Beyond LIBOR: a primer on the new benchmark rates

The transition from a reference rate regime centred on interbank offered rates (IBORs) to one based on a new set of overnight risk-free rates (RFRs) is an important paradigm shift for markets. This special feature provides an overview of RFR benchmarks, and compares some of their key characteristics with those of existing benchmarks. While the new RFRs can serve as robust and credible overnight reference rates rooted in transactions in liquid markets, they do so at the expense of not capturing banks' marginal term funding costs. Hence, there is a possibility that, under the new normal, multiple rates may coexist, fulfilling different purposes and market needs.

JEL classification: D47, E43, G21, G23.1

For decades, IBORs have been at the core of the financial system's plumbing, providing a reference for the pricing of a wide array of financial contracts. These include contracts for derivatives, loans and securities. As of mid-2018, about $400 trillion worth of financial contracts referenced London interbank offered rates (LIBORs) in one of the major currencies.2

There is currently considerable momentum for transitioning away from LIBOR benchmarks.3 A major impetus for reform comes from the need to strengthen market integrity following cases of misconduct involving banks' LIBOR submissions. To protect them against manipulation, the new (or reformed) benchmark rates would ideally be grounded in actual transactions and liquid markets rather than be derived from a poll of selected banks. But the significant decline in activity in interbank deposit markets, together with structural changes in the money market landscape since the Great Financial Crisis (GFC), has complicated the search for alternatives. The reform process constitutes a major intervention for both industry and regulators, as it is akin to surgery on the pumping heart of the financial system.

Key takeaways

- The new risk-free rates (RFRs) provide for robust and credible overnight reference rates, well suited for many purposes and market needs. In the future, cash and derivatives markets are expected to migrate to the RFRs as the main set of benchmarks. The transition will be most challenging for cash markets because of the bespoke nature of contracts and structurally tighter links to interbank offered rates.

- To manage asset-liability risk, financial intermediaries may continue to need a set of benchmarks that provide a close match to their marginal funding costs - a feature that RFRs or term rates linked to them are unlikely to deliver. This may call for RFRs to be complemented with some form of credit-sensitive benchmark, an approach already undertaken in some jurisdictions.

- It is possible that, ultimately, a number of different benchmark formats will coexist, fulfilling a variety of purposes and market needs. The jury is still out on whether any resulting market segmentation would lead to material inefficiencies or could even be optimal under the new normal.

In the major currency areas, authorities have already started publishing rates intended to eventually replace (or complement) the IBOR benchmarks. The initial focus has been on introducing credible, transaction-based overnight (O/N) RFRs anchored in sufficiently liquid money markets. Currently, cash and derivatives markets linked to the new RFRs are still in their infancy, but are gradually gaining in liquidity. In addition, a number of jurisdictions in which it was deemed feasible to reform IBOR-style benchmarks have opted for a two-benchmark approach complementing the new ones based on RFRs.

This special feature outlines some key aspects of the new reference rates. First, it sets out a framework and a taxonomy for the main characteristics of existing and new benchmark rates with the aim of highlighting the key trade-offs involved. Second, it reviews the state of financial markets linked to the new RFRs and what this means for the future of term benchmark rates (ie those longer than overnight). Third, it takes a closer look at the implications for banks' asset-liability management. It concludes by touching upon some broader issues surrounding the transition, such as legacy exposures linked to IBORs and cross-currency implications.

Further reading

Desirable features of reference rates and main trade-offs

Devising a new reference rate is no easy task. This is because it may not be feasible to preserve all the desirable characteristics of IBORs while also ensuring that the new rates are grounded in actual transactions in liquid markets. Moreover, for the reform to succeed, a new reference rate must be broadly accepted by market participants that currently rely on IBORs.

The ideal

The ideal reference rate - one that could, like a Swiss army knife, serve every conceivable purpose - would have to:

(i) provide a robust and accurate representation of interest rates in core money markets that is not susceptible to manipulation. Benchmarks derived from actual transactions in active and liquid markets, and subject to best-practice governance and oversight, represent arguably the best candidates in terms of this criterion;

(ii) offer a reference rate for financial contracts that extend beyond the money market. Such a reference rate should be usable for discounting and for pricing cash instruments and interest rate derivatives. For example, overnight index swap (OIS) contracts of different maturities should reference this rate without difficulty, providing an OIS curve for pricing contracts at longer tenors;4 and

(iii) serve as a benchmark for term lending and funding. Given that financial intermediaries are both lenders and borrowers, they require a lending benchmark that behaves not too differently from the rates at which they raise funding. For instance, banks may fund a long-term fixed rate loan to a client by drawing on short-term (variable rate) funding instruments. To hedge the associated interest rate risk, a bank may enter into an interest rate swap as a fixed rate payer in return for receiving a stream of floating interest rate payments determined by a benchmark that reflects the bank's funding costs. If the two types of rate diverge, the bank runs a "basis risk" between its asset and liability exposures.5

In the past, market participants were guided in their choice of benchmarks more by funding cost considerations than the other considerations listed. For instance, in the late 1980s, market participants around the world shifted from using benchmarks based on US Treasury bill rates to those based on eurodollar rates (McCauley (2011)). The primary driver of this "benchmark tipping" was that, in seeking to manage asset-liability mismatches, banks found eurodollar rates a much closer approximation to their actual borrowing costs and lending rates than US T-bill rates (Box A).

The practical

Albeit imperfectly, LIBOR fulfils the second and third of the desirable reference rate features set out above, serving as both a viable reference rate and a term benchmark capturing fluctuations in banks' marginal funding costs. But it fails to meet the first criterion for four reasons.

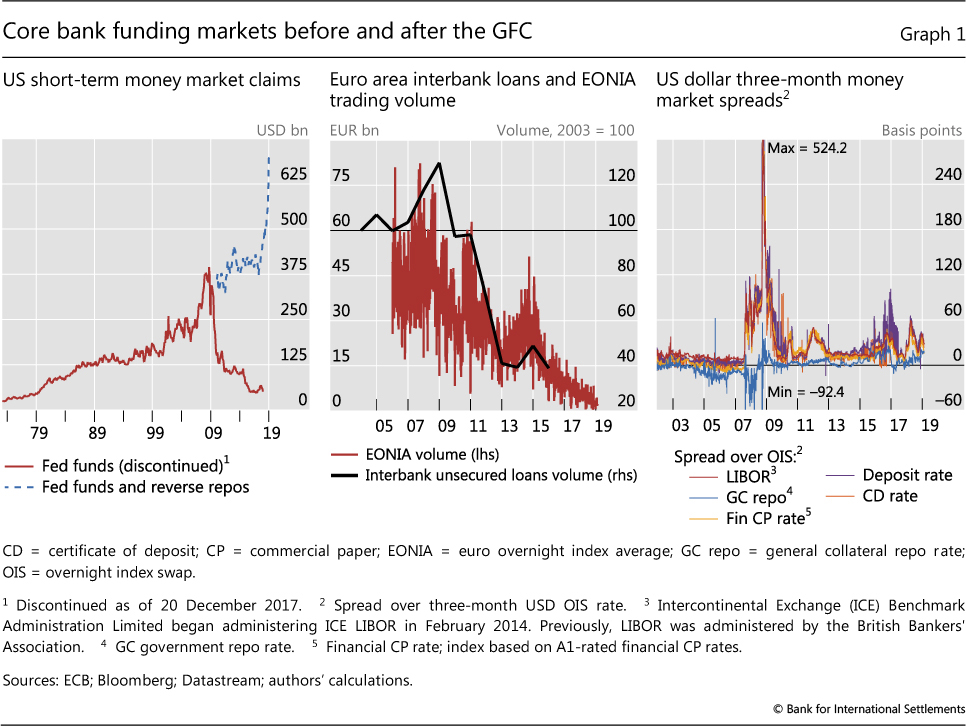

First, in what has turned out to be a design flaw, LIBOR was constructed from a survey of a small set of banks reporting non-binding quotes rather than actual transactions. This created ample scope for panel banks to manipulate LIBOR submissions (Gyntelberg and Wooldridge (2008), Vaughan and Finch (2017)).6

Second, sparse activity in interbank deposit markets stood, and still stands, in the way of a viable transaction-based benchmark based on interbank rates. Even before the GFC, very few actual transactions underpinned the submissions for the longer LIBOR tenors. Since then, interbank trading has plummeted, especially in the unsecured segment (Graph 1, left-hand and centre panels). This was in no small measure driven by the abundant supply of reserve balances created as a result of central banks' unconventional policies (eg Bech and Monnet (2016)). Post-crisis, banks also repriced the risks associated with unsecured interbank lending, reflecting higher balance sheet costs due to tighter risk management and implementation of the new regulatory standards (BIS (2018)) (most notably through the liquidity standards).7 Interbank market activity is thus unlikely to recover much, even if central banks decide to reabsorb such excess liquidity (Kim et al (2018)).

Third, the increased dispersion of individual bank credit risk since 2007 has undermined the adequacy of benchmarks such as LIBOR that aim to capture common bank risk, even for users seeking a credit risk exposure (BIS (2013)). Moreover, money market pricing has become more sensitive to liquidity and credit risk, with banks reducing term lending to each other and increasingly turning to non-banks to source unsecured term funding. This has also exacerbated the dispersion among key money market rates (Duffie and Krishnamurthy (2016)) as well as the divergence between risk-free rates and credit/liquidity-sensitive benchmarks such as LIBOR (Graph 1, right-hand panel).

Box A

LIBOR and "benchmark tipping": then and now

This is not the first time a major shift towards a fundamentally different set of reference rates has taken place in the financial system. However, in contrast to earlier examples of "benchmark tipping", the ongoing reform process is a public-private effort to shift away from unsecured interbank rates towards near risk-free benchmarks. This contrasts with the market-driven process from the late 1980s to the early 1990s of shifting away from risk-free reference rates based on US Treasury bill rates towards benchmarks that embed credit risk based on IBORs. Ironically, back then, market participants transitioned away from using risk-free benchmarks to the risky ones based on eurodollar rates. Banks seeking to manage asset-liability mismatches found the latter a much closer approximation to their actual borrowing costs and lending rates. Otherwise, hedging, say, a portfolio of privately issued securities with a short position in T-bill futures exposed dealers to so-called basis risk, as reflected in a widening TED spread.

This contrasts with the market-driven process from the late 1980s to the early 1990s of shifting away from risk-free reference rates based on US Treasury bill rates towards benchmarks that embed credit risk based on IBORs. Ironically, back then, market participants transitioned away from using risk-free benchmarks to the risky ones based on eurodollar rates. Banks seeking to manage asset-liability mismatches found the latter a much closer approximation to their actual borrowing costs and lending rates. Otherwise, hedging, say, a portfolio of privately issued securities with a short position in T-bill futures exposed dealers to so-called basis risk, as reflected in a widening TED spread.

LIBOR emerged in the late 1960s to support the burgeoning syndicated loan market. In 1986, the British Bankers' Association (BBA) assumed control of the rate, taking responsibility for its publication until January 2014. The BBA collected interbank offered rate quotes from a panel of banks, reflecting the rates at which banks said they could borrow funds from other banks, just prior to 11:00 local time. The top and bottom four responses were discarded in computing LIBOR as an interquartile trimmed mean of the submissions. At one point, the BBA was computing LIBOR for 10 currencies. By October 2013, that number had dropped to five: the US dollar, euro, sterling, yen and Swiss franc. Some central banks have also relied on LIBOR for their operational policy targets (most notably the Swiss National Bank). Following the cases of LIBOR misconduct, in June 2012 the UK Treasury commissioned Martin Wheatley, then CEO-designate of the Financial Conduct Authority (FCA), to establish an independent review into the setting and usage of LIBOR. The findings, along with a plan for the reform of the benchmark, were published in September 2012 in the Wheatley Review. In April 2013, the FCA was given responsibility for regulating LIBOR, while a new private organisation, the Intercontinental Exchange (ICE) Benchmark Administration Limited (IBA), began to administer ICE LIBOR starting in February 2014, following a tender process.

A number of official bodies have steered the reform process since then. In February 2013, the G20 tasked the Financial Stability Board (FSB) with reviewing and reforming major reference rates. To take the work forward, the FSB commissioned an Official Sector Steering Group (OSSG) to monitor and oversee the efforts to implement the reforms. The FSB has convened a Market Participants Group (MPG) to represent private sector interests and address issues that may arise in the implementation and transition (FSB (2014a)). In July 2013, the International Organization of Securities Commissions (IOSCO) published an overarching framework for the principles underlying benchmarks for use in financial markets (IOSCO (2013)). This was followed by the July 2014 publication of FSB proposals on the implementation of the IOSCO principles by benchmark administrators as the starting point for robust reference rates (FSB (2014b)). The FSB continues to monitor and report on progress (eg FSB (2018)). Since then, various new committees and working groups comprising the official and private sectors have sought to establish viable alternative RFRs. Central banks have taken a lead role in the reforms, both as convenors of the committees or working groups tasked with identifying the new RFRs, and as benchmark administrators. This is largely because reference rates have the character of public goods. Further, the private sector faces coordination challenges while central banks have a long history of producing such measures due to their importance in policymaking (Dudley (2018)).

LIBOR has a host of cousins across currency areas and jurisdictions. As the dominant euro benchmark, EURIBOR was the second most widely used benchmark next to LIBOR. Other financial centres such as Hong Kong SAR, Mumbai, Singapore, Sydney, Tokyo and Toronto featured their own fixings in HIBOR, MIBOR, SIBOR, the bank bill swap rate (BBSW), TIBOR and CDOR, respectively. Overall, there were at least 13 similar poll- or quote-based IBOR-style benchmarks. Notably, several jurisdictions with their own IBORs have opted to reform and retain these rates, where reform was deemed feasible. In these cases, a credit-sensitive term benchmark will coexist with the local currency RFR. The reforms of credit-sensitive term benchmarks also aim to bring them into compliance with IOSCO principles by rooting them as far as possible in transactions or executable quotes, subjecting them to stricter oversight, and broadening the set of counterparties to include borrowing from non-banks.

The reforms of credit-sensitive term benchmarks also aim to bring them into compliance with IOSCO principles by rooting them as far as possible in transactions or executable quotes, subjecting them to stricter oversight, and broadening the set of counterparties to include borrowing from non-banks.

McCauley (2001) referred to this process as "benchmark tipping", defined as a strategic situation in which the benefits of a given benchmark choice to one player depend in a positive manner on a similar choice by other players. Currency areas that have opted for such an approach include Australia, Canada and Japan, where reformed editions of the BSSW, CDOR and TIBOR will continue to exist. Meanwhile, attempts to reform EURIBOR are still in flux (EMMI (2019)).

Fourth, due to regulatory and market efforts to reduce counterparty credit risk in interbank exposures, banks have also tilted their funding mix towards less risky sources of wholesale funding (in particular, repos). Derivatives market reforms (such as the mandatory shift to central clearing of standardised over-the-counter (OTC) derivatives, and a move towards more comprehensive collateralisation of OTC derivatives positions) have also increased the importance of funding with little or no credit risk. As a result, markets for swaps and other derivatives have already been transitioning away from LIBOR to OIS rates for discounting and valuation purposes for more than a decade. Against this background, the current reform effort can be seen as, in part, broadening the existing sweep to encompass cash markets and cementing the shift in a clear set of standards.

In light of these issues, reform efforts have focused on linking the new benchmarks with actual transactions in the most liquid segments of money markets. In practice, this has meant that the new reference rates incorporate some (or all) of the following attributes:

(i) shorter tenor, essentially by moving to O/N markets, where volumes are larger than for longer-dated tenors such as three months;

(ii) moving beyond interbank markets to add bank borrowing from a range of non-bank wholesale counterparties (cash pools/money market funds, other investment funds, insurance companies etc); and

(iii) in some jurisdictions, drawing on secured rather than unsecured transactions. The secured transactions could also include banks' repurchase agreements (repos) with non-bank wholesale counterparties.

These changes bring the reformed benchmarks into line with the principles set out by IOSCO (2013) that have served as an important guide for the subsequent work of the FSB and market stakeholders (Box A). These stress that interest rate benchmarks should be anchored in active markets and derived from transactional data where possible, combined with best-practice governance arrangements for benchmark administrators.

Trade-offs

From the above discussion, it is clear that any practical solution will almost inevitably entail trade-offs. A preference for O/N RFRs because of the liquidity and structural features in underlying markets has important implications for the type of term reference rate that will eventually form the backbone of the new regime. Such choices, in turn, will impact the economic characteristics of term benchmarks as well as their suitability for different uses. For example, OIS contracts of different tenors can be linked to the new O/N RFRs. The fixed rates in the OIS market yield a term structure based on risk-free rates, which, in turn, can be used as a reference curve in derivatives markets or for securities issued by governments or corporates. Yet LIBOR also incorporates a risk premium that borrower banks have to pay to compensate lenders for the risks of supplying funds on unsecured terms beyond overnight.8 This risk premium comes on top of the expected average level of O/N rates embedded in an OIS rate. For hedging refinancing risks by banks for instance, term rates derived from O/N RFRs alone may thus not be sufficient.

Against this background, authorities in jurisdictions where it was deemed feasible to reform credit-sensitive term benchmarks similar to LIBOR have opted for a "two-benchmark" approach (as advocated by Duffie and Stein (2015)). This combines a benchmark based on O/N RFRs with another based on reformed term rates which embed a credit risk component, which would be more suitable for banks' asset-liability management.

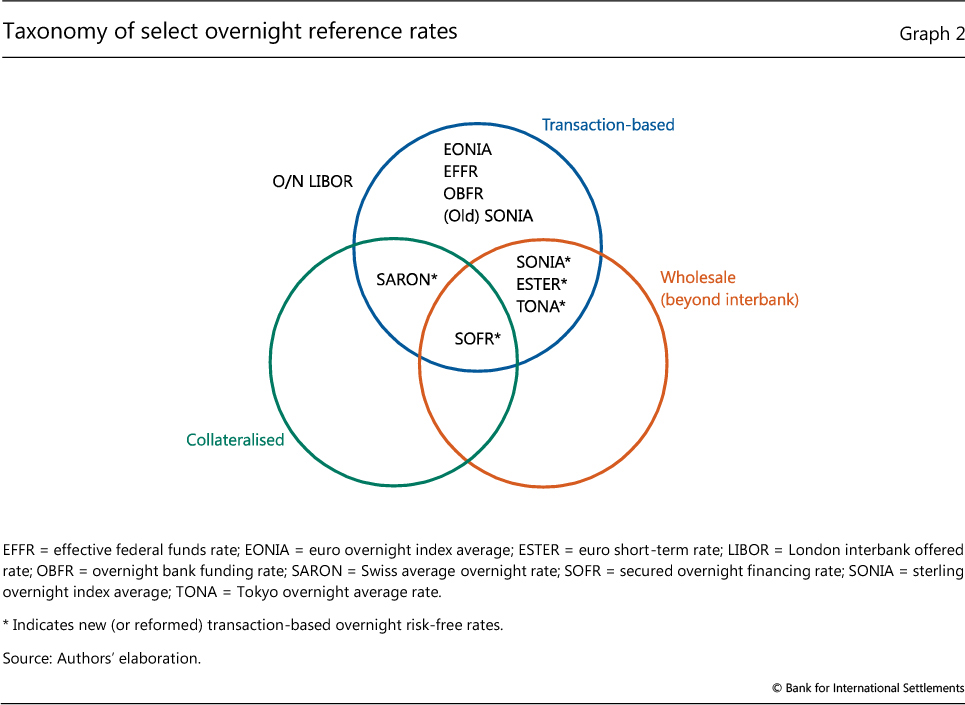

A taxonomy and properties of the new overnight RFRs

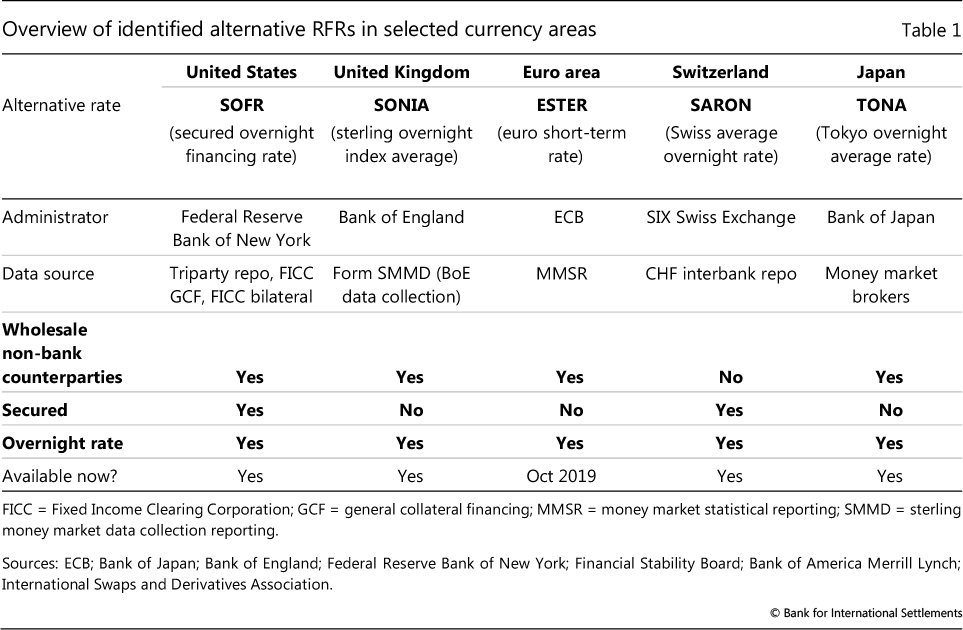

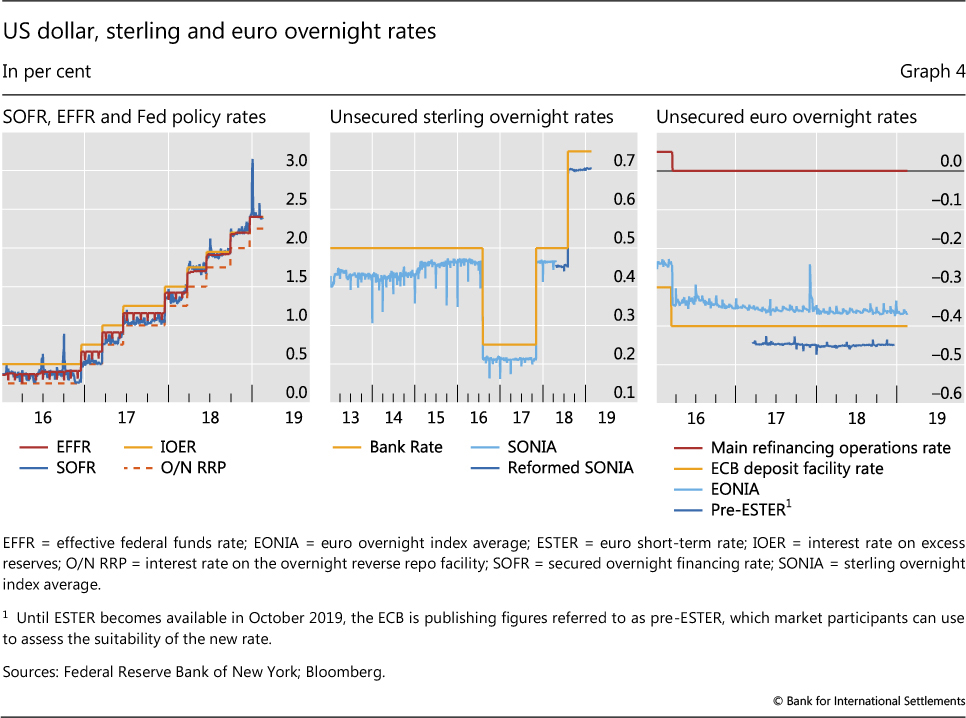

Authorities have taken steps to identify and construct alternative RFR benchmarks compliant with standards such as the IOSCO principles. Five of the largest currency areas have all moved to an O/N benchmark as the backbone of the new regime (Table 1). Graph 2 shows a classification of the old and new O/N reference rates based on key features, ie whether the rate (i) is transaction-based; (ii) is based on collateralised (secured) money market instruments; and (iii) reflects borrowing costs from wholesale non-bank counterparties. For ease of comparison, existing (or old) RFRs as well as O/N LIBOR are also shown.

A major feature for all currencies, with the exception of the Swiss franc, is that the range of eligible transactions is no longer limited to interbank, and includes interest rates paid by banks to non-bank lenders. The United States and Switzerland have further opted to base the secured overnight financing rate (SOFR) and Swiss average overnight rate (SARON) on secured (repo) transactions. Choices between unsecured and secured O/N RFRs have to a large extent been made on the basis of the liquidity and structural features of underlying money markets (FRBNY (2018)).9 One advantage of the United Kingdom's (unsecured) sterling overnight index average (SONIA) is that it has been in existence since 1997. The Bank of England took over the administration of SONIA in April 2016, while the publication of "reformed SONIA" began in April 2018 (Bank of England (2018b)).

Basic characteristics of overnight reference rates

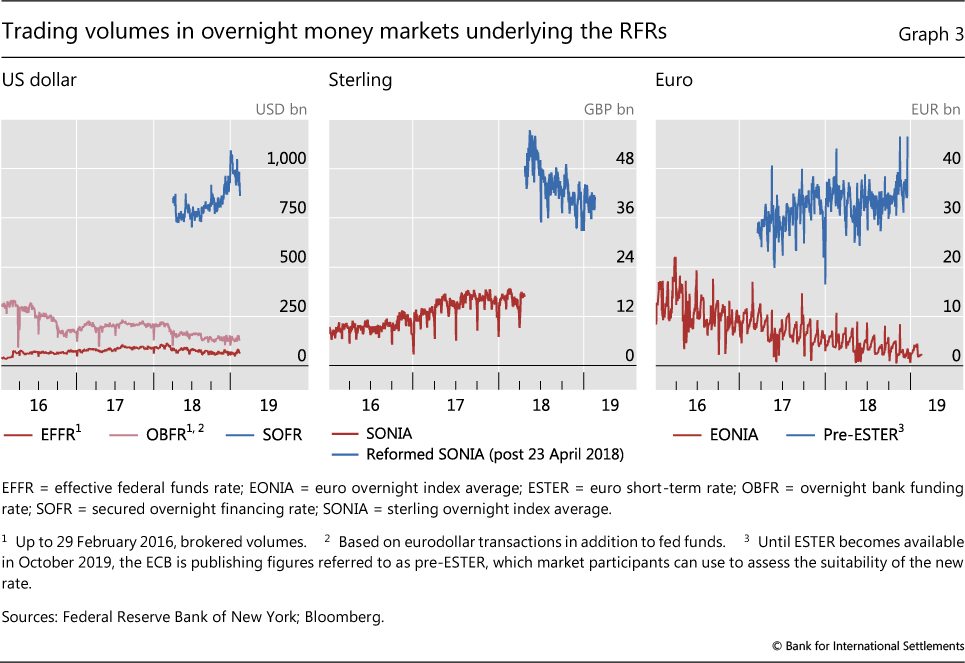

The overnight RFRs are rooted in much deeper markets than their predecessors. Volumes underlying the new US SOFR benchmark dwarf those of the overnight bank funding rate (OBFR), an O/N rate covering the federal funds market and the (offshore) eurodollar market (Graph 3, left-hand panel). The inclusion of non-bank counterparties has also significantly raised the volumes underlying the (reformed) SONIA and the predecessor to the definitive euro short-term rate (pre-ESTER) (Graph 3, centre and right-hand panels).10 For instance, in the case of SONIA, more than 70% of the underlying volume is made up of transactions with money market funds (MMFs) and other investment funds (Bank of England (2018a)), with funding from other banks and broker-dealers contributing less than 15%.

Movements in the new O/N RFRs track changes in key policy rates reasonably well. This can be said of SOFR (Graph 4, left-hand panel) as well as the reformed SONIA and pre-ESTER (Graph 4, centre and right-hand panels). Although the RFRs exhibit a spread to key policy rates (eg the rate of remuneration of reserve balances by banks), the stability of that spread suggests that monetary policy pass-through should generally be satisfactory, at least in normal times.11

However, the inclusion of borrowing costs from non-banks in the calculation may have implications for how the new RFRs behave compared with key policy rates. Non-banks typically have no access to a central bank's deposit facilities. Due to segmentation, the new benchmarks are at times more likely to move outside the desired target ranges of central banks, or below the floor set by the deposit facility rate. In addition, differences in regulatory costs imply that the cost of bank borrowing from non-banks is somewhat lower than comparable interbank rates. That being the case, the reformed SONIA and pre-ESTER tend to fluctuate below the respective central bank deposit facility rates.

In turn, RFRs based on repo markets can also be expected to trade at different levels compared with unsecured O/N rates and, for some jurisdictions, to be more volatile. SOFR has increasingly tended to trade above the range set by the rate of remuneration on banks' excess reserves (interest rate on excess reserves, IOER) and the rate on the Federal Reserve's O/N reverse repo facility (RRP), which bounds the effective federal funds rate (EFFR). As it is rooted in repo markets, SOFR instead lies above the triparty general collateral (GC) and below The Depository Trust & Clearing Corporation's (DTCC's) GCF Treasury repo rate. Finally, SOFR also exhibits volatility due to conditions in collateral markets and dealer balance sheet management. A notable recent example is the December 2018 spike, which was due to a glut in Treasury markets interacting with banks' year-end window-dressing (Box B).

That said, the EFFR was also susceptible to such window-dressing behaviour, although it was affected differently from SOFR. The EFFR used to show a tendency to drop at month-ends because of balance sheet window-dressing by non-US banks facing month-end disclosure requirements. Still, downward spikes in the EFFR have never breached the floor set by the O/N RRP rate. Non-US banks have had a large presence in the fed funds and eurodollar markets because they could exploit arbitrage opportunities offered by the IOER.12 The monthly periodicity in the EFFR disappeared around 2018 once the "IOER-fed funds arbitrage" became unprofitable.

Box B

SOFR and supply and demand conditions in collateral markets

The secured overnight financing rate (SOFR) is based on secured overnight (O/N) transactions that reflect funding conditions in Treasury repo markets. To recall, a repo is a form of collateralised short-term loan, in which the cash borrower pledges a security as collateral while agreeing to repurchase it at a (typically) higher price at a future date. Historically, Treasury repos have served as an important source of funding for dealers in government securities, allowing them to raise cash in exchange for Treasuries pledged as collateral.

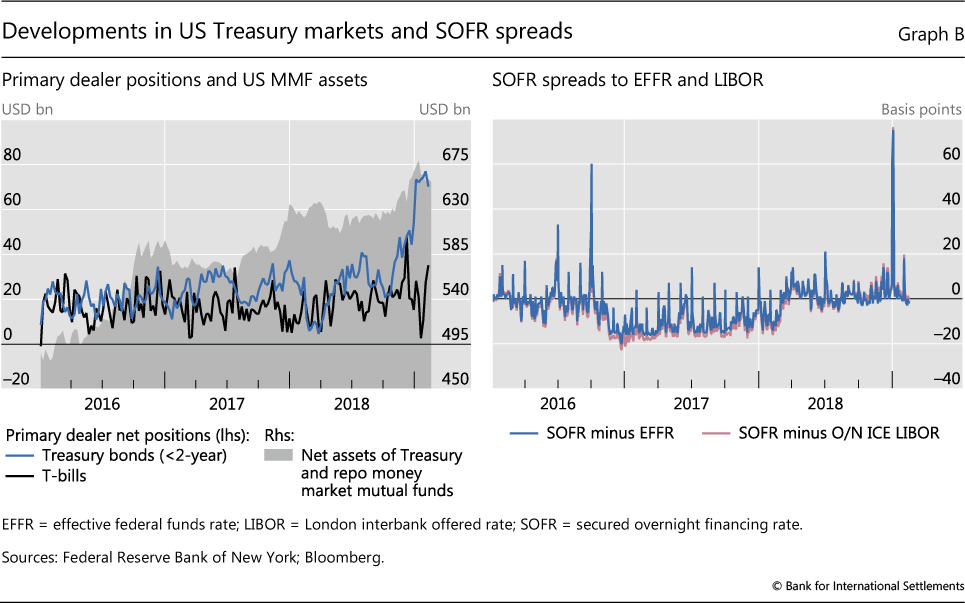

In normal times, repo rates tend to respond to the "cash" leg, ie the demand for, and supply of, funds against the collateral. However, this need not always be the case. For example, in flight-to-safety episodes when US Treasury collateral is in high demand, the collateral leg influences the cash leg, causing repo rates to fall. As a result, benchmarks based on repo rates, such as SOFR or the Swiss average overnight rate, will reflect the supply/demand conditions not only in funding markets, but also in markets for securities that serve as collateral. At times, this can cause the rates to diverge significantly and persistently from benchmarks based on unsecured rates. For example, SOFR was particularly compressed relative to the effective federal funds rate and O/N USD LIBOR from late 2016 to early 2018, in large part because of increased demand for Treasuries as balances shifted to government-only money market funds (MMFs) on the back of US MMF reform (Graph B). The spread then turned positive in Q1 2018 as the supply of Treasuries was boosted by higher securities issuance by the US government. The dynamics of SOFR spreads illustrate SOFR's sensitivity to supply/demand conditions in US Treasury markets.

The pressure on the cash leg could also go in the opposite direction if there is a glut of collateral, rather than a scarcity. The spikes that SOFR exhibits around quarter-ends illustrate the point. These spikes reflect banks' balance sheet management around reporting dates for their exposures under the Basel III leverage ratio and surcharges for global systemically important banks. The spike at end- December 2018 is especially noteworthy (Graph B, right-hand panel). The magnitude was amplified because the US Treasury held additional auctions at year-end, a time when dealer balance sheets were particularly inelastic due to regulatory reporting, being already loaded with Treasury securities. Repo rates jumped as a result, reflecting the emergence of a premium for cash (discount for collateral) in secured funding markets, thus causing SOFR to jump.

See Chen et al (2017) for a detailed quantitative assessment. See eg CGFS (2017).

Implications for monetary policy

At present, central banks have yet to decide and communicate what role, if any, the new benchmarks will eventually play for the conduct of monetary policy. An obvious issue is whether any shift in operational targets might be warranted (or will be necessary because of the discontinuation of existing benchmarks). Should central banks decide to target these rates explicitly, they would need to carefully evaluate the benefits and downsides of possible expansions to the set of counterparties in monetary operations (as well as remuneration policies).13

Implications for monetary transmission could also emerge, warranting further analysis. For benchmarks based on secured transactions, fluctuations in the new reference rate could be partly driven by the demand for and supply of safe assets available to the public, with central banks' own outright asset purchases or sales likely to exert a non-negligible impact on that supply. Increasing usage of RFRs based on secured transactions could hence possibly alter the transmission of balance sheet policies to a broader set of interest rates and asset prices. It is conceivable that the transition to risk- free benchmarks could reinforce the broader transmission of policies. This effect, however, could also be mitigated (or even undone), as banks are likely to find other ways to pass changes in actual funding or hedging costs on to their customers.

Developing RFR-linked financial markets and term rates

The development of liquid financial markets linked to the new rates is crucial if the reforms are to succeed. In addition, term rates must eventually emerge if the new RFRs are to satisfy the second and third key features of an all-in-one benchmark - that is, to serve as an effective reference for financial contracts and discount curves, and to serve as a benchmark for lending/funding rates. While SONIA-linked OIS markets have already been in existence for a while, providing a term benchmark for sterling, OIS markets referencing the new RFRs would have to develop to replace the existing ones referencing traditional O/N rates such as EFFR or EONIA.

There is an inherent chicken-and-egg problem for underlying markets that have to develop from scratch. It is difficult for deep cash markets to emerge in the absence of liquid derivatives markets used to hedge the associated exposures, and vice versa. Users of derivatives markets have been accustomed to using term rates based on compounded O/N rates, and therefore should find transitioning to the new O/N RFR based benchmarks less difficult. But participants in cash markets have been accustomed to using interest rates set for the entire term at the beginning of the period, finding the associated certainty useful for budgeting, cash flow and risk management purposes. That being the case, one open issue for cash markets is whether the transition to term rates derived from O/N RFRs is simply a question of "plumbing" or if it involves any notable economic trade-offs.

State of market development

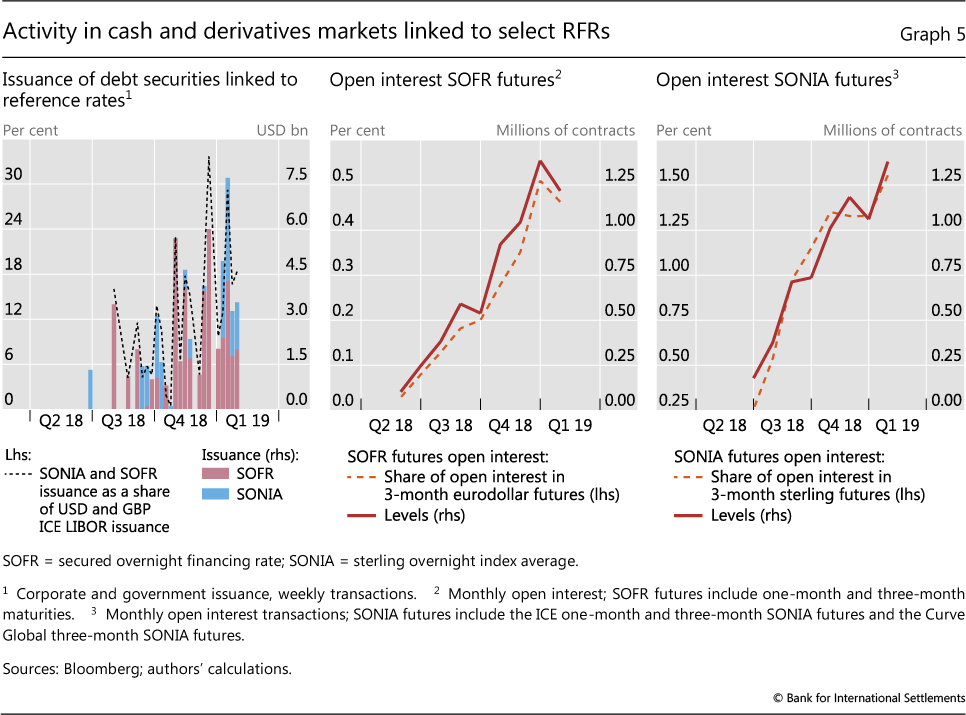

The chicken-and-egg problem accentuates the need for the official sector to take on a coordinating role (Maechler and Moser (2018)). Indeed, it was sovereigns, supranationals and agencies (SSAs) that paved the way as the first issuers of RFR-linked floating rate notes (FRNs). Private financial issuers have now started to follow suit.14 Since mid-2018, the issuance of SOFR- and SONIA-linked securities has gradually picked up (Graph 5, left-hand panel). During a few weeks in late 2018, more than a third of the issued floaters referenced the new RFRs. That said, the volatility of the secured SOFR, especially around year-ends (see above and Box B), deterred some corporates from issuing SOFR-linked securities in early 2019, according to market sources. Market contacts further indicate that issuers of SOFR notes often immediately hedge their funding using LIBOR-SOFR basis swaps. This suggests that the development of the SOFR-linked cash market lags that of the SONIA-linked market for the time being.

With respect to derivatives, major futures exchanges (such as the Chicago Mercantile Exchange (CME) and Intercontinental Exchange (ICE)) have launched contracts linked to SOFR and SONIA since early 2018. Since then, open interest has increased notably (Graph 5, centre and right-hand panels). It is envisioned that liquid SOFR-linked OTC markets, such as OIS markets, will develop in due course. One market that is already well developed is the OTC market for SONIA swaps, where the amounts outstanding compare favourably with those of LIBOR- linked swaps. Arguably, this is due to the fact that the rate, in an older form, has existed since 1997. Overall, the transition of cash instruments to RFR benchmarks should lead to greater liquidity in OIS markets. These should see large trading volumes in response to monetary policy announcements, and also as a reflection of hedging activity related to the various forms of investment and funding that have migrated to new RFR benchmarks.

Despite this build-up of momentum, IBOR-linked business is still dominant in many market segments. Issuance of securities linked to LIBOR is still considerably greater than that linked to the new benchmarks. According to market sources, the transition in loan markets, a segment which is more difficult to monitor due to its opaqueness, has also yet to lift off. And open interest on SOFR and SONIA futures currently stands at no more than 1% of that of their much more mature IBOR-linked counterparts.15

Towards term benchmark rates

A crucial, yet challenging, area of the reform process is the extension of the reference curve from O/N to term rates. In line with the desirable features of benchmarks outlined above, term benchmarks would ideally be grounded in transactions where market participants lock in their actual funding costs for a particular horizon. This would satisfy the third key feature of an all-in-one solution - namely, providing a benchmark for term funding and lending that is closely related to financial intermediaries' marginal funding cost.

Types of term benchmark rate

The economic properties of different types of term rate vary according to how they are constructed. It is helpful to distinguish along two dimensions. The first is whether or not the rate is known at the beginning of the period to which it applies, and whether it reflects expectations about the future or merely past realisations of O/N rates. The second is whether the term rate is based on the pricing of instruments used to raise term funding or on derivatives used to hedge fluctuations in O/N rates.

Backward- vs forward-looking term rates

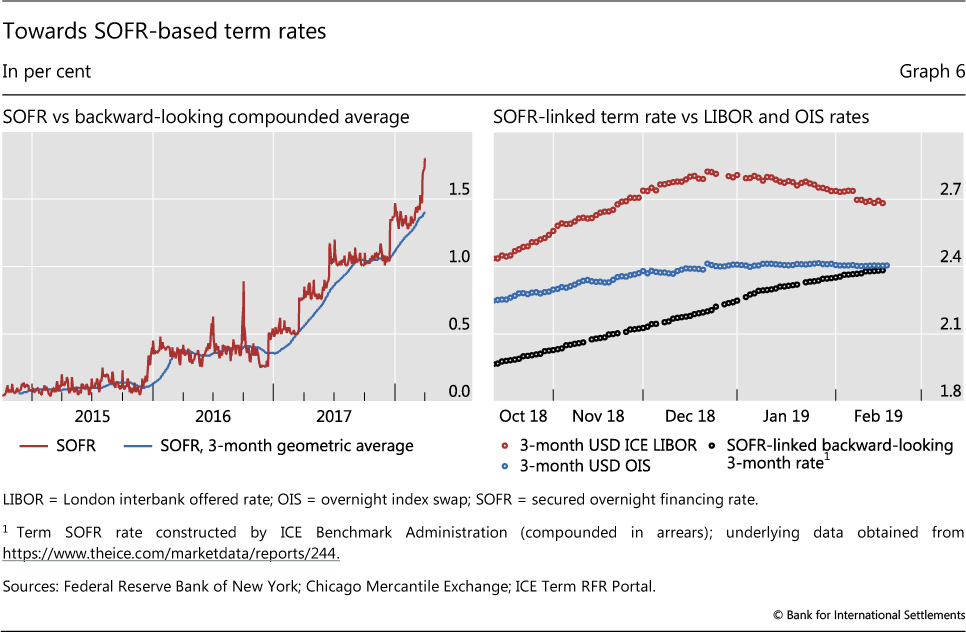

The simplest way to obtain a term rate is to construct it mechanically from past realisations of O/N rates. The leading examples are so-called backward-looking term rates based on a methodology known as "compounded in arrears". To determine the interest payment obligation over a three-month horizon, the compounded O/N RFRs over the same three-month period would be used - a computation which is feasible only once the full realisation of O/N rates is known, ie at the end of the period.16 An advantage is that these term rates can be computed simply from O/N RFRs, even in the absence of underlying transactions in term instruments or in derivatives.17 By construction, backward-looking term rates do not reflect expectations about future interest rates and market conditions.

Backward-looking compounded rates have a number of use cases in cash and derivatives markets. For example, a three-month backward-looking average SOFR (Graph 6, left-hand panel) can be used as a reference rate by issuers of FRNs or for determining floating leg payments in the SOFR-linked OIS. A rate of this type is less prone to quarter- or year-end volatility due to its construction as a geometric average daily rate. The associated smoothness should render the rate attractive for market participants. But, by the same token, it also tends to lag the actual movements in the O/N rate. Especially when short rates exhibit a trend due to central bank easing or tightening, these backward-looking rates will be sluggish to respond to actual developments in O/N market interest rates. Similarly, thanks to its backward-looking construction, the SOFR-linked three-month compounded-in-arrears term rate, used in pricing SOFR futures, appears to have lagged the EFFR-linked forward-looking OIS rate during a recent period of rising rates (Graph 6, right-hand panel).

Forward-looking term rates, by contrast, are known at the beginning of the period to which they apply and are not based on mechanical compounding of O/N rates. Because forward-looking rates are an outcome of a market-based price formation process, they embed market participants' expectations about future interest rates and market conditions. For such rates, the interest obligation received/paid over, say, a three-month horizon is set at the beginning of the term over which the rate applies. Many market participants, especially in cash markets, value this certainty for budgeting, cash flow and risk management purposes. Moreover, the design of existing operational systems in cash markets relies on such rates.

Forward-looking term rates based on term funding instruments vs derivatives

One can further distinguish between forward-looking term rates based on the pricing of funding instruments and those based on derivatives pricing. Term rates based on funding instruments can capture fluctuations in intermediaries' actual term funding costs, which can change over time due to credit and term liquidity premia. Examples are unsecured money market rates akin to three-month LIBOR as well as secured borrowing rates in term repo markets. Such term rates can also be constructed based on the pricing of funding vehicles which banks use to raise wholesale funding from non-banks such as MMFs. Prominent examples of such instruments are commercial paper and certificates of deposit. Such term rates, particularly when based on unsecured funding instruments, would reflect fluctuations in financial intermediaries' marginal term funding costs in their entirety.

By contrast, term rates based on derivatives reflect the market-implied expected path of future O/N rates over the term of the contract, but do not embed premia for term funding risk. An example of a derivatives-based term rate is the interest rate on the fixed leg of an OIS linked to the new O/N RFRs. That rate can be used once the corresponding derivatives markets in SOFR, ESTER, SARON etc have been developed. Another example would be a market-implied rate derived from futures prices linked to the new O/N RFRs. However, such derivatives are not term funding instruments, but are intended as instruments for hedging fluctuations in O/N rates. Term rates based on derivatives will therefore not capture fluctuations in intermediaries' term funding risk.

Hence, despite being forward-looking, term rates constructed from derivatives linked to the new RFRs will have structural features that are different from those of existing IBOR benchmarks. As discussed above, the derivatives-based SOFR-linked forward-looking term benchmark does not yet exist, as derivatives markets linked to SOFR are still in their infancy. But, even when liquidity in the SOFR-linked OIS market develops sufficiently to produce a market-based forward- looking term rate, the resulting curve will essentially be risk-free. Consequently, it will resemble the currently available (EFFR-linked) OIS rate more than it does LIBOR.

Implications for banks' asset-liability management

The new RFR-based benchmarks clearly fulfil the first two of the three desirable features of an all-in-one benchmark rate. Where they seem to fall short is the third key feature, ie serving as a benchmark for term funding and lending by financial intermediaries. Term rates derived from market prices for RFR-linked derivatives (eg OIS or futures) will readily yield a risk-free term structure that can be used for discounting purposes and fulfil various needs in the market. But banks will still lack a benchmark that adequately reflects their marginal funding costs as a substitute for LIBOR. This speaks to the limitations of using O/N rates, instead of those based on term transactions, to create term benchmarks.

As a consequence, banks' asset-liability management could become more challenging in the world of new benchmark rates. Specifically, banks could be exposed to basis risk in periods when their marginal funding costs diverge from interest rates earned on their assets benchmarked to the new RFRs, resulting in a margin squeeze. Consider, for instance, the case where a bank holds a large amount of RFR-linked floating rate loans (RFR plus x basis points) on the asset side of its balance sheet, while its marginal costs of refinancing may diverge if the funding mix includes a variety of secured and unsecured sources. The issue may be exacerbated due to banks' usual practice of funding illiquid assets (eg a loan with terms that are committed over a longer horizon) with instruments of shorter duration - in other words, if banks engage in maturity transformation. The costs at which banks can refinance will be subject to uncertainty as market-wide compensations for term funding risk (an amalgam of credit and term liquidity risk) evolve. If these risks cannot be adequately hedged, it is likely that they will be passed on to clients in one form or another.18

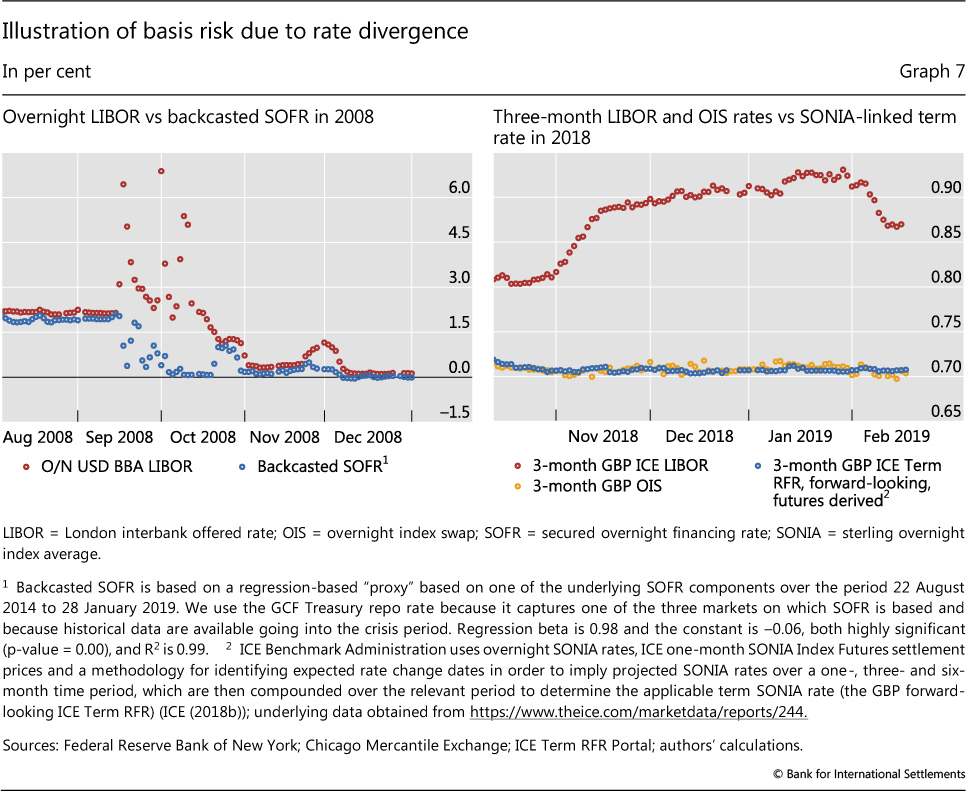

What is more, RFRs based on secured rates (ie repo rates) can actually move in the opposite direction to unsecured ones - a situation most likely to occur when markets are under stress. To illustrate this for O/N rates, we construct a backcasted SOFR to proxy for the rate's hypothetical behaviour during the GFC. We estimate the proxy by regressing SOFR published since 2014 on its close secured rate equivalent, ie the GCF Treasury repo rate. We then use the latter, along with the estimated regression coefficients, to generate backward-projected values for SOFR.19 The spread of the backcasted SOFR to O/N LIBOR widened significantly during the peak of the crisis (Graph 7, left-hand panel). The forces driving unsecured O/N rates (including credit risk) pulled these rates higher as the unsecured interbank markets froze. At the same time, the forces driving secured O/N rates were pulling them lower, owing to a collateral shortage and flight to safety. While such extreme situations do not happen frequently, if they do occur the repercussions can be significant for the financial system.

For longer tenors, term rates based on new RFRs are likely to deviate persistently from their LIBOR counterparts even in normal times. To illustrate this, consider the preliminary term rates based on futures linked to the reformed SONIA. In November 2018, three-month GBP LIBOR rose as funding costs for UK banks increased on the general tightening of financial conditions and the resurgence of Brexit-related concerns. Yet the SONIA futures-implied rates failed to reflect this change (Graph 7, right-hand panel). Instead, the "quasi" forward-looking term rates linked to SONIA appeared to closely track the virtually risk-free three-month OIS rates.20

In search of credit-sensitive term benchmarks

While the sensitivity of banks' profit margins to the spread between their actual funding costs and the risk-free rates may have declined, it has not disappeared. Granted, banks in aggregate may be less reliant on unsecured funding sources than they were pre-GFC, implying a generally lower level of basis risk in the financial system. Yet while the reliance on unsecured wholesale funding has lessened, it has not gone away (for example, see Box C for the amount of outstanding CP obligations). It has also shifted to non-bank wholesale (as opposed to interbank) funding sources. Such unsecured term funding obtained from wholesale non-bank lenders, eg money market funds, is an important marginal source of funding.

According to a 2017 survey conducted by a LIBOR panel bank, 80% of respondents indicated they would prefer LIBOR to remain in some form. Market sources also indicate that basis risk is a central consideration for dealers that currently trade SOFR futures. Such increased riskiness is likely to be passed on to borrowers, eg via higher loan rates, higher fees for services or reduced credit availability.

A "two-benchmark" approach

Given the importance of credit-sensitive term benchmarks, authorities have opted to complement the RFRs with reformed and improved local IBOR-type rates in jurisdictions where this was deemed feasible. In Japan, the reformed TIBOR will coexist with TONA; and in the euro area, there is an ongoing effort to reform EURIBOR to complement ESTER. In both cases, the reformed credit-sensitive term benchmarks are (or will be) computed using some form of hybrid methodology to address the scarcity of underlying term transactions, using techniques such as interpolation and expert judgment, and the inclusion of wholesale funding from non-bank counterparties (Bank of Japan (2016b), EMMI (2019)).

In some other jurisdictions, credit-sensitive term benchmarks were based on somewhat different instruments and may require less substantive reforms. In Australia, the reformed BBSW will be based primarily on transactions, supplemented with executable quotes when necessary, complementing the O/N benchmark based on the Reserve Bank of Australia's cash rate (Alim and Connolly (2018)). In Canada, the liquidity underlying CDOR, which is based on the bankers' acceptance market, has actually been on the rise (McRae and Auger (2018)), making its retention as a credit-sensitive term benchmark that much easier. Over time, additional market solutions may also emerge. Recent attempts by ICE to improve or replace LIBOR offer two such examples (Box C).

An obvious outcome of such uneven approaches to tackling credit-sensitive term benchmarks could be increased market segmentation and a wider variety of benchmarks coming into use across the financial system. Depending on their sophistication, some market players may be better able to adjust than others. On the one hand, this may reduce network efficiencies that come with an all-in-one solution. On the other hand, different benchmarks could emerge that are better fit for individual purposes than the "Swiss army knife approach" implicit in a single benchmark.

Box C

Private sector initiatives to create credit-sensitive term benchmarks

As part of its efforts to improve the LIBOR benchmark, and to bring it into line with IOSCO principles, the ICE Benchmark Administration (IBA) has set a list of objectives and introduced methodologies to produce a reformed LIBOR. In April 2018, the IBA announced that it intends to gradually shift the panel banks to the so-called waterfall methodology for computing LIBOR (ICE (2018a)). The key priorities are to: (i) base LIBOR on transactions to the greatest extent possible; (ii) expand the universe of eligible transactions to include wholesale funding from non-banks; and (iii) use techniques such as interpolation, plus expert judgment, to address gaps in eligible transactions. The IBA expects the transition to the new waterfall methodology to be completed by no later than the first quarter of 2019.

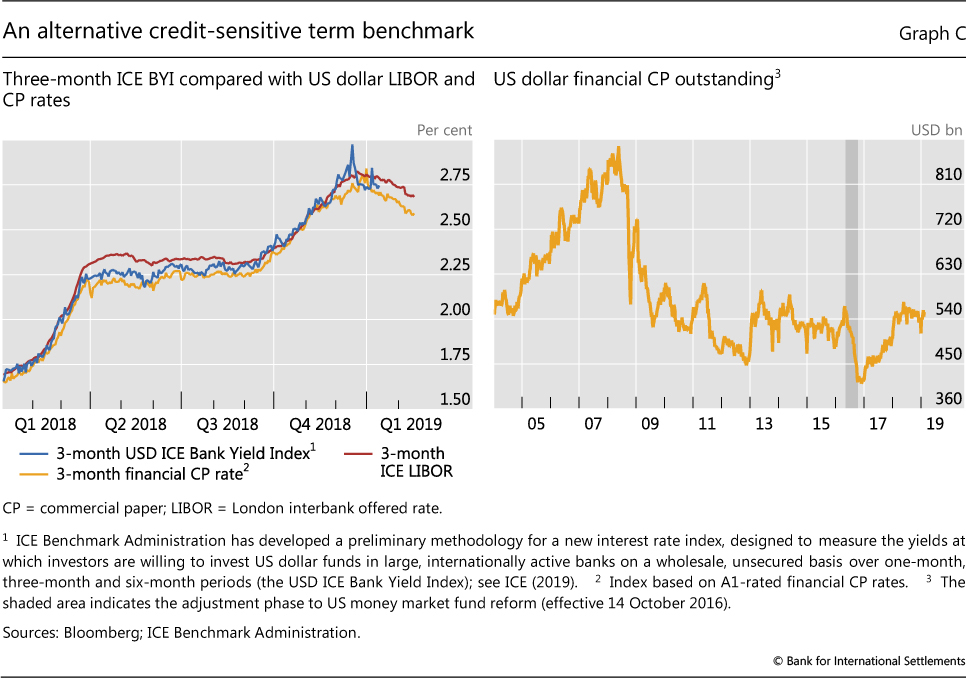

In January 2019, the IBA announced that it was exploring yet another credit-sensitive term benchmark particularly suitable for cash markets. Called the US Dollar ICE Bank Yield Index (BYI) (Graph C, left-hand panel), it seeks to measure the interest rates at which investors are willing to invest in the unsecured debt obligations of a broad set of large internationally active banks for a specified forward-looking tenor (ICE (2019)). The index is underpinned entirely by transaction data representing short-term, unsecured bank funding vehicles. The set of lenders that fund these instruments is broad, and includes central banks, governments, non- bank financials, sovereign wealth funds and non-financial corporates in order to maximise volumes. The instruments include unsecured term deposits, commercial paper (CP) and certificates of deposit (CDs).

This indicates that unsecured term funding still plays a pivotal role in bank balance sheets. It is mostly wholesale non-bank financials such as money market funds that invest in these short-term funding vehicles. For example, while the CP liabilities of US banks have declined from their pre-crisis peak, the long-term average hovers around $500 billion, which is comparable to the size of the market 15 years ago (Graph C, right-hand panel). More broadly, term deposits, CP and CDs still represent an important marginal source of term funding for banks.

Transition issues

Quite apart from the characteristics of the new RFR-based benchmarks, as discussed above, transition issues loom large. The most pressing one is perhaps the migration of legacy LIBOR-linked exposures to the new benchmarks should LIBOR publication cease after 2021. Trillions of dollars of legacy contracts will still be outstanding at that time. Given the material prospect of a possible LIBOR discontinuation, it is crucial from a financial stability perspective that credible fallback language be inserted into contracts.

In response, industry bodies, such as the International Swaps and Derivatives Association (ISDA) at the request of the FSB, have been consulting with stakeholders concerning fallback options. The main goal is to agree ex ante rather than ex post on the fallbacks should the benchmark cease to exist, ie before winners and losers are evident. For derivatives contracts, one feasible option could be shifting to a compounded RFR-linked backward-looking term rate plus a (constant) spread based on historical differences with LIBOR (ISDA (2018)).

The transition appears to be more challenging for cash instruments due to their more bespoke nature. Unlike with derivatives, there is no body that could help coordinate on an overarching industry-wide solution. According to some estimates, the amount of business loans, consumer loans, FRNs and securitised products referencing USD LIBOR with a maturity date after 2022 exceeds $2 trillion (BlackRock (2018)). One can envision several different ways to address the transition. Floating rate cash instruments could be converted to fixed rate contracts. Alternatively, if contract terms have been amended accordingly, the floating rate might switch to an adjusted RFR-based term rate (similar to the solution for derivatives sketched out above). Some issuers may also recall LIBOR-linked debt instruments and replace them with those linked to the new benchmarks.

The transition will also raise important cross-currency issues. While these go beyond the scope of this article, they deserve an in-depth analysis in future work, not least because USD LIBOR has provided a unifying element to global funding markets. For example, Australian banks fund a large part of their home currency assets in US dollar markets. They can then hedge this funding using cross-currency basis swaps that reference USD LIBOR in one leg and the Australian dollar BBSW rate in the other. If US dollar benchmarks shift to quasi risk-free SOFR-linked rates, while the liquid benchmarks in other currency areas are based on unsecured transactions, new instruments may have to be developed to manage the ensuing basis risks.

In addition, interest rate benchmarks in a number of small open economies that lack deep money markets in their own currencies often rely on FX swap-implied benchmarks with USD LIBOR or EURIBOR as the input.21 Such local benchmarks are hence vulnerable to spillovers from the reform process in major currency areas, in turn posing potential market functioning risks.

Conclusion

This special feature has mapped out the landscape of new RFR benchmarks, their basic characteristics compared with LIBOR, and the main trade-offs. A key conclusion is that a "Swiss army knife" solution for benchmark rates does not exist. That is, an all-purpose, all-in-one benchmark may be neither feasible nor desirable. The new RFRs provide for robust and credible overnight reference rates. In principle, they should also allow for the creation of term benchmarks beyond overnight tenors, which makes them well suited to many purposes and market needs (eg computation of interest obligations in cash instruments or discounting and valuation in derivatives markets). Where these indicators are less suitable, however, is in capturing fluctuations in the marginal funding costs of financial intermediaries. This, in turn, intensifies the challenge of hedging particular types of risk, especially asset-liability mismatches on banks' balance sheets. It is hence possible either that reformed benchmarks suitable for such purposes will retain market share or that new market solutions will emerge.

As a consequence, the ultimate outcome of this transition may well feature the coexistence of multiple rates. These would have a variety of characteristics to fulfil differing purposes and market needs. The jury is still out on whether any resulting market segmentation would lead to material costs and inefficiencies, or whether this "new normal" might actually be optimal.

References

Abranetz-Metz, R, M Kraten, A Metz and G Seow (2012): "Libor manipulation?", Journal of Banking and Finance, vol 36, no 1, pp 136-50.

Alim, S and E Connolly (2018): "Interest rate benchmarks for the Australian dollar", Reserve Bank of Australia, Bulletin, September.

Bailey, A (2017): "The future of LIBOR", Bloomberg London event, 27 July.

Bank for International Settlements (BIS) (2013): "Towards better reference rate practices: a central bank perspective", report by a working group established by the BIS Economic Consultative Committee.

--- (2018): 88th Annual Report, Chapter III, June.

Bank of England (2018a): "Sterling money markets: beneath the surface", Bank of England, Quarterly Bulletin, Q1.

--- (2018b): "SONIA: key features and policies", November.

Bank of Japan (2016a): Report on the identification of a Japanese yen risk-free rate, Study Group on Risk-Free Reference Rates, December.

--- (2016b): Revision to the "JBA TIBOR Code of Conduct", etc. for Implementing the JBA Tokyo Inter Bank Offered Rate ("JBA TIBOR") Reforms (3rd Consultative Document), General Incorporated Association JBA TIBOR Administration, November.

Basel Committee on Banking Supervision (BCBS) (2013): Basel III: the Liquidity Coverage Ratio and liquidity risk monitoring tools, January.

--- (2014): Basel III: the Net Stable Funding Ratio, October.

Bech, M and C Monnet (2016): "A search-based model of interbank money market and monetary policy implementation, Journal of Economic Theory, vol 164, pp 32-67.

BlackRock (2018): "LIBOR: the next chapter", ViewPoint, April.

Chen, C, M Cipriani, G La Spada, P Mulder and N Shah (2017): "Money market funds and the new SEC regulation", Federal Reserve Bank of New York, Liberty Street Economics, March.

Committee on the Global Financial System (CGFS) (2017): "Repo market functioning", CGFS Papers, no 59, April.

Dudley, W (2018): "The transition to a robust reference rate regime", remarks at the Bank of England's Markets Forum, London, 24 May.

Duffie, D and A Krishnamurthy (2016): "Passthrough efficiency in the Fed's new monetary policy setting", in Designing resilient monetary policy frameworks for the future, proceedings of the Federal Reserve Bank of Kansas City Jackson Hole Symposium.

Duffie, D and J Stein (2015): "Reforming LIBOR and other financial benchmarks", Journal of Economic Perspectives, vol 29, no 2, pp 191-212.

European Central Bank (ECB) (2018): Report by the working group on euro risk-free rates; on the transition from EONIA to ESTER, December.

European Money Market Institute (EMMI) (2019): Blueprint for the Hybrid Methodology for the Determination of EURIBOR, February.

Federal Reserve Bank of New York (FRBNY) (2018): Second report of the Alternative Reference Rates Committee, March.

Financial Stability Board (FSB) (2014a): Market participants group on reforming interest rate benchmarks: final report, March.

--- (2014b): Reforming major interest rate benchmarks: progress report, November.

--- (2018): Reforming major interest rate benchmarks: progress report, November.

Gefang, D, G Koop and S Potter (2010): "Understanding liquidity and credit risks in the financial crisis", Journal of Empirical Finance, no 18, pp 903-14.

Gyntelberg, J and P Wooldridge (2008): "Interbank rate fixings during the recent turmoil", BIS Quarterly Review, March, pp 59-72.

Intercontinental Exchange Benchmark Administration (IBA) (2018a): "ICE LIBOR evolution", April.

--- (2018b): "ICE term risk free rates", October.

--- (2019): "US Dollar ICE Bank Yield Index", January.

International Organization of Securities Commissions (IOSCO) (2013): Principles for Financial Benchmarks, final report, FR07/13.

International Swaps and Derivatives Association (ISDA) (2018): "Anonymized narrative summary of responses to the ISDA consultation on term fixings and spread adjustment methodologies", December.

Keating, T and M Macchiavelli (2018): "Interest on reserves and arbitrage in post-crisis money markets", Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series, March.

Kim, K, A Martin and E Nosal (2018): "Can the US interbank market be revived?", Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series, no 2018-88.

Kloster, A and O Syrstad (2019): "Nibor, Libor, and Euribor - all IBORs, but different", Central Bank of Norway, Norges Bank Staff Memo, no 2/2019, forthcoming.

Maechler, A and T Moser (2018): "Ten years after the crisis: evolving markets and the challenges for the SNB", speech, Money Market Event, 8 November.

McCauley, R (2001): "Benchmark tipping in the money and bond markets", BIS Quarterly Review, March, pp 39-45.

McCauley, R and P McGuire (2014): "Non-US banks' claims on the Federal Reserve", BIS Quarterly Review, March, pp 89-97.

McRae, K and D Auger (2018): "A primer on the Canadian bankers' acceptance market", Bank of Canada, Staff Discussion Papers, June.

Michaud, F-L and C Upper (2008): "What drives interbank rates? Evidence from the Libor panel", BIS Quarterly Review, March, pp 47-58.

Potter, S (2017): "Money markets at a crossroads: policy implementation at a time of structural change", remarks at the Master of Applied Economics Distinguished Speaker Series, University of California, Los Angeles, April.

Schrimpf, A (2015): "Outstanding OTC derivatives positions dwindle as compression gains further traction", BIS Quarterly Review, December, pp 25-6.

Vaughan, L and G Finch (2017): The Fix: how bankers lied, cheated and colluded to rig the world's most important number, Bloomberg, Wiley Publishing.

1 The authors would like to thank Iñaki Aldasoro, Luis Bengoechea, Claudio Borio, Stijn Claessens, Benjamin Cohen, Marc Farag, Ingo Fender, Ulf Lewrick, Robert McCauley, Elena Nemykina, Jean-François Rigaudy, Catherine Schenk, Hyun Song Shin, Olav Syrstad, Kostas Tsatsaronis and Laurence White for helpful comments, and Anamaria Illes for excellent research assistance. The views expressed in this article are those of the authors and do not necessarily reflect those of the BIS.

2 Even though most of this amount refers to the notional value of derivatives, meaning that actual net exposures are considerably lower (eg Schrimpf (2015)), the sheer scale of funding and investment activity predicated on LIBOR cannot be understated.

3 Over the past 18 months, the reform process has accelerated following a speech by the CEO of the United Kingdom's Financial Conduct Authority, who raised serious concerns about LIBOR's sustainability and announced that, after 2021, the FCA will no longer "persuade or compel" banks to submit the rates required to calculate LIBOR (Bailey (2017)).

4 An OIS is an interest rate swap in which daily payments of a reference O/N rate, such as the effective federal funds rate or the euro overnight index average, are exchanged for a fixed rate over the contract period. The OIS rate is the fixed leg of such a swap, and captures the expected path of the O/N rate over the contract term.

5 In general terms, basis risk can be defined as the risk that the value of a hedge (either a derivative or a contrary cash position) will not move in line with that of the underlying exposure.

6 LIBOR could be manipulated in two ways. First, some banks used their submissions to misrepresent their creditworthiness by understating their borrowing costs. Second, contributing trading desks colluded on their submissions in order to move LIBOR in a way that favoured their derivative positions (see also Abranetz-Metz et al (2012) and Duffie and Stein (2015)).

7 Banks have a strong incentive to deposit extra cash at central banks instead of lending to other banks, as holdings of reserves contribute to the minimum regulatory high-quality liquid asset (HQLA) requirement. By contrast, short-term unsecured wholesale bank funding is unattractive under the Liquidity Coverage Ratio (BCBS (2013)), being subject to greater rollover risk. Moreover, banks have lengthened their funding maturities, incentivised by the Net Stable Funding Ratio (BCBS (2014)).

8 LIBOR incorporates both term liquidity and credit premia, although the relative contribution of the two can differ over time and by maturity (Michaud and Upper (2008), Gefang et al (2010)).

9 In this regard, high trading volume appears to have been a necessary, but not sufficient, condition for authorities' choice of a particular market as a basis for the new RFRs. For instance, one reason for the decision by the Alternative Reference Rate Committee (ARRC) not to base the new RFR on the federal funds or eurodollar market is that O/N transactions in these markets have been dominated by arbitrage trades with little underlying economic rationale (FRBNY (2018)). In contrast, in the euro area it is the secured benchmark which would have been problematic, not least because of the high segmentation in repo markets due to differences in the credit quality of the sovereign bonds serving as collateral.

10 ESTER will be published by the ECB starting October 2019 (at the latest) and must replace EONIA in all new contracts starting 1 January 2020. In the meantime, the ECB has begun publication of "pre-ESTER" to facilitate a smooth transition to the new benchmark (ECB (2018)). On 25 February, EU policymakers agreed on an extension that allows EONIA and EURIBOR to be used by firms based in the bloc until the end of 2021.

11 In a similar vein, Potter (2017) points out that the existence of wider post-GFC money market spreads arising from segmentation, and the fact that banks no longer treat their balance sheet as costless, have not materially impeded the Federal Reserve's ability to steer short-term interest rates under its current operating framework.

12 Unlike US banks, foreign banks could place borrowed funds (typically from government-sponsored enterprises such as the Federal Home Loan Banks) with the Fed to earn the IOER without being subject to the Federal Deposit Insurance Corporation's charges for insured deposits, or the more stringent US leverage ratio regulations in the case of European and Asia-Pacific banks (McCauley and McGuire (2014), Keating and Macchiavelli (2018)).

13 In recent years, there has been a tendency for central banks to open up access to deposit facilities to critical financial market infrastructures such as central counterparties, mostly for financial stability reasons. In some cases, central banks have also allowed non-bank financial institutions such as money market funds to access reverse repo facilities in order to strengthen their control over key money market rates (most notably in the case of the United States). Traditionally, access to the central bank's credit operations was granted only to banks.

14 Quasi-government and agency issuers were the first to open up the market (the European Investment Bank for SONIA and Fannie Mae for SOFR), thereby playing an important coordinating role. The Asian Development Bank and Export Development Canada also issued SONIA-linked debt securities in early 2019. Private issuers, including Barclays, Credit Suisse and MetLife, have also entered the SOFR-linked market. SOFR-linked notes have typically been in shorter maturities of three months to two years. The main US investors have been MMFs, which prefer to buy and hold shorter-term securities with daily floating rates. SONIA-linked notes have been issued with somewhat longer maturities, ranging from one to five years.

15 A similar observation can be made in the case of SARON in Switzerland.

16 Participants in interest rate derivatives markets are accustomed to this type of rate. For example, floating rate payments at the maturity of an OIS contract are typically determined by compounding in arrears the O/N rates realised during the term of the swap.

17 For instance, the US ARRC has published a timeline for a paced transition with the ultimate goal of creating a term RFR based on SOFR derivatives once liquidity has developed sufficiently. For the time being, backward-looking compounded term rates can be constructed based on O/N SOFR rates. Similar approaches have been considered in other currency areas (eg Switzerland).

18 Banks are likely to differ in the extent to which they are exposed to such issues depending on their business model and where they are domiciled. For instance, the issue could be more pronounced for a global non-US bank with a large US dollar book, which needs to roll over its USD funding in offshore markets. A US bank with access to a large amount of insured retail deposits, by contrast, would be affected to a lesser extent.

19 We use the GCF Treasury repo rate because it captures one of the three markets on which SOFR is based and because historical data are available going into the crisis period. The regression beta is 0.98 and the constant is -0.06, both highly significant (p-value = 0.00), and R2 is 0.990 (sample period: 22 August 2014 to 28 January 2019). For comparison, the analogous regression using the triparty GC repo rate yields a regression beta of 0.99 and a constant of 0.04 with an R2 of 0.998. The sign of the constants is consistent with SOFR fluctuating below the GFC Treasury repo rate and above the triparty GC repo rate. The somewhat higher significance of the coefficient estimates in the triparty GC repo rate regression is also consistent with much higher transaction volume in this market compared with the GCF market. Another important market segment underlying SOFR is the bilateral repo market.

20 We call them "quasi" forward-looking here because the ICE Benchmark Administration derives the associated (preliminary) three- and six-month term rates using only the ICE one-month SONIA index futures settlement prices. The reason is that liquidity is still lacking in longer tenors. Hence, even the so-called forward-looking rate shown incorporates a degree of compounding (ICE (2018b)).

21 One example where this has been the case is the Norwegian krone benchmark NIBOR (see Kloster and Syrstad (2019) for a discussion).