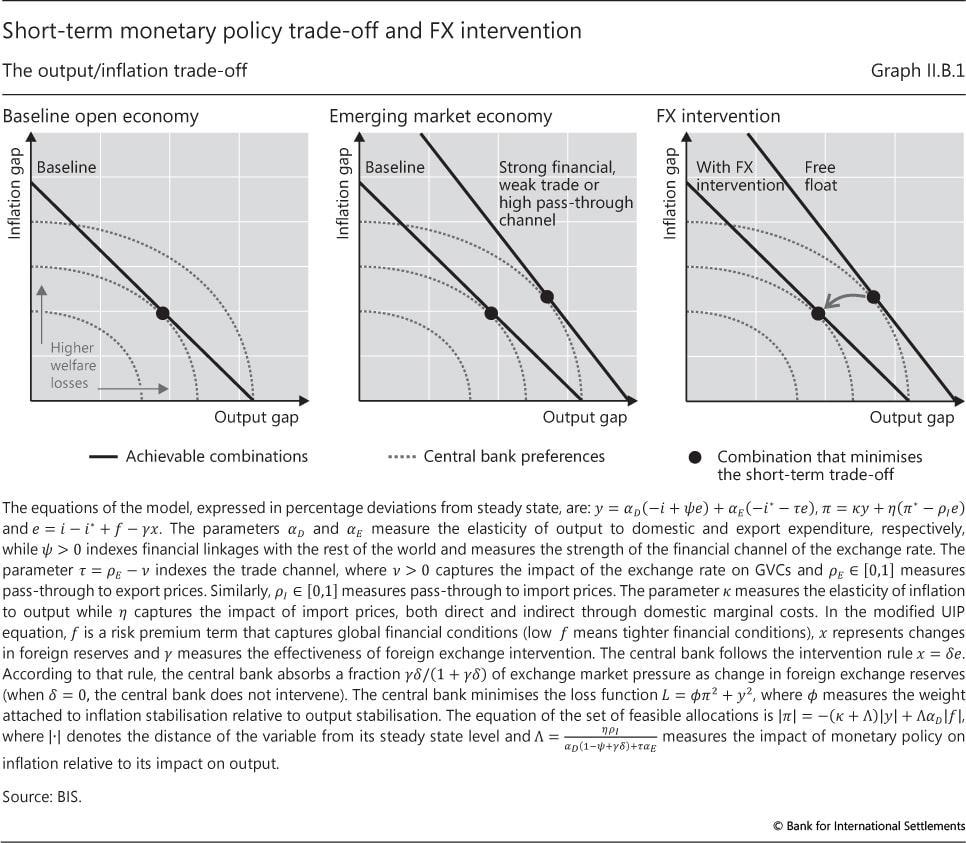

The strength of these channels determines the ultimate impact of capital flows on economic activity and inflation, and therefore shapes the trade-offs faced by central banks. Consider, first, the case of a baseline open economy lacking a financial channel and featuring a moderate inflation pass-through and a strong trade channel. In this situation, the appreciation caused by a capital inflow surge reduces inflation and output. By cutting its policy rate, the central bank can counteract this contractionary effect, but it cannot fully stabilise output and inflation at the same time. This is because the exchange rate affects inflation not only through the output gap but also directly through import prices via the exchange rate. Hence, the central bank faces a trade-off between output and inflation stabilisation, as represented by the downward-sloping line in Graph II.B.1 (left-hand panel). Greater inflation stabilisation is achieved only at the cost of more output variability, and vice versa. By changing its policy rate, the central bank can move along the frontier and achieve different combinations of inflation and output stabilisation. The central bank will choose the combination it prefers. The dotted curves in the graph provide a conventional representation of the central bank preferences. Points on the same curve represent combinations that the central bank values equally (ie give rise to the same welfare loss), while higher curves are associated with worse outcomes. The origin of the graph represents the first best, ie the point where output is at potential and inflation is equal to its target. The central bank sets the interest rate to implement the feasible combination of output and inflation gaps that lies on the curve closest to the first best.

Hence, the central bank faces a trade-off between output and inflation stabilisation, as represented by the downward-sloping line in Graph II.B.1 (left-hand panel). Greater inflation stabilisation is achieved only at the cost of more output variability, and vice versa. By changing its policy rate, the central bank can move along the frontier and achieve different combinations of inflation and output stabilisation. The central bank will choose the combination it prefers. The dotted curves in the graph provide a conventional representation of the central bank preferences. Points on the same curve represent combinations that the central bank values equally (ie give rise to the same welfare loss), while higher curves are associated with worse outcomes. The origin of the graph represents the first best, ie the point where output is at potential and inflation is equal to its target. The central bank sets the interest rate to implement the feasible combination of output and inflation gaps that lies on the curve closest to the first best.

Trade-offs worsen in the case, more realistic for an EME, where the exchange rate also affects domestic financial conditions, its pass-through to inflation is high due to foreign currency trade invoicing, or the trade channel is weaker due to the combination of foreign currency trade invoicing and trade financing. A strong financial channel and a weak trade channel reduce the contractionary effect of capital inflows on output, while a high degree of pass-through raises the negative impact of exchange rate appreciation on inflation. As a result, output and inflation move in a less synchronised way. Thus, the combinations of output and inflation gaps the central bank can achieve through interest rate policy shift outwards, further away from the origin (Graph II.B.1, centre panel). The central bank can attain the same level of inflation only by boosting output further beyond its potential. If the financial channel is particularly strong, dominating the trade channel, then output actually rises in response to an exchange rate appreciation. In this case, the trade-off between output and inflation is even worse, as the two variables move in opposite directions.

FX intervention is assumed to affect the exchange rate independently of conventional interest rate policy and can thus help to improve policy trade-offs. Specifically, to the extent that FX intervention can limit exchange rate movements by absorbing part of the capital flows, it makes it easier to stabilise the economy in response to shifts in global financial conditions (Graph II.B.1, right-hand panel). The feasible combinations of output and inflation gaps attainable with changes in interest rates shift back inwards towards the origin, improving outcomes.

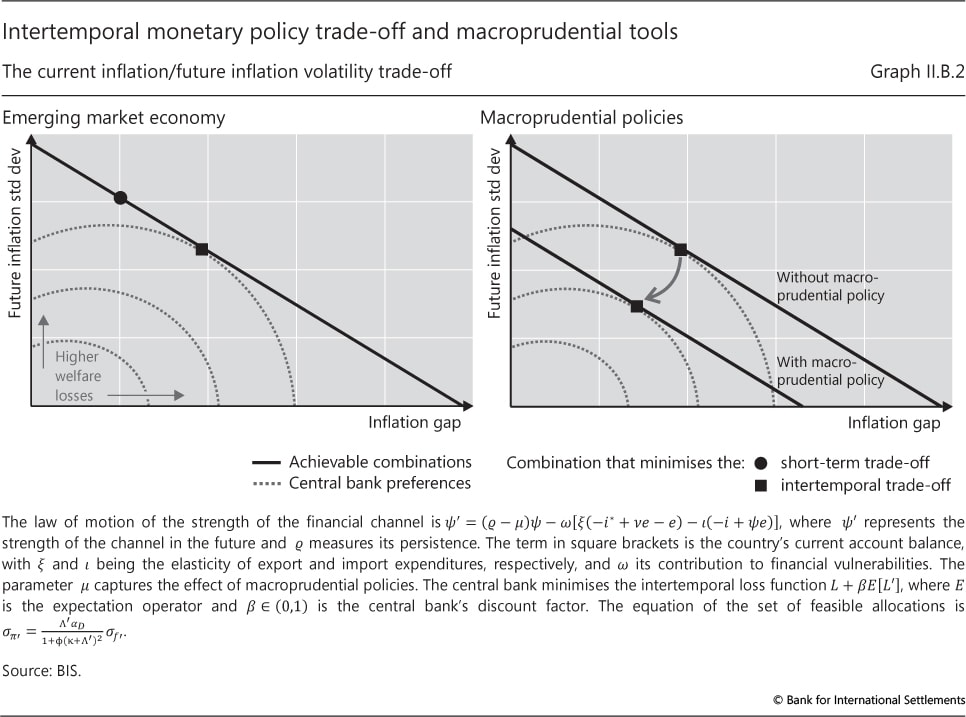

In addition to these immediate trade-offs, there are also intertemporal ones. Capital inflows lead to an increase in foreign debt, weakening the country's foreign asset position and possibly translating into a wider build-up of financial imbalances. This increases the economy's sensitivity to capital flow swings over time, as debt accumulates. Hence an intertemporal trade-off arises between inflation stability today and inflation volatility tomorrow. Specifically, the larger the cumulated capital inflows, the stronger the risks and impact of their potential future reversal. For example, in the face of a capital inflow surge and associated exchange rate appreciation, the central bank may cut its policy rate to mitigate the downward pressure on inflation. But to the extent that policy easing boosts imports and worsens the current account, the resulting increase in foreign debt raises the economy's exposure to capital flow reversals down the road, increasing future macroeconomic volatility. Taking this into consideration would mean tempering policy easing, and tolerating larger inflation deviations from target today in order to have more stability in the future (moving from the dot to the square in Graph II.B.2, left-hand panel).

Taking this into consideration would mean tempering policy easing, and tolerating larger inflation deviations from target today in order to have more stability in the future (moving from the dot to the square in Graph II.B.2, left-hand panel).

Macroprudential measures can ameliorate this intertemporal trade-off by mitigating the build-up of financial vulnerabilities and hence reducing the economy's sensitivity to capital flow and associated exchange rate swings. This would shift the trade-off frontier towards the origin (Graph II.B.2, right-hand panel). Foreign exchange intervention can have a similar effect. However, while macroprudential measures improve the economy's resilience, foreign exchange intervention directly limits foreign debt accumulation by leaning against exchange rate appreciation, further improving the trade-off.

Foreign exchange intervention can have a similar effect. However, while macroprudential measures improve the economy's resilience, foreign exchange intervention directly limits foreign debt accumulation by leaning against exchange rate appreciation, further improving the trade-off.

See footnote in Graph II.B.1 for a short summary of the model's key elements and the online appendix for a more detailed exposition. As discussed in the main text, capital flows can also impact domestic financial conditions directly, not only through the exchange rate. The analysis developed in this box would not change in the presence of such a direct link. Monetary policy might also affect capital flows through its impact on the carry trade. This channel can weaken and even reverse the transmission of monetary policy to the domestic economy. See P Cavallino and D Sandri, "The expansionary lower bound: contractionary monetary easing and the trilemma", BIS Working Papers, no 770, February 2019. The "divine coincidence", ie the possibility that interest rate policy could alone close both inflation and output gaps simultaneously, generically fails when the policy rate affects inflation in ways other than through the output gap, eg through the prices of imported goods via the exchange rate. As discussed in the main text, there are many reasons not included in the model that make it suboptimal to completely stabilise the exchange rate through intervention. For the case of the quasi-fiscal cost of intervention, see P Cavallino, "Capital flows and foreign exchange intervention", American Economic Journal: Macroeconomics, vol 11, no 2, April 2019, pp 127-70. To simplify the analysis, we assume that the country's exposure is proportional to its net foreign asset position. Hence, a reduction in the domestic policy rate increases financial vulnerabilities if it worsens the current account. However, this condition might be too restrictive, given that a country's exposure is a function of its gross, rather than just net, asset position. See eg C Borio and P Disyatat, "Global imbalances and the financial crisis: link or no link?", BIS Working Papers, no 346, May 2011. In our model, foreign debt amplifies the impact of capital flow and associated exchange rate swings and raises macroeconomic volatility. In reality, the build-up of financial vulnerabilities affects not only the exposure to but also the likelihood of a capital flow reversal. This channel worsens the intertemporal trade-off. More generally, if one also took into account the impact of monetary easing on domestic credit growth, the intertemporal trade-off would be even worse. See T Adrian and N Liang, "Monetary policy, financial conditions, and financial stability", International Journal of Central Banking, vol 14, no 1, January 2018, pp 73-132. As for foreign exchange intervention, we abstract from any cost of macroprudential measures. For example, countercyclical regulatory rules might induce volatility in capital requirements that can translate into volatility in other macroeconomic variables, including the exchange rate. See P-R Agénor, K Alper and L Pereira da Silva, "Sudden floods, macroprudential regulation and stability in an open economy", Journal of International Money and Finance, vol 48, November 2014, pp 68-100.

From a broader perspective, sound monetary policy frameworks need to be complemented by sound structural, fiscal and regulatory policies at the national level. One especially relevant element is the development of a stronger domestic base of institutional investors, reducing the dependence on foreign funding. At the same time, sound policy frameworks at the national level need to be complemented by a credible and effective global financial safety net that would mitigate risks of speculative attacks and reduce the need for self-insurance through large-scale FX reserve accumulation.

Endnotes

1 The classification is based on self-classification of the individual countries as well as the information provided in the IMF's Annual Report on Exchange Arrangements and Exchange Restrictions.

2 See eg R Clarida, J Gali and M Gertler, "Monetary policy rules and macroeconomic stability: evidence and some theory", The Quarterly Journal of Economics, vol 115, no 1, February 2000, pp 147-80; J Gali and T Monacelli, "Monetary policy and exchange rate volatility in a small open economy", Review of Economic Studies, vol 72, 2005, pp 707-34; and M Woodford, Interest and prices: foundations of a theory of monetary policy, Princeton University Press, 2003.

3 According to de facto classifications of exchange rate regimes proposed by academic researchers and which are based on the actual behaviour of exchange rates rather than official labels, EME inflation targeters are commonly characterised as managed floaters or as having crawling bands or pegs, while in advanced economies free floating is quite common. See E Ilzetzki, C Reinhart and K Rogoff, "Exchange arrangements entering the 21st century: which anchor will hold?", Quarterly Journal of Economics, vol 134, no 2, May 2019.

4 The reference group of inflation targeting advanced economies comprises the countries that have operated inflation targeting regimes throughout the past two decades. This includes Australia, Canada, New Zealand, Norway, Sweden and the United Kingdom.

5 See J Frankel, "Systemic managed floating", Open Economies Review, vol 30, no 2, April 2019, pp 255-95.

6 See BIS, "Understanding globalisation", 87th Annual Report, June 2017, Chapter VI.

7 See eg H S Shin, "The second phase of global liquidity and its impact on emerging economies", in K Chung, S Kim, H Park, C Choi and H S Shin (eds), Volatile capital flows in Korea, Palgrave Macmillan.

8 For evidence for the link between global financial conditions and capital flows to EMEs, see eg S Ahmed and A Zlate, "Capital flows to emerging market economies: a brave new world?", Journal of International Money and Finance, vol 48, November 2014, pp 221- 48; F Bräuning and V Ivashina, "US monetary policy and emerging market credit cycles", Journal of Monetary Economics, forthcoming; and S Avdjiev, L Gambacorta, L Goldberg and S Schiaffi, "The shifting drivers of global liquidity", NBER Working Papers, no 23565, June 2017.

9 According to Engel's law: as income rises, the proportion of income spent on food falls. Since EMEs have lower incomes on average than advanced economies, their consumption baskets tend to have a higher weight on food. For a more detailed discussion, see C Ho and R McCauley, "Living with flexible exchange rates: issues and recent experience in inflation targeting emerging market economies", BIS Working Papers, no 130, February 2003.

10 For more detailed analyses on the evolution and drivers of inflation in EMEs, see J Ha, A Kose and F Ohnsorge, "Inflation in emerging and developing economies", World Bank Publications, March 2019.

11 See IMF, World Economic Outlook, October 2018, for a more detailed analysis of the anchoring of inflation expectations in emerging market and advanced economies.

12 See G Gopinath, E Boz, C Casas, F Díez, P-O Gourinchas and M Plagborg-Møller, "Dominant currency paradigm", NBER Working Papers, no 22943, March 2019.

13 See C Upper and M Valli, "Emerging derivatives markets", BIS Quarterly Review, December 2016, pp 67-80.

14 See eg F Liriano, "The use of foreign exchange derivatives by exporters and importers: the Chilean experience", paper presented at the Eighth IFC Conference on Statistical implications of the new financial landscape, Basel, September 2016; and T Chuaprapaisilp, N Rujiravanich and B Saengsith, "FX hedging behaviour among Thai exporters: a micro-level evidence", Puey Ungphakorn Institute for Economic Research, PIER Discussion Papers, no 81, February 2018.

15 For more details of global trade financing, see Committee on the Global Financial System, "Trade finance: developments and issues", CGFS Papers, no 50, 2014.

16 See V Bruno, S-J Kim and H S Shin, "Exchange rates and the working capital channel of trade fluctuations", AEA Papers and Proceedings, May 2018, vol 108, pp 531-36.

17 See J Caruana, "Monetary policy for financial stability", keynote speech at the 52nd SEACEN Governors' conference, Naypyidaw, Myanmar, 2016.

18 For formal evidence of the link between global and emerging market equity returns and interest rates, see H Rey, "Dilemma not trilemma: the global financial cycle and monetary policy independence", in Global dimensions of unconventional monetary policy, proceedings of the Federal Reserve Bank of Kansas City Jackson Hole symposium, August 2014; M Obstfeld, "Trilemmas and trade-offs: living with financial globalisation", BIS Working Papers, no 480, January 2015; and B Hofmann, and E Takáts, "International monetary spillovers", BIS Quarterly Review, September 2015, pp 105-18.

19 See M Chui, E Kuruc and P Turner, "A new dimension to currency mismatches in the emerging markets: non-financial companies", BIS Working Papers, no 550, March 2016, for a more detailed analysis of foreign currency borrowing and currency mismatches in EMEs.

20 See Chui et al (2016), op cit.

21 See A Carstens and H S Shin, "Emerging markets aren't out of the woods yet", Foreign Affairs, 15 March 2019. Committee on the Global Financial System, "Establishing viable capital markets", CGFS Papers, no 62, 2019, provides a detailed analysis of the strength of institutional investor bases in advanced and emerging market economies.

22 This mechanism can be described as an exchange rate risk-taking channel, as exchange rate swings influence the lending capacity of global investors through their risk constraints; see B Hofmann, I Shim and H S Shin, "Bond risk premia and the exchange rate", BIS Working Papers, no 775, March 2019.

23 See C Borio, P McGuire and R McCauley, "Global credit and domestic credit booms", BIS Quarterly Review, September 2011, pp 42-57; and S Avdjiev, P McGuire and R McCauley, "Rapid credit growth and international credit: challenges for Asia", BIS Working Papers, no 377, April 2012.

24 See C Borio and P Lowe, "Assessing the risks of banking crises", BIS Quarterly Review, December 2002, pp 43-54; and P-O Gourinchas and M Obstfeld, "Stories of the twentieth century for the twenty-first", American Economic Journal: Macroeconomics, January 2012, vol 4, no 1, pp 226-65.

25 For more detailed discussions of this point, see Rey (2014), op cit; and Obstfeld (2015), op cit.

26 See eg BIS, 74th Annual Report, June 2004, particularly Box IV.B.

27 Throughout this chapter, the term "FX intervention" is used to refer exclusively to sterilised FX intervention. "Non-sterilised" interventions alter the level of bank reserves and, all else equal, go hand in hand with a change in the policy rate. The exception is when central banks operate with a floor (excess reserves) system, so that the policy rate is set equal to the deposit facility. But, in that case, bank reserves are effectively perfect substitutes for short-term government paper, making the distinction dubious at best. For a more detailed discussion, see P Disyatat, "Monetary policy implementation: misconceptions and their consequences", BIS Working Papers, no 269, December 2008.

28 The literature identifies two channels through which interventions can affect the exchange rate. The first is the signalling channel, which changes market participants' expectations about macroeconomic conditions or future policy. The second is a portfolio balance channel, which operates whenever assets denominated in different currencies are imperfect substitutes. For a survey of the early literature, see L Sarno and M Taylor, "Official intervention in the foreign exchange market: is it effective and, if so, how does it work?", Journal of Economic Literature, vol 39, no 3, September 2001, pp 839-68. For recent theoretical contributions on the portfolio balance channel, see X Gabaix and M Maggiori, "International liquidity and exchange rate dynamics", Quarterly Journal of Economics, vol 130, no 3, August 2015, pp 1369-420; and P Cavallino, "Capital flows and foreign exchange intervention", American Economic Journal: Macroeconomics, vol 11, no 2, April 2019, pp 127-70.

29 For an overview of the evidence, see A Ghosh, J Ostry and M Qureshi, Taming the tide of capital flows: a policy guide, MIT Press, 2018; and L Menkhoff, "Foreign exchange intervention in emerging markets: a survey of empirical studies", The World Economy, vol 36, no 9, September 2013, pp 1187-2008. See also recent high-frequency evidence for Israel in I Caspi, A Friedman and S Ribon, "The immediate impact and persistent effect of FX purchases on the exchange rate", Bank of Israel, Discussion Papers, no 2018.04, June 2018; and for Colombia, B Hofmann, H S Shin and M Villamizar-Villegas, "FX intervention and domestic credit: evidence from high-frequency micro data", BIS Working Papers, no 774, March 2019.

30 See also J Davis, D Crowley and M Morris, "Reserve adequacy explains emerging-market sensitivity to US monetary policy", Federal Reserve Bank of Dallas, Economic Letter, vol 13, no 9, December 2018, pp 1-4; P García and C Soto, "Large hoardings of international reserves: are they worth it?", Central Bank of Chile, Working Papers, no 299, 2004; R Llaudes, F Salman and M Chivakul, "The impact of the great recession on emerging markets", IMF Working Papers, no WP/10/237, October 2010; and A Silva, "The self-insurance role of international reserves and the 2008-2010 crisis", Central Bank of Brazil, Working Paper Series, no 256, November 2011. More generally, O Blanchard and G Adler, "Can foreign exchange intervention stem exchange rate pressures from global capital flow shocks?", NBER Working Papers, no 21427, July 2015, find that FX intervention mitigates the impact of shifts in global capital flows on the economy.

31 See Ghosh et al (2018), op cit; and R Chang, "FX intervention redux", NBER Working Papers, no 24463, March 2018.

32 High-frequency evidence for Colombia paints a similar picture; see Hofmann et al (2019), op cit.

33 See eg A Barajas and A Morales, "Dollarization of liabilities: beyond the usual suspects", IMF Working Papers, no WP/03/11, 2003; and J Berrospide, "Exchange rates, optimal debt composition, and hedging in small open economies", Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series, no 2008-18, January 2008.

34 For example, in 2013 the Bank of Mexico swapped long-term securities for short-term securities via auctions in order to address stock adjustment by global investors. This policy stabilised conditions in peso-denominated bond markets.

35 See BIS, "Moving forward with macroprudential frameworks", Annual Economic Report, June 2018, Chapter IV; and C Borio, "Macroprudential frameworks: experience, prospects and a way forward", speech on the occasion of the Annual General Meeting of the Bank for International Settlements, Basel, 24 June 2018.

36 For recent reviews of the effectiveness of macroprudential instruments, see G Galati and R Moessner, "What do we know about the effects of macroprudential policy?", Economica, vol 85, no 340, October 2018, pp 735-70; and S Claessens, "An overview of macroprudential policy tools", Annual Review of Financial Economics, vol 7, no 1, December 2015, pp 397-422.

37 See S Ingves, "It takes all sorts - macroprudential oversight in the EU", keynote address at the First ESRB Annual Conference, September 2016.

38 See eg V Bruno, I Shim and H S Shin, "Comparative assessment of macroprudential policies", Journal of Financial Stability, vol 28, February 2017, pp 183-202; and L Gambacorta and A Murcia, "The impact of macroprudential policies and their interaction with monetary policy: an empirical analysis using credit registry data", BIS Working Papers, no 636, April 2017.

39 See, in particular, the IMF's explicit endorsement of the use of capital controls to calm volatile cross-border capital flows under its institutional view: IMF, The liberalization and management of capital flows: an institutional view, November 2012.

40 BIS (2018), op cit.

41 See eg G Pasricha, M Falagiarda, M Bijsterbosch and J Aizenman, "Domestic and multilateral effects of capital controls in emerging markets", Journal of International Economics, vol 115, November 2018, pp 48-58.

42 See P-R Agénor and L Pereira da Silva, Integrated inflation targeting: another perspective from the developing world, BIS-CEMLA, February 2019, for a detailed discussion of the benefits and challenges in the use and calibration of policy rates, FX intervention and macroprudential tools in an integrated macro-financial stability framework.