The evolution of central banks' lending operations: insights from the Markets Committee Compendium

Central banks' monetary policy operational frameworks have evolved in response to pandemic-era interventions, the resurgence of inflation and changes in market structure. The transition to smaller balance sheets, coupled with the growing footprint of non-bank financial institutions, is having a material impact on liquidity demand. Against this backdrop, central banks have begun recalibrating their lending operations, which comprise lending facilities and open market operations that extend funds to private sector borrowers on a collateralised basis. Drawing insights from the updated Markets Committee Compendium, this article examines the key design features and trade-offs related to the counterparty access policies, the collateral framework, pricing and disclosure practices of lending operations.1

JEL classification: E41, E42, E52, E58.

Central bank operational frameworks are mechanisms and tools designed to align the operational target with the desired policy stance. At their core, these frameworks manage the supply of reserves to meet demand at the desired policy rate. As some major central banks reduce their balance sheet size, effective liquidity tools have become even more crucial in meeting demand for reserves and curbing excessive volatility in money markets. In addition, the growing footprint of non-bank financial institutions (NBFIs) has placed new demands on central banks' frameworks. Central banks have thus begun to re-examine the design of their liquidity toolkit.

Against this backdrop, the Markets Committee2 has updated the Compendium of monetary policy frameworks and central bank market operations. With data as of end-2025, the Compendium provides new insights about the design of central banks' lending operations (Box A), including counterparty access, collateral frameworks, pricing methods and disclosure practices.3 A key Compendium feature is a classification of lending operations by function, which refers to the policy objective: monetary policy implementation and transmission, financial stability or payments system support. This classification helps to compare lending operations rigorously across central banks.

Key takeaways

- The updated Markets Committee Compendium, with new information about counterparty access and collateral frameworks, provides valuable insights about the "nuts and bolts" of operational frameworks.

- The transition to regimes with less abundant reserves involved a recalibration of central banks' liquidity toolkit to encourage use whenever economically sensible.

- Central banks have taken different approaches to expanding liquidity access to non-bank financial institutions (NBFIs) and in collateral frameworks. Central banks balance the ability to provide liquidity with risk and cost considerations.

This article explores central banks' lending operations, which involve tools to extend funds to private sector entities for a fixed period and on a collateralised basis. These include lending facilities and certain open market operations (OMOs),4 differing in terms of availability and who initiates use. Standing lending facilities are available on any business day, with usage initiated by the counterparty, while discretionary lending facilities are available in periods set by the central bank, typically in response to market stress; once activated, drawings are initiated by the counterparty. Repurchase agreements, a type of OMO in which the central bank provides reserves against collateral, are initiated by the central bank on a recurring or ad hoc basis.

The Compendium highlights that central banks share common objectives for lending operations, but the number and type of operations employed vary significantly.5 In terms of their design features, banks are almost universally eligible as counterparties, while access for NBFIs is more limited and varies by jurisdiction and type. Most jurisdictions accept domestic government bonds as collateral, but acceptance of private sector or foreign issued collateral is jurisdiction-specific and depends on the operation's function.

The Compendium also highlights how central banks balance trade-offs in designing lending operations. For counterparty access policies, they aim to provide sufficient liquidity to the financial system without taking on excessive credit risk with NBFIs. Similarly, accepting a broad range of collateral types eases liquidity provision, but with potentially greater operational costs and risks to central bank balance sheets. In setting prices, central banks want to ensure liquidity is drawn when needed without encouraging excessive reliance on the central bank (eg the central bank becoming a substitute for market funding).

The next section examines the recent evolution in central bank operational frameworks and the recalibration of lending operations. The following section highlights new elements in the updated Markets Committee Compendium, covering specific design features of lending operations and the key policy considerations that underpin those choices. The final section concludes. A box provides a primer on the Compendium database.

Operational frameworks amidst cyclical and structural shifts

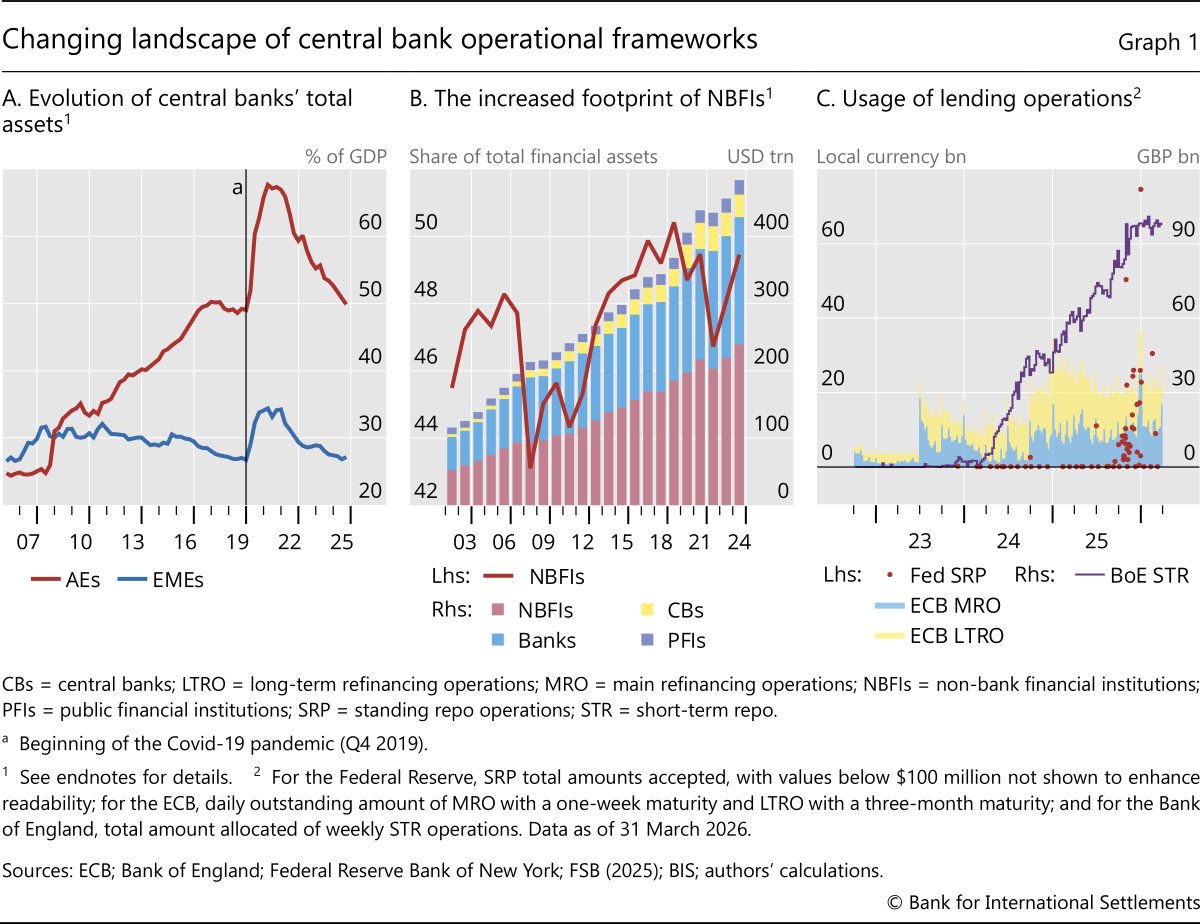

Central banks' operational frameworks have evolved significantly over the past two decades. Those in major advanced economies (AEs) that engaged in asset purchase programmes and long-term lending programmes following the Great Financial Crisis (GFC) and the Covid-19 pandemic (Graph 1.A) saw balance sheet expansions and a significant increase in the level of central bank reserves.6 Those in some emerging market economies (EMEs) grew their balance sheets by accumulating foreign exchange reserves, although asset purchases also contributed. Overall, however, EME central bank balance sheets grew by far less than those of their AE counterparts, with the majority continuing to operate with scarce reserves.7

After peaking during the Covid-19 pandemic, many AE central banks have been shrinking their balance sheets by unwinding unconventional policy measures. When a central bank seeks to maintain a low opportunity cost for banks to hold reserves while simultaneously shrinking its balance sheet, it must be prepared to buffer variations in reserve demand to avoid volatility in money market rates (Cavallino et al (2025)). This in turn requires lending operations that enable the level of reserves to adjust in response to fluctuations in demand.

In addition to these cyclical changes, macro-financial structural changes – most notably the growing footprint of NBFIs (Graph 1.B) – have implications for the effectiveness of liquidity provision tools. While NBFIs may improve market resilience by diversifying the pool of market participants, the inherent flightiness of certain NBFIs may exacerbate volatility in particular money market segments and undermine market liquidity during periods of stress, as observed during the March 2020 market turmoil.

Against this backdrop, many central banks have been recalibrating their liquidity tools to encourage use by eligible counterparties – when economically sensible for liquidity management, and to adapt to structural shifts in the financial system. For instance, the Federal Reserve removed the aggregate operational limit for its standing repo operations in 2025, and the European Central Bank (ECB) reduced the spread between the interest rate on the main refinancing operations (MRO) and its deposit facility. In 2022, the Bank of England introduced the short-term repo (STR) facility to keep short-term market interest rates aligned with the policy rate as reserves declined. Subsequently, in 2025, it increased the reserves available at indexed long-term repo (ILTR) operation auctions at fixed minimum spreads (Bank of England (2025)). Importantly, to promote use, the UK Prudential Regulatory Authority (PRA) affirmed that it would view use of both the STR and ILTR tools as routine sterling liquidity management. The Bank of England also recalibrated their bilateral facilities – the usage of which the PRA also supports. Additionally, the Bank of England introduced the contingent NBFI repo facility (CNRF),8 enabling eligible pension funds, insurers and investment funds to borrow cash during periods of market-wide disruption that temporarily increase NBFIs' demand for liquidity, and where that demand is outside the reach of the Bank's routine liquidity facilities. Uptake patterns have started to reflect these developments, with usage increasing since late 2023 (Saporta (2024); Perli (2025); Iskaki et al (2026)) (Graph 1.C).

Lending facilities and open market operations

The updated Compendium characterises OMOs and lending facilities by their function for the first time, along with details about its pricing methodology, collateral framework and the range of market participants that have access.

A bird's eye view across jurisdictions

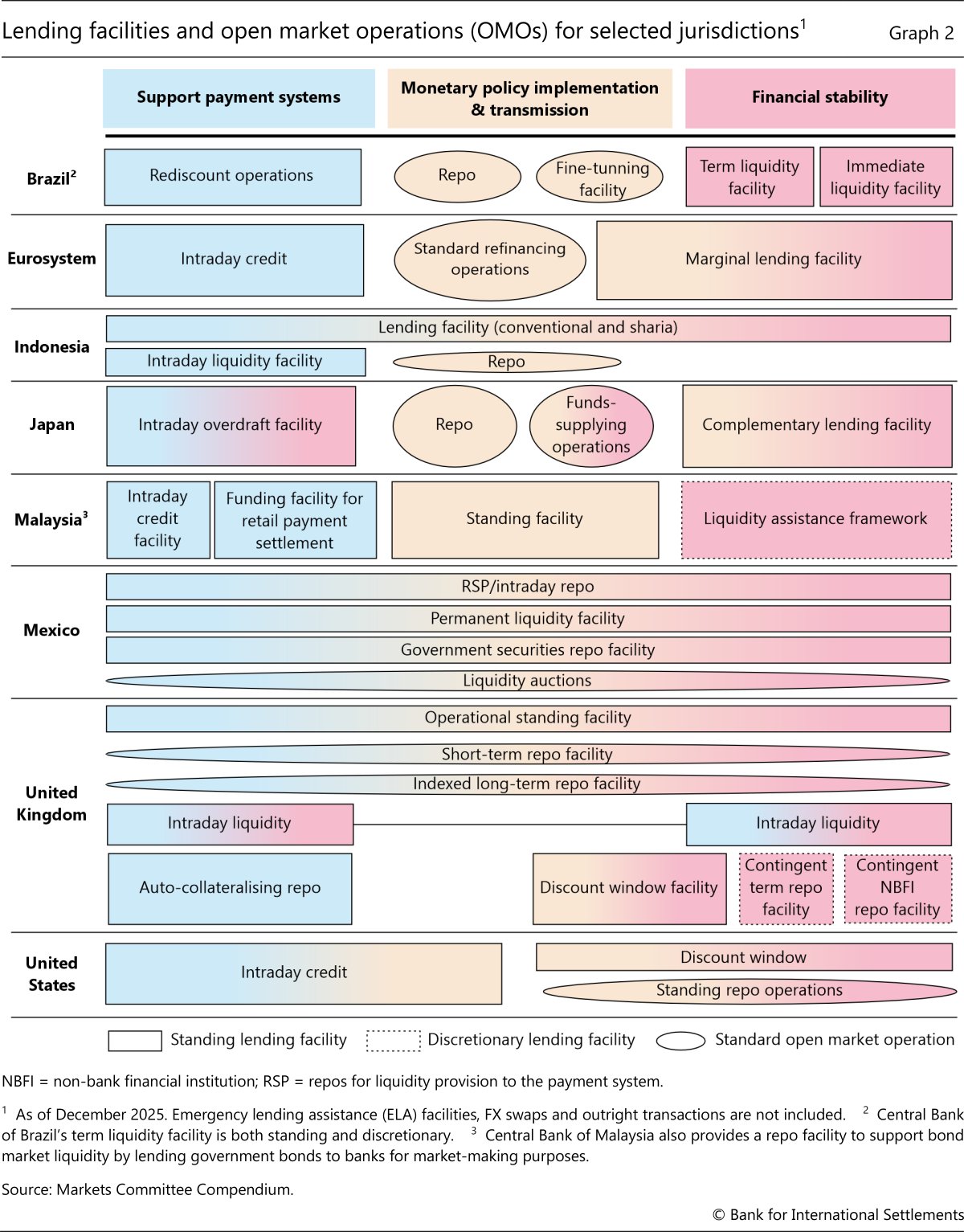

OMOs and lending facilities have three broad functions: to implement monetary policy, to promote financial stability and to support payment systems (Graph 2). In the context of monetary policy implementation, these tools serve to control short-term interest rates, manage reserves and transmit policy decisions by influencing market conditions and signalling the central bank's policy stance. For financial stability objectives, they contribute to stabilising market conditions and addressing liquidity pressures, thereby limiting systemic risks. And for payments systems, they underpin smooth functioning by providing participants with access to central bank liquidity, addressing timing mismatches in payments and avoiding disruptions.

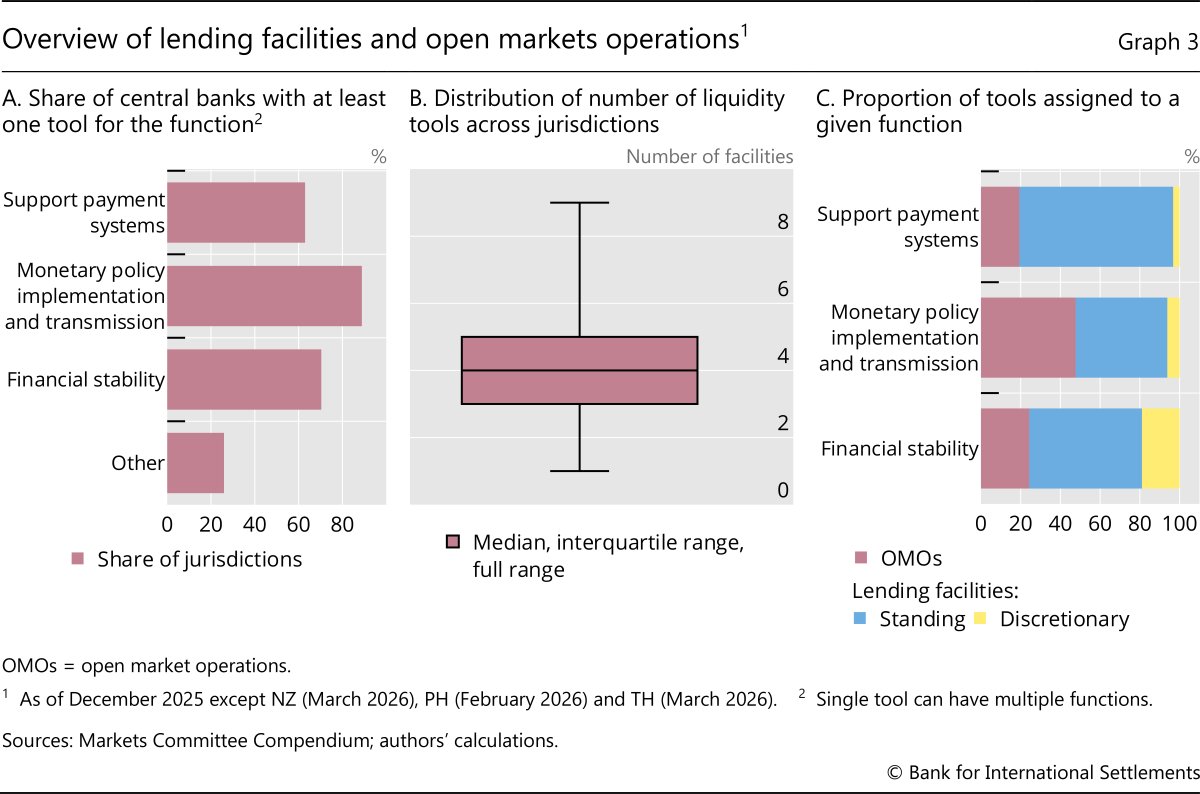

Although central banks share common objectives (Graph 2), they use a different mix of OMOs (ovals) and facilities (rectangles) to achieve these objectives. The most visible difference across central banks is in the number of tools, which varies from one to nine (average of four) (Graphs 2 and 3.B). Some central banks – eg the Bank of England and the Central Bank of Brazil – use a relatively large number of instruments, many with a specific purpose. Others – eg the Federal Reserve, ECB, Bank of Mexico and Bank Indonesia – have a streamlined framework with fewer tools that serve multiple objectives.

For a given policy objective, the choice of the tool, or combination of tools, reflects domestic legal and market structural factors, experience with past episodes of market stress and/or the central bank's assessment of the effectiveness and costs of the toolkit (Arseneau et al (2025)). Most central banks allocate at least one tool for monetary policy implementation (Graph 3.A); most combine OMOs and lending facilities (see Graph 3.C). By contrast, some do not have an explicit tool to support payment systems functioning or to promote financial stability.9 For the former, standing lending facilities dominate, while for the latter both standing and discretionary facilities are important.

Central banks face trade-offs in choosing the number and function of the OMOs and lending facilities in their toolkit. A greater number may enable a central bank to differentiate eligible counterparties and collateral, and tailor pricing and tenor, for each policy objective.10 At the same time, it requires more resources to operationalise, both for the central bank and its counterparties. A complex framework can also be opaque and disproportionately benefit the more sophisticated market participants (Bindseil (2016)). Discretionary facilities help manage the trade-off between flexibility and complexity as the central bank can respond to specific types of stress by activating the facility on a temporary basis.11 Alternatively, central banks can maintain a small number of facilities, but adjust the modalities (lower pricing, broader collateral) depending on the circumstances.

Counterparty access

The structure of the financial sector, the breadth of financial intermediaries' business models and their regulatory treatment, and the type of liquidity tool all determine how central banks determine the mix of eligible counterparty types.

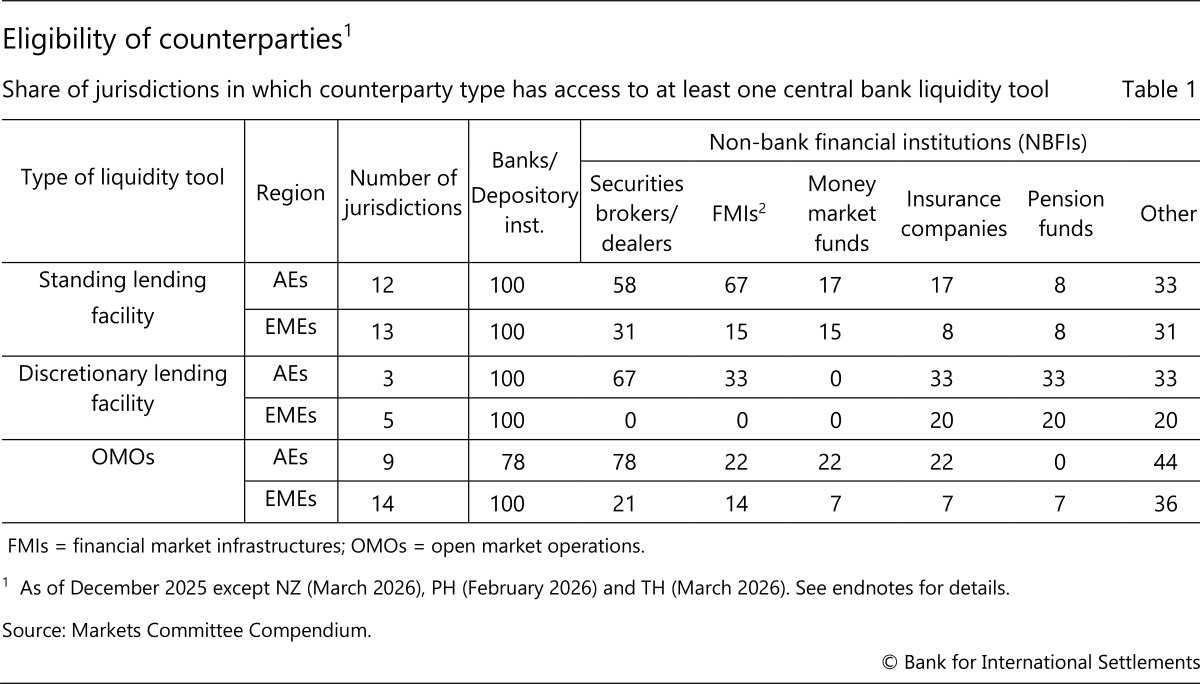

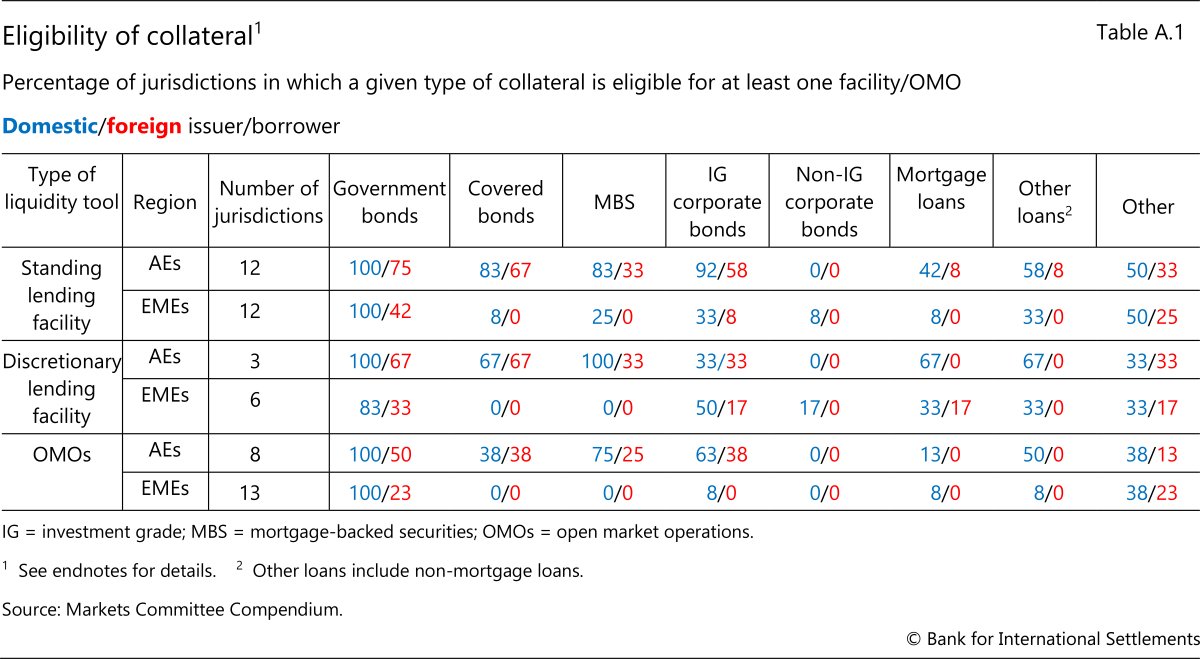

Banks, which play a pivotal role in financial intermediation, monetary policy transmission and maturity transformation, are eligible counterparties in virtually all jurisdictions (Table 1). Moreover, they are eligible not only for standing lending facilities but also for discretionary facilities and OMOs.

Further reading

For NBFIs, eligibility across central banks depends on the entity type and the liquidity tool. For example, securities brokers/dealers are eligible at a majority of AE central banks, again with relatively broad access to the different liquidity tools. This reflects their outsized role as intermediaries in money markets. Financial market infrastructures (FMIs), such as central clearing counterparties and payments platforms, are also eligible in a majority of AEs, predominantly at standing facilities, given their central role for the functioning of the financial system. For both types of counterparties, eligibility is much more restricted at EME central banks.12 In both AEs and EMEs, other NBFIs (eg insurance companies, money market funds (MMFs) or investment funds) are far less commonly eligible for lending operations.

This heterogeneity of NBFI eligibility in part reflects jurisdiction- and market-specific factors. At a few central banks (eg Swiss National Bank), insurance companies, MMFs and investment/pension funds have access to OMOs and standing facilities if they meet regulatory criteria and are deemed important for liquidity in the money market. Conversely, some central banks (eg Bank of England, drawing lessons from the March 2020 and September 2022 gilt turmoil episodes; Bank of Canada, during the Covid-19 pandemic) have granted those regulated NBFIs with a prominent role in core markets access to discretionary facilities during periods of financial stress.13 Finally, NBFI access can also be indirect. The Federal Reserve's money market mutual fund liquidity facility was activated during the subprime crisis and the Covid-19 pandemic to alleviate redemption pressures. Eligible banks and dealers received non-recourse loans from the Federal Reserve to purchase high-quality assets from MMFs, which they pledged as collateral.

More generally, access policies for NBFIs to the central banks' liquidity tools can reflect how much a central bank is willing to incur market or credit risk in their operations. Central banks with a broad access policy can allocate liquidity directly to counterparties experiencing liquidity strains, reducing the risk of fire sales. However, doing so exposes the central bank to the credit risk of counterparties that are often more lightly regulated than banks. Asset purchases by the central bank can be targeted to specific market segments, but they expose the central bank to market risk.14

The trade-offs around access may become more acute as NBFIs' role in financial intermediation continues to expand. While central banks' liquidity support can be stabilising, it can also incentivise NBFIs to take on funding and leverage risk. A potential remedy is to condition NBFIs' access on proportionate regulation of maturity mismatches and leverage (Aramonte et al (2022); Garcia Pascual et al (2025)).

Collateral frameworks

The breadth of the central bank's collateral framework – ie the range of assets a central bank is willing to accept in exchange for liquidity – has a direct bearing on the potential amount of liquidity support it can provide. The framework can also influence market functioning by affecting the availability or scarcity of certain types of collateral. Finally, it shapes both the risks that the central bank faces and the costs associated with valuing, transferring and legally securing collateral.

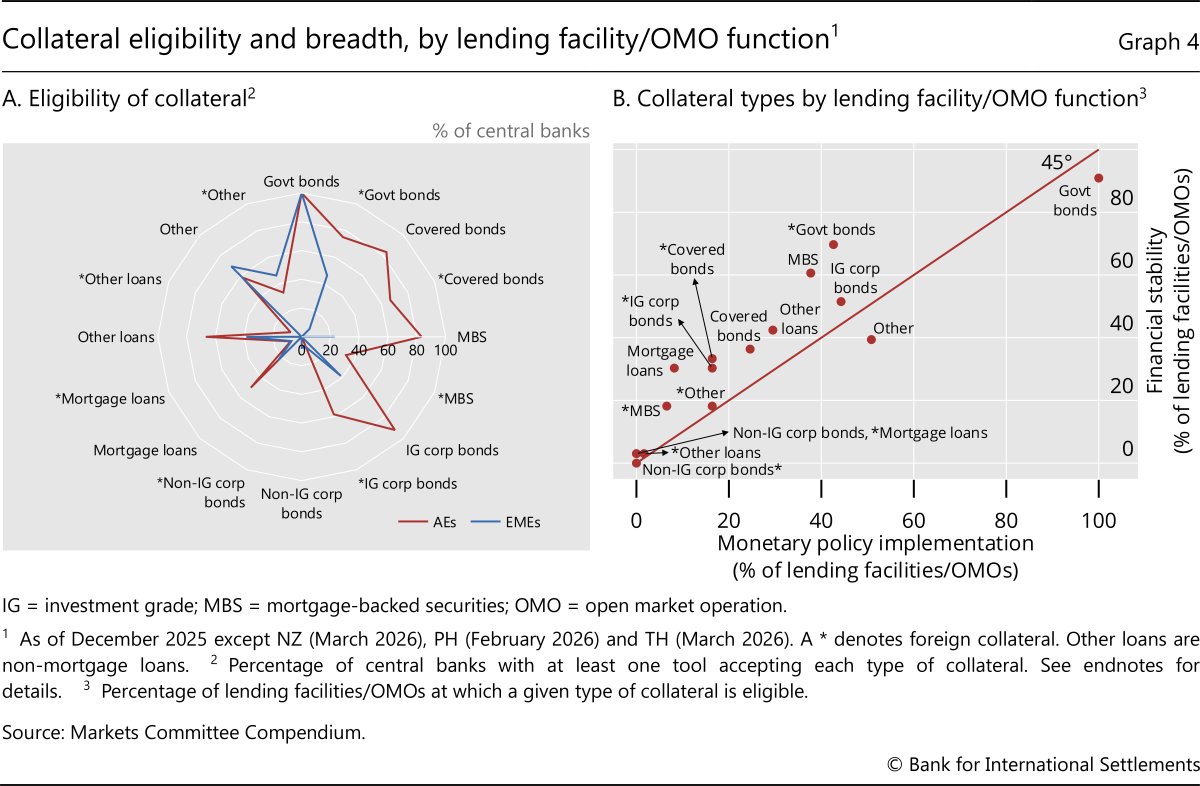

All central banks accept domestic government bonds as collateral in at least one tool, but they differ greatly in their acceptance of privately or foreign issued assets (Graph 4.A). AE central banks tend to have broader collateral frameworks; most accept investment grade corporate bonds, mortgage-backed securities, covered bonds and other loans, and about half accept mortgage loans, with loans typically being eligible at financial stability-related facilities (see below). By contrast, EME central banks accept a much narrower range of private sector assets and are also less inclined to accept collateral where the debtor is a non-resident entity.

A closer look at loan collateral reveals other significant differences. Mortgage loans are less often eligible than non-mortgage loans, despite the former typically being safer and more standardised. This is because it is challenging in some jurisdictions to secure legal rights over real estate. To address this, the Swiss National Bank, for instance, accepts mortgages with legal and operational safeguards, transferring them to a fiduciary account at an independent FMI. By contrast, the ECB accepts mortgage loans in its permanent collateral framework if they are securitised as covered bonds or as mortgage-backed securities.

For some collateral types, the cross-border dimension increases the complexity and risk involved. Most AE central banks accept bonds issued by foreign entities, but loans to foreign borrowers are typically not eligible for several reasons. First, cross-border enforcement of claims can be cumbersome. Second, ring-fencing can be a barrier as loans, unlike bonds, often remain on a bank's balance sheet when pledged as collateral. Third, if a bank lends to a foreign borrower via a branch or subsidiary, the home central bank may view the loan as primarily eligible at the host central bank.

The breadth of eligible collateral in part depends on the function of the lending facility/OMOs (Graph 4.B). For tools that support monetary policy implementation, collateral is often restricted to core, liquid instruments (notably government bonds), which reduces operational costs. By contrast, tools that promote financial stability typically allow a broader collateral range, with the most notable difference being the eligibility of loans.15 This broader set of eligible assets allows the central bank to rapidly scale up its liquidity provision in stress periods. Still, some central banks (eg ECB) have a broad collateral range (including non-mortgage loans) for both functions. One motivation is to accommodate the liquidity needs of banks with different business models.

Choosing an appropriate breadth for collateral involves trade-offs.16 A broad framework may be more market neutral, as it does not privilege specific asset types or business models. Moreover, broader eligibility increases a central bank's capacity to meet counterparties' liquidity needs (Choi et al (2021)). Finally, it can provide stronger support for market functioning: when a central bank accepts less liquid or non-marketable collateral, marketable collateral remains available for market-based secured funding and derivative transactions.

At the same time, a broad collateral framework may have drawbacks. For one, it may be more burdensome to operate, because the central bank and its counterparties must establish processes for valuing the collateral and ensuring its operational and legal transferability (Chailloux et al (2008); Buessing-Loercks et al (2020)). For another, a broad framework that eases access to liquidity support may incentivise market participants to take on more liquidity risk. Similarly, looser requirements on collateral credit quality may prompt banks to weaken their lending standards (Nyborg (2017)). Finally, the central bank may be exposed to adverse selection, ie market participants post riskier collateral at its facilities, saving the safer collateral for use in the market (Chailloux et al (2008)). Haircuts can mitigate these risks.

Over time, central banks have expanded collateral eligibility to reflect developments in financial markets, with the most notable changes occurring during stress episodes (CGFS and Markets Committee (2015); Buessing-Loercks et al (2020)). New types of instruments have become eligible, particularly during the GFC (eg asset-backed securities, commercial paper, credit claims). In addition, credit quality requirements have been lowered. As a specific example, the ECB expanded its temporary collateral framework during the euro area sovereign debt crisis and the Covid-19 pandemic (but later transitioned back to its permanent framework). Some temporary measures that proved effective, such as the eligibility of bonds in the main foreign currencies, were permanently integrated in 2024 (Gomes et al (2025)).

Apart from eligibility, operational readiness – ie the ability of the central bank and its counterparties to mobilise eligible collateral – has gained attention in recent years. Insufficient preparation at Credit Suisse, as well as at several US regional banks, exacerbated the 2023 banking turmoil (Coelho et al (2024)). Readiness is essential for ensuring that liquidity support can be executed in a timely manner and that the full breadth of the collateral framework can be utilised. Some central banks encourage banks (eg Bank of England) or even require them (eg Swiss National Bank for its liquidity-shortage financing facility) to preposition collateral. Regular testing of the collateral process also helps ensure preparedness (Coelho et al (2024)). For internationally active banks, operational readiness is also important for obtaining foreign currency liquidity support from the central banks in their host jurisdictions (CGFS (2026)).

Pricing

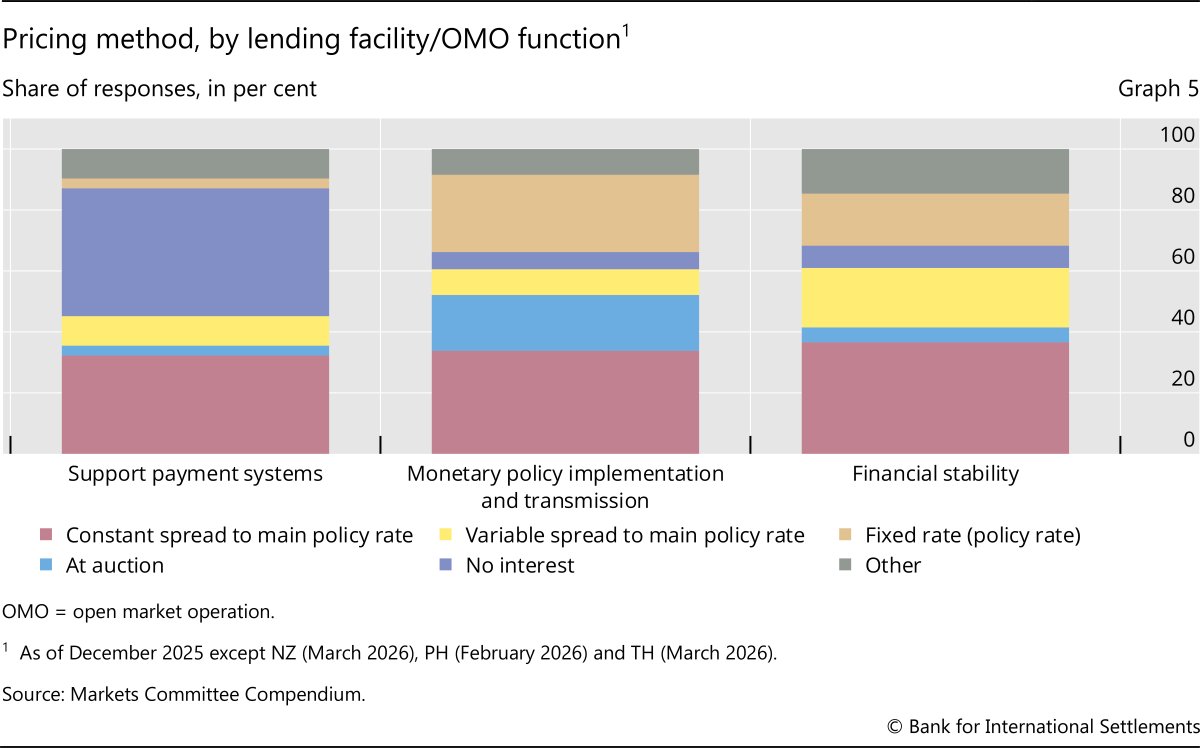

When setting prices, central banks balance market discipline considerations against the need to ensure that liquidity is actually drawn when needed.17 Pricing above policy or market rates helps maintain market discipline and prudent liquidity management. However, excessively high rates can deter usage even in periods of stress, potentially undermining the effectiveness of liquidity provision. For financial stability facilities, central banks can address this trade-off by setting the lending spread above the policy rate but below market rates during periods of stress.

Central banks price facilities according to their function. Those for monetary policy implementation are typically priced at the policy rate or with a fixed spread to it (Graph 5).18 For those that support financial stability, the spread is usually higher. Facilities that support payments systems are more usually free of charge, in line with the typically very short maturity (mostly intraday).

Recent pricing adjustments by a number of central banks illustrate the trade-off. In 2020, during the Covid-19 pandemic, the Federal Reserve reduced the discount window primary credit rate and set it at the top of the federal funds target range to encourage borrowing and support liquidity. The Federal Reserve has maintained this pricing policy since then, emphasising that it views the use of the discount window as appropriate under both normal and stressed market conditions. In 2026, the Bank of England also lowered the discount window spreads to enhance its accessibility as a liquidity tool. At the same time, it maintained tiered pricing based on collateral quality to preserve incentives for sound liquidity management.

Disclosure practices

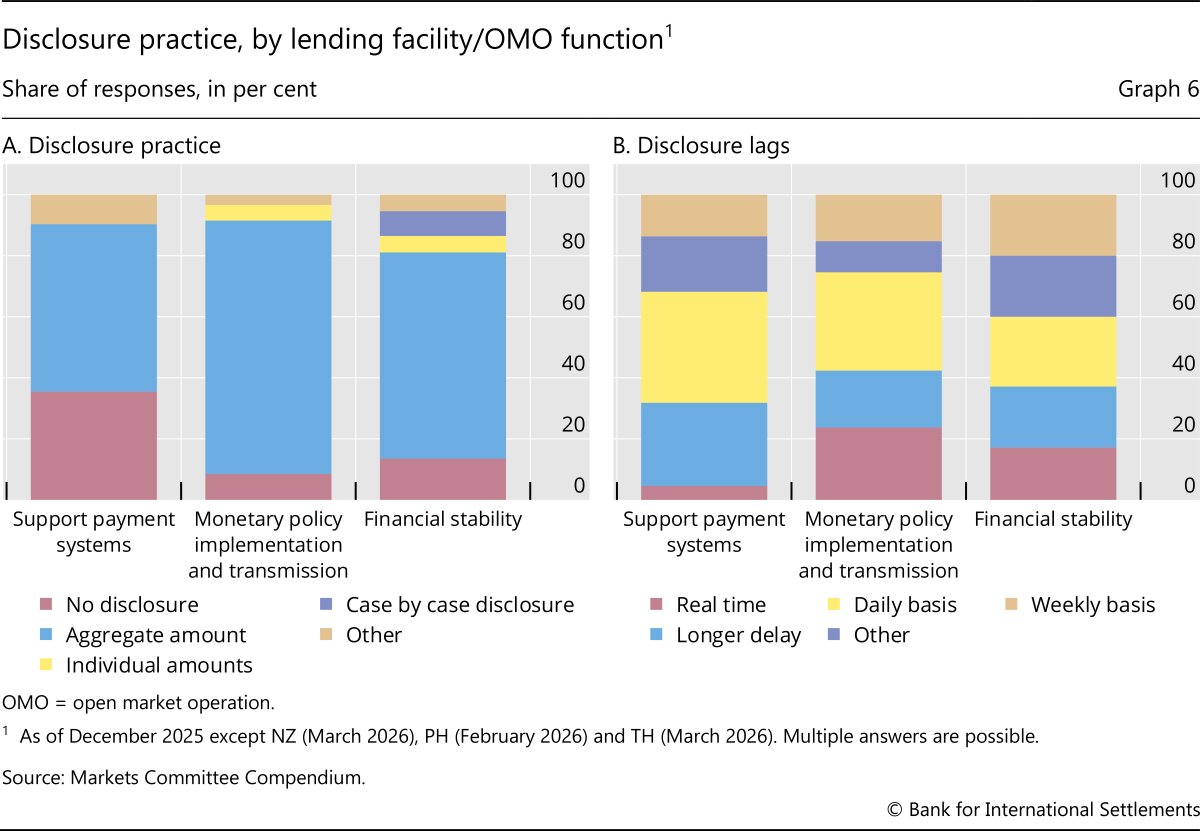

In disclosing information about the frequency and scale of usage of lending facilities and OMOs, central banks must balance transparency and accountability with operational effectiveness and market stability. While transparency is essential for public accountability, disclosures that directly or indirectly reveal liquidity support to individual entities can create stigma and discourage usage in episodes of stress and may thus undermine the effectiveness of the liquidity provision framework.

Overall, central banks' preferred disclosure practice is to report aggregate usage (Graph 6). Only a few disclose the names of counterparties. While aggregate disclosure can mitigate stigma concerns, large-scale use by a single counterparty may be visible in published data or could reasonably be inferred (Lee and Sarkar (2018)). During the Covid-19 pandemic, the Federal Reserve reduced the granularity of weekly disclosures for each of the Federal Reserve banks to balance reporting transparency requirements with protecting borrower confidentiality. Discount window lending is now included with a broader balance sheet item, which reduces but does not eliminate the possibility of inferring borrowing by a larger bank.19 Another possibility is to disclose aggregate figures for financial stability facilities with a longer lag. For example, the Bank of England reports aggregated data for its discount window facility with a five-quarter lag.

Conclusion

The updated Markets Committee Compendium provides valuable insights into the design and functioning of central banks' lending operations across jurisdictions. By categorising operations by type and function, the Compendium enables a nuanced understanding of how central banks navigate trade-offs in areas such as counterparty access, collateral frameworks, pricing and disclosure practices.

As central banks reduce their balance sheet sizes, lending operations play a bigger role again in ensuring desired monetary conditions. Accordingly, central banks are recalibrating their lending operations to encourage use when economically sensible. With NBFIs' growing footprint, some central banks are also reviewing their access policies and the breadth of their collateral frameworks, to enhance their liquidity provision capacity in times of stress.

While these adjustments contribute to financial market resilience, there are trade-offs. Central banks must ensure that broader collateral policies and more attractive pricing do not undermine market discipline or encourage excessive reliance on the central bank. Moreover, they must balance the benefits of broader counterparty and collateral eligibility against the increased operational complexity and risks to their own balance sheets. Adequate regulatory safeguards are essential to promote prudent liquidity risk management among banks and NBFIs. Regular testing or collateral prepositioning are effective means to ensure operational readiness, enabling operations involving a broad range of collateral and counterparties to be conducted safely and efficiently.

Looking ahead, the effectiveness of central bank lending operations will depend on their ability to adapt flexibly to both cyclical and structural changes. The insights from the Compendium serve as a valuable resource for policymakers and market participants alike, fostering a deeper understanding of the mechanisms that underpin monetary policy implementation and global financial stability.

References

Aramonte, S, A Schrimpf and H S Shin (2022): "Non-bank financial intermediaries and financial stability", BIS Working Papers, no 972.

Arseneau, D, M Carlson, K Chen, M Darst, D Kirkeeng, E Klee, M Malloy, B Malin, E O'Malley, F Niepmann, M-F Styczynski, M Vanouse, and A Vardoulakis (2025): "Central bank liquidity facilities around the world", FEDS Notes, Board of Governors of the Federal Reserve System.

Bank of England (2025): Transitioning to a repo-led operating framework – discussion paper feedback statement.

Bindseil, U (2016): "Evaluating monetary policy operational frameworks," paper presented at the Federal Reserve Bank of Kansas City Jackson Hole symposium.

Bindseil, U, M Corsi, B Sahel and A Visser (2017): "The Eurosystem collateral framework explained", European Central Bank Occasional Paper Series, no 189.

Borio, C (2001): "A hundred ways to skin a cat: comparing monetary policy operating procedures in the United States, Japan and the euro area", BIS Papers, no 9.

----- (2023): "Getting up from the floor", BIS Working Papers, no 1100.

Buessing-Loercks, M, D King, I Mak, and R Veyrune (2020): "Expanding the central bank's collateral framework in times of stress", Special Series on Covid-19, International Monetary Fund.

Cantú, C, P Cavallino, F De Fiore and J Yetman (2021): "A global database on central banks' monetary responses to Covid-19", BIS Working Papers, no 934.

Cap, A, M Drehmann and A Schrimpf (2020): "Changes in monetary policy operating procedures over the last decade: insights from a new database", BIS Quarterly Review, December.

Cavallino, P, M Drehmann, R Finlay and J Remache (2025): "Monetary policy operational frameworks – a new taxonomy", BIS Quarterly Review, September.

Chailloux, A, S Gray, and R McCaughrin (2008): "Central bank collateral frameworks: principles and policies", IMF Working Papers, no 222.

Choi, D, J Santos and T Yorulmazer (2021): "A theory of collateral for the lender of last resort", Review of Finance, vol 25, no 4.

Committee on the Global Financial System (CGFS) (2026): "Foreign currency funding risk and cross-border liquidity", CGFS Papers no 71.

Committee on the Global Financial System (CGFS) and Markets Committee (2015): "Central bank operating frameworks and collateral markets", CGFS Papers, no 53.

Committee on Payments and Market Infrastructures (CPMI) (2022): Improving access to payment systems for cross-border payments: best practices for self-assessments.

Ennis, H (2016): "Models of discount window lending: a review", Federal Reserve Bank of Richmond Economic Quarterly, vol 102, no 1.

Financial Stability Board (FSB) (2025): Global monitoring report on non-bank financial intermediation.

Garcia Pascual, A, T Piontek, R Veyrune, and J Wu (2025): "Addressing market dysfunction and liquidity stresses in nonbank financial intermediaries", International Monetary Fund Global Financial Stability Note, no 4.

Gomes, D, S Sauer, I Alexopoulou, C Brancatelli, and D Gybas (2025): "Changes to the Eurosystem collateral framework to foster greater harmonisation", European Central Bank Economic Bulletin, no 1.

Iskaki, V, T Linzert, Y Schneider, M Skrzypińska and O Vergote (2026): "How banks are adjusting to declining reserves", The ECB Blog.

Kelly, S (2024): "Policy note: weekly Fed report still drives discount window stigma", Journal of Financial Crises, vol 6, no 3.

Lee, H and A Sarkar (2018): "Is stigma attached to the European Central Bank's marginal lending facility?", Liberty Street Economics.

Markets Committee (2022): Market dysfunction and central bank tools.

Nyborg, K (2017): "Central bank collateral frameworks", Journal of Banking and Finance, vol 83.

Perli, R (2025): "Money market conditions and the Federal Reserve's balance sheet", remarks at the US Treasury Market Conference, New York.

Saporta, V (2024): "Let's get ready to repo!", speech at the Association for Financial Markets in Europe, London.

Endnotes

Graph 1.A: Simple average. Retrieved from the BIS central bank total assets data set. Quarterly data. Last observation is Q3 2025. AEs include AU, CA, CH, EA, GB, HK, JP, KR, NZ, SE, SG and US. EMEs include BR, CL, CN, ID, IN, MX, MY, PE, PH, TH, TR and ZA.

Graph 1.B: The sample covers AU, BR, CA, CH, CL, CN, EA, GB, HK, ID, IN, JP, KR, MX, SG, TR, US and ZA. Banks are all deposit-taking corporations.

Graph 4.A: AEs include AU, CA, CH, EA, GB, HK, JP, KR, NZ, SE, SG and US. EMEs include BR, CN, CO, ID, IN, KH, MX, MY, PH, TH, TR, VN and ZA.

Table 1: AEs include AU, CA, CH, EA, GB, HK, JP, KR, NZ, SE, SG and US. EMEs include BR, CL, CN, CO, ID, IN, KH, MX, MY, PH, TH, TR, VN and ZA.

Table A.1: AEs include AU, CA, CH, EA, GB, HK, JP, KR, NZ, SE, SG and US. EMEs include BR, CN, CO, ID, IN, KH, MX, MY, PH, TH, TR, VN and ZA.

Appendix

1 The views expressed in this publication are those of the authors and not necessarily those of the Bank for International Settlements or its member central banks. We thank Elena Munteanu and Yui Ching Li for excellent research support; and Paolo Cavallino, Mathias Drehmann, Gaston Gelos, Daniel Rees, Andreas Schrimpf, Frank Smets, Nikola Tarashev, Philip Wooldridge and representatives from Markets Committee member central banks for helpful comments. All remaining errors are our own.

2 The Markets Committee is a central bank forum comprising senior officials with expertise in central bank operations and their interactions with financial markets. For further information on the Markets Committee, its current membership and work, see https://www.bis.org/about/factmktc.htm.

3 Cap et al (2020) discuss the 2020 update of the Markets Committee Compendium, which captures changes in operational frameworks after the Great Financial Crisis.

4 Other types of OMOs that are not covered here are outright transactions that involve the buying and selling of securities in the open market, for example as part of asset purchase programmes. In addition, foreign exchange (FX) swaps are not included in the analysis.

5 This aligns with the discussion in Borio (2001), which compares the monetary policy operating procedures in the United States, Japan and the euro area.

6 See Cantú et al (2021) on central banks' monetary response to the Covid-19 pandemic; Cavallino et al (2025) on the taxonomy of operational frameworks; and Borio (2023) on trade-offs between different operational frameworks.

7 EME central banks often use FX swaps and issue central bank bills to sterilise reserves.

8 The Bank of England introduced the CNRF in response to events such as the 2020 "dash for cash" and the 2022 liability-driven investment (LDI) funds episode, during which the gilt market faced severe dysfunction arising from a temporary increase in NBFIs' demand for liquidity.

9 See CPMI (2022) for an overview of payment system participants' settlement accounts.

10 Arseneau et al (2025) find that when moving from business as usual to stress-related facilities, collateral schemes become broader, tenors become longer and pricing becomes more expensive.

11 Cantú et al (2021) report that about two thirds of the lending operations policies in place during the Covid-19 pandemic were newly established.

12 The share of NBFIs in the domestic financial sector's total assets is smaller in EMEs than in AEs, which can be an explanation for lower access.

13 While the Bank of Canada uses the generic term "NBFIs" in its access guidelines, the Bank of England explicitly mentions insurance companies, pension funds and liability-driven funds.

14 See Markets Committee (2022) for an in-depth discussion.

15 The Central Bank of Brazil accepts government bonds only for liquidity tools for monetary policy implementation. Banks rely on other collateral types when accessing tools for financial stability.

16 Bindseil et al (2017) identify both primary objectives (eg support monetary policy, protect against losses) and secondary objectives or constraints (eg market neutrality and cost efficiency).

17 For a survey of the literature analysing these trade-offs, see for example Ennis (2016).

18 For a few facilities for monetary policy implementation, no price is charged. This reflects the fact that at some central banks, the intraday facility can also serve monetary policy implementation.

19 Inference depends on the volatility/volume of other assets in the balance sheet item (Kelly (2024)).