Interest rate risk management by EME banks

Banks' management of interest rate risk depends on their business model as well as the environment in which they operate1. In comparison with banks in many advanced economies, banks in emerging market economies (EMEs) make less use of interest rate derivatives. Instead, they mitigate the impact of rate changes on their net interest income by minimising repricing gaps between assets and liabilities. The management of interest rate risk might become more challenging with the expansion of EME banks' securities holdings.

JEL classification: G21, E40.

The stress triggered by the collapse of Silicon Valley Bank in March 2023 put the spotlight on banks' management of interest rate risk (IRR). Banks manage this risk in various ways, depending on their business model as well as the macro-financial and institutional environment in which they operate. In comparison with banks in many advanced economies (AEs), banks in emerging market economies (EMEs) make less use of derivatives to manage IRR.2 We find that they limit the repricing gaps between assets and liabilities to reduce the impact of rate changes on their interest income. Specifically, they rely heavily on time deposits for funding, and extend floating rate or short-term loans with interest rate sensitivity similar to that of their deposits.

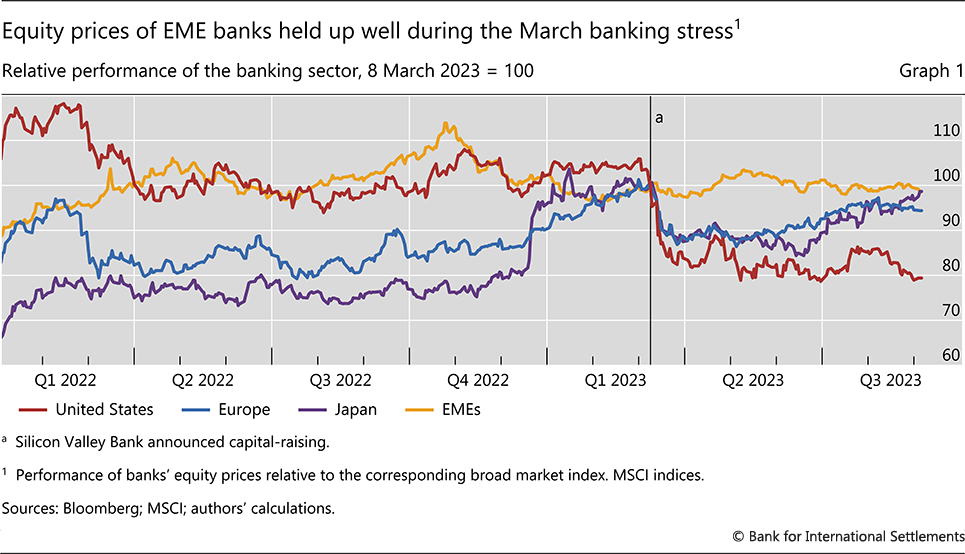

In a sign of investors' confidence in EME banks' management of IRR, the banking stress in March 2023 did not have a significant effect on EME banks. That episode led investors to reassess banks' vulnerability to higher interest rates. US banks saw their equity prices plunge, along with European and Japanese banks (Graph 1). Those facing persistent market scepticism, as indicated by a low price-to-book ratio, were hit particularly hard (BIS (2023)). In contrast, the equity prices of EME banks continued to track the broader market, as they had since the start of global monetary tightening in 2022. Even the prices of EME banks with low price-to-book ratios held up well.

In recent years, however, EME banks' exposure to interest rate-driven swings in valuation has been growing. In particular, the share of their assets invested in longer duration securities has expanded. This increases the importance of hedging the impact of interest rate changes on non-interest income, for example, with interest rate derivatives.

Key takeaways

- Banks in emerging market economies (EMEs) mitigate interest rate risk by extending floating rate or short-term loans with interest rate sensitivity similar to that of their deposits.

- EME banks make less use of derivatives to manage interest rate risk than their peers in many advanced economies.

- EME banks' securities holdings are increasing – changing the nature of their exposure to interest rate risk.

The rest of this feature is organised as follows. The next section discusses different ways in which banks are exposed to IRR. The feature then summarises evidence about the sensitivity of net interest income to interest rates and examines how EME banks limit such sensitivity. The subsequent section broadens the perspective to the sensitivity of overall profitability followed by a section on EME banks' increasing securities holdings. The concluding section outlines how approaches to IRR management might need to evolve as balance sheets become more complex. Box A analyses differences in the size and growth of interest rate derivatives markets across countries.

Interest rate risks on banks' balance sheets

Fluctuations in market interest rates directly affect a bank's profits through changes in net interest income and swings in the valuation of outstanding positions. Profits in turn influence a bank's net worth (or economic value). Banks manage these effects through the composition of their assets and liabilities.

The exposure of net interest income to IRR depends on the relative sensitivity of yields on interest-earning assets and interest-bearing liabilities to market rates. The relative sensitivity of yields is in turn influenced by differences in the time remaining to the next repricing, which is dependent on contractual terms for floating rate assets and liabilities, and happens at maturity for fixed rate ones.3 For example, if loans reprice more frequently than deposits, then higher market rates will boost banks' net interest margins (NIMs). The more sensitive deposit rates are to market rates, however, the stronger the rise in funding costs, thus eroding the boost to margins.

Interest rate moves also affect valuations. The longer the duration of an instrument, the greater the direct impact of rate changes on its (net present) value. Higher rates might further depress valuations indirectly through credit losses as the business cycle matures and borrowers' debt servicing costs rise. Accounting rules determine how such valuation gains and losses are recognised.4 If a bank does not value assets at market prices, unrealised losses can accumulate on its balance sheet as rates rise. These losses surface if the assets need to be sold, for instance, to meet deposit withdrawals.

Banks can manage IRR by either adjusting the composition of their balance sheet or hedging with derivatives. One approach is to match the interest rate sensitivity of assets and liabilities in specific repricing buckets. This is effective for mitigating IRR when net interest income accounts for the bulk of profits. It is more difficult to implement when the interest rate sensitivity of the asset portfolio is inherently different from that of the funding instruments. In addition, such rigid minimisation of repricing gaps might not suit a bank's business model.

A comprehensive approach to IRR hedging involves matching the interest rate sensitivity of an entire portfolio of assets to that of liabilities so as to minimise the impact of changes in interest rates on a bank's economic value. This can be done, for example, with derivative overlays that leave the balance sheet unchanged but reduce the gap between the effective duration of assets and liabilities. Supervisors frequently require banks to measure their IRR exposure using economic value models, in addition to measuring the impact of rate moves on net interest income (BCBS (2019)).

Interest rate sensitivity of net interest income

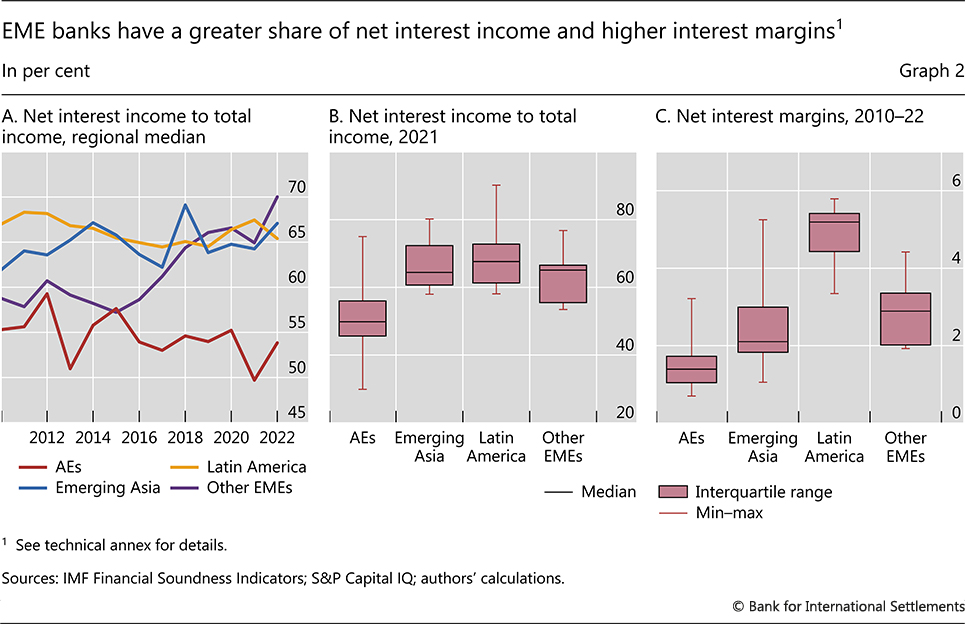

Net interest income accounts for a high share of banks' total income, particularly at EME banks. In recent years, net interest income has accounted for around 65% of total income at the median EME bank, compared with less than 55% at the median AE bank (Graphs 2.A and 2.B). Thus the interest rate sensitivity of net interest income has an important influence on a bank's overall IRR exposure.

Interest rate increases are usually found to have a positive impact on net interest income, but the impact is often small. This is particularly the case for short-term rates. The effect of changes to the slope of the yield curve tend to be similar, although less definitive (eg Altavilla et al (2018), Claessens et al (2018), CGFS (2018)).

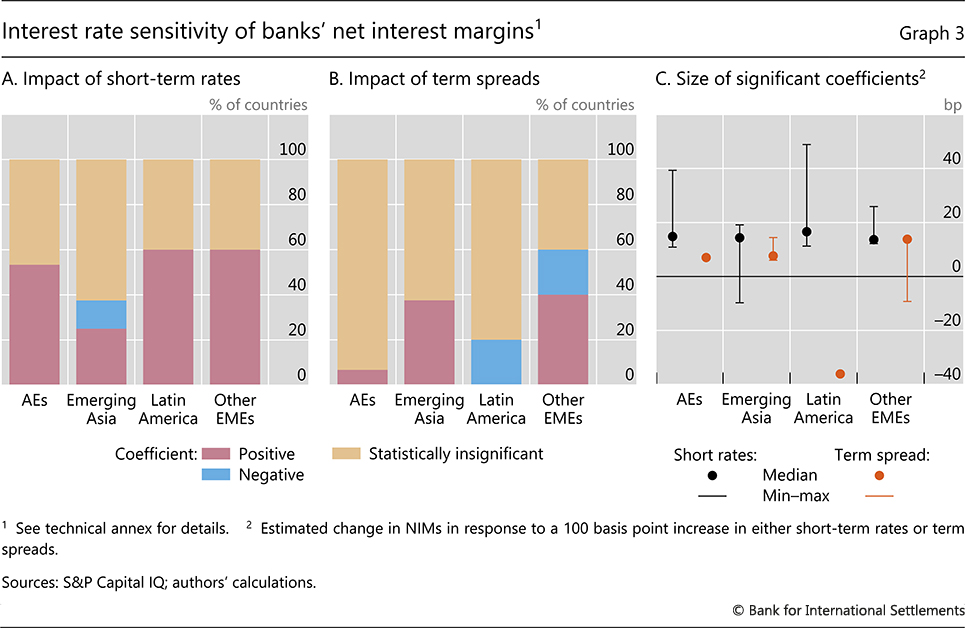

Similar results are found using a sample of over 1,200 banks in 33 countries covering the period 2010–22 (see the technical annex for an explanation of the methodology). Changes in short-term rates have a positive impact on banks' NIMs in a majority of countries in each region, with the exception of emerging Asia (Graph 3.A). The impact of the yield curve's slope is more mixed – it is positive in some countries, negative in others and insignificant in most (Graph 3.B). The level of short-term rates and the slope of the yield curve often move together, so the two variables are sometimes jointly significant despite being individually insignificant.

Even so, the estimated economic significance is typically small. Across banks in each region, a 100 basis point increase in short-term rates tended to boost NIMs by less than 20 basis points over four quarters (Graph 3.C). This compares with an average NIM over the 2010–22 period of about 210 basis points in emerging Asia, nearly 520 basis points in Latin America and roughly 290 basis points in other EMEs (in eastern Europe, the Middle East and Africa) (Graph 2.C). The boost to NIMs was more material for banks in AEs, where NIMs averaged only 140 basis points.

What explains the low interest rate sensitivity of EME banks' net interest income? The composition of their balance sheets suggests that they limit their IRR exposure through frequent repricing of both assets and liabilities.

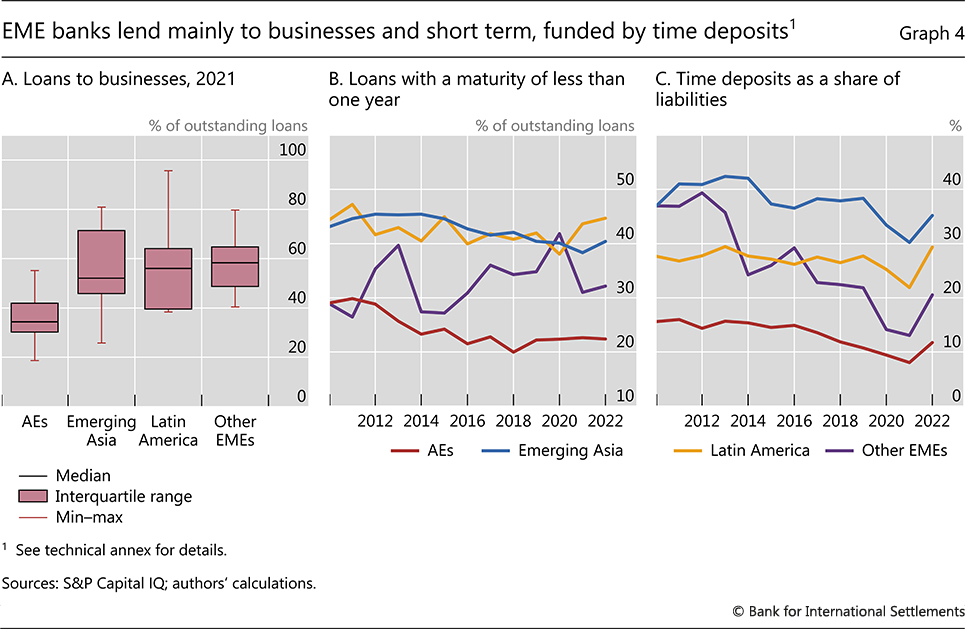

On the asset side, a high share of EME banks' loans have floating rates or short maturities (or often both). Business loans account for the largest share of EME banks' outstanding loans (Graph 4.A), and they typically have floating rates. Indeed, in most of the countries in our sample, the overwhelming majority of loans to businesses had floating rates as of 2021.5 By contrast, owing to large residential mortgage markets, lending to households makes up the largest share of AE banks' loan books. In general, mortgages are more likely than business loans to have long maturities at fixed rates.

The share of short-term loans is similarly high at EME banks. At the median bank in emerging Asia and Latin America, more than 40% of the outstanding loans have a remaining maturity of less than one year (Graph 4.B). By comparison, only 20% of the loans at the median AE bank are similarly short term. Among banks in other EMEs, the share lies in between. Overall, there is evidence that the loan rates of EME banks tend to reprice frequently and thus move with market rates.

On the liability side, EME banks rely heavily on time deposits, which bear interest and have a defined maturity date. Such deposits can be readily matched with assets in specific repricing or maturity buckets. At banks in emerging Asia, time deposits have accounted for about 35% of total liabilities in recent years, and even more historically (Graph 4.C). The share for banks in Latin America was around 30%. In contrast, at the typical AE bank, time deposits recently accounted for only 10% of liabilities. Time deposits at banks in other EMEs were also low in recent years, mainly because of the narrow yield differential with demand deposits in several eastern European countries where policy rates were kept low. At EME banks, demand deposits accounted for most of the remainder of their liabilities.

Time deposits are more expensive than demand deposits but are usually less costly than market funding. Whereas demand deposits typically pay no or minimal interest, interest rates on time deposits adjust with market rates. The higher cost of time deposits comes with a reduced likelihood of unexpected outflows because early withdrawals are either not permitted or allowed only with penalties. This is particularly relevant for EME banks, as they operate in a more volatile macro-financial environment than their AE peers. The higher incidence of interest rate and other shocks in EMEs suggests a higher likelihood of depositors withdrawing funds at short notice. The restrictions associated with time deposits reduce this likelihood.

Interest rate sensitivity of return on assets

Net interest income gives only a partial picture of banks' exposure to IRR as it excludes the impact of valuation changes. For a fuller picture, we now turn to banks' overall profitability, as measured by their return on assets (ROA).

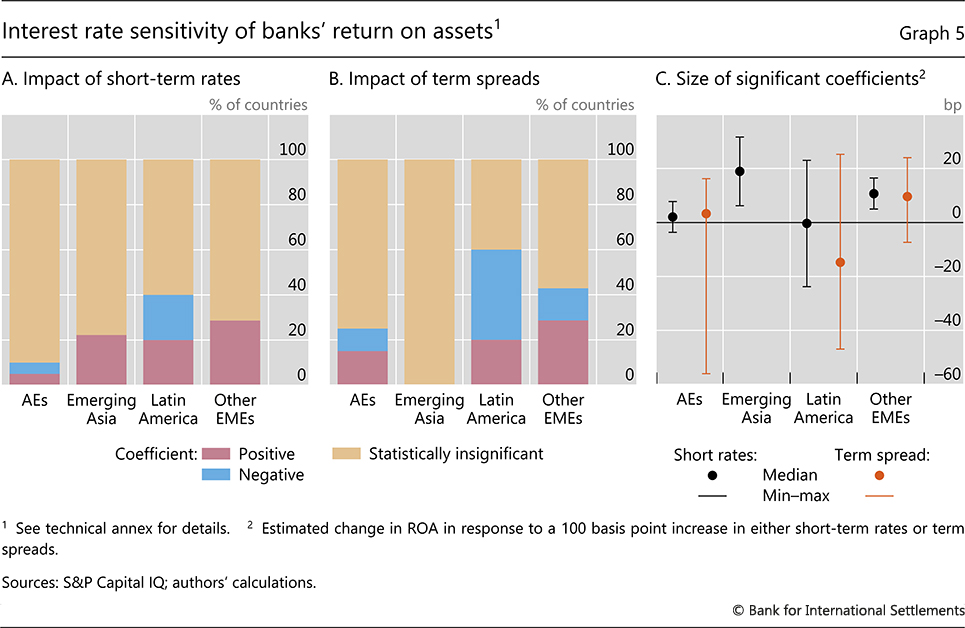

Previous studies generally concluded that banks' ROA was less sensitive to interest rates than NIMs (eg Borio et al (2017)). Using our sample of over 1,200 banks, we find similar results (Graph 5). In the majority of countries, the positive effect of higher rates on net interest income seems to be offset by a negative impact of other factors, such as portfolio valuations. In some countries, particularly in Latin America, the negative impact dominates. In general, the estimated economic significance is smaller than in the case of NIMs.

The use of derivatives likely explains some differences across banks in the sensitivity of their ROA to interest rates.6 Some banks use interest rate derivatives to reduce mismatches in the duration of their assets and liabilities. For example, a positive duration gap between loans and deposits can be offset with an interest rate swap to receive floating rates

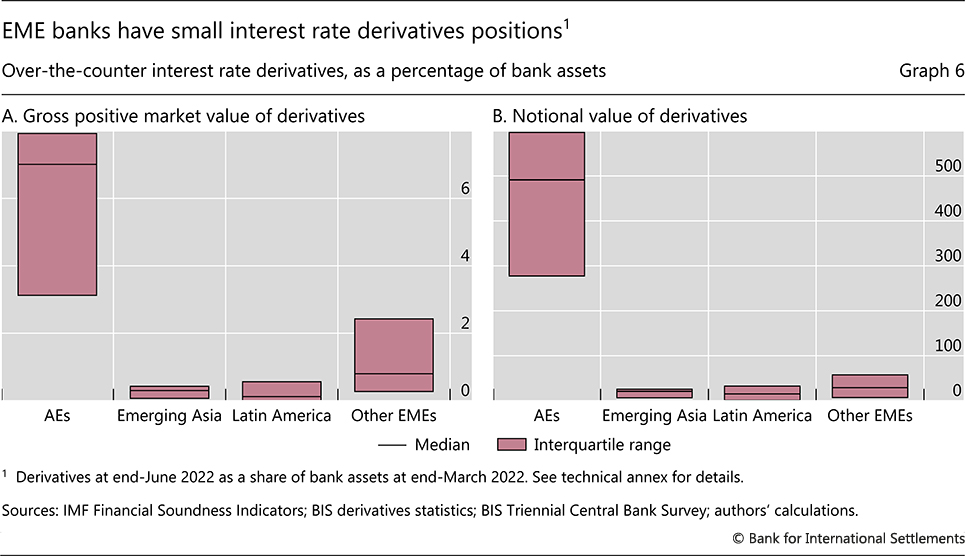

The use of interest rate derivatives is much greater among banks in AEs, particularly large complex entities, than among those in EMEs. For the median AE banking system, the gross market value of interest rate derivatives was equivalent to almost 7% of total assets in early 2022 (Graph 6.A). Their notional value was about five times larger than total assets (Graph 6.B). By contrast, derivatives were a much smaller proportion of EME banks' assets. Banks in Czechia and South Africa were notable exceptions, with relatively large interest rate derivatives positions. Not coincidentally, these two countries also have deep interest rate derivatives markets (Box A).

Interest rate risk and securities holdings

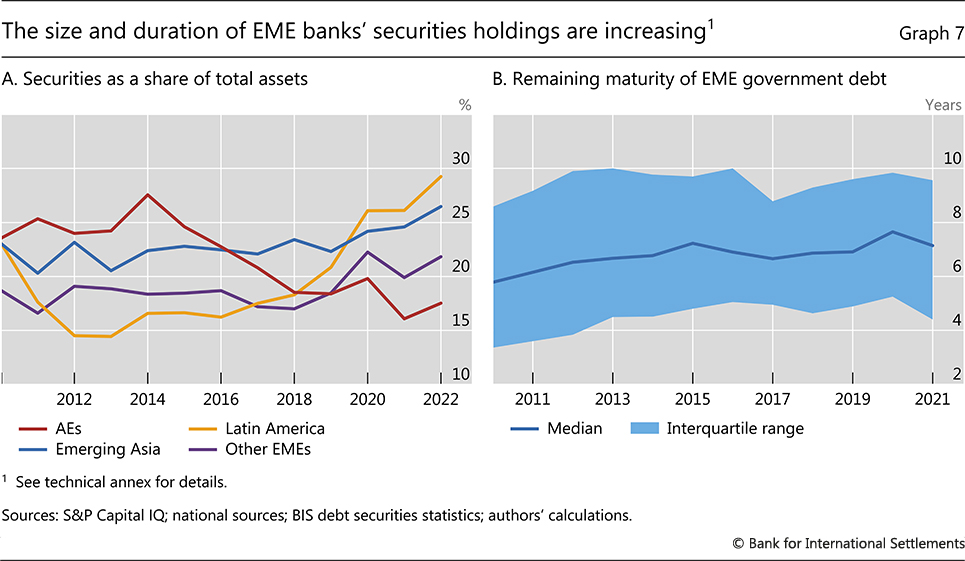

For EME banks, valuation losses arising from interest rate moves were not, historically, a significant source of exposure to IRR. However, this is changing as the size and duration of their securities holdings increase.

The share of securities in total assets has trended up at EME banks in recent years and has significantly exceeded that at AE banks since the Covid-19 crisis (Graph 7.A). For EME banks, this share rose as they stepped in to absorb the increased supply of government debt. Meanwhile, AE banks' share declined as central banks increased their bond holdings through large-scale asset purchases. In 2022, securities accounted for almost 30% of assets at banks in Latin America, 26% in emerging Asia and 22% in other EMEs, compared with 17% in AEs.

Further reading:

In some cases, along with a higher share of securities, the duration of EME banks' holdings increased, as governments extended the maturity of their debt.7 The maturity of outstanding government bonds in the median EME increased from less than six years in 2010 to more than seven in 2021 (Graph 7.B).

The increasing size and duration of EME banks' securities holdings change the nature of their IRR exposure. In particular, they increase the importance of hedging the impact of interest rate changes on other (non-interest) sources of income. These impacts are more effectively hedged by managing the interest rate sensitivity of the entire portfolio rather than matching specific repricing buckets, ie minimising duration gaps rather than repricing gaps.

Moreover, valuation losses are an important channel through which IRR exposures can become intertwined with funding risks. For example, Silicon Valley Bank had accumulated significant unrealised losses on its securities holdings, and the prospect of realising these losses to meet funding outflows raised solvency concerns that eventually precipitated a depositor run. To the extent that EME banks value their securities portfolios at market prices – which many do (IMF (2023)), not least as a result of supervisory guidance – they need to recognise and address losses promptly and thus the interaction of IRR and funding risk is likely to play out differently.

Conclusions

Net interest income accounts for a high share of EME banks' total income, and they manage the impact of IRR on their net interest income by holding assets and liabilities that reprice frequently. In particular, EME banks extend loans with floating rates or short maturities, mainly to businesses. This limits the repricing gaps with time deposits on which EME banks rely heavily for funding.

As balance sheets become more complex and business models change, hedging the impact of interest rate changes on non-interest sources of income and net worth might become more challenging. Securities already account for a large share of EME banks' assets, increasing their exposure to valuation losses. The duration of banks' assets is also likely to increase as mortgage markets develop, and fee income is likely to expand as asset management grows. This would increase the heft of IRR exposures that are inherently difficult to hedge by minimising repricing gaps.

Interest rate derivatives are a flexible tool for managing IRR, but these markets are still poorly developed in many EMEs. Interest rate derivatives markets in many EMEs lack the depth that banks might need in order to meet an increase in their hedging demand. At the same time, banks' limited participation so far is an important reason why these markets remain illiquid and small (Acharya (2018)). Removing obstacles to foreign participation in local derivatives markets can propel their development (Box A).

References

Acharya, V (2018): "Understanding and managing interest rate risk at banks", speech at the Fixed Income Money Markets and Derivatives Association Annual Dinner, Mumbai, 15 January.

Altavilla, C, M Boucinha and J Peydró (2018): "Monetary policy and bank profitability in a low interest rate environment", Economic Policy, vol 33, October.

Bank for International Settlements (BIS) (2023): "Navigating the disinflation journey", Annual Economic Report 2023, Chapter I.

Bank of Korea (2022): Financial markets in Korea, July.

Basel Committee on Banking Supervision (BCBS) (2019): "Interest rate risk in the banking book", The Basel Framework, no SRP31, December.

Borio, C, L Gambacorta and B Hofmann (2017): "The influence of monetary policy on bank profitability", International Finance, vol 20, spring.

Caballero, J, A Maurin, P Wooldridge and D Xia (2022): "The internationalisation of EME currency trading", BIS Quarterly Review, December, pp 49–65.

Claessens, S, N Coleman and M Donnelly (2018): ""Low-for-long" interest rates and banks' interest margins and profitability: cross-country evidence", Journal of Financial Intermediation, vol 35, July.

Coelho, R, F Restoy and R Zamil (2023): "Rising interest rates and implications for banking supervision", FSI Briefs, no 19, May.

Committee on the Global Financial System (CGFS) (2018): "Financial stability implications of a prolonged period of low interest rates", CGFS Papers, no 61.

Drechsler, I, A Savov and P Schnabl (2021): "Banking on deposits: maturity transformation without interest rate risk", Journal of Finance, vol 76, no 3, June.

Hardy, B and S Zhu (2023): "Covid, central banks and the bank-sovereign nexus", BIS Quarterly Review, March, pp 55–69.

Huang, W and K Todorov (2022): "The post-Libor world: a global view from the BIS derivatives statistics", BIS Quarterly Review, December, pp 19–32.

IMF (2023): "A financial system tested by higher inflation and interest rates", Global Financial Stability Report, April.

Technical annex

The analysis in this feature is based mainly on bank-level data from the SNL module of S&P Capital IQ. The sample comprises entities classified by SNL as banks, credit unions, mutuals, mortgage banks or mortgage brokers. Banks for which key balance sheet items, such as total assets, are missing or discontinuous are excluded. Countries where data for fewer than five banks are available are excluded. Whenever feasible, data refer to banks' local operations in a country, ie unconsolidated data, or data at the lowest level of consolidation. The full sample comprises 4,185 banks from 43 countries over the 2010–22 period.

The estimates shown in Graphs 3 and 5 are computed from bank-level regressions of changes in NIMs or ROA on changes in short-term interest rates and term spreads, following Drechsler et al (2021). Regressions on NIMs cover 1,239 banks in 33 countries, and on ROA 1,639 banks in 41 countries. Data are quarterly from Q1 2010 to Q4 2022, although availability varies by bank. The short-term rate refers to the quarterly average of the three-month interbank rate where available; otherwise the three-month local currency government bond yield (in BE, DE, ES, FR, GR, IN, IT, NL, PH and PT) or one-year yield (in AT, FI and IE). The term spread refers to the 10-year government yield minus the short-term rate. The regressors include all lags between zero and three, as well as a constant and bank-level fixed effects. Graphs 3 and 5 show the significance at the 95% level and the sum of coefficients on all four lags.

Aggregates in Graphs 2.C, 4 and 7.A are computed by first taking asset-weighted medians across banks in each country and then the median across countries in a region. Aggregates in Graphs 2.A and 2.B and the denominators used in Graphs 6.A and 6.B refer to banking system data from the IMF Financial Soundness Indicators.

Countries are grouped into regions as follows: AEs (20) = AT, AU, BE, CA, CH, DE, DK, ES, FI, FR, GB, IE, IT, JP, NL, NO, NZ, PT, SE and US; emerging Asia (10) = CN, HK, ID, IN, KR, MY, PH, SG, TH and TW; Latin America (6) = AR, BR, CL, CO, MX and PE; and other EMEs (7) = CZ, HU, IL, PL, SA, TR and ZA. Owing to data availability, some countries are excluded from the regional aggregates shown in some graphs.

Graph 2.A: Excluded: JP and NZ for AEs; HK and TW for emerging Asia.

Graph 2.B: Excluded: AT, JP and NZ for AEs; HK, SG and TW for emerging Asia.

Graph 2.C: Excluded: AR. IL, IN, SA and ZA start in 2011; JP in 2012.

Graph 3: Excluded: AU, BE, FR, GB and IE for AEs; HK and SG for emerging Asia; AR for Latin America; HU and ZA for other EMEs.

Graph 4.A: Excluded: JP and US for AEs. IL starts in 2012, IN in 2013. AR stops in 2021.

Graph 4.B: Excluded: JP and US for AEs. IN starts in 2011. IT stops in 2019.

Graph 4.C. Excluded: FI and SE for AEs. TR for other EMEs: IN starts in 2011, JP in 2012.

Graph 5: Excluded: SG for emerging Asia, AR for Latin America.

Graph 6.A: Excluded: AT, BE, JP, NO and NZ for AEs; HK, ID, PH, SG and TW for emerging Asia; CZ and IL for other EMEs.

Graph 6.B: Excluded: AT, BE, JP, NO and NZ for AEs; HK, PH, SG and TW for emerging Asia; CZ for other EMEs.

Graph 7.B: EMEs = AR, BR, CL, CO, CZ, HK, HU, ID, IL, IN, KR, MX, MY, PE, PH, PL, RU, SA, SG, TH, TR, TW and ZA.

1 The authors thank Douglas Araujo, Claudio Borio, John Caparusso, Stijn Claessens, Rodrigo Coelho, Renzo Corrias, Jon Frost, Ulf Lewrick, Benoit Mojon, Noel Reynolds, Hyun Song Shin, Nikola Tarashev, Christian Upper, Goetz von Peter, Raihan Zamil and Sonya Zhu for valuable comments and discussion. The views expressed in this feature are those of the authors and do not necessarily reflect those of the Bank for International Settlements.

2 In line with the BIS's country groupings, the following 11 economies are categorised as AEs: Australia, Canada, Denmark, the euro area, Japan, New Zealand, Norway, Sweden, Switzerland, the United Kingdom and the United States. All other economies covered in this feature are categorised as EMEs. These groupings are intended solely for analytical convenience and do not represent an assessment of the stage reached by a particular country in the development process.

3 The interest rate sensitivity of yields on a bank's assets and liabilities is also influenced by competition in loan and funding markets.

4 The accounting and regulatory treatment of valuation gains and losses differs across jurisdictions, and sometimes even across banks within the same jurisdiction (Coelho et al (2023)). Under International Financial Reporting Standards, instruments held for trading are valued at fair value and valuation changes are recognised in non-interest income. Instruments available for sale are also valued at fair value but valuation changes are recognised only in equity. Instruments held to maturity are valued at amortised cost as long as they remain in this category.

5 Based on loan-level data from Capital IQ on borrowing by non-financial firms.

6 This assumes that gains and losses on derivatives are recorded in non-interest income. If the requirements for hedge accounting are met then they can be recorded as a component of equity.

7 Higher holdings of government debt also tightened the sovereign-bank nexus. This has contributed to an increase in the correlation between bank and sovereign credit default swaps in EMEs since the Covid-19 crisis (Hardy and Zhu (2023)).