BIS global liquidity indicators at end-June 2023

Key takeaways

- The BIS global liquidity indicators (GLIs) in Q2 2023 show a contraction in both dollar and euro credit to non-banks in EMDEs compared with a year earlier.

Global liquidity indicators at end-June 2023

The BIS global liquidity indicators (GLIs) track total credit to non-bank borrowers, covering both loans extended by banks and funding from global bond markets through the net issuance (gross issuance less redemptions) of international debt securities (IDS). The main focus is on foreign currency credit denominated in the three major reserve currencies (US dollars, euros and Japanese yen) to non-residents, ie borrowers outside the respective currency areas.2

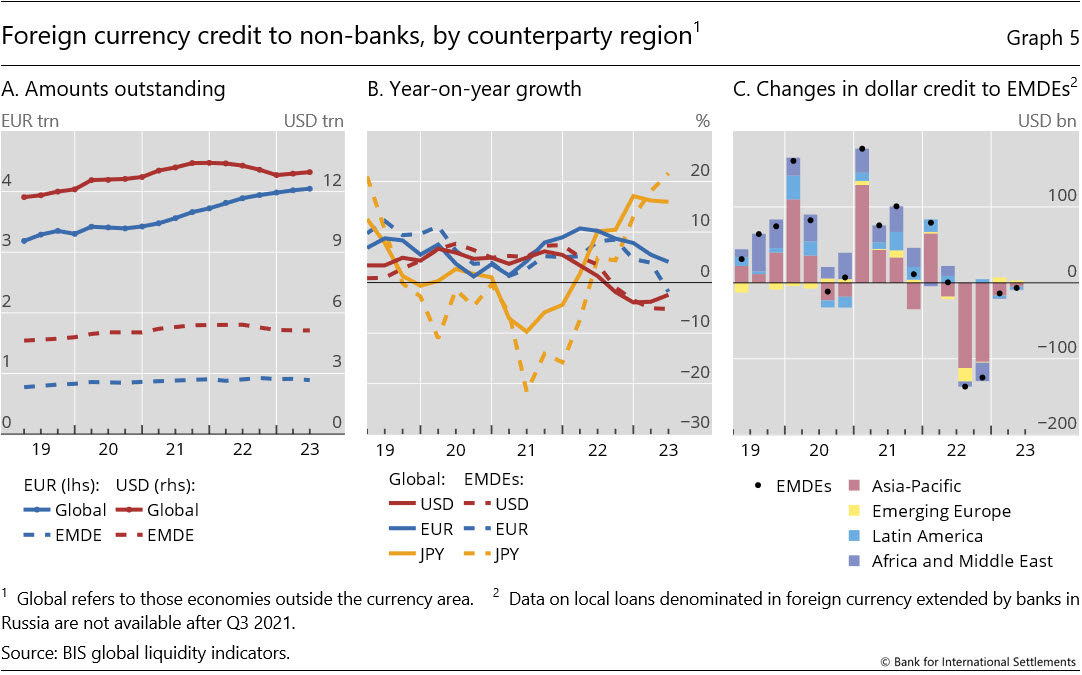

Foreign currency credit in the three major currencies rose slightly in Q2 2023. The quarterly increase of $77 billion in US dollar credit to non-banks outside the United States left the outstanding stock at $13 trillion (Graph 5.A, solid red line). Even so, the yoy growth rate remained negative at –2% (Graph 5.B, solid red line). Euro-denominated credit to non-banks outside the euro area stabilised at €4 trillion (Graph 5.A, solid blue line), up 4% from a year earlier. Yen credit outside Japan continued to expand rapidly, driven by bank loans. The outstanding stock reached ¥58 trillion ($400 billion), up 16% from a year earlier (Graph 5.B, solid yellow line).

For non-banks in EMDEs, growth in credit denominated in dollars, euro and yen diverged. After three consecutive quarterly contractions, dollar credit to EMDEs remained weak in Q2 2023, leaving the stock near $5.1 trillion (Graphs 5.A and Graph 5.C). Greater net issuance of IDS and an increase in cross-border loans to non-banks during Q2 partly offset the sizeable drop in dollar-denominated local bank loans.3

In contrast to dollar credit, the growth in yen credit to non-banks in EMDEs continued to accelerate, exceeding 20% yoy (Graph 5.B, dashed yellow line). This pushed the outstanding stock to ¥16 trillion ($116 billion). The rapid growth in yen credit reflected mainly increased bank lending, which grew by 30% yoy. Since mid-2022, yen credit to non-bank borrowers in Asia-Pacific has expanded the most (¥1.9 trillion), followed by credit to those in Latin America (¥710 billion) and Africa and the Middle East (¥255 billion). Despite these developments, foreign currency credit in yen remains considerably smaller than the corresponding stocks of dollar and euro credit.

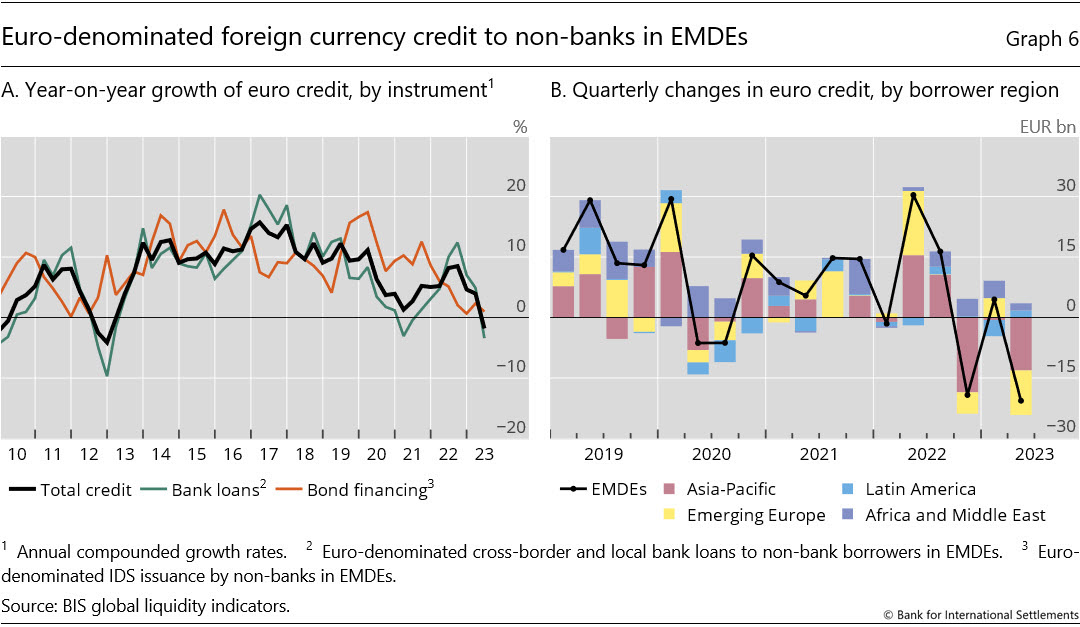

For its part, euro credit to non-banks in EMDEs fell by €21 billion in Q2 2023, leaving the outstanding stock at €890 billion. This contributed to a yoy contraction of 2%, the weakest rate of growth since end-2012 (Graph 6.A, black line). The decline reflected mainly a drop in bank loans, which shrank at a rate of 3% yoy (green line). The contraction in euro credit vis-à-vis non-bank borrowers in Asia-Pacific (– €13 billion) and emerging Europe (–€11 billion) accounted for the decline in the latest quarter (Graph 6.B).

2 For more details, see the GLI methodology.

3 As discussed in the previous section, cross-border bank credit in dollars to EMDEs (all sectors) declined in Q2 2023; this was due to reduced lending via banks' related offices located in EMDEs. The GLI figures analysed here capture only dollar credit to non-banks in EMDEs; it includes loans to non-banks (cross-border and local) and debt securities issued by non-banks.