Negative rates and bank business models

(Extract from page 15 of BIS Quarterly Review, September 2016)

Low profitability has challenged banks' traditional business models in the current environment of persistently low interest rates and compressed term premia.

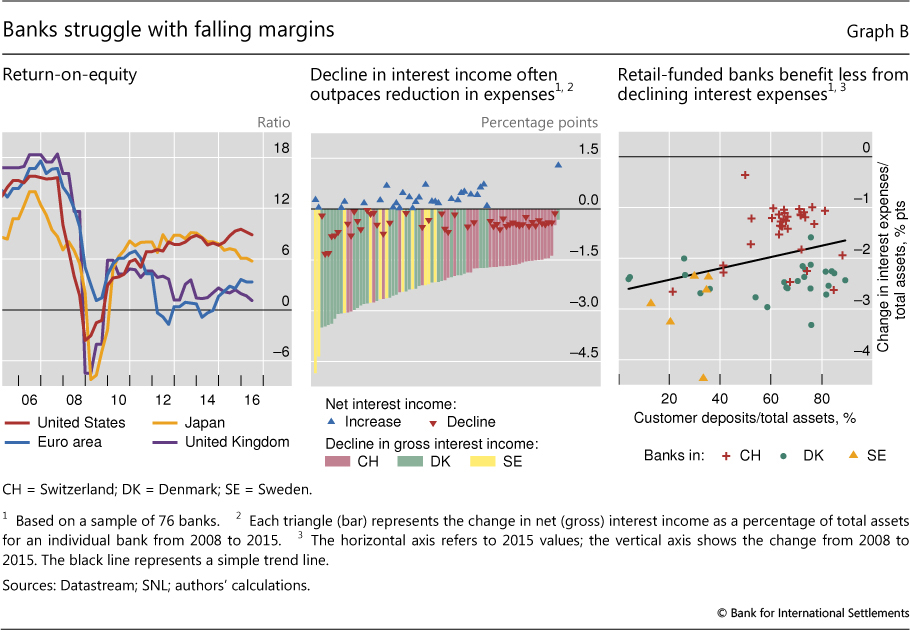

Market valuations indicate that investors remain sceptical of banks' ability to generate earnings in a low-rate, low-growth environment. Bank return-on-equity ratios have never recovered to the levels observed before the GFC, though they exhibit significant differences across jurisdictions (Graph B, left-hand panel). Flattening yield curves and low long-term rates are among the factors that markets are weighing more closely as they ask whether, and how, banks' profitability can recover.

have never recovered to the levels observed before the GFC, though they exhibit significant differences across jurisdictions (Graph B, left-hand panel). Flattening yield curves and low long-term rates are among the factors that markets are weighing more closely as they ask whether, and how, banks' profitability can recover.

Profitability has been constrained by flatter yield curves. Long-term rates have fallen, especially where investors have expected low short-term rates to prevail for longer and central banks have engaged in large-scale asset purchases to compress term premia. A decline in the level of interest rates can improve banks' net income in the short run, as their portfolios of securities benefit from one-off capital gains, and also if funding for the banks becomes cheaper. However, in the long run the flattening of the curve can drive down returns from maturity transformation and compress net interest margins.

Furthermore, as interest rates decline and move into negative territory, repricing banks' liabilities in lockstep with assets in order to protect margins will become increasingly difficult. Banks appear reluctant to pass negative short-term rates to depositors. Thus, pressures on net interest margins are particularly pronounced in countries with negative interest rates. For example, many banks in Denmark, Sweden and Switzerland have seen the compression in gross interest income (bars in Graph B, centre panel) outpacing the reduction in interest expenses, resulting in declining net interest margins (triangles in same panel) over recent years. A critical issue in this context is the extent to which banks' liabilities are tilted in the direction of retail deposits and similar funding sources (right-hand panel).

Ultimately, country-specific factors will dictate whether and how banks can compensate for lower net interest margins. Stronger economies will allow banks to expand the volume of their traditional lending activities. Some banks may be able to compensate for part of their lost revenues by relying on alternative sources of income such as trading and fee-generating services, while others may be able to reap efficiency gains, for example by addressing overcapacity or by bringing down cost-to-income ratios.

The reported return-on-equity ratios are unadjusted for risk. See C Borio, L Gambacorta and B Hofmann, "The influence of monetary policy on bank profitability", BIS Working Papers, no 514, 2015; and BIS, 86th Annual Report, 2016, Chapter VI.