Equity pledge financing and the Chinese stock market

Since March 2017, Chinese regulators have pursued concerted measures aimed at reducing leverage in the financial system and managing financial sector risks. These measures have reduced shadow credit sharply since March 2018, exerting pressure on financing by privately owned enterprises (POEs) and small and medium-sized firms. With a slowing economy and falling equity prices, new measures have been taken to contain emerging risks, from equity pledge financing (EPF) - that is, lending extended to key shareholders or managers of listed companies who pledge their shareholdings as collateral. This box reviews the latest developments in EPF, their relationship with the recent market decline, the risks that EPF poses, and how regulators and firms have responded.

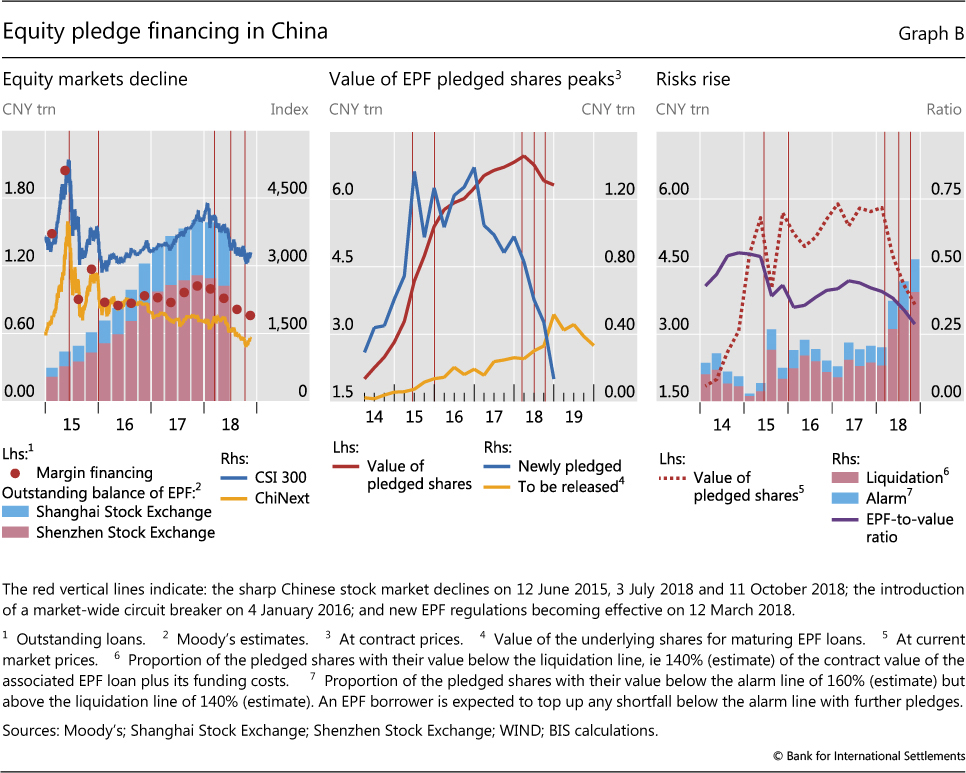

EPF grew very rapidly in China starting in 2014. Though hit hard by the market meltdown in the second half of 2015, EPF recovered strongly, with outstanding equity pledge loans peaking at CNY 1.6 trillion in Q4 2017 (Graph B, left-hand panel). Notably, the value of newly pledged shares had already started to fall sharply from Q1 2017, even as the outstanding amount continued to grow (centre panel).

Chinese stock markets reversed course in 2018. From its peak in January 2018, the CSI 300 Index fell 31% by 18 October, before a moderate recovery (Graph B, left-hand panel). Unlike the 2015 stock market turbulence, where margin financing (ie loans secured against the securities the borrowers purchase) played a key role, the current episode has highlighted the risks of EPF. The Shenzhen Stock Exchange, including the technology-oriented ChiNext Market, saw heavier share price declines; companies listed there tended to be more exposed to EPF risks.

Nevertheless, EPF remains a salient feature of the Chinese equity markets: at end-October 2018, the contract value of pledged shares was CNY 6.3 trillion (Graph B, centre panel). By some estimates, as many as 3,540 listed companies had shares pledged under EPF, with 22.5% of them having over 30% of their shares pledged.

EPF presents several risks. First, EPF exposes the company to the risk of an unintended change in shareholding structure (a new set of shareholders with a potentially different risk appetite and time horizon) if the pledged shares have to be liquidated. Second, the lenders bear liquidity risks. As of Q3 2018, over 50% of lenders were securities firms. In the event of a default, securities firms are prevented from liquidating the pledged shares immediately, as shareholders with a 5% or higher stake are not allowed to sell more than 1% of their shareholding within 90 consecutive days in the secondary market. This rule, and trading suspensions, reduce the liquidity of the pledged shares. Third, while only 20% of direct EPF lenders were banks in Q3 2018, most EPF lending ultimately relied on bank funding. An EPF failure could weaken banks' balance sheets. As equity prices fell in 2018, many of these risks rose significantly. In Q4 2018, as more EPF loans came due, the underlying pledged shares to be released were estimated at CNY 517 billion, a potentially significant overhang on market valuations.

The Chinese authorities have tightened EPF regulations since September 2017, amid the ongoing efforts to reduce financial leverage and risk. Significant new rules came into effect in March 2018. The rules restricted the EPF-to-value (ETV) ratio to no more than 60% and placed limits on the fraction of a company's shares that can be pledged (both overall, and to a single securities firm or asset management product).

Tighter regulation and falling equity prices have been the main drivers of a sharp decline in EPF in 2018. The market value of pledged shares fell from CNY 5.8 trillion at end-March 2018 to CNY 3.7 trillion at end-October (Graph B, right-hand panel). As share prices fell, the proportion of pledged shares with their current market value falling below the "liquidation" and "alarm" lines (set by lenders relative to the value of the associated EPF loans including funding costs) rose sharply (Graph B, right-hand panel, red and blue bars). Share values below the "alarm" line oblige borrowers to make up the shortfall in collateral, while lenders can force liquidation once prices fall below the "liquidation" line. Forced sales of shares correspondingly picked up as from June.

With their share prices under pressure, listed companies scrambled for solutions. Some requested trading suspensions by exchanges; such suspensions rose significantly in 2018. Nearly 60% of suspensions were applied to companies which had pledged 30% of their shares or more. However, this became more difficult as new guidelines released on 6 November discouraged listed companies from arbitrarily applying for a trading suspension or delaying the resumption of trading without proper justification. Second, firms with strong cash flows turned to stock buybacks, which would raise share prices and lower EPF risks. A third approach involves direct intervention by state funds. State entities have invested heavily in listed private firms this year, taking control of over 20 listed POEs.

The Chinese authorities have recently taken new initiatives to stabilise the equity market, support financing for POEs and contain risks associated with EPF. These include recent targeted measures by the central bank and banking regulators to promote funding for POEs. Moreover, in October the regulators announced new rules allowing insurers to provide special asset management products to institutional investors for investment in equities and in bonds issued by listed companies and their shareholders, in order to help EPF participants and support POEs. Organised by the Securities Association of China, 11 securities firms agreed to contribute CNY 25.5 billion to a parent asset management plan aimed at helping listed companies with growth prospects but EPF difficulties. Already, two "special bailout bonds" have been issued under the plan. Regulators have also established a pilot "credit protection tool" to support bond financing by POEs. Several local governments have set up funds to support POEs with EPF difficulties. These measures appear to have helped contain EPF risks; the ETV ratio dipped further, to below 30% at end-October.