II. High public debt and shifting financial markets: challenges for central banks

- Chapter II: Data behind the graphs

- Press release: Global economic pressure points call for policy discipline: BIS

Key takeaways

- Central banks face mounting challenges from the interplay of near record-high public debt with the growing role of non-banks in sovereign debt markets. This new fiscal-financial stability nexus amplifies and accelerates the transmission of market stress.

- More frequent and sharper shifts in sovereign bond values can tighten financial conditions, while inflation expectations may also be disrupted. At the same time, high debt levels complicate monetary policy transmission. Central banks may need to intervene more frequently to address market dysfunction.

- While central banks have navigated these challenges effectively, lasting success depends on sound fiscal and financial foundations. Public finances must follow a credible, sustainable path. Financial stability risks should be addressed with consistent regulation, and central bank backstops should remain temporary, targeted and reversible.

Introduction

Following the Great Financial Crisis (GFC) and the Covid-19 pandemic, public debt has risen to near post-World War II highs in many economies. And it might climb higher, with current fiscal deficits still large and high fiscal pressures coming from ageing populations and public investment needs. Alongside this debt surge, the structure of sovereign bond markets has changed markedly. Hedge funds are playing an increasing role in intermediating government debt, often through highly leveraged and funding-dependent strategies that hinge on both banks and other non-bank financial institutions (NBFIs).

These shifts have created a new fiscal-financial stability nexus. While the traditional bank-sovereign nexus remains important, stress can now spread rapidly and more widely – via funding markets, across borders and between banks and non-banks. Government bond market liquidity can be ample for prolonged periods, yet dry up quickly in response to shocks, raising borrowing costs. As a result, fiscal space may shrink well before any limit implied by long-run fundamentals is reached.

Against this backdrop, central banks might find fulfilling their mandates more difficult. Three challenges, in particular, are likely to intensify.

First, as investors reassess fiscal sustainability and market liquidity, sovereign yields may swing more sharply and frequently. Such fiscal risk repricing can tighten financial conditions quickly and weigh on demand, especially if amplified by NBFI deleveraging. The effects on inflation are, however, more uncertain. Weaker demand may be disinflationary, but a reassessment of fiscal sustainability may also become inflationary if it triggers exchange rate depreciation or disrupts inflation expectations. These inflationary channels are more likely to operate when monetary policy credibility is weak.

Second, high public debt can make monetary transmission more complex and uncertain. When this debt is high, rate hikes raise government interest payments and transfer income to bondholders, supporting demand and attenuating the contractionary effect. But higher interest payments can also worsen the fiscal outlook, lift risk premia and tighten financial conditions. Debt maturity influences the balance between these channels: shorter maturities speed up the pass-through to fiscal costs and bondholder income, while longer maturities expose bondholders to valuation losses that can trigger deleveraging and tighten credit.

Finally, central banks may need to step in more often to address market dysfunction in repurchase agreement (repo) and government bond markets. But repeated interventions, through largescale purchases or lending operations, could encourage investors to take on more risk and borrow more, increasing the fragility of the financial system. They could also weaken the market discipline that constrains fiscal excess. And, in an inflationary environment, such interventions could make it harder to stabilise inflation.

Central banks have so far navigated these challenges well, but lasting success requires sound fiscal and regulatory foundations. This points to three policy priorities. On the fiscal front, governments must move towards a more symmetric fiscal policy, supporting the economy in downturns but rebuilding fiscal buffers in expansions. For countries with high debt levels, credible medium-term fiscal frameworks are needed to ensure that fiscal consolidation takes place. On the regulatory side, authorities should pursue "congruent regulation". This would imply regulatory frameworks that apply similar stringency to financial intermediaries posing similar risks to financial stability, regardless of their legal form or business model. Given NBFI vulnerabilities, it is especially important to consistently tighten safeguards against excessive leverage, liquidity mismatches and fragile funding structures that can amplify stress in government bond markets. Finally, central bank liquidity backstops to address market dysfunction should be carefully designed to be temporary, targeted and easily reversible, to avoid blurring the monetary policy stance, encouraging excessive leverage or entrenching the very fragilities they are meant to address.

These policy actions reinforce each other. Stronger fiscal frameworks reduce fiscal risk and ease pressures on financial markets. A more resilient financial system improves fiscal space and makes it less vulnerable to liquidity shocks and deleveraging. Credible monetary policy preserves price stability and supports financial conditions, with positive spillovers for both fiscal policy and financial stability.

Near record-high public debt and evolving fiscal space

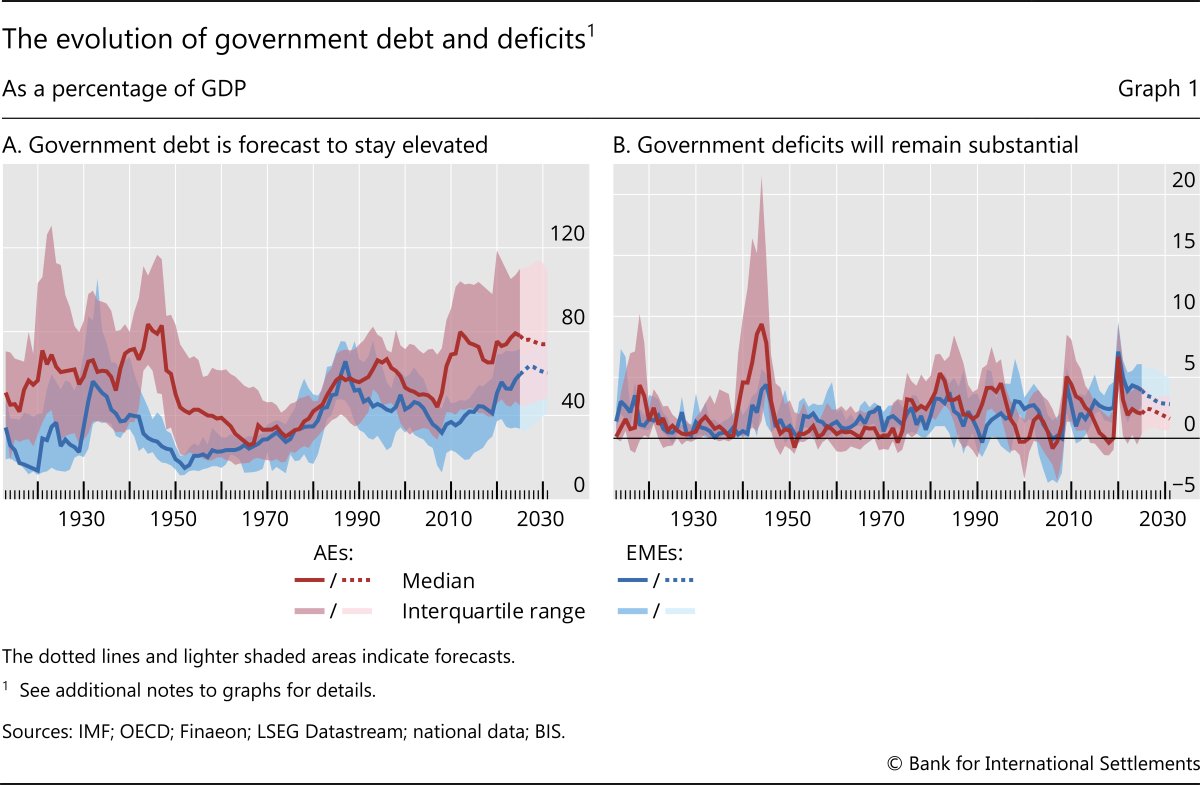

Public debt in many economies has risen to near post-World War II highs (Graph 1.A) and, with large current fiscal deficits (Graph 1.B), it is expected to stay elevated in the coming years. The high level of debt largely reflects a series of major global shocks over the past two decades. In the wake of the GFC, the deep and prolonged recession eroded tax revenues and lifted cyclical spending. At the same time, governments enacted sizeable discretionary stimuli to support demand and facilitate private sector deleveraging. Many economies then shifted to fiscal consolidation in the early 2010s, most notably between 2011 and 2014, but the pandemic and Russia's invasion of Ukraine prompted another round of large fiscal expansion to protect jobs and preserve the purchasing power of households and firms. Debt levels could climb even higher if the energy supply disruption caused by the conflict in the Middle East proves to be protracted (Chapter I).

Debt increases, however, have varied significantly across countries, reflecting differences not only in exposure to shocks but also in fiscal policy responses. As recoveries took hold, divergences persisted. In several jurisdictions, fiscal consolidation has been insufficient or delayed, while in others – notably in the United States – fiscal policy turned strongly expansionary in the years preceding the pandemic. Empirical analysis confirms that fiscal policy has generally become less responsive to rising debt since the GFC and remained highly asymmetric over the business cycle, expanding aggressively in downturns but adjusting little during expansions (Box A). Some countries, however, bucked this trend. While large advanced economies (AEs) and several emerging market economies (EMEs) have driven the rise in global debt aggregates, several smaller economies have managed to contain debt and deficit levels.

Looking ahead, fiscal pressures are set to persist. Ageing populations will continue to exert upward pressure on pension and healthcare expenditures in many countries, while demands for higher public investment – especially infrastructure, defence and renewable energy – are intensifying. Without offsetting measures such as higher government revenues, other public spending cuts or changes in the interest rate-growth differential, these spending pressures imply a substantial increase in public debt across jurisdictions beyond 2031.1

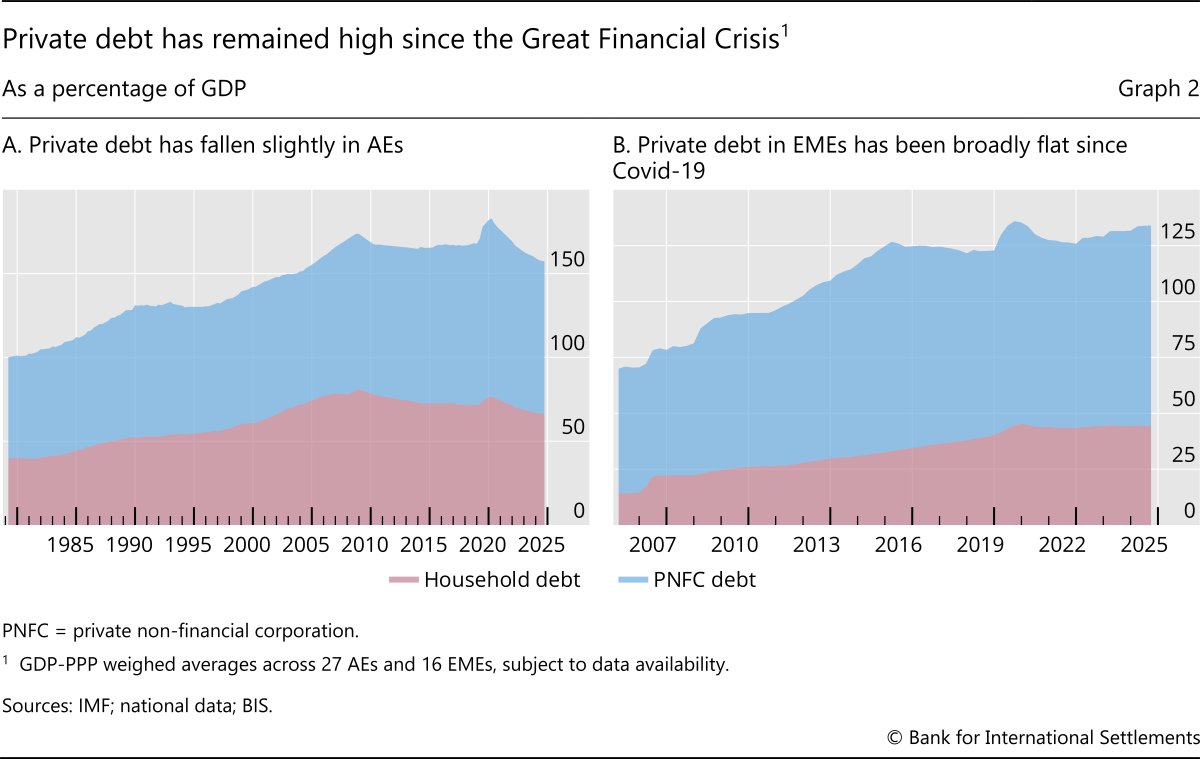

Further strains may arise from the materialisation of contingent liabilities.2 In particular, public debt may increase due to the fiscal costs of future financial crises, which tend to be linked to the scale of private non-financial sector debt.3 While private debt has fallen slightly since the GFC, it remains historically high in several AEs (Graph 2). Moreover, it has increased in several small open AEs such as Sweden and Switzerland, as well as in several EMEs, with notable increases in Brazil and China. Additional risks to public debt could arise from the losses incurred by state-owned enterprises and subnational governments, which are often backed by explicit and implicit guarantees, and by the fiscal burden of natural disasters, which may intensify in the future due to climate change.

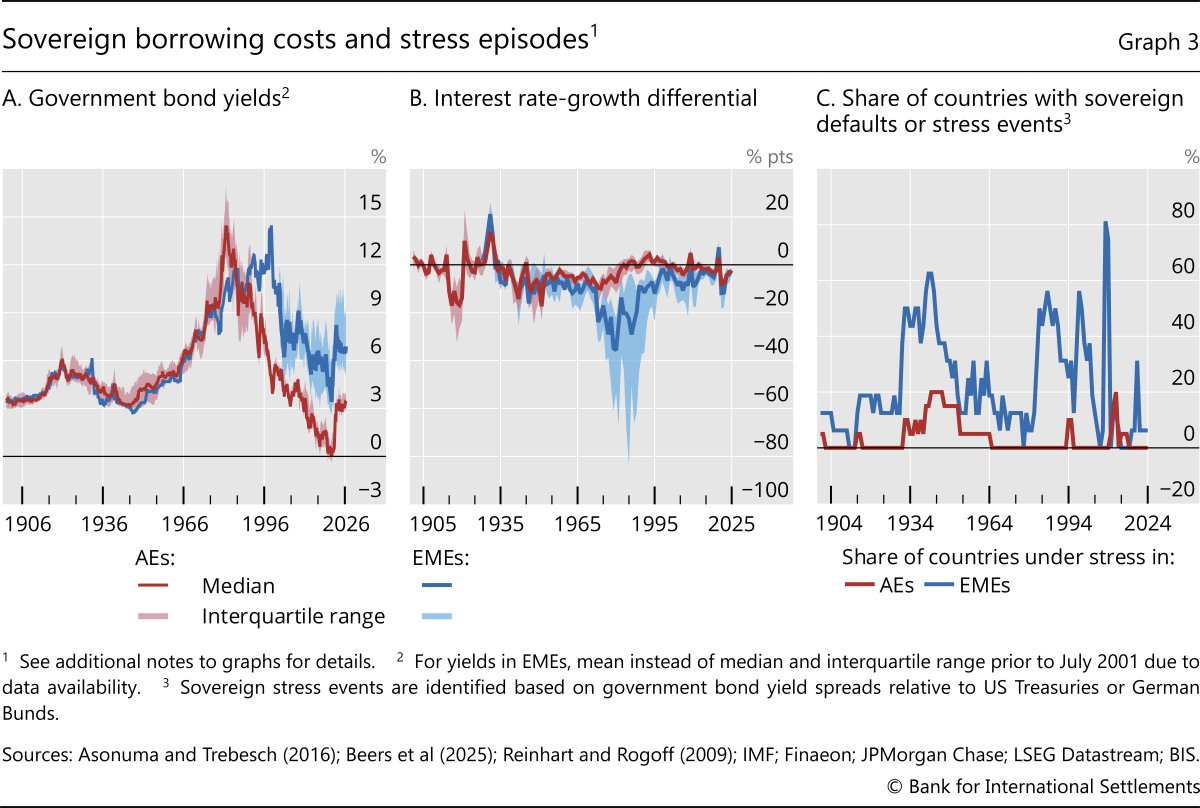

Elevated public debt and rising fiscal pressures coincide with a less benign financial environment than the one that prevailed in the aftermath of the GFC. Sovereign bond yields in AEs and EMEs are significantly higher today than at their trough during the pandemic (Graph 3.A), reflecting higher real rates and term premia. GDP growth has also slowed from post-pandemic peaks. As a result, the interest rate-growth differential has narrowed (Graph 3.B).4 Together with higher debt stocks, these developments have already pushed up interest payments as a share of GDP across many countries, with interest costs set to become one of the largest spending items in many AEs and EMEs (Chapter I).5 They have also led some countries to shorten the maturity of newly issued debt, albeit from historically long average maturities.

Whether fiscal pressures will prove manageable depends on how borrowing costs evolve. Two factors are key: (i) the structural demand for government bonds, which is determined by demographic trends, productivity growth, household saving behaviour and fiscal policy itself, especially the generosity and design of public pension systems; and (ii) the capacity of the financial system to intermediate that demand, which can shift rapidly in response to shocks and compress fiscal space well before any limit implied by long-run fundamentals is reached.

Structural demand for government debt is likely to remain strong, but its long-run path is uncertain. Falling fertility rates, rising longevity and the shift towards a defined contribution pension system should boost aggregate saving and demand for safe assets, suggesting that interest rates could remain low relative to income for a prolonged period.6 On that basis, some studies argue that many economies should retain ample fiscal space despite historically high debt levels.7 However, as populations age and shift from saving to dissaving, while also demanding more health and social services, aggregate saving may fall, putting upward pressure on real interest rates – although the timing and scale of this fall are highly uncertain.8 In addition, an escalation in geopolitical tensions could disrupt flows of capital and labour and reduce the perceived safety of assets, potentially reversing downward interest rate trends sooner than demographics and other structural factors alone would suggest.9

Financial intermediation capacity introduces a more abrupt source of fiscal risk. The capacity of banks and NBFIs to intermediate and hold government debt may vary over time and can be affected by shocks to either the government or the financial sector. Fiscal space may therefore shift and borrowing costs may spike well before any limit implied by longterm structural factors is reached (Box B). Furthermore, the same deterioration in fundamentals can compress fiscal space far more severely when the financial system is fragile or when debt is high. Hence, debt tolerance is heterogeneous and can change over time: a debt burden that appears manageable in one country or period may become fragile in another as the structure of financial intermediation and financial conditions evolve.10

This makes it difficult to identify a single threshold beyond which debt becomes unsafe. Empirical evidence nevertheless points to several warning indicators of sovereign distress. First, high debt ratios can indicate solvency vulnerabilities, while large gross refinancing needs and short debt maturities signal rollover risk.11 Likewise, a high proportion of debt denominated in foreign currency or linked to inflation or short-term interest rates can heighten vulnerability to adverse exchange rate, inflation or interest rate shocks. Large current account deficits can also signal dependence on external financing that can reverse abruptly, as seen in some euro area economies in 2010–12 and several crises in emerging markets in the 1980s and 1990s. By contrast, the interest rate-growth differential seems to have limited predictive power for sovereign debt crises. Such crises have often occurred when this differential was low or negative (Graphs 3.B and 3.C). Moreover, this differential tends to rise only shortly before crises, leaving little time for corrective policy actions.12

Still, the financial system evolves continuously, so warning indicators and policy prescriptions must adapt to changing conditions. Debt maturity is a case in point: short maturities heighten rollover risk, yet longer maturities do not guarantee financial resilience. If duration risk is concentrated in the private sector, adverse shocks can trigger deleveraging and weaken market liquidity, amplifying the tightening of financial conditions. Similarly, issuing debt in domestic currency mitigates exchange rate risk but does not fully insulate governments from shifts in global financial conditions.

A new form of fiscal-financial stability nexus

Alongside the public debt surge, the structure of the global financial system has evolved, reshaping the link between public finances and financial stability. Near record-high public debt is now increasingly held and intermediated by NBFIs, whose balance sheets, funding models and risk management practices differ markedly from those of banks. While there is a broad variety of NBFIs and greater NBFI participation does not in itself imply fragility, the growing role of leveraged and funding-dependent NBFIs increases the system's sensitivity to liquidity shocks. This has given rise to a new fiscal-financial stability nexus, with amplification channels that operate even when bank solvency risks are contained.

The increasing role of NBFIs in government bond markets

The NBFI classification captures very different investor types. Realmoney investors such as many insurance companies and pension funds provide longterm demand and deepen markets, and they can help to diversify risks, including across borders. Sovereign bond intermediation, however, increasingly involves leveraged hedge funds, which are highly active in futures and spot markets and are financed via repos, often supplied by banks. Other segments, notably money market funds (MMFs) and open-ended bond funds, can face redemption-driven liquidity strains that can also transmit and amplify shocks. Stablecoin issuers are a new emerging type of NBFI. They also have a large footprint in the bond markets of some jurisdictions and bring new vulnerabilities (Chapter III).

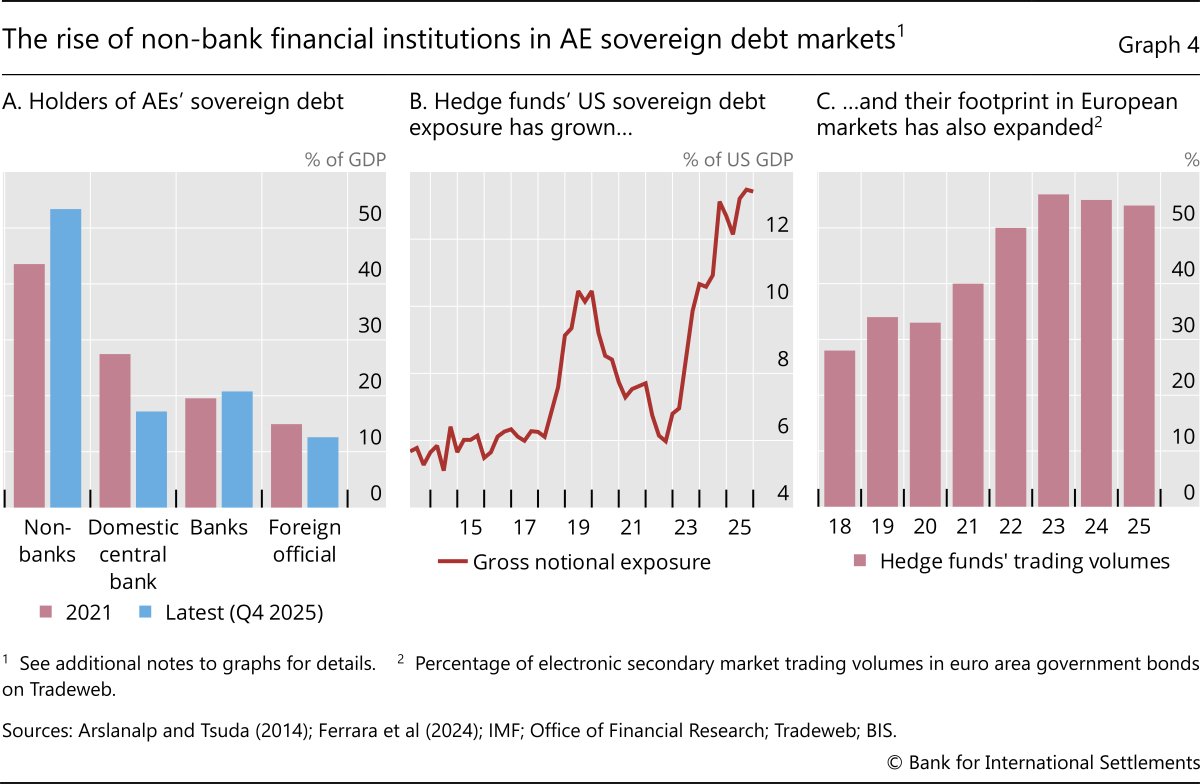

NBFIs in general have become the largest holders of sovereign debt in AEs, driven by a range of factors. Their share of total sovereign debt holdings rose from 44% in 2021 to 53% in 2025 (Graph 4.A). Several forces help to explain this shift. On the supply side, large and persistent fiscal deficits, reinforced by the pandemic, lifted sovereign bond issuance, outpacing growth in credit to the private sector.13 On the intermediation side, post-GFC changes in regulation and business models made balance sheet-intensive market-making more costly for banks. While banks continue to play a central intermediation role, their capacity to warehouse risks has not kept pace with the growth of sovereign debt. At the same time, capital markets expanded, with deeper derivative and repo markets. Easy access to secured financing coupled with persistent relative-value opportunities, in turn, supported the demand from hedge funds. Another factor on the demand side was rising long-term liabilities of insurance companies and pension funds, which have supported demand for government debt as a safe, liquid asset used for duration management and hedging.14 In addition, in recent years, higher risk-free rates also increased the appeal of fixed income in strategic asset allocations.

At the same time, official demand waned. As quantitative tightening progressed over 2022–25, the share of government bond holdings by domestic central banks fell from 27% to 17% and that of the foreign official sector from 15% to 13%. This increased the amount of sovereign debt that had to be absorbed by private investors.

Among private investors in AEs, leveraged hedge funds have become pivotal in intermediating sovereign debt. Measured relative to GDP, US sovereign debt exposures of hedge funds in the United States have more than doubled since 2022 as leveraged relative-value strategies expanded rapidly (Graph 4.B).15 The rise in hedge funds' trading footprint is also evident in other major AEs. In the euro area, hedge funds' share of electronic trading in government bonds has increased markedly (Graph 4.C), with similar patterns observed in Canada and the United Kingdom.

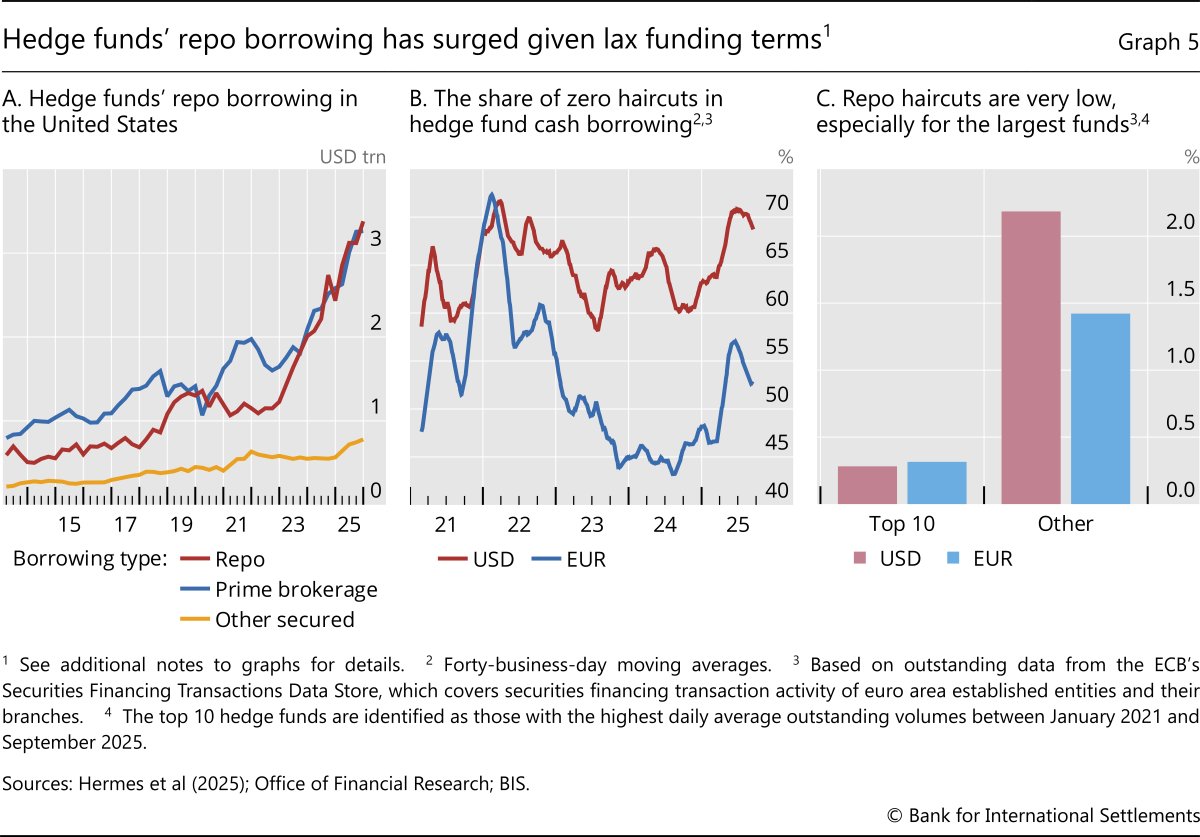

The large-scale emergence of hedge funds as core intermediaries in government bond markets has given rise to new financial stability vulnerabilities. To boost returns on small price differences, hedge funds employ high leverage, typically funded through short-term repo borrowing and facilitated by prime brokerage and derivatives intermediation (Graph 5.A). This reliance on funding-dependent liquidity – abundant in calm conditions but prone to evaporate when risk capacity tightens – leaves core markets more exposed to sudden deleveraging and episodes of market dysfunction.

Lax funding terms amplify these vulnerabilities, especially for the largest hedge funds. In recent years, a large share of repos has been extended at zero or near-zero haircuts, effectively allowing borrowing against most of the market value of collateral. Around 70% of bilateral USD repos and more than 50% of bilateral EUR repos with hedge funds are transacted at zero haircuts (Graph 5.B).16 Average haircuts are compressed, and the most favourable terms are concentrated among the largest funds (Graph 5.C). These funding structures enable high leverage but leave positions acutely sensitive to shifts in margins, haircuts and derivatives pricing. When funding terms tighten – as they did during the March 2020 margin calls or the April 2025 unwind of swap-spread trades – rapid deleveraging and fire sales can amplify yield spikes.

Beyond hedge funds, other NBFIs can also amplify stress in government bond markets. For instance, insurance companies and pension funds use interest rate swaps and repo-financed positions to manage the maturity mismatch of assets and liabilities. A rise in yields can reduce the value of these hedges and increase margin calls. To meet these, insurance companies and pension funds may, in turn, sell their most liquid assets – frequently government bonds – which can add to upward pressure on yields, increasing margin calls further. Separately, some MMFs and open-ended funds exhibit liquidity mismatches: they offer daily redemptions while holding assets whose market liquidity can dry up in stress. In periods of outflows, such funds may sell government bonds held for liquidity management to meet redemptions, which can lead to feedback loops and impair market functioning. Such dynamics were evident during the March 2020 "dash for cash".17

Since the footprint of NBFIs in sovereign debt markets has widened, the traditional bank-sovereign nexus may have changed. The bank-sovereign nexus came to the fore during the European sovereign debt crisis more than a decade ago. Higher sovereign yields triggered mark-to-market losses on banks' sovereign bond holdings and eroded banks' capital and intermediation capacity, reinforcing the rise in yields.

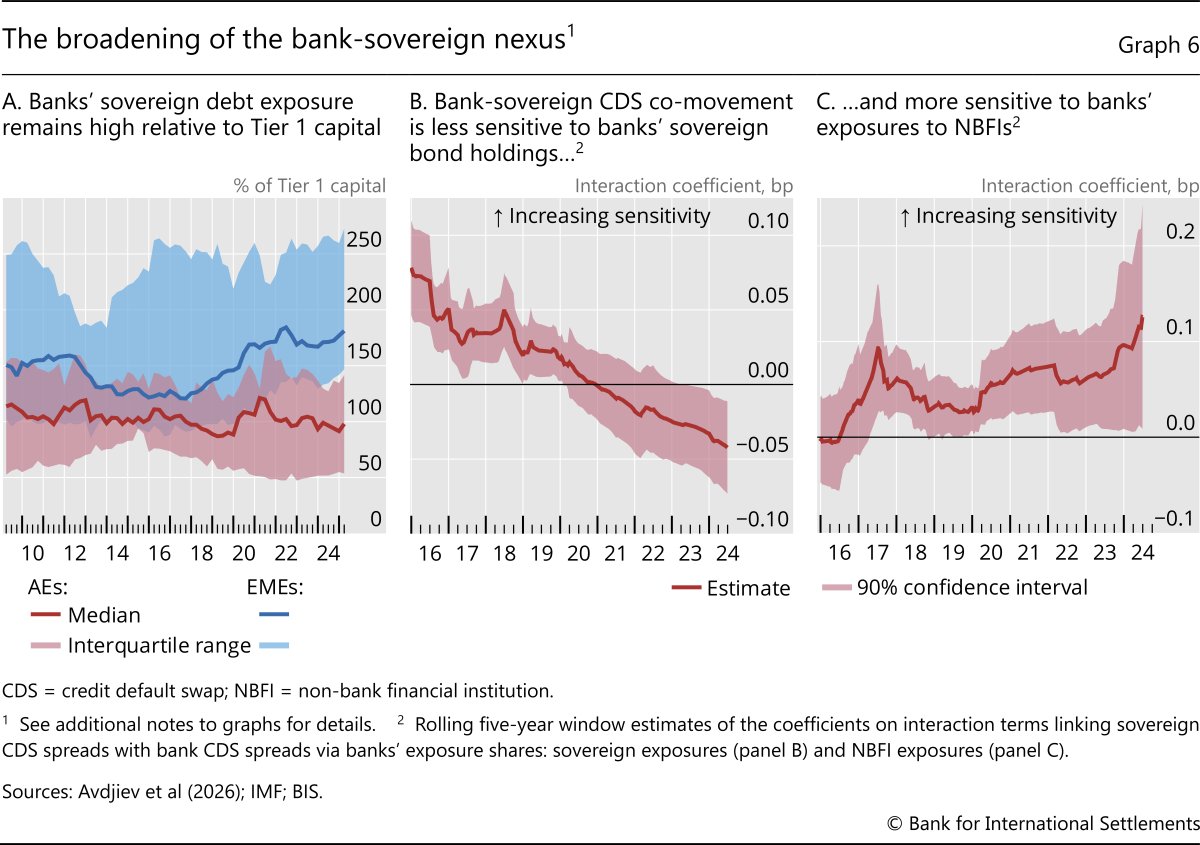

Banks' sovereign debt exposures seem to suggest that the bank-sovereign nexus remains an important potential amplification channel, in particular in EMEs. Banks' share of sovereign debt holdings has been broadly stable at about 20% over the past five years (Graph 4.A). And exposures remain material: banks' sovereign bond holdings relative to Tier 1 capital are comparable to levels seen 10–15 years ago (Graph 6.A). As of 2025, across countries, the median ratio of banks' sovereign exposures to Tier 1 capital is around 180% in EMEs and just under 100% in AEs.

However, there is evidence that the direct bank-sovereign nexus may have become less pronounced than a decade ago. For instance, cross-country bank-level evidence from Europe shows that bank-sovereign risk co-movement has become less dependent on banks' direct sovereign bond holdings (Graph 6.B). The post-GFC regulatory reform agenda has played an important part in reducing the strength of the bank-sovereign nexus. Banks now hold more and better-quality capital, maintain larger liquidity buffers and rely on more stable funding sources, significantly increasing the overall resilience of the financial system.

At the same time, banks' interconnections with NBFIs seem to have created indirect transmission channels from sovereign risk to banks.18 Banks provide repo financing, prime brokerage and derivatives intermediation to hedge funds, asset managers, insurers and pension funds. They also extend credit lines and offer collateral and margin services. On the liability side, NBFIs supply a meaningful share of banks' funding – through MMF deposits, purchases of bank paper and secured finance. All these NBFI linkages can expose banks indirectly to considerable sovereign risk. Evidence from the same European banks suggests that banks' exposures to NBFIs have become a significant determinant of the co-movement between bank and sovereign credit default swap (CDS) spreads over the past few years (Graph 6.C).19

Market functioning and fiscal policy interactions

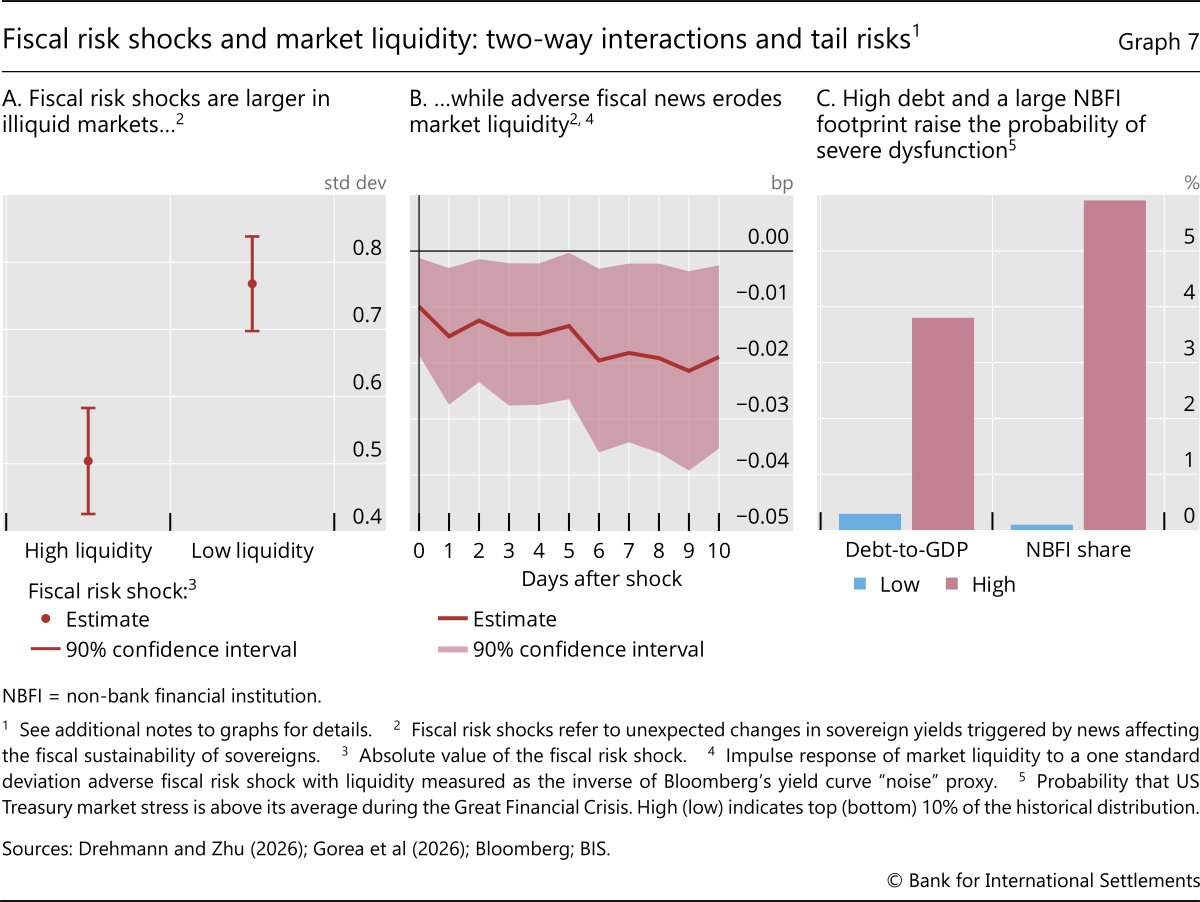

A critical dimension of the new fiscal-financial stability nexus is the interactions between fiscal risks, sovereign bond market functioning and intermediaries' balance sheet health (Box B). These are multifaceted. Take a negative shock that leads markets to reassess the fiscal sustainability of a jurisdiction. In illiquid conditions, when intermediaries' balance sheet capacity is strained, the impact on yields will be higher than otherwise. At the same, the initial shock will also tighten margins and compress intermediaries' risk-bearing capacity, prompting deleveraging, which will further impair market functioning. Empirical estimates confirm this interaction: the absolute magnitude of fiscal surprises is larger in illiquid markets (Graph 7.A), and adverse fiscal surprises, in turn, erode market liquidity (Graph 7.B).

The new nexus is also evident from the fact that high levels of public debt and a large footprint of NBFIs can significantly increase the likelihood of market dysfunction. This is, for example, the case in the US Treasury market – one of the most critical financial markets. Estimates indicate that the probability of experiencing a stress event similar to the GFC within the next three months is about 10 times higher when the ratio of public debt to GDP is high than when it is low (approximately 3.8% versus 0.3%). Likewise, the probability of such an event rises considerably when the share of NBFIs is high (Graph 7.C).

Fiscal space can erode quickly as the fiscal-financial stability nexus unfolds. In general, the interactions make it hard to cleanly separate the impact of a fundamental fiscal shock from the subsequent amplification due to market dysfunction. But the 2022 UK gilt episode, for instance, illustrates quantitatively how market dysfunction amplified yields beyond the underlying fiscal shock. Estimates indicate that forced liability-driven investment (LDI) sales generated peak price discounts of around 7%, with roughly half of the post-announcement price drop reflecting fire sales beyond the underlying fiscal surprise.20 Outside the United Kingdom, similar dynamics have been documented in core bond markets, including during the March 2020 US dash for cash and, more recently, the April 2025 rates volatility, when margin spirals and dealer balance sheet constraints contributed to sharp moves in yields.21

International spillovers and the FX-repo link

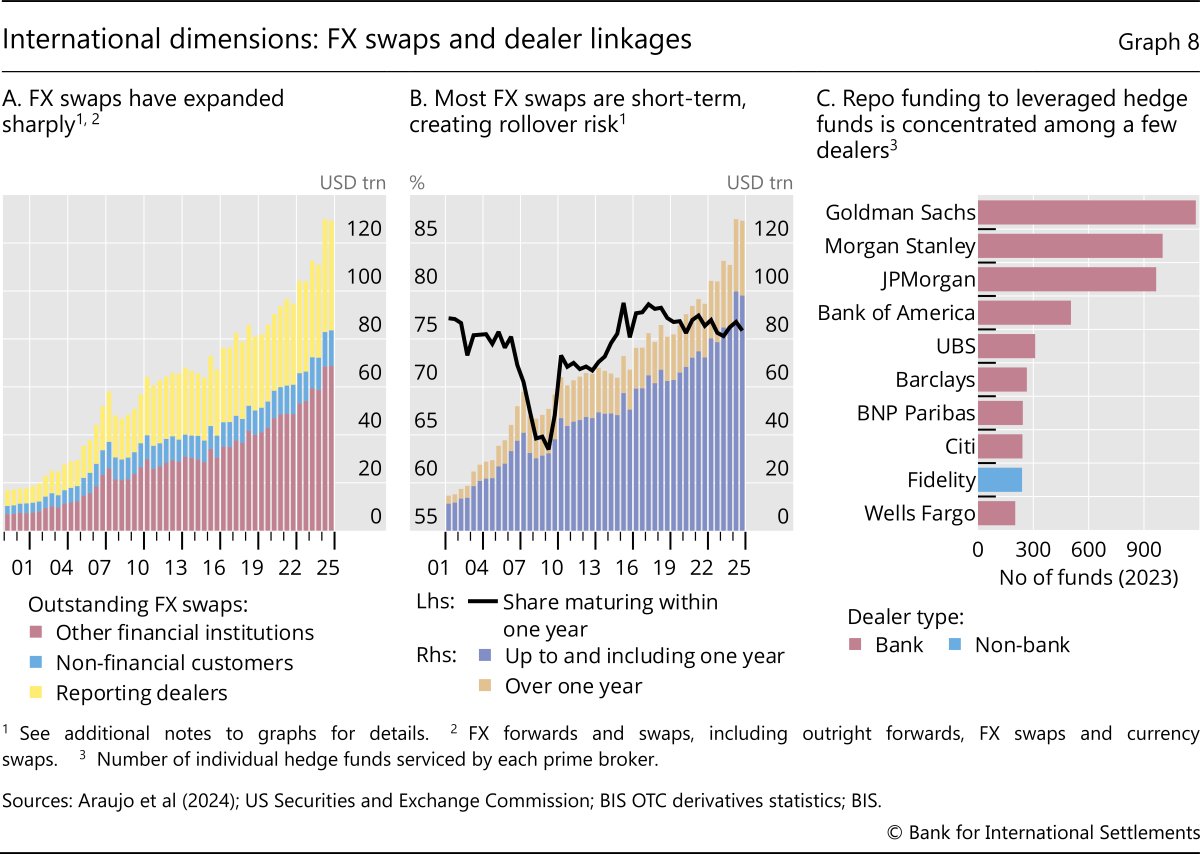

Cross-border, foreign exchange (FX) hedged positions create additional fragility beyond the domestic channels discussed above, particularly for USD exposures held by non-US investors. Asset managers, pension funds and insurers commonly hedge the currency risk on USD assets with short-dated FX swaps and forwards. The FX derivatives market has expanded rapidly since the GFC. Outstanding FX swaps, forwards and currency swaps reached about $130 trillion at the end of 2025, up from about 50 trillion in 2009. Growth has been the fastest among financial counterparties (Graph 8.A, red bars). Most contracts are short-term – roughly three quarters mature within one year (Graph 8.B). Hedging long-dated assets with such short-dated swaps transforms currency risk into rollover risk. Abrupt shifts in FX swap market conditions – reflecting dealer balance sheet constraints, margin changes or liquidity squeezes – can thus trigger funding stress and portfolio outflows, raising local currency sovereign yields.

Tight linkages between the FX swap and repo markets amplify these spillovers. Major dealer banks intermediate in both markets and substitute across them as balance sheet constraints tighten. While FX swaps are largely off balance sheet, both activities draw on dealers' risk budgets, so stress in one market can curtail capacity in the other.22 When FX swaps are not rolled over, asset managers must source dollars to close positions, which can trigger dollar funding strains. This dynamic was evident in March 2020.23 Concentration adds to the fiscal-financial stability nexus: a small number of dealers account for the bulk of repo lending to leveraged hedge funds (Graph 8.C), increasing the risk that strains propagate quickly across funding markets and jurisdictions, with amplified yield pressure.

In EMEs, these international spillovers may interact with domestic market structure and intermediation constraints. Although many EMEs have reduced foreign-currency borrowing by developing local-currency sovereign bond markets, this has not eliminated vulnerability to external financial shocks. Rather, as in "original sin redux", currency and duration risk are transferred to foreign investors, whose outflows can push up local-currency yields when the dollar appreciates or global risk appetite deteriorates.24 Because many EMEs still have relatively shallow domestic institutional investor bases and thin hedging markets, the retreat of foreign investors can leave domestic banks and other domestic investors to absorb a larger share of sovereign issuance, reinforcing the link between sovereign stress, bank balance sheets and domestic financial conditions.

When fiscal and financial risks reach the central bank

High public debt and the broader fiscal-financial stability nexus described above are likely to complicate the task of central banks. Larger debt stocks make public finances more sensitive to monetary policy decisions, while persistent fiscal pressures or strains can feed more directly into inflation expectations and financial conditions.25

Such interactions have arisen before. In the 1980s and 1990s, for example, several EMEs across Latin America and the Russian Federation, saw fiscal imbalances, fragile banking systems and currency mismatches erode monetary credibility, trigger exchange rate adjustments and, in several cases, fuel high inflation. In the euro area, during the 2010–12 sovereign debt crisis, the bank-sovereign nexus amplified initial fiscal concerns into broader financial stress, prompting extraordinary monetary measures.26

What is new is the emergence of these links in several major AEs where fiscal sustainability had rarely been in doubt, alongside significant changes in the structure of the financial system in these and other economies. As a result, many central banks now face a more complex and less predictable environment.

Three interrelated challenges, in particular, stand out. First, fiscal risk could be repriced more frequently and abruptly, while the effects of fiscal policy on activity and inflation could become more sensitive to financial conditions and shifts in inflation expectations. Second, monetary policy transmission may increasingly depend on fiscal conditions and the private sector's exposures to sovereign debt, with the level and maturity profile of public debt and its distribution across investor types becoming more important. Finally, central banks may be called upon more often to stabilise government bond markets. Yet frequent interventions risk blurring the policy stance, encouraging higher leverage and hence entrenching the very fragilities that necessitate them. These three challenges are examined in turn.

The effects of fiscal risk repricing and fiscal policy

Fiscal risk repricing occurs when investors assess that fiscal sustainability has worsened and require a higher risk premium to hold government debt. It matters in two distinct ways. First, when triggered by expansionary fiscal measures, it may weaken or even offset the intended demand-supporting effects of the stimulus. Second, repricing can also occur without any new fiscal measures, for example when markets react to a growth downgrade or a shift in global risk sentiment. In this case, it acts as a shock on its own.

The macroeconomic effects of risk repricing operate first through financial conditions. A change in fiscal risk typically raises government bond yields. Since sovereign yields are a benchmark for private sector funding costs, this tends to tighten borrowing conditions for households and firms and weigh on aggregate demand. Risk repricing could also trigger capital outflows and currency depreciation, as investors' confidence takes a hit. This can further tighten financial conditions, especially where foreign-currency liabilities or imported inputs are key. These effects can be amplified by NBFI channels: deleveraging, margin calls or liquidity strains can reinforce the initial rise in yields, causing a negative feedback loop.

A second channel operates through inflation expectations and exchange rate pass-through. As the fiscal outlook worsens, inflation expectations could also be disrupted. This may occur, for instance, if monetary policy is expected to remain looser to limit the fiscal impact of higher interest rates.27 The currency may also weaken, especially if a change in the perceptions of fiscal risk triggers capital outflows, thereby lifting imported inflation and reinforcing price pressures even as demand softens.28

The credibility of monetary policy is key to the strength of both channels. Credibility limits the extent to which fiscal stress translates into higher expected inflation, and by reducing the inflation risk compensation investors demand to hold longer-term assets, it also moderates the tightening of financial conditions. The response of fiscal policy to heightened fiscal risk can also shape the transmission. Consolidation measures that help restore market confidence can contain the rise in risk premia and the tightening of financial conditions, but they also weigh on demand and can reinforce disinflationary pressures.29

Measuring how changes in fiscal risk affect the economy is challenging. A wide range of factors influence sovereign yields, many of which also independently affect output and inflation. One approach to isolating the effects of risk repricing from other influences is to focus on episodes when sovereign yields rise while yields on high-grade corporate bonds of comparable maturity fall. This negative co-movement typically reflects investors reassessing fiscal risk rather than reacting to changes in inflation developments, monetary policy or other common influences.30

Evidence from this approach, using a broad panel of AEs and EMEs since 2010, confirms that, on average, fiscal risk repricing tightens financial conditions, weighs on output and affects inflation, although with considerable cross-country variation that makes estimates somewhat imprecise.31 Sovereign yields rise and currencies depreciate (Graph 9.A). Moreover, price pressures rise for about a year, as inflation expectations are revised up and currency depreciation lifts imported inflation. In the medium term, however, tighter financial conditions weigh on demand, leading to persistent disinflation and weakness in real activity (Graph 9.B). These effects tend to be more pronounced when the central bank responds passively – allowing the real policy rate to turn negative after the shock – compared with situations in which the central bank responds actively to inflation pressures (Graph 9.C). This suggests that accommodation does not necessarily shield the economy from the adverse consequences of fiscal risk repricing but could actually amplify them.

In addition to evidence from fiscal risk repricing, empirical studies that isolate the impact of specific fiscal policy changes confirm the relevance of offsetting channels and inflation pressures. For instance, fiscal multipliers tend to be smaller – and can even turn negative – when public debt levels are high.32 Moreover, fiscal expansions are found to be significantly more inflationary when public debt is allowed to rise without a clear expectation of future stabilisation.33

Exchange rate movements and shifts in inflation expectations are central to how fiscal policy raises inflation. In EMEs, fiscal expansions are estimated to produce larger exchange rate depreciations than in AEs, while also shifting the expected inflation distribution towards higher inflation outcomes. Unexpected increases in public debt also raise long-term inflation expectations, especially when debt is already high and dollarisation is significant. These effects, however, are much smaller under credible inflation targeting frameworks, underscoring the importance of institutional safeguards in anchoring inflation expectations.34 In AEs, the link between high public debt and inflation expectations is also evident: for instance, surveys across several countries show that informing households about high public debt raises their inflation expectations, with a considerably larger rise among those who have less confidence in the central bank's determination to fight inflation.35

Monetary policy transmission

Fiscal risk repricing could also be triggered by monetary policy changes. When the central bank hikes rates, higher interest payments on a large debt stock can worsen the fiscal outlook and prompt markets to reassess fiscal risk. Spreads and term premia may therefore widen, amplifying the tightening of financial conditions that normally arises through standard transmission channels, including bank lending and broader credit channels. This may, in turn, amplify the drag on economic activity. Additionally, the deterioration of fiscal positions may affect inflation expectations in a way that reduces the disinflationary impact of monetary policy.

Beyond fiscal risk repricing, a second channel – closely related but distinct – operates through valuation effects. All else being equal, a rate hike reduces bond prices, resulting in capital losses for investors and financial institutions holding public debt, even without any reassessment of fiscal risk. These losses erode risk-bearing capacity and tighten credit supply, thereby amplifying yield movements.36 Thus, the valuation channel strengthens the contractionary impulse to activity. But, unlike the repricing channel, it need not dampen the disinflationary effect of monetary policy: absent changes in fiscal risk, the larger drag on output could reinforce disinflation through the standard aggregate demand-Phillips curve mechanism.

Finally, a third channel works through interest income effects. Higher interest rates raise government interest payments, boosting income for private bondholders. If not offset by higher taxes or reduced transfers, this income transfer supports aggregate spending. Unlike the valuation channel, which reduces aggregate demand and reinforces disinflation, the interest income channel weakens both the output contraction and the disinflation from rate hikes, with larger debt stocks boosting these offsetting effects.37, 38

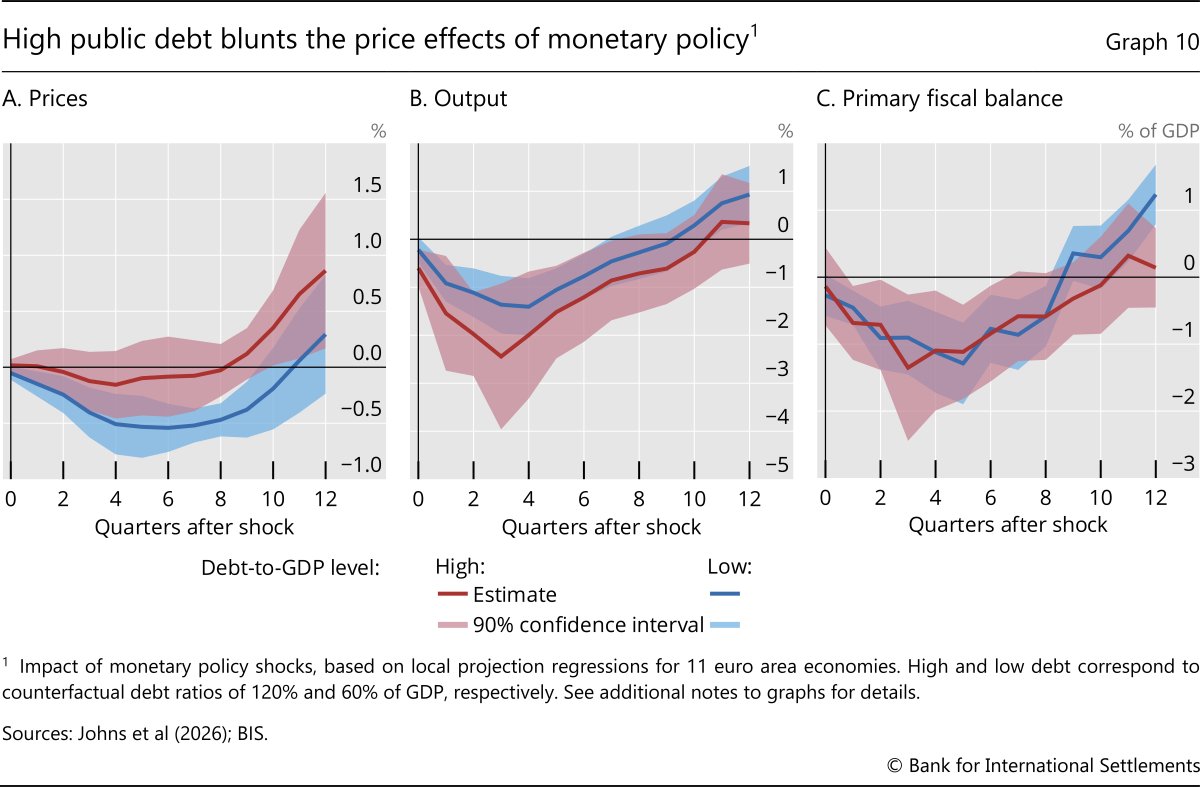

The limited available evidence suggests that higher debt does alter monetary policy transmission. In the United States, changes in interest rates have had a smaller impact on industrial production and unemployment when public debt levels were high, consistent with interest income effects weakening monetary transmission.39 In the euro area, the evidence points to higher debt levels having a different impact on output and inflation. Graph 10 illustrates this by comparing counterfactual responses at debt ratios of 120% and 60% of GDP while holding the maturity profile fixed at the same sample average. Countries with higher debt exhibit a weaker disinflationary response to monetary tightening (Graph 10.A) and a larger decline in output (Graph 10.B), although the output difference relative to those with low debt is not statistically significant.40 In both high and low debt countries, the primary fiscal balance tends to deteriorate following a rate hike (Graph 10.C), rather than adjust to absorb higher debt service costs, indicating that the interest income channel is operational.41 , 42

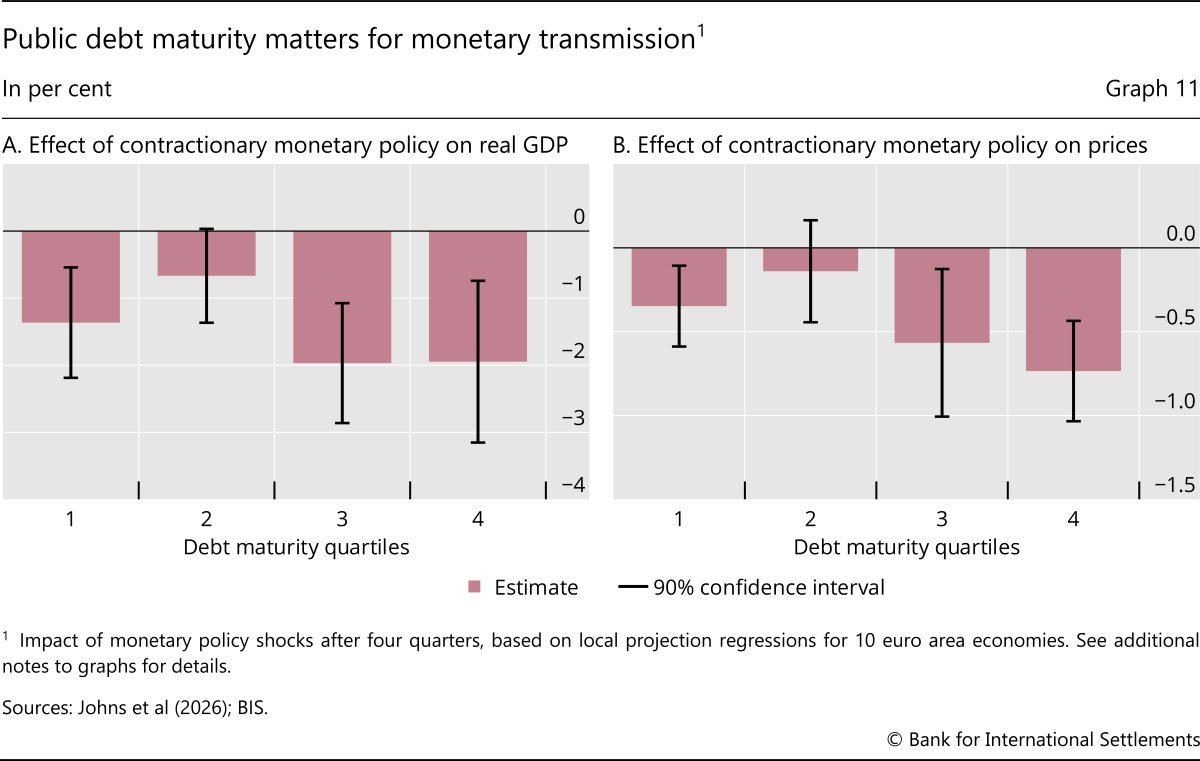

The maturity structure of public debt also matters. When maturities are long, the valuation channel is stronger: bond prices are more sensitive to yield changes, the income transfer to bondholders is deferred, and monetary policy is more powerful. As maturities shorten, more debt rolls over quickly at higher rates, strengthening the income channel and weakening the disinflationary impact of monetary tightening. At very short maturities, however, rollover risk could re-emerge as an amplifying force: frequent refinancing needs may leave governments more exposed to abrupt repricing of fiscal risk, which can feed back more quickly into higher sovereign borrowing costs and tighter financial conditions.

Evidence from euro area data is consistent with this non-linear pattern. Monetary policy tends to have its strongest effects in countries where debt maturities are long (Graph 11), in line with stronger valuation effects and a more delayed income transfer. In countries with medium maturities, policy transmission is relatively weaker, possibly because the income channel partly counteracts valuation effects. In countries with the shortest maturities, however, both the output contraction and disinflation intensify again, suggesting potentially greater sensitivity to refinancing pressures and fiscal risk repricing.43

These findings matter for the current environment, with public debt elevated and, in some economies, average maturities shorter than at their post-pandemic peaks. If debt continues to roll over at higher rates, the interest income effects could become more significant, potentially weakening the disinflationary impact of monetary policy. And if maturities shorten further, economies could also become more sensitive to fiscal risk repricing. Together, these developments would worsen the trade-off central banks face by making policy rate increases more consequential for fiscal positions while rendering their effects on output and inflation less predictable.

Addressing market dysfunction

Beyond complicating the transmission of fiscal and monetary policies, high public debt and the broader fiscal-financial stability nexus also heighten the risk of market dysfunction. Such episodes can threaten financial stability and further undermine monetary transmission, leaving central banks with little choice but to intervene. Asset purchase programmes and emergency lending operations are powerful backstops to restore market functioning and ease funding strains, whether the vulnerability crystallises in the banking or NBFI sector. In practice, however, NBFIs in many jurisdictions do not have access to lending operations. When NBFIs are at the centre of the dysfunction, central banks must therefore rely on asset purchases.

Although effective, central bank backstops give rise to several interrelated challenges.

First, providing backstops can challenge the calibration and implementation of the central bank's monetary policy stance. Backstops should only seek to restore temporary dysfunction, not provide longer-term stimulus. In practice however, drawing that distinction can be difficult. This can complicate the calibration of the monetary policy stance and challenge central bank communication, especially in a high-inflation environment. But even when market stress coincides with a downturn, using asset purchases for dual purposes – as many central banks did in March 2020 – carries its own danger. The imperative to bolster market confidence may crowd out concerns about overstimulating the economy, prompting purchases that prove too large and subsequently too slow to unwind once market functioning is restored.44

Second, the expectation of ex post central bank support can create ex ante moral hazard, leaving the system more vulnerable to future episodes of market dysfunction. If market participants come to view central bank backstops as likely, they may take on greater liquidity or duration risk, run with thinner buffers or rely more on short-term funding. The result is a more fragile market structure, prone to larger and more frequent episodes of dysfunction.

Third, large-scale interventions can also exacerbate underlying fiscal problems, raising the risk of more severe and more abrupt repricing of fiscal risk or loss of market confidence later on. By dampening the impact of fiscal developments on government bond yields beyond what fundamentals warrant, central bank backstops may weaken market discipline.45 Governments may then use the resulting fiscal space for further expansions, creating larger vulnerabilities in the future.

Finally, largescale balance sheet operations can also create risks for central bank independence. For example, large-scale purchases of government bonds could create perceptions that, beyond macro-financial conditions, monetary policy decisions may be influenced by central banks' sovereign debt exposures or that fiscal considerations are constraining the pursuit of price stability. Such perceptions could contribute to a de-anchoring of inflation expectations, especially in countries with a history of fiscal dominance. Large-scale purchases can also expose central banks to losses. While losses and negative equity do not directly affect the ability of central banks to operate effectively, large losses can draw heavy public criticism, as seen in several jurisdictions in recent years. Such criticism can undermine legitimacy and ultimately independence.

Confronting the emerging policy challenges

The challenges discussed above call for a multipronged policy response. What follows addresses each dimension in turn: monetary policy, fiscal policy, regulation and the design of central bank backstop facilities.

Monetary policy

Monetary policy will have to walk a fine line in the years ahead. With public debt at post-war peaks, high interest payments can weaken the impact of policy tightening on inflation (see the previous section), potentially requiring a stronger policy response. At the same time, sovereign debt markets have become more exposed to leveraged and liquidity-dependent intermediaries, potentially making risk premia, financial conditions and market functioning more sensitive to policy tightening. Policy calibration may therefore become more difficult: too little tightening could undermine inflation control, while too much could trigger larger than expected market reactions.

A gradual approach to interest rate hiking may therefore appear preferable under uncertainty, but excessive caution carries its own risks.46 If monetary policy is perceived as constrained by debt service costs or concerns about market stress, inflation expectations could become less firmly anchored. Financial conditions could also tighten regardless, through higher term premia and currency depreciation. As discussed in the previous section, these risks are more acute where monetary policy credibility is weak.

Central bank independence is therefore essential. It shields policymakers from political pressures tied to high public debt and helps anchor expectations when fiscal or financial risks intensify. However, even the strongest institutional arrangements cannot be fully credible without fiscal sustainability and a resilient financial system.47 Credibility ultimately hinges on measures (discussed below) that reduce the likelihood of the central bank being confronted with difficult trade-offs between price stability and financial stability.

Fiscal policy

Putting public finances on a credibly sustainable path is the most fundamental policy priority. This, in turn, requires restoring symmetry to fiscal policy. In many countries, policy has long been asymmetric over the business cycle, expanding aggressively in downturns but failing to consolidate sufficiently in expansions (Box A). Rebuilding buffers therefore means taking advantage of good times: unless market access is at risk, consolidation should proceed once the recovery in activity has firmed and financial conditions have normalised. To minimise growth costs, fiscal adjustment should also proceed gradually. But gradualism works best if it is anchored in credible mediumterm frameworks, well-specified and enforced fiscal rules and independent fiscal councils.48

The composition of consolidation matters as much as its pace. For instance, indiscriminate cuts to public investment can be self-defeating if they undermine potential growth and, in turn, fiscal sustainability. This risk is especially relevant for countries that face both high debt and anaemic growth. High debt could sap growth, while weak growth makes debt harder to reduce, creating a debt trap. Breaking this loop may require protecting or reallocating spending towards infrastructure, education and technological innovation. These areas can raise potential growth, expand the tax base and crowd in private capital. To maximise these gains, public investment should be accompanied by structural reforms that boost productivity more broadly and improve the efficiency with which capital is allocated and used (Chapter I).49

Regulation

The post-GFC reform agenda has delivered a markedly stronger financial system. Banks are now much better capitalised, they hold larger liquidity buffers, and macroprudential authorities have the mandate and tools to address several macroprudential risks. Regulatory reforms to ensure that NBFIs do not undermine financial stability have also been on the policy agenda for several years, but further reforms are needed.

A guiding principle for regulatory design should be to pursue "congruent regulation". This would imply regulatory frameworks that apply similar stringency to financial intermediaries posing similar risks to financial stability, regardless of their legal form or business model. While a useful guiding principle, designing congruent regulatory frameworks is challenging in practice. Gauging contributions to systemic risks is inherently difficult, the more so given the heterogeneity of NBFIs and their business models. That said, a range of activity and entitybased tools can be deployed to move towards congruent regulatory treatment. But implementation is further challenged by a fragmented institutional architecture that often assigns, even within a jurisdiction, the authority to design regulatory frameworks to multiple authorities in charge of different NBFI sectors. Greater cooperation at the national and international level would be important to overcome this gridlock.

In the context of the fiscal-financial stability nexus, regulatory measures that address systemic vulnerabilities in government bond markets are particularly important. Two frequently made proposals for regulatory measures merit further consideration.

One proposal is greater use of central clearing for cash and repo markets. This could enhance the resilience of government bond markets, although it is not a panacea.50 Central clearing can support intermediation activity by freeing up dealers' balance sheet capacity, given reduced counterparty risk and multilateral netting. Central clearing can also address the asymmetry observed in bilateral markets, where haircuts for the largest hedge funds tend to be smaller than those for other participants (see Graph 5.C). By encouraging all-to-all trading, the market may become less fragmented and more resilient. That said, mandatory central clearing brings its own financial stability risks. These include the increased systemic importance of central counterparties, which would be significant. Margins could also be substantial and they could even exacerbate the unwinding of leveraged trades.

Another proposal is to impose minimum haircuts to limit the build-up of leverage. Zero haircuts effectively allow some market participants, such as hedge funds, to operate with as much leverage as they wish. Some market participants argue that haircuts are set at the portfolio level rather than trade by trade. In practice, this is difficult to do effectively: dealers often lack a complete view of clients' aggregate exposures, and correlations within a portfolio can break down under market-wide shocks, leaving counterparties more exposed than anticipated.51 But minimum haircuts should be applied in a targeted manner. In many repo transactions, haircuts are designed to protect the collateral provider (ie the cash borrower) rather than the cash lender. A uniform minimum could therefore inadvertently favour one side of the trade, ie the cash or collateral lender.

In addition, prudent banking regulation and continued supervision remain critical to avoid the build-up of systemic risks from leveraged investors in government bond markets. As discussed in this chapter, banks, and in particular a small group of prime brokers, are key providers of funding to these NBFIs in repo and FX swap markets. It is therefore critical that these banks carefully manage their counterparty credit risk in relation to NBFIs and prevent them from taking on excessive leverage. This must be enforced by prudent supervision and the application of robust regulatory frameworks related to market and counterparty credit risk, as specified in Basel III and implemented in many jurisdictions.

The design of central bank backstop facilities

The key overarching consideration for the design of any central bank backstop facility is to satisfy the backstop principle. This principle stipulates that central banks play a role in preventing market dysfunction from harming the real economy. At the same time, these interventions and backstop facilities should not disrupt price discovery or risk management during normal times, ensuring markets remain self-reliant, reinforced through appropriate macro- and microprudential regulation and supervision.52

One key design feature to implement the backstop principle aligns with the Bagehot principle. For lending operations this stipulates providing liquidity during stress against good collateral at a penalty rate. However, this is challenging. Facilities must be unattractive in normal times but sufficiently appealing during stress to ensure take-up without stigma that could amplify liquidity hoarding. Committing to a pricing schedule ex ante and maintaining it ex post is difficult in rapidly evolving, uncertain conditions. Similarly, pricing asset purchases for market functioning along the lines of the Bagehot principle is very complex, as in principle the central bank should purchase an asset at a penalty rate but still at a price that improves the market dysfunction. This requires distinguishing between price movements driven by fundamentals and those caused by market dysfunction. This is particularly challenging during stress, as dysfunction often stems from news about fundamentals, such as fiscal shocks.

Other design features can also help. One is to design interventions to be temporary and targeted to mitigate long-term side effects. The Bank of England's response to the LDI crisis in 2022 offers a blueprint: narrow, time-limited operations with explicit eligibility, clear triggers and a well-communicated exit. Another feature is to announce open-ended purchases rather than specific targets. This helps to address risks that purchases prove too large and too slow to reverse ex post. The design can also include an option to partly reverse initial purchases once market functioning is restored. Finally, communication has a role to play in anchoring expectations and preserving credibility.

Given NBFIs' central role in the fiscal-financial stability nexus, developing tools and expanding counterparty access to lending to NBFIs may be useful but involves trade-offs. Expanding counterparty access would allow central banks to address dysfunction through lending rather than asset purchases. Depending on the source of the dysfunction, lending operations may be preferrable to asset purchases since they are more targeted and do not remove all risks from NBFIs' balance sheets. Since they have a predefined maturity, lending operations do not permanently increase the central bank balance sheets or the liquidity provision to the system either. However, expanding access introduces operational and counterparty risks for the central bank and may heighten the potential for moral hazard and systemwide externalities. To manage these risks, expanding counterparty access to NBFIs requires them to be adequately regulated and at a minimum supervised.

Conclusion

Historically high public debt and structural shifts in financial markets are creating a more demanding environment for central banks. These shifts have narrowed the arm's length separation between monetary, fiscal and financial stability policies. When fiscal positions appear unsustainable, markets may demand higher compensation for holding government debt, financial conditions can tighten and pressures may build for monetary accommodation or central bank intervention. When financial fragility is pervasive, it can amplify shocks to sovereign yields, compress fiscal space and constrain monetary policy. These risks are not hypothetical: tensions between policies have already surfaced in some economies, and recent market disruptions have exposed vulnerabilities that could resurface.

The goal should be to preserve or restore an environment in which each policy can deliver on its mandate without being unduly constrained by the others. By delivering on their mandates, policies reinforce each other. Disciplined fiscal policy underpins monetary credibility and financial stability. Robust regulation strengthens market resilience, preserves fiscal space and reduces the need for frequent central bank interventions. Credible monetary policy anchors inflation expectations and helps contain sovereign and exchange rate risk premia, thus strengthening both fiscal sustainability and financial stability.

Policymakers should not wait for vulnerabilities and the emerging challenges to worsen. Acting early to strengthen fiscal frameworks, financial resilience and monetary credibility would preserve room for manoeuvre across policy domains. Delay would instead make adjustment more costly and increase the likelihood that future shocks force difficult choices between price stability, financial stability and fiscal sustainability.

Endnotes

1 See Hernández de Cos (2025) for a discussion of long-term debt projections.

2 Contingent liabilities are not always fully reflected in fiscal accounts or analyses of debt sustainability. Hence, they are often referred to as "hidden debt". See Reinhart (2015). When they are revealed, they can trigger a sharp repricing of fiscal risk or even a crisis.

3 The main fiscal cost of financial crises – measured by the increase in public debt in the years following a financial crisis – is often indirect, due to the loss of output and fiscal revenue as well as discretionary fiscal measures. The direct costs, such as bailouts, are smaller on average and tend to be recouped partly or entirely several years after the crisis. See eg Amaglobeli et al (2017) and Borio et al (2020).

4 Even against the backdrop of a secular downward trend in interest rates, the very low interest rates observed post-GFC appear to be an anomaly. Historical research using century-long data by Rogoff et al (2024) shows that while there have been several prolonged periods of exceptionally low real interest rates, these episodes have invariably come to an end, suggesting the potential for some upward reversion.

5 According to International Monetary Fund projections, interest payments will account for more than half of the rise in nominal debt in AEs and EMEs during 2025–30, excluding stock-flow adjustments (IMF (2026)).

6 The negative interest rate-growth differential partly reflects financial repression, which was particularly pronounced in EMEs, as well as the high inflation of the 1970s, prior to the liberalisation of financial markets (Mauro and Zhou (2021)). When this differential is negative for structural rather than these more transient reasons, debt ratios can be stabilised even without primary surpluses, lowering the perceived cost of fiscal expansion. An implication, which gained wide policy traction post-GFC, is that governments – especially those borrowing in their own currency – have more fiscal room than traditionally assumed, and that the welfare costs associated with higher public debt, such as the crowding out of private investment, are modest (Blanchard (2019)).

7 For instance, Auclert et al (2025) estimate that US public debt could rise to about 250% of GDP. Importantly, stabilising debt at such high levels would require an implausibly large permanent fiscal adjustment of at least 10% of GDP.

8 See Goodhart and Pradhan (2020).

9 See eg Rogoff (2020, 2021).

10 Reinhart et al (2003) show that "safe" debt-level thresholds vary widely across countries depending on the depth of their financial markets in addition to their history of inflation and default.

11 See eg Arellano and Ramanarayanan (2012) who document that, in EMEs, as sovereign spreads rise, debt maturity shortens and short-term spreads widen by more than long-term ones, a pattern consistent with rollover vulnerability.

12 Mauro and Zhou (2021), drawing on a data set of 55 countries over up to 200 years, find that the interest rate-growth (r-g) differential has essentially no predictive power for government defaults. Furthermore, this differential is not independent of debt levels. Countries with higher initial debt ratios tend to experience shorter negative r-g episodes and a more right-skewed distribution of outcomes, implying that tail risk of a reversal is greatest precisely when debt is already elevated (Lian et al (2020)). In past episodes, large negative r-g differentials have also sometimes reflected high inflation and financial repression, further weakening the predictive power of this metric.

13 See IMF (2025).

14 While the amount of government bond exposures of pensions funds and the insurance sector increased in recent years, their shares relative to total portfolios of the respective sectors have tended to decline (see eg Ding et al (2026) for pension funds and Aquilina, Garavito et al (2025) for the life insurance sector).

15 See Sushko and Todorov (2025).

16 See Hermes et al (2025).

17 See Schrimpf et al (2020) and Ghio et al (2023).

18 See eg Acharya et al (2024) and Borio et al (2023) for a recent review.

19 These results are from Avdjiev et al (2026). See also Aquilina, Cornelli and Tarashev (2025) for related analysis.

20 See Pinter et al (2024).

21 See FSB (2022) and Hernández de Cos (2025).

22 See Du et al (2025).

23 See CGFS (2020).

24 See Carstens and Shin (2019).

25 For an account of the forces that have led to the current situation, see BIS (2023).

26 Beyond these acute episodes, persistently high public debt has also weighed on trend growth in several economies, mainly by pushing up higher risk premia, requiring more distortionary taxation and lowering investment (see eg BIS (2013); Cecchetti et al (2011); Fatás et al (2019)).

27 See eg Kase et al (2026) and Schmidt (2025).

28 When fiscal sustainability is in question, the standard relationship between policy and the exchange rate can reverse: a monetary tightening or a fiscal shock that would normally appreciate the currency can instead depreciate it, as sovereign risk premia dominate the conventional interest rate channel. See eg Alberola et al (2021).

29 See Hernández de Cos and Moral-Benito (2013).

30 See Gómez-Cram et al (2024) for the economic intuition. Gorea et al (2026) perform a high-frequency identification by isolating episodes in which sovereign yield increases coincide with drops in the yields of ultra-safe corporate bonds.

31 Limited data availability for corporate and government bond yields in EMEs contributes to imprecise local projection estimates in Graph 9. Results are similar, and precision improves, when estimated using a more limited sample of mainly AEs. See Gorea et al (2026) for details.

32 See eg Ilzetzki et al (2013) and Nickel and Tudyka (2014).

33 See eg Banerjee et al (2022); Bianchi et al (2023); and Smets and Wouters (2024).

34 See Banerjee et al (2023) for the effects on inflation through the exchange rate and Brandão-Marques et al (2024) for the impact of debt surprises.

35 See Grigoli and Sandri (2024).

36 Leveraged intermediation by NBFIs can also make monetary transmission state-dependent. When leverage is high, the pass-through of policy shocks is amplified (Banerjee et al (2025, 2026)).

37 This channel is mostly relevant for domestic bondholders. Its strength diminishes with the share of debt held by foreign investors.

38 For theoretical exposition of the valuation and income effect channels, and how they differ from the standard intertemporal substitution channel, see Caramp and Silva (2023) and Caramp and Feilich (2024). These debt-related channels depend not only on the expected path of short-term real interest rates but also on the stock and maturity of public debt.

39 See Caramp and Feilich (2024). The authors do not report results for inflation.

40 In Graph 10.A, differences between impulse response functions for prices are statistically significant at all horizons, whereas in Graph 10.B, the differences for output are statistically significant only at very short horizons.

41 For evidence on the fiscal backing of monetary policy, see also Smets and Wouters (2024) for the United States and Afonso et al (2023) and Kloosterman et al (2024) for the euro area.

42 Evidence from the locational BIS international banking statistics shows key interactions, namely that fiscal tightening amplifies the impact of monetary tightening (Pradhan et al (2024)).

43 The results shown in Graphs 11.A and 11.B remain robust when the maturity structure is approximated using four bins rather than the weighted average maturity. Each bin represents the volume of debt, as a share of GDP, corresponding to a specific residual maturity. This approach highlights that both the overall level of debt and its maturity composition play a role in the transmission mechanism (Johns et al (2026)). The results are also robust to using total debt rather than market-held debt.

44 See eg Chavaz and Smets (2025) and English and Sack (2024).

45 See eg Wolswijk (2026) and Broeders et al (2023).

46 See Brainard (1967) on why the optimal response to uncertainty about the policy multiplier is an attenuated one. See also Goodfriend (1991) on interest rate smoothing as a strategy to minimise adverse financial market reactions. See Söderström (2002) on why a more aggressive response is needed in response to uncertainty about inflation persistence.

47 See eg Bianchi and Melosi (2022). Drazen and Masson (1994) distinguish between the credibility of policymakers and that of policies.

48 See eg Balasundharam et al (2023).

49 See eg Draghi (2024). Public support for general purpose innovation is key to boosting private innovation (Gazzani et al (2025)). See also Carstens (2025) and Fornaro and Wolf (2025).

50 Mandatory central clearing has already been decided in some jurisdictions, such as in the United States. See eg FSB (2025).

51 Moreover, when repos that are part of a broader portfolio are stripped out, haircuts remain very low (Hermes et al (2025)).

52 See Markets Committee (2022).

Additional notes to graphs

Graph 1: The sample covers 27 AEs and 24 EMEs, subject to data availability. For government debt, general (if not available, central) government debt at nominal (if not available, market) value.

Graph 3.A: Data are monthly and include 10-year local-currency government bond yields, where available. More historical data are based on a mix of instruments. The sample covers 25 AEs and 18 EMEs, subject to data availability.

Graph 3.B: Interest rates are estimated as the ratio of annual government interest payments to the stock of government gross debt. Growth is annual growth in nominal GDP. The sample covers 26 AEs and 18 EMEs, subject to data availability.

Graph 3.C: Sovereign defaults are based on Asonuma and Trebesch (2016), Beers et al (2025) and Reinhart and Rogoff (2009). Non-default stress events are included from 1994 onwards due to data availability. Such events are identified based on government bond spreads relative to US Treasuries or German Bunds (for European countries), using a threshold for the level of spreads of above 10 percentage points and a threshold for the quarterly change in spreads above the 98th percentile. The sample covers 20 AEs and 16 EMEs, subject to data availability.

Graph 4.A: Aggregate debt divided by the aggregate GDP of 24 AEs.

Graph 4.B: Data are based on responses to US Securities and Exchange Commission Form PF.

Graph 4.C: The observation for 2025 covers data until August 2025.

Graph 5.A: Data are based on responses to US Securities and Exchange Commission Form PF.

Graphs 5.B and 5.C: Transactions with investment funds as cash borrowers, with specific collateral, no net exposure and bilateral segment only. See Hermes et al (2025) for further details.

Graph 6.A: Banks' (other depository corporations') claims on central, state and local government by residence, as a percentage of banks' (deposit takers') Tier 1 capital. AEs = AT, AU, BE, CZ, FI, FR, GR, IL, IT, LU, NL, PT and US; EMEs = AE, BR, CL, CO, HU, MX, MY, PH, PL, TH, TR and ZA.

Graphs 6.B and 6.C: Estimates are obtained from a daily banklevel panel regression of bank CDS spreads on sovereign CDS spreads interacted with banks' exposure shares. The specification includes bankquarter fixed effects. Exposure measures are scaled by each bank's total exposures (to all borrowers). Sovereign CDS spreads are demeaned by counterparty country. Counterparty countries: BG, BR, CL, CY, EE, ES, GR, HR, HU, IE, IN, IT, KR, LT, LV, MT, MX, PE, PL, PT, RO, RS, RU, SI, SK and TR. Countries of lending banks: AT, BE, DE, DK, ES, FI, FR, GB, GR, IE, IT, NL, NO, PT and SE.

Graphs 7.A and 7.B: The sample covers DE, ES, FR, GB, IT, JP and US, using daily data from May 2011 to November 2025. Fiscal risk shocks are from Gorea et al (2026).

Graph 7.A: Daily market liquidity states are determined based on Bloomberg's yieldcurve "noise" proxy, where liquidity is deemed to be high (low) when the proxy is below (above) the country-specific median.

Graph 7.B: The average daily change in the noise measure is 0.001 basis points, so a one-unit shock (equivalent to a one standard deviation increase in the fiscal risk shock, which raises 10-year government yields by approximately 30 basis points (see Graph 9.A)) increases the noise measure by around 20 times its mean, or 0.02 basis points.

Graph 7.C: Probabilities are estimated following Aldasoro et al (2025). The sample period is from July 2011 to January 2024.

Graphs 8.A and 8.B: The BIS OTC derivatives statistics comprise data reported every six months by dealers in 12 jurisdictions (AU, CA, CH, DE, ES, FR, GB, IT, JP, NL, SE and US) plus data reported every three years by dealers in more than 30 additional jurisdictions. For periods between Triennial Surveys, the outstanding positions of dealers in these additional jurisdictions are estimated by the BIS.

Graph 8.B: The share maturing within one year is calculated as a percentage of the data for which maturities are reported.

Graph 9: Estimated using a monthly sample from 2010 to 2025. The sample covers 25 AEs and 15 EMEs, subject to data availability.

Graph 9.A: Cumulative six-month impact of a 1 percentage point increase in five-year government bond yields due to a fiscal risk shock, as estimated using a panel local projection model.

Graph 9.C: Cumulative two-year impact of a 1 percentage point increase in five-year government bond yields due to a fiscal risk shock, conditional on the monetary policy response. Passive monetary policy episodes are defined by negative real policy rates for six out of eight months after a positive fiscal risk shock.

Graph 10: The sample covers AT, BE, DE, ES, FI, FR, GR, IE, IT, NL and PT from 2001 to 2020. Public debt is divided into four buckets, reflecting ultra short debt, short debt, medium maturity debt and long debt. Monetary policy shocks are from Jarociński and Karadi (2020) and interacted with the public debt buckets. For estimations with high and low debt, the maturity profile is held fixed at the sample average of each maturity bucket. The size of the monetary policy shock is one standard deviation.

Graph 11: The sample covers AT, BE, DE, ES, FI, FR, IE, IT, NL and PT from 2001 to 2020. Monetary policy shocks are from Jarociński and Karadi (2020) and are interacted with the weighted average maturity of privately held public debt. Maturities are divided into four quartiles based on the distributions of the average maturity (in years): first quartile = 5.9; second quartile = 6.5; third quartile = 7.2, fourth quartile = 13.7. The size of the monetary policy shock is one standard deviation.

References

Acharya, V, N Cetorelli and B Tuckman (2024): "Where do banks end and NBFIs begin?", NBER Working Papers, no 32316.

Afonso, A, J Alves and S Ionta (2023): "The effects of monetary policy surprises and fiscal sustainability regimes in the euro area", ISEG – Lisbon School of Economics and Management, Working Papers REM, no 281.

Aguiar, M, M Amador, E Farhi and G Gopinath (2015): "Coordination and crisis in monetary unions", Quarterly Journal of Economics, vol 130, no 4.

Alberola, E, C Cantú, P Cavallino and N Mirkov (2021): "Fiscal regimes and the exchange rate", BIS Working Papers, no 950.

Aldama, P and J Creel (2022): "Real-time fiscal policy responses in the OECD from 1997 to 2018: procyclical but sustainable?", European Journal of Political Economy, vol 73(C), 102135.

Aldasoro, I, P Hördahl, A Schrimpf and S Zhu (2025): "Predicting financial market stress with machine learning", BIS Working Papers, no 1250.

Amaglobeli, D, N End, M Jarmuzek and G Palomba (2017): "The fiscal costs of systemic banking crises", International Finance, vol 20, no 1.

Aquilina, M, G Cornelli and N Tarashev (2025): "Commonality under pressure: banks and funds", BIS Quarterly Review, March.

Aquilina, M, F Garavito, G Gelos, U Lewrick, F Packer, G Pinter, V Sushko and K Todorov (2025): "The transformation of the life insurance industry: systemic risks and policy challenges", BIS Papers, no 161.

Araujo, D, B Cohen and K Tracol (2024): "The prime broker–hedge fund nexus: recent evolution and implications for bank risks", BIS Quarterly Review, Box C, March.

Arellano, C (2008): "Default risk and income fluctuations in emerging economies", American Economic Review, vol 98, no 3.

Arellano, C and A Ramanarayanan (2012): "Default and the maturity structure in sovereign bonds", Journal of Political Economy, vol 120, no 2.

Arslanalp, S and T Tsuda (2014): "Tracking global demand for advanced economy sovereign debt", IMF Economic Review, vol 62, no 3.

Asonuma, T and C Trebesch (2016): "Sovereign debt restructurings: preemptive or post-default", Journal of the European Economic Association, vol 14, no 1.

Auclert, A, H Malmberg, M Rognlie and L Straub (2025): "The race between asset supply and asset demand", NBER Working Papers, no 34470.

Avdjiev, S, B Hardy and M Jager (2026): "The evolving nexus: sovereigns, banks and NBFIs", BIS Working Papers, forthcoming.

Balasundharam, V, O Basdevant, D Benicio, A Ceber, Y Kim, L Mazzone, H Selim and Y Yang (2023): "Fiscal consolidation: taking stock of success factors, impact, and design", IMF Working Papers, no 63.

Banerjee, R, V Boctor, A Mehrotra and F Zampolli (2022): "Fiscal deficits and inflation risks: the role of fiscal and monetary policy regimes", BIS Working Papers, no 1028.

-----(2023): "Fiscal sources of inflation risk in EMDEs: the role of the external channel", BIS Working Papers, no 1110.

Banerjee, R, L Boneva, G Pintor and V Sushko (2026): "Monetary policy transmission to exchange rates: the role of currency carry trades", BIS Bulletin, no 124.

Banerjee, R, B Hofmann, D X Ng and G Pinter (2025): "The rise of non-bank financial institutions: implications for monetary policy", BIS Bulletin, no 116.

Bank for International Settlements (BIS) (2013): Annual Economic Report 2013, Chapter IV.

----- (2023): Annual Economic Report 2023, Chapter II.

Beers, D, O Ndukwe and J Berry (2025): "BoC–BoE sovereign default database: what's new in 2025?", Bank of Canada Staff Analytical Notes, no 2025-24, October.

Bi, H (2012): "Sovereign default risk premia, fiscal limits, and fiscal policy", European Economic Review, vol 56, no 3.

Bianchi, F, R Faccini and L Melosi (2023): "A fiscal theory of persistent inflation", Quarterly Journal of Economics, vol 138, no 4.

Bianchi, F and L Melosi (2022): "Inflation as a fiscal limit", in Reassessing constraints on the economy and policy, proceedings of the Federal Reserve Bank of Kansas City Jackson Hole Symposium.

Blanchard, O (2019): "Public debt and low interest rates", American Economic Review, vol 109, no 4.

Borio, C, J Contreras and F Zampolli (2020): "Assessing the fiscal implications of banking crises", BIS Working Papers, no 893.

Borio, C, M Farag and F Zampolli (2023): "Tackling the fiscal policy-financial stability nexus", BIS Working Papers, no 1090.

Bouabdallah, O, C Checherita-Westphal, T Warmedinger, R De Stefani, F Drudi, R Setzer and A Westphal (2017): "Debt sustainability analysis for euro area sovereigns: a methodological framework", ECB Occasional Papers, no 185.

Brainard, W (1967): "Uncertainty and the effectiveness of policy", American Economic Review, vol 57, no 2.

Brandão-Marques, L, M Casiraghi, G Gelos, O Harrison and G Kamber (2024): "Is high debt constraining monetary policy? Evidence from inflation expectations", Journal of International Money and Finance, vol 149, 103206.

Broeders, D, L de Haan and J W van den End (2023): "How quantitative easing changes the nature of sovereign risk", Journal of International Money and Finance, vol 137, 102881.

Calvo, G (1988): "Servicing the public debt: the role of expectations", American Economic Review, vol 78.

Caramp, N and E Feilich (2024): "Monetary policy and government debt", Journal of Money, Credit and Banking, vol 58, no 2.

Caramp, N and D Silva (2023): "Fiscal policy and the monetary transmission mechanism", Review of Economic Dynamics, vol 51.

Carstens, A (2025): "Sustaining trust and stability", speech at the BIS Annual General Meeting, Basel, 29 June.

Carstens, A and H S Shin (2019): "Emerging markets aren't out of the woods yet", Foreign Affairs, 15 March.

Caselli, F, H Davoodi, C Goncalves, G H Hong, A Lagerborg, P Medas, A Nguyen and J Yoo (2022): "The return to fiscal rules", IMF Staff Discussion Notes, no 2.

Cecchetti, S, M Mohanty and F Zampolli (2011): "The real effects of debt", in Achieving maximum long-run growth, proceedings of the Federal Reserve Bank of Kansas City Jackson Hole Symposium.

Chavaz, M and F Smets (2025): "Quantitative easing at 25: time for a makeover?", in D Aikman and R Barwell (eds), The UK monetary policy roundtable, National Institute for Economic and Social Research.

Checherita-Westphal, C and J Semeano (2020): "Interest rate-growth differentials on government debt: an empirical investigation for the euro area", ECB Working Paper, no 2486.

Checherita-Westphal, C and V Žďárek (2017): "Fiscal reaction function and fiscal fatigue: evidence for the euro area", ECB Working Paper, no 2036.

Cheng, G, A Cornevin and B Hofmann (2026): "Other days, other ways? Fiscal and monetary policy reaction functions over the past seven decades", BIS, mimeo.

Cole, H and T Kehoe (2000): "Self-fulfilling debt crises", Review of Economic Studies, vol 67, no 1.

Committee on the Global Financial System (CGFS) (2020): "US dollar funding: an international perspective", CGFS Papers, no 65.

Corsetti, G and L Dedola (2016): "The mystery of the printing press: monetary policy and self-fulfilling debt crises", Journal of the European Economic Association, vol 14, no 6.

Ding, D, X Fang, B Hardy and K Lewis (2026): "Global pension asset allocations and debt markets", BIS Papers, no 172.

Draghi, M (2024): The future of European competitiveness, report to the European Commission, September.

Drazen, A and P Masson (1994): "Credibility of policies versus credibility of policymakers", Quarterly Journal of Economics, vol 109, no 3.

Drehmann, M and S Zhu (2026): "NBFIs, high public debt and the risk of market dysfunction", BIS Bulletin, forthcoming.