Public support for ESG markets: an Asian perspective

Environmental and social issues are particularly acute in the Asia-Pacific region. The region has experienced about 40% of all global climate disasters over the last three decades. Moreover, it was hard hit by the pandemic, which exacerbated social disparities. Against this backdrop, policy authorities in the region have stepped up their efforts to address environmental and social issues. This box takes stock of recent developments in Asian ESG markets and provides an overview of policy efforts to foster such markets.

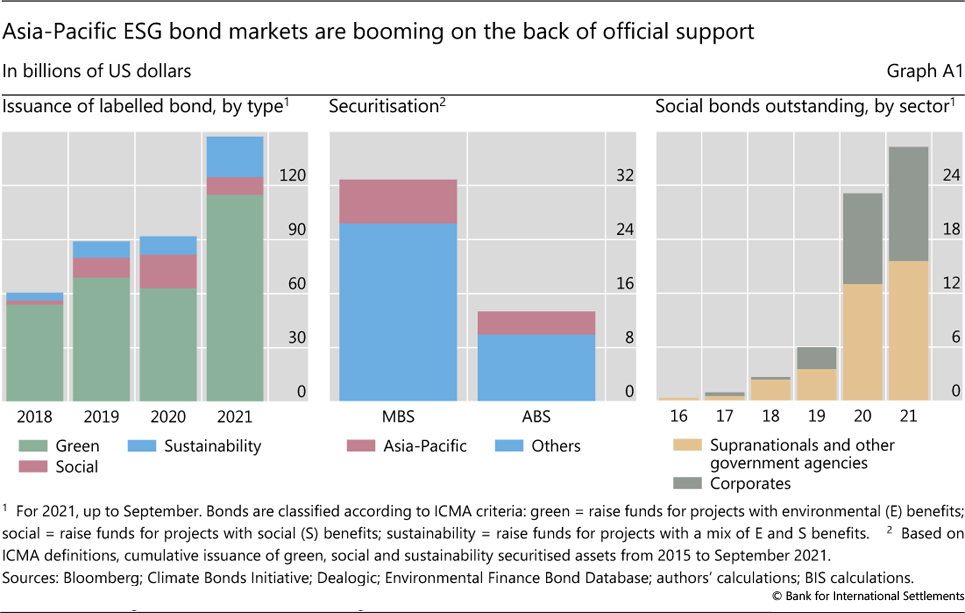

The development of ESG markets in the Asia-Pacific region is well under way. The region accounts for about 20% of global outstanding amounts of labelled bonds. The year to date has seen strong issuance, up 66% compared to 2020 (Graph A1, left-hand panel). The region is also well represented in the nascent ESG securitisation markets, with a 20% share (centre panel).

The year to date has seen strong issuance, up 66% compared to 2020 (Graph A1, left-hand panel). The region is also well represented in the nascent ESG securitisation markets, with a 20% share (centre panel).

Several regional authorities are deploying a wide range of measures to actively foster ESG markets. The People's Bank of China (PBoC) has taken the lead in the development of taxonomies, issuing the Green Bonds Catalogue and joining forces with the EU to standardise taxonomies across different regions. New Zealand has made climate risk disclosures mandatory for banks and insurers. Hong Kong SAR has announced that climate-related disclosures will be mandatory for listed firms and various financial institutions no later than 2025. In addition, climate stress tests are under way or have been planned in several jurisdictions, including Australia, China, Hong Kong, Japan and Singapore. The Hong Kong Monetary Authority and the Monetary Authority of Singapore subsidise the issuance costs of green bonds and loans. Central banks in the region are also integrating ESG principles into monetary policy and reserve management operations. Green bonds have become eligible collateral for the PBoC's lending facilities. The PBoC, the Bank of Japan and the Central Bank of Malaysia (BNM) have announced facilities to subsidise loans to commercial banks that either support decarbonisation sectors (PBoC and BNM) or purchase green bonds or extend green loans (Bank of Japan).

The People's Bank of China (PBoC) has taken the lead in the development of taxonomies, issuing the Green Bonds Catalogue and joining forces with the EU to standardise taxonomies across different regions. New Zealand has made climate risk disclosures mandatory for banks and insurers. Hong Kong SAR has announced that climate-related disclosures will be mandatory for listed firms and various financial institutions no later than 2025. In addition, climate stress tests are under way or have been planned in several jurisdictions, including Australia, China, Hong Kong, Japan and Singapore. The Hong Kong Monetary Authority and the Monetary Authority of Singapore subsidise the issuance costs of green bonds and loans. Central banks in the region are also integrating ESG principles into monetary policy and reserve management operations. Green bonds have become eligible collateral for the PBoC's lending facilities. The PBoC, the Bank of Japan and the Central Bank of Malaysia (BNM) have announced facilities to subsidise loans to commercial banks that either support decarbonisation sectors (PBoC and BNM) or purchase green bonds or extend green loans (Bank of Japan).

In addition, regional and multilateral development banks have been playing an especially active role in deepening ESG markets, particularly the labelled bonds segments. On the supply side of these markets, the Asian Development Bank (ADB) and various government agencies in Korea and Japan have issued the bulk of social bonds in the region (Graph A1, right-hand panel). Agencies and multilateral development banks are also helping support demand for new ESG assets by mobilising private and public capital. The Asian Infrastructure Investment Bank (AIIB), for example, has provided anchor capital for a fund dedicated to climate bonds. In collaboration with the development financing community, the BIS is establishing an Asian Green Bond Fund, to channel global central bank reserves to green projects in the Asia-Pacific region.

The views expressed in this box a re those of the authors and do not necessarily reflect those of the BIS. Based on data from Bloomberg, as of end-November 2021. The ESG structured products segment is still small overall. At about $10 billion, ABS backed by green and social bonds correspond to less than 1% of the outstanding stock of the underlying securities. For a full review, see De la Serve, M-E, D Revelin and K Triki, "Green finance in the Asia-Pacific region: mobilisation spearheaded by central banks and supervisory authorities", Banque de France Bulletins, no 237, article 4, September 2021. For more details, see S Tiwari, "Greening Asia for the long haul: What can central banks do?", Brookings Institute Future Development Blog, October 2021.