Cross-border links between banks and NBFIs

Box extracted from chapter "International finance through the lens of BIS statistics: offshore activity"

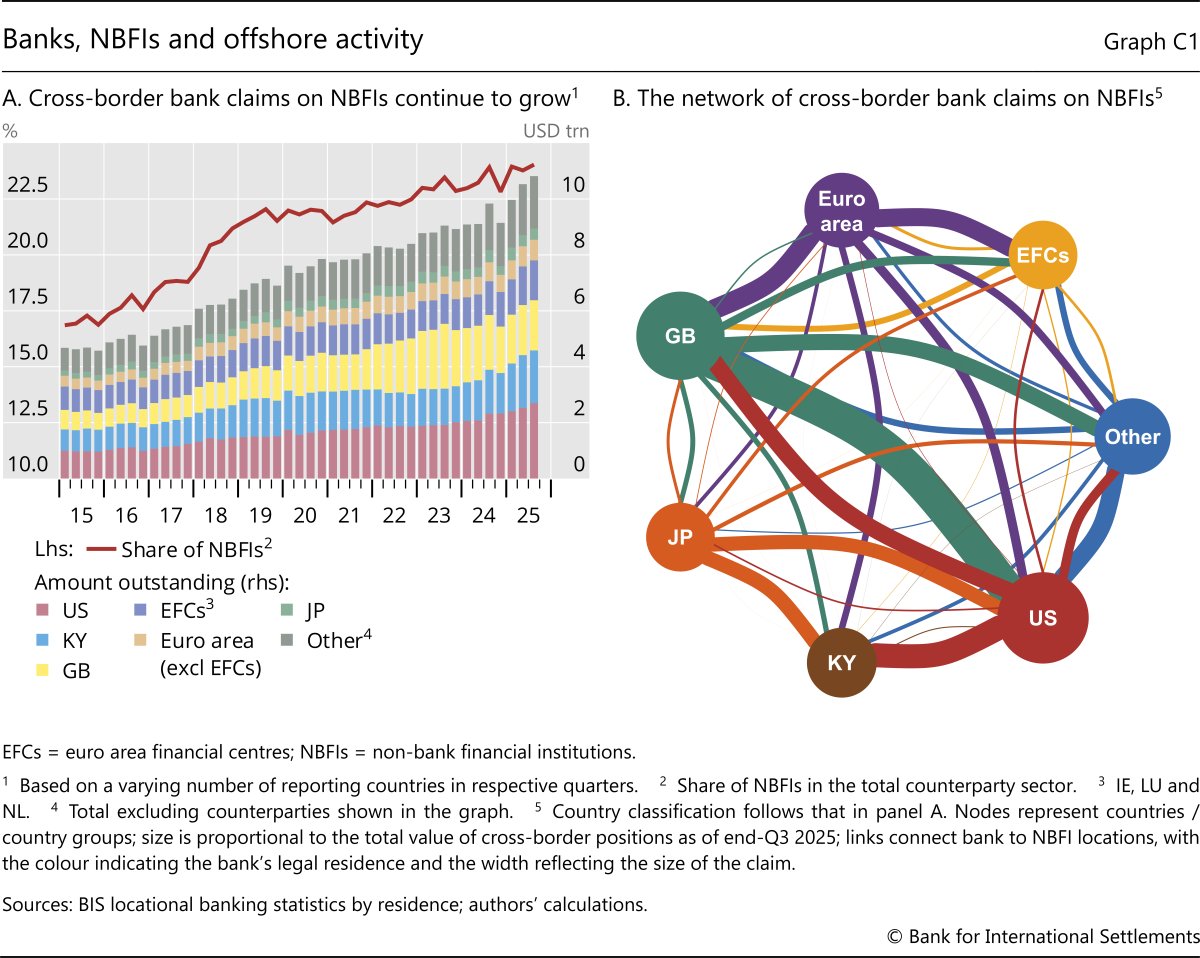

The growing role of non-bank financial institutions (NBFIs) in intermediating cross-border flows has gone hand in hand with a proliferation of links between banks and NBFIs (Aldasoro et al (2020)) – links that often boost offshore activity. Owing to such links, banks' claims on NBFIs expanded much faster than overall cross-border bank lending, taking their share from 7% of overall lending in 2015 to 24% in 2025 (Graph C1.A, red line). This growth was largely concentrated on NBFIs located in the United States, the United Kingdom, the Cayman Islands and euro area financial centres (García Luna and Hardy (2019)).

NBFIs comprise a diverse set of market participants, ranging from investment funds and hedge funds to securitisation vehicles and central counterparties. The sectoral breakdown in the BIS international banking statistics is too coarse to distinguish among NBFIs, but the geographical distribution of bank-NBFI links hints at these NBFIs' underlying activities (Graph C1.B). Banks in the United States have strong links with Caribbean financial centres, especially the Cayman Islands, which probably reflects securitisation activity and prime brokerage (Barth et al (2025)). Banks in Japan also have sizeable claims on NBFIs in Caribbean financial centres, consistent with holdings of securities issued by securitisation vehicles (eg collateralised loan obligations). Central clearing probably contributes to strong ties between the United States and the United Kingdom, as both host large internationally active clearing houses for derivatives and repurchase agreements. Banks in the euro area and other advanced economies (eg Canada and Australia) have substantial claims on NBFIs in euro area financial centres (Ireland, Luxembourg and the Netherlands), in line with exposures to investment funds and other asset managers located there.

The views expressed here are those of the authors and not necessarily those of the BIS or its member central banks.