Towards liquid and resilient government debt markets in EMEs

Over the last 20 years, government debt markets in emerging market economies (EMEs) have grown and matured. Not only has it become easier for foreign investors to participate in these markets, but also the local investor base has deepened. Our findings show that the investor base and size of hedging markets affect the liquidity and resilience of EME government debt markets. In times of stress, a greater presence of domestic banks helps stabilise liquidity conditions, while domestic and foreign non-banks could propagate external shocks. Countries with more developed hedging markets exhibit more resilient liquidity conditions after major shocks. 1

JEL classification: D53, E63, G15, G18, H63.

Government debt markets play a crucial role in the financial system and economy at large. By providing a benchmark to price financial assets, well-functioning government debt markets in local currency ensure the transmission of monetary policy to the wider economy and facilitate the development of corporate bond and other markets. Deep and liquid debt markets are thus a cornerstone of the financial system, especially if they remain liquid in times of stress.2 Less liquid markets, by contrast, tend to propagate adverse shocks more quickly (eg Boermans et al (2016)).

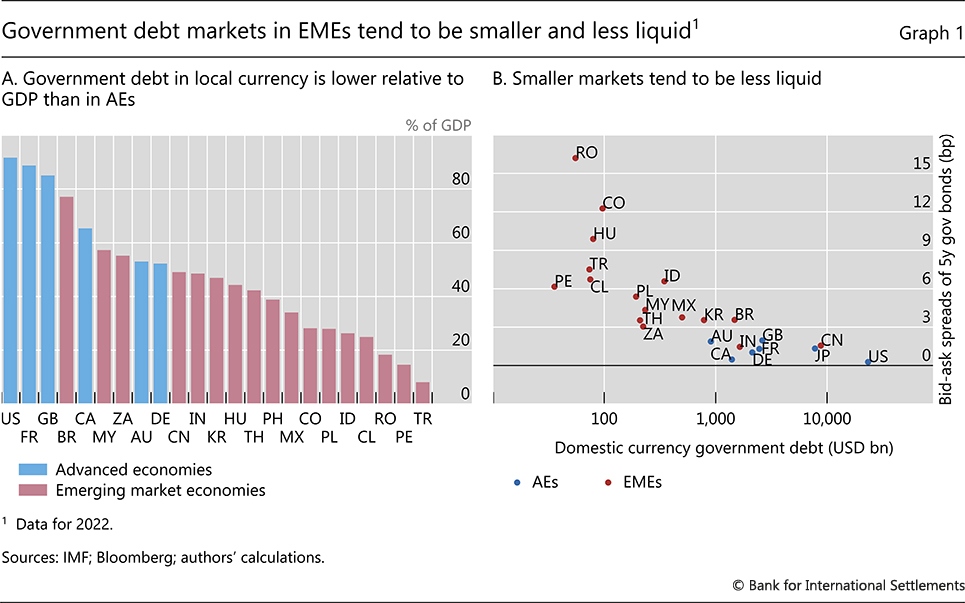

Over the last 20 years, debt markets in emerging market economies (EMEs) have grown and matured. It has become easier for foreign investors to participate, and the domestic investor base has grown. Overall, EMEs tend to have smaller government debt markets than advanced economies (AEs) (Graph 1.A), both in absolute terms and relative to gross domestic product (GDP). These smaller markets also generally tend to be less liquid (Graph 1.B). Yet as financial markets in EMEs grow bigger, broader and more liquid (BIS (2020)), this could alter liquidity conditions and how resilient these markets are to shocks.

Key takeaways

- The presence of different investor types and the size of hedging markets affect the liquidity and resilience of government debt markets in EMEs.

- In times of stress, a deep domestic investor base protects EME debt market liquidity while non-bank investors exacerbate shocks.

- EMEs with deeper hedging markets weather shocks to liquidity conditions better than others during observed stress events.

Against this background, this article shows that the composition of the investor base and the depth of hedging markets affect liquidity conditions and the resilience of local currency government bond markets in EMEs. This applies in both tranquil times and times of stress, although the role played by different investor groups changes. We focus on market liquidity, ie the ability to trade immediately at "market" prices and with minimum impact on prices.3 We also look at the resilience of liquidity, ie how quickly liquidity measures return to long-run averages.

This article is organised as follows. First, we discuss how market liquidity and resilience are measured as well as trends in AEs and EMEs over time. Next, we consider the roles of the investor base and hedging markets in market liquidity. We then present evidence on market liquidity during normal and stress periods and during three specific shocks. The final section concludes.

Measuring market liquidity and resilience

Market liquidity is a multi-faceted concept. At the most basic level, it refers to the ease with which securities can be traded. In practice, a market is liquid if securities can be bought and sold quickly in large amounts without affecting prices adversely.4 We gauge liquidity using a measure that considers transaction costs – the difference between quoted bid and ask prices from Bloomberg, adjusted by their average price. While these quotes are only indicative, ie they do not commit market makers to trade at these prices, they are widely available and tend to proxy high-frequency measures reasonably well (Schestag et al (2016)).5

Liquidity is resilient if transaction costs quickly return to normal levels after being hit by a shock.6 We proxy resilience with the speed at which bid-ask spreads return to long-term levels, ie their speed of mean reversion. We measure this over a one-year window since estimates over shorter windows are more unstable. In a resilient market, we expect the speed of mean reversion to be high.

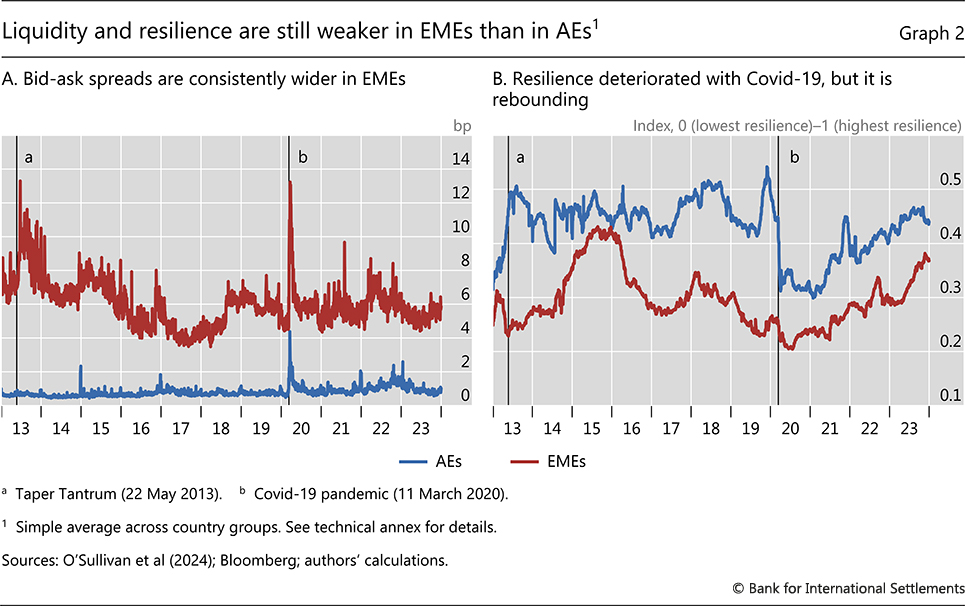

Our measures confirm that bond markets in EMEs tend to have wider bid-ask spreads (Graph 2.A) and lower resilience than those in AEs (Graph 2.B). Bid-ask spreads on EME government debt have followed a cyclical pattern over the past decade but without any overall trend. They spiked during the 2013 Taper Tantrum and the March 2020 Covid-19 turmoil. Resilience is lower than in AEs, as indicated by the lower degree of mean reversion in spreads. The resilience of liquidity in EME debt markets rose from mid-2013 to the end of 2015 but fell in 2016 on the back of lower commodity prices. During the Covid-19 pandemic, resilience deteriorated less in EMEs than in AEs. Over the last three years, markets in both EMEs and AEs appear to have become more resilient again.

Developing liquid and resilient government debt markets

Developing liquid and resilient markets for government debt is a key policy objective shared by governments (including their debt management offices) and central banks (Tombini (2023)). Even though financial markets in EMEs have developed substantially and have become more accessible to foreign investors over the past two decades,7 they still lag those in AEs. CGFS (2019) provides a broad overview of the factors that are important for developing deep and liquid markets. These factors range from the fundamental, such as the rule of law and efficient legal and judicial frameworks, to the technical, like the ability to buy back debt or swap illiquid for liquid issues. Two factors are key in developing liquid and resilient government debt markets in EMEs: (i) a broad and diversified investor base and (ii) deep hedging markets.

The role of the investor base

A diverse investor base is a precondition for liquid markets, as different investment needs, beliefs and strategies make it less likely for all market participants to buy or sell at the same time. A growing literature shows that long-term investors such as pension funds and insurance companies can stabilise markets (Fang et al (2023), Zhou (2024)). Long-term investors rarely sell their securities though; rather, they tend to hold them to maturity. Thus, they need to be complemented by traders with a shorter horizon. These include, in some markets, leveraged investors and high-frequency traders. Bringing these different players together requires market intermediaries – notably market-makers in banks8 and brokerage houses. Their main function is to facilitate trading and the sharing of risks among the investors.

Diversification of the investor base can also take place across borders. Not only do foreign investors provide additional funds, but they also tend to face different circumstances, trading needs and expectations than local investors. This means that their entry can increase market liquidity and depth (CGFS (2019)). That said, high foreign participation also exposes a market to global risk factors and the potential for adverse spillovers (Carstens and Shin (2019), Ho and Ho (2022), Zhou (2024)). Shocks to global risk aversion may lead foreign investors to retrench and shed EME assets for reasons unrelated to domestic conditions. Without a developed domestic investor base able to step in and absorb foreigners' asset sales, this can lead to large swings in bond prices, which can affect the liquidity and resilience of government debt markets, especially in EMEs.

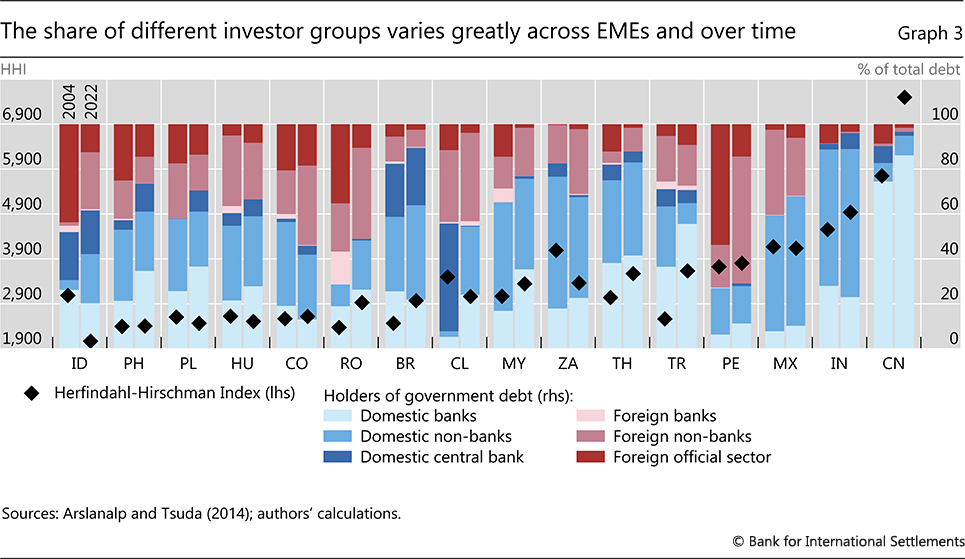

We analyse the investor base in 16 EMEs, drawing on updated data from Arslanalp and Tsuda (2014). The data break down the investors in government debt into six groups: (i) domestic banks, (ii) domestic non-banks, (iii) the central bank, (iv) foreign banks, (v) foreign non-banks and (vi) foreign official institutions.9 Among these categories, non-banks encompass a particularly diverse group of participants: institutional investors like pension funds, insurance companies, mutual funds, hedge funds, proprietary trading firms and any other investor that is not a bank.10

The composition of the investor base, and the diversification across borders and types of institution, varies greatly across EMEs and over time (Graph 3). In most countries, domestic non-banks are the most important group of investors. But there are exceptions. For example, in China and Türkiye, domestic banks are by far the most important holders of government debt. In Chile, Colombia, Romania and Peru, it is foreign non-banks. What is common across countries is that holdings by the domestic central bank and, especially, the foreign official sector are nowadays small compared with (domestic and foreign) private positions. Some debt markets, notably those of Colombia, Indonesia, the Philippines and Poland have seen the investor base become more diversified over time; other markets, eg in India, Mexico and China, have seen less diversity.11 Finally, foreign banks are the group with the lowest participation in EMEs, with an average of 1.1% of the total government debt holdings in our sample.

Hedging markets

Market liquidity also depends on the presence and size of complementary markets, such as those for repos and derivatives. Repos allow investors to borrow against their securities holdings when faced with cash needs, rather than selling them. They also support liquidity provision more directly by allowing securities dealers to fund their trading inventories, to reuse securities held by long-term investors for trading and to lever up their securities portfolios (CGFS (2017, 2019)). Derivatives, in turn, permit investors to adjust their exposure to exchange and interest rate risk instead of transacting in the market for the underlying bonds.12

While the development of complementary markets has its merits, it also raises certain concerns that warrant consideration. Since repos tend to be short term, relying on them for funding leads to a shortening of maturities and higher roll-over risk. They can also be used to lever up excessively. This can give rise to procyclicality, increasing financial stability risks, especially if the underlying collateral is illiquid (CGFS (2017)). Similarly, derivatives can transmit external shocks instead of dampening them.

Further reading

Comprehensive data for repo markets are not readily available. According to CGFS (2017), in mid-2016, around $12 trillion of repo and reverse repo transactions against government bonds were outstanding globally. Of these, nearly $9 trillion were collateralised with government bonds. While the share of EMEs in the global total is tiny, some EMEs have quite sizeable repo markets. For instance, in Mexico, the outstanding volume of repos amounted to 21% of outstanding government bonds in mid-2016, which was in line with most AEs (CGFS (2017)).

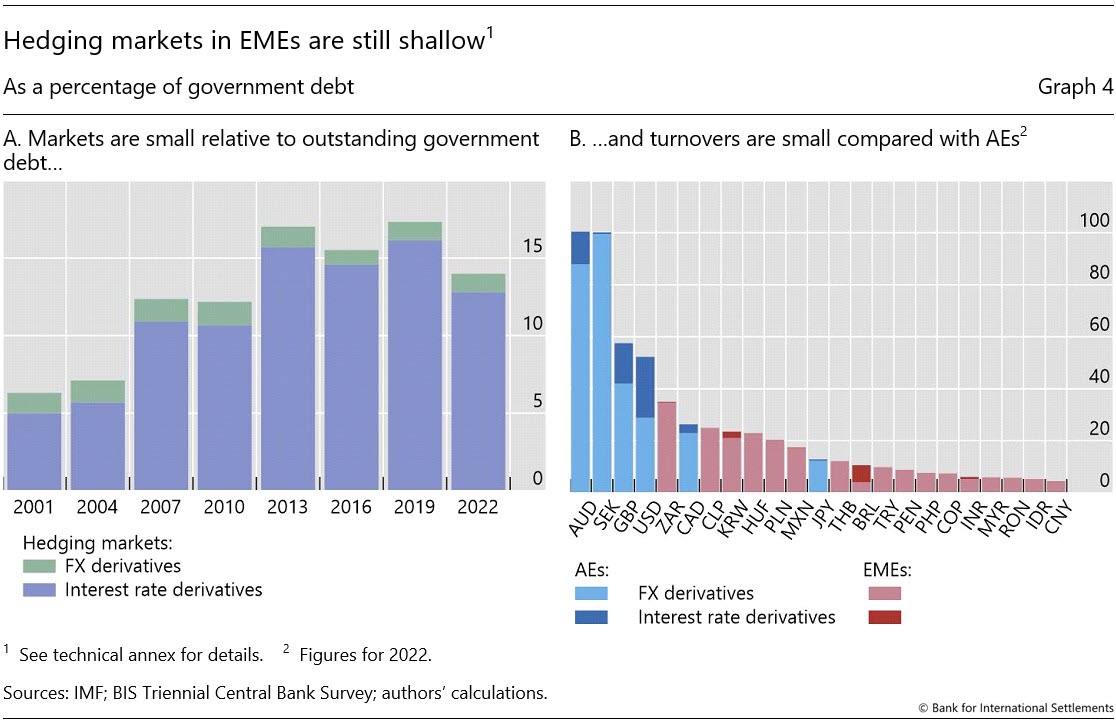

Over the past decade, growth in the markets to hedge currency and interest rate risk has not kept up with the increase in overall government debt in EMEs (Graph 4.A). While these markets continued to grow – both in terms of dollar volumes and relative to GDP – derivatives turnover fell when expressed relative to government debt outstanding (due to the strong rise of the latter). Some EMEs do have relatively deep markets, but they lag their AE peers (Graph 4.B).

A common obstacle to developing hedging markets is an imbalance between players who want to hedge themselves against a specific risk and those prepared to take the other side. Since macroeconomic risks, such as exchange rate and interest rate risk, are not easy to diversify, financial intermediaries are often not prepared to sell the appropriate insurance unless they are able to offload their positions to investors who are exposed to such risks in opposite ways (Upper and Valli (2016)).13,14

Liquidity after adverse spillovers

Different investor groups can shield or erode government bond market liquidity, both in tranquil times and during episodes of stress. Moreover, major shocks can affect liquidity in EMEs differently, depending on the depth of their hedging markets.

The type of investor

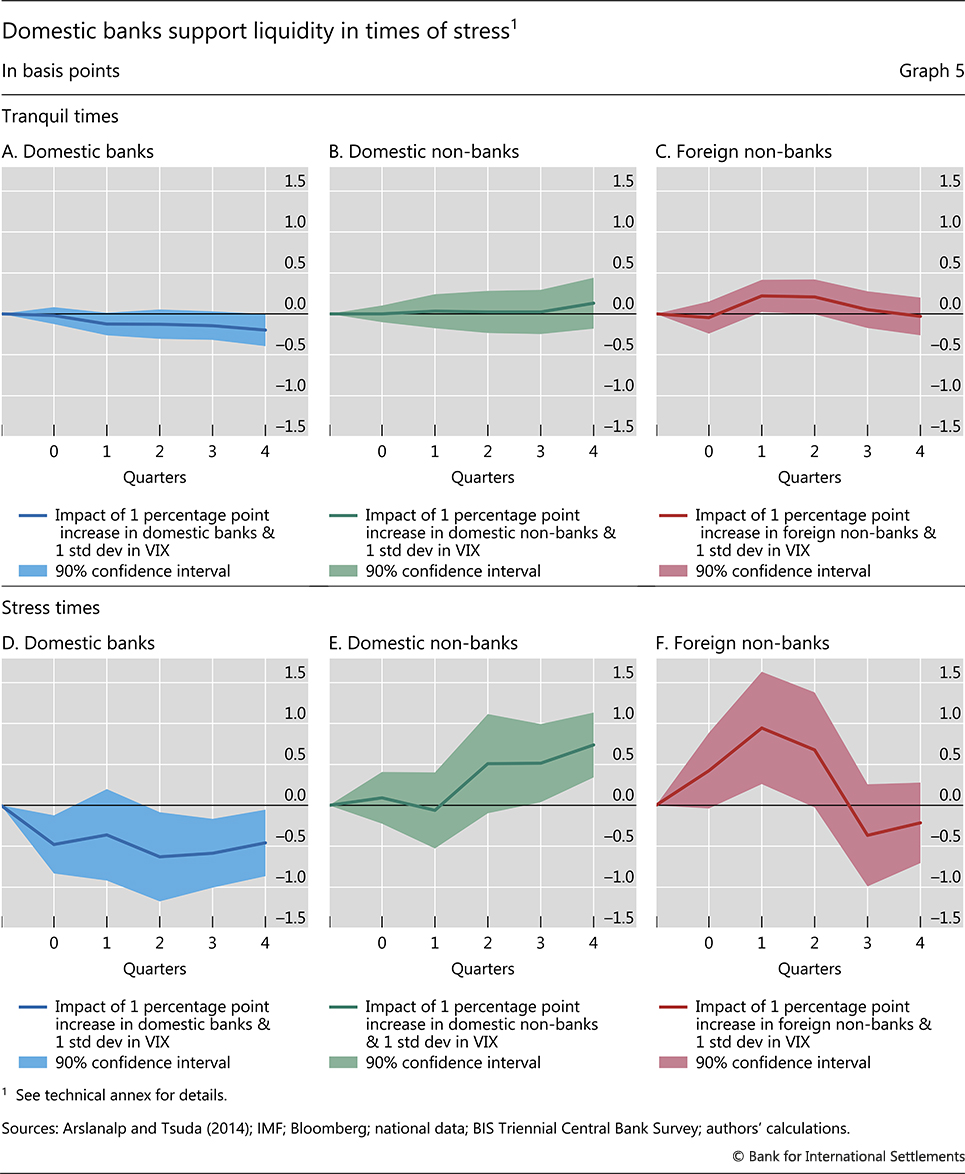

The composition of the investor base affects how market liquidity responds to external shocks. The role of different investors varies between tranquil and stress periods – the latter defined as periods with the Chicago Board Options Exchange Volatility Index (VIX) above the 75th percentile of the distribution.15 Panel local projections (Jordà (2005)) for 16 EMEs show that increases in the VIX – as a measure for global shocks – tend to be associated with deteriorating liquidity (ie widening spreads) in government bond markets.16 A one standard deviation increase in the VIX is linked to a 0.7 basis point (bp) widening in spreads in tranquil times and a 6.7 bp widening in stress times. These relate to an average level of bid-ask spreads of 6.5 bp in our sample.

In tranquil times, a larger share of foreign non-bank investors tends to marginally increase the impact of VIX changes on liquidity. A 1 percentage point (pp) higher share of foreign investors is associated with an additional 0.2 bp widening in the bid-ask spread after an increase of one standard deviation in the VIX (Graph 5.C). A higher share of domestic banks, by contrast, reduces the impact of VIX increases on liquidity, although the results are not statistically significant (Graph 5.A). The role of domestic non-bank investors in tranquil periods is neutral (Graph 5.B).17 These findings are broadly in line with the literature, in which foreign investors may amplify shocks.

In times of stress, a greater footprint of domestic banks tends to stabilise liquidity, while a greater share of non-banks (both foreign and domestic) tends to amplify liquidity strains (Graphs 5.D, 5.E and 5.F). A 1 pp higher share of domestic banks dampens the impact of a one standard deviation change in the VIX by 0.6 bp (Graph 5.D), or one tenth. By contrast, a similarly higher share of domestic and foreign non-banks amplifies it by 0.7 bp and 0.9 bp, respectively (Graphs 5.E and 5.F).18 Unfortunately, we are not able to disentangle which types of non-bank investors could explain this finding, ie whether it is insurance companies, mutual funds, hedge funds, proprietary trading firms or others.

The depth of hedging markets

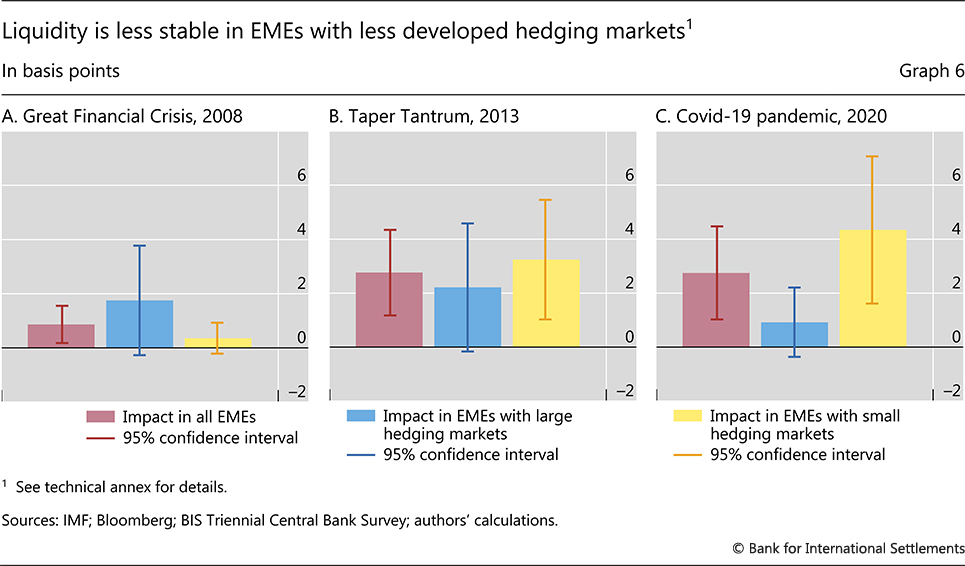

There are good reasons to believe that liquidity in EMEs with well-developed hedging markets will be more resilient to major shocks. To examine this, we compare liquidity in the 90 days before and after the Great Financial Crisis in 2008, the Taper Tantrum in 2013 and the Covid-19 pandemic in 2020.

Bid-ask spreads widened during all three episodes. The smallest effect was after the Lehman Brothers bankruptcy, at around 1 bp (Graph 6.A). The highest was after both the 2013 Taper Tantrum and the Covid-19 pandemic, at almost 3 bp (Graphs 6.B and 6.C). During the Taper Tantrum and the Covid-19 pandemic, spreads widened more significantly (approximately 3 and 4 bp, respectively) in EMEs with below-median depth in hedging markets. In EMEs with more developed complementary markets, liquidity conditions appeared more resilient, in particular amid the turmoil in fixed income markets during the Covid-19 pandemic.

Conclusion

Liquid and resilient government debt markets are key to ensuring the smooth functioning of the financial system. This is especially so in EMEs, where market functioning can easily be buffeted by spillovers. Government bond markets in EMEs tend to be less liquid than those in AEs, and liquidity takes longer to revert to "normal" values after a disruption.

Our main contribution is to show how the investor base and the size of hedging markets matter for the behaviour of liquidity in EMEs. In periods of stress, when bond markets are at risk of outflows and liquidity is most valuable, domestic banks support the stability of liquidity conditions, while domestic and foreign non-banks are associated with less stable liquidity. In parallel, EMEs with well-developed hedging markets appear to be more resilient to major shocks. The results in this article align with financial theory and previous evidence. They underscore the importance for EMEs to foster a diverse investor base and develop their complementary markets.

Going forward, there are numerous avenues for further research. In particular, there is scope to collect and assess data on repo and derivatives markets across countries over time. It would also be useful to gather a full breakdown of debt holdings, especially within the non-bank sector and their country of residence. This would help researchers examine the behaviour and impact of different non-bank investors (see also McGuire et al (2024) in this issue). Finally, on the basis of more granular data, there is scope to further improve the measurement of market liquidity, particularly in times of stress.

References

Aguilar A, C Cantú and R Guerra (2023): "Fiscal and monetary policy in emerging market economies: what are the risks and policy trade-offs?", BIS bulletin, no 71, March.

Aldunate F, Z Da, B Larrain and C Sialm (2023): "Pension fund flows, exchange rates, and covered interest rate parity". American Finance Association 2024 Conference.

Amihud, Y (2002): "Illiquidity and stock returns: cross-section and time-series effects". Journal of Financial Markets, vol 5, no 1, pp 31–56.

Arslanalp, S and T Tsuda (2014): "Tracking global demand for emerging market sovereign debt", IMF Working Papers, no WP/14/39.

Avalos, F and R Moreno (2013): "Hedging in derivatives markets: the experience of Chile", BIS Quarterly Review, March, pp 53–63.

Bank for International Settlements (2020): "Implications of financial market development for financial stability in emerging market economies". Note submitted to the G20 International Financial Architecture Working Group, July.

----- (2022): Foreign exchange markets in Asia-Pacific, report by a study group established by the Asian Consultative Council of the Bank for International Settlements, October.

Bekaert G and M Hoerova (2014): "The VIX, the variance premium and stock market volatility". Journal of Econometrics, vol 183, no 2, pp 181–192.

Boermans, M, J Frost and S Steins Bisschop (2016): "European bond markets: do illiquidity and concentration aggravate price shocks?", Economic Letters, vol 141, pp 143–146.

Carstens, A and H S Shin (2019): "Emerging markets aren't out of the woods yet", Foreign Affairs, March.

Committee for the Global Financial System (2017): "Repo market functioning", CGFS Papers, no 59.

----- (2019): "Establishing viable capital markets", CGFS Papers, no 62.

----- (1999): "Market liquidity: research findings and selected policy implications", CGFS Papers, no 11.

Fang, X, B Hardy and K Lewis (2023): "Who holds sovereign debt and why it matters", BIS Working Papers, no 1099, May.

Harris, L (1990): "Liquidity, trading rules and electronic trading systems", Monograph Series in Finance and Economics, Monograph 1990-4, New York University Salomon Center.

Ho, E and C Ho (2022): "Foreign participation in local currency government bond markets in emerging Asia: benefits and pitfalls to market stability", Journal of International Money and Finance, vol 128, 102699.

Jordà, Ò (2005): "Estimation and inference of impulse responses by local projections", American Economic Review, vol 95, no 1, pp 161–182.

McGuire, P, G von Peter and S Zhu (2024) "International finance through the lens of BIS statistics: residence vs nationality", BIS Quarterly Review, March, pp X–Y.

O'Sullivan, C, V Papavassiliou, R Wekesa Wafula and S Boubaker (2024): "New insights into liquidity resiliency", Journal of International Financial Markets, Institutions and Money, vol 90, 101892.

Schestag, R, P Schuster and M Uhrig-Homburg (2016): "Measuring liquidity in bond markets", Review of Financial Studies, vol 29, no 5, pp 1170–1219.

Tombini, A (2023): "Policies for liquid and well-functioning sovereign debt markets", Contribution to a panel on Sovereign debt: liquidity and consequences, Central Bank Research Association (CEBRA) Annual Meeting, hosted by the Federal Reserve Bank of New York, 5 July.

Upper, C and M Valli (2016): "Emerging derivatives markets?", BIS Quarterly Review, December, pp 67–80.

Zhou, H (2024) "The fickle and the stable: global financial cycle transmission via heterogeneous investors", unpublished working paper, Princeton University.

Technical annex

Graphs 2.A–B: Simple average across 16 EMEs (BR, CL, CN, CO, HU, ID, IN, MX, MY, PE, PH, PL, RO, TH, TR and ZA) and seven AEs (AU, CA, DE, FR, GB, JP and US).

Graph 2.B: The resilience measure is based on O'Sullivan et al (2024). A higher (lower) value denotes a faster (slower) adjustment of spreads to a three-year mean in logs.

Graphs 4.A–B: Average daily turnover in spot and derivatives markets, including exchange-traded derivatives. Turnover is scaled by the government debt of the country issuing the currency.

Graph 4.A: Equally weighted average figures covering 16 EME currencies.

Graphs 5.A–F: Cumulative response from local panel projections for 16 EMEs from Q1 2004 to Q4 2022, where data are available. We regress bid-ask spreads of five-year local currency government bonds on the lag of the same variable, the VIX in logs, the share of the type of investors, the interaction term of the VIX and the investor type, four lags of a vector of controls that includes the level of the yields, the policy rate, the ratio of government debt to GDP, the size of hedging markets and the HHI of holdings. The regressions include fixed effects and Driscoll and Kraay standard errors, accounting for cross-sectional dependence. Tranquil (stress) regimes are defined when the VIX is below (above) the long-term 75th percentile.

Graphs 6.A–C: Panel estimations of the daily data of bid-ask spreads of the five-year government bonds in a 90-day window before and after the three shocks, with country fixed effects. Standard errors clustered by country. EMEs with large (small) hedging market groups are defined as countries above (below) the sample median for the 16 EMEs. The Great Financial Crisis is dated to 15 September 2008, the Taper Tantrum to 22 May 2013 and the Covid-19 pandemic to 11 March 2020.

Annex: measurement and econometric approach

Measuring resilience

Following O'Sullivan et al (2024) and earlier work, we measure resilience as the pace of mean reversion in liquidity estimated with the following equation:19

where Lt denotes the bid-ask spread on day t, Φ the long-run value of liquidity, k the speed of adjustment to this value and Et a normally distributed white noise error. A higher speed of adjustment parameter k indicates higher resilience.

Empirically, we address serial correlation in the residuals by incorporating past liquidity changes as supplementary explanatory variables in the model.20 For each country's benchmark bonds, we estimate the following empirical model using daily liquidity data:

where t denotes the time index, Y denotes the relative measure of bid-ask spreads relative to a mean in logs, and our dependent variable ΔL/Yi.t denotes the spread over a long-run benchmark. Finally, Vol denotes the volatility of bonds of the same maturity.

To ensure our resilience measure is robust, we set negative values to zero. This fosters a more meaningful and realistic representation of resilience characteristics in our analysis.

Measuring the effect of different types of investors on liquidity

We estimate impulse response functions via local projections (Jordà (2005)) to trace out the effects of global shocks on EME liquidity conditions. We use interaction terms to assess how these are shaped by the presence of different investor groups, and we distinguish between tranquil and stress periods. Specifically, we estimate the following equation:

where Yi,t+h is the cumulative effect of the bid-ask spreads of five-year government bonds for quarters h, from 0 to 4 quarters; Yi,t-1 denotes the lag of the bid-ask spreads; V1Xt is the log of the VIX; and Invi,t is investor type. Xit-1 is a vector of domestic variables with four lags that includes the level of five-year government bond yields, the policy rate, the ratio of government debt to GDP, the size of hedging markets and the HHI of holdings. R denotes the regime of interest: tranquil versus stress times.

The stress regime covers observations when VIX levels are in the top quartile, and the tranquil times regime considers data when VIX is below the top quartile. We are interested in the coefficient β4 of the interaction between the VIX and the type of investor. The regressions include country fixed effects. Standard errors are clustered by country for a panel of 16 EMEs with quarterly observations, spanning from the first quarter of 2004 to the fourth quarter of 2023. To retain sufficient degrees of freedom, we enter one investor group at the time.

Measuring the effect of exogenous shocks on liquidity in EMEs with hedging markets of different sizes

We estimate the effect of three different shocks on the bid-ask spreads of all EMEs in our sample. We then distinguish between those with a hedging market larger or smaller than the median. For this, we use the following equation:

where yit is the bid-ask spread of five-year government bond yields, and EMEs denotes either all EMEs or those with large or small hedging markets. Shockt is a dummy equal to one during the 90-day period after each of the stress periods. The regressions include country fixed effects. Standard errors are clustered by country for a panel of 16 EMEs with a 90-day window before and a 90-day window after each shock.

1 The opinions expressed in this article are those of the authors and do not necessarily reflect those of the Bank for International Settlements. We would like to thank Ryan Banerjee, Claudio Borio, Gaston Gelos, Bryan Hardy, Peter Hördahl, Benoît Mojon, Gabor Pinter, Andreas Schrimpf, Ilhyock Shim, Hyun Song Shin, Vladyslav Sushko, Philip Wooldridge and seminar participants at the BIS Representative Office for the Americas for useful comments and suggestions, and Alison Arnot for editorial support.

2 Surges in risk premia play an important role in the transmission of stress to EMEs (Aguilar et al (2023)). To some extent, robust liquidity can help shield EME government bond markets from such surges during episodes when global financial conditions tighten.

3 This is distinct from (but closely related to) funding liquidity, which refers to the ability to obtain funding at prices reflecting the underlying demand and supply.

4 More technically, one can distinguish between tightness (how far transaction prices deviate from mid-market prices), depth (the volume that can be traded without affecting the prevailing market price) and resilience (the speed with which price fluctuations from trades dissipate). See CGFS (2000).

5 Alternative measures tend to require data that are not available for a broad range of countries. These include the Amihud (2002) illiquidity measure, which requires information on volumes, and the micro-founded measures used in the market microstructure literature, which tend to be based on order book data. Moreover, measures based on daily prices do not significantly outperform quoted spreads. Schestag et al (2016) show that the correlation between Bloomberg bid-ask spreads and liquidity gauges constructed from order book data is about 0.7–0.8 at a monthly frequency.

6 Our definition of resilience differs somewhat from that commonly used in the market microstructure literature, where it typically refers to the speed by which the order book is replenished after a temporary imbalance (Harris (1990)).

7 A good example is the Asian Bond Markets Initiative, launched in December 2002 by the Association of Southeast Asian Nations (ASEAN), China, Japan and Korea. This initiative has stimulated the development of domestic bond markets as a source of long-term funding for Asian borrowers. It has also promoted local currency bonds as a new asset class for both resident and non-resident investors. Local currency government debt relative to GDP in ASEAN countries rose from 30% in December 2004 to 37% in September 2023.

8 Strictly speaking, this applies only to banks' trading assets. Banks also hold government securities as investments or to meet regulatory standards, which they often hold to maturity.

9 The holdings data do not allow us to distinguish between different instruments, for example local or foreign currency bonds and bank loans. We assume that the holding shares reported in the data apply to local currency bonds, which account for the bulk of public debt in most of the countries in our sample.

10 Fang et al (2023) and Zhou (2024) show that different types of non-banks in the euro area may behave quite differently.

11 We measure diversification with a Herfindahl-Hirschman index (HHI) proxy, which is equal to the sum of the squared market shares of each investor group. With six groups, it can range from 1,667 to 10,000, with lower values indicating greater diversification.

12 Reducing currency risk, for instance by allowing foreign investors to hedge, should make markets more resilient. The widening in spreads on EME government bonds in stress periods primarily reflects an increase in the currency risk premium (Ho and Ho (2022)).

13 An interesting example of the importance of domestic investors is Chile, where local pension funds had large foreign asset holdings and were required to hedge them in domestic currency. This made them a natural counterparty to foreign investors hedging their investments in assets denominated in Chilean pesos (Avalos and Moreno (2013)). The large-scale pension fund withdrawals in the wake of the Covid-19 pandemic led to a fall in the funds' foreign asset holdings. This could reduce their ability to act as stabilisers in the future (Aldunate et al (2023)).

14 BIS (2022) discusses other factors that have been holding back derivatives activity in Asian EMEs and policy measures to develop hedging markets in the region.

15 The VIX is an amalgam of uncertainty and risk aversion and is widely used in empirical research as a measure of the global price of risk (Bekaert and Hoerova (2014)). High readings of the VIX tend to be associated with periods of investor retrenchment and outflows from risky assets.

16 See the annex for details.

17 The statistical significance and magnitude of the impact of domestic investors increases when we set the cut-off between tranquil and stress periods at the median. In this case, both domestic banks and non-banks dampen the effect of VIX increases, while foreign non-bank investors continue to amplify it. We did not estimate similar responses for the domestic central bank, foreign banks and the foreign official sector, since their shares in total holdings tend to be very small.

18 These findings are largely robust to changes in threshold, the use of alternative measures of the global price of risk and the use of a triple interaction term with changes to the VIX, the type of investor and a dummy variable of a high financial stress regime.

19 This is different but similar to an error-correction model (ECM). In an ECM, the error correction relates to the last-period's deviation from a long-run equilibrium and it influences its short-run dynamics.

20 This step is crucial in eliminating potential bias in estimating resilience, represented by the parameter k.