Fast payments: design and adoption

The payments landscape is evolving rapidly, and fast payment systems (FPS) have emerged as a key innovation. Jurisdictions differ in their approach to designing FPS and in user adoption. In this article we lay out the main design features of FPS that may foster adoption. Cross-country regressions suggest that adoption of fast payments is greater when the public sector plays an active role in the FPS. Other design factors important for adoption are non-bank participation, more use cases and more cross-border connections. 1

JEL classification: H41, L10.

Fast payments, the (near-) real-time transfer of funds between end users, are at the forefront of digitalisation in payments.2 Concerted efforts by both the public and private sectors have transformed the payments landscape by offering faster, cheaper and more inclusive payments. Households and businesses in over 100 jurisdictions now have access to fast payments, with more to be launched in the coming years (CPMI (2021), World Bank (2021)).

Fast payment systems (FPS) enable swift processing of retail transactions to ensure the immediate availability of funds for the recipient. FPS is an umbrella term that encompasses the infrastructure, participating payment service providers (PSPs), end user-facing services and underlying rules that govern the processing and delivery of fast payments.3

Key takeaways

- Fast payments have achieved mass adoption in some jurisdictions but not in others – with adoption likely depending on the design characteristics of different fast payment systems (FPS).

- Adoption of fast payments tends to be more widespread when the central bank owns the FPS, when non-banks participate and when the number of use cases and cross-border connections is greater.

- These insights can help inform the design and development of FPS and other payment infrastructures.

The growing importance of FPS warrants a closer examination of their design features and uptake. Countries have taken different approaches to designing FPS, depending on central bank mandates, societal preferences and changing technological constraints. For example, in some jurisdictions, the public sector – typically led by central banks – plays a more active role by owning and operating FPS. In others, the private sector plays this role. In some FPS, non-bank PSPs offer fast payment services, but not in others. This heterogeneity is also present in the settlement infrastructure and number of (domestic and cross-border) use cases.

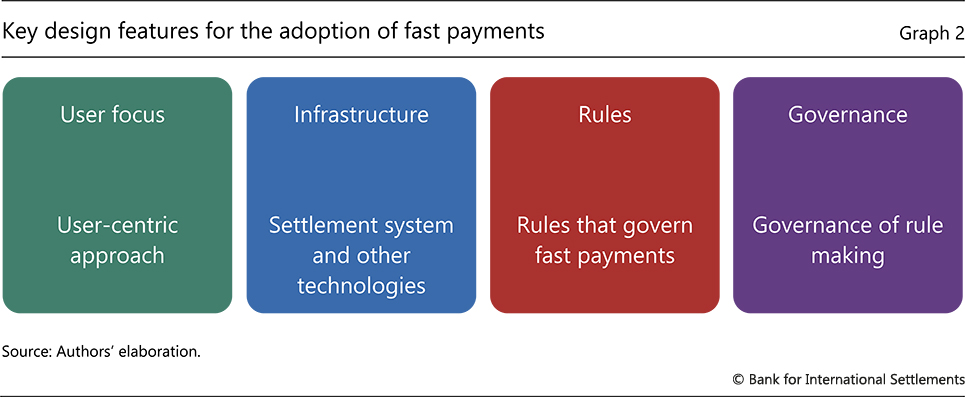

To understand how these differences in design relate to the adoption of fast payments, we conduct a cross-country quantitative analysis of fast payments adoption in 13 jurisdictions. We assess key design features of FPS under four headings: user focus, infrastructure, rules and governance. We include proxies for them in our quantitative analysis.

These design features can have important implications for FPS adoption. User focus captures whether the FPS has features that help meet end user needs, such as a wide scope of domestic and cross-border use cases. Infrastructure captures systems and technology that enable fast payments, which influence the incentives of PSPs to take part in the FPS. Rules, ie requirements and expectations for all stakeholders, define for example which types of institutions (eg banks, non-banks) participate in an FPS. More broadly, governance captures the ownership structure and decision-making process of FPS, which may affect the goals of an FPS and how these goals are achieved. While the uptake of fast payments is influenced by many country-specific characteristics beyond FPS design, the insights from this analysis are helpful for jurisdictions considering the design and development of an FPS.4

Our results suggest that adoption of fast payments indeed depends on design elements in our categorisation. FPS transactions per capita are higher when there is central bank ownership of an FPS (governance), participation by non-bank PSPs (rules) and a greater number of use cases and cross-border connections (user focus).

The rest of the article proceeds as follows. The first section provides an overview of the evolution and potential benefits of fast payments. The second presents our categorisation of key FPS design features. We then draw on these features to study – in a cross-country panel setting – which are most conducive to adoption. The fourth section concludes.

Fast payments: an overview

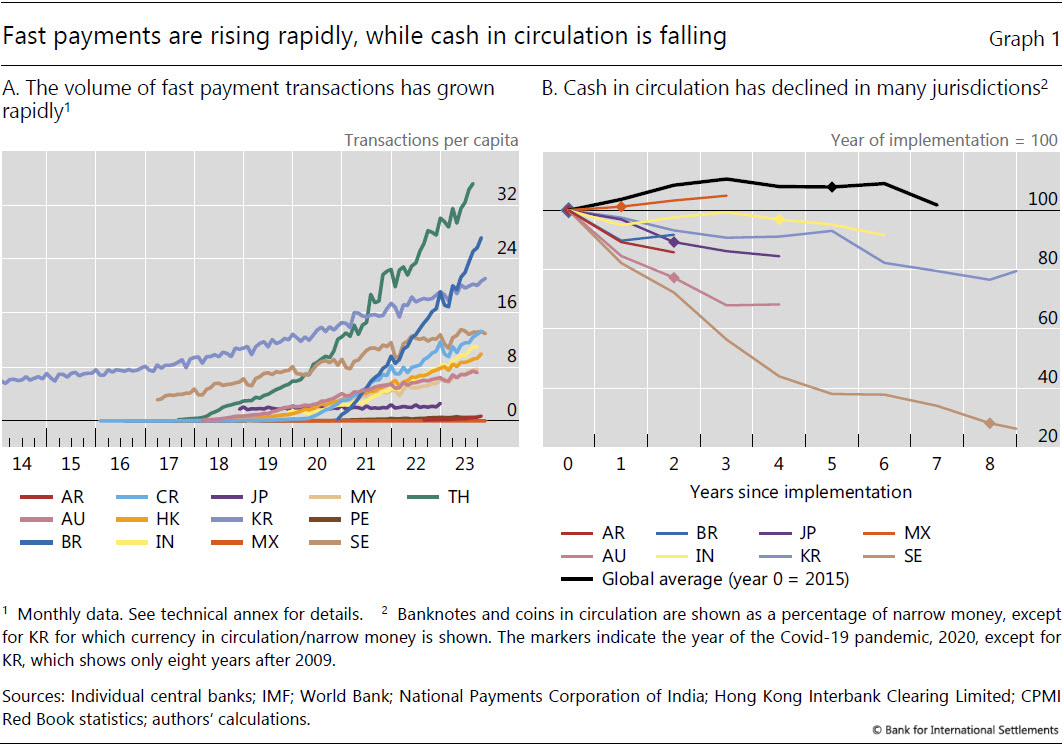

In recent decades, the market for retail payments has undergone significant changes. Driven by technological advances and changing user preferences, digital payments have become increasingly popular.5 The Covid-19 pandemic further accelerated the digitalisation of payments (Auer et al (2022), Glowka et al (2023), Di Iorio et al (2024)). In particular, the use of fast payments has soared (Graph 1.A), albeit to different extents in different jurisdictions.

In line with the trend towards payments digitalisation, the number of fast payments has grown rapidly in most jurisdictions. The biggest markets for fast payments in 2022 (by number of transactions) were India (48.6 billion), China (16.6 billion), Thailand (9.7 billion) and Brazil (8.7 billion).6 In per capita terms, Thailand (35 transactions per person per month), Brazil (27) and South Korea (21) see the largest fast payments volumes. The rise in FPS use has coincided with a fall in cash use in many of these countries (Graph 1.B). This points to increasing digitalisation of payments.

The popularity of fast payments stems from the variety of benefits they provide. Fast payments can offer individuals and businesses with a fast, reliable and secure digital alternative to cash. This is particularly useful in countries with low debit and credit card penetration. Yet even in countries with high card use, fast payments can offer faster and cheaper access to funds for businesses.7 By generating digital footprints, they can provide a gateway to other retail financial services (like credit) for the financially excluded (Aguilar et al (2024), CPMI and World Bank (2020)). Moreover, when fast payments enable interoperability, they allow users to move money easily across PSPs, thus boosting competition (World Bank (2021)). For governments, which are also important end users of payment services, fast payments can help streamline direct benefit transfers or wage payments. For example, in some jurisdictions, governments relied on FPS to distribute Covid-19-related benefit payments to those in need (IMF (2021)). FPS can also trigger enhancements in the larger payment ecosystem and enable further innovations (CPMI (2016)).8

At the same time, FPS exhibit significant network effects that are inherent to payments (Bolt and Humphrey (2005)). As adoption expands, fast payments become more valuable to existing and new users. This may lead to a virtuous cycle where new users encourage further users to join and benefit. A larger user base also offers incentives for the private sector to innovate and develop new payment solutions.

Central banks and the private sector have both been actively involved in the provision of fast payments. In general, payment infrastructures like FPS require significant investment and coordination among many stakeholders. Central banks, often in collaboration with private sector PSPs, can help overcome coordination problems associated with a revamp of existing infrastructures or building new ones (CPMI (2016)). This collaboration can be important in reconciling competing goals in the provision of FPS, which exhibit characteristics of a public good.9

Around the world, FPS have been launched with diverse policy objectives. The most common motivations centre around enhancing financial inclusion, fostering competition between PSPs, driving digitalisation, developing payment infrastructures and enabling innovation (Aurazo et al (2024), CPMI (2016), CPMI (2021), World Bank (2021)). These varied motivations have resulted in a diverse range of FPS design choices. We delve into these design choices in the next section.

Key elements of fast payment system design

In this section, we identify and categorise key elements relevant to the design of FPS that can affect end user adoption of fast payments. We highlight four groups of design features of FPS: user focus, infrastructure, rules and governance (Graph 2).10

User focus

At the heart of FPS design and fast payments adoption is the end user. A user-centric design approach anticipates gaps in market offerings and adapts to changing user needs. An example of such an approach is to enable a wide scope of use cases that are valuable to the end user, eg payments to merchants, bill payments, person-to-person (P2P) payments and government-to-person (G2P) payments.

Aliases are another design feature that provide added value to end users. Aliases are alternatives to bank account numbers that can be used to initiate payments. For example, CoDi, in Mexico, offers the option to use mobile phone numbers to initiate and receive payments. In Thailand, PromptPay offers other aliases in addition to mobile phone numbers, such as the national ID number, e-wallet number and corporate identification number for businesses.

Cross-border functionalities can expand the utility of FPS beyond domestic transactions. These allow users to transact seamlessly across different jurisdictions, enhancing the convenience and efficiency of international transactions. Cheap and fast cross-border transactions can also broaden firms' access to global markets.

User focus can include provision of standardised mobile applications and open application programming interfaces (APIs). Standardised apps may foster ease of use. APIs can facilitate data exchange and make the end user experience smoother.

Infrastructure

Infrastructure refers to the underlying plumbing, ie the systems and technology that enable the provision of fast payments to end users. For fast payments, the key infrastructure is the wholesale settlement system, which settles payment obligations between the PSPs of the end users.

Fast payments are instant or "near-instant" for end users but do not necessarily require real-time settlement among PSPs. Final settlement of obligations among PSPs can occur on either a real-time or a deferred net basis. The use of real-time gross settlement (RTGS) versus deferred net settlement (DNS) models may affect PSPs' cost structure and incentives to participate in the FPS and offer fast payments to clients.11

The decision to introduce fast payments also comes with the choice of using or enhancing a pre-existing wholesale settlement system or building a new one.12 Opting for a new dedicated wholesale system likely entails larger costs, which can translate into differences in end user pricing and may ultimately affect FPS adoption.

Apart from the settlement system, various other types of infrastructure are key to the functioning of an FPS. These may be additional systems like proxy databases, which are responsible for enabling aliases. Additionally, FPS may also rely on messaging standards like ISO 20022 or API standards for communication between PSPs. Auxiliary infrastructures such as cloud computing can also be important to provide scalability for the delivery of fast payments (see Brainard (2022)).

Rules

Rules are key to the functioning of any FPS. They define the requirements and expectations for all stakeholders, including the end users. For example, rules define who is allowed or required to participate in the FPS (eg only banks or also non-bank PSPs). Rules can define other aspects, such as the pricing structure (eg fees charged by the system operator to the participants, fees that PSPs can set for end users), transaction limits and financial requirements (eg capital levels for participating banks and non-banks). The rules may also include the initiation methods (eg whether a user can initiate a payment with a smartphone, web interface or quick response (QR) code or from an automatic teller machine (ATM)).

There is substantial heterogeneity in the rulebooks of fast payments around the world. For example, in Brazil, the central bank mandates the participation of large banks in Pix (Duarte et al (2022)). This differs from other jurisdictions such as India, Thailand and Sweden, where participation is voluntary. Similarly, non-bank PSPs are allowed to participate in the FPS in some jurisdictions but not in others. For example, CoDi in Mexico, Swish/BiR in Sweden and FedNow in the United States are open only to banks (due to legislative requirements in some cases). This heterogeneity is also evident in other aspects of the rulebook, for example, the regulation of end user fees.

Governance

Governance defines how rules (discussed above) and decisions are made for the FPS. Ownership and operation of the FPS are important aspects of governance. Because payment systems have characteristics of a public good, these aspects can reflect the ultimate objectives of an FPS and thus affect end user adoption. Such public goods can be offered by the public sector or by the private sector with public regulation and oversight.

Further reading

The role of the public and private sector in FPS can vary substantially. An FPS may be owned and operated only by the public sector (central banks or other public institutions), as with CoDi in Mexico. Alternatively, both the public and private sector can sit at the decision-making table, irrespective of the ownership or operating model. For example, Brazil's Pix is publicly owned and operated, but hosts an official forum for discussion with the private sector and develops products and services through public consultations. In India, private banks and the central bank jointly govern the rule making for UPI through an organisation created for this specific purpose, the National Payments Corporation of India. Governance may also be only private. In Sweden, the Swish mobile app and underlying BiR settlement system are owned and operated entirely by private banks. Even if a central bank does not engage in the rule making and the FPS is governed only by the private sector, the central bank, as an overseer, still has an interest in the smooth functioning of the FPS.

Cross-country analysis of fast payments adoption

With the key elements of FPS design features at hand, we now seek to provide a deeper understanding of design factors that foster FPS adoption across jurisdictions. The focus on end user adoption is relevant due to its importance in driving network effects. To measure adoption, we focus on the per capita number of FPS transactions.13 We base our analysis on the FPS in 13 jurisdictions, at a monthly frequency, between April 2001 and December 2023. The choice of these jurisdictions is based on the availability of monthly numbers of FPS transactions. In total, we have 1,030 observations at the country-month level.14

To study the design factors conducive to FPS adoption, we specify a panel regression with fixed effects of the form:

where the variable to be explained, ΔFPS transactionsit, is the change (in levels) in the per capita number (or volume) of FPS transactions in country i between month t and the previous month.

As explanatory variables, we include some of the design features presented in the previous section. The selection of our explanatory variables is motivated by the elements of the design framework but are constrained by data availability. Number of use casesit represents the user focus element of our framework in the previous section. Potential uses include P2P payments, payments to merchants, bill payments, cross-border payments, scheduling future payments, bulk payments and request to pay functionality. Another important feature that matters for user-centric design is the cross-border integration of an FPS. # Crossborder connectionsit is the number of other FPS that the users in country i can transact with.

We also consider explanatory variables that capture the underlying infrastructure, participation of non-banks and public vs private ownership of the FPS. The variable Settlement platformit takes the value of 1 if the underlying settlement platform of the FPS is based on RTGS and 0 if it is DNS; NBFI participationit is 1 if non-bank PSPs are allowed to participate; and Public FPSit captures the governance of an FPS – it is 1 if the FPS is owned by the public sector and 0 otherwise.

Additionally, we control for various factors that may also affect adoption. ΔFPS transactionsit-1 is the lagged change in per capita volume of FPS transactions (in levels) and controls for adoption dynamics and the size of the user base in the previous period.15 We also include country fixed effects and year fixed effects. Country fixed effects control for institutional factors in each jurisdiction that do not change over time. Year fixed effects control for time-specific developments, such as the Covid-19 pandemic. Countries may differ along many dimensions outside of our framework – eg in terms of general legal frameworks, market conditions and social preferences. There may also be common elements across countries that change over time (eg due to the Covid-19 pandemic). Including both country and time fixed effects is therefore our preferred regression specification.

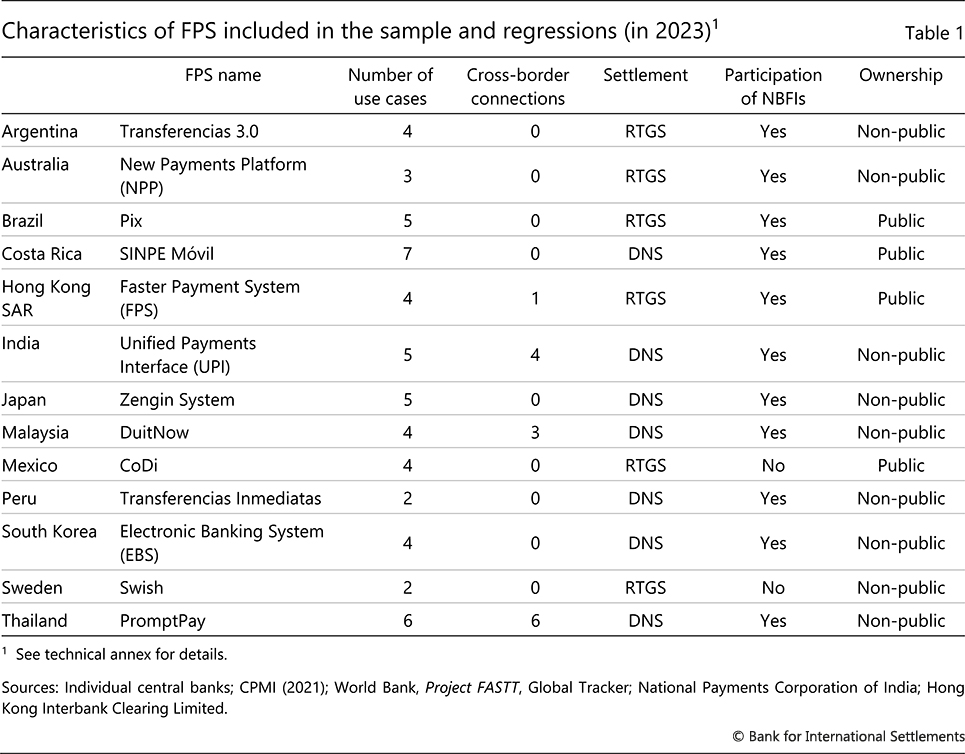

In Table 1, we summarise key characteristics of the FPS covered in our regression analysis. Note that some of these, eg number of use cases, number of cross-border connections and participation of non-bank PSPs, evolve over time. While our data set captures this time variation, the table reports just a snapshot of data for 2023.

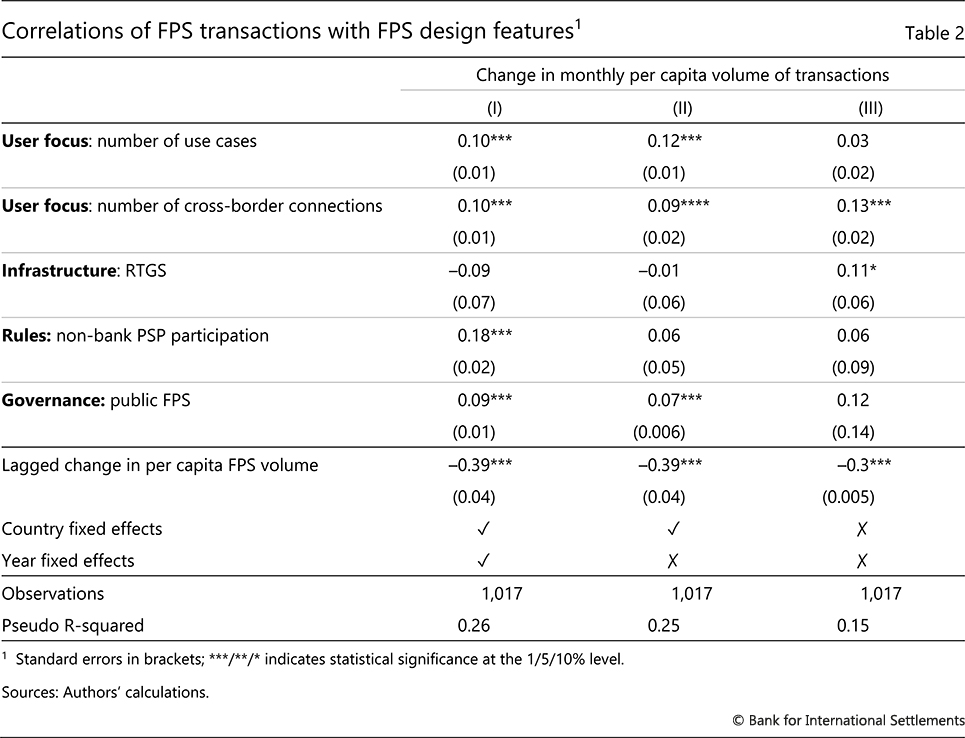

Our regressions (Table 2) show that uptake of fast payments is indeed higher when certain design features are in place. In our preferred specification (column I), we find a larger growth in the monthly volumes of FPS transactions when there are more use cases and cross-border connections, when non-bank PSPs participate and when the FSP is publicly owned. In contrast, the type of settlement system is not significantly linked to changes in monthly volume of FPS transactions.16

These relationships are not only statistically significant but also have a sizeable magnitude. The average number of FPS transactions per capita is five per month in our sample. Non-bank PSP participation is associated with an increase of 3.5% in the number of FPS transactions per capita. An additional use case offered by the FPS is associated with a 2% increase and an additional cross-border connection with an increase of the same magnitude. Public ownership of FPS entails an increase of 1.8% in the number of FPS transactions.

The adoption of FPS may also be reflected beyond narrow metrics of transactions, notably in indicators of financial inclusion. In some jurisdictions, the introduction of FPS has indeed gone hand in hand with greater access to digital payments and other services. Box A shows that there is a robust relationship between FPS and access to transaction accounts, payments and credit in different jurisdictions.

Our results highlight the importance of collaboration between the public and private sectors as well as of user-centric design. FPS owned by the public sector (often central banks) may be operated in a way that allows for wider participation and lower fees. They may have explicit mandates to make the retail payments market more open, inclusive and competitive. Some FPS, like Pix in Brazil, also mandate participation by large private banks.17 Meanwhile, participation of non-bank PSPs in the FPS may foster the uptake of fast payments when these non-bank PSPs offer new payment methods or provide payment services to customers that are not served by banks. Simultaneously, a variety of uses for fast payments and cross-border connections makes the FPS more valuable for users.

Of course, the industrial organisation of the banking and payments market may also matter. In particular, public ownership by itself may not be enough to foster end user adoption. Given the oligopolistic market structure of many banking industries, large banks may still find ways to reinforce their competitive advantage by excluding or limiting participation of smaller competitors or non-bank PSPs. In some instances, large banks may have insufficient incentives to join a public FPS, and participation may need to be mandated. In other cases, there may be competing FPS initiatives. These considerations underscore the importance of broad buy in and of a collaborative approach between the public and private sector.

Conclusions

Fast payments offer secure, low-cost and quick transactions and are becoming increasingly popular across many jurisdictions. They foster competition among PSPs and serve as a gateway to additional financial services. The public good characteristics of FPS make their design important for central banks and public policy.

We present key design features that are conducive to the adoption of fast payments. There are four groups: user focus, infrastructure, rules and governance. We find that the adoption of FPS is stronger with central bank ownership, more use cases, more cross-border connections and participation by non-bank PSPs.

The insights from our quantitative analysis may be relevant for other public infrastructures, such as central bank digital currency (CBDC) systems and unified ledgers. Publicly owned FPS may be designed to prioritise a public good perspective, aiming for open, inclusive and competitive payment markets. A user-centric approach, addressing diverse needs such as P2P transactions, merchant payments and cross-border transactions is also important. The inclusion of non-bank providers may improve access for underserved customers. Keeping these features in mind may help to build strong public infrastructures that are widely adopted and support policy goals.

References

Aguilar, A, J Frost, S Kamin, R Guerra and A Tombini (2024): "Digital payments, informality and productivity", mimeo.

Auer, R, G Cornelli and J Frost (2022): "The pandemic, cash and retail payment behaviour: insights from the future of payments database", BIS Working Papers, no 1055, December.

Aurazo, J, H Banka, J Frost, A Kosse and T Piveteau (2024): "Central bank digital currencies and fast payment systems: rivals or partners?", mimeo.

Bank for International Settlements (2020): "Central banks and payments in the digital era", Annual Economic Report, Chapter III, June

Bech, M and J Hancock (2020): "Innovations in payments", BIS Quarterly Review, March, pp 21–36.

Bolt, W, and D Humphrey (2005): "Public good issues in TARGET: natural monopoly, scale economies, network effects and cost allocation", European Central Bank Working Paper Series, no 505, July.

Brainard, L (2022): "Progress on fast payments for all - an update on FedNow", speech at the FedNow Early Adopter Workshop, Rosemont, Illinois, 29 August.

Committee on Payments and Market Infrastructures (CPMI) (2016): "Fast payments – enhancing the speed and availability of retail payments", CPMI Reports, no 154, November.

Cornelli, G, L Gambacorta, H Qiu and V Shreeti (2024): "Fast payments and crowding-in of private investment", mimeo.

Cornelli, G, J Frost, J Warren, C Yang and C Velasquez (2024): "Retail fast payment systems as a catalyst for digital finance", mimeo.

CPMI (2021): "Developments in retail fast payments and implications for RTGS systems", CPMI Papers, no 201, December.

CPMI (2023): Linking fast payment systems across borders: considerations for governance and oversight, Interim report to the G20, October.

CPMI and World Bank (2020): "Payment aspects of financial inclusion in the fintech era", CPMI Papers, no 191, April.

Di Iorio, A, A Kosse and R Szemere (2024): "Tap, click and pay: how digital payments seize the day", CPMI Briefs, no 3, February.

Duarte, A, J Frost, L Gambacorta, P Koo Wilkens, H S Shin (2022), "Central banks, the monetary system and public payment infrastructures: lessons from Brazil's Pix", BIS Bulletin, no 52, March.

Glowka, M, A Kosse and R Szemere (2023): "Digital payments make gains but cash remains", CPMI Briefs, no 1, January.

International Monetary Fund (IMF) (2021): "Policy responses to Covid-19", Policy Tracker.

Petralia, K, T Philippon, T Rice and N Veron (2019) : "Banking disrupted?: financial intermediation in an era of transformational technology," International Center for Monetary and Banking Studies.

World Bank (2021): Considerations and lessons for the development and implementation of fast payment systems, September.

Glossary

Alias: a single piece of information (eg mobile phone number, e-mail address, tax identification, a string of characters, etc) that represents the set of information required to identify a bank account (eg bank name, bank branch, bank account number).

Application programming interface (API): a set of rules and specifications followed by software programs to communicate with each other, and an interface between different software programs that facilitates their interaction.

Deferred net settlement (DNS): a net settlement model that settles on a net basis at the end of a predefined settlement cycle.

Fast payments: real-time or near real-time transfers of funds between accounts of end users as close to a 24 hour per day and seven days per week basis as possible. End users can be individuals, merchants, businesses or public institutions. Funds can be commercial bank money or e-money.

Fast payment system (FPS): the infrastructure, participating payment service providers (PSPs), end user-facing services, as well as the underlying rules that govern the processing and delivery of fast payments.

Payment service provider (PSP): a financial institution that offers payment services. A PSP may be a bank or a non-bank financial institution.

Proxy database: a database system that connects aliases to bank account information.

Real-time gross settlement (RTGS): the real-time settlement of payments, transfer instructions or other obligations individually on a transaction-by-transaction basis.

Technical annex

Graph 1.A: The relevant central banks that provided the data on the volume of transactions are: Central Bank of the Argentina, Reserve Bank of Australia, Central Bank of Brazil, Central Bank of Costa Rica, Bank of Japan, Bank of Korea, Central Bank of Malaysia, Bank of Mexico, Central Reserve Bank of Peru, Sveriges Riksbank and Bank of Thailand. The data on population are retrieved from the World Bank.

Table 1: The relevant central banks that provided the information are the same as in Graph 1.A. Some of these characteristics, like the number of use cases, cross-border connections and participation of non-bank PSPs, have evolved over time. We report data from the latest period available. For ownership, non-public refers to FPS that are either semi-public or private. Semi-public FPS are owned partly by private institutions and partly by public institutions. Examples of use cases are peer-to-peer payments, payments to merchants, bill payments and cross-border payments. Cross-border connections refer to the number of FPS that the users in the country can transact with internationally.

1 The authors thank Iñaki Aldasoro, Douglas Araujo, Jose Aurazo, Claudio Borio, Giulio Cornelli, Sebastian Doerr, Rodney Garratt, Gaston Gelos, Thomas Lammer, Benoît Mojon, Takeshi Shirakami, Andreas Schrimpf, Tara Rice, Hyun Song Shin, Alexandre Tombini and Peter Wierts for helpful comments. We thank Cecilia Franco and Ilaria Mattei for excellent research assistance, and Joon Suk Park, Koji Takahashi and central bank counterparts for support with data on fast payment systems. The views expressed in this article are those of the authors and do not necessarily reflect those of the Bank for International Settlements (BIS) or the BIS Committee on Payments and Market Infrastructures (CPMI).

2 For the formal definition used in this article, see the glossary. The meaning of the term "fast payments" may vary slightly based on the context in which it is used. See CPMI (2016), Bech and Hancock (2020), World Bank (2021).

3 Like fast payments, the use of the term "fast payment systems" can also vary. It sometimes refers to only the infrastructure underlying the delivery of fast payments, its governing rules and participants (see CPMI (2016, 2021)). Our interpretation is wider and includes the end user-facing services offered by multiple participants, such as the mobile payment app built on top of these infrastructures, and the rules governing these.

4 Other factors that may influence the adoption of fast payments that are unrelated to the design of the FPS may include availability of other payment alternatives, internet and smartphone penetration, digital literacy, general legal frameworks (for example, legal provisions for non-bank participation) and societal preferences.

5 For a discussion on changing user preferences and the impact of technological developments in the financial sector, see Petralia et al (2019).

6 Data for India (IMPS and UPI) and China (IMPS) are taken from Table 8 ("Volume of transactions processed by selected payment systems") of the financial market infrastructures and critical service providers data made available through the BIS Data Portal (https://data.bis.org/topics/CPMI_FMI). Data for Brazil (Pix) and Thailand (PromptPay) are sourced from the Central Bank of Brazil and the Bank of Thailand.

7 For example, for merchants, the cost of using Pix, the FPS in Brazil, is 0.22% of the transaction value (Duarte et al (2022)). This is much lower than the average fees for credit (2.2%) and debit cards (1.1%).

8 For example, some jurisdictions used the launch of an FPS as an opportunity to implement the ISO 20022 messaging standard for other payment systems as well. The use of fast payments may also help encourage the use of QR codes for other applications.

9 Public goods are defined as being non-rival (use by one party does not diminish the ability of another to use them) and non-excludable (no party can be excluded from using them). FPS can be provided as a public good, both when publicly owned or privately owned, and subject to public regulation and oversight. If there were no public regulation and oversight, a payment system operated solely by private parties may have inefficiencies. In particular, private providers may have an incentive to charge high fees for use and/or to restrict access to only certain participants in order to obtain monopoly rents. In the absence of public sector involvement, there could also be coordination failures in payment system provision. While the public sector may face better incentives to operate such a system, adoption may be low without sufficient buy-in by private PSPs. For further details, see BIS (2020).

10 This is not intended to be an exhaustive list, but rather it provides one approach to analysing important key design features of FPS.

11 The use of RTGS versus DNS generally involves a trade-off between liquidity costs and settlement risks. This trade-off may vary depending on the size of the transactions. Given the retail nature of fast payments, the credit and liquidity risks may be limited. PSPs' incentives to participate in the FPS also depend on other system design features, such as operational arrangements, liquidity management features and risk management mechanisms. See CPMI (2021) for a discussion of different setups of RTGS and DNS systems.

12 South Korea's Electronic Banking System (EBS) settles the payment obligations of PSPs on a deferred basis in the pre-existing BoK+ Wire system (RTGS). Brazil already had a functioning RTGS system prior to the launch of Pix and decided to develop a new RTGS system to guarantee service levels with a more modern technology. In India, an RTGS system also existed prior to the launch of the United Payments Interface (UPI), but UPI functions on a DNS system.

13 There are other ways to measure successful adoption of fast payments, especially given the diverse policy objectives of jurisdictions. Other relevant metrics may include private investment in payment markets (Cornelli, Gambacorta, Qiu and Shreeti (2024)) or downloads of digital finance apps (Cornelli, Frost, Velasquez, Warren and Yang (2024)).

14 Note that not all jurisdictions have an FPS throughout the length of the sample. The countries in our sample are Argentina, Australia, Brazil, Costa Rica, Hong Kong SAR, India, Japan, Malaysia, Mexico, Peru, South Korea, Sweden and Thailand, each of which introduced an FPS at some point during this period.

15 Although using the lagged dependent variable in our regression may introduce Nickell bias, our primary focus is on the coefficients of design variables, not the lagged dependent variable per se.

16 Similar results hold when using only country fixed effects (column II) or no fixed effects (column III). Our results are robust to other specifications that consider the dependent variable and the lagged dependent variable in levels. We also include the age of the FPS as an additional control variable, and our results do not change. Finally, results are robust to using the lagged level of FPS transactions per capita as a control and to using the level of FPS transactions per capita as a dependent variable.

17 Ideally, mandatory participation by banks would be a further variable in our regressions. Yet unfortunately, data on this design feature are not readily available.