Playing it safe: global systemically important banks after the crisis

Post-crisis reforms aim to mitigate the systemic risks that arise from global systemically important banks (G-SIBs). Based on our estimates of G- SIBs' probability of distress, we find that their resilience has improved in recent years on the back of higher capital ratios. Furthermore, by benchmarking G-SIBs' balance sheet adjustments against those of other major banks, we show that these adjustments accord with the incentives set by the post-crisis regulatory framework. This suggests that the systemic importance of G-SIBs has declined in recent years.1

JEL classification: G21, G28, C25.

During the Great Financial Crisis (GFC), the distress of large, complex and interconnected financial institutions undermined financial stability. Post- crisis financial reforms aim to reduce the systemic risk of these global systemically important banks (G-SIBs). They seek to increase the banks' resilience or, in other words, make them less likely to fail. And, they encourage these banks to reduce their systemic importance or, roughly speaking, soften the impact on the financial system if they were to face distress. Two key elements of these reforms - henceforth jointly referred to as the "G-SIB framework" - are the assessment methodology to identify G-SIBs and the capital surcharges imposed on these banks.

This special feature assesses whether G-SIBs' resilience and systemic importance have evolved in line with regulatory objectives since the GFC. We start by reviewing trends in resilience. Specifically, we estimate G-SIBs' probability of distress (PD) based on bank-specific and macroeconomic risk factors. Our estimates point to a decline in G-SIBs' PDs on the back of higher capital ratios and reduced funding risk after the GFC. Weak profitability, however, has hindered further improvements in recent years.

While the G-SIB framework has helped raise banks' capital ratios, it may also have reduced their PDs by encouraging changes in their funding mix. To test this, we exploit national differences in the framework's implementation. We find that the wholesale funding ratio of US G-SIBs has fallen further than that of EU G-SIBs. This is consistent with the US regulation which, unlike the EU's, incorporates this ratio in the calculation of capital surcharges.

Key takeaways

- The risk posed by global systemically important banks (G-SIBs) has declined in line with the incentives set by the post-crisis regulatory framework.

- Higher capital ratios and a shift towards more stable sources of funding have strengthened G-SIBs' resilience.

- G-SIBs' systemic importance has fallen in recent years relative to that of other banks.

Turning to the framework's second objective, we show that G-SIBs' systemic importance, as captured by the G-SIB assessment methodology, has on average been declining since it was put in place. This decline reflects a downward trend in regulatory indicators for bank size, interconnectedness and complexity.

When G-SIBs' post-crisis balance sheet adjustments are benchmarked against those of non-G-SIBs, several other trends emerge that are consistent with the incentives generated by the framework. For one, while G-SIBs have been expanding more slowly than non-G-SIBs since the GFC, the difference has widened after the introduction of the G-SIB framework. Relative to their peers, G-SIBs have also cut back on their securities holdings and reduced their reliance on interbank deposits after the regulatory change. Lending has evolved similarly for G-SIBs and other banks.

Further reading

In the following section, we present the G-SIB framework, ie the assessment methodology and its approach to strengthening G-SIB resilience. We then estimate the PDs of major banks to analyse structural trends and drivers of bank resilience. Next, we look at changes in banks' systemic importance through the lens of the G-SIB framework. To tease out the role of the G-SIB assessment and capital surcharges in driving these changes, we contrast G-SIBs' post- crisis adjustments with those of non-G-SIBs. The final section concludes.

G-SIB assessment methodology and capital surcharges

First published by the Basel Committee on Banking Supervision (BCBS) in 2011, the G-SIB framework is designed to reduce G-SIBs' probability of failure (BCBS (2018)). To that end, it sets out a methodology to identify G-SIBs, and defines capital surcharges that increase in step with a bank's approximated systemic importance. While this feature focuses on the impact of the framework, the new regulatory landscape for G-SIBs also provides for more intensive supervision as well as more effective resolution regimes (FSB (2013)).

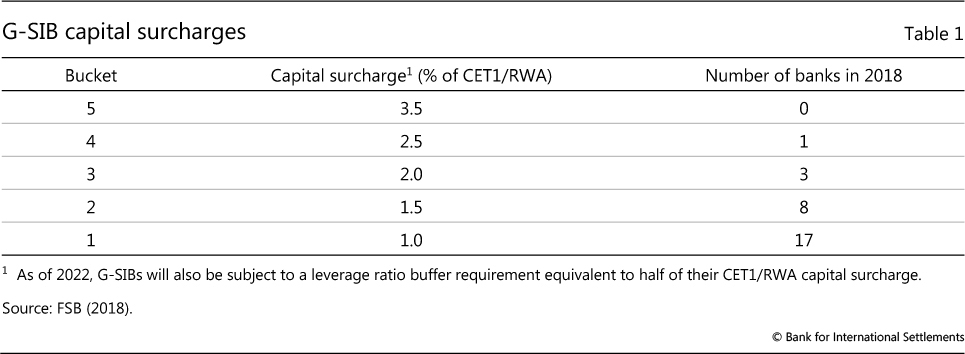

The assessment methodology seeks to measure banks' relative systemic importance. The measurement is based on indicators of bank size, interconnectedness, the substitutability of their services, cross-border lending and funding, and the complexity of their portfolios. Each indicator is normalised by dividing the bank's indicator value by the sum of the indicator values across the largest global banks, the so-called assessment sample. A bank's systemic importance proxy - its G-SIB score - is equal to the weighted average of its normalised indicators. Banks above a score cutoff are designated as G-SIBs.2 G-SIB assessment results are published annually. In the most recent result, 29 banks were designated as G-SIBs. The assessment sample currently comprises 76 banks, with a total size of more than €73 trillion at end-2017.3

The G-SIB framework seeks to enhance bank resilience by imposing varying capital surcharges. The surcharge (or the higher loss absorbency requirement) is expressed as a ratio of Common Equity Tier 1 capital to risk-weighted assets (CET1 ratio). It currently varies between 1 and 3.5%, depending on the G- SIB score. Banks with a higher G-SIB score are allocated to a higher "bucket" and face a higher capital surcharge (Table 1). Conceptually, this is designed to reduce each G-SIB's potential impact of failure on the financial system to that posed by the non-G-SIB with the highest score (BCBS (2011), Passmore and von Hafften (2019)). In turn, since capital is costly, the surcharges encourage G-SIBs to reduce their systemic importance.

Bank resilience: trends and drivers

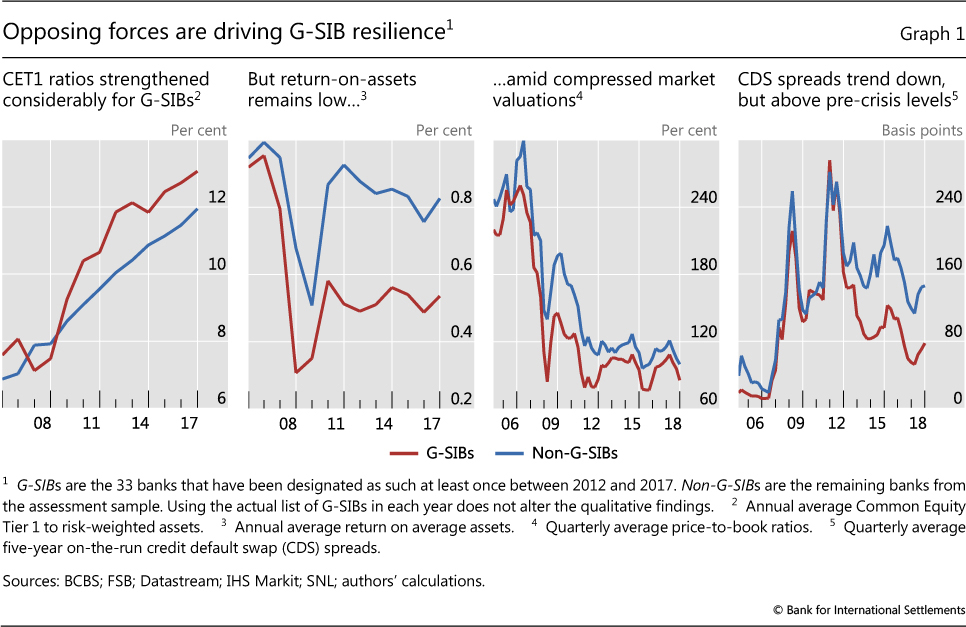

Assessing how banks' resilience has evolved in recent years must take account of some opposing forces. On the one hand, the capital ratios of both G- SIBs and non-G-SIBs have trended up (Graph 1, first panel), suggesting a substantial improvement in resilience. On the other hand, profitability has yet to recover for many G-SIBs (Graph 1, second panel), which weighs on their ability to strengthen or even maintain capital buffers in the medium term. Indeed, equity investors seem to be sceptical about the odds of such a recovery in the near future, as reflected in the low market valuations of many banks (Graph 1, third panel; BIS (2019)).

Relying only on market-based measures to gauge bank resilience falls short of providing a comprehensive assessment. For instance, credit default swap (CDS) spreads have generally trended down in recent years, while remaining above their pre-crisis levels (Graph 1, fourth panel). But market-based measures can give ambiguous signals regarding resilience for the following reasons. For one, these measures tend to be prone to swings in investor risk appetite, with limited ability to predict future distress (Borio and Drehmann (2009)). CDS spreads, for instance, reached long-term lows in the run-up to the GFC - clearly a misleading benchmark. Second, post-crisis regulation may have shifted the relationship between some of these measures and bank resilience. Regulatory reforms to improve the resolvability of major banks have, for example, helped to weaken market expectations for public sector support, thus redistributing risks to bank creditors.4 This would widen CDS spreads, even in the absence of any change in bank resilience.

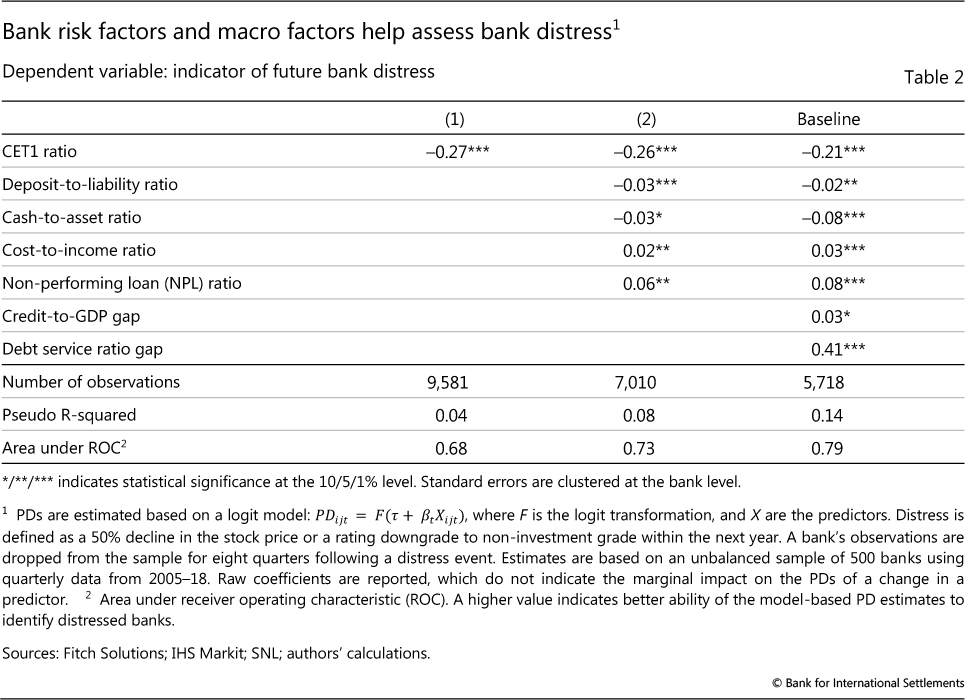

To apply a more structured approach to assessing bank resilience, we estimate banks' PD based on a parsimonious logit model. The model combines market indicators of distress, bank risk factors and indicators of macroeconomic conditions.

We define bank distress as a 50% decline in the stock price or a rating downgrade to non-investment grade within the next year.5 This choice is motivated by the observation that market prices are good coincident indicators of distress, despite typically having limited longer-term predictive power. For bank risk factors, we include measures of bank capitalisation, asset quality, efficiency and liquidity (as listed in Table 2). As macro predictors, we consider the credit-to-GDP gap and the debt service ratio gap as early warning indicators of overheating in credit markets (Aldasoro et al (2018)). Our analysis covers an (unbalanced) sample of around 500 large banks globally using quarterly data from 2005 to 2018. Table 2 presents estimates of the baseline model (third column), which we select based on comparing alternative specifications in terms of their goodness of fit and predictive ability.6 While we use this model for the estimates that follow, they are robust to alternative specifications, as well as to changing the definition of distress or the forecasting horizon.7

A model-based approach to measuring resilience has several advantages. For one, the model combines various determinants of bank resilience, which helps assess the joint effect of these determinants. This is especially useful when potential drivers of resilience, as in our case, point in opposite directions. In addition, the regression estimates allow us to tease out the relative contribution of specific drivers of PDs. For instance, the model provides an estimate of the decline in PDs due to an increase in capital ratios, controlling for changes in, say, profitability. In turn, this helps identify the direct effect of regulatory reforms on resilience.

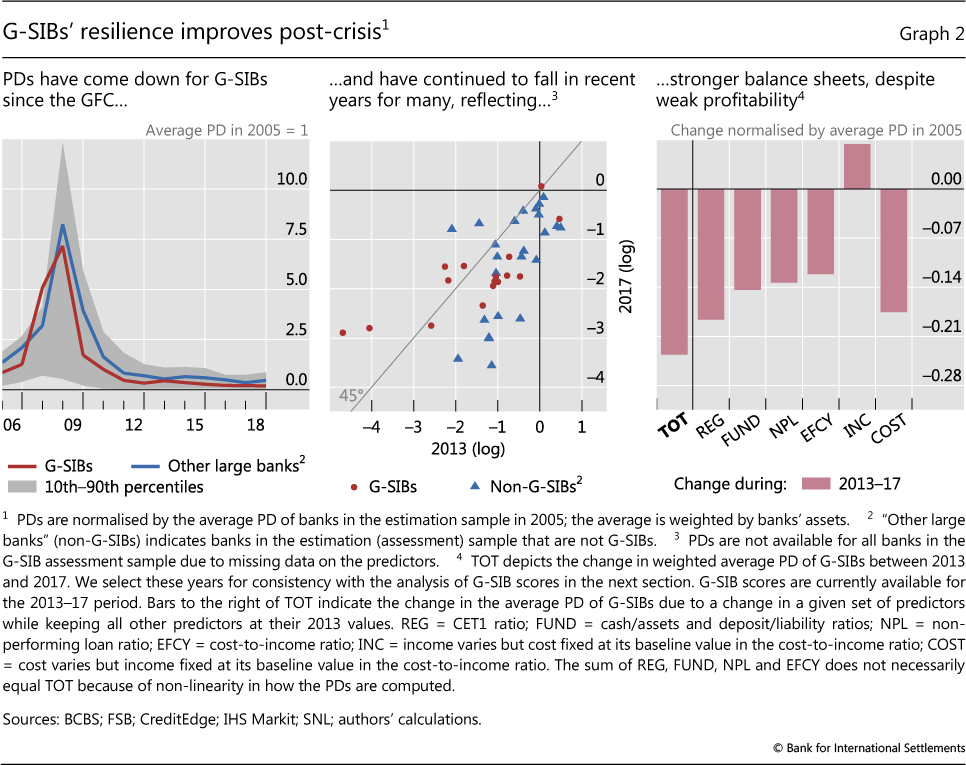

Our PD estimates point to an improvement in G-SIBs' resilience over time and relative to that of other banks. G-SIBs' estimated PDs have, on average, declined significantly relative to the aftermath of the GFC and also relative to their pre-crisis levels. And, they have continued to decline in recent years (Graph 2, left-hand and centre panels). Furthermore, while PDs have come down for both G-SIBs and non-G- SIBs, estimated PDs are lower for G-SIBs, consistent with the framework's aim of bolstering the resilience of systemically important banks.

By decomposing the contribution of bank-level predictors to the decline in G-SIBs' PD estimates, we reveal the opposing forces at work (Graph 2, right-hand panel). PDs have declined on average because of improvements in G-SIBs' capital buffers and the reduced risks of funding disruptions since the GFC, a trend that has continued in recent years. At the same time, cost-to-income ratios have declined only modestly, with lower revenues offsetting the effect of cost savings.

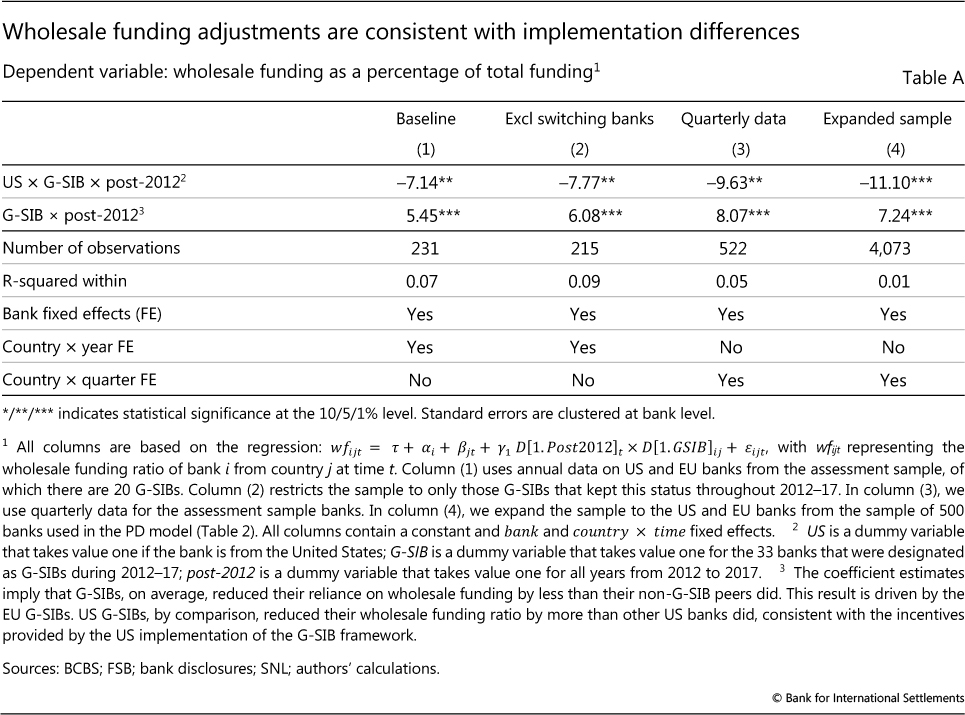

Our results indicate that increased capital ratios have been a key factor in improving resilience. However, the framework could impact PDs through other channels as well, such as through its effect on the funding mix. In particular, differences in the implementation of the G-SIB framework in the United States and the European Union tally with observed changes in banks' reliance on wholesale funding (see box), a key source of funding risk and driver of PDs during the GFC (Passmore and von Hafften (2019)).

Exploiting transatlantic differences to tease out the role of the G-SIB framework

Confounding factors complicate the task of identifying the drivers of G-SIBs' post-crisis adjustments. These factors include concurrent regulatory reforms, macroeconomic policies, and structural changes in financial markets. One way to overcome this obstacle is to ask whether the effects of the G-SIB framework varied according to differences in the way it was implemented in different jurisdictions. We make use of the fact that the European Union's implementation is based on the BCBS assessment methodology, whereas the United States uses two distinct methods to calculate capital surcharges (BCBS (2014, 2016)). The first one is identical to the BCBS methodology, while the second, among other differences, takes into account G-SIBs' reliance on short-term wholesale funding. US banks are subject to the higher of the two surcharges, which has been the second one to date. As such, we conjecture that US G-SIBs have had stronger incentives than their EU peers to reduce their reliance on wholesale funding.

To test our hypothesis, we set up a regression that identifies trends within US G-SIBs relative to (i) their pre-2012 trends; (ii) EU G-SIBs; and (iii) US and EU non-G-SIBs. We restrict the sample to only the US and EU banks from the assessment sample (34 in total). These large internationally active banks are subject to similar regulatory requirements, suggesting that the non-G-SIBs in the sample represent a suitable control group in order to identify the effect of differences in the G-SIB assessment methodologies across the Atlantic.

The results in Table A support our hypothesis. US G-SIBs reduced their short-term wholesale funding after 2012 by roughly 7 percentage points more than the EU G-SIBs did (first row, column (1)). This result is robust to excluding G-SIBs designated after 2012 ("switching banks", column (2)), using quarterly instead of annual data for the assessment sample (column (3)) or using an expanded sample of banks (column (4)).

Systemic importance through the G-SIB framework's lens

Having established that G-SIBs have become more resilient, we now ask how their systemic importance has evolved. To do so, we rely on the evolution of the G-SIB scores for several reasons. First, the scores are designed to capture many dimensions of banks' systemic footprint, based on the lessons drawn from the GFC and other crises. Second, since the score determines banks' capital surcharges, it is a natural starting point for assessing the G-SIB framework's impact on banks' balance sheet adjustments.

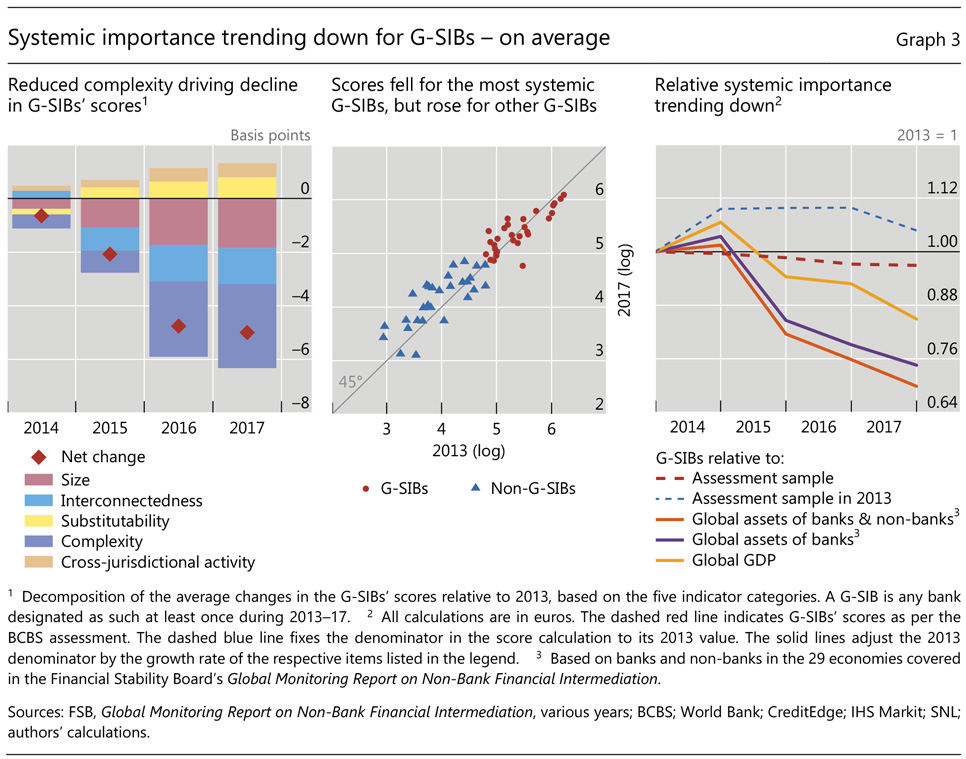

Overall, G-SIBs' average score declined relative to that of non-G-SIBs in several - but not all - dimensions of systemic importance (Graph 3, left-hand panel). First, G-SIBs grew more slowly than non-G-SIBs. Second, G-SIBs' regulatory proxies for complexity diminished due to a decline in their over-the-counter derivatives books and securities holdings - both in absolute terms and relative to those of non-G-SIBs. Third, proxies for G-SIBs' interconnectedness with the financial system declined, driven mainly by their falling share of intra-financial liabilities.

An opposing force, however, is an increase in G-SIBs' relative contribution to cross-jurisdictional activity.8 Since the scores are based on the relative shares of banks in the assessment sample, the mirror image of reduced scores for G-SIBs is an increase in the average score of non-G-SIBs.

Individual bank results provide a more nuanced view on how G-SIBs' scores have evolved since the introduction of the framework (Graph 3, centre panel). A number of G-SIBs did see a rise in scores, reflecting, among others, regional differences in financial sector growth (BCBS (2019)). Yet scores have typically come down for the banks with the highest ones in 2013, consistent with the incentives provided by imposing higher surcharges on these banks (Table 1).

One drawback of the G-SIB assessment methodology is that trends affecting the entire assessment sample can remain hidden below the supervisory radar screen. For example, if each bank were to double each of its indicator values, the scores would be unchanged, even though the systemic importance of the banks in the assessment sample relative to the broader economy would undoubtedly increase.9

We thus assess how G-SIBs' scores have evolved relative to alternative benchmarks. We start by comparing the evolution of G-SIBs' scores against those of the assessment sample in 2013.10 Using this conservative yardstick, we find that G-SIBs' systemic importance rose initially, but has stabilised since 2014 and, more recently, fallen (Graph 3, right-hand panel). Broader trends in economic or financial activity provide alternative benchmarks. We therefore adjust the 2013 reference values by the annual growth rate of global GDP, of the global banking sector's assets, and of the global financial assets of banks and non-banks, respectively. Each of these measures points to a downward trend in the relative systemic importance of G-SIBs (Graph 3, right-hand panel).11 This conclusion is also supported by popular proxies for systemic risks, such as SRISK (Brownlees and Engle (2016)), which declined by roughly 17% for G-SIBs from 2013 to 2017.

These trends may reflect a broader cyclical decline in G-SIBs' risk-taking, and not necessarily be driven by introduction of the G-SIB assessment methodology and the phase-in of the capital surcharges. Indeed, Adrian et al (2018) highlight that banks' balance sheet management has undergone profound changes since the GFC. This reflects the need of many major banks to bring leverage - which had spiked in the run-up to the crisis - back to sustainable levels. On top of that, broader challenges to banks' profitability, such as low interest rates and new non-bank competitors, required decisive changes to banks' business models. Teasing out the effect of regulatory reforms among these other business developments is a daunting task.

To make some progress in this regard, we look for shifts in G-SIBs' balance sheet adjustments relative to those of non-G-SIBs. This analysis requires both pre- and post-crisis data. G-SIB scores, however, have been available only since 2013. Thus, we use banks' balance sheet disclosures to proxy some components of the score.

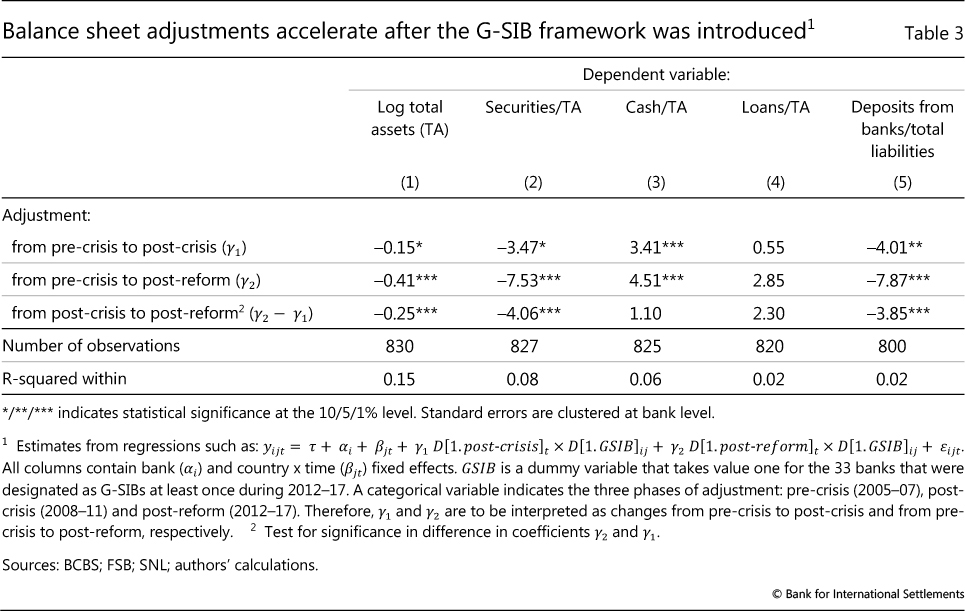

We adopt a difference-in-difference approach, distinguishing between three phases: (i) the run-up to the GFC, 2005-07 ("pre-crisis"); (ii) the GFC and its immediate aftermath, 2008-11 ("post-crisis"); and (iii) the years since the framework's introduction, 2012-17 ("post-reform"). This approach lets us assess shifts in G-SIBs' adjustments relative to those of non-G-SIBs from one phase to another (Table 3). In particular, shifts in banks' relative adjustments from the post-crisis to the post-reform phase help us assess the role of the framework.

In line with previous research (Violon et al (2017)), we find that several adjustments accord with the incentives that arise from the framework.

First, G-SIBs had already been growing more slowly than other banks in the aftermath of the GFC (Table 3, first row, column (1)). Yet the wedge widened after the introduction of the framework (third row, column (1)).

Second, relative to their peers, G-SIBs cut their securities holdings by more post-crisis (first row, column (2)). Again, the difference in G-SIBs' adjustment became more pronounced after the framework was introduced (third row, column (2)). To examine how G-SIBs rebalanced their asset mix, we perform the same comparative analysis for banks' cash holdings and loans (as a share of total assets). We find that G-SIBs raised their cash holdings by relatively more post-crisis (first row, column (3)), but no additional effect arises after the regulatory reform (third row, column (3)). For loans, the estimates do not suggest that G-SIBs reduced their lending by more than their peers did since the GFC or after the introduction of the reform (column (4)).

Third, G-SIBs reduced the share of uncollateralised borrowing from banks in their overall funding mix relative to non-G-SIBs. This development started off post-crisis (first row, column (5)), but again became more pronounced after the framework was put in place (column (5), third row). This result tallies with the overall reduction in G-SIBs' interconnectedness scores, which encompass intra-financial liabilities (Graph 3, left-hand panel).

The above findings are suggestive that the framework has encouraged G-SIBs to reduce their systemic importance. Yet several qualifications remain. One is the effect of confounding factors, such as macroeconomic policies or structural changes in the market environment (Adrian et al (2018)), which could blur the framework's impact.12 Quantitative easing, for example, may have affected G-SIBs' balance sheets differently than it did those of their peers. Another possibility is strategic adjustments by banks along dimensions that help to reduce the G-SIB scores. This could include raising risk-taking along other dimensions that are less constrained by regulation, or by compressing their balance sheets around the end-of-year disclosures (Aldasoro et al (2019), Behn et al (2019)). If this is the case, the systemic importance of G-SIBs might be understated.

Conclusion

This special feature finds that G-SIBs have become more resilient in recent years, thanks to a build-up in capital buffers and a shift to more stable sources of funding. Weak profitability, however, has hindered further improvements. G-SIBs' systemic importance, as approximated by the BCBS assessment methodology, has declined on average over this period, relative to other banks and also the broader financial system. Overall, banks' post-crisis balance sheet adjustments tally with the incentives provided by the G-SIB capital surcharges.

The systemic risk posed by a bank depends on its systemic importance and resilience. Our findings thus point to a general decline in such risks. Post- crisis reforms to establish effective resolution regimes, not covered in this feature, are likely to have further supported this trend. Yet the measurement of systemic risk remains subject to uncertainty despite the contributions of academic research and supervisors. For one, measures of systemic risk may underestimate the impact of complex interlinkages in the banking sector, particularly during episodes of stress (Acemoğlu et al (2015)). Moreover, risks may be migrating outside the traditional banking sector and thus outside the scope of the G-SIB framework.

These considerations call for continued monitoring by supervisors, and highlight the value of strengthened cross-border resolution arrangements (FSB (2015)). They also underscore the benefits of cooperative efforts to gather and analyse detailed information on globally active banks, such as through the International Data Hub (FSB-IMF (2018)).

References

Acemoğlu, D, A Özdağlar and A Tahbaz-Salehi (2015): "Systemic risk and stability in financial networks", American Economic Review, vol 105, no 2, pp 564-608.

Adrian, T, J Kiff and H S Shin (2018): "Liquidity, leverage, and regulation 10 years after the Global Financial Crisis", Annual Review of Financial Economics, vol 10, November, pp 1-24.

Aldasoro, I, C Borio and M Drehmann (2018): "Early warning indicators of banking crises: expanding the family", BIS Quarterly Review, March, pp 29-45.

Aldasoro, I, T Ehlers and E Eren (2019): "Global banks, dollar funding, and regulation", BIS Working Papers, no 708, May.

Bank for International Settlements (2019): Annual Economic Report 2019, Chapter I, June.

Basel Committee on Banking Supervision (2011): Global systemically important banks: assessment methodology and the additional loss absorbency requirement, November.

--- (2014): Regulatory Consistency Assessment Programme (RCAP) Assessment of Basel III regulations - European Union, December.

--- (2016): Regulatory Consistency Assessment Programme (RCAP) Assessment of Basel III G-SIB framework and review of D-SIB framework - United States, June.

--- (2018): Global systemically important banks: revised assessment methodology and the higher loss absorbency requirement, July.

--- (2019): "An examination of initial experience with the global systemically important bank framework", BCBS Working Papers, no 34, February.

Behn, M, G Mangiante, L Parisi and M Wedow (2019): "Behind the scenes of the beauty contest: window dressing and the G-SIB framework", ECB Working Paper Series, no 2298, July.

Betz, F, S Oprică, T Peltonen and P Sarlin (2014): "Predicting distress in European banks", Journal of Banking & Finance, vol 45, pp 225-41.

Borio, C and M Drehmann (2009): "Towards an operational framework for financial stability: 'fuzzy' measurement and its consequences", BIS Working Papers, no 284, June.

Brownlees, C and R Engle (2016): "SRISK: a conditional capital shortfall measure of systemic risk", The Review of Financial Studies, vol 30, no 1, pp 48-79.

Financial Stability Board (2013): Progress and next steps towards ending "too-big-to-fail" (TBTF), report of the FSB to the G20, September.

--- (2015): Principles for cross-border effectiveness of resolution actions, November.

--- (2018): List of global systemically important banks (G-SIBs), November.

Financial Stability Board-International Monetary Fund (2018): The financial crisis and information gaps. Second phase of the G20 data initiative, third progress report, September.

Neuberg, R, P Glassermann, B Kay and S Rajan (2016): "The market-implied probability of European government intervention in distressed banks", Office of Financial Research Working Papers, no 16-10, October.

Passmore, W and A von Hafften (2019): "Are Basel's capital surcharges for global systemically important banks too small?", International Journal of Central Banking, vol 15, no 1, pp 107-56.

Violon, A, D Durant and O Toader (2017): "The impact of the identification of GSIBs on their business model", Bank of France, Débats économiques et financiers, no 33, December.

1 The authors would like to thank Iñaki Aldasoro, Douglas Araujo, Claudio Borio, Stijn Claessens, Dietrich Domanski, Neil Esho, Marc Farag, Eva Hüpkes, Simonetta Iannotti, Benoît Mojon, Goetz von Peter, Fernando Restoy, Christian Schmieder, Verena Seidl, Hyun Song Shin, Costas Stephanou, Előd Takáts, Nikola Tarashev and Philip Wooldridge for helpful comments. Alan Villegas provided outstanding research assistance. The views expressed in this article are those of the authors and do not necessarily reflect those of the Bank for International Settlements.

2 Scope is allowed in the framework for supervisors to override G-SIB designations using their supervisory judgment (BCBS (2018)).

3 Size is measured in terms of the banks' leverage ratio exposure measure, which comprises on-balance sheet exposures (such as loans), derivative exposures, exposures from securities financing transactions and off-balance sheet items (eg standby letters of credit).

4 In line with this interpretation, credit rating agencies have lowered their estimates of the likelihood of sovereign support for many banks in recent years. Furthermore, contract terms for CDS have been adjusted post-crisis to cover losses from government intervention and bail-in events (Neuberg et al (2016)).

5 Based on this definition, about 2.5% of the bank-quarter observations indicate distress, three fifths of which occurred during the GFC. While failures and resolutions would provide a more severe measure of distress, such events are too rare in the case of large banks to support a meaningful PD model.

6 The area under ROC of the baseline model, for instance, equals 79%. The classification accuracy - that is, the rate at which the model predicts the correct outcome - is 71%. These goodness-of-fit statistics are in line with comparable models in the literature (eg Betz et al (2014)).

7 Alternative definitions of distress include a decline in stock prices by at least 40% over the next four quarters or a decline of 30% within the next quarter. These alternative definitions help ensure that the model is robust, in particular, to noise in stock prices.

8 The observed increase in G-SIBs' scores in the substitutability category is due to the imposition of a maximum score ("cap") in that category. Excluding the effect of the cap would reduce G-SIBs' substitutability-related scores. In its next review of the G-SIB assessment methodology, the BCBS will consider alternatives to the application of the cap (BCBS (2018)).

9 Since the scores are based on banks' relative shares, they - in principle - always add up to 100%. Technically, year-on-year differences in scores do not net out exactly across the banks in the assessment sample due to the cap on scores in the substitutability category.

10 This comparison is based on normalising a bank's indicator by the sum of all the banks' indicator values in 2013, the first year of observation.

11 One driver of this result is the fact that, between 2013 and 2017, the global assets of banks and non-banks - in the 29 economies covered in the Financial Stability Board's Global Monitoring Report on Non-Bank Financial Intermediation - grew at an average annual rate of more than 10%. By comparison, G-SIBs' total assets grew by around 5% annually.

12 Another confounding factor is the anticipation effect, ie banks may frontload their response to regulation before it enters into force.