Green bonds: the reserve management perspective

Central banks' frameworks for managing foreign exchange reserves have traditionally balanced a triad of objectives: liquidity, safety and return. Pursuing these objectives involves explicit trade-offs. Recently central banks have shown interest in incorporating environmental sustainability objectives into their reserve management frameworks. Rather than a triad, central banks may analyse (and weigh) a tetrad of reserve management objectives in allocating part of their foreign exchange reserves to green bonds.1

JEL classification: E58, F31, G11, G17.

Central banks are playing an increasingly active role in promoting the move towards a sustainable global economy (Carney (2015), ECB (2019)). A pertinent example is the recently established Network for Greening the Financial System (NGFS), which brings together around 40 central banks, supervisory agencies and international financial institutions to develop a coordinated response to climate-related risks in the global financial system (NGFS (2019), Pereira da Silva (2019)).2

Central banks can use various tools to support the greening of the financial system. These range from disclosure requirements and the provision of data to the integration of climate-related risks into financial stability assessments (Volz (2017)). In addition, central banks can help mobilise funds to contribute to the large-scale public sector investment required to reach the goals of the Paris Agreement on climate change. In this context, a key tool is the portfolios of assets that central banks have been entrusted to manage in the context of their countries' exchange rate policies: foreign exchange (FX) reserves.3

Key takeaways

- Central bank reserve managers are considering how to incorporate environmental sustainability objectives into their portfolios.

- Sustainability as a reserve management objective needs to be balanced against liquidity, safety and return.

- Green bonds' safety and return support their incorporation into reserve portfolios, but their accessibility and liquidity currently pose some constraints.

In this feature, we explore how environmental sustainability objectives might fit within central banks' reserve management frameworks. This requires expanding the usual triad of reserve management objectives - liquidity, safety and return - into a tetrad. Using the example of green bonds, we find that sustainable investments can be included in reserve portfolios without forgoing safety and return, although their accessibility and liquidity currently pose some constraints. The results of an illustrative portfolio construction exercise suggest that adding both green and conventional bonds can help generate diversification benefits and, hence, improve the risk-adjusted returns of traditional government bond portfolios.

Further reading

The feature is organised as follows. The next two sections explore how sustainability considerations can be integrated into the reserve management framework. The following section examines green bonds' liquidity, safety and return and assesses their diversification benefits. The final section concludes.

Reserve management process

Any debate about whether FX reserves can be employed to pursue sustainability objectives traces back to a discussion of the purposes for holding reserves. Historically, the objective behind reserve accumulation has been to assure markets that the national authorities can meet their external financial obligations and, more generally, to instil confidence in the domestic economy. Reserve managers, in turn, have traditionally emphasised their ability to mobilise reserves (eg for FX intervention purposes), prioritising the liquidity and safety (or capital preservation) of reserve assets in their asset allocation decisions.

More recently, however, reserves are widely perceived as exceeding the levels indicated by standard adequacy metrics, at least for some countries (IMF (2016)). According to IMF data, total reserves increased by about 10% annually over the 2000-18 period, reaching about $11.5 trillion at end-2018. This growth was mostly a by-product of central banks' monetary and exchange rate policies rather than for explicit adequacy purposes. Anecdotal evidence suggests that the resulting "excess" levels of reserves have led reserve managers to place more emphasis on achieving adequate returns, for example by diversifying the asset and currency composition of their portfolios.

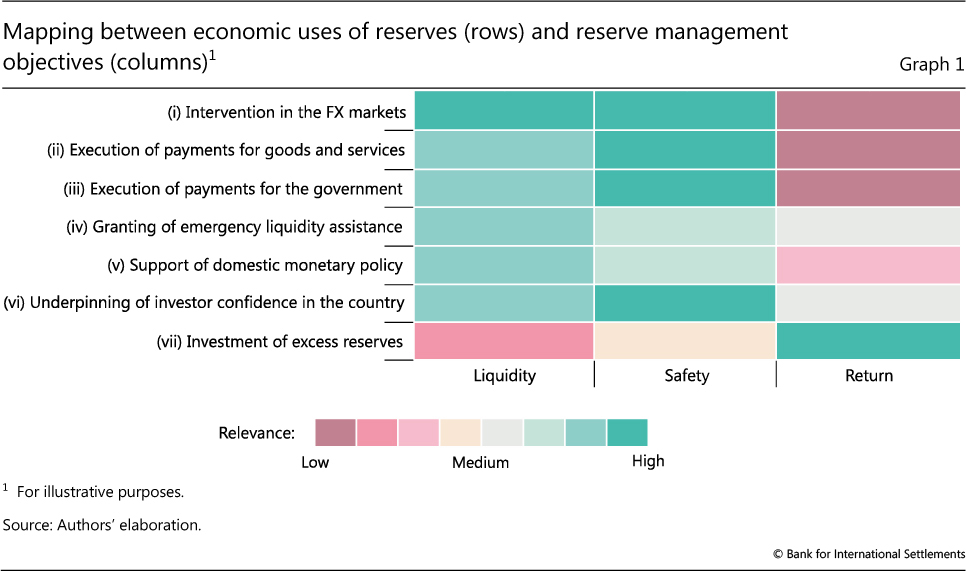

This suggests a direct link (or "mapping") between the seven economic uses of reserves that are usually identified in the literature (Borio et al (2008)) and the triad of objectives (ie liquidity, safety and return) commonly pursued by reserve managers. We express the relevant trade-offs by way of a 7 x 3 matrix (Graph 1), with different colour codes illustrating the possible weights that reserve managers are likely to give to their various objectives.

Graph 1 suggests that different economic uses are likely to lead to different portfolio allocations. For example, a reserve manager who needs to regularly smooth liquidity conditions in the FX market vis-à-vis the euro (Graph 1, row (i)) will tend to favour assets providing sufficient liquidity and safety (in terms of both credit and market risk; green shading). This suggests large allocations to short-dated, high credit quality, euro-denominated securities, even for low- or negative-yielding returns on those funds (red shading). Yet, when investing the portion of the reserves considered "excess" from an adequacy perspective (row (vii)), the same reserve manager will tend to more strongly emphasise return (green shading), probably yielding more risky and diversified portfolios. This would entail some costs in terms of liquidity (red shading) and, to a lesser extent, safety (beige shading).4

Of course, the trade-offs between the various objectives are not one-to-one, and the economic uses of reserves are not mutually exclusive. In practice, therefore, central banks will look across several objectives, as specified in their mandates, to set liquidity, safety and return requirements accordingly.

In the portfolio construction exercise, this is often done as part of a hierarchical tranching approach that divides the reserve portfolio into sub- portfolios: a liquidity and/or working capital tranche and a separate investment tranche. That is, parts of the portfolio are reserved exclusively for assets that meet a specific threshold requirement for liquidity, limiting the extent to which FX reserves may be invested in assets considered "less liquid". Then safety requirements are set, which may be reflected in market and credit risk investment targets or guidelines (eg a volatility objective or asset class and currency exposure limits) - this limits the extent to which FX reserves may be invested in assets considered "less safe". Finally, the reserve manager would find the portfolio that maximises return subject to these constraints. At this stage, the "excess" reserves not needed for liquidity or working capital purposes would be allocated more freely as part of the investment tranche. Under an alternative approach, the manager first sets liquidity requirements, but then trades off safety and return jointly in the portfolio optimisation process.5

Introducing sustainability: objectives and tools

There are two - not mutually exclusive - ways for central banks to include sustainability in their reserve management process: explicit and implicit integration. The choice of approach mainly depends on governance considerations and, in particular, central bank mandates.

Explicit integration can be achieved by central banks that are able to specify sustainability as one of the policy purposes for holding reserves. In Graph 1, this would entail adding one or more rows, representing new economic uses of reserves (eg supporting the transition to a low-carbon economy) to guide portfolio choice. In practice, this would imply changing the central bank's statutes or other key governance documents, which may face legal or political constraints.6 To the best of our knowledge, no central bank has yet taken this step, even though some already aim for sustainability as part of their current, general statutory mandate.7

Implicit integration involves introducing sustainability into the pursuit of the traditional economic uses of reserves. This requires recognising the indirect ways in which sustainability (or the lack thereof) affects central banks' existing policy objectives. One key factor is risk management. Central banks using their FX reserves as a means to underpin investor confidence in the country (Graph 1, row (vi)), for example, may decide to tilt their reserve portfolios towards assets deemed less exposed to possible long-term financial losses arising from climate risks.8

Irrespective of the chosen approach, including sustainability in the reserve management process introduces additional trade-offs. In the context of Graph 1, this would involve expanding the triad of liquidity, safety and return to a tetrad, with sustainability as the fourth reserve management objective. In practice, this would then be reflected in changes to the central bank's investment and/or risk management guidelines.9

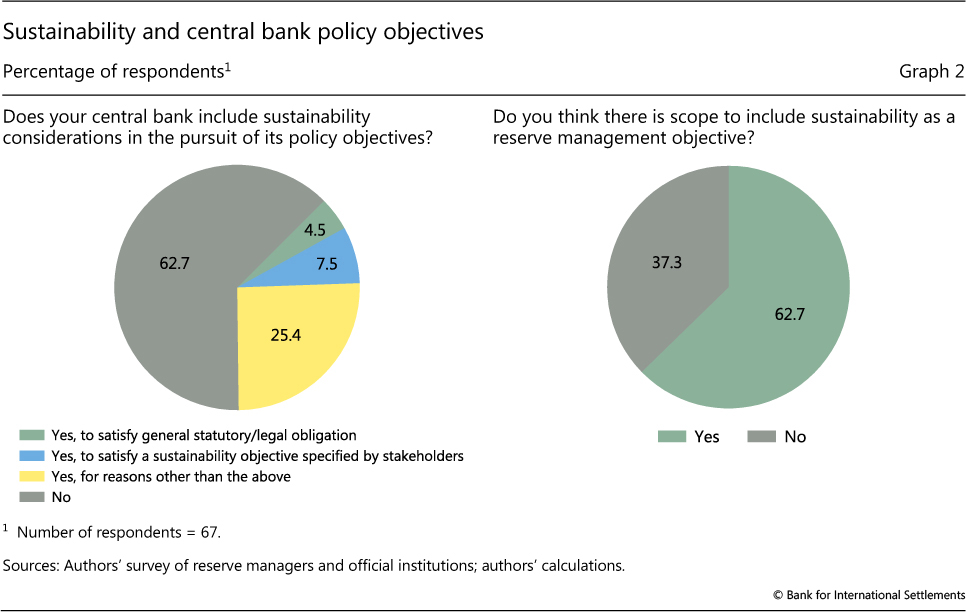

Survey results suggest that most central banks do not currently include sustainability considerations in the pursuit of their policy objectives (Graph 2, left-hand panel).10 And those which do include them do not necessarily aim to satisfy a general statutory or legal obligation. Indeed, over half of the institutions in the sample consider that there is scope to include sustainability as a fourth reserve management objective without necessarily adjusting mandates and, hence, the stated uses of their reserves (right-hand panel).

As regards the choice of tools, central banks' preference seems to be green bond investments, followed by the use of criteria encompassing social and governance considerations in addition to environmental ones (Box A).11 Focusing on green bonds allows them to finance green projects in a potentially meaningful way, while staying within the fixed income asset class that is the core of their reserve portfolios. As the market is still evolving, green bond investing also offers central banks the opportunity to help develop standards and practices (eg in the context of the certification of green bonds according to their likely environmental or climate-related effects).

Box A

Green bonds: features and trends

Green bonds are fixed income securities whose proceeds are used to finance new or existing eligible green projects, eg projects to combat pollution, climate change or the depletion of biodiversity and natural resources (Ehlers and Packer (2017), BIS (2019)). They are either asset-backed or asset-linked, and issuers must declare the types of green projects eligible to receive funds at issuance. Green bonds are the biggest part of the broader universe of socially responsible investments, which include bonds and equities from issuers identified by so-called environmental, social and governance (ESG) standards.

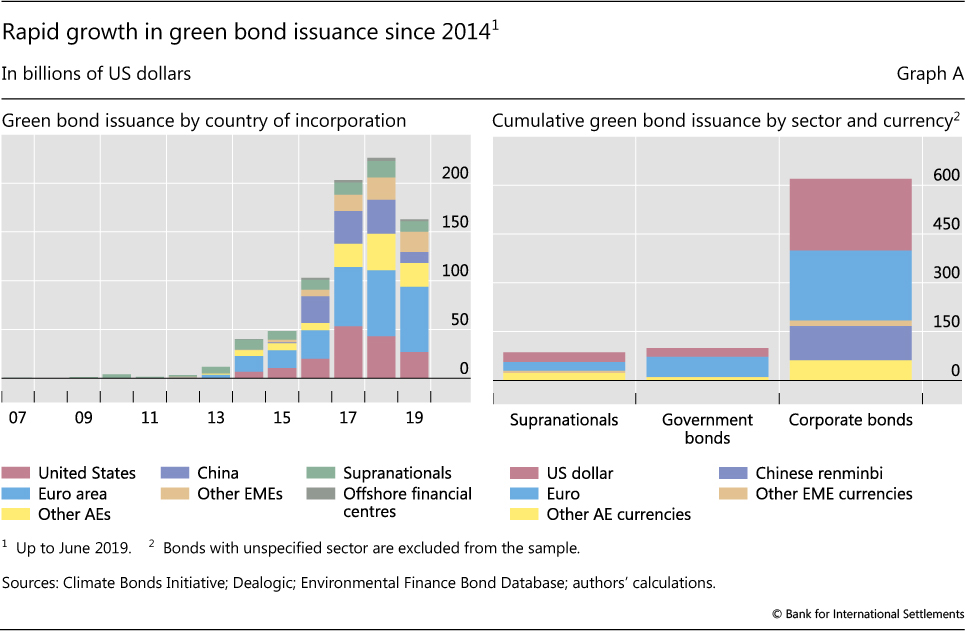

Issuance has grown rapidly in recent years, rising from less than $50 billion in 2014 to close to $230 billion in 2018 (Graph A, left-hand panel). A key catalyst for market development was the 2014 introduction by the International Capital Market Association (ICMA) of the Green Bond Principles (GBPs). The GBPs govern: (i) the use of proceeds; (ii) the process for project evaluation and selection; (iii) the management of proceeds; and (iv) reporting. Bonds meeting the GBPs or the Climate Bond Initiative's (CBI) Climate Bonds Standard (CBS) are eligible for green bond certification by either third-party providers or the CBI. Certification gives comfort to investors that the bonds confer environmental or climate-related benefits, helping to safeguard against "greenwashing".

Supranationals and advanced economy issuers initially dominated the market. Corporates (mainly from the financial, utility and industrial sectors), municipals and emerging market issuers, particularly from China, then gained market share. Issuance was typically in the borrower's local currency, predominantly in euros and US dollars, but other currencies, in particular the Chinese renminbi, recently gained in volume (Graph A, right-hand panel). As a result, the green bond market has gone from being predominantly supranational and euro-based to representing a more broadly diversified universe in both issuer and currency terms.

ESG investing is based on the notion that ESG factors are drivers of a company's long-term value, risk and return, and that they signal how sustainable the company is over the long term. Many jurisdictions have developed their own national taxonomies of what constitutes eligibility as a green bond.

Green bond eligibility as a reserve asset

Within this reserve management framework, a key question is how well green bonds meet the desirable liquidity, safety and return characteristics. We look at each of these characteristics in turn and then discuss potential diversification benefits.

Green bond liquidity

An instrument is said to be liquid if transactions in it can take place rapidly and with little impact on price (Borio et al (2008)). On this basis, eligibility of green bonds as a reserve asset will depend on at least two considerations.

The first concerns the stock of instruments available for investment. Both the size and diversity of the green bond market have grown considerably over time (Box A). However, at current levels, the US dollar and euro segments each represent only about 6.5% of global FX reserves, limiting the scope for investments. Outstanding amounts also continue to be small relative to their conventional comparators, with $750 billion worth of green bond volumes compared with almost $120 trillion worth of conventional securities. The same is true for key market segments relevant for reserve managers, such as government bonds and those issued by international organisations. Given large oversubscriptions in primary markets (CBI (2018)) and low secondary market turnover, accessibility of green bonds will tend to be limited, especially if investors hold these bonds to maturity. The flip side, however, is that if strong demand persists, it should make it easier for investors to offload their bonds, if required.

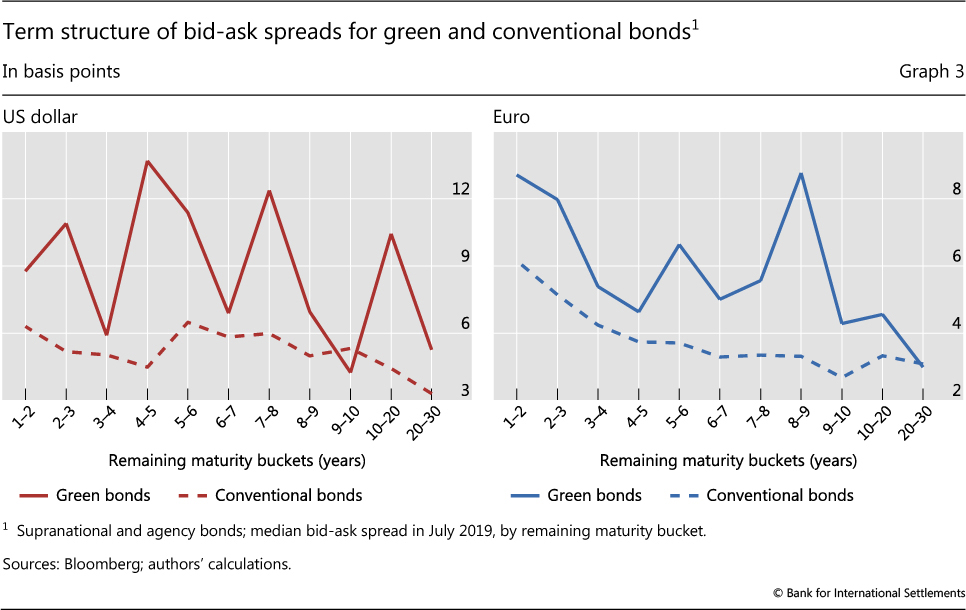

The second consideration concerns the cost of trading, which is inherently difficult to measure. One proxy is bid-ask spreads. Graph 3 reports median bid-ask spreads for US dollar- and euro-denominated green bonds and their conventional counterparts from supranational and agency issuers, organised by maturity bucket. The resulting bid-ask term structures suggest that green bonds tend to be more costly to buy and sell, trading with wider spreads than their conventional counterparts. Results are similar across the entire market.

As a result, green bonds may not be eligible for the liquidity or working capital tranches of central banks' reserve portfolios. Inclusion in investment tranches, in turn, is constrained by the market's still limited size. Central banks would thus have to limit the size of their allocations.

Green bond safety

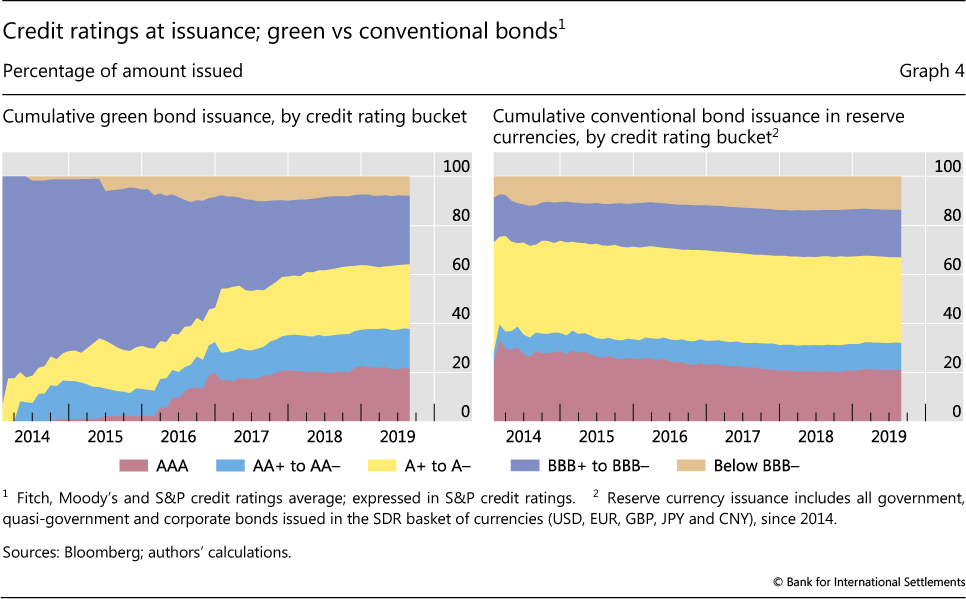

To assess the eligibility of green bonds from a credit risk perspective, we investigate the credit ratings of newly issued green bonds by issuance year, and compare these with those of conventional bonds. While the concept of safety goes well beyond credit ratings, central banks typically constrain the credit quality of their reserve portfolios by imposing rating requirements on their investments. For example, a common requirement is to exclude bonds with ratings of BBB+ and below. Green bonds are mostly backed by the full balance sheet of the issuer, and not only by the cash flows related to the climate- friendly project financed from the proceeds (Ehlers and Packer (2017)), allowing direct comparisons across both market segments.

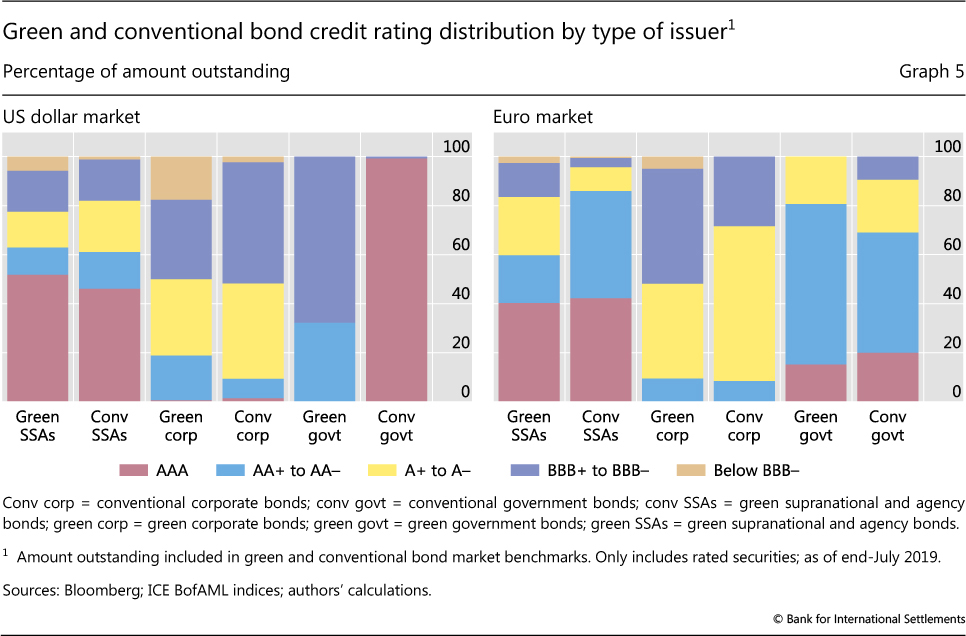

We find that the ratings compositions of green and conventional bond markets have broadly converged, supporting eligibility. Although green bond at- issuance ratings in 2014 were more concentrated in the lower end of the investment grade spectrum, this predominance has gradually waned (Graph 4, left-hand panel). This puts high-graded green bonds (above BBB+) at about 65% of new issuance by 2019, broadly comparable to the conventional comparator market (right-hand panel). Recent data for total amounts outstanding at the sectoral level appear to confirm this observation. Across sectors, credit quality is broadly similar for both green and conventional markets (Graph 5). The main exception is government bonds, where credit quality in green-labelled instruments tends to be lower, particularly in the US dollar market, in part because only a few countries have so far issued in this space.

Green bond return

The third aspect of eligibility is return. Evidence from both primary and secondary markets points to a small and negative yield premium ("greenium").12 However, much of this evidence is at the security level, which restricts the analysis to a relatively small sample of matched bonds. The more relevant question for reserve managers is how a portfolio of green bonds is likely to behave vis-à-vis one composed of conventional bonds with similar characteristics. We thus take the analysis to the asset class level and focus on relative returns for fixed income indices.

To control for differences in index composition, we compare two "matched" indices: one for green and the other for conventional bonds. Given limited availability of green bonds, we select an available green bond index as our reference portfolio. We then build a portfolio of conventional bonds that matches its characteristics in terms of sectors, rating composition and duration.13 To do this, we dissect the green bond index (in US dollars or euros) into each issuer sector i and credit rating bucket j. Then, we construct a synthetic conventional portfolio that matches this breakdown, by applying the green index's sector and rating weights to individual conventional bond indices for each combination of sector i and credit rating bucket j. We also ensure that the conventional indices closely track the green portfolio's duration. We then compare index performance, assuming rebalancing costs to be zero for both portfolios. Of course, the issuer and rating composition of the two portfolios will change over time, which must be taken into account when the indices are rebalanced.

On this basis, the yield to maturity of the portfolio of the conventional index (in either US dollars or euros) at every month-end t is:

where  and

and  are the weights that sector i and rating bucket j have at month t in the green benchmark,

are the weights that sector i and rating bucket j have at month t in the green benchmark,  is the yield to maturity of the conventional index of sector i and rating bracket j, and

is the yield to maturity of the conventional index of sector i and rating bracket j, and  is the yield to maturity of the complete conventional bond portfolio. This can then be contrasted with the yield of the green portfolio. In line with established practice, in order to isolate the compensation of green and conventional bonds relative to their risk-free benchmark, we remove the risk-free component of the yields to maturity by subtracting the zero coupon yield of the government instrument with equivalent duration.14

is the yield to maturity of the complete conventional bond portfolio. This can then be contrasted with the yield of the green portfolio. In line with established practice, in order to isolate the compensation of green and conventional bonds relative to their risk-free benchmark, we remove the risk-free component of the yields to maturity by subtracting the zero coupon yield of the government instrument with equivalent duration.14

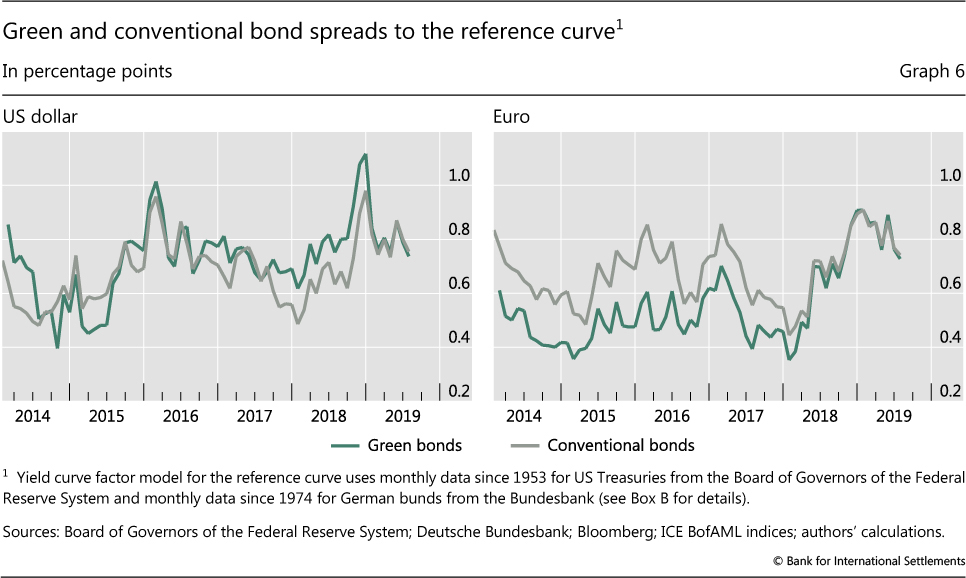

Our results (Graph 6) suggest that green bonds compare reasonably well with their conventional peers. Based on our approach, a US dollar investor tracking the green index would have enjoyed a spread 4 basis points above that of the conventional benchmark (positive "portfolio greenium"), while the euro-based investor would have earned 12 basis points less than the comparator market (negative portfolio greenium). However, this greenium estimate has varied considerably over time, due in part to differences in issuer composition across benchmarks, even when credit rating and sector breakdowns are set equal. It also appears that the portfolio greenium narrowed over time as the green bond market developed, with the spread between conventional and green returns closing as of 2019.

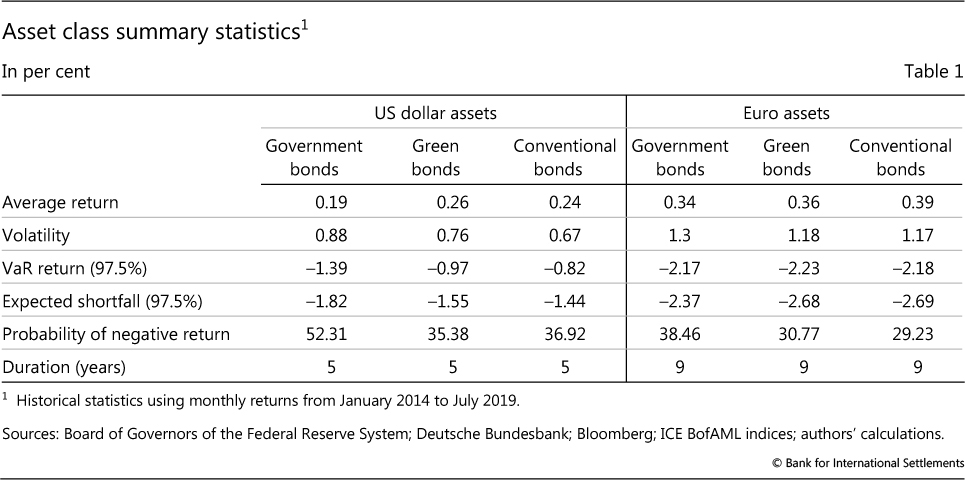

Absolute returns paint a similar picture. Table 1 reports summary statistics comparing the risk-return properties of green and conventional bonds. A couple of points stand out. First, both types of portfolios possess broadly comparable historical returns. For example, between 2014 and mid-2019 US dollar green bonds had an average monthly return of 0.26%, while the conventional benchmark returned 0.24% over the same period. Second, we observe that, in both the US dollar and euro cases, the volatility and tail risk of the conventional and green instruments are broadly similar, slightly favouring green bonds. This confirms the point that, from a safety perspective, investment in green bonds would not seem to subject reserve managers to higher risk than their conventional alternative. This holds regardless of whether safety is defined in terms of price volatility, performance in extreme scenarios or the probability of facing a negative return.

Diversification benefits

Having established the eligibility of green bonds as reserve assets - at least outside reserve managers' liquidity tranches - does it make sense to add green bond allocations from a portfolio perspective? Answering this question involves trading off green bonds' safety and return in a portfolio context, after taking the portfolio's liquidity requirements into account. To assess this, we conduct an illustrative portfolio construction exercise. The results suggest that adding both green and conventional bonds can help generate diversification benefits and, hence, improve the risk-adjusted returns of traditional government bond portfolios (Box B).

Box B

Diversification benefits of green bonds: illustrative asset allocation exercise

Do green bond investments generate diversification benefits relative to their conventional peers? To answer this question, we construct simple, illustrative reserve portfolios comprising three assets: zero coupon government bonds, and the green and conventional bond portfolios built for the earlier analysis of returns. We explore any potential diversification benefits in green bonds by running separate asset allocation exercises for US dollar- and euro-denominated portfolios. We do this for both prospective and historical returns.

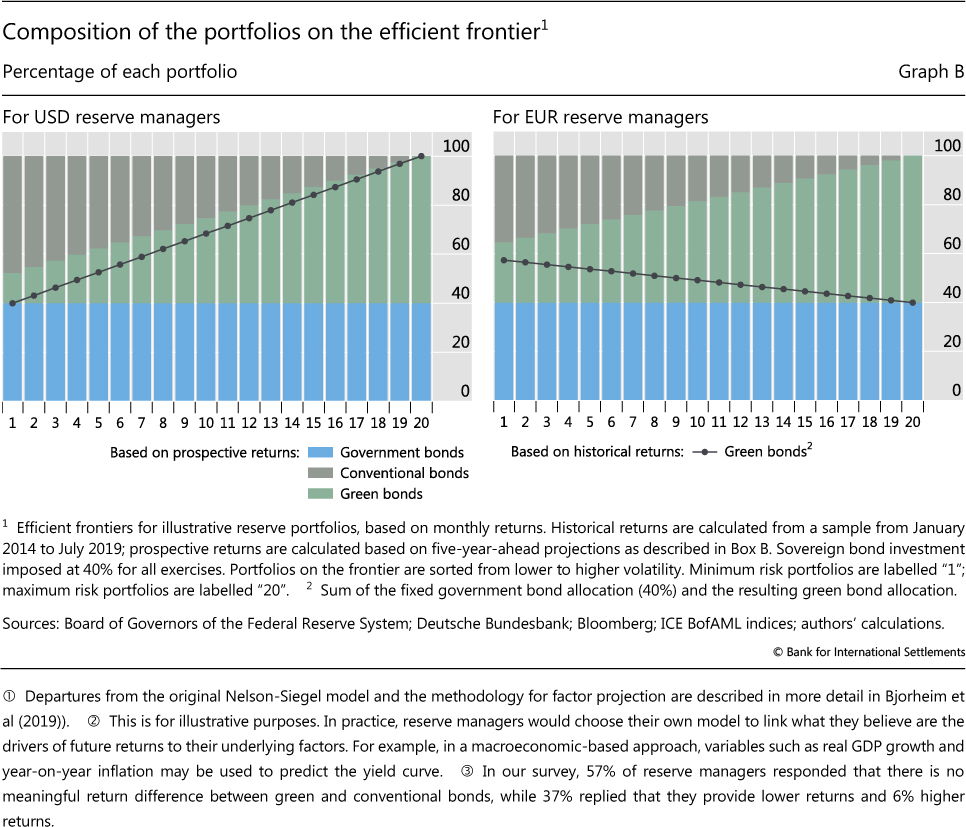

Methodology

Following a hierarchical approach to portfolio construction, we begin by setting liquidity requirements by means of a constraint of 40% to be invested in government bonds. Then we use a standard mean-variance optimisation algorithm to trade off safety and return, combining conventional and green bonds to obtain the best possible pairs of expected return and volatility. To derive prospective risk and return measures of bonds of different maturities, we employ a forward-looking, factor-based approach to asset allocation performed in three steps: (i) factor identification and projection; (ii) return projection; and (iii) portfolio optimisation.

First, we identify and estimate the underlying statistical factors of government bond yield curves. To achieve this, we use a dynamic Nelson-Siegel term structure model, modified slightly from the version proposed by Diebold and Li (2006). The model decomposes historical yields into three factors: the short rate, slope and curvature, which are then projected forward. For the purposes of this study, we rely on a simple autoregressive model that generates projected paths for all three factors over the next five years. For green bonds and their conventional counterparts, additional spread factors, representing compensation for risks beyond those embedded in the government yield curve, are estimated and projected using the same autoregressive approach.

Second, we use our yield curve factor estimations to project the zero coupon term structure of interest rates for each period in our projection horizon. For green bonds and their conventional counterparts, we add the relevant spread factor projections to identify the prospective yields of each asset. Armed with these simulated yield distributions, we can then estimate a prospective return distribution for each generic asset class, from which forward-looking summary statistics - such as the expected return (mean), volatility (standard deviation) and other risk metrics - are derived. As implementation considerations typically come at a later stage of the FX reserve management process, the derived prospective return distributions do not include transaction costs.

To keep the analysis simple, we assume equal expected returns for green and conventional bonds. Specifically, we restrict the paths of green and conventional bond spreads to be, on average, equal and constant over time and close to their current levels. This reflects the empirical evidence of small and possibly vanishing greenium effects (Graph 6) as well as results from our survey, in which a majority of reserve managers saw no meaningful difference between green and conventional bond returns.

Finally, we estimate an expected return vector and a variance-covariance matrix from the prospective asset return distributions. On this basis, a standard (Markowitz) mean-variance algorithm is applied to derive a frontier of efficient portfolios, including the global minimum variance portfolio.

Results

Our results are shown in Graph B. Portfolios further along the frontier, which are denoted by increasing portfolio numbers on the x-axis, imply higher volatility. The results based on prospective returns (coloured bars) suggest that, even though green and conventional bonds are assumed to have equal returns on average, including both in the illustrative reserve portfolio helps improve the risk-adjusted returns of government bonds, once liquidity requirements at the overall portfolio level are taken care of. For example, in the minimum risk portfolios (labelled "1" in both panels), we find that green and conventional bonds are both present, illustrating diversification benefits. The same applies to the maximum risk portfolio (labelled "20").

Results based on historical returns (over the January 2014-July 2019 period) are also generated for comparison purposes. The results are qualitatively similar to those based on prospective returns (Graph B; black lines). For US dollar and euro portfolios, green bonds are present in all but one of the portfolios along the efficient frontier. This is despite the history of greenium effects (Graph 6), particularly in the euro-denominated market, which reduces green bond allocations relative to the prospective return case. Allocations in the minimum risk portfolios are anchored by the relative size of historical return volatilities observed for both green and conventional bonds.

Of course, real world asset allocation exercises would tend to involve a wider range of eligible assets as well as additional constraints. This will change the resulting portfolio weights for the overall FX reserves. Nonetheless, our illustrative exercise suggests that, when deciding their portfolio allocations, reserve managers can reap diversification benefits from even subtle differences in risk-return properties between green and conventional bond portfolios.

Departures from the original Nelson- Siegel model and the methodology for factor projection are described in more detail in Bjorheim et al (2019)). This is for illustrative purposes. In practice, reserve managers would choose their own model to link what they believe are the drivers of future returns to their underlying factors. For example, in a macroeconomic-based approach, variables such as real GDP growth and year-on-year inflation may be used to predict the yield curve. In our survey, 57% of reserve managers responded that there is no meaningful return difference between green and conventional bonds, while 37% replied that they provide lower returns and 6% higher returns.

Conclusion

While central banks are playing an increasingly active role in promoting green finance, comparatively little attention has been paid to how they might integrate sustainability into their policy frameworks - specifically for their FX reserves.

Sustainability might be integrated into the reserve management process either explicitly by articulating sustainability as a defined purpose for holding reserves, or implicitly as a supporting aspect of existing policy purposes. Central banks' choice between either of these approaches will depend primarily on their legal and governance frameworks. In both cases, however, it will involve additional trade-offs, turning the classical triad of liquidity, safety and return into a tetrad of reserve management objectives.

Analysing the asset class properties of green bonds enables us to explore how well a sustainability objective might coexist with the classical triad. Reserve managers evaluating the potential eligibility of green bonds as an asset class may find that their accessibility and liquidity currently pose some constraints. This is one reason reserve managers may wish to limit the total volume of green bonds held, particularly in the light of the relatively small (but rapidly growing) size of the market. The extent of this limit will depend on the priority a reserve manager gives to sustainability in its reserve management objectives.

Overall, however, we find that sustainability objectives can be integrated into reserve management frameworks without forgoing safety and return. The results of an illustrative portfolio construction exercise suggest that adding both green and conventional bonds can help generate diversification benefits and, hence, improve the risk-adjusted returns of traditional government bond portfolios. To the extent that central bank involvement helps to establish minimum standards and practices in a still developing market, this would tend to confer additional benefits: for example, by guarding against greenwashing (BIS (2019)).

Of course, instruments such as green bonds are only one tool for implementing sustainability objectives. Some central banks - particularly those with abundant FX reserves, which are more likely to hold less traditional reserve assets - may have more options for doing so, for example by making sustainable investment choices in the corporate bond or equity parts of their portfolios, or by adding new asset classes (such as green infrastructure). After all, there is more than one way to go green.

References

Bank for International Settlements (2019): "The BIS's support of green finance", Annual Report 2018/19, June, p 33.

Bank of France (2018): Responsible investment charter of the Banque de France.

Bjorheim, J, J Coche, A Joia and V Sahakyan (2018): "A macro-based process for actively managing sovereign bond exposures", in N Bulusu, J Coche, A Reveiz, F Rivadeneyra, V Sahakyan and G Yanou (eds), Advances in the practice of public investment management, pp 103-29.

Borio, C, J Ebbesen, G Galati and A Heath (2008): "FX reserve management: elements of a framework", BIS Papers, no 38, March.

Carney, M (2015): "Breaking the tragedy of the horizon - climate change and financial stability", speech given at Lloyd's of London, 29 September.

Climate Bond Initiative (2018): Green bond pricing in the primary market.

Diebold, F and C Li (2006): "Forecasting the term structure of government bond yields", Journal of Econometrics, vol 130, no 1, pp 337-64.

Dikau, S and U Volz (2019): "Central bank mandates, sustainability objectives and the promotion of green finance", University of London Department of Economics, Working Paper, no 222.

Ehlers, T and F Packer (2017): "Green bond finance and certification", BIS Quarterly Review, September, pp 89-104.

Elsenhuber, U and A Skenderasi (2019): "ESG investing: how public investors can implement sustainable investing", mimeo. Forthcoming in Proceedings of the 2018 Public Investors Conference.

European Central Bank (2019): "Climate change and financial stability", Financial Stability Review, May.

International Monetary Fund (2016): "Guidance note on the assessment of reserve adequacy and related considerations", IMF Policy Paper, June.

McCauley, R (2008): "Choosing the currency numeraire in managing official foreign exchange reserves", in R Pringle and N Carver (eds), RBS reserve management trends 2008, pp 25-46.

Monnin, P (2018): "Integrating climate risks into credit risk assessment: current methodologies and the case of central banks corporate bond purchases", Council on Economic Policies, Discussion Note 2018/4.

Netherlands Bank (2019): Responsible investment charter.

Network for Greening the Financial System (2019): A call for action: climate change as a source for financial risk.

Pereira da Silva, L (2019): "Research on climate-related risks and financial stability: an 'epistemological break'?", May.

Volz, U (2017): "On the role of central banks in enhancing green finance", UNEP Inquiry Working Paper, no 17/01, February.

Zerbib, O (2019): "The effect of pro-environmental preferences on bond prices: Evidence from green bonds", Journal of Banking and Finance, vol 98, pp 39-60.

1 The authors are staff members of the BIS Banking Department, which offers financial products, including investment pools dedicated to green bonds, to central bank clients. The views expressed in this article are the authors' and do not necessarily reflect those of the BIS. We thank Claudio Borio, Pierre Cardon, Stijn Claessens, Torsten Ehlers, Ulrike Elsenhuber, Kumar Jegarasasingam, Frank Packer, Jean-François Rigaudy, Hyun Song Shin, Philip Wooldridge and Peter Zöllner for comments, and Nicolas Lemercier for excellent research assistance.

2 The NGFS is a voluntary, consensus-based forum collaborating to develop climate- and environment-related risk management practices in the financial sector and to mobilise mainstream finance to support the transition towards a sustainable economy.

3 Another possibility is central banks' pension fund portfolios, where portfolio managers tend to enjoy some flexibility regarding asset allocation (Elsenhuber and Skenderasi (2019)). Other portfolios (eg those accumulated in the context of unconventional monetary policies), in contrast, would tend to be dedicated solely to fulfilling monetary policy objectives, limiting the scope for active portfolio allocation decisions (NGFS (2019)).

4 A key aspect of these decisions is the choice of the appropriate unit of account (numeraire) for the reserve portfolio. See McCauley (2008) for details.

5 In the mean-variance approach, for example, this would mean finding the portfolio with the highest risk-adjusted return, regardless of the absolute level of volatility.

6 There are also questions about the appropriate assignment of explicit sustainability objectives in the broader policymaking context, which could also be vested with sovereign wealth funds.

7 In an analysis of central bank mandates, Dikau and Volz (2019) find that the goal of supporting sustainable growth is directly included in at least a dozen central banks' mandates, and indirectly in the mandates of many others.

8 An example of this type of analysis, applied to central bank bond purchases, is Monnin (2018).

9 Examples include the Bank of France and the Netherlands Bank, which recently took the pioneering step of adopting responsible investment charters for their own funds and, in the latter case, also for their FX reserves. See Bank of France (2018) and Netherlands Bank (2019).

10 Authors' July-August 2019 survey of reserve managers from 67 central banks and other national authorities.

11 In the survey, 76% of respondents identified green bonds as their tool of choice for including sustainability considerations in reserve management activities, followed by 51% of respondents who indicate using metrics such as environmental, social and governance criteria in investment decision-making.

12 Zerbib (2019) provides a comprehensive literature review. He finds, controlling for liquidity, an average green bond premium of -2 basis points. This suggests that, on average, holding such bonds to maturity yields a lower return.

13 Bloomberg Barclays MSCI indices are used as a basis for the green bond universe and ICE BofAML indices for the conventional bond market. The underlying sectors used are: agencies, corporates, governments, municipals and covered bonds. The underlying credit rating brackets are: AAA, AA+ to AA-, A+ to A-, and BBB+ to BBB-.

14 The reference curve for this purpose is obtained by applying the shadow short rate approach for modelling the term structure of interest rates (Bjorheim et al (2018) and Box B).