Achievements and challenges in ESG markets

Financial markets can support the transition to a more sustainable and fairer economy by influencing firms' funding costs. To explore this mechanism, we study the extent to which investors respond to signals about the environmental or social benefits stemming from given projects or firms. We find evidence of a carbon risk premium: debt from entities with a higher carbon footprint trades at marginally higher yields, all else the same. We also document that investors are willing to pay a social premium – which we refer to as "socium" – when a firm issues a social rather than a conventional bond. The magnitudes of the carbon risk premium and socium are modest but non-negligible in some industrial sectors and market segments. Some obstacles – such as "ESG washing" – stand in the way of further ESG market deepening, limiting contributions to sustainable development. 1

JEL classification: Q01, Q5

Climate change and rising concerns over social issues have put the spotlight on the environmental costs and social disparities generated by economic activity. While climate-related concerns were first to come to the fore, the Covid pandemic has drawn attention to social considerations.

Financial markets – and in particular the markets for assets with environmental, social and governance (ESG) benefits – can play a key role in mitigating environmental externalities and social disparities. ESG markets have the potential to influence the allocation of economic resources by adjusting firms' funding costs. For this mechanism to work well, two conditions need to be met. First, there needs to be reliable information about the ESG benefits generated by projects and firms. Second, investors need to be responsive to this information.

Given such potential, policymakers have joined the general public in encouraging market participants to support the transition to a sustainable economy. For example, the Network for Greening the Financial System (NGFS) – representing 100 central banks and supervisory authorities – explicitly seeks to "mobilise capital for green and low-carbon investments in the broader context of environmentally sustainable development".

Key takeaways

- Bonds from firms with higher carbon emissions tend to trade at marginally higher risk-adjusted yields, with the size of this carbon premium being larger for firms within energy-intensive sectors.

- Investors are willing to pay a premium at issuance for social rather than conventional bonds denominated in the US dollar or the euro: a "socium", which corresponds on average to more than a one-notch credit rating upgrade.

- Ensuring that ESG markets rest on robust foundations, which include reliable taxonomies, is essential for their contribution to sustainable development.

This special feature explores two questions related to financial markets' role in the transition to a more sustainable and fairer economy. Is there evidence that market participants respond to signals about the environmental and social benefits of projects or firms? What are the major roadblocks standing in the way of further ESG market development, and what are some possible solutions?

Our main contribution is novel empirical evidence on whether financial markets reward activity with perceived ESG benefits and penalise actions perceived to be harmful. In particular, we add to the fast-growing literature on climate risk in financial markets (see Giglio et al (2021) for a review) with evidence on the pricing of this risk in corporate bond markets. We are also among the first to shed light on whether bond markets pay attention to social issues.

We highlight three takeaways. First, we find that bonds issued by "browner" firms – those with higher carbon emissions – tend to trade at marginally higher yields on secondary markets after adjusting for credit risk. This probably reflects the preference of environmentally responsible investors. That said, the magnitude of the impact – the so-called carbon risk premium – is generally quite small and reaches non-negligible levels only for firms in energy-intensive sectors.

Second, we show that social bonds denominated in the US dollar or the euro have been issued at a price premium compared to standard bonds. There is thus a social premium – which we refer to as "socium" – in a market segment that grew more than fivefold between 2019 and 2021.2 On average, the socium corresponds to a rating upgrade of more than one notch.

Third, we emphasise the importance of reliable information for ensuring that ESG markets rest on robust foundations. We review roadblocks undermining trust in ESG designations and possible solutions, including efforts already under way.

This special feature is organised as follows. We first provide an overview of ESG markets. We then discuss how investors respond to signals about projects' or firms' role in environmental and social issues. We conclude by highlighting the importance of reliable ESG information for ESG market development.

ESG markets: an overview

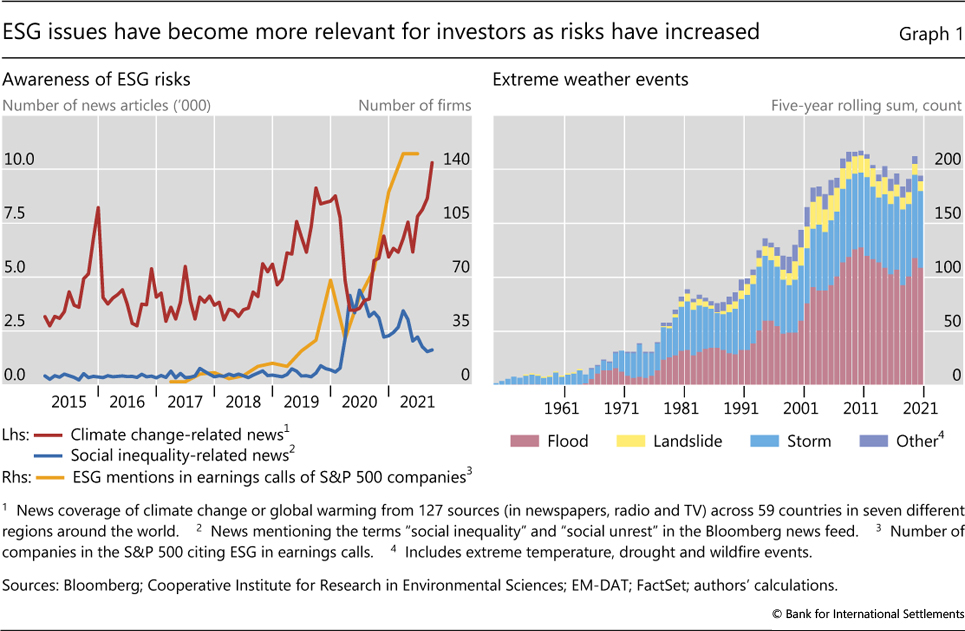

Awareness of environmental and social issues has been rising in recent years. Overall, the broad ESG topic has become more relevant for investors, with the term "ESG" increasingly mentioned in large companies' earnings calls (Graph 1, left-hand panel).

This partly reflects mounting environmental risks associated with climate change.3 As a result of rising global temperatures, adverse weather events have become more frequent over the past three decades (Graph 1, right-hand panel). In addition to these physical risks, climate change also poses transition risks – which are related to regulatory measures, changes in consumer preferences or technology that may impair the viability of particular sectors.

At the same time, the Covid-19 pandemic has highlighted the pervasiveness of social disparities. For instance, firms receiving public support have come under scrutiny over their labour practices.4 More generally, there is evidence that investors are paying increasing attention to social issues in the post-pandemic world.5

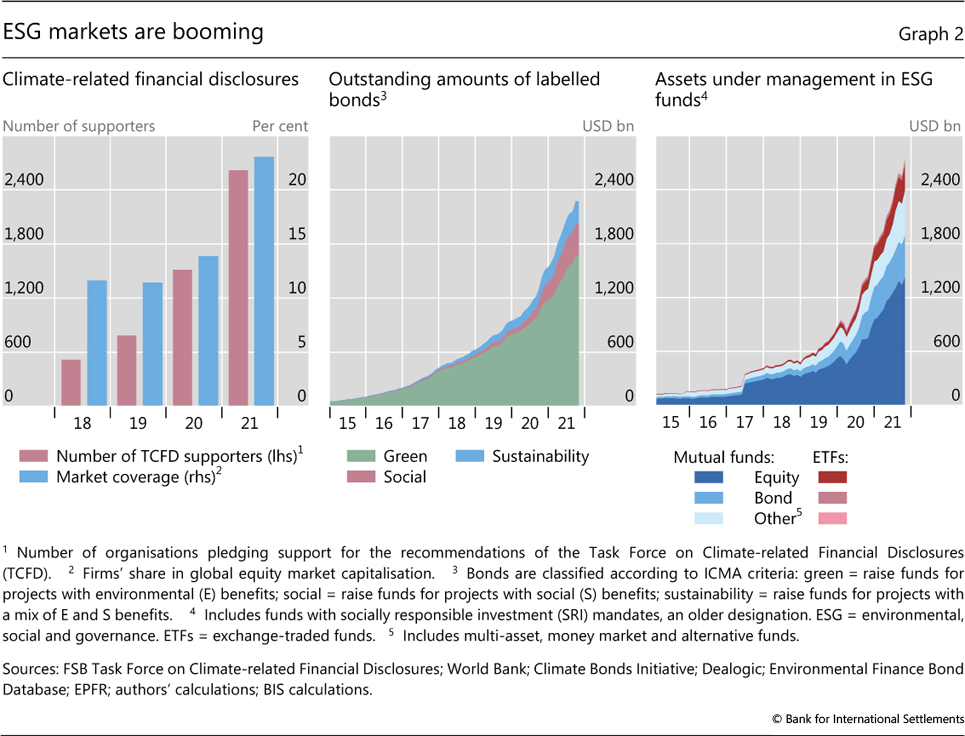

In parallel, a growing number of private and public initiatives have emerged to foster sustainable finance – investment products and services that intend to support the transition to a more sustainable and fairer economy. Many of these initiatives focus on improving investors' information about the ESG benefits generated by projects and firms (see Box A for examples).6 Some manifest themselves as a rising number of entities supporting climate-related risk disclosures: a fivefold increase since 2018 (Graph 2, left-hand panel). There are also efforts to mobilise private and public capital in support of broad ESG goals.

Against this backdrop, the markets for ESG assets are booming. The outstanding amount of "labelled" bonds – use-of-proceeds bonds to finance projects with environmental or social benefits – has risen more than tenfold over the past five years, and now stands at more than $2 trillion.7 Green bonds account for the lion's share of this amount (Graph 2, centre panel). Assets under management (AUM) in funds that self-identify as having ESG mandates have also grown manyfold over the last five years, and now stand at about $2.4 trillion (right-hand panel). ESG mutual funds hold mostly equities (more than 60% of AUM), followed by bonds (around 20%).

The footprint of retail investors in the ESG fund segment is rising, as indicated by the growing AUM of passive funds (ETFs). Like mutual funds, ESG ETFs also focus primarily on equities.

Market developments also reflect the increased prominence of social issues since the outbreak of the Covid-19 pandemic. Social bond issuance has surged recently, with outstanding amounts growing more than fivefold between 2019 and 2021 (Graph 2, centre panel). Such securities tend to be issued by supranationals (33% of total amounts outstanding), sovereigns, government agencies and development banks (46%), as well as corporates (21%). Most social bonds are issued in either the euro (67%) or the US dollar (15%).

In interpreting these market developments, it is necessary to keep in mind that the term "ESG assets" covers a wide range of investment products, with a universally accepted, standardised classification yet to emerge. For instance, the ESG designation can be self-attributed by the very firms issuing securities (eg labelled bonds) or by asset managers marketing their investment products.8 Alternatively, the designation may be assigned by a specialised provider of ESG ratings, with firms' voluntary disclosures providing a key input. When it comes to exposures to climate-related transition risks, such providers and investors seem to be converging on disclosed carbon emissions as a reasonable proxy.9 But there is no similar metric when social aspects are involved.

ESG preferences and the cost of debt

ESG markets have the potential to reallocate resources to economic activities that generate fewer environmental externalities and social disparities. A precondition for this mechanism to work is that market participants respond to information about the extent to which a given asset is associated with such activities. Part of this response may have to do with the information's relevance for assessing the asset's riskiness, ie if assets yielding such benefits are perceived as less risky, all else equal. In addition, the response may work through a preference channel. Investors committed to supporting sustainability goals might have a preference, all else the same, for assets that they perceive as helping to achieve those goals.10

We look for empirical evidence that the preference channel matters – over and above any risk considerations – for the costs of debt finance in two ESG market segments. In E space, we study the impact of a firm's carbon footprint on its borrowing costs, which we approximate with secondary market bond yields. In S space, we examine how the "social bond" label affects a bond's yield at issuance (primary market).

The preference channel and the relative cost of debt in E space

Is there a carbon risk premium in corporate bond markets – one of the main sources of firm financing? In other words, do investors demand a higher yield when trading bonds issued by corporations with heavier carbon footprints? To answer this question, we measure a firm's carbon footprint through its carbon emissions11 and use secondary market corporate bond yields to gauge investors' response.12 We then analyse the relationship between the two while controlling for credit risk and other bond characteristics.

Our data set is as follows. We gather data on both direct and indirect carbon emissions from Trucost. Direct emissions refer to emissions from production (also known as "scope 1"). Indirect emissions refer to those coming from the consumption of purchased electricity, heat or steam ("scope 2").13 For bond pricing, we use secondary market quotes of option-adjusted spreads, provided by Refinitiv. We assume that estimates of five-year probabilities of default (PD), provided by Bloomberg, capture investors' perceptions of credit risk. We thus use these estimates to abstract from the risk channel and focus on the preference channel. Our analysis focuses on US and EU companies and bonds issued by them. Box B provides further detail on our empirical setup and reports additional results.

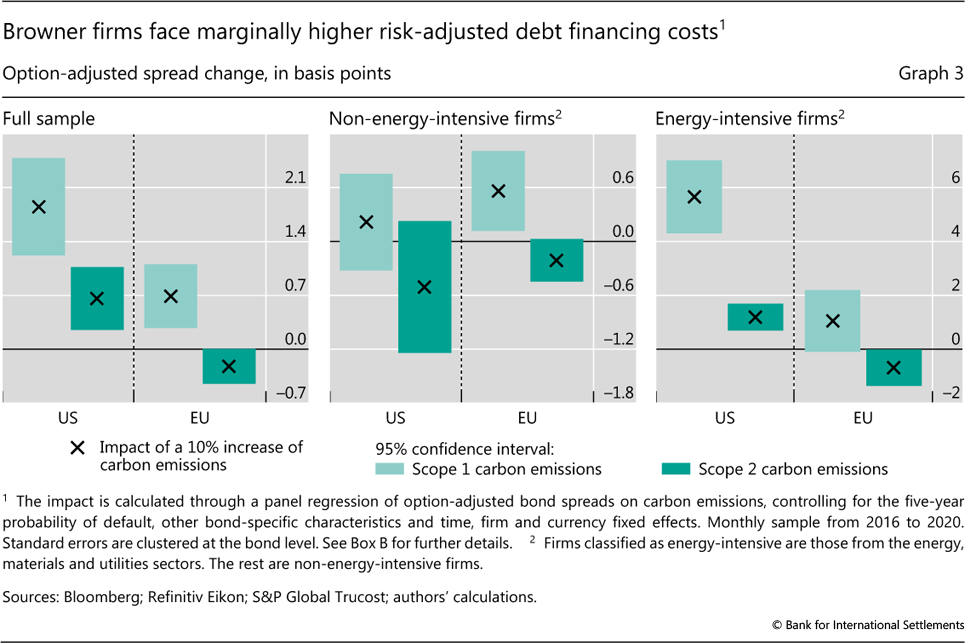

Considering firms in all sectors, we find that bonds issued by those with more carbon emissions ("browner" firms) tend to have statistically higher risk-adjusted spreads, even though the difference is economically negligible (Graph 3, left-hand panel). Through the preference channel, a 10% increase in direct carbon emissions would lead to an increase of 2 basis points in corporate bond spreads for US bonds and 0.7 basis points for EU bonds (Graph 3, left-hand panel). These results are orders of magnitude smaller than the median spread in our sample, at 115 basis points. The impact of indirect emissions is even smaller, at 0.7 basis points and effectively zero for US and EU bonds, respectively.

That said, zooming in on firms in energy-intensive sectors – which we define as energy, materials and utilities – reveals more material effects through the preference channel. Indeed, the overall results are heavily influenced by other firms, whose carbon emissions do not have a significant impact on their risk-adjusted spreads (Graph 3, centre panel). By contrast, the impact within the set of energy-intensive firms is not only statistically significant but also of non-negligible economic importance (right-hand panel). In the case of US bonds in particular, a 10% increase in direct carbon emissions would translate to a 6 basis point increase in spreads, which corresponds to a rating deterioration of 0.3 notches.14 The differentiated impact across industries probably reflects investors' greater scrutiny of firms traditionally viewed as brown.

Taken together, we find some evidence supporting the presence of a preference channel in E space. However, the economic impact is rather small. This could be because the supply-demand imbalances arising from investors' preferences are not large enough to offset arbitrage forces that reflect purely financial considerations.

The preference channel and the relative cost of debt in S space

Might investors value the social label enough to pay a premium for holding social rather than conventional bonds? In other words, is there a socium?

To answer this question, we match social bonds issued by banks and corporates between 2016 and 2021 with conventional securities that share similar risk characteristics.15 For each matched pair, we compute the socium as the yield spread between the social and conventional bond at issuance (that is, on primary markets). We carry out the analysis at the security level because there is no equivalent to carbon emissions in S space: market participants have not yet converged on a set of metrics capturing the social benefits generated at the firm level.16

Further reading

- Aramonte S, Zabai A (2021): Sustainable finance: trends, valuations and exposures, BIS Quarterly Review, September.

- Ehlers T, Mojon B and Packer F (2020): Green bonds and carbon emissions: exploring the case for a rating system at the firm level, BIS Quarterly Review, September.

- Ehlers T, Packer F and de Greiff K (2021). The pricing of carbon risk in syndicated loans: which risks are priced and why?, BIS Working Paper No 946.

In matching bonds, we use several criteria in the spirit of Larcker and Watts (2020) and Flammer (2021). We first try to match the social bond with a conventional bond that is issued by the same firm. Within that firm, we look for a bond with the same rating as and a similar remaining maturity to the social bond at the time of data retrieval. If several such bonds exist, we pick the one whose issuance date is closest to the social bond's. Conversely, if no such bond exists, we look for a security that is issued by a firm in the same sector as the social bond issuer and has similar characteristics to the social bond (again, credit rating and maturity).

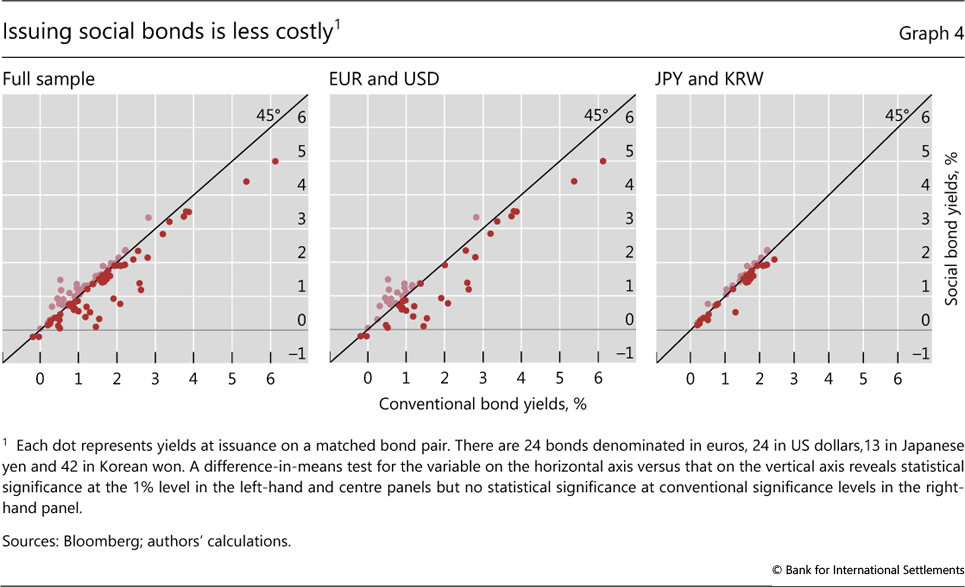

We find that investors are indeed willing to pay a socium. That is, social bond yields at issuance are systematically lower than the yields on conventional bonds (Graph 4, left-hand panel). The mean socium in the full sample is statistically significant, at approximately 12 basis points. To gauge the economic significance of this estimate, we express it in "rating-notch equivalents" following Baker et al (2018).17 We find that the average socium corresponds to a rating upgrade of about 1 to 1.5 notches. The results are in line with market intelligence reporting that social bond issues are oversubscribed (Bloomberg (2021)) – enough investors have a preference for these assets to affect their issuance price.

We next investigate whether the socium is currency-specific. To date, most corporate social bonds have been issued in euros (41% of amount outstanding), followed by US dollars (23%), Japanese yen (16%) and Korean won (10%). Corporate issuance in euros is associated with companies domiciled in the European Union (95%), whereas about a third of dollar-denominated issuance has taken place outside the United States. We split the sample by currency: one subsample includes bonds issued in euros and dollars, the other in yen and won.18 For the first subsample, we find the same average socium as in the overall sample: 21 basis points (Graph 4, centre panel). By contrast, there is no socium for securities denominated in won or yen (right-hand panel).

Taken together, our results in E and S space suggest that investors do respond to signals stemming from carbon footprint data and bond labels. While some of the effects are extremely small at present, ESG markets hold the potential to influence the allocation of economic resources.

Concluding observations

For ESG markets to support the transition to a more sustainable and fairer economy, it is not enough that investors respond to environmental and social signals. Another prerequisite is that these signals provide accurate ESG information.

Whether booming ESG markets rest on solid foundations remains an open question, not least because of growing concerns about "ESG washing" – that is, a misleading attribution of the ESG designation. These concerns are stoked by the absence of universal taxonomies and standardised, mandatory disclosures. For instance, ESG ratings are provided by a small group of agencies, which disagree as to how to interpret firms' voluntary ESG disclosures (Berg et al (2019)).19 This indicates uncertainty about the ESG benefits reaped by retail investors piling into ETFs that rely on specific ESG ratings (Graph 2, right-hand panel). Similar concerns apply to the nascent ESG derivatives market, and in particular its index segment.20

Another issue is that the current ESG designation system might fail to align incentives with broad environmental goals at the level where decisions are made – the firm. This is particularly relevant when the designation is at the level of a security (ie labelled bonds). Green bond labels are a case in point. For these labels to imply emission reductions,21 the attendant projects would have to have a radical impact on the activities of the bond issuer. However, issuance of green bonds does not necessarily indicate a material reduction in carbon intensities at the firm level over time (Ehlers et al (2020)).

Any ESG designation needs to rest on a reliable taxonomy. Accordingly, some jurisdictions, notably China and the European Union, have already developed and adopted sustainable finance taxonomies, while others are taking steps in that direction (eg Canada, the United Kingdom). Classification systems have also emerged from the private sector (eg the Climate Bonds Taxonomy). The emerging consensus (G20 (2021)) is that, in an effective classification system, ESG assets will be those whose environmental and social benefits are material and consistent with broader sustainability goals (eg as set out in the Paris Agreement or the UN Sustainable Development Goals).

It is also important to standardise ESG taxonomies and make them comparable across countries. This is high on the policy agenda, as indicated by the G20's Sustainable Finance Roadmap and by the priorities of COP 26. Some progress has already been made on this front. The European Commission and the People's Bank of China recently released their Common Ground Taxonomy, which identifies a set of economic activities recognised as environmentally sustainable by both the EU's and China's own classification systems.

Reliable taxonomies rest on reliable and informative metrics, which are still in the making. The metrics employed to quantify ESG benefits should be science-based (for environmental benefits) or fact-based and verifiable (for social and other benefits). While carbon emissions may be a reasonable proxy for the environmental benefits associated with firms, open questions remain concerning carbon accounting for sovereign or supranational issuers. Importantly, investors have not yet agreed on how to quantify social benefits (ADB (2021)). Given the multifaceted nature of social issues, it is likely that the quantification process will have to rely on a menu of (possibly ad hoc) metrics rather than a single indicator.

References

Asian Development Bank (2021): Primer on social bonds and recent developments in Asia, February.

Baker, M, D Bergstresser, G Serafeim and J Wurgler (2018): "Financing the response to climate change: the pricing and ownership of US green bonds", NBER Working Papers, no 25194, October.

Basel Committee on Banking Supervision (2021): Principles for the effective management and supervision of climate-related financial risks, November.

Basirov, A, F Fontan and A Gourc (2020): "2020 vision: social bonds and the S in ESG", BNP Paribas, 2 September.

Berg, F, J Koelbel and R Rigobon (2019): "Aggregate confusion: the divergence of ESG ratings", MIT Sloan School Working Papers, no 5822-19, August.

Bloomberg (2021): "Do-good' bonds promise social change investors take on faith", 11 February.

Bolton, P and M Kacperczyk (2021): "Global pricing of carbon-transition risk", NBER Working Papers, no 28510, February.

Boubakri, N and H Ghouma (2010): "Control/ownership structure, creditor rights protection, and the cost of debt financing: international evidence", Journal of Banking & Finance, vol 34, no 10, pp 2481–99.

Ehlers, T, B Mojon and F Packer (2020): "Green bonds and carbon emissions: exploring the case for a rating system at the firm level", BIS Quarterly Review, September, pp 31–47.

Ehlers, T and F Packer (2017): "Green bond finance and certification", BIS Quarterly Review, September, pp 89–104.

Ehlers, T, F Packer and K de Greiff (2021): "The pricing of carbon risk in syndicated loans: which risks are priced and why?", Journal of Banking & Finance, pp 106–80.

Fields, P, D Fraser and A Subrahmanyam (2012): "Board quality and the cost of debt capital: the case of bank loans", Journal of Banking & Finance, vol 36, no 5, May, pp 1536–47.

Financial Times (2020): "Coronavirus forces investor rethink on social issues", 30 April.

Flammer, C (2021): "Corporate green bonds", Journal of Financial Economics, vol 142, no 2, November, pp 499–516.

Giglio, S, B Kelly and J Stroebel (2021): "Climate finance", Annual Review of Financial Economics, vol 13, pp 15–36.

Gompers, P, J Ishii and A Metrick (2003): "Corporate governance and equity prices", The Quarterly Journal of Economics, vol 118, no 1, February, pp 107–56.

Group of 20 (2021): 2021 Synthesis Report of the Sustainable Finance Working Group, October.

Hong, H, FW Li and J Xu (2019): "Climate risks and market efficiency", Journal of Econometrics, vol 208, no 1, January, pp 265–81.

International Swaps and Derivatives Association (2021): "Overview of ESG-related derivatives products and transactions", Research Notes, January.

Larcker, D and E Watts (2020): "Where's the greenium?", Journal of Accounting and Economics, vol 69, nos 2–3, April–May, article 101312.

Murfin, J and M Spiegel (2020): "Is the risk of sea level rise capitalized in residential real estate?", The Review of Financial Studies, vol 33, no 3, March, pp 1217–55.

Neilan, J, P Reilly and G Fitzpatrick (2020): "Time to rethink the S in ESG", Harvard Law School Forum on Corporate Governance, 28 June.

Pedersen, L, S Fitzgibbons and L Pomorski (2021): "Responsible investing: the ESG-efficient frontier", Journal of Financial Economics, vol 142, no 2, November, pp 572–97.

1 We thank Claudio Borio, Stijn Claessens, Mathias Drehmann, Ingo Fender, Kumar Jegarasasingam, Corrinne Ho, Benoît Mojon, Frank Packer, Hyun Song Shin and Nikola Tarashev for helpful comments and suggestions. We are also grateful to Adam Cap and Anamaria Illes for excellent research assistance and Branimir Gruić and Jakub Demski for help with the sustainable bond database. The views expressed are those of the authors and do not necessarily reflect the views of the Bank for International Settlements.

2 While the carbon risk premium goes to the investor (compensation for bearing higher risk), the socium goes to the issuer (reward for being socially responsible).

3 We abstract from other sources of environmental risks, such as pollution, loss of biodiversity, etc.

4 See Neilan et al (2020) and FT (2020) for a discussion.

5 According to a BNP Paribas survey, 70% of the investors responding after the pandemic's outbreak are concerned with social issues, compared to 50% pre-pandemic. See Basirov et al (2020).

6 The Basel Committee on Banking Supervision (BCBS) is also active in this area. The BCBS has recently published a set of guidance principles for banks on the issue of management of climate-related risks: see BCBS (2021).

7 Issuers typically follow market-based guidelines (eg ICMA principles) to label their bonds, depending on the use of proceeds. Securities issued to finance projects with explicit environmental benefits (eg retrofitting an existing building for energy efficiency) can be labelled as green. Bonds raising funds for projects with specific social benefits (eg providing social housing, delivering affordable basic infrastructure like electricity or sanitation or essential services like access to healthcare or education, supporting employment) can be labelled as social. Sustainable bonds finance projects with a mix of environmental and social benefits. Third-party verification is not required. What is required in addition to disclosing use of proceeds, however, is that the proceeds be ring-fenced for the specific project that the security was issued to finance. Importantly, labelled bonds differ from so-called project bonds in that the cash flows of the former are backed by the entire revenue stream of the issuer.

8 In selecting their investment portfolios, some asset managers follow the UN Principles for Responsible Investment.

9 Physical risks are harder to quantify, not least because they depend in complex ways on firms' geospatial characteristics. Existing literature seems to suggest that physical climate risks are not priced in correctly; see Hong et al (2019) and Murfin and Spiegel (2020) for examples.

10 In the language of Pedersen et al (2021), the preference channel corresponds to "ESG-motivated" investors.

11 We use carbon emissions in tonnes of CO2 instead of carbon intensities (calculated as the ratio of emissions to revenue in USD millions). From an intuitive standpoint, a reduction in emissions intensity may not be consistent with a decrease in total emissions, the ultimate environmental goal. Our choice is consistent with the literature: see Bolton and Kacperczyk (2021) for an example.

12 Even though primary markets provide a more direct gauge of funding costs, secondary markets reflect investors' preferences at a higher frequency. To the extent that there is a reasonable alignment between the two markets (a standard assumption in the related literature), our choice allows us to work with richer information on funding costs.

13 Trucost also provides data on indirect emissions from the production of purchased materials, product use, waste disposal, outsourced activities, etc ("scope 3"). We abstract from scope 3 data because of concerns with the reliability of the underlying reporting.

14 A one-notch rating change corresponds to a change to an adjacent rating, eg from A+ to A. Our result is the average of individual notch changes across all bonds. To estimate each individual notch change, we divide the 6 basis point impact by the difference between two (mean) spreads: that in the bond's credit rating and that in the adjacent rating, one notch below. Our sample is comprised of bonds with ratings ranging from AAA to C on the Fitch scale.

15 Only 10 of the bonds in our sample were issued before 2019.

16 Others have studied the response of corporate bond yields at issuance to the green label with mixed results. Examples include Ehlers and Packer (2017), who find a green issuance premium ("greenium") of 18 basis points, and Flammer (2021), who finds no evidence of a greenium.

17 For each matched pair, we computed the yield spread at issuance between the social and the conventional bond and recorded the credit rating of the conventional bond (based on Bloomberg's composite credit rating) on the coarse scale AAA/AA/A/BBB/BB. When the spread was negative (positive), we divided it by the average yield difference between: (i) an index of bonds with the same rating as the conventional bond; and (ii) an index of bonds with a one-grade higher (lower) rating on the coarse scale. Multiplying this ratio by three (since there are three notches between adjacent grades on the coarse scale) delivers an estimate of the rating upgrade (downgrade) implicit in the social bond's relative yield. The numbers reported in the text are based on averages across the pair-specific estimates of up-/downgrades. The underlying bond index data are from the ICE BofA Global Corporate Index family and cover the past 10 years.

18 We aggregate by relevance of currency denomination in the corporate social bonds market. The euro and the US dollar account for 64% of outstanding amounts. If we split the sample further to isolate bonds issued in euros and dollars we still find evidence of a socium significantly different from zero at the 1% level, but the two subsamples are very small (24 bonds each).

19 Examples of ESG rating agencies include ASSET4 (Refinitiv), , ISS (Deutsche Börse Group), KLD (MSCI Stats), MSCI, RobecoSAM (S&P Global), Sustainalytics, and Vigeo Eiris (Moody's).

20 Global stock exchanges, including Eurex, Intercontinental Exchange (ICE), CME Group, Nasdaq, Chicago Board Options Exchange (CBOE), Euronext and Japan Exchange Group, have introduced equity index futures and options contracts tied to ESG benchmarks (see ISDA (2021)).

21 Green bond labels can signal other environmental benefits than reducing carbon emissions (eg promoting biodiversity or fostering processes that reduce consumption of natural resources).