Stress in European money market funds at the outbreak of the pandemic

European money market funds (EMMFs) were not immune to the acute stress that rocked their US counterparts in March 2020. In several respects, the European developments echoed those in the United States. This box reviews the dynamics of EMMF outflows in the light of the US experience, including the role played by investors of different sizes and the importance of funds' liquidity.

In several respects, the European developments echoed those in the United States. This box reviews the dynamics of EMMF outflows in the light of the US experience, including the role played by investors of different sizes and the importance of funds' liquidity.

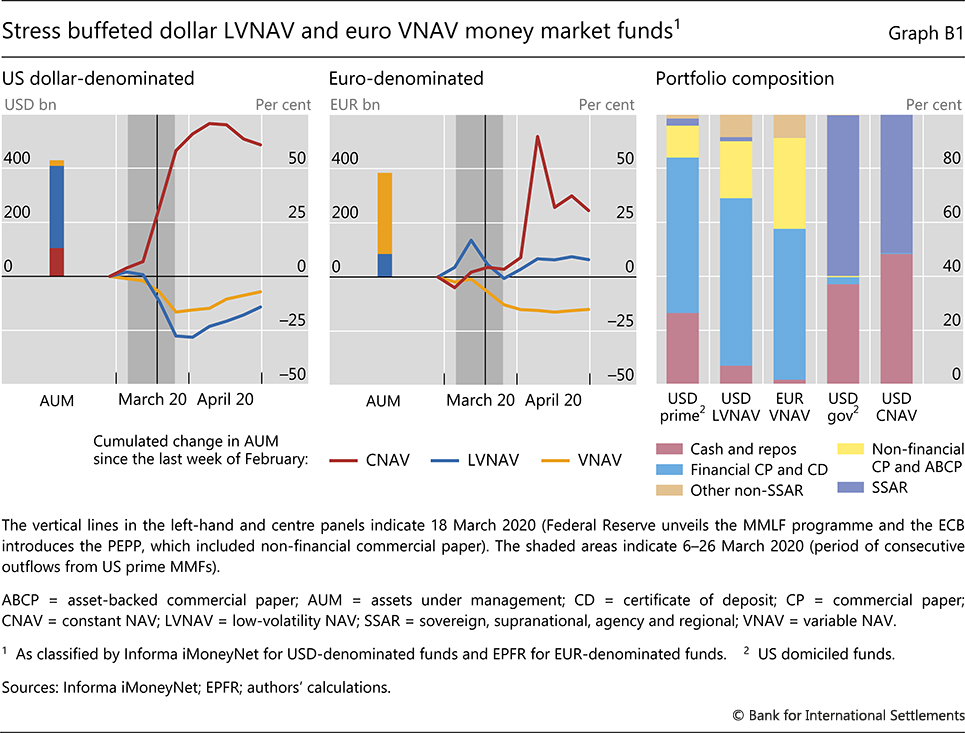

EMMFs can be classified into three main groups: (i) constant net asset value (CNAV); (ii) low-volatility NAV (LVNAV); and (iii) variable NAV (VNAV). While CNAV funds price their portfolios at amortised nominal value, VNAV funds price them at market value. LVNAV funds stand in between: they normally price their portfolios like CNAV funds but must convert into VNAV funds if the volatility of their portfolios' market value exceeds certain thresholds. LVNAV and VNAV funds represent about 90% of EMMFs' overall assets under management (AUM), and they are mainly denominated in US dollars and euros, respectively (Graph B1, left-hand and centre panels, stacked bars). CNAV funds account for the remaining 10% of AUM and are almost entirely denominated in dollars.

The most stressed EMMFs, dollar-denominated LVNAV and euro-denominated VNAV funds, held predominantly non-government securities and had a similar experience to their US counterparts, prime institutional funds. A substantial share of these funds' assets consists of banks' commercial paper and certificates of deposit and, to a lesser extent, short-term debt of non-financial firms (Graph B1, right-hand panel). At the peak of the stress, the dollar LVNAV funds lost almost 30% of their February 2020 AUM (left-hand panel, blue line), representing almost $90 billion. In the euro-denominated segment, the losses of the VNAV funds by the end of March were higher than 15% of pre-stress AUM (centre panel, yellow line), or more than €50 billion. EMMF outflows started broadly at the same time as those in US prime MMFs (left-hand and centre panels, shaded areas). However, while outflows from US prime MMFs ebbed after the Federal Reserve introduced the Money Market Fund Liquidity Facility (MMLF) in late March 2020 (vertical lines), withdrawals from dollar-denominated EMMFs persisted through the end of the month. That probably reflected the fact that the Federal Reserve's liquidity support did not extend to EMMFs. In addition, redemptions continued to trickle out of euro VNAV funds through end-March and until mid-April, as the ECB's new Pandemic Emergency Purchase Programme (PEPP) was picking up momentum.

That probably reflected the fact that the Federal Reserve's liquidity support did not extend to EMMFs. In addition, redemptions continued to trickle out of euro VNAV funds through end-March and until mid-April, as the ECB's new Pandemic Emergency Purchase Programme (PEPP) was picking up momentum.

As investors shifted away from riskier assets, MMFs investing mostly in government securities – CNAV funds in Europe, similar to government funds in the United States – received large inflows. While dollar CNAV funds gained more than 65% of their pre-Covid balances, this was still about $15 billion less than the outflows from other dollar-denominated EMMFs. Similarly, outflows from euro VNAV funds were only minimally captured by euro CNAVs or other euro-denominated EMMFs. All this suggests that a significant portion of EMMF losses may have turned into euro area overnight bank deposits, which saw unusual inflows of about €200 billion in March 2020, and possibly also flowed into US government MMFs, whose AUMs expanded much more than US prime MMFs contracted.

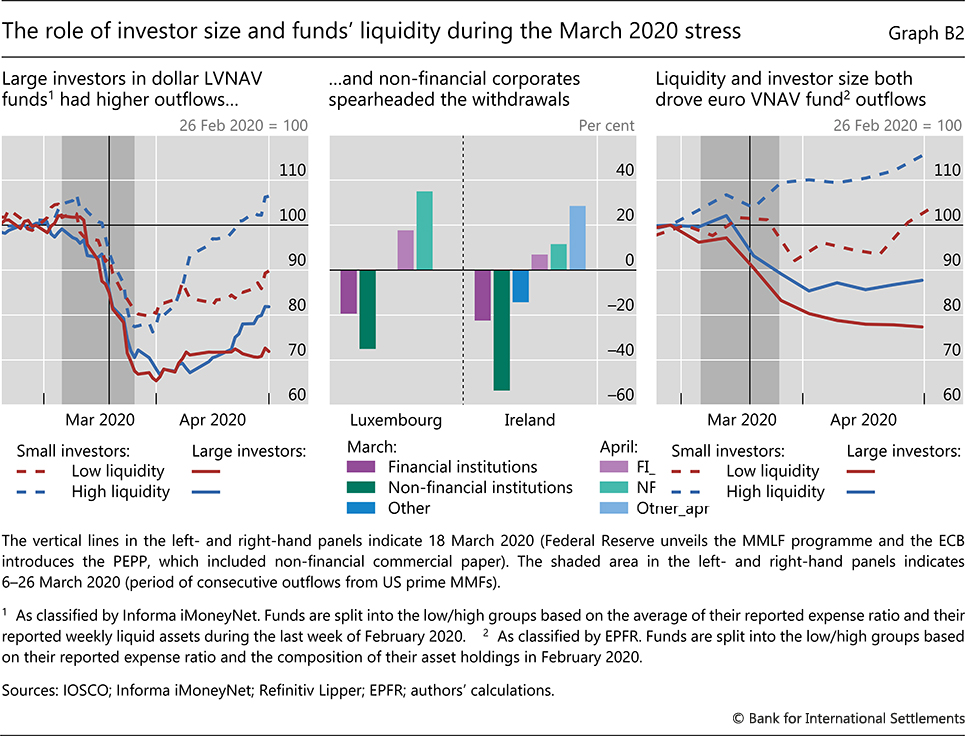

Did funds' investor size and liquidity positions play a role in EMMFs' experience, as was the case for US MMFs? We focus on dollar LVNAV and euro VNAV funds, the two types of EMMFs most affected by the stress, and partition the funds of each type into four groups using two criteria. First, we distinguish funds populated by large or small investors. We do this based on the funds' expense ratio – a common approach in the academic literature. The underlying idea is that MMFs catering to larger investors usually require larger minimum investments, and consequently tend to have lower expense ratios. Second, we differentiate high- from low-liquidity funds, using the portfolio share of their liquid assets in the last week of February 2020. Crossing the two features, we obtain four groups of funds, for which we document the flows in March and April 2020.

Second, we differentiate high- from low-liquidity funds, using the portfolio share of their liquid assets in the last week of February 2020. Crossing the two features, we obtain four groups of funds, for which we document the flows in March and April 2020.

Large investors spearheaded the withdrawals from both European dollar LVNAV funds and US prime funds, although the main players were non-financial corporates in Europe and financial institutions in the United States. By end-March, EMMF withdrawals by large investors exceeded those by smaller investors by about 10% of the pre-shock AUM, irrespective of the funds' underlying liquidity conditions (Graph B2, left-hand panel). Non-financial institutions withdrew more than financial institutions from Luxembourg- and Ireland-domiciled funds. In fact, non-financial investors' redemptions represented between 35 and 53% of their holdings, as opposed to 19 to 22% of financial institutions' holdings (centre panel). This suggests that European outflows were mainly driven by precautionary motives – eg corporate treasurers securing dollar cash balances – in contrast to the need to cover margin calls by financial institutions in the United States.

In fact, non-financial investors' redemptions represented between 35 and 53% of their holdings, as opposed to 19 to 22% of financial institutions' holdings (centre panel). This suggests that European outflows were mainly driven by precautionary motives – eg corporate treasurers securing dollar cash balances – in contrast to the need to cover margin calls by financial institutions in the United States.

In April, the recovery of both European dollar LVNAV and US prime funds were led by small investors, although their liquidity preferences differed across jurisdictions: high-liquidity in Europe and low-liquidity in the United States. In Europe, high-liquidity funds with small investors saw a reversal of their entire March outflows by end-April (Graph B2, left-hand panel, dashed blue line). In the United States, by contrast, low-liquidity prime MMFs were the main recipients of inflows when small investors returned. Low-liquidity EMMFs recorded a relatively tepid recovery, with little regard for their typical investor's size (solid and dashed red lines). A possible reason is that, as already noted, dollar-denominated European funds did not benefit from the backing of the Federal Reserve's MMLF programme.

Low-liquidity EMMFs recorded a relatively tepid recovery, with little regard for their typical investor's size (solid and dashed red lines). A possible reason is that, as already noted, dollar-denominated European funds did not benefit from the backing of the Federal Reserve's MMLF programme.

Turning to euro VNAV funds, large investors again spearheaded withdrawals, generally from less liquid funds, while small investors were quicker to return after the turmoil. Funds mostly serving large investors recorded withdrawals of between 20% (low liquidity) and 15% (high liquidity) of their pre-Covid AUM in March. At the same time, funds with small investors saw redemption of less than 10% of pre-shock AUM (low liquidity) or even recorded inflows (high liquidity). In April, funds serving larger investors did not see a noticeable rebound in their AUM, while less liquid funds catering to smaller investors fully recovered their losses.

The views expressed are those of the authors and do not necessarily reflect the views of the BIS. There are several studies of the March 2020 stress in US prime money market funds, eg F Avalos and D Xia, "Investor size, liquidity and prime money market fund stress", BIS Quarterly Review, March 2021; M Cipriani and G La Spada, "Sophisticated and unsophisticated runs", Federal Reserve Bank of New York, Staff Reports, no 956, December 2020; L Li, Y Li, M Macchiavelli and X Zhou, "Runs and interventions in the time of Covid-19: Evidence from money market funds", Federal Reserve Board, manuscript. This programme allowed banks to borrow from the Federal Reserve by pledging a wide range of assets purchased from prime and tax-exempt MMFs. Eligible assets included the most distressed ones, such as commercial paper and certificates of deposit. The loans to the participating banks were given on a non-recourse basis (ie banks did not bear credit risk) and were exempt from regulatory capital requirements. The facility eased the stress by making banks willing buyers of illiquid assets, thus providing liquidity to MMFs to meet redemptions. In so doing, it reduced investors' pre-emptive withdrawals. The PEPP was announced on 18 March 2020 and implemented on 24 March 2020, when the minimum remaining maturity of eligible non-financial commercial paper for both the PEPP and the Corporate Sector Purchase Programme was reduced from six months to 28 days. L Schmidt, A Timmermann and R Wermers, "Runs on money markets mutual funds", American Economic Review, vol 106, no 9, 2016. The expense ratio measures the operational costs of an investment fund (eg management, shareholder services and other administrative fees). The investor pays these costs through a reduction in the investment's rate of return. The four groups include a relatively balanced number of funds. In the euro VNAV segment, there are 51 funds managing $212 billion in the large investor-low liquidity group, 38 funds managing $13 billion in the small investor-low liquidity group, 37 funds managing $56 billion in the large investor-high liquidity group, and 49 funds managing $13 billion in the small investor-high liquidity group. The corresponding figures for the dollar LVNAV segment are 22 funds managing $92 billion, 30 funds managing $20 billion, 41 funds managing $73 billion, and 34 funds managing $79 billion. Luxembourg and Ireland are the two major jurisdictions hosting dollar-denominated LVNAV funds. See IOSCO, "Money market funds during the March–April episode", IOSCO Thematic Note, November 2020. For a description of the stress in US markets resulting from margin calls, see A Schrimpf, H S Shin and V Sushko, "Leverage and margin spirals in fixed income markets during the Covid 19 crisis", BIS Bulletin, no 2, April 2020. See Avalos and Xia, ibid.