Monetary policy: more accommodation, less room

Abstract

Monetary policy remained exceptionally accommodative as the room for manoeuvre shrank and the prospects for further delay in policy normalisation increased. Against the backdrop of diverging monetary policies among the major advanced economies, some central banks continued to supplement historically low policy rates with further expansion of their balance sheets. Inflation developments played a big role in policy decisions, as exchange rate swings and declines in commodity prices affected headline inflation. At the same time, central banks had to factor in the inflationary cross-currents coming from a mix of cyclical and secular drivers, with the latter continuing to keep a lid on underlying inflation. Central banks also had to grapple with concerns about the seemingly diminished effectiveness of monetary policy through domestic channels. Naturally, external channels took on greater prominence, but they also presented additional challenges to price and financial stability. More broadly, the evolving policy tensions between price and financial stability underscored the need to raise the prominence of financial stability considerations, both of a domestic and external nature, in current monetary policy frameworks. Further progress has been made in understanding the trade-offs and in operationalising such a framework.

Full text

Monetary policy remained very accommodative over the past year as the room for manoeuvre narrowed. This long-standing exceptional stance was maintained against the backdrop of stubbornly low headline inflation in many economies, uneven global economic momentum and maturing domestic financial cycles in a number of emerging market economies (EMEs) and in some of the advanced economies least affected by the Great Financial Crisis.

Various domestic and external themes were prominent. Growing uncertainty about the timing and size of the policy divergence among the major advanced economies complicated policy and contributed to exchange rate fluctuations. Declining commodity prices weighed heavily on policy considerations. While these developments raised questions about the anchoring of inflation expectations, central banks also had to grapple with conflicting domestic and global inflation cross-currents of a cyclical and secular nature.

Meanwhile, there were lingering concerns about the declining effectiveness of domestic channels of monetary policy and about the side effects of persistent accommodation. The external channels, notably the exchange rate, became more prominent and raised challenges of their own.

In a broader perspective, another year of very accommodative policy, along with expectations of a more moderate pace of normalisation, highlighted the growing tensions between price stability and financial stability. These tensions heightened interest in evaluating the costs and benefits of more financial stability-oriented monetary policy frameworks and in their practical implementation.

The first section reviews the past year's monetary policy and inflation developments. The second examines challenges associated with the growing importance of the external channels of monetary policy as domestic channels wane. The third, taking further the analysis presented in previous years, explores how monetary policy frameworks can evolve to better account for financial stability and more effectively address the trade-offs between price stability and financial stability.

Recent developments

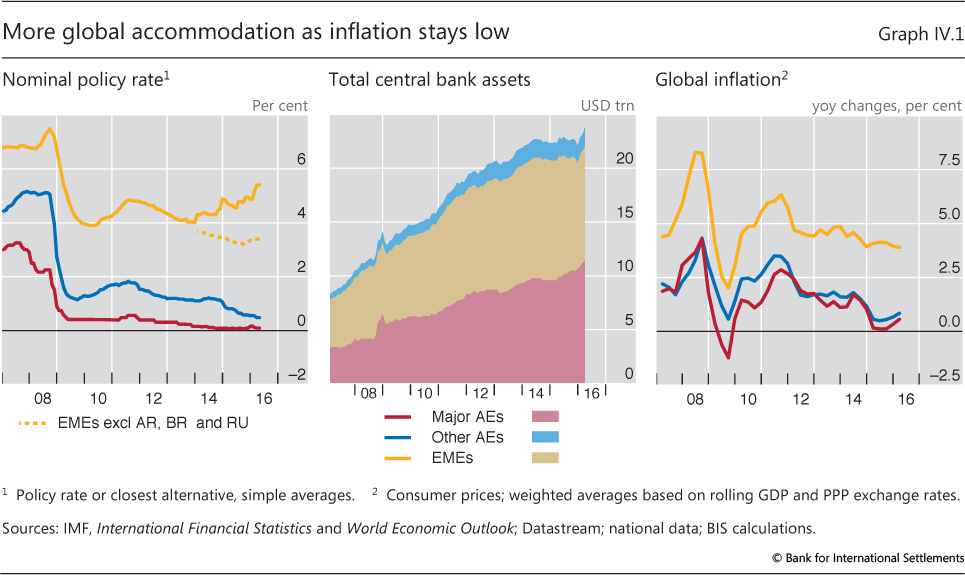

Central banks held nominal policy rates very low (Graph IV.1) amid increased prospects of a further delay in normalisation. The size of central bank balance sheets remained near historical highs, and some are poised to expand further. This transpired against the backdrop of low headline inflation, moderate economic expansion and tightening labour markets. The main differences across economies arose from variations in their exposure to exchange rate fluctuations, commodity price swings, financial market volatility and uncertainty about growth prospects.

Monetary policy normalisation delayed further

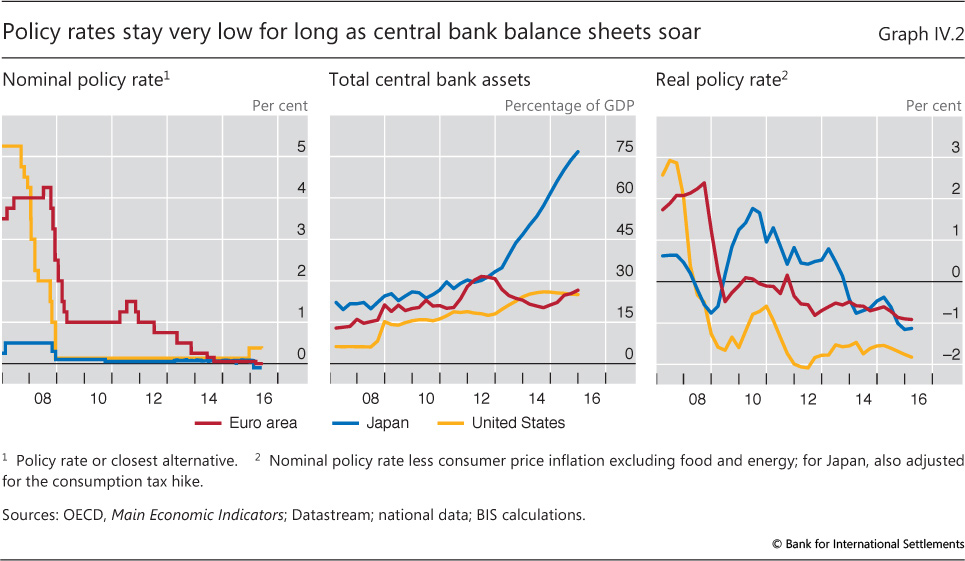

Central banks from the major advanced economies began the period under review with policy rates near zero and balance sheets larger than at the outset of the preceding year (Graph IV.2). With core inflation positive, real policy rates remained exceptionally low. In fact, real policy rates have not been so low for so long since the start of the postwar period. Where domestic conditions differed, the prospects for policy divergence loomed large.

In the United States, the long-awaited policy rate lift-off came in December. The 25 basis point increase in the target band raised the effective federal funds rate to roughly 35 basis points. In taking its action, the Federal Reserve cited an improvement in labour market conditions, a pickup in underlying inflation pressures and a more favourable economic outlook, but also stated that current conditions would warrant "only gradual" further increases in the policy rate. However, early in 2016, higher downside risks to the recovery and a spike in global financial market volatility led market participants to expect an even slower normalisation of the policy rate, including with a lower end point. The Federal Reserve's pace of normalisation is expected to be unusually gradual by historical standards.

Meanwhile, the ECB and the Bank of Japan eased policy further at the turn of the year. They cut policy rates and ramped up non-standard monetary measures. The size of their balance sheets continued to grow.

The ECB held its main policy rate (the rate on its main refinancing operations - MRO) just above zero for most of the period but cut rates in March 2016. It lowered the MRO rate to zero and the interest rate on the deposit facility to -40 basis points. With the euro overnight interest rate (EONIA) tracking the deposit rate, policy was more accommodative than indicated by the MRO rate alone. The ECB also launched a set of new measures that boosted the pace of its asset purchase programme, expanded asset eligibility to include non-financial corporate bonds and made its targeted longer-term refinancing operations (TLTRO) more attractive. The package sought to ease financing conditions, support the economy and address disinflationary risks.

The Bank of Japan eased policy to achieve its 2% inflation target. With downside inflation risks emerging, especially from lower oil prices, weak external demand and yen appreciation, it enhanced its Quantitative and Qualitative Monetary Easing (QQE) programme in December and January. Its balance sheet reached new heights (Graph IV.2, centre panel). It also adopted negative policy rates for the first time, applying the negative rate only to marginal increases in current account balances so as to protect bank profitability (Chapter VI). The objective of the various measures was to lower the sovereign yield curve and benchmark lending rates.

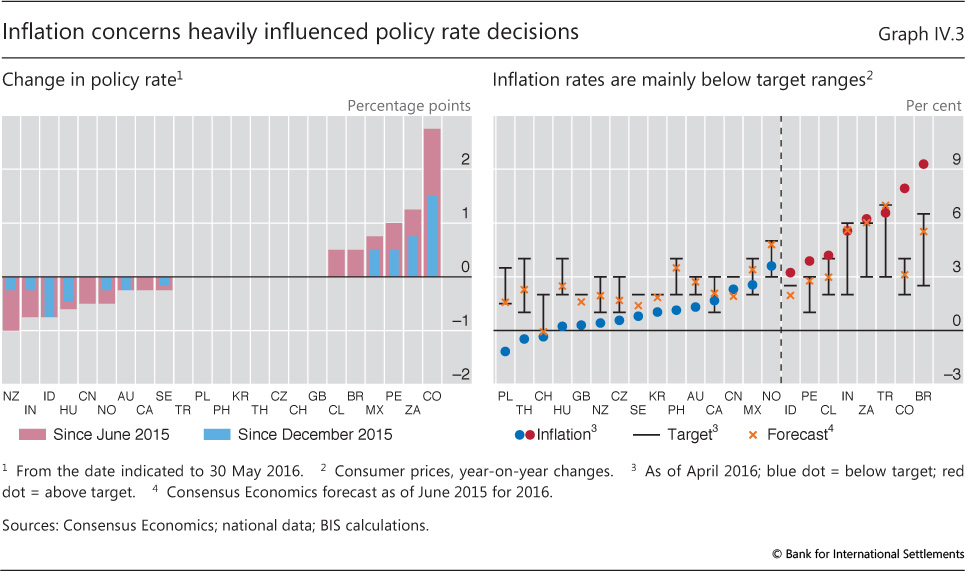

Central banks outside the major advanced economies faced a more diverse set of challenges. A roughly equal number cut rates, kept them unchanged or raised them (Graph IV.3, left-hand panel). Most had policy rates below historical averages.

Deviations from inflation targets were a dominant theme for most central banks. With sharp commodity price drops pushing headline inflation down, those central banks already facing low core inflation trends cut rates further from historically low levels, including Australia, Canada, New Zealand and Norway. Inflation in some of these economies remained below target despite currency depreciations. At the same time, the growth of credit and house prices raised financial stability concerns, especially given high household debt.

Economic weakness in China proved to be challenging at home and abroad, inducing an easing bias, especially in Asia. The People's Bank of China, also addressing low inflation and financial stability concerns, cut its interest rates and the required reserve ratio five times beginning in early 2015. The depreciation of the renminbi helped soften the blow to the economy but increased the challenges faced by many of China's regional and global trading partners. The general slowdown in EMEs and lower inflation led Indonesia to cut rates and Korea and Thailand to maintain a very accommodative monetary policy stance.

Most central banks with policy rates at or near the lower bound and facing very low inflation - including Switzerland, the United Kingdom and some eastern European economies - kept rates unchanged given their limited policy room. In Sweden, however, where inflation was well below target despite robust growth, the central bank pushed rates deeper into negative territory, expanded its purchases of securities and, at an unscheduled policy meeting, increased its readiness to intervene in the currency market. Like the Swiss National Bank, the Swedish central bank expressed concerns about strong mortgage lending growth and residential property price increases. The Czech Republic maintained its exchange rate floor to reduce downside inflation risks from currency appreciation. These economies remained particularly exposed to exchange rate-induced disinflationary spillovers from the ECB's accommodative policy.

For others, sharp exchange rate depreciations and the associated higher inflation led to policy rate hikes. The central banks of South Africa, Turkey and many commodity-exporting EMEs in Latin America, whose currencies fell sharply, saw inflation run above target and either raised or maintained high rates despite deteriorating growth prospects. As a result, inflation was generally expected to finish 2016 inside the respective target bands of these countries (Graph IV.3, right-hand panel). Brazil and Colombia continued to address persistent above-target inflation with relatively high policy rates. In India, despite inflation running above the mid-point of the medium-term 4% target, the central bank cut rates, as falling inflation, albeit from high rates, was seen as consistent with its disinflation "glide path" announced the previous year.

Inflationary cross-currents

In the period under review, inflation continued to be driven by a complex mix of near-term, cyclical and secular factors (see also the detailed discussion in the 85th Annual Report).

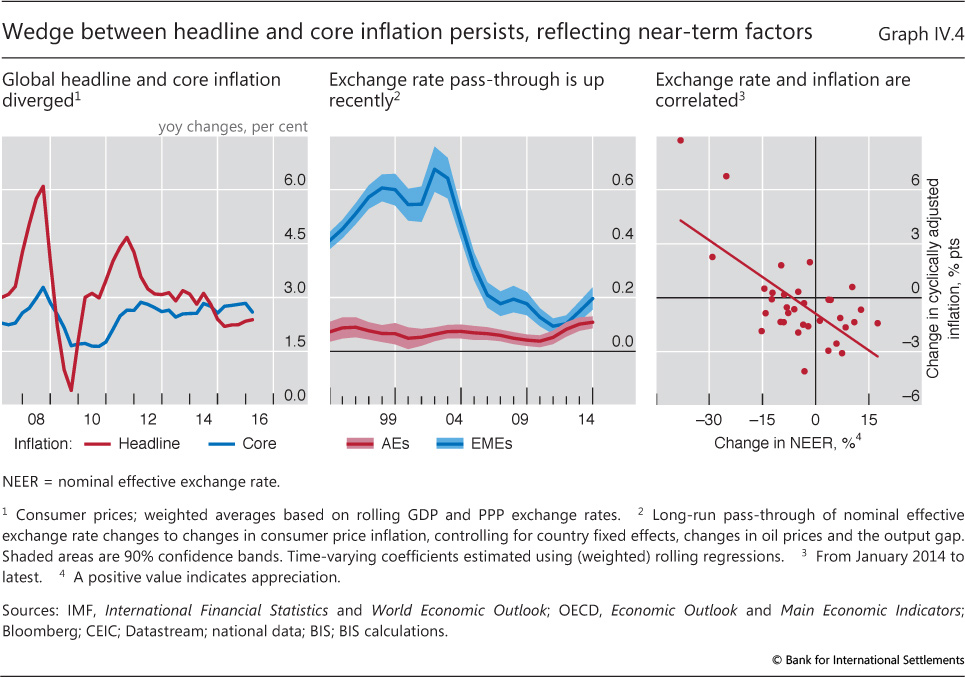

As noted above, among the near-term, proximate determinants of inflation, commodity prices and exchange rates loomed large. The sharp drop in commodity prices in 2015, especially the oil price, widened the wedge between headline and core inflation (Graph IV.4, left-hand panel). The large exchange rate changes influenced inflation to an extent that differed across countries, based in part on the incidence of second-round effects. Empirical evidence indicates that the pass-through to prices has generally fallen over time, first in advanced economies and later in EMEs (Graph IV.4, centre panel). Even so, it more recently appears to have picked up somewhat, possibly reflecting the size and greater persistence of exchange rate movements (Chapter III, and Graph IV.4, right-hand panel).

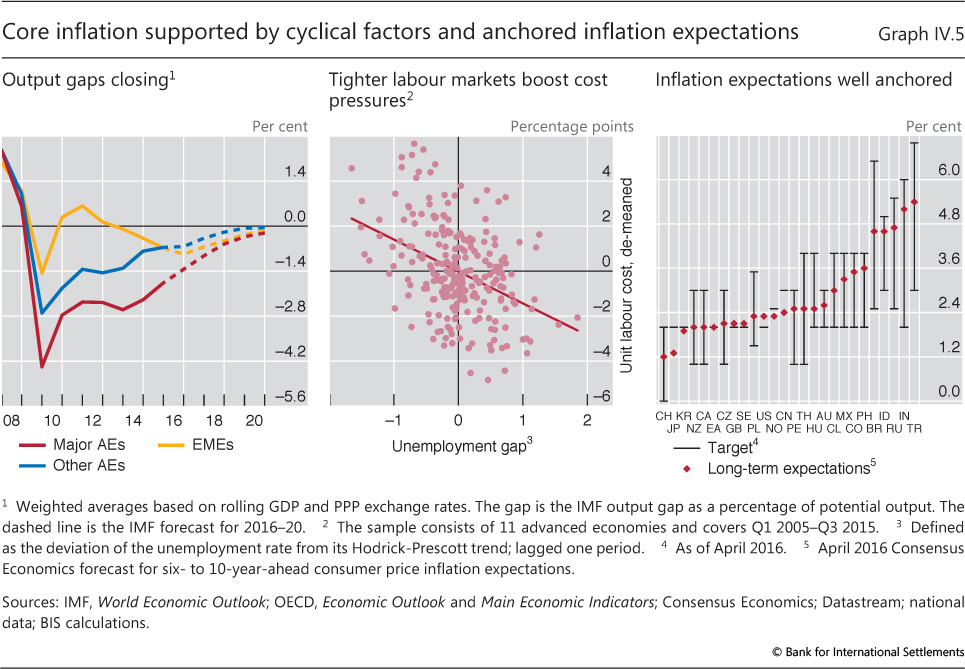

Cyclical demand drivers, notably various measures of economic slack, indicate a modest rise in the momentum of global inflation (Graph IV.5). Measures of slack, such as unemployment rates and conventionally measured output gaps (domestic and global), are shrinking. With a lag, tighter labour markets point to incipient wage pressures.

Secular drivers, such as globalisation and technology, continue to hold down inflation. In many respects, these forces result in "good" disinflation, ie linked to a supply side expansion, in contrast to costly cyclical-demand-driven disinflation.

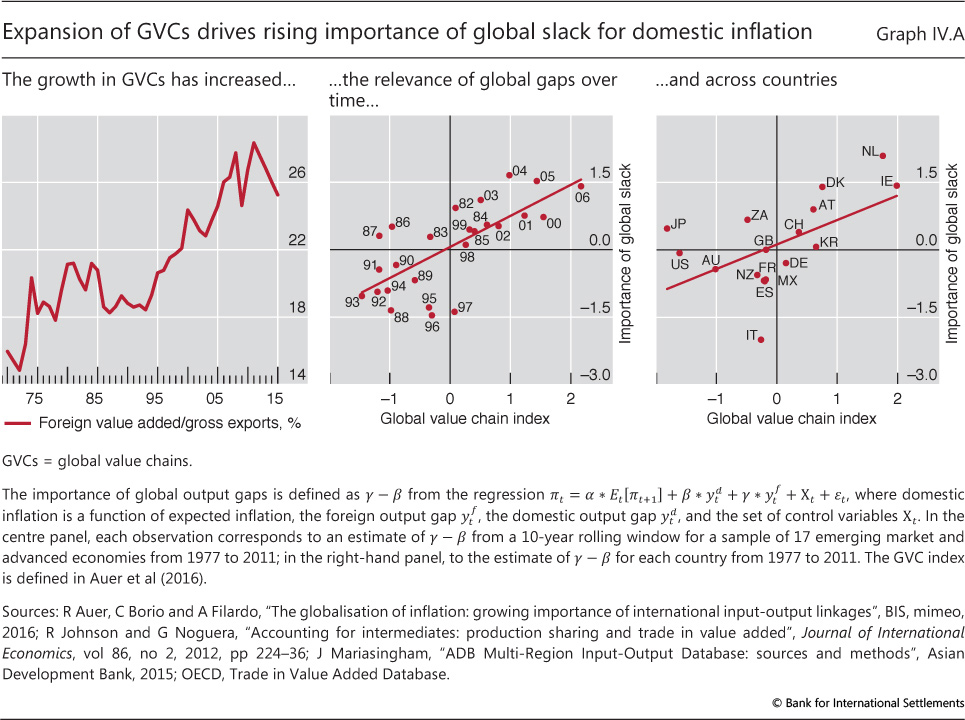

In fact, technological advances and other favourable global supply side forces appear to have become more prominent. One reason is that cost-cutting innovations are being transmitted more quickly through expanding global value chains (GVCs). These forces have kept a lid on prices directly, via low-cost tradable goods, as well as indirectly, by boosting competitive pressures on tradable and non-tradable inputs such as labour. Indeed, recent evidence indicates that the expansion of GVCs has had a significant effect on inflation, helping to account for the greater role of global slack in determining domestic inflation (Box IV.A).

Trends in long-run inflation expectations also play a role. Over the past year, persistent deviations of inflation from target - mostly on the low side but in some cases on the high side - have raised concerns about de-anchoring. For example, persistently low headline inflation, even if driven by transitory forces, could raise price stability risks if second-round effects were to take hold and feed into wage and inflation expectations. Risks would be higher if doubts grew about the ability of monetary authorities to boost inflation.

This puts the spotlight on the reliability of different indicators of inflation expectations. So far, survey-based measures suggest that long-term expectations remain well anchored in most economies (Graph IV.5, right-hand panel). In contrast, the message coming from financial markets is more mixed. In a number of countries, asset price indicators have pointed to a possible weakening in the anchor. That said, there are a number of reasons to question the reliability of these measures. The financial assets typically used to assess long-term inflation expectations (such as the five-year five-year-forward break-even rates) are subject to several distortions. These include liquidity and term premia, which can be hard to interpret at times. And the recent strong correlation between the decline in these measures and that in oil prices remains a puzzle. The oil price decline should not have a lasting effect on inflation five to 10 years down the road. Hence, the correlation suggests that short-term market conditions may be having an undue influence.

Box IV.A

Global value chains and the globalisation of inflation

The rise of global value chains (GVCs) has made them a key channel through which the drivers of domestic inflation have become more global. GVCs are supply chains in which different stages of production are strategically dispersed and coordinated around the globe. Their growth has transformed the nature of international production and trade. The growth is evident in the steady increase over the past several decades in the fraction of the value added of exports of goods and services due to their import content, which grew from 18% in 1990 to around 25% in 2015 (Graph IV.A, left-hand panel).

Their growth has transformed the nature of international production and trade. The growth is evident in the steady increase over the past several decades in the fraction of the value added of exports of goods and services due to their import content, which grew from 18% in 1990 to around 25% in 2015 (Graph IV.A, left-hand panel).

This trend has had implications for inflation dynamics. Domestic production costs depend not only on price developments at home but also on developments abroad, both directly and indirectly. And GVCs provide various channels through which foreign price pressures are transmitted to domestic inflation. The direct channel is through price pressures for imported inputs. The indirect channel is through implicit competition at each of the increasing number of links along the whole supply chain (ie contestability of markets). These channels are relevant for import-competing goods and services and also for non-tradable inputs, such as labour. Moreover, the trends in GVCs over time and across countries have strengthened these channels.

The impact of GVCs on inflation dynamics has been significant in recent decades. Recent research finds a strong positive relationship between the growth of GVCs and the strengthening of global factors influencing domestic inflation. Over time, the growth of GVCs has coincided with the rising importance of global output gaps in explaining domestic inflation developments (Graph IV.A, centre panel). This correlation between GVCs and global output gaps can also be seen cross-sectionally (Graph IV.A, right-hand panel): those countries that are more highly integrated into GVCs exhibit a stronger association between global output gaps and domestic inflation.

Over time, the growth of GVCs has coincided with the rising importance of global output gaps in explaining domestic inflation developments (Graph IV.A, centre panel). This correlation between GVCs and global output gaps can also be seen cross-sectionally (Graph IV.A, right-hand panel): those countries that are more highly integrated into GVCs exhibit a stronger association between global output gaps and domestic inflation.

The stages include design, production and marketing, among other activities. See the 84th Annual Report, Chapter III, for evidence on the rising importance of global gaps; see also Auer et al (2016).

Shifting from domestic to external monetary policy channels

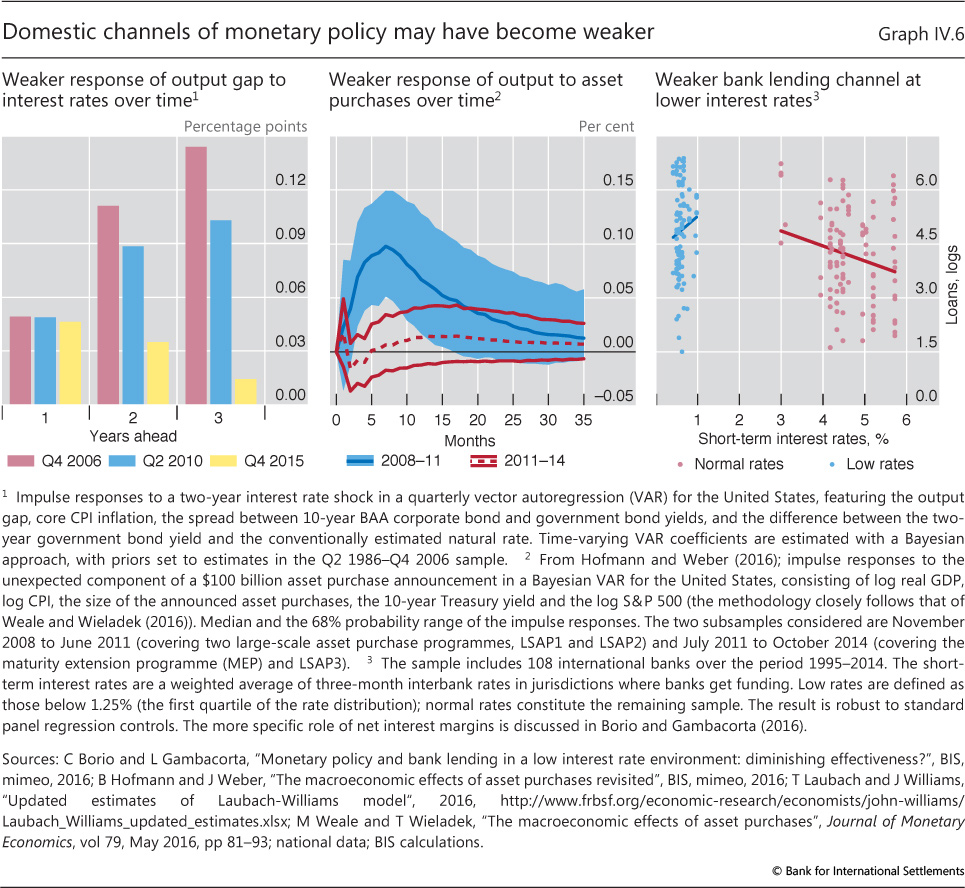

Global demand has grown only moderately and inflation has remained stubbornly low in advanced economies and some EMEs despite an extended period of exceptionally accommodative monetary policy. There is a general sense that post-crisis monetary policy has faced stiff headwinds, which may have sapped its effectiveness. Several factors have played a role, including large debt overhangs, an impaired banking system and the need to shift resources away from temporarily bloated sectors, such as construction and financial services. Simple analyses provide suggestive supportive evidence. In the United States, for instance, there are signs that the impact of policy on output via interest rates may have declined (Graph IV.6, left-hand panel). Policy's impact on inflation also appears to be more muted, given indications of a further weakening of the apparent link between measures of slack and inflation - a well known phenomenon.

These headwinds should have been abating owing to the gradual re-absorption of debt overhangs and improvements in impaired bank balance sheets. Nevertheless, the domestic channels through which unconventional monetary policies work may have become less effective as these measures have intensified and time has worn on. This could help explain why external channels, ie the exchange rate, have gained prominence in the policy debate. A greater role for the exchange rate, however, raises a number of issues that deserve special attention.

The diminishing effectiveness of domestic channels...

Changes in policy rates influence spending through a variety of channels. Lower interest rates reduce the cost and improve the availability of external funding for both households and firms, including by boosting asset prices and cash flows. More generally, they provide incentives to bring spending forward by reducing the return on savings and hence the amount of future consumption that has to be given up by consuming more today.

The various types of so-called unconventional monetary policies adopted post-crisis operate in broadly similar ways. Large-scale asset purchases are designed to boost the price (ie compress the yield) of the corresponding assets and, through portfolio adjustments, those of others. Lending on favourable terms (ie long maturities, generous collateral valuations etc) is intended to improve funding conditions. Signalling the future path of the policy rates (ie forward guidance) seeks to lower the yield curve, especially over the policy horizon. And driving the policy rate into negative territory aims at shifting the yield curve downwards.

There may be reasons for believing that the effect of these policies on domestic financial conditions could decline over time. In some cases, declining effectiveness may reflect improving market conditions. For instance, some argue that balance sheet measures, such as asset purchase programmes, are likely to be most effective when financial markets are segmented and dislocated, so that the authorities' intervention works through alleviating the corresponding stresses. As the crisis forces waned, the apparent effectiveness of large-scale asset purchases in influencing output declined (Graph IV.6, centre panel).

In other cases, it is the impact of these measures on financial intermediation that may be contributing to the decline. A possible example is the impact on the financial system's profitability and resilience, and hence on its ability to support the economy. As rates fall further, possibly becoming negative, and retail bank deposit rates remain sticky, the compression of banks' interest margins may reduce their profitability as well as their ability and incentive to lend (Chapter VI). Some evidence suggests that the impact of interest rates on lending weakens as they fall to very low levels and squeeze net interest margins (Graph IV.6, right-hand panel). This might reflect the lower profitability of the lending business, possibly in combination with scarce capital. In Switzerland, for example, following the introduction of negative interest rates, banks initially raised mortgage rates in order to protect their profits (Chapter II).

In yet other cases, broader behavioural factors may be at work. For instance, it is well known that investment is not very responsive to interest rates: when interest rates are extraordinarily low, firms may be more tempted to borrow simply in order to buy back shares or acquire other firms (Chapter II). Similarly, at very low rates the need to save more for retirement becomes more evident, as highlighted by the large underfunding of pension funds (Chapter VI). Likewise, households' confidence may be shaken by the prospect of negative nominal interest rates, given the widespread attention paid to nominal variables (ie "money illusion") and the sense of direness that adopting negative rates may convey. A recent survey finds that only a small percentage of households would spend more if faced with negative rates, while a similar percentage would actually spend less.1

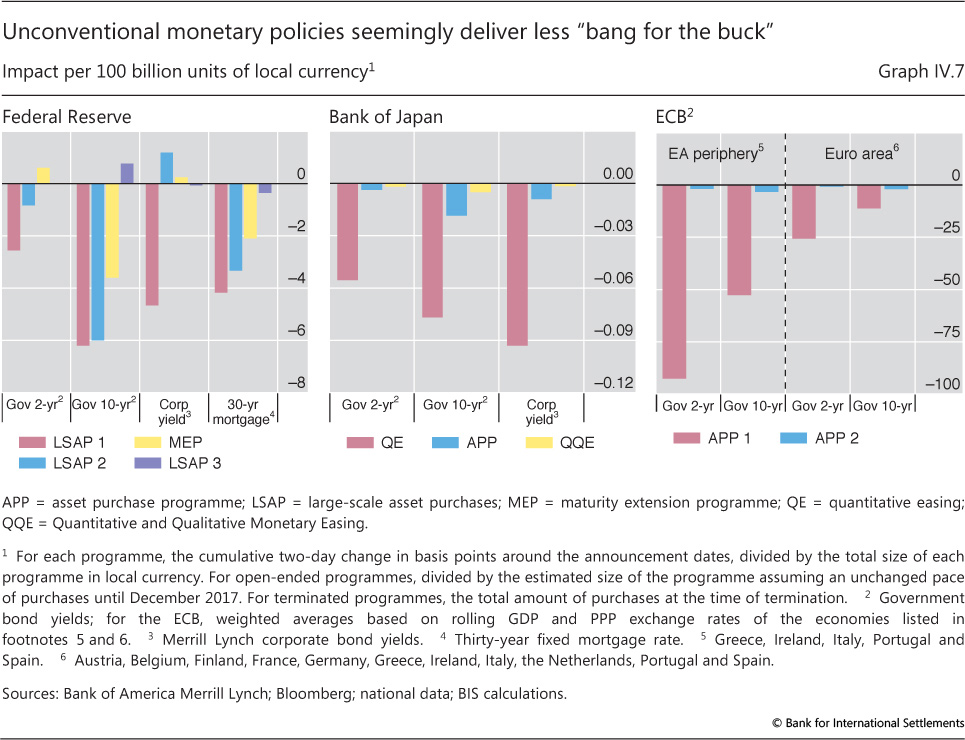

Behavioural factors may also complicate any additional policy easing. To have a big impact on yields and prices, easing must generally surprise markets. But surprising them becomes harder once they become used to large doses of accommodation: the bar rises with every measure taken. As a result, bigger measures may be needed to generate a given effect. This may be a reason, though not the only one, why successive large-scale asset purchase programmes appear to have had a smaller impact on yields for any given size of purchase (Graph IV.7).

More generally, there are natural limits to the process - to how far interest rates can be pushed into negative territory, central bank balance sheets expanded, spreads compressed and asset prices boosted. And there are limits to how far spending can be brought forward from the future. As these limits are approached, the marginal effect of policy tends to decline, and any side effects - whether strictly economic or of a political economy nature - tend to rise. This is why central banks have been closely monitoring these side effects, such as the impact on risk-taking, market functioning and financial institutions' profitability.

...and the rising prominence of external channels

As the effectiveness of domestic channels seems to have waned in recent years, a key external channel - ie the exchange rate - has naturally attracted greater attention. All else equal, monetary policy easing generally depreciates the currency, even if only as a by-product.

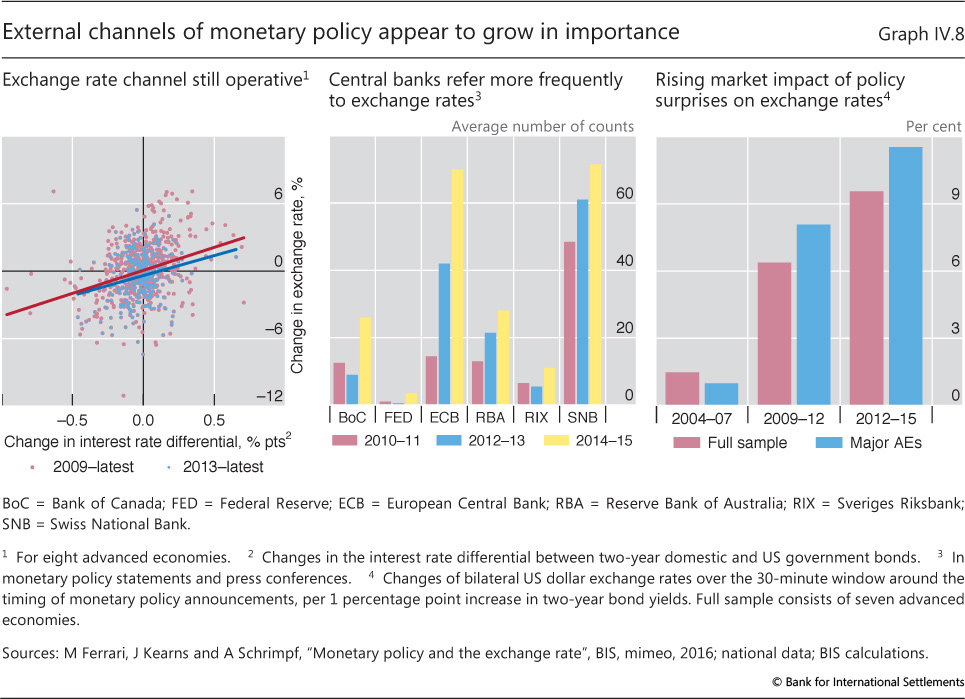

Indeed, shifts in the monetary policy stance continue to influence exchange rates. The relationship between exchange rates and interest rate differentials over the past few years has been fairly stable (Graph IV.8, left-hand panel). Monetary policy decisions have loomed large in medium-term currency swings in recent years (Chapter II). Similarly, the more prominent role of the exchange rate is evident from the greater frequency with which central bank statements make reference to them (Graph IV.8, centre panel) and from the seemingly larger exchange rate moves in response to policy announcements (right-hand panel).

From a purely domestic perspective, the exchange rate channel has a number of advantages for those economies facing stubbornly low inflation and growth. In the presence of too much debt and an impaired banking system, currency depreciation boosts demand while at the same time increasing saving (eg firms' profits). This can help repair balance sheets more quickly. Historically, depreciations have helped countries recover from crises. In addition, they have a quicker, if generally temporary, effect on inflation, unlike the weaker and more uncertain impact through domestic slack.

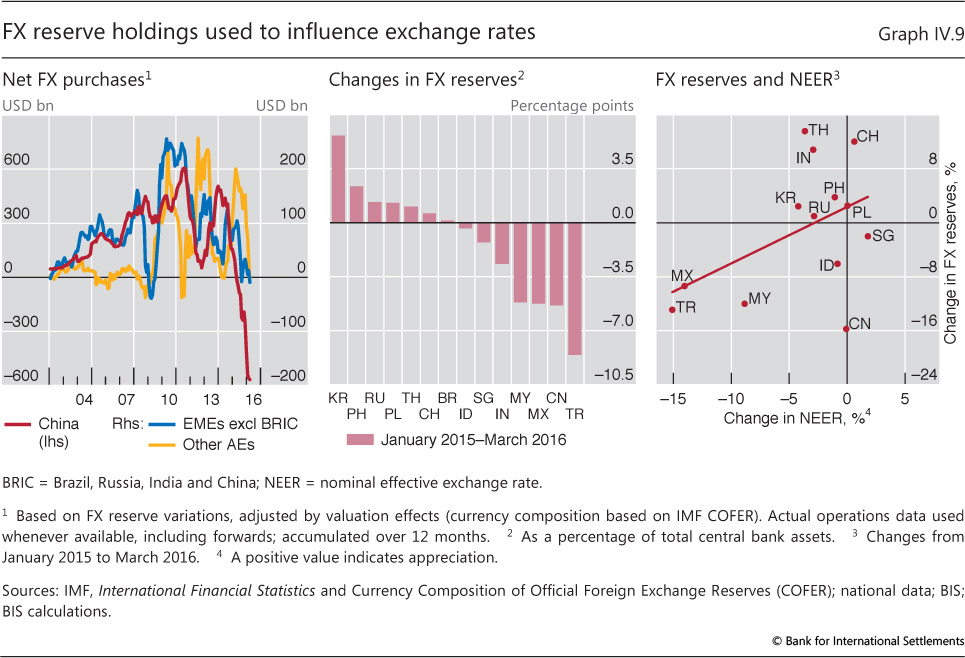

The de facto more prominent role of exchange rates, however, is not without problems. One country's currency depreciation is another's appreciation, and that appreciation may not be welcome. This is especially so in a world in which many central banks are facing inflation rates stubbornly below target and are seeking to boost demand and where some have been facing the build-up of financial imbalances. In this environment, central banks are becoming exposed to risks of large capital inflows, including in foreign currency (Chapter III). Hence, there has been a growing emphasis on foreign exchange intervention to stem appreciation pressures, including by countries that had been reluctant to do so in the past (Graph IV.9, left-hand and centre panels). The alternative or complement to such intervention has been easing monetary policy itself. Thus, easing in the large economies, home to international currencies, has induced easing elsewhere.2

As a result, the exchange rate has not only redistributed global demand, but has also affected the stance of monetary policy at the global level. This arguably has contributed to financial imbalances in those countries that have been experiencing financial booms, notably many EMEs (Chapter III). And as the monetary policy stance has begun to turn in the United States, commodity prices have plunged and domestic financial cycles have been maturing, the process has started to reverse. Thus, depreciation pressures over the past year have prompted many countries to run down reserves (Graph IV.9). Moreover, for countries with high levels of foreign currency debt, the hoped-for expansionary effects may not materialise (Chapter III).

All this suggests that limits apply to the effectiveness of the external channel, especially from a global perspective. Some of the limits simply reflect the fact that, as discussed before, the domestic measures that result in currency depreciation in the first place can be pushed only so far and have their own well known side effects. But others stem from the additional constraints created by the global interaction of national monetary policies. These are even harder to address, given the dynamics involved.

Monetary policy frameworks: integrating financial stability

Another year of exceptionally accommodative monetary policy has highlighted the tension between price stability and financial stability. In many countries, interest rates have been kept extraordinarily low in order to boost inflation. In some cases, this has occurred even as strong credit and asset price increases have raised concerns about the build-up of vulnerabilities. In other cases, concerns about the impact of low interest rates on the profitability and soundness of financial institutions have been more prominent (Chapter VI). All this has added fuel to the debate over whether existing monetary policy frameworks can adequately address the trade-offs, especially in the light of complications arising from exchange rate swings.

Factoring in domestic financial cycle considerations

The tensions between price stability and financial stability reflect in part the different policy horizons over which central banks aim to achieve their primary goals. Price stability typically focuses on inflation developments over a horizon of roughly two years or so. Financial stability risks develop over a much longer horizon, as systemic financial strains emerge only infrequently: the corresponding financial booms and busts last considerably longer than traditional business cycles. One lesson from the crisis is the need to look beyond short-term inflation stabilisation to ensure overall stability: low and stable inflation does not guarantee financial, and thus macroeconomic, stability.

At least two concerns have been holding back a more systematic incorporation of financial stability considerations into monetary policy. The first is that, even if monetary policy did try to incorporate them, doing so would not improve economic outcomes. The second is the lack of operational guides for implementing such a policy, beyond general indicators of the build-up of financial risks, such as those used in macroprudential frameworks. On balance, therefore, central banks have preferred to rely increasingly on macroprudential measures to address financial stability risks while keeping monetary policy firmly focused on short-term output and inflation objectives - a kind of separation principle.

The first concern has received particular attention over the past year. Additional research has found that a policy of "leaning against the wind" is unlikely to produce net benefits. In this work, a financial stability-oriented monetary policy is interpreted as one that focuses narrowly on pursuing traditional objectives most of the time: it deviates at the margin and temporarily only to avert a financial crisis when signs of financial imbalances emerge, such as unusually rapid credit growth. For a range of parameter values drawn from empirical studies, this research finds that leaning against the wind would be counterproductive in terms of deviations of output, unemployment and inflation from desirable levels.

Such research is very useful. At the same time, there are reasons for believing that it may underestimate the overall benefits of a financial stability-oriented monetary policy. Some of these reasons are of a more technical nature. The research typically assumes that the policy response does not affect the cost of crises, that these crises occur with a given frequency and that they do not result in permanent output losses - so that eventually output returns to its pre-crisis trend. These assumptions tend to reduce the costs of crises and limit the potential benefits of leaning against the wind. For example, the empirical evidence suggests that recessions that coincide with financial crises typically lead to permanent output losses and that growth rates may sometimes be persistently lower thereafter (Chapter V).

Other reasons have to do with the general interpretation of a financial stability-oriented monetary policy. It is indeed possible that if the policy amounts simply to responding to signs of financial imbalances at a somewhat advanced stage, it could end up doing too little too late. It could even be seen as precipitating the crisis it was supposed to avert. But a financial stability-oriented monetary policy is better interpreted as one that takes financial stability considerations into account all the time. In doing so, it would respond systematically to financial conditions to keep them on an even keel throughout the entire financial cycle. The idea is not to be too far away for too long from some notion of financial equilibrium.

Two strands of recent BIS research provide some support for this view. They share the view that financial developments are a core feature of economic fluctuations, whether these result in crises or not. The research considers the possible benefits of a financial stability-oriented monetary policy applied over the whole financial cycle. One strand highlights the analytical case for a leaning-against-the-wind monetary policy. It argues that persistent swings in financial booms and busts lend support to the case for leaning. Indeed, this research finds that in this context the question is not so much whether there are gains, but how large they are (Box IV.B).

The second strand, of a more empirical nature, estimates a small set of equations that describe the behaviour of the US economy, drawing on a more granular description of the financial cycle. It suggests that the implementation of such a systematic leaning strategy might have resulted in significant output gains (Box IV.C). Moreover, since, on average, economic slack is estimated to have been lower in this case, there appears to have been no necessary trade-off in terms of lower inflation. Any losses in the form of lower output and inflation in the short run are estimated to be more than offset in the longer run. And, intuitively, these estimates suggest that the earlier the policy is implemented, the larger are the gains.

Box IV.B

Analytical case for a "leaning against the wind" monetary policy

A growing body of research is employing numerical simulations to evaluate the benefits and costs of monetary policy leaning against the build-up of financial imbalances. The various approaches assess the benefits of leaning in terms of a reduction in the likelihood of a crisis, and in its magnitude; and they assess the costs in terms of lower output or higher unemployment in the leaning phase. The results are critically sensitive to three sets of factors: (i) the process driving the evolution of the likelihood of a crisis and its magnitude; (ii) the impact of a tighter monetary policy during the boom on the likelihood of a crisis and its magnitude; and (iii) how a policy easing affects output during the bust. This box discusses the sensitivity of cost-benefit assessments to the modelling approaches.

Clearly, as long as monetary policy cannot completely undo the costs of a crisis by "cleaning up" afterwards (ie point (iii) above) and it can reduce its probability or magnitude (ie point (ii) above), then leaning would produce some benefits. Intuitively, it would then pay to sacrifice at the margin a bit of output today to avoid possible future output losses. Thus, ignoring the potential role of other tools (eg prudential measures) and broader considerations, the question concerning optimal policies is less about whether to lean than about how much.

Some studies find that the net benefits of leaning are small or - in the case of a one-off policy tightening at some stage in the boom - even negative. Certain assumptions underpinning the calibration contribute to this conclusion, including the assumption that there is no permanent loss in output (Chapter V). But a key assumption involves the evolution of the likelihood of a crisis and its magnitude. Some models assume both that the magnitude of a crisis is independent of the size of the financial boom ahead of distress and that the crisis risk is not expected to grow over time. For instance, the typical variable used to track the evolution of the likelihood of a crisis is credit growth, which itself is naturally mean-reverting. These assumptions effectively imply that there is little or no cost to delaying to lean. And they encourage consideration of counterfactual experiments in which the authorities simply deviate temporarily from their policy rule to influence the variable of interest, here credit growth, with a short horizon.

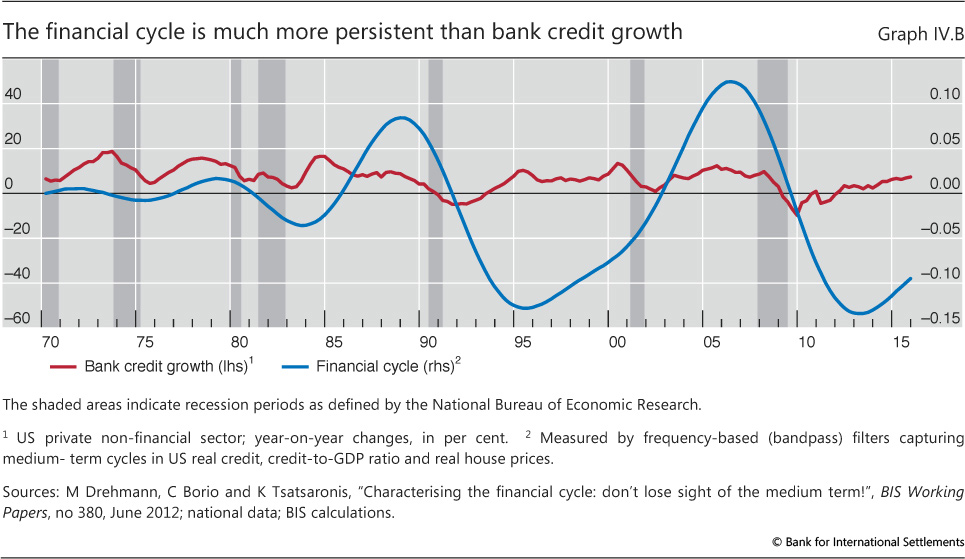

But the dynamics underlying crisis risks may be different. Credit growth has been found to be a good leading indicator, although by no means the only one. Other indicators put more emphasis on the gradual build-up of vulnerabilities; these are captured by the cumulative increases in debt stocks and, relatedly, in cumulative deviations of asset prices, especially property prices, from historical norms. In particular, cumulative deviations of the ratio of private sector credit to GDP or debt service ratios from such norms have been found to be especially important (see Box III.A and references therein). The idea of the financial cycle generalises these dynamics: it reflects prolonged credit and asset price booms followed by busts, with banking stress typically taking place close to the peak of the cycle. The contrast with the evolution of credit growth is obvious (Graph IV.B). The persistent nature of the stock variables highlights the importance of understanding crisis dynamics, and economic fluctuations more generally, through the lens of the cumulative process of the financial cycle.

although by no means the only one. Other indicators put more emphasis on the gradual build-up of vulnerabilities; these are captured by the cumulative increases in debt stocks and, relatedly, in cumulative deviations of asset prices, especially property prices, from historical norms. In particular, cumulative deviations of the ratio of private sector credit to GDP or debt service ratios from such norms have been found to be especially important (see Box III.A and references therein). The idea of the financial cycle generalises these dynamics: it reflects prolonged credit and asset price booms followed by busts, with banking stress typically taking place close to the peak of the cycle. The contrast with the evolution of credit growth is obvious (Graph IV.B). The persistent nature of the stock variables highlights the importance of understanding crisis dynamics, and economic fluctuations more generally, through the lens of the cumulative process of the financial cycle.

The policy implications are significant. If the evolution of financial stability risks is more akin to the financial cycle view, then failing to lean has a cost. In the absence of any action, the risks increase over time, and so do the costs if larger imbalances lead to larger busts. This puts a premium on early action and on a through-the-cycle, long-term perspective. Recent work has formalised this intuition. By calibrating a model to a stylised financial cycle, the benefits from leaning can increase considerably relative to those found in other approaches: it pays to lean early and systematically. This evidence is consistent with that based on a more granular financial cycle calibration (Box IV.C).

By calibrating a model to a stylised financial cycle, the benefits from leaning can increase considerably relative to those found in other approaches: it pays to lean early and systematically. This evidence is consistent with that based on a more granular financial cycle calibration (Box IV.C).

Obviously, the analysis here is a partial one and leaves out many considerations. These include credit growth associated with financial deepening and innovation; aspects of the uncertainty about the state of the economy and its behaviour; and the effectiveness of alternative instruments, notably prudential policies. In addition, it abstracts from the general equilibrium effects, especially important in small open economies, through which monetary policy can have an impact on exchange rates and capital flows and complicate a leaning strategy (see the main text). Nevertheless, the analysis sheds light on the importance of properly characterising crisis risks over time when assessing the costs and benefits of leaning against financial booms and busts. It thus sharpens the questions that need to be addressed both analytically and empirically.

Deviations of inflation from target may also be included. But since these studies do not consider the possibility of negative supply side shocks, there is no trade-off between stabilising output and inflation See eg L Svensson, "Cost-benefit analysis of leaning against the wind: are costs larger also with less effective macroprudential policy?", IMF Working Papers, no WP/16/3, January 2016; and A Ajello, T Laubach, D López-Salido and T Nakata, "Financial stability and optimal interest-rate policy", Board of Governors of the Federal Reserve System, mimeo, February 2015. M Schularick and A Taylor, "Credit booms gone bust: monetary policy, leverage cycles, and financial crises, 1870-2008", American Economic Review, vol 102, no 2, 2012, pp 1029-61. A Filardo and P Rungcharoenkitkul, "Quantitative case for leaning against the wind", BIS, mimeo, 2016.

The second strand of research also yields hints about possible measures of the financial cycle as policy guides. Two readily available financial measures are potential candidates (Box III.A): leverage as reflected in the ratio of private sector debt to assets (property prices and equities); and the debt service burden. Deviations of these measures from their long-run values help define in more practical terms the notion of financial equilibrium. For example, responding to the debt service ratio can play a role in improving macroeconomic outcomes above and beyond the traditional gauges of inflation and economic activity. Leaning early to prevent the debt service burden from getting too far out of line could foster more stable financial conditions; a late response, once the signs of financial imbalances are all too evident, could precipitate a bust and a costly recession.

The second strand of research also sheds light on the question of how to think about the natural, or equilibrium, interest rate. This is the concept to which policymakers sometimes appeal when assessing the appropriate policy stance. As commonly estimated, this rate draws heavily on the behaviour of inflation. All else equal, declines in inflation signal below-potential output and a policy rate above the natural rate.

The analysis has yielded a number of observations. First, once financial factors are taken into account, and given a build-up of financial imbalances, the estimates of natural rates are higher than commonly thought. This is because financial factors, better than inflation, provide useful information about cyclical fluctuations of output around potential. Before the financial crisis, for instance, inflation was low and stable, and it was the outsize financial boom that arguably pointed to output running consistently ahead of its potential.

A second observation is that, against this benchmark, the policy rate has been consistently below the estimated natural rate, both pre- and post-crisis. To the extent that they may have contributed to the costly financial boom and bust, low rates in the past can then be seen as one reason for even lower rates today. This finding underscores the concern about the potential easing bias in current frameworks. Moreover, had policy succeeded in mitigating the financial cycle, and therefore its costs, equilibrium rates could also be higher today.

Box IV.C

The financial cycle, the natural rate of interest and monetary policy

How should monetary policy respond to the financial cycle? This box highlights two key insights from recent BIS research. The first comes from supplementing the standard approach for estimating the natural interest rate by incorporating explicitly the influence of two financial cycle proxies: the leverage and debt service burdens of the business and household sectors (see Box III.A for details). Doing so yields what might be termed a finance-neutral natural rate. The second and related insight comes from a counterfactual experiment that assesses whether a monetary policy rule that responds systematically to the financial cycle can improve macroeconomic outcomes.

A finance-neutral natural rate

At the heart of the conventional approach is a natural rate of interest with two key characteristics. First, the natural rate is defined as that which would prevail when actual output equals potential output. Second, inflation is the key signal of unsustainability. All else equal, if output is above potential, inflation will tend to rise; if it is below, inflation will tend to fall. However, pre-crisis experience indicates that inflation may be low and stable even if output is moving along an unsustainable path because financial imbalances are growing. Hence, it may be misleading to rely heavily on inflation to estimate potential output and its difference from actual output (ie the output gap) - a common measure of economic slack (Chapter V). This, in turn, can generate distorted estimates of the natural rate.

The alternative approach makes only a small modification, adding the two financial-cycle proxies to estimate the (finance-neutral) output gap and natural rate simultaneously. It exploits the fact that the deviations of leverage and the debt service burden from their respective long-run (ie steady state) values have a sizeable influence on the evolution of expenditures and output and provide a measure of how far the economy is away from financial equilibrium.

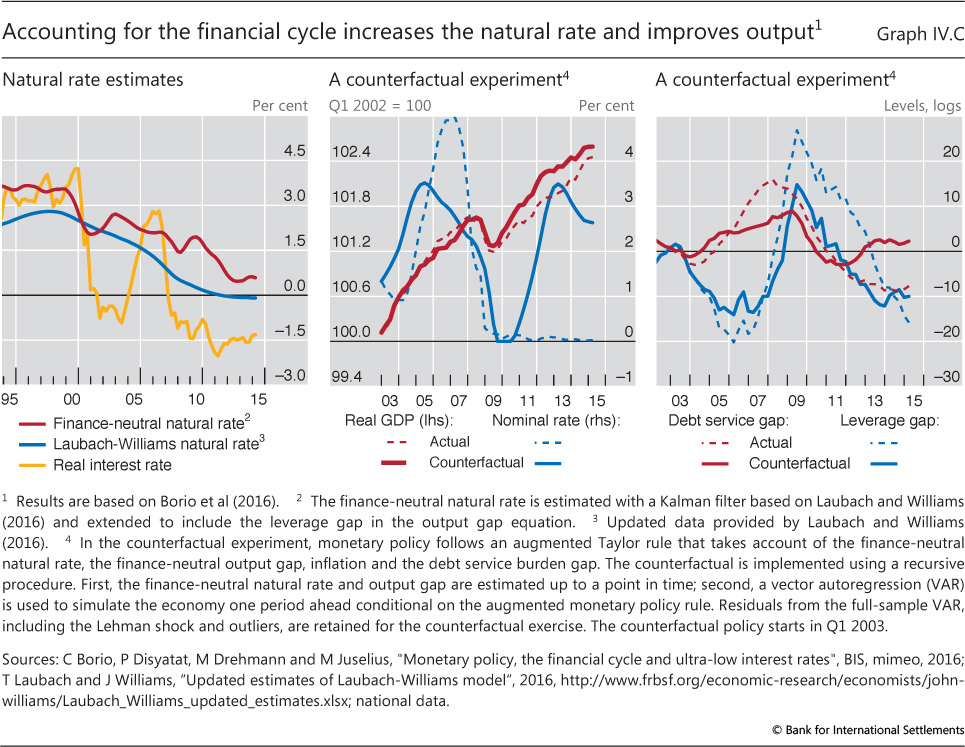

Finance-neutral estimates of the natural rate differ significantly from conventional ones. This is illustrated for the United States using quarterly data from 1985 to 2015. For example, the finance-neutral natural rate is currently positive and not below zero, in contrast to what the conventional approach indicates (Graph IV.C, left-hand panel). In line with the fall in trend output growth, the estimate of the finance-neutral natural rate has declined over time, but it has nearly always exceeded the conventional estimate, most notably by more than 1.5 percentage points post-crisis. Interestingly, since 2009, the policy rate adjusted for inflation has been consistently well below the finance-neutral natural rate.

Responding throughout the financial cycle

A monetary policy rule that responds systematically to the financial cycle draws on the previous estimates of the natural interest rate and output gap. It starts from a standard rule in which, given the estimate of the natural rate, the policy rate responds to deviations of inflation from target and to the output gap. The rule is then augmented to respond to a financial cycle proxy - the deviation of the debt service burden from its long-run equilibrium (ie the "debt service gap"). The counterfactual experiment relies on a broader econometric system that traces the dynamics of the economy (a vector autoregression - VAR).

The simulations suggest that a monetary policy which takes financial developments systematically into account at all times can dampen the financial cycle, leading to significant output gains (Graph IV.C, centre panel). According to the simulations, implementing the policy starting in 2003 could have resulted in output gains of roughly 1% per year, or 12% cumulatively. The medium-term gain exceeds the near-term cost during the leaning phase, which amounts to about 0.35% per year until 2007.

The counterfactual policy rate path indicates that policy leans early against the build-up of the imbalances and, as a result, gains considerable room for manoeuvre after the bust (centre panel). On average, the policy rate is 1 percentage point higher until mid-2005 as the debt service gap rises alongside credit and property prices. It then starts to decline, close to the property price peak, as the debt service burden begins to weigh more heavily on output. Such a policy dampens the financial boom as measured by the leverage and debt service gaps (right-hand panel). The benefits become fully apparent after the September 2008 Lehman shock (still included in the simulations). A smaller debt overhang results in a much shallower recession and allows policymakers to start normalising policy as early as 2011.

The counterfactual exercise also points to a smaller decline in the finance-neutral natural rate (not shown). This is around 40 basis points higher, on average, after the recession in 2009, suggesting that potential output growth is more resilient. This, in turn, supports policy normalisation.

In the exercise, the output gains come with little change in overall inflation performance, even though interest rates are generally higher than in the baseline. This is not too surprising. Confirming well known findings, economic activity has little traction on inflation in the estimation; and, importantly, output is on average higher and the output gap lower in the counterfactual. In fact, even though inflation is around 10 basis points lower in the early part of the counterfactual, it ends up around 25 basis points higher. This suggests that mitigating really bad outcomes could help with both output and inflation.

The gains are larger if one starts the counterfactual experiment further back in time, eg in 1996. An earlier implementation succeeds in better containing financial imbalances. In this case, output is cumulatively some 24% higher (1.2% per year).

This exercise carries a number of important caveats. The most critical one is that the estimated relationships are assumed to be invariant to the change in the policy rule. Even so, the analysis suggests that a monetary policy framework that responds systematically to the financial cycle has the potential to promote better output and, as a result, better inflation performance over the medium term.

C Borio, P Disyatat, M Drehmann and M Juselius, "Monetary policy, the financial cycle and ultra-low interest rates", BIS mimeo, June 2016. See eg M Woodford, Interest and prices, Princeton University Press, 2003. Technically, all estimation errors (residuals) are retained, including the large negative output residual around the Lehman crisis, which indicates that the VAR cannot fully account for the fall in output at that point. This also means that, by construction, this residual source of output variation cannot be smoothed out in the counterfactual exercise.

Finally, moving the economy closer to financial equilibrium may require the policy rate to deviate considerably from the natural rate in the short run - even the natural rate which incorporates the role of financial factors.

Clearly, any such research is subject to a number of caveats, and counterfactual exercises are fraught with serious difficulties. Even so, the results are consistent with the general proposition that a financial stability-oriented strategy means more than occasionally leaning against the wind. The costs and benefits of the strategy are best assessed over the course of the full financial cycle. And it suggests that policy choices at any given time can have important implications for financial developments both today and in the future, in turn significantly constraining future policy options (Chapter I).

Factoring in exchange rate considerations

Experience over the past several years has shown that risks to financial stability can originate both domestically and internationally. As an example, the unsustainable credit and asset price booms in past decades have been accompanied by waves of cross-border lending by both banks and non-banks (Chapter III). The impact of external influences has been felt especially by financially integrated small open economies. Such dynamics complicate financial stability-oriented monetary policymaking.

The potency of these international forces helps explain why central banks keep a close eye on global developments. Exchange rate flexibility can help promote financial stability, but only up to a point. On the one hand, flexibility may reduce incentives to stoke financial booms through one-sided exchange rate expectations, thereby helping insulate economies from international financial influences. On the other hand, prolonged unidirectional swings in the exchange rate are still possible. These, in turn, can fuel the build-up of financial imbalances, including by encouraging currency mismatches. A key mechanism operates through the greater willingness to provide foreign currency funding to domestic borrowers that have such mismatches: when these borrowers' foreign currency liabilities exceed their assets, a local currency appreciation improves their balance sheets (ie the risk-taking channel of the exchange rate) (Chapter III). These factors help explain why central banks are reluctant to see large deviations of their policy rates from those that prevail in key international currencies, most notably the US dollar.

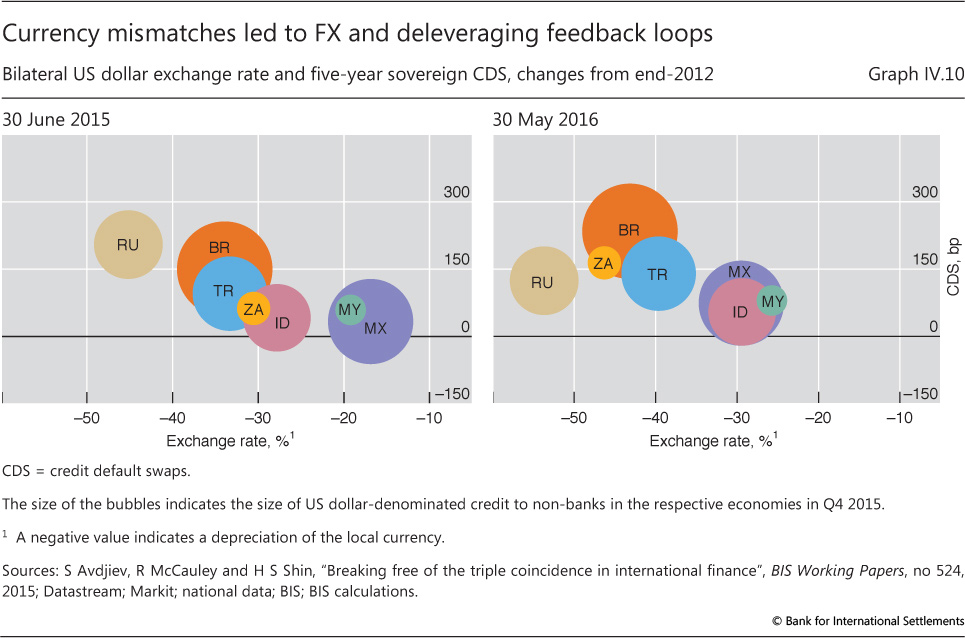

Of course, when external financial conditions reverse, in response to either global developments or a turn in domestic financial cycles, they can create serious economic strains. The currency depreciates, foreign currency debt burdens rise and spreads soar (Graph IV.10).

The previous discussion suggests that the influence of central banks whose currencies are used extensively abroad (ie international currencies) extends well beyond national borders.3 This is not only because the rest of the world can borrow heavily in those currencies, but also because even financial asset prices denominated in domestic currencies are especially sensitive to conditions in the core currency economies. If business cycles are well synchronised, such influences may not be a major concern. This is also true for financial cycles. However, when they are out of synch, the concerns become more significant, especially if monetary policies in core currency economies diverge significantly from each other and from those elsewhere.

This raises tough challenges for small open economies seeking to pursue a financial stability-oriented monetary policy. The concern is that a tightening of monetary policy designed to rein in a financial boom may be partly offset by the induced portfolio adjustments and foreign currency borrowing, thereby leading to an unwelcome exchange rate appreciation and further foreign currency borrowing. The ample global liquidity that has prevailed in recent years heightens such risks. Moreover, the appreciation would also reduce inflation, at least temporarily, exacerbating the trade-off with price stability whenever inflation fell below objectives.

There are at least a couple of ways in which this trade-off may be addressed. One is to lean against the currency appreciation through foreign exchange intervention. This strategy has been used extensively in the past. It also has a favourable by-product - the accumulation of foreign exchange reserve buffers. The buffers would come in handy once the tide reverses. However, the historical record on the ability of intervention to rein in an appreciation is not clear-cut. And, at times, uncomfortably large interventions may be necessary.

A second strategy is to rely more on other policies in order to lighten the burden on monetary policy. Prudential, and in particular macroprudential, policies are essential in this context. Many countries have chosen this approach. Another possibility, hardly explored in practice, is to enlist the support of fiscal policy (Chapter V). As a last resort, one might also envisage temporary and careful use of capital flow management measures, as long as the imbalances do not reflect fundamental domestic disequilibria.

In all these strategies, it is important to avoid unbalanced policies that pull in opposite directions. An obvious example is easing monetary policy with an eye to currency appreciation while tightening macroprudential measures. This mix might send conflicting signals about policymakers' intentions. Experience suggests that these tools work best when used as complements rather than substitutes (see the 84th Annual Report).

The additional difficulties that arise in pursuing a financial stability-oriented monetary policy in small open economies raise broader questions about the design of the international monetary and financial system. As discussed in Chapter V of last year's Annual Report, there is a need to establish adequate anchors for the system as a whole. For monetary policy, this means a number of options with increasing degrees of ambition. One is enlightened self-interest, based on a thorough exchange of information. For example, when setting domestic policies, countries would individually seek to take spillovers and spillbacks more systematically into account; large jurisdictions that are home to international currencies have a special responsibility. Going one step further (and beyond the coordination seen during crises), cooperation could extend to occasional joint decisions on both interest rates and foreign exchange intervention. The third, and most ambitious, possibility would be to develop and implement new global rules of the game that would help instil greater discipline in national policies.

1 ING, "Negative rates, negative reactions", ING Economic and Financial Analysis, 2016.

2 See M Carney, "Redeeming an unforgiving world", speech at the 8th Annual IIF-G20 Conference, Shanghai, China, February 2016; and R Rajan, "Towards rules of the monetary game", speech at the IMF/Government of India Conference, New Delhi, India, March 2016.

3 For an in-depth discussion, see the 85th Annual Report, Chapter V.