The rise of private markets

The last two decades have seen the growth and consolidation of private markets. These revolve around funds gathered from institutional investors by "alternative asset managers", typically private equity or venture capital firms that have subsequently expanded into credit. In an environment of light regulation, long investor horizons and low interest rates, the involvement of private market funds in firms' investment financing and restructuring has grown over time. The interactions of these increasingly important non-bank financial intermediaries with the wider economy and their response to monetary policy have not been fully explored. We find that, despite long investment horizons, private markets are as procyclical as public markets. As for monetary policy, its transmission differs according to the type of private market fund, exerting the strongest effect on private credit funds. 1

JEL classification: G15, G23, G32.

External financing is increasingly intermediated outside traditional channels. Banks and other institutions active in public capital markets, such as equity and corporate bond mutual funds, remain key financing sources for large and mature corporates. That said, "alternative asset managers" (AAMs) have become pivotal for smaller firms globally, including in emerging market economies (EMEs). Many AAMs were established as private equity firms that later expanded into credit, thus turning themselves into one-stop capital providers for firms less able or willing to access traditional sources.

Private markets have three features that distinguish them from public markets. First, there is limited liquidity transformation because investors commit capital for extended periods. Second, these investors tend to be large and sophisticated entities such as pension funds, whose focus on long-term returns enables target companies to confront significant earnings volatility. Third, the regulation of private market investment vehicles is relatively light, partly reflecting the lesser degree of liquidity mismatches and also the limited presence of retail investors.

Key takeaways

- Private capital markets have become a major force in all aspects of firm financing and restructuring in advanced and also emerging economies, particularly in Asia.

- Financing is routed mainly through "alternative asset managers", which offer a suite of private equity, venture capital and private credit funding options across the life cycle of companies.

- Compared with public markets, the funding provided through private markets is just as procyclical, while sensitivity to monetary policy varies across business segments.

Private markets confer important benefits. They provide young and innovative firms with better access to finance, thus supporting long-term economic growth. AAMs also add value by advising entrepreneurs and introducing start-up firms to a wide network of industry contacts. This eases funding constraints, which may arise from a lack of tangible assets to post as collateral or from an inability to shoulder the compliance costs of mandatory disclosures in public markets.

From a policy perspective, some aspects of private market functioning may deserve attention. We find procyclical risk-taking patterns, similar to those seen in public markets and stemming from search for yield and fund leverage. Separately, monetary policy transmission appears weak in some segments, but in private credit it is comparable with that in public markets. Further work on these and related issues would help to ensure that private markets do not become a blind spot for policymakers.

The rest of this special feature is organised as follows. The first section surveys the global growth of private markets, placing it in the context of evolving trends in public markets. The second presents the private market ecosystem. The third explores policy relevant issues, including procyclicality.

The global footprint of private markets

Private markets encompass a varied set of transaction types implemented through specialised funds. Some of these focus on providing equity capital by acquiring a minority stake in small start-up firms with high growth potential (venture capital, VC), or in somewhat more mature firms with good prospects or under restructuring (growth capital, GC). We refer to these collectively as VGC funds. In turn, so-called private equity (PE) funds specialise in mergers and acquisitions (M&A), aiming mainly to acquire controlling stakes in more established (often publicly traded) corporates, with the purpose of improving their value through restructuring for subsequent resale. By contrast, the assets of private credit (PC) funds typically consist of loans to small firms with high credit risk. Finally, there are funds that focus on "real assets", investing in infrastructure, real estate, commodities and other materials and resources. The box presents an overview of business segments and investment vehicles.

The rise of private markets reflects in part structural shifts in financial intermediation that trace their roots to the 1980s. These shifts started in the United States and stemmed from changes in banks' business practices and the role of public markets.2 Echoing their success in the United States, private markets began to develop in other parts of the world.

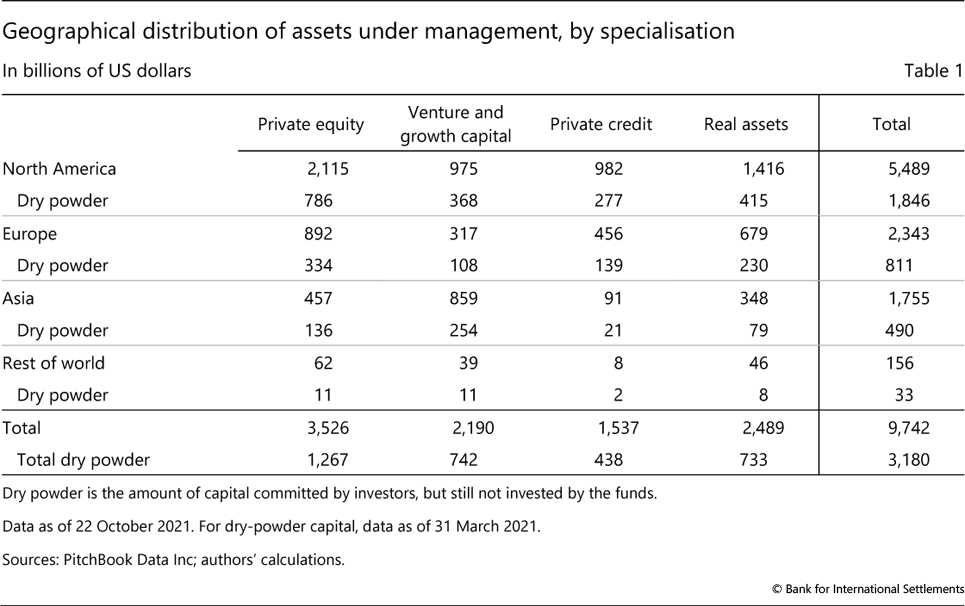

Private markets are largest in North America and Europe, and feature a different mix of specialisations in Asia. Of the nearly $10 trillion in global assets under management (AUM) – which compares with an estimated $40 trillion in non-government mutual funds – 56% are domiciled in North America, 24% in Europe and 18% in Asia (Table 1). The relative weight of the various fund specialisations is similar in North America and Europe, with PE and real assets representing about 40% and almost 30%, respectively, in both areas. In Asia, however, VGC encompasses half of the assets and PC is comparatively smaller.

In all jurisdictions, a substantial part of the funds raised are not immediately deployed. So-called "dry powder" represents commitments made by ultimate investors that have not been disbursed, typically because suitable deals have yet to be identified. Dry powder stood at about $3 trillion overall in early 2021 and represented about 40% of PE assets in North America and Europe, and approximately 30% of VGC assets in Asia (Table 1). These large, untapped capital commitments suggest a strong demand for exposure to private market assets.

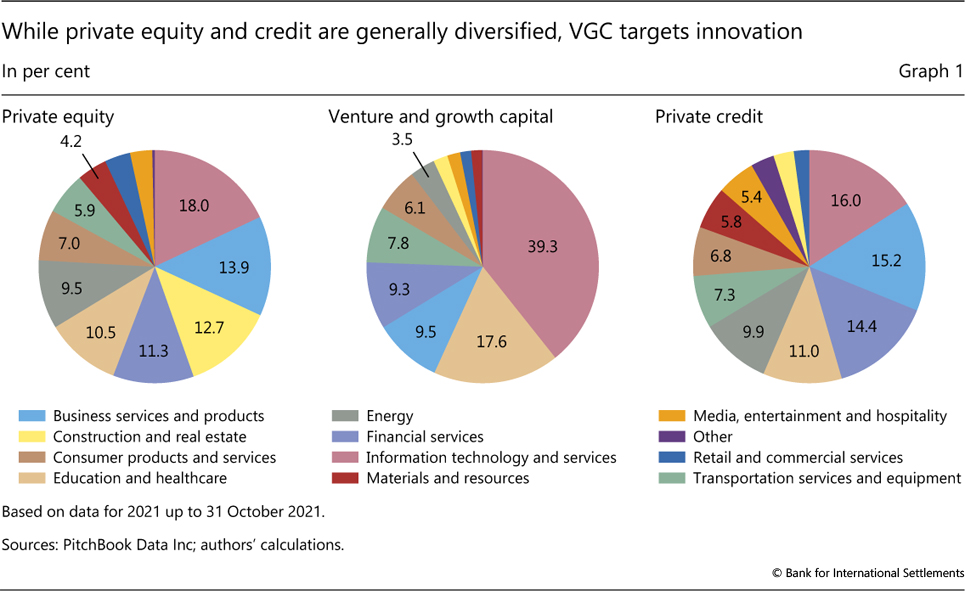

Private market funds with different specialisations tend to invest in different industries. We focus now on the fund types that are most closely linked to company funding: PE, VGC and PC, setting real assets aside. Given that it often involves highly leveraged transactions, PE has traditionally focused on less cyclical sectors with more resilient cash flows (Borio (1990)). At present, information technology, business services, education and healthcare, and financial services comprise more than half of the global portfolio of these funds, while construction, energy, and resources represent only about a quarter (Graph 1, left-hand panel). By contrast, VGC is heavily tilted towards the more innovative areas of the economy. Information technology is by far the main recipient of VGC financing, accounting for about 40% of the global portfolio. It is followed by education and healthcare, business services and financial services, including fintech, representing almost 30% (centre panel). PC's industry portfolio is diversified along much the same lines as that of PE, but with a noticeably smaller share of construction and real estate (right-hand panel).

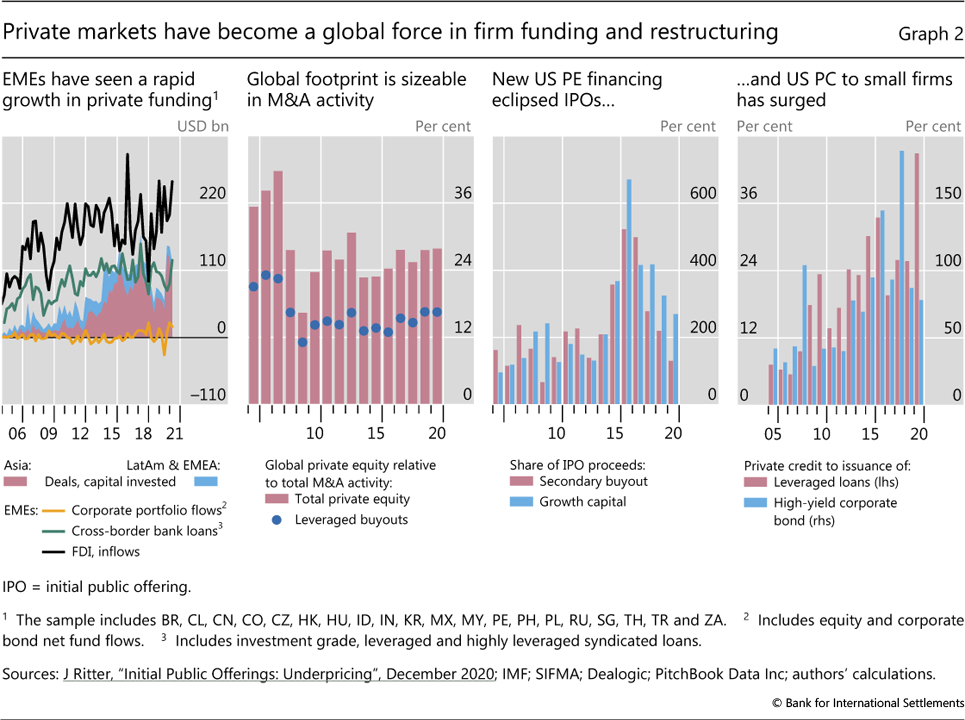

In terms of activity flows, EME private markets have become comparable with the more traditional part of the financial system. Capital invested in EMEs through private markets rose markedly in the mid-2010s, targeting mostly emerging Asia (Graph 2, first panel, solid areas). Investment funds mobilised by private markets to and within EMEs have eclipsed portfolio flows to EME corporate assets (yellow line). Moreover, private investments have matched syndicated lending to EME corporates since the mid-2010s surge (green line), when they also started to approach the volumes of gross foreign direct investment flows (black line).3

The footprint of private funds has become material in many market segments. Overall acquisition activity by global PE funds makes up about a quarter of global M&A volumes (Graph 2, second panel, red bars). This activity is based mainly on leveraged buyouts (LBOs), which have continued to represent about 15% of total global M&A since the Great Financial Crisis (GFC) (blue dots). In turn, the propensity of firms to remain private for longer than in the past, particularly in the United States, has boosted another PE business line – secondary buyouts. These deals consist in the acquisition of a private company, which is sponsored by a private market fund, by yet another private market fund. In recent years, secondary buyouts in the United States have often exceeded the volume of initial public offerings (IPOs), which have long been the main route for early investors who wish to liquidate their stakes (third panel, red bars).4 The propensity of US companies to stay private is also behind the growth-capital segment of VGC outpacing IPOs for most of the last two decades (blue bars).5 On the PC side, lending flows to small and risky firms have increased markedly, now amounting to a meaningful fraction of the leveraged loan and high-yield bond issuance by more established firms (fourth panel).

Key players in the private market ecosystem

Activity in private markets revolves around institutional investors, which provide nearly all the capital, and AAMs, which intermediate the funds.

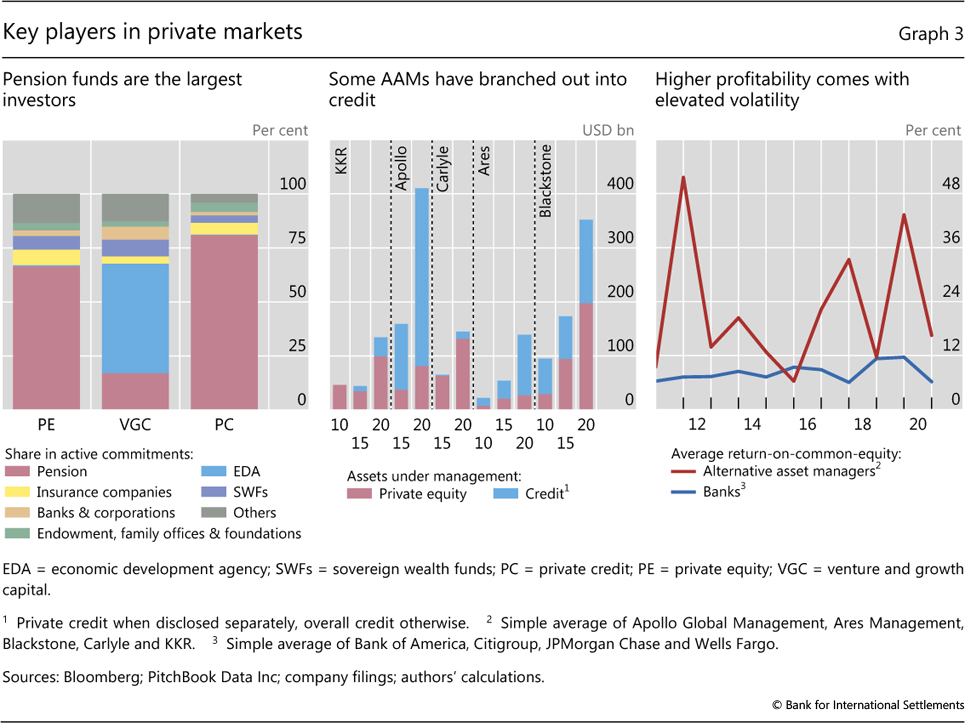

The ultimate investors are typically large entities. Pension funds are the dominant players in PE and PC, with a share often exceeding 70% of capital commitments (Graph 3, left-hand panel). By contrast, economic development agencies – usually supranational or governmental entities – take the leading role in VGC. Insurance companies also have a relatively large participation in the safer business segments (PE and PC), while sovereign wealth funds focus more on PE and VGC. Finally, the limited activity of banks and corporations is tilted towards VGC.

Many AAMs grew organically by adding activities to their initial monoline focus. AAMs often trace their roots to private equity and/or venture capital and have used the expertise and relationships developed in these sectors to expand to other sectors, including credit. The overall expansion took place on the back of a relatively light regulatory regime for AAM funds. The main reasons for the light touch are the small involvement of retail investors and the limited degree of liquidity transformation, since private funds tend to be of the closed-end type.6 Despite commonalities in their evolution, however, the relative weight of credit and equity instruments in asset portfolios varies across the largest AAMs, which manage about 15% of global PE assets (Graph 3, centre panel).

Further reading

- Aramonte S (2020): Private credit: recent developments and long-term trends, BIS Quarterly Review, March.

- Aramonte S, Avalos F (2019): Structured finance then and now: a comparison of CDOs and CLOs, BIS Quarterly Review, September.

The profitability of AAMs is higher but more volatile than that of banks. AAMs earn steady fees for asset allocation and ancillary services. They also invest their own capital in the funds they manage, thus taking on risk that manifests itself as large year-to-year swings in profitability (Graph 3, right-hand panel). Part of the additional return on equity obtained by these firms stems from liquidity risk (which earns a premium of about 3% a year; see Franzoni et al (2012)) and probably also reflects compensation for acquiring information about their target companies. These companies often lack established track records or face stern business or organisational challenges.

Banks have significant exposures to private markets. Besides subscription credit lines to funds (see Box), the main connection stems from PE transactions, particularly LBOs, which are funded largely with leveraged loans. Banks typically coordinate the origination of these loans and finance a share of them, maintaining a meaningful exposure until they ultimately offload most of it.7 Banks' involvement then becomes indirect, through the credit they provide to entities such as hedge funds that invest in the ultimate buyers of leveraged loans, such as specialty funds and collateralised loan obligations.

Private markets, cyclicality and monetary policy

Studies indicate that private markets can benefit economic growth. Investors in these markets have long horizons and can tolerate temporary underperformance, thus helping more innovative firms reach maturity. Even during recessions, firms backed by private equity have better access to funding and can engage in capital investment. And in case of financial distress, AAMs contribute to a swifter resolution.8

Against this backdrop, we gather preliminary evidence on two policy-relevant issues worth exploring: the procyclicality of private markets and their response to monetary policy. The purpose is less to provide definitive answers than to motivate research. The empirical analysis that follows focuses on the United States, where the depth of financial markets allows us to obtain reliable price-based measures of risk profiles for private funds, despite the lack of detailed information on the underlying portfolios.9

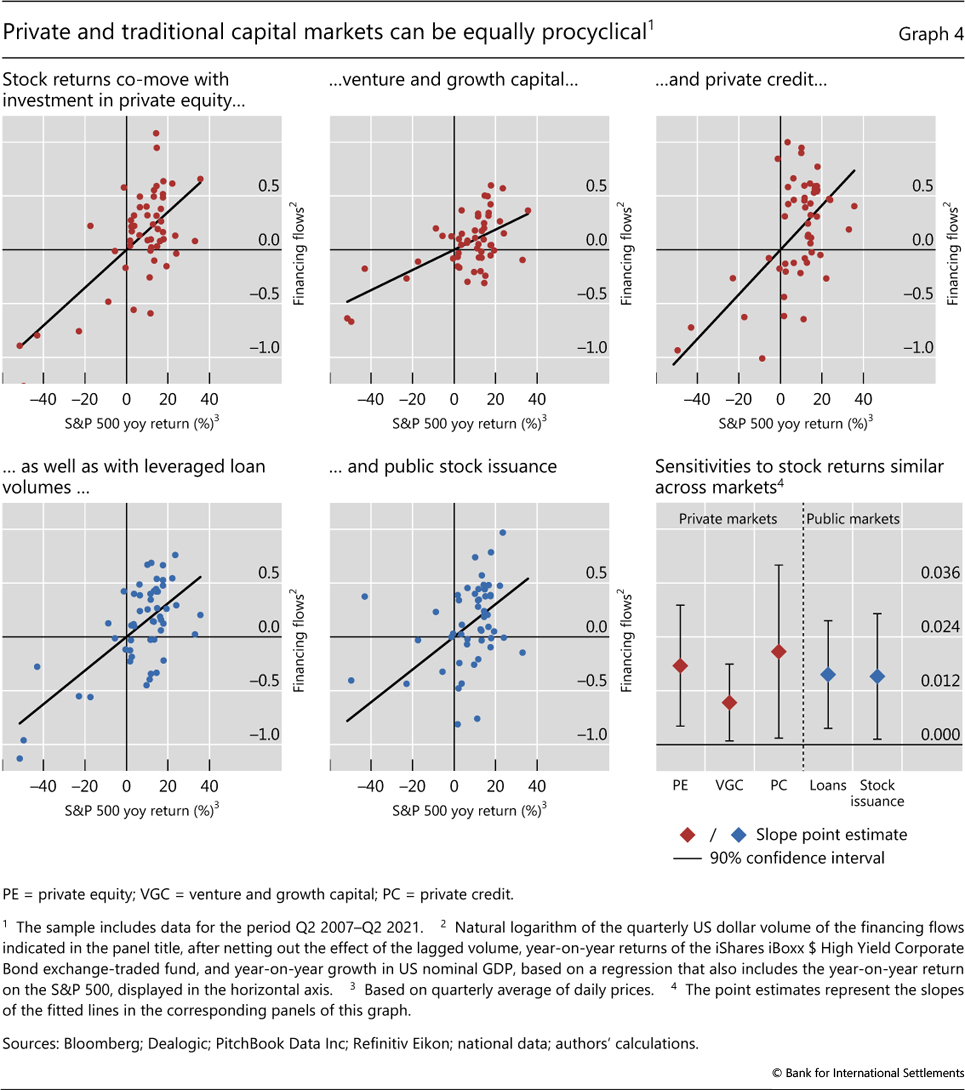

While private markets feature final investors with long horizons, they appear every bit as procyclical as public markets. Capital deployment in PE, VGC and PC is positively correlated with stock market returns, ie more transactions are completed in bullish times (Graph 4, upper panels). In fact, the sensitivity of private market investment to stock market returns is almost identical to those of leveraged loans and equity public offerings, suggesting that a common factor drives all of them (lower panels). Academic studies connect increases in certain private market activities, chiefly LBOs, to the lower risk premia that accompany periods of high stock returns. These lower risk premia raise the present value of the future efficiency gains from corporate restructuring. Relatedly, some of these transactions require bridge financing or high-yield bond issuance, which are themselves procyclical.10

More generally, leverage can contribute to procyclicality. Fund managers can support more debt when their net asset value rises, thus expanding their balance sheets. Conversely, when this value falls in a downturn, they may need to cut their holdings in order to keep leverage within acceptable limits. The propensity to take leverage can vary across markets and investment vehicles. For instance, business development companies (BDCs), a type of private credit fund that can be bought by retail investors, can incur debt up to twice their net assets. This limit is substantially higher than for mutual funds, whose debt cannot exceed one half of net assets.

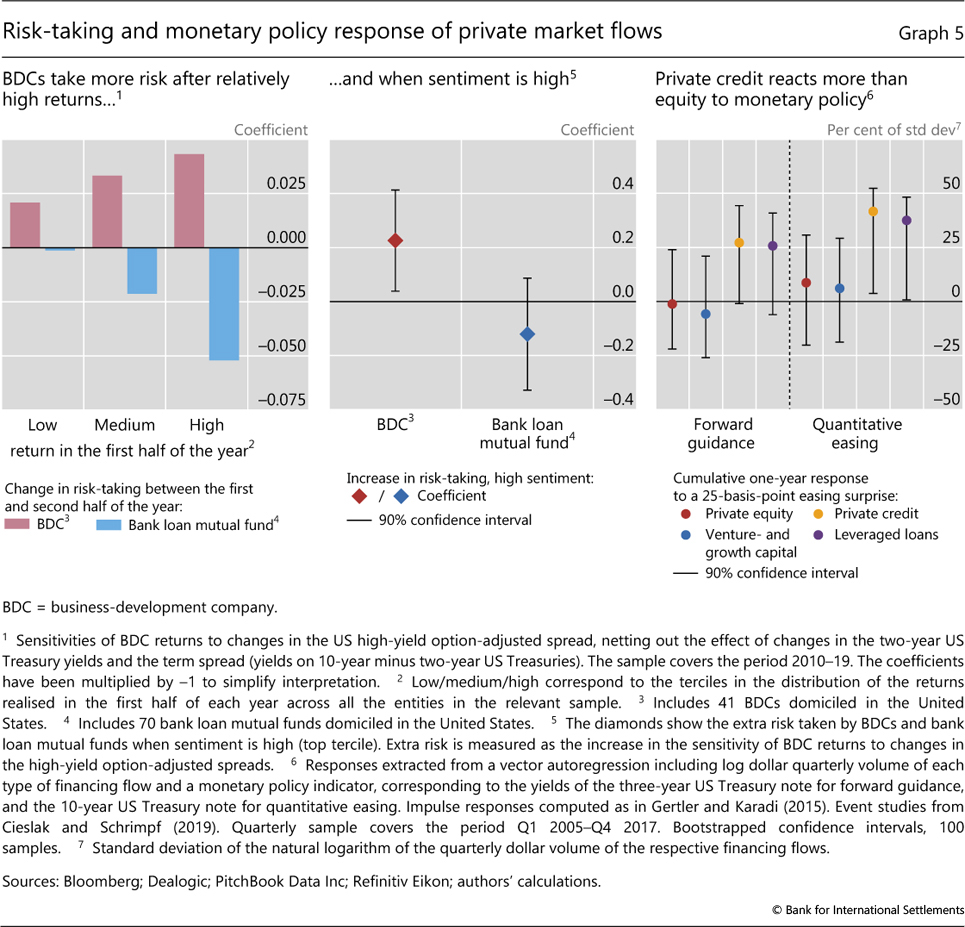

The effect of rising net asset values on risk-taking differs starkly between public and private market funds that invest in credit. In public markets, mutual fund managers that outperform their peers in the first half of the year take less risk in the rest of the year (Graph 5, left-hand panel, blue bars). They do so to mitigate the risk of large losses that would reverse the high returns achieved early on. Obtaining relatively high returns in the full calendar year is key for fund managers to maximise future inflows and fee income (Kempf et al (2009)). In private credit, however, the closed-end nature of investment vehicles eliminates flow-related incentives and drives managers to exploit the higher risk-taking capacity that comes on the back of outperformance. That is, rising net asset values beget risk-taking capacity. Consistent with this, BDCs tend to increase their exposure to credit risk after achieving relatively high returns early in the year, exactly contrary to what mutual funds invested in leveraged loans do (red bars).11

Search for yield characterises private markets, especially PC, on both the investor and manager side. Some of the largest investors, including pension funds, have explicit return targets and are thus attracted by the high coupons that prevail in private credit, exceeding 10% per year. Similarly attractive are rate floors that shield investors from falling rates. On the managers' side, BDCs appear to search for yield: their returns become more sensitive to changes in credit risk at times of strong market sentiment, ie when markets are buoyant and credit spreads compressed. This effect is somewhat stronger than in the case of actively managed mutual funds investing in leveraged loans (Graph 5, centre panel).

Monetary policy affects the real economy partly through credit availability. Thus, given the growing role of private markets as a financing source, it is useful to gauge how sensitive their activities might be to monetary policy surprises. We compute the cumulative response, within a year, of private financing flows to unexpected changes in forward guidance (FG) and quantitative easing (QE), two key post-GFC monetary policy tools (Graph 5, right-hand panel).12 The responses appear to vary across funds with different specialisations. Funds focused on equity investments (PE and VGC) show minimal reaction to FG and QE news. On the other hand, PC funds appear more sensitive to both measures of policy surprises, on a par with the response of leveraged loans.

Conclusions

Private markets have become an important financing channel for the real economy, especially in North America and Europe. They also appear significant in EMEs, where their yearly transactions compare in volume with banks' syndicated loans. In Asia, the dominant private market activity is venture and growth capital, which tends to be most geared to fostering innovation. Private capital is typically deployed through closed-end funds with long-term commitments, thus limiting liquidity transformation. For the most part, this insulates fund managers from short-term pressures, facilitating investment in innovative companies or mature companies in need of restructuring. An investor base of highly sophisticated and professional investors, together with the limited liquidity mismatches, adds to the resilience of this type of funding.

In this feature we focus on two traditional issues that concern policymakers: procyclicality and the response of financing flows to monetary policy. We find that private market activities seem to exhibit relatively high procyclicality in risk-taking. This is possibly linked to leverage and search for yield, despite the long horizons of investors. Furthermore, the effectiveness of monetary policy appears to vary according to the type of fund, with funds specialised in equity investments showing minimal response, but those involved in private credit reacting more strongly. These are preliminary answers that invite further research, not least to monitor possible emerging vulnerabilities in this growing corner of the financial markets.

References

Agarwal, V and N Naik (2004): "Risks and portfolio decisions involving hedge funds", Review of Financial Studies, vol 17, no 1, pp 63–98.

Aramonte, S (2020): "Private credit: recent developments and long-term trends", BIS Quarterly Review, March.

Aramonte, S, S Lee and V Stebunovs (2019): "Risk taking and low longer-term interest rates: evidence from the U.S. syndicated term loan market", Journal of Banking and Finance, forthcoming.

Axelson, U, T Jenkinson, P Strömberg and M Weisbach (2013): "Borrow cheap, buy high? The determinants of leverage and pricing in buyouts", Journal of Finance, vol 68, no 6, pp 2223–67.

Bernstein, S, J Lerner and F Mezzanotti (2019): "Private equity and financial fragility during the crisis", Review of Financial Studies, vol 32, no 4, pp 1309–73.

Berger, A, A Kashyap, J Scalise, M Gertler and B Friedman (1995): "The transformation of the US banking industry: what a long, strange trip it's been", Brookings Papers on Economic Activity, vol 1995, no 2, pp 55–218.

Borio, C (1990): "Banks' involvement in highly leveraged transactions", BIS Economic Papers, no 28.

Boucly, Q, D Sraer and D Thesmar (2011): "Growth LBOs", Journal of Financial Economics, vol 102, pp 432–53.

Cerutti, E and S Claessens (2017): "The great cross-border bank deleveraging: supply constraints and intra-group frictions", Review of Finance, vol 21, no 1, pp 201–36.

Cieslak, A and A Schrimpf (2019): "Non-monetary news in central bank communication", Journal of International Economics, no 118, pp 293–315.

Davydiuk, T, T Marchuk and S Rosen (2020): "Direct lenders in the US middle market", working paper.

Doidge, C, A Karolyi and R Stulz (2017): "The US listing gap", Journal of Financial Economics, vol 123, no 3, pp 464–87.

Franzoni, F, E Nowak and L Phalippou (2012): "Private equity performance and liquidity risk", Journal of Finance, vol 67, no 6, pp 2341–73.

Gertler, M and P Karadi (2015): "Monetary policy surprises, credit costs, and economic activity", American Economic Journal: Macroeconomics, vol 7, no 1, pp 44–76.

Haddad, V, E Loualiche and M Plosser (2017): "Buyout activity: The impact of aggregate discount rates", Journal of Finance, vol 72, no 1, pp 371–414.

Hotchkiss, E, D Smith and P Strömberg (2021): "Private equity and the resolution of financial distress", Review of Corporate Finance Studies, forthcoming.

Kempf, A, S Ruenzi and T Thiele (2009): "Employment risk, compensation incentives, and managerial risk taking: Evidence from the mutual fund industry", Journal of Financial Economics, vol 92, no 1, pp 92–108.

Kortum, S and J Lerner (2000): "Assessing the contribution of venture capital to innovation", RAND Journal of Economics, vol 31, no 4, pp 674–92.

Samila, S and O Sorenson (2011): "Venture capital, entrepreneurship, and economic growth", Review of Economics and Statistics, vol 93, no 1, pp 338–49.

Tian, X and T Wang (2014): "Tolerance for failure and corporate innovation", Review of Financial Studies, vol 27, no 1, pp 211–55.

1 The authors thank Stefan Avdjiev, Claudio Borio, John Caparusso, Stijn Claessens, Egemen Eren, Jon Frost, Benoît Mojon, Andreas Schrimpf, Nikola Tarashev and Karamfil Todorov for helpful comments and discussions, Giulio Cornelli and Logan Casey for excellent research assistance, and Branimir Gruić and Jakub Demski for help with loan issuance data. The views expressed in this article are those of the authors and do not necessarily reflect those of the Bank for International Settlements.

2 For the transformation of the US banking system, see Berger et al (1995), and references therein. For changes in global banking after the GFC see eg Cerutti and Claessens (2017). For changes in the US stock markets, see Doidge et al (2017).

3 Private market funds with a regional focus raise capital both locally and internationally. To the extent that the capital deployed was committed by domestic limited partners, they will not show as FDI. If the funds have been committed by non-residents, there will be some overlap between FDI and private market flows. As portfolio flows are routed through public markets, their overlap with private market flows is less of an issue.

4 IPOs have traditionally been a way for early investors to exit their investment in private companies. The share of IPOs sponsored by private market funds, mainly PE or VC firms, has risen over time: from 46% during 1990–98 to 80% in 2019–21. This also speaks to the growing importance of private markets in early-stage corporate financing.

5 Growth capital transactions typically target private firms with high growth potential that are mature enough to go public through an IPO. IPOs have stagnated: in 2020, IPO proceeds were about the same as in 1999 in nominal terms, and the number of firms going public was about a fourth (see "IPO Statistics from 2020 and earlier years"). As a result, listed companies are now older and more mature (see eg Doidge et al (2017)).

6 Regulatory treatments can vary. For instance, certain US investment vehicles accessible to retail investors, known as business development companies, are subject to provisions similar to those applicable to mutual funds.

7 See Aramonte et al (2019) for evidence based on US supervisory data.

8 See: Boucly et al (2011) for the impact of LBOs on corporate profitability, growth and capital expenditures, Tian and Wang (2014) for the effect of investor tolerance of short-run underperformance by innovative firms; Bernstein et al (2019) for funding patterns of PE-backed firms during the GFC; Hotchkiss et al (2021) for the resolution of financial distress; Kortum and Lerner (2000) and Samila and Sorenson (2011) for the long-term benefits of venture capital for innovation and economic growth; and Davydiuk et al (2020) for the role of BDCs in offsetting reductions in bank financing.

9 This practice is common in academic studies of intermediaries with opaque portfolios (eg Agarwal and Naik (2004)).

10 For the role of the equity premium, see Haddad et al (2017). The fall in the equity risk premium reduces the expected return of common stock, an alternative asset allocation option for AAMs. This increases the relative value of illiquid investments with higher expected returns, such as buyouts. For the role of funding costs, see Axelson et al (2013).

11 BDCs can fine-tune their risk exposure in several ways. While they invest mainly in loans, which are very illiquid, they also hold other securities, such as preferred stocks, that can be traded more easily. In addition, some BDCs disclose that they can use derivatives to hedge credit risk.

12 We do not include reactions to unexpected changes in policy rates because they were few over the sample period we study.