Shifting tides - market liquidity and market-making in fixed income instruments

Drawing from a recent report by the Committee on the Global Financial System, we identify signs of increased fragility and divergence of liquidity conditions across different fixed income markets. Market-making is concentrating in the most liquid securities and deteriorating in the less liquid ones. The shift reflects cyclical (eg changes in risk appetite) as well as structural (eg tighter risk management or regulation) forces affecting both the supply of and demand for market-making services. Although it is difficult to definitively assess the market implications, we outline several possible initiatives that could help buttress market liquidity.1

JEL classification: G14, G21, G23.

Recent bouts of volatility remind us that liquidity can evaporate quickly in financial markets. The bond market sell-off in 2013 ("taper tantrum") highlighted that liquidity strains can spread rapidly across market segments (BIS (2013)). In sovereign debt and, to an even greater degree, corporate bond markets, liquidity hinges in large part on whether specialised dealers ("market-makers") respond to temporary imbalances in supply and demand by stepping in as buyers (or sellers) against trades sought by other market participants. Analysing what drives the behaviour of these liquidity providers is a precondition for understanding how well placed markets are to accommodate potential future shifts in supply and demand, particularly during times of elevated market uncertainty.

In the wake of the recent global financial crisis, several developments suggest that market-makers are changing their business models. These changes, their drivers and the potential impact that both might have on fixed income markets are of particular interest to policymakers, given the relevance of these markets to monetary policy and financial stability.

This feature article draws on recent work by the Committee on the Global Financial System (CGFS) to investigate trends in market-making and what they mean for the financial system (CGFS (2014)).2 We use a simple conceptual framework to assess how supply and demand for liquidity have changed in fixed income markets, particularly in markets for sovereign and corporate bonds.

We see signs that market liquidity is increasingly concentrating in the most liquid securities, while conditions are deteriorating in the less liquid ones ("liquidity bifurcation"). The trend can be seen in both the supply of and demand for market-making services, and reflects both post-crisis cyclical conditions (such as diminished bank risk appetite and strong bond issuance) and structural changes in the markets themselves (such as tighter risk management or regulatory constraints). Yet it is difficult at this stage to say definitively what these developments mean for fixed income markets over the long term. Nevertheless, we consider what kinds of policies and market initiatives might help support market liquidity in the future.

The remainder of this article is organised as follows. The first section looks into the link between market-making and market liquidity, and identifies recent trends and their drivers. The second section discusses implications for markets and policy, followed by a short conclusion.

Market-making and market liquidity

Markets are liquid when investors are able to buy or sell assets with little delay, at low cost and at a price close to the current market price (see eg CGFS (1999)). Market liquidity depends on a variety of factors, including market structure and the nature of the asset being traded. Another key distinction (see the next section) is between normal times ("fair weather" liquidity) and more stressed environments, when the functioning of markets is challenged by large order imbalances (Borio (2009)).

One feature of bond markets that limits their liquidity is that individual issuers may have a large number of different securities outstanding. This makes bonds a relatively heterogeneous asset class in which many securities are thinly traded.3 At the same time, institutional investors often hold assets to maturity and, when they do trade, do so in large amounts. Thus, trading in any individual issue is often infrequent and lumpy. This reduces the probability of matching buyers and sellers of any given bond at any given time. For that reason, bond markets, particularly those for corporate issues, tend to rely on market-makers, typically banks or securities firms.

The essence of market-making is to fill client orders in one of two ways. In the first instance, a market-maker matches a buyer and a seller of an asset, a practice known as agency trading. If no match can readily be found, the market-maker will itself step in as buyer or seller. In other words, the institution executes its client's trade by using its own balance sheet, a practice known as principal trading. In doing so, market-makers provide "immediacy services" to clients and other market participants. Their readiness to immediately execute a trade supports market liquidity and facilitates price discovery. The market-maker's willingness to absorb temporary imbalances in supply and demand is thus vital to smooth market functioning.

Box 1

The economics of market-making

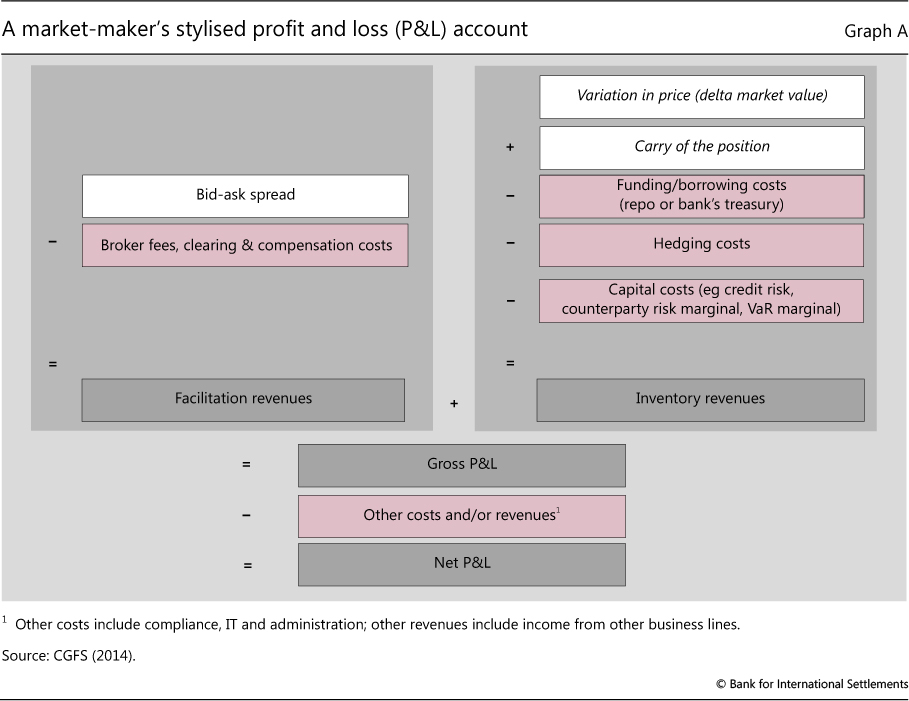

Market-makers follow a number of different business models, but broadly share some common features (CGFS (2014)). These include a sufficiently large client base to get a good view of the flow of orders; the capacity to take on large principal positions; continuous access to multiple markets, including funding and hedging markets; the ability to manage risk, especially the risk of holding assets in inventory; and market expertise in providing competitive quotes for a range of securities.

A stylised profit and loss (P&L) account (Graph A) maps these features into two broad revenue categories. One is called facilitation revenues. These reflect bid and ask spreads - that is, the difference between the market-maker's prices for buying and selling an asset, net of the cost of trading. The second is termed inventory revenues. These reflect changes in the value of an asset held in inventory, plus accrued interest, and funding and hedging costs. Regulatory requirements will affect profits via their impact on capital, funding and hedging costs, as well as the direct costs of compliance. It follows that market-makers will set their bid and ask prices based on their expectations of the cost and risk of holding assets in inventory. Spreads will tend to be narrow if market-makers believe they can execute trades quickly and cheaply, or if funding and hedging costs are low. Thus, a market's liquidity depends on the depth and efficiency of related markets, such as those for funding and hedging.

The difference between actual and desired inventory levels is important to market-makers, who all have risk management frameworks that set limits on holdings of different assets. When institutions approach those limits, they tend to adjust their quoted prices to realign their inventory. As a result, if an institution is trying to reduce risk, it may cut back on its market-making activity. If many market-makers are reducing risk at the same time, markets lose liquidity. Moreover, when market volatility rises, standard risk assessment models will signal that a market-maker's inventory has become riskier. That may prompt the market-maker to further trim its holdings. In turn, bid-ask spreads may widen, which could ultimately provoke additional volatility and diminish liquidity further.

Risk-taking is an integral part of market-making, particularly in less liquid markets like those for corporate bonds. Market-makers must be willing to take on risk by building inventory positions (see Box 1 for a discussion of the economics of market-making).4 As with other types of financial intermediation, willingness to build positions depends on assessments of risk and return. The riskier a position, the greater the return a market-maker will demand. Risk tolerance is also a factor, and will in turn be influenced by the market-maker's balance sheet strength and funding conditions. Given the recent crisis experience, many of these factors are evolving.

Gauging recent market developments

How have market-making and bond market liquidity changed post-crisis? Unfortunately, there is no single measure of market liquidity or of market-making activity to provide a clear-cut answer (Fleming (2003)). In addition, data with which to evaluate liquidity trends across markets and debt instruments are also hard to come by. Nevertheless, available data and softer sources of information, such as market intelligence, allow some inferences to be drawn. Overall, these suggest that market liquidity is increasingly concentrating in the most liquid securities and market segments, while conditions are deteriorating in the less liquid ones.

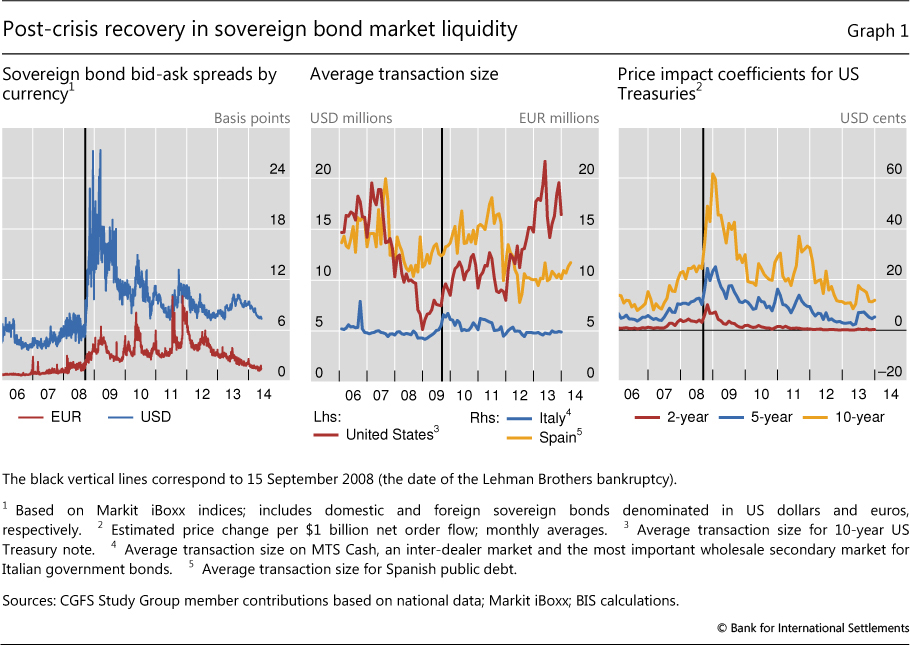

Sovereign bond market liquidity recovered strongly after the financial crisis, as suggested by several metrics (Graph 1). The left-hand panel charts the gap between market-maker buying and selling prices for sovereign bonds denominated in US dollars and euros, respectively. These bid-ask spreads have broadly returned to levels comparable to those that prevailed before the global financial crisis, indicating that liquidity has largely recovered in major sovereign bond markets. That tallies with other measures of liquidity, such as trading volume and the average size of transactions (Graph 1, centre panel). Interviews with market participants confirm this trend.5

Another widely followed liquidity measure is the price impact coefficient. This metric looks at how much securities prices rise or fall when investors initiate a transaction (Fleming (2003)). For US Treasury securities, the estimated price impact rose sharply when markets were stressed in late 2008, underscoring how costly it was to execute trades even in one of the most liquid bond markets (Graph 1, right-hand panel). Since then, the estimated price impact coefficient in the US Treasury market has more or less returned to pre-crisis levels, notwithstanding some brief spikes when markets turned volatile.

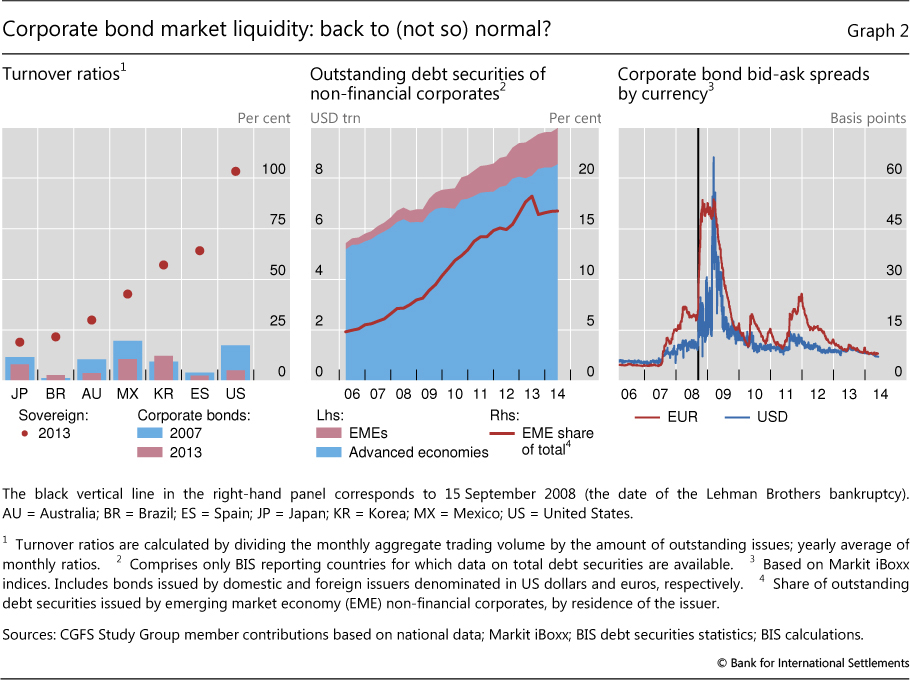

Data for other debt markets, such as corporate bonds, are typically more difficult to obtain. However, turnover ratios, which measure trading volumes divided by outstanding amounts, broadly gauge differences across countries in both sovereign and corporate bond markets (Graph 2, left-hand panel). To be sure, corporate bonds are generally much less liquid than sovereign bonds. But, starting from these lower levels of market liquidity, corporate bonds seem to have witnessed a decline in liquidity in many jurisdictions - at least according to this particular metric.

Yet, if corporate bonds have indeed become less liquid, it is not because trading volumes are lower. Rather, trading volumes have not kept pace with the surge in debt issuance, reflecting in particular favourable funding conditions in many advanced and emerging market economies (Graph 2, centre panel). Meanwhile, bid-ask spreads in major corporate bond markets have narrowed sharply in recent years, but remain somewhat wider than the levels observed immediately before the global financial crisis (Graph 2, right-hand panel). While these observations suggest that liquidity conditions may have deteriorated relative to those in 2005-06, most observers agree that bid-ask spreads at the time had been unduly narrow owing to market participants' search for yield in the run-up to the crisis (BIS (2005)) - an environment bearing some similarities with current conditions (BIS (2014)).

Supporting the mixed picture presented above, market intelligence confirms that differentiation in liquidity conditions across and within market segments is growing - pointing to increased market bifurcation. In interviews, many market participants say trading large amounts of corporate bonds has become more difficult. They note, for example, that the size of large trades of US investment grade corporate bonds (so-called "block trades") has continuously declined in recent years.6 Furthermore, in most corporate bond markets, trading appears to be highly concentrated in just a few liquid issues, and concentration appears to be increasing in some market segments. For one, the share of securities whose 12-month trading volume equals at least half of the number of securities outstanding has fallen from 20% to less than 5% in the US corporate bond market since 2007 (CGFS (2014)).

Increased bifurcation reflects changes in the behaviour of both market-makers' and their clients - that is, in the supply of and demand for market-making services. On the supply side, one apparent trend is that market-makers are focusing on activities that require less capital and less willingness to take risk. In line with this trend, in many jurisdictions banks say they are allocating less capital to market-making activities and are trimming their inventories, particularly by cutting holdings of less liquid assets.

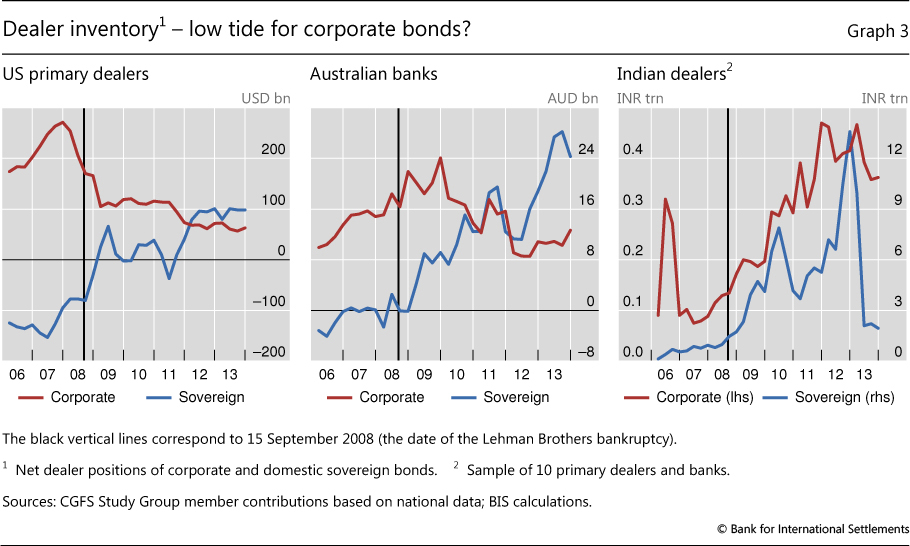

However, trends differ across countries. In the United States, the net corporate debt securities holdings of securities dealers, including securitisations backed by assets such as credit card debt, have fallen sharply since 2008. By contrast, net US Treasury positions rose during the financial crisis and are now net positive, as dealers have closed short positions (ie positions that rise in value when the price of an asset falls) and accumulated securities holdings (Graph 3, left-hand panel). Australia shows a similar trend. Australian banks, which were less exposed to the global financial crisis, have been raising their domestic government bond inventories since 2008 and cutting those of corporate bonds since 2010 (Graph 3, centre panel). By contrast, dealers in countries such as India were building both types of inventories until mid-2013, before selling off their sovereign holdings during the taper tantrum (Graph 3, right-hand panel).

Another trend is greater focus on core markets and clients. A number of market-makers have reportedly become more selective, mainly servicing core clients that generate income in other business lines. Others are narrowing their scope to a smaller range of markets. In many jurisdictions, market-making has thus shifted from a principal trading model towards a client-driven brokerage model. As a result, many market-makers have become reluctant to absorb large positions and consequently need more time to execute large trades.

In Australia, for example, several foreign banks have ceased their market-making in corporate bond and derivatives markets in recent years and have drawn down their inventories.7 In core markets, such as domestic sovereign bonds, domestic dealers are likely to pick up at least part of the slack. But, in less active markets, domestic banks may also be pulling back, resulting in an overall loss of liquidity.

In addition, proprietary trading (ie position-taking for purposes other than market-making) has reportedly diminished or assumed a more marginal importance for banks in most jurisdictions. Expectations are for banks' proprietary trading to generally decline further or to be shifted to less regulated entities in response to regulatory reforms targeting these activities (Duffie (2012)). Overall, though, such a wind-down of proprietary trading will tend to limit market-makers' ability to redistribute risky positions. Combined with reduced risk-taking in the financial system as a whole, this would then further reduce market-makers' willingness to build up large inventories of less liquid assets.

Drivers

What are the drivers of these changes in the supply of market-making services? Evidence suggests that these trends stem from a broader post-crisis response that has both cyclical and structural elements.

On the more cyclical side, as noted above, market participants confirm a reappraisal of risk tolerance among market-makers in the wake of the financial crisis and associated cutbacks in market-making activity - a finding supported by recent research (Adrian et al (2013)). Market-makers in many jurisdictions are thus raising the risk premia they demand in exchange for their services. They are also reviewing their risk management operations and are increasingly assessing the value of trades on a case by case basis.

On the structural side, regulators have taken steps to strengthen the financial system. These include requiring key market-making institutions to strengthen their balance sheets and their funding models. Such structural improvements protect the financial system by making it less likely that banks will suffer liquidity crises or that such crises will spread contagiously from one institution to another (see below). However, many market participants expect that this will come at the expense of raising market-makers' costs, which could reinforce the liquidity bifurcation described above - although that is likely to happen to different degrees across asset classes and jurisdictions (see CGFS (2014), especially Appendix 4).

Importantly, these trends are taking place just as demand for and dependence on market liquidity are on the rise. The new-issue bond market is expanding (Shin (2013)) and assets under the management of investment funds that promise daily liquidity are growing rapidly - as suggested by the increasing presence of exchange-traded funds in corporate bond markets in recent years (see also Box 2). Meanwhile, bond markets are concentrating as key participants, such as asset managers, shrink in number but expand in size.8 As a result, market liquidity may increasingly come to depend on the portfolio allocation decisions of only a few large institutions. And, more broadly, investors may find that liquidating positions proves more difficult than expected, particularly in the context of an adverse shift in market sentiment.

Implications for markets and policy

What do the changes in market-making described here mean for markets and policy? There are at least two key issues. First, reduced market-making supply and increased demand imply upward pressure on trading costs, reduced secondary market liquidity, and potentially higher financing costs in new-issue markets. Second is the question of how markets will behave under stress - that is, whether they will be able to function in an orderly fashion in response shocks or broad changes in market sentiment.

Cost of trading and issuing debt

At this stage, there is no strong evidence of a broad-based rise in trading costs (see above). In part, this may be because higher costs show up in ways that market data cannot easily detect. For example, more time may be needed to execute large trades, or different tiers of clients might have to pay different prices for trades - two trends that often come up in discussions with market participants. In addition, in the new-issue market, borrowers in many countries have benefited from favourable funding conditions in recent years. Nonetheless, perhaps unsurprisingly, market participants say that observed changes should eventually give rise to higher trading costs, even though pass-through to clients and issuers may still be limited.

One development that may have contained the pass-through of trading costs is a change in how portfolio managers execute trades. For example, trading has reportedly shifted towards splitting transactions into smaller amounts to make execution easier. However, smaller asset management firms may find it difficult to bear the costs of acquiring the technology necessary to carry out such a strategy. Thus, this trend could eventually widen the gap in trading capacity among firms, contributing to greater market tiering.

A second mitigant of underlying pressures on trading costs is the growing use of electronic trading in bond markets. Although starting from relatively low levels, given the less liquid and more heterogeneous assets traded in bond markets (as compared with, for example, equities or foreign exchange), demand is growing for the price transparency and lower transaction costs that electronic trading offers. Electronic platforms (if not single dealer-based) support market liquidity by providing participants immediate access to multiple dealers. Still, these venues are most commonly used only for a limited range of small, standardised transactions. And, ultimately, they tend to rely on the same market-makers that otherwise provide liquidity outside these platforms.

Market robustness and liquidity illusion

Will current trends in market-making render markets more vulnerable to supply-demand imbalances? The answer depends on a variety of factors, including how much market-makers' willingness to provide liquidity has changed, and whether other market participants are willing and able to fill any gap in market-making capacity.

Part of the answer lies in the realm of bank regulation. Regulatory reforms are seeking to improve bank capacity to absorb losses, limit leverage and promote more stable funding. Having more resilient banks with sufficient capital and liquidity reduces the probability of widespread liquidity crises.9 That would help make market-making more robust, though probably at lower levels of activity in normal times. In addition, better capitalisation and more limited leverage can help keep banks from building overly extended positions in financial markets, reducing the risks of sudden market reversals with large imbalances in buy and sell orders.

Another part lies in dealers' risk tolerance, which has declined in many jurisdictions since the global financial crisis. This has occurred even as liquidity premia and, hence, market-maker compensation remain largely unchanged in many markets. In the short term, for given risk-adjusted profitability targets, this implies that dealers will be less willing to take on large positions and the associated inventory risks. They may also be likely to reduce their exposure more decisively during periods of elevated market volatility. That said, their willingness to absorb major supply and demand imbalances has always been limited and should be expected to remain so (see Box 2).

Pullbacks by market-makers, in turn, provide opportunities for other market participants to step in as liquidity providers, mitigating the impact on market liquidity. But how will these alternative liquidity providers perform in strained markets? On the one hand, new liquidity providers are likely to have fewer incentives to support market liquidity under more stressed conditions, because they lack access to any ancillary revenues from their clients. On the other hand, a wider range of liquidity providers could make supply more reliable, especially in the context of electronic trading.

Nonetheless, dealers will remain the key liquidity providers in bond markets for the foreseeable future. Over time, this suggests rising bid-ask spreads relative to past levels for more illiquid assets, such as corporate bonds, to help market-makers cover their operating costs. Under a benign scenario, this would bring bid-ask spreads and other liquidity metrics more into line with actual market-making capacity and costs. This would help mitigate the risks associated with what is widely perceived as a "liquidity illusion".10 The transition to such a market environment, however, could be accompanied by strained market conditions, as suggested by recent episodes of elevated bond market volatility.

Policy implications

Policy responses to the developments reviewed above fall into two broad areas: supporting initiatives seeking more appropriately priced and robust liquidity conditions; and possible backstops addressing potential vulnerabilities under adverse scenarios.

Supporting initiatives. First, market participants and relevant authorities should work to dispel liquidity illusion - that is, the overestimation of market liquidity, particularly how easy it would be for market participants to exit from their positions in more stressed environments. From an individual market participant's point of view, liquidity conditions might seem adequate. But that liquidity could prove fragile if everybody heads for the exits at the same time - a risk that needs to be internalised by the bond investor community.11 Key to managing the resulting coordination problem is for market-makers, as well as asset managers and other investors, to improve their liquidity risk management. Dedicated liquidity stress tests are a vital tool in that regard. In addition, improved market transparency and monitoring - for example, via more detailed disclosures of market-maker inventories and risk-taking - could help market participants better understand which market segments or trades are likely to be crowded.12 In addition, policymakers may want to assess how the combined impact of regulations and other policy initiatives affect market-making and overall market robustness.

Box 2

Inventory levels and asset price sensitivity: catching the falling knife?

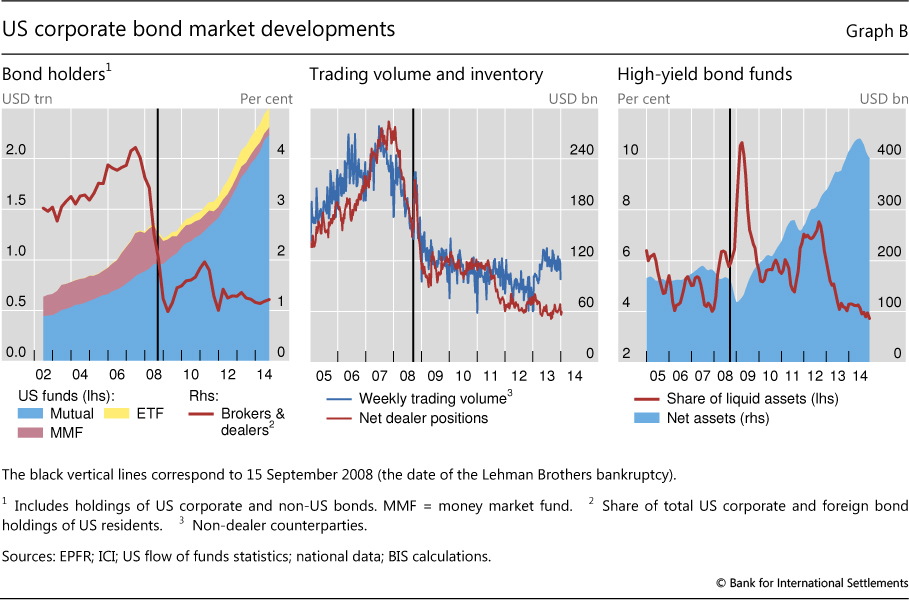

Analysts often point to shrinking dealer inventories of corporate and high-yield bonds and how they compare with flows into fixed income investment funds, particularly those that claim to provide "daily liquidity", such as mutual funds and exchange-traded funds (ETFs). US fund holdings have grown by more than $1 trillion over the past five years. At the same time, net dealer holdings have contracted significantly since the onset of the financial crisis (Graph B, left-hand and centre panels). Do these developments mean that markets are less resilient to shocks, ie that liquidity risks have increased? And how important are market-making trends in determining the liquidity of these markets?

One reading of shrinking dealer inventory is that market-makers are less likely to accommodate any sales from return-sensitive investors. For example, in today's low interest rate environment, what would happen if many investors wanted to trim their bond holdings because they expected yields to rise? The key factors here are market-maker risk limits and whether market-makers were prepared to maintain or increase inventories in response to a shock. Lower risk tolerance and tighter capital management among market-makers clearly lower their willingness to commit their balance sheets. Yet an important notion is that one cannot expect market-makers to deliberately expose themselves to losses when market valuations change (often referred to as "catching the falling knife"). Dealers tend to cut back their inventory decisively when markets are stressed. Indeed, that is what happened when US bond yields spiked in mid-2013 (Adrian et al (2013)). Thus, market-makers are not likely to accommodate broad changes in market sentiment, even if they readily provide liquidity under normal circumstances.

In the current environment, therefore, narrow bid-ask spreads for market-makers should not be seen as a sign that liquidity risks are low. Nor do lower inventories imply increased liquidity risks, as suggested by rising trading volumes over recent years (Graph B, centre panel). Instead, strong demand in fixed income markets has meant that liquidity risks have shifted to investors. While many of these are well equipped to bear these risks, there are signs that liquidity buffers have been trending down in some market segments (Graph B, right-hand panel). This suggests that some asset managers may be ill-prepared to manage bigger swings in market sentiment.

Second, sovereign issuers may want to make sure that arrangements are in place to give market-makers appropriate incentives to support liquidity in the secondary market. Private debt issuers, in turn, could explore the admittedly limited potential for greater standardisation of issuance practices to help concentrate liquidity in a smaller number of securities.

Backstops. Given moral hazard concerns, regular liquidity-providing activities are likely to remain central banks' main line of defence in stressed environments. However, as suggested in CGFS (2014), establishing or expanding regular securities lending facilities could be considered as an additional option to improve, as needed, liquidity in key markets during times of stress and to support the robustness of the associated repo markets. Considering other, more direct measures13 to support market functioning would give rise to even trickier cost-benefit trade-offs (eg due to the risk of distorting economic incentives for market participants). Policymakers would have to carefully assess these trade-offs if they were to consider whether and under what conditions they might be prepared to adjust existing backstops in the future.

Conclusion

A variety of cross-currents are roiling the market-making world today. It is difficult to predict what the effects will be in different parts of the world and for different asset classes. But market-making practices are clearly evolving, putting upward pressure on bid-ask spreads and trading costs, and causing activity to concentrate in the most liquid instruments and move away from the less liquid ones. This could make market liquidity more fragile in the short term, especially in the current low interest rate environment, in which new-issue volume and the participation of interest rate-sensitive investors have increased. Yet industry and policy efforts can help to ensure that over time the pricing of market-making services becomes more consistent with the actual costs and risks involved. For some markets, the narrow spreads seen in the past may have to give way to more realistic premia for providing liquidity to the market.

References

Adrian, T, M Fleming, J Goldberg, M Lewis, F Natalucci and J Wu (2013): "Dealer balance sheet capacity and market liquidity during the 2013 selloff in fixed-income markets", Liberty Street Economics, 16 October.

Bank for International Settlements (2005): "So far, so good", 75th Annual Report, June, Chapter I.

--- (2013): "Markets precipitate tightening", BIS Quarterly Review, September, pp 1-11.

--- (2014): "Buoyant yet fragile?", BIS Quarterly Review, December, pp 1-12.

Borio, C (2009): "Ten propositions about liquidity crises", BIS Working Papers, no 293, November.

Comerton-Forde, C, T Hendershott, C Jones, P Moulton and M Seasholes (2010): "Time variation in liquidity: the role of market-maker inventories and revenues", Journal of Finance, vol 65(1), pp 295-331.

Committee on the Global Financial System (1999): "Market liquidity: research findings and selected policy implications", CGFS Papers, no 11, May.

--- (2014): "Market-making and proprietary trading: industry trends, drivers and policy implications", CGFS Papers, no 52, November.

Duffie, D (2012): "Market making under the proposed Volcker Rule", Rock Center for Corporate Governance at Stanford University Working Paper, no 106, January.

Fleming, M (2003): "Measuring Treasury market liquidity", Federal Reserve Bank of New York, Economic Policy Review, vol 9(3), September, pp 83-108.

Huberman, G and D Halka (2001): "Systematic liquidity", Journal of Financial Research, vol 24(2), pp 161-78.

Keynes, J (1936): The general theory of employment, interest and money.

Madhavan, A (2000): "Market microstructure: a survey", Journal of Financial Markets, vol 3(3), pp 205-58.

McKinsey and Company (2012): "Searching for profitable growth in asset management: it's about more than investment alpha", September.

Nesvetailova, A (2008): "Three facets of liquidity illusion: financial innovation and the credit crunch", German Policy Studies, vol 4(3), pp 83-132.

Shin, H S (2013): "The second phase of global liquidity and its impact on emerging economies", remarks at the 2013 Asia Economic Policy Conference at the Federal Reserve Bank of San Francisco.

Tierney, J and K Thakkar (2015): "Corporate bonds: the hidden depths of liquidity", Deutsche Bank - Konzept, January, pp 26-35.

Tucker, P (2009): "The repertoire of official sector interventions in the financial system: last resort lending, market-making, and capital", speech at the 2009 Bank of Japan International Conference, Tokyo, May.

1 The views expressed in this article are those of the authors and do not necessarily reflect those of the BIS or the Committee on the Global Financial System. We are grateful to Denis Beau, Claudio Borio, Dietrich Domanski, Michael Fleming, Masazumi Hattori, Robert McCauley, Christian Upper, Sam Zuckerman and the members of the recent CGFS Study Group for useful comments and inputs as well as to Mario Morelli, Jhuvesh Sobrun and José María Vidal Pastor for able research assistance.

2 The report, entitled Market-making and proprietary trading: industry trends, drivers and policy implications, was prepared by a Study Group chaired by Denis Beau (Bank of France). The CGFS is a BIS-based committee of senior central bank officials that monitors developments in global financial markets for central bank Governors (see www.bis.org/about/factcgfs.htm).

3 The iBoxx US dollar corporate bond index, for example, comprises more than 4,200 bonds from 1,200 issuers (associated with 900 companies), all with varying credit ratings, coupons and other structural features; see Tierney and Thakkar (2015).

4 For more detail, see, for example, Madhavan (2000) and Duffie (2012).

5 The recent CGFS Study Group conducted series of interviews with market-makers as well as representatives of the broader banking and asset management communities. For more detail, see CGFS (2014).

6 According to FINRA's TRACE data, the average transaction size declined from more than $25 million in 2006 to about $15 million in 2013.

7 While foreign banks in Australia accounted for nearly 50% of the total amount of banks' net trading securities in 2006, their share fell to less than 13% by end-2013.

8 For example, according to McKinsey (2012), the top 20 US asset managers increased their share of global assets under management from 22% in 2002 to almost 40% by 2012.

9 Several notions of illiquidity contagion have been studied in the literature; see, for example, Huberman and Halka (2001) and Comerton-Forde et al (2010).

10 "Liquidity illusion" describes a situation in which market participants systematically underestimate the cost of liquidating the assets that they hold; see Nesvetailova (2008).

11 Or, as Keynes (1936) would have put it, "there is no such thing as liquidity of investment for the community as a whole".

12 Naturally, disclosure requirements for market-makers will have to strike a balance between improving market transparency and mitigating the risk that market participants can trade against market-makers based on the disclosed information (eg by disseminating sufficiently aggregate data and at suitable reporting lags).

13 Such more direct central bank interventions in securities markets could include outright purchases and sales of securities to support the functioning of particular markets that are judged as critical to financial stability. These measures, which would be considered only once other measures have been exhausted, are sometimes referred to as "market-making of last resort". See, for example, Tucker (2009).