Uncovering FX settlement risk: new measures from the 2025 BIS Triennial Survey

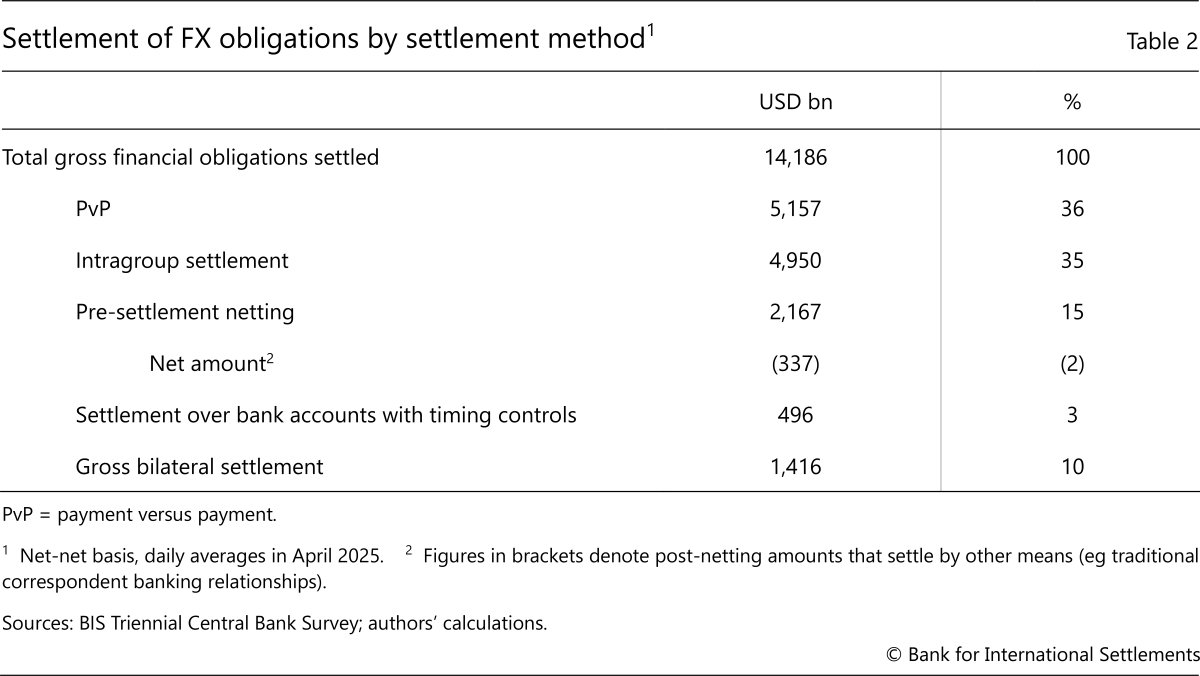

Foreign exchange settlement risk is the risk that one party to a currency trade fails to deliver the currency owed. It can result in significant losses and undermine financial stability. To shed light on the scale of trades most at risk, the April 2025 Triennial Survey categorised settlement amounts by settlement method. Just over $5 trillion, or 36% of the average daily settlement during the month, settled via payment versus payment (PvP), which eliminates FX settlement risk. A further $7.6 trillion (54%) involved settlement methods such as pre-settlement netting that mitigate but do not eliminate settlement risk. More than $1.4 trillion (10%) were settled on a gross bilateral basis, which is fully exposed to settlement risk.1

JEL classification: E42, F31, G15

On the afternoon of 26 June 1974, the German authorities ordered Bankhaus Herstatt into liquidation. The bank was closed at 3.30 pm Frankfurt time, after which its New York correspondent bank suspended all outgoing US dollar payments from Herstatt's account. This action left Herstatt's counterparties exposed for the full value of the Deutsche marks they had already paid in Frankfurt earlier in the day to settle US dollar-Deutsche mark foreign exchange (FX) trades. The collapse of Herstatt was a watershed moment in the history of financial markets, exposing the systemic risk associated with FX settlement. This type of risk, also referred to as "Herstatt risk", occurs when one party to an FX trade fulfils its obligation to deliver currency but does not receive the corresponding currency in return.

The failure triggered a loss of trust in financial markets. Market participants began to delay payments until they had received confirmation of their counterparties' payments. This brought cross-border payments and, with them, FX trades to a halt, threatening a spiral into a global financial crisis (see Schenk (2014); Norman (2015)). The turmoil subsided only after major central banks signalled their readiness to provide sufficient liquidity. In its aftermath, what is now the Basel Committee on Banking Supervision (BCBS) was established at the end of 1974. This was followed by the creation in 1990 of the Committee on Payment and Settlement Systems (CPSS), the precursor to the BIS Committee on Payments and Market Infrastructures (CPMI), to address policy issues related to payment systems used for the settlement of domestic and cross-border transactions.

Key takeaways

- The BIS 2025 Triennial Survey of FX markets classifies the use of FX settlement methods to help assess FX settlement risk, ie the risk that one party to a currency trade fails to deliver the currency owed.

- In April 2025, 90% of the average daily settlement was via methods which eliminate or minimise FX settlement risk. But 10%, or $1.4 trillion, remained exposed to these risks.

- Public and private sector stakeholders should continue their efforts to reduce FX settlement risk for a broader range of currencies and market participants.

The CPSS's first task resulted in the G10 Central Bank Governors' strategy to reduce FX settlement risk (CPSS (1996)). The strategy consisted of three elements: (i) action by individual banks to control their FX settlement exposures; (ii) action by industry groups to provide risk-reducing multicurrency services for settling FX trades; and (iii) action by central banks to induce private sector progress. A key milestone of this process was the launch of CLS Bank (CLS) in 2002. CLS provides a payment-versus-payment (PvP) service called CLSSettlement that eliminates FX settlement risk.

Half a century after the Herstatt failure, the 2025 BIS Triennial Survey of FX markets provides a fresh stocktake on FX settlement risk. The 2025 survey is based on a methodology that was jointly developed on behalf of the Markets Committee by the Global Foreign Exchange Committee (GFXC),2 in cooperation with experts from the CPMI, central banks, local FX committees and the BIS. The methodology also underpins the GFXC semiannual FX settlement survey.

The new survey methodology classifies FX settlement according to the method used. Just over one third of the average daily settlement volume in April 2025, or $5.2 trillion, was settled via PvP, which eliminates settlement risk. Three other methods – intragroup settlement, pre-settlement netting, which reduces gross payment amounts to a smaller net payment, and settlement over bank accounts with settlement timing controls – all mitigate but do not eliminate FX settlement risk. Roughly $7.6 trillion, or 54% of the total, was settled via these methods. Finally, gross bilateral settlement, which exposes the counterparties to FX settlement risk to the full trade value, made up the remaining $1.4 trillion, or 10% of total settlement, in April. The more granular survey data reveal that the main reasons for relying on this settlement method were that the counterparty did not have PvP access or that the currency pairs or trade type were not eligible for PvP settlement.

The 2025 survey results, compared with those from a similar survey in 2006, show that efforts by the private and public sectors to reduce FX settlement risks have borne fruit.3 The overall share of settlement on a gross bilateral basis has decreased substantially. But the survey also underscores the need for further collaboration to address potential vulnerabilities.

The remainder of the article is structured as follows. The next two sections detail the new survey methodology and the key insights from the 2025 survey on FX settlement risk. The final section concludes with an overview of the ongoing public and private sector efforts to further reduce FX settlement risk. A statistical annex provides the full breakdown of the surveyed data.

The 2025 methodology for assessing FX settlement risk

The Herstatt episode exemplified the nature of FX settlement risk and its implications for financial stability. This risk materialises when one party to an FX transaction has delivered the required currency with finality while the other counterparty fails to deliver the corresponding currency, for instance because that counterparty is in default. A failure constitutes an extreme event, but the potential exposures can be very large given the sizeable trades in FX markets and the fact that the full value of a trade is subject to loss (principal risk). Moreover, a single payment failure can erode market confidence, giving rise to a payment gridlock and severe market disruptions, as witnessed in the aftermath of the Herstatt failure.

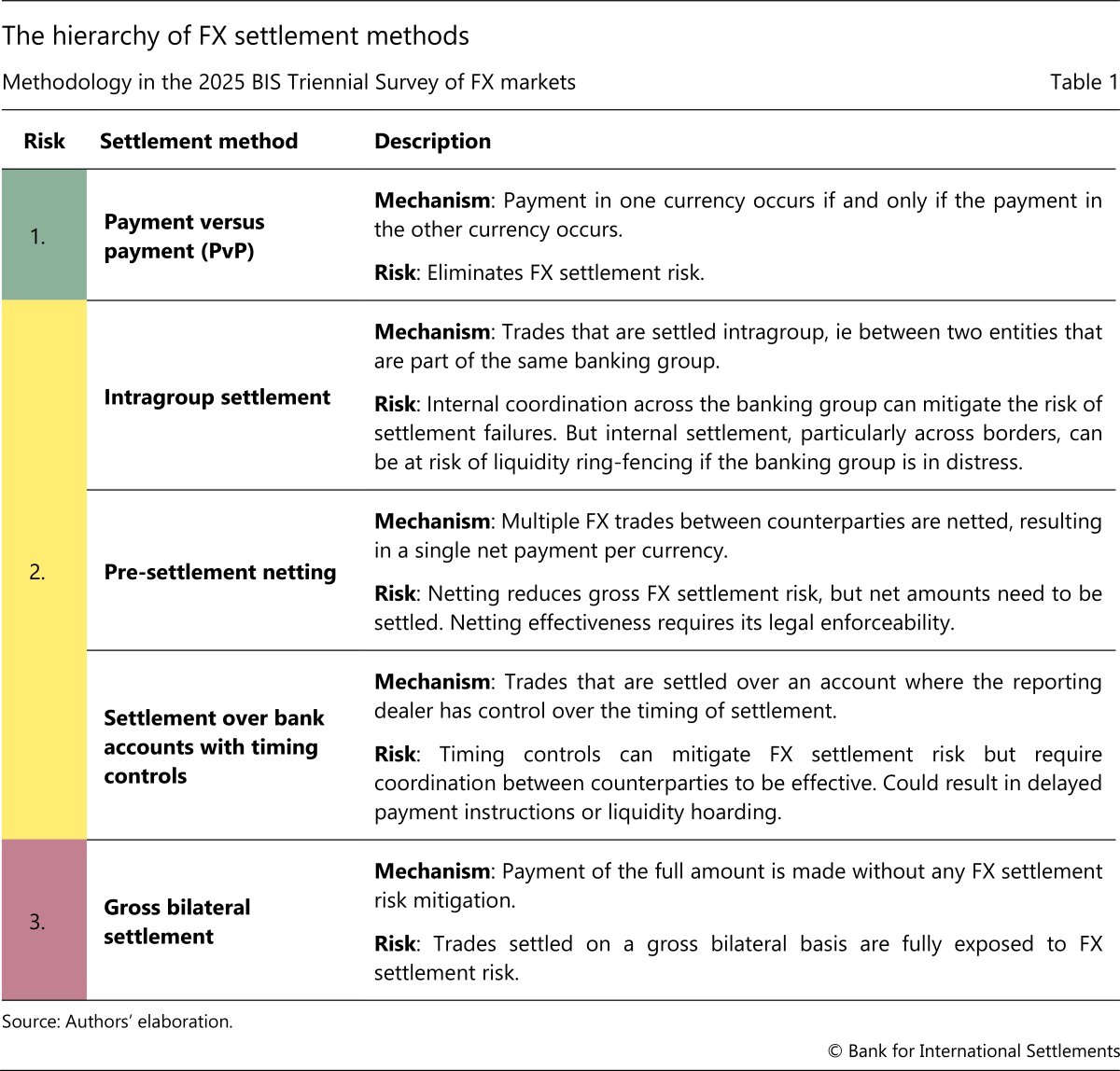

To manage this risk, a variety of settlement methods have been developed, which are surveyed in the April 2025 Triennial Survey. The survey classifies settlement based on a hierarchy of five settlement methods (Table 1): (i) PvP systems; (ii) pre-settlement netting; (iii) intragroup settlement; (iv) settlement over bank accounts with settlement timing controls; and (v) gross bilateral settlement. This methodology is aligned with the approach for managing FX settlement risk in the GFXC's revised January 2025 FX Global Code, in particular the revised Principle 35, which recommends FX market participants consider the hierarchy to reduce FX settlement risk (GFXC (2025)).

Trades settled via a PvP system are not subject to FX settlement risk. A PvP system ensures that the final payment of one currency occurs if and only if the final payment of the other currency occurs. The PvP function is distinct from the function of a central counterparty (CCP), which interposes itself as a counterparty to all its participants and assumes their obligations.4 Hence, the PvP function alone does not eliminate replacement cost risk (ie the risk of incurring extra costs when replacing the original transaction at current market prices) or the liquidity risks of not receiving a currency when expected.

Beyond eliminating FX settlement risk, PvP systems generate other benefits. For one, a PvP mechanism can function as a coordinating and stabilising device in decentralised FX markets during times of market stress. Since obligors know for sure that their payments will never be processed unless the same is true for incoming payments, a PvP mechanism can help to prevent a payment gridlock.5 An additional benefit is that PvP systems can often enable netting of payments, offering advantages for liquidity management.

The largest and best known PvP system is CLSSettlement, which settles payments involving 18 major currencies.6 Given its systemic importance, CLS is subject to stringent risk management requirements and cross-border cooperative oversight by the Federal Reserve Bank of New York and other central banks that issue CLS-eligible currencies. The 2025 survey asked reporting dealers to separately report settlement volumes for CLS-eligible and CLS-ineligible currency pairs.

Several other PvP systems have emerged, some of which settle currency pairs that are not CLS-eligible (CPMI (2023)). These include: B3 Foreign Exchange Clearinghouse (B3) in Brazil since 2002 (settling in the Brazilian real and US dollar); CCIL in India since 2015 (settling in the Indian rupee and US dollar); CHATS in Hong Kong SAR since 2000 (settling in the Hong Kong dollar, offshore renminbi (CNH), euro, Indonesian rupiah, Malaysian ringgit, Thai baht and US dollar); and Buna in the United Arab Emirates since 2023 (settling in the UAE dirham, euro, Egyptian pound, Jordanian dinar, Saudi riyal and US dollar).

Beyond PvP, other settlement methods can reduce but not eliminate FX settlement risk.

First, dealer banks may settle their internal transactions (ie transactions between two entities that are part of the same banking group) on an intragroup basis. This could include settlement of transactions between desks and branches within the same legal entity, between the headquarters and its subsidiaries, and between two subsidiaries or affiliated entities within the banking group. The probability of FX settlement risk materialising from intragroup trades is relatively low as there are strong incentives at the group level to coordinate trades and ensure timely settlement. However, intragroup settlement is not risk-free: in severe stress scenarios, liquidity can get trapped in a particular entity, for example if a national authority imposes ring-fencing measures or payment moratoriums. Trapped liquidity can disrupt the sequence of internal payments in the entire group, in turn crystallising liquidity or credit risk that spills over to the rest of the group or even outside it.

Second, pre-settlement netting of outstanding trades can reduce FX settlement risk. It nets out multiple trades between two parties that have matching characteristics (eg currency, value date) to reduce gross settlement amounts into a single, smaller net amount to be settled for each currency. This reduces settlement risk to the extent that the final net amounts to be settled are smaller than the original gross settlement amounts. However, pre-settlement netting's effectiveness at mitigating risk requires the legal enforceability of netting agreements in the event of a default, which may not be fully ensured for all counterparties, currencies or jurisdictions. Moreover, the net amounts still need to be settled by another method such as traditional correspondent banking relationships and are subject to counterparty credit risk. In the survey, the netted transactions were not distributed to other buckets of settlement methods to avoid double-counting, and therefore their method of settlement is not known.

Third, reporting dealers may also settle across bank accounts with settlement timing controls. Such trades are typically with other (non-reporting) financial institutions or with non-financial customers that have an account with the reporting dealer. To manage settlement risk in this case, the reporting dealer in effect settles its obligation only when the other party has paid with finality or has posted sufficient collateral.7 This approach, however, may create asymmetries, as client counterparties may lack equivalent controls. In addition, timing controls could result in or amplify delayed settlements, liquidity hoarding and reduced FX trading activity in times of stress.

Trades that do not settle via one of the methods above must settle on a gross bilateral basis through traditional correspondent banking relationships, exposing the counterparties to FX settlement risk for the full amount. To understand why some trades settle without any risk mitigation, the 2025 Triennial Survey asked reporting dealers to classify trades settled on a gross bilateral basis by whether the transactions were eligible for applicable PvP systems and, if not, whether this was because: (i) the counterparty is not a direct or indirect member of the applicable PvP system; (ii) the currency pair is ineligible; or (iii) the trade type is ineligible. This information gives policymakers more information about how to target market participants' efforts to further mitigate FX settlement risk.

For the April 2025 survey, reporting dealers in 49 jurisdictions provided data on the use of different settlement methods during the month. The survey covers settlement of all FX trades that involve two-way payments.8 Volumes are based on actual settlement during the month of April rather than settlement volumes derived from turnover figures for that month.9 To align the survey with how FX settlement risk is managed in practice, the reporting basis is the global banking group determined by the location of the corporate headquarters rather than the sales desk, which is the basis in the turnover part of the Triennial Survey.

FX settlement risk in April 2025

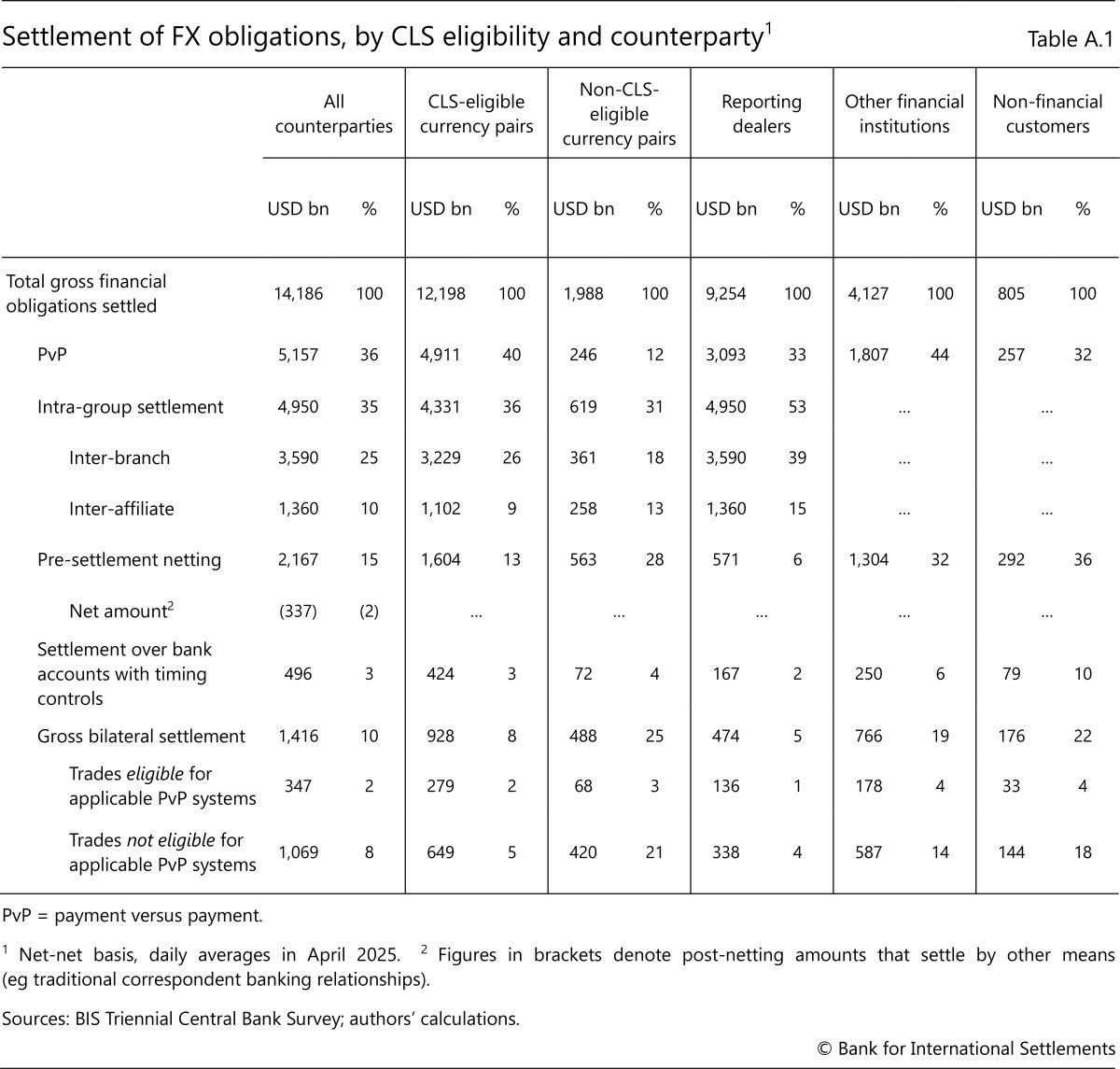

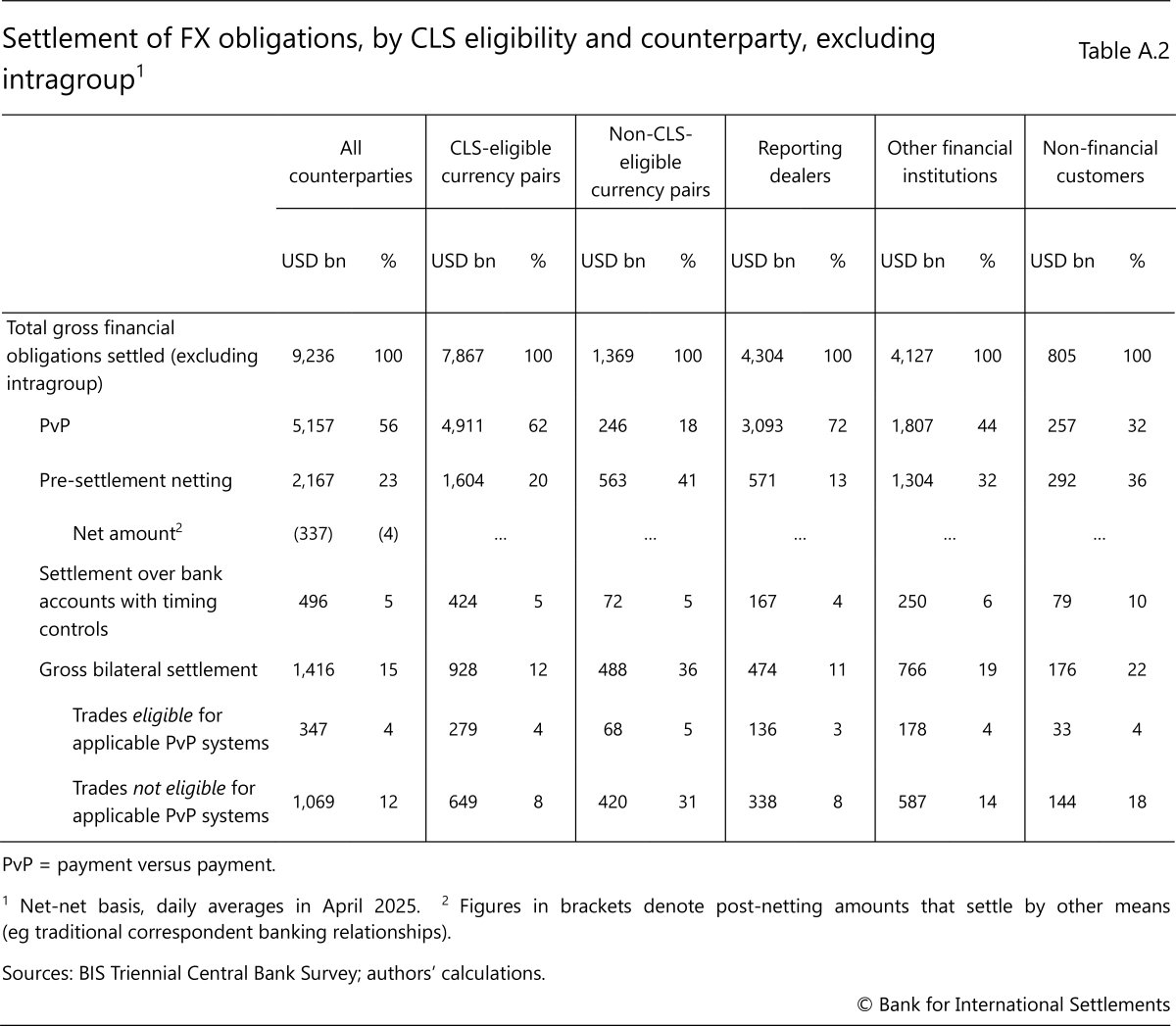

More than $14 trillion worth of gross financial obligations were settled on an average day in April 2025 (Table 2). Just over one third (36%) of these were settled via PvP systems, eliminating FX settlement risk. More than $2 trillion (15%) were subject to pre-settlement netting, leaving a post-netting amount of $337 billion. This amount needed to be settled by other means (eg traditional correspondent banking relationships), and thus was subject to some counterparty credit risk. More than one third of the average daily amount (35%) settled intragroup, highlighting the size and complexity of reporting dealers' internal funding structures and operations. By contrast, only a small fraction (3%) settled over bank accounts where reporting dealers have control over the timing of settlement. Finally, 10% were settled on a gross bilateral basis. These transactions settle without any mitigation method for FX settlement risk and hence are the most concerning from a systemic risk perspective.

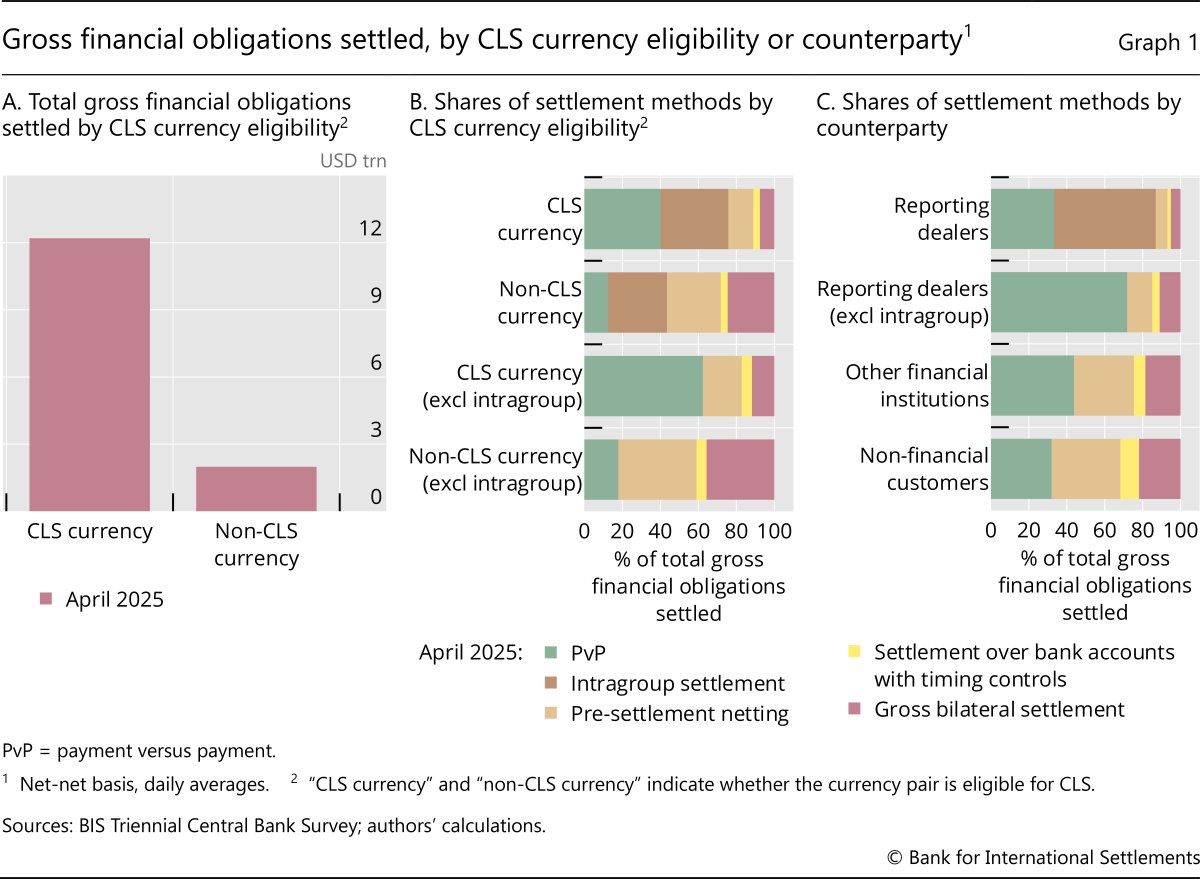

Settlement via PvP systems was especially prevalent for trades in CLS-eligible currencies. More than four fifths of the average daily settlement – or $12.2 trillion – involved CLS-eligible currency pairs (Graph 1.A), reflecting the importance of these major currencies in global FX markets (see Huang et al (2025) Of these, 40% were settled via PvP systems. By contrast, only 12% of trades that involved non-CLS-eligible currency pairs settled via (non-CLS) PvP systems (Graph 1.B).

The use of PvP systems to mitigate risk is most common for transactions between reporting dealers (Graph 1.C). This is not surprising given that many dealer banks are CLS members. PvP settlement was used to settle $3.1 trillion of inter-dealer trades per day, or 33% of the average of inter-dealer trades settled ($9.3 trillion). At the same time, more than $4.9 trillion (or more than 53%) of all inter-dealer trades settled intragroup. Excluding these intragroup settlements leaves $4.3 trillion of inter-dealer trades with external counterparties that settled via other methods, of which a full 72% were settled via PvP systems – much more than the PvP share of trades with other (non-reporting) financial institutions (44%) or with non-financial counterparties (32%) (Table A.2 in the statistical annex).

There was also significant use of pre-settlement netting to manage FX settlement risk. Only 2% of all settled inter-dealer trades were settled over bank accounts with timing controls, rising to 10% of settled trades with non-financial customers. Pre-settlement netting was more important: 15% of total settlement and a third of the settlement of trades with other financial institutions and with non-financial customers were subject to netting (Table A.1). In volume terms, pre-settlement netting reduced around $2.2 trillion on average per day to $337 billion to be settled by other means. The survey did not collect data regarding how this net amount was distributed across counterparty types. Anecdotally, however, compression from netting tends to be higher for inter-dealer obligations than for those with customers, since customers tend to have directional FX positions.

The remaining obligations of more than $1.4 trillion on average per day were settled on a gross bilateral basis, exposing the counterparties to FX settlement risk for the full amount. External inter-dealer transactions that settled this way amounted to $474 billion, or 11% of all external inter-dealer settlement (5% of total inter-dealer settlement, if intragroup settlement is included). This share of risky external inter-dealer obligations is roughly half of those observed for obligations with other financial institutions (19%) and with non-financial customers (22%) (Graph 1.C). The next section explores why risk mitigation techniques were not applied in these transactions.

Reasons for gross bilateral settlement

While only 10% of the average daily FX settlement in April 2025 settled on a gross bilateral basis, the average absolute amount was still large, surpassing $1.4 trillion per day. The 2025 survey methodology introduced questions that help to understand why risk mitigation techniques were not applied to these FX obligations. This information can help policymakers target efforts that incentivise further risk mitigation.

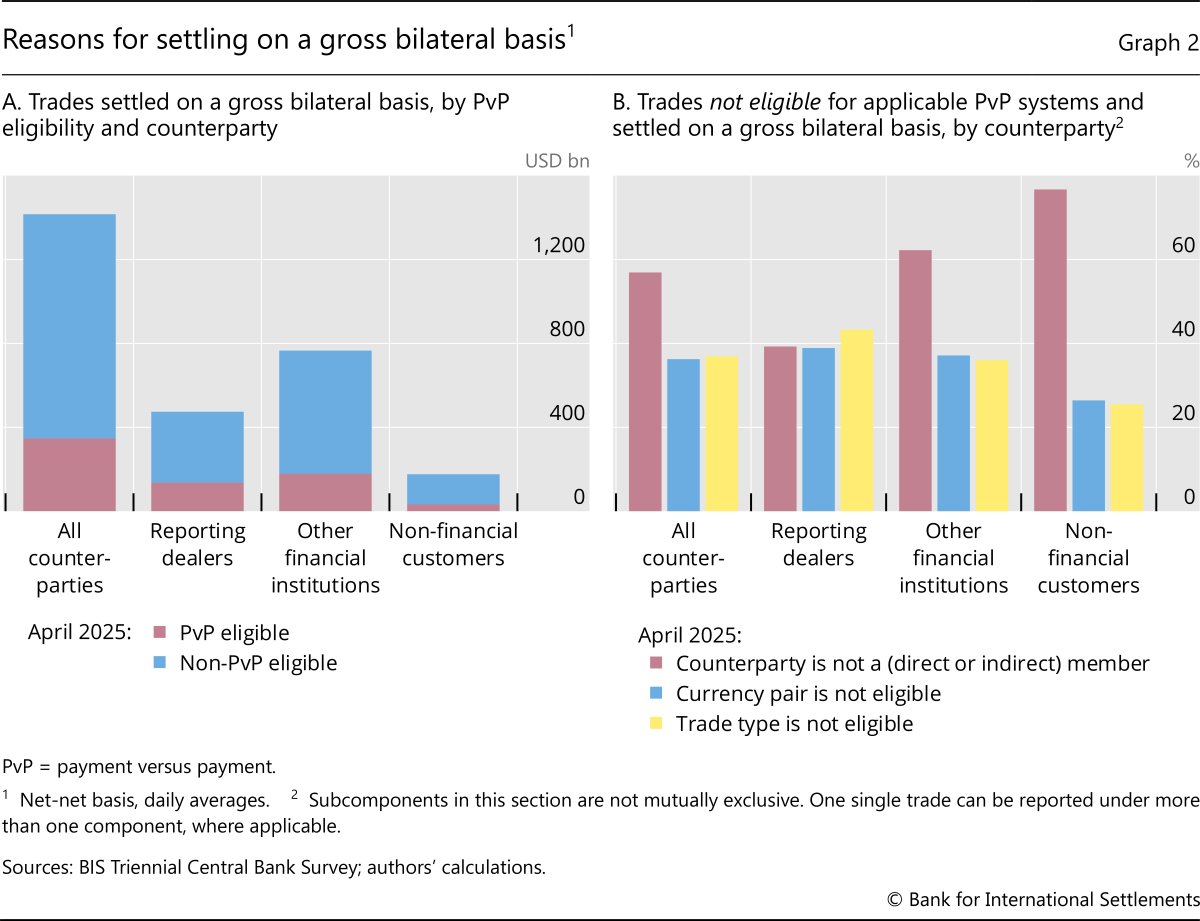

Of the total amount settled on a gross bilateral basis per day, 25% or $347 billion was eligible for settlement in a PvP system (Graph 2.A). More than half of this amount involved transactions with other financial institutions ($178 billion), with trades between reporting dealers making up much of the remainder ($136 billion). These trades involved PvP-eligible currency pairs and products, and were with counterparties that were direct or indirect members of an applicable PvP system. As such, it should have been possible to eliminate settlement risk in these transactions.

There are several anecdotal reasons why trades settled on a gross bilateral basis even though they were eligible for PvP settlement. For one, operational issues might result in trades missing the cutoff times for PvP settlement. Other reasons include challenges in managing credit risk exposures to correspondent banks that some banks use for payments to or from a PvP system, or meeting tight payment schedules of a PvP system.10 Continued industry-wide efforts to foster clear understanding of FX settlement risk and further implementation of relevant supervisory and industry guidance can help to onboard these types of trades, notably the supervisory guidance developed by the BCBS (2013) and the GFXC Global FX Code.

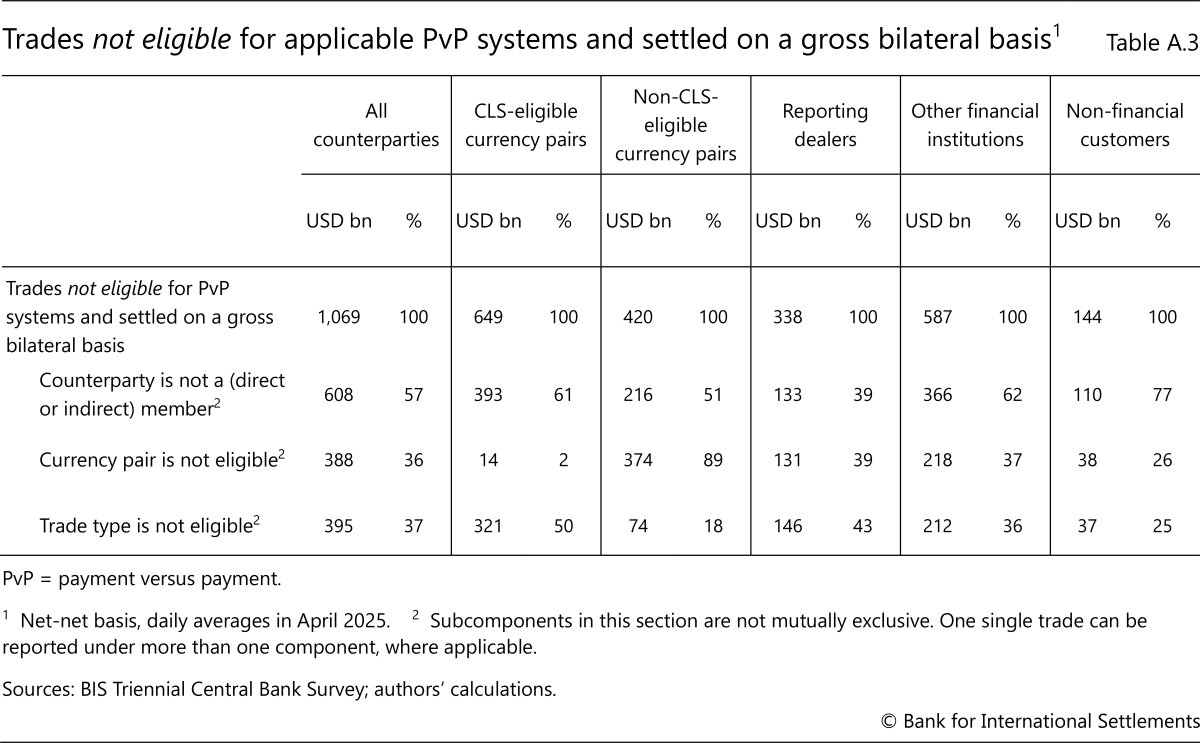

Three quarters of the trades that settled on a gross bilateral basis were not eligible for PvP systems. Three (sometimes overlapping) reasons help to explain this (Graph 2.B, Table A.3, Statistical Annex).

The most common reason was that the counterparty did not have direct or indirect access to PvP systems (57%). This issue is more acute in settlement of transactions with other (non-reporting) financial institutions and with non-financial customers than in inter-dealer transactions, where both sides to the trade tend to have direct PvP access. Continuing efforts to broaden direct and indirect access to more market participants therefore remains important, in particular as the role of non-bank financial institutions (NBFIs) in FX intermediation continues to expand.

Further reading

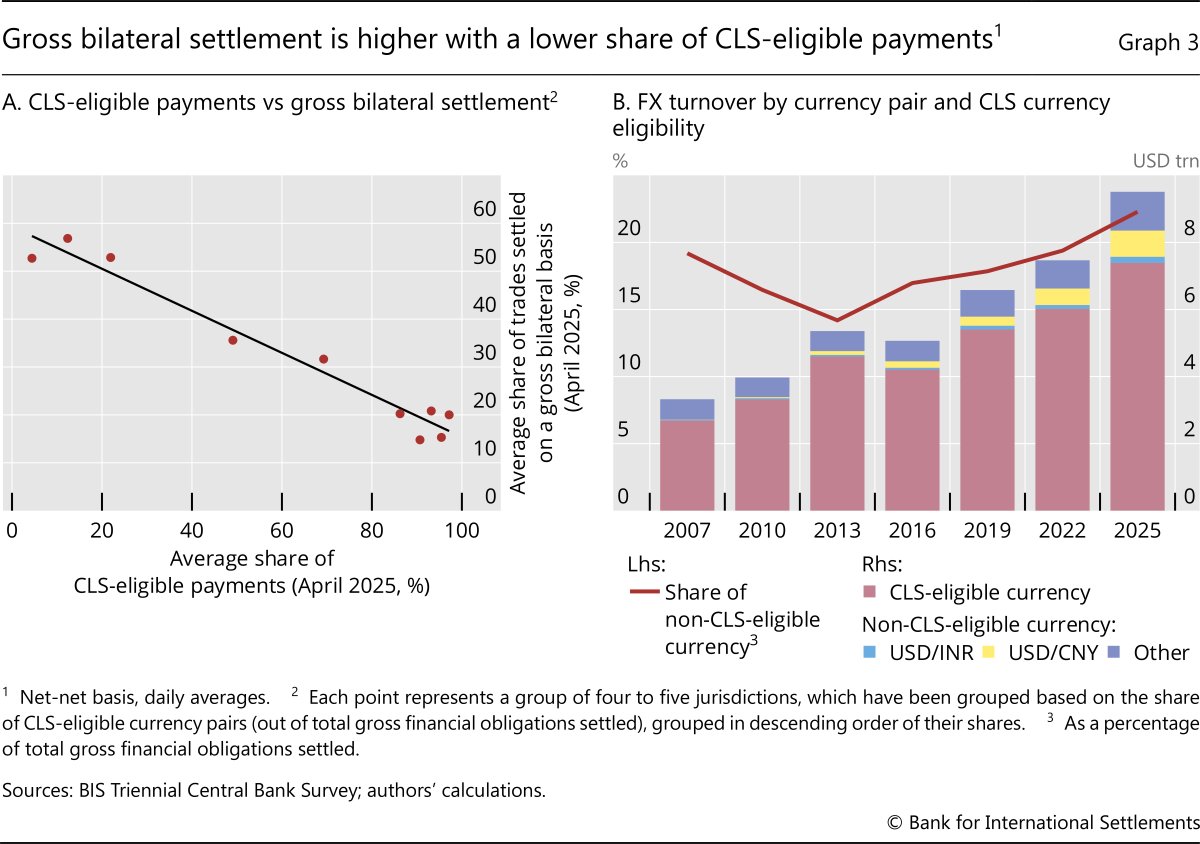

The second reason for gross bilateral settlement was that currency pairs were not eligible for PvP settlement. This was the case for 36% of the trades that settled on a gross bilateral basis because of any of the three ineligibility issues. It is therefore not surprising that reporting dealers that transacted more in CLS-eligible currencies reported a lower share of overall transactions settled on a gross bilateral basis (Graph 3.A).

Enlarging the set of eligible currencies for PvP systems will probably become more important as the role of non-eligible currencies increases in global financial markets. However, this often comes with several structural challenges. These include establishing robust legal frameworks (eg to ensure settlement finality), improving FX convertibility by removing or loosening capital or FX controls, increasing operational reliability of wholesale payment systems and internal systems of participating banks, and securing liquidity providers in local currencies. Thus, increasing PvP adoption in this way may be pursued as part of broader efforts to modernise a nation's payment ecosystem and capital market. Where PvP settlement is not practical or too costly, pre-settlement netting solutions with robust legal and operational arrangements could be explored as a shorter-term solution.

The third reason trades were settled on a gross bilateral basis was that the trade type was ineligible for PvP settlement (37%). PvP systems are generally designed for T+1 or T+2 settlement and they operate on specific cutoff times for settlement instruction submission (eg 12 am CET for next-day settlement). With such cutoff times, same-day (T+0) trades currently cannot be settled via PvP. As more jurisdictions move to T+1 for securities settlement cycles, market participants' needs for same-day FX swaps may increase to fund cross-border securities transactions, which may, in turn, lead to an increase in trades settled on a gross bilateral basis.

The evolution of FX settlement risk over the past 20 years

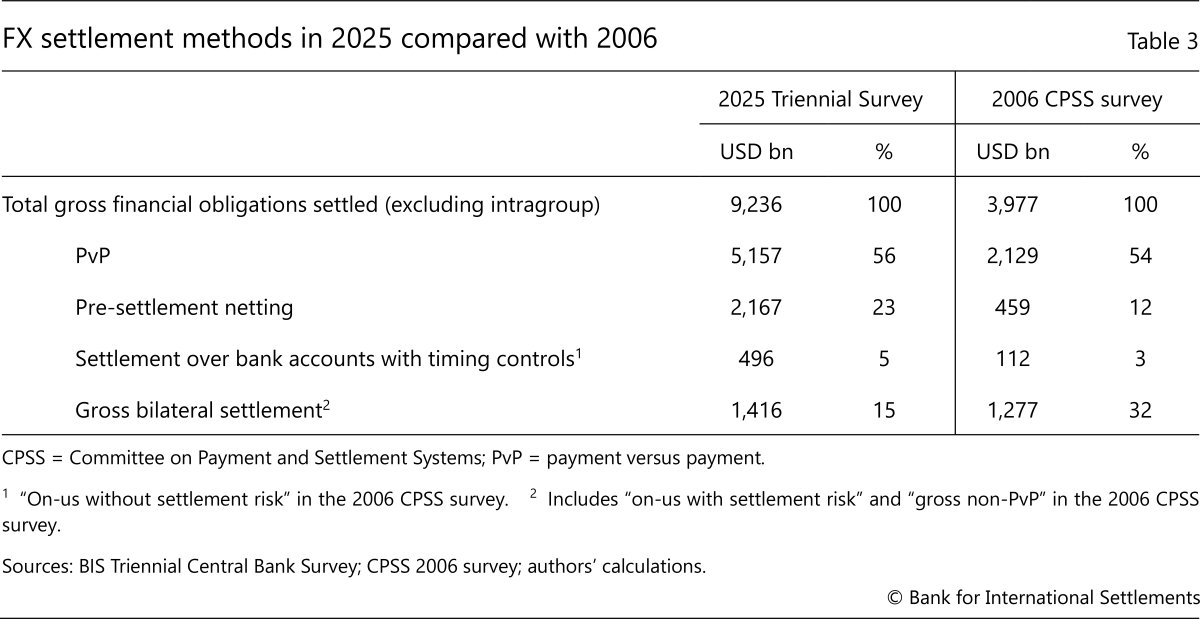

Over the last 20 years, there has been a substantial reduction in the share of transactions subject to FX settlement risk. This is evident from a comparison of the 2025 Triennial Survey with the 2006 CPSS survey of FX settlement risk.11 This comparison highlights that trades settled on a gross bilateral basis have more than halved, from 32% of the average daily settlement in 2006 to 15% in 2025 (Table 3). This reflects ongoing private and public sector efforts to reduce settlement risk.

Even so, PvP settlement increased only modestly in the last two decades, from 54% of average daily settlement to 56%. This rise reflects broader membership and currency coverage by CLSSettlement as well as a larger role of other PvP systems. However, these factors were somewhat offset by the rising share of non-CLS eligible currencies in global FX market turnover, from 19% in 2007 to 22% in 2025 (Graph 3.B). The growing footprint of NBFIs in FX markets was also a factor: in the 2025 survey, NBFIs are generally reported as other financial institutions, for which the use of PvP settlement is much lower than for inter-dealer trades (Graph 1.C).

The main driver that reduced FX settlement risk was greater use of pre-settlement netting. The fractions of trades subject to pre-settlement netting nearly doubled, from 12% of average daily settlement in 2006 to 23% in 2025. Pre-settlement netting gained ground with the rise of service providers that facilitate netting. For example, CLS istarted CLSNet in 2018, which is a bilateral payment netting calculation service for FX trades.12 CLSNet can be used for various FX instruments (eg to/next and same-day trades) and it covers more than 120 currencies, including those not currently settling in CLSSettlement's PvP system.

Settlement fails

The 2025 survey collected, for the first time, data on settlement fails, defined as trades that had been due to settle during April 2025 but that remained unsettled at the end of the month. Settlement fails can incur a financial penalty and also cause market risk (replacement cost risk), liquidity risk and/or reputation risk for the involved parties.

The 2025 survey shows that settlement fails were limited, accounting for only 0.01% of total gross financial obligations settled. Settlement fails among reporting dealers ($121 million) were lower than those with other non-reporting financial institutions ($1.4 billion), potentially reflecting the different levels of operational sophistication and risk controls across counterparty types.

Continued monitoring of settlement fails will be important, especially as more jurisdictions move to shorter securities settlement cycles. Shorter cycles reduce the window to execute and settle FX trades used to fund cross-border securities transactions. As such, firms have less time to rectify confirmation- or settlement-related issues. Unless mitigated (eg via greater automation and straight through processing), this could lead to more failed FX (and associated securities) trades.

Mitigating FX settlement risk: past achievements and the road ahead

For several decades, private and public sector stakeholders have collaborated to mitigate FX settlement risk and promote robust risk management by FX market participants. This has followed the three-pronged approach developed in 1996 by the CPSS, which called for actions by: (i) individual banks to control their FX settlement exposures; (ii) industry groups to provide risk-reducing multicurrency services for settling FX trades; and (iii) central banks to induce private sector progress (CPSS (1996)).

Comparing the results of the 2025 survey with those from 2006 shows that these ongoing efforts have borne fruit and that the overall share of settlement on a gross bilateral basis has decreased substantially. However, due to growth in global FX markets, a large sum of $1.4 trillion is still at risk every day. The 2025 survey highlights the need to further reduce risk, which is on the agendas of several global committees.

The GFXC, as a private-public partnership, has continuously promoted best practices to mitigate FX settlement risk. The 2024 update to the FX Global Code reaffirmed that all market participants have a role to play. The update also introduced the settlement hierarchy (ie the waterfall approach) for mitigating FX settlement risk, which served as the basis for the 2025 Triennial Survey methodology. Further, the updated Code urges market participants to regularly review settlement choices to further reduce risk. The GFXC has also been a strong proponent of enhancing transparency on the magnitude of FX settlement risk. Complementing the Triennial Survey, the GFXC will continue to gather data from some of its member jurisdictions on a semiannual basis.13

In the meantime, as part of the G20 roadmap to enhance cross-border payments, the CPMI, working closely with industry, has explored ways to increase PvP adoption. The March 2023 CPMI report "Facilitating increased adoption of PvP" outlined potential roles for both private and public sector stakeholders.14 More recently, the CPMI has been engaging with the private sector to further address operational barriers to PvP adoption. Private sector experts under the CPMI's Cross-border Payments Interoperability and Extension (PIE) Taskforce conducted further surveys and analysis and suggested possible next steps.15

In addition to these efforts, private sector companies have recently begun offering, or are in the process of developing, new services to complement or expand existing PvP systems. Some of these initiatives leverage innovative technologies, such as distributed ledger technology, that allow for smart contracting to only execute settlement if both parties pay. The BIS Innovation Hub has been exploring longer-term innovative solutions through various projects, such as Projects Jura, Mariana, Rialto and Agorá.

These diverse efforts address several key areas that help to reduce FX settlement risk: increasing the use of PvP systems for already eligible trades; expanding membership and currency coverage within PvP systems; incorporating FX trades with shorter settlement cycles into PvP settlement; and promoting greater use of biliteral netting. The updated Survey methodology provides useful insights into the potential scale of further risk reduction benefits in these areas.

More than 50 years have passed since the failure of Bankhaus Herstatt, yet more remains to be done. Enhanced transparency through the BIS Triennial Survey, alongside the GFXC Survey, plays a valuable role by supporting collaborative efforts as global FX markets continue to evolve.

References

Basel Committee on Banking Supervision (BCBS) (2013): Supervisory guidance for managing risks associated with the settlement of foreign exchange transactions, February.

CLS (2026): "BIS Triennial Survey 2025: FX settlement risk – You can't fix what you can't measure", Shaping FX series, 3 February.

Committee on Payment and Settlement Systems (CPSS) (1996): HYPERLINK "https://www.bis.org/cpmi/publ/d17.htm"Settlement risk in foreign exchange transactions, March.

----- (2008): Progress in reducing foreign exchange settlement risk, May.

Committee on Payments and Market Infrastructures (CPMI) (2023): Facilitating increased adoption of PvP, March.

Cross-border Payments Interoperability and Extension Taskforce: Task Team 1 (2025): FX settlement risk mitigation in (wholesale) cross-border payments, March.

Global Foreign Exchange Committee (GFXC) (2025): Outcomes of the three-year review of the FX Global Code, January.

Huang, W, I Krohn and V Sushko (2025): "Global FX markets when hedging takes centre stage", BIS Quarterly Review, December.

Norman, B (2015): "BoE archives reveal little known lesson from the 1974 failure of Herstatt Bank", Bank Underground, Bank of England, June.

Schenk, C (2014): "Summer in the City: banking failures of 1974 and the development of international banking supervision", The English Historical Review, vol 129, no 540.

Shirakawa, M (2009): "International policy response to financial crises", remarks at the Federal Reserve Bank of Kansas City Jackson Hole symposium, 21 August.

Statistical annex

1 The views expressed in this publication are those of the authors and not necessarily those of the BIS or its member central banks. We thank Iñaki Aldasoro, Gaston Gelos, Branimir Gruić, Matthew Hartley, Henry Holden, Philippe Lintern, James O'Connor, Josh Perers Cook, Daniel Rees, Tara Rice, Hyun Song Shin, Andreas Schrimpf, Costas Stephanouand Goetz von Peter for helpful comments and inputs, and Fanni Leppanen for excellent research assistance.

2 The GFXC brings together central banks and private sector participants with the aim of promoting a robust, liquid, open and appropriately transparent FX market, supported by resilient infrastructure.

3 Due to methodological changes, the 2025 survey results cannot be compared with those from the 2019 and 2022 BIS Triennial Surveys on FX settlement risk.

4 Some PvP systems also act as a CCP. See CPMI (2023).

5 See Shirakawa (2009) on the role of PvP mechanisms in sustaining market liquidity in US dollar swap markets during the Great Financial Crisis.

6 As of June 2026, CLS-eligible currencies are: AUD, GBP, CAD, DKK, EUR, HKD, HUF, ILS, JPY, KRW, MXN, NZD, NOK, SGD, ZAR, SEK, CHF and USD.

7 In some cases, the reporting dealer and its external counterparty may both hold accounts with the same (third-party) bank used for FX settlement, and both legs of their trade may be settled across the books of that bank, which uses an internal risk mitigation mechanism to control the timing of settlement of both legs.

8 Instruments that involve a single payment only are not included (eg non-deliverable forwards, option premia).

9 For example, trades that took place in April but settled in May were included in the FX settlement measures derived from turnover data in the 2019 and 2022 surveys, but not in the 2025 survey.

10 Tight payment schedules of a PvP system may be a challenge for certain currencies whose local funding markets are less liquid. In this case, a dealer who sold a currency to a counterparty without having the offsetting position already locked in may prefer not to settle via PvP.

11 The 2006 CPSS survey used a methodology similar to the 2025 Triennial Survey, except that intragroup settlement was excluded. As noted in footnote 3, methodological changes preclude comparisons with the 2019 and 2022 survey results.

12 The delivery of the net payment amounts is managed by CLSNet users outside the service through existing correspondent banking relationships.

13 GFXC data for the reporting months of April and October will be published on a global aggregated basis. The GFXC's data collection uses the same methodology and reporting template as the Triennial Survey to ensure data consistency and comparability between the two surveys. Although fewer jurisdictions take part in the GFXC Survey, the majority of global FX trade settlement is captured.

14 These include: (i) aligning correspondent banks' operating hours and processes; (ii) exploring potential changes to conventions for an international value date; and (iii) promoting integration and interoperability between legacy and emerging systems.

15 See Cross-border Payments Interoperability and Extension Taskforce: Task Team 1 (2025).