What constitutes an international debt security in BIS statistics?

The BIS has published international debt securities (IDS) statistics since the 1980s, with coverage stretching back to the 1960s. They report outstanding amounts as well as both gross and net debt issuance, with the latter equal to the former minus repayments. These statistics include aggregates that can be grouped, for instance, by the country or sector of the immediate issuer's residence, the country or sector of the ultimate parent, or the currency of denomination. The definition of IDS has evolved over time to reflect changes in financial markets and to keep the statistics relevant for financial stability analysis. The BIS currently treats a security as an IDS if its issuance targets a market outside the country of the immediate issuer's residence.

The BIS currently treats a security as an IDS if its issuance targets a market outside the country of the immediate issuer's residence.

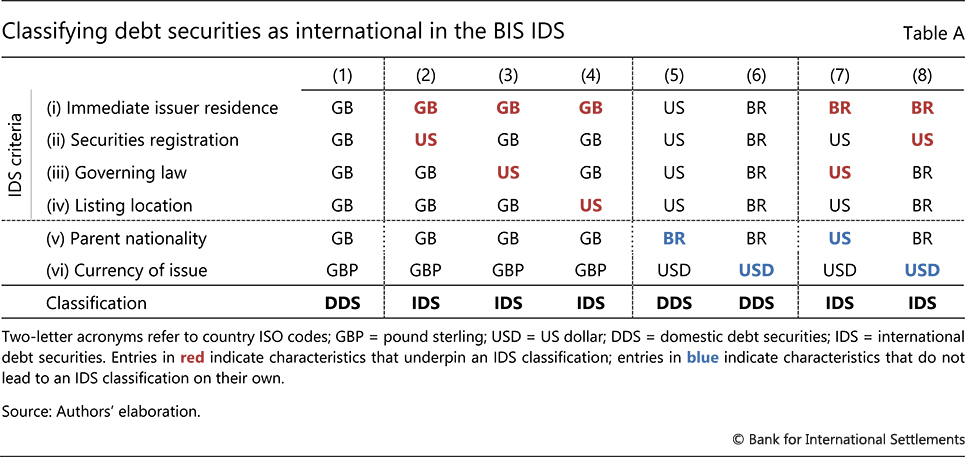

Concretely, to include an issue in the IDS statistics, the BIS assesses (i) the residence of the immediate issuer; (ii) the location of the issue's registration; (iii) the governing law; and (iv) the listing location (Table A). When all four characteristics refer to the same country, the issue is classified as a domestic debt security (DDS, column 1). When at least one points to a different country, the security is classified as international.

(iii) the governing law; and (iv) the listing location (Table A). When all four characteristics refer to the same country, the issue is classified as a domestic debt security (DDS, column 1). When at least one points to a different country, the security is classified as international. For example, if a resident of the United Kingdom issues a security governed by English law and listed on the London Stock Exchange but registered in the United States, then this is an IDS (column 2). The security would also be considered international if, say, the UK resident issued it under New York law or listed it on the New York Stock Exchange (columns 3 and 4).

For example, if a resident of the United Kingdom issues a security governed by English law and listed on the London Stock Exchange but registered in the United States, then this is an IDS (column 2). The security would also be considered international if, say, the UK resident issued it under New York law or listed it on the New York Stock Exchange (columns 3 and 4).

The IDS classification does not refer to the issuer's nationality or the currency of the issue's denomination. Thus, an issue through an "offshore" affiliate – ie an office located outside the parent's country of nationality – might not be classified as IDS. For instance, this would happen if a Brazilian firm issues through its affiliate in the United States, provided that characteristics (ii)–(iv) all point to the United States (column 5). Likewise, if all-Brazilian debt is issued in US dollars, it would be a DDS (column 6). That said, such scenarios are rare: ie they account for 7.4% and 0.3%, respectively, of the raw data on gross issuance in Q1 2021. In the vast majority of cases, issuances through offshore affiliates or in foreign currencies satisfy the IDS selection criteria in scenarios such as those in columns 7 and 8.

For a comprehensive overview of the statistics see B Gruić and P Wooldridge, "Enhancements to the BIS debt securities statistics", BIS Quarterly Review, December 2012, pp 63–76. The IDS statistics approach euro area countries individually, ie if a company in France lists a bond issue in Frankfurt or on a euro area-wide exchange, then this issue would be an IDS. This is the location of the authorities with administrative responsibilities for the issue and often of the relevant repository. The country of registration is indicated by the first two digits of the issue's ISIN number. In practice, there are instances where no information on the location of listing, registration and governing law is available. In such cases, information on where the issue is sold is used. If the issue is classified as foreign on this basis, it is part of the IDS. Foreign issues are defined by a non-resident issuing in the local market of a given country in domestic currency, and are identified by market participants with specific names (ie "Yankee bonds" for USD or "Samurai bonds" for JPY). Column (7), where residence and nationality differ, is an example of "offshore" IDS issuance. Column (8), where residence and nationality coincide, is in turn an example of "onshore" IDS issuance.