The new US intermediate holding companies: reducing or shifting assets?

Recent volatility in the US bond market recalls long-standing concerns about market-making capacity, especially for corporate bonds. This box examines how the balance sheets of foreign banking organisations (FBOs) with big US broker-dealers have responded to the implementation of the Dodd-Frank Act. Despite their reduction of assets subject to new US capital requirements, their market-making capacity in US corporate and agency bonds has not suffered.

This box examines how the balance sheets of foreign banking organisations (FBOs) with big US broker-dealers have responded to the implementation of the Dodd-Frank Act. Despite their reduction of assets subject to new US capital requirements, their market-making capacity in US corporate and agency bonds has not suffered.

This law required the Federal Reserve to enhance prudential standards for bank holding companies (BHCs) with assets over $50 billion, including through stress tests, capital plans and living wills. On the principle of "national treatment", the Fed required FBOs with $50 billion or more in US subsidiary (also known as "non-branch") assets to put all their US subsidiaries under an intermediate holding company (IHC) by 1 July 2016.

On the principle of "national treatment", the Fed required FBOs with $50 billion or more in US subsidiary (also known as "non-branch") assets to put all their US subsidiaries under an intermediate holding company (IHC) by 1 July 2016.

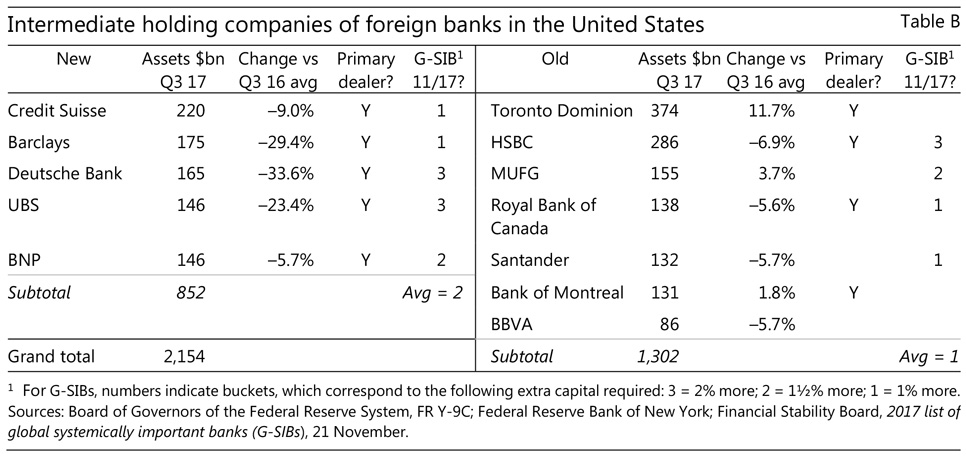

Foreign banks changed their operations and legal structures in response to this IHC requirement in several ways. Some squeezed subsidiaries' assets enough to avoid the IHC requirement altogether. Others already had separately capitalised BHCs, converted them into IHCs, and maintained or grew assets. Since these ("old") IHCs had largely adapted their operations to host capital requirements, we take them as a control group. Finally, five FBOs with Fed primary dealers, who had to set up new IHCs, have since reduced IHC assets (Table B) and appear to have also shifted assets to their offshore and US bank branches not subject to the US capital requirements.

Five banks on a 2014 Federal Reserve "illustrative list" of 17 banks that might have needed to set up IHCs ended up with subsidiary assets low enough not to do so. One of the five, Royal Bank of Scotland, had committed to its main owner, the UK Treasury, to downsize irrespective of the IHC threshold. Of the others, Société Générale had subsidiary assets over $50 billion as late as 30 June 2015 but managed them below the threshold by year-end.

that might have needed to set up IHCs ended up with subsidiary assets low enough not to do so. One of the five, Royal Bank of Scotland, had committed to its main owner, the UK Treasury, to downsize irrespective of the IHC threshold. Of the others, Société Générale had subsidiary assets over $50 billion as late as 30 June 2015 but managed them below the threshold by year-end.

Deutsche Bank established an IHC, but only after cutting its US subsidiary assets very substantially. Its former US BHC, named Taunus, had $355 billion in assets at end-2011 before it relinquished its BHC status in early 2012. Its new IHC reported assets at end-Q3 2016 of just $203 billion. Other FBOs may also have cut subsidiary assets before setting up new IHCs in 2016, again with the effect of limiting US capital charges, but data are lacking.

Its new IHC reported assets at end-Q3 2016 of just $203 billion. Other FBOs may also have cut subsidiary assets before setting up new IHCs in 2016, again with the effect of limiting US capital charges, but data are lacking.

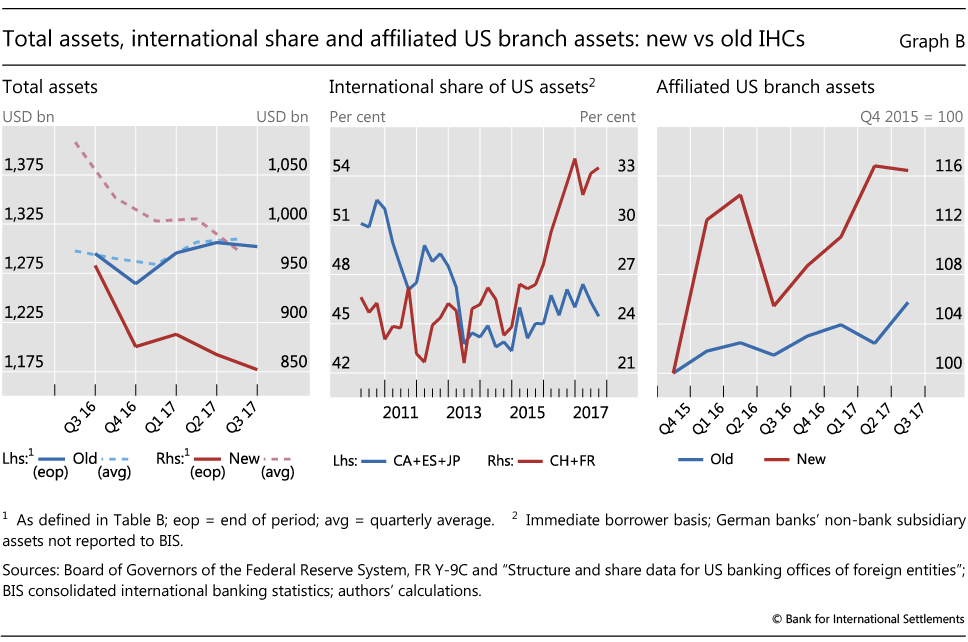

Since establishment, every new IHC has reduced its assets and therefore its required capital. Between Q3 2016 and Q3 2017, the new IHCs shrank their total assets by about $100 billion or 10% (Graph B, left-hand panel, either quarter-average or end-of-quarter). In contrast, FBOs with pre-existing BHCs ("old IHCs") kept their total US assets unchanged at $1.3 trillion. The new IHCs shrank their trading assets by $50 billion, moving or cutting Treasury securities but keeping agency and corporate bonds roughly unchanged. Trading asset levels at the old IHCs were stable.

If the new IHCs have shed assets in their US subsidiaries, did they also shift assets offshore? FBOs could do so either by rebooking existing assets or by booking new assets offshore. BIS consolidated international banking data are consistent with such a shift. In particular, Swiss and French banks have indeed grown (mostly offshore) international claims on US residents faster than locally booked claims on US residents (Graph B, centre panel). From a pre-IHC trough of 24% in 2014, the ratio of international claims on US residents of banks headquartered in these new IHC countries to their total US claims increased to 33% in the third quarter of 2017, an increase of 9 percentage points at the margin and a share increase of more than a third. In contrast, the ratio for the countries with banks operating with old IHCs barely increased, from 43% to 45%.

The FBOs with the new IHCs look to have shifted assets to US branches as well (Graph B, right-hand panel). From end-2015 to September 2017, US branch assets for FBOs with new IHCs increased by 16%. By contrast, during that same time, US branches of FBOs with old IHCs increased by 6%. If the branches affiliated with new IHCs had shown similar asset growth, their assets would have been $58 billion less. As with shifts of assets to foreign branches, operational, transfer accounting and legal constraints presumably limited the shifts from IHCs to their respective US branches.

We conclude that foreign banks facing the IHC requirement did not sit still. At least one FBO avoided the IHC mandate by shrinking assets while another cut assets significantly before the IHC deadline. All the new IHCs have subsequently reduced their footprints. Asset shifts within FBOs from IHCs to offshore or US bank branches would have reduced the specific US capital charges. One caveat is the limitation of our natural experiment: our control group with pre-existing BHCs has a greater weight of banking in their business models and, relatedly, a lower capital surcharge for consolidated size, interconnectedness, substitutability, span and complexity (Table B, "G-SIFI?" column).

Any shrinkage of trading books by foreign-owned primary dealers could worsen the perceived disproportion between the huge stock of US corporate bonds outstanding and dealer inventory. Thus far, however, the new IHCs' asset reduction has spared their trading book of agency and corporate bonds.

Committee on the Global Financial System, "Fixed income market liquidity", CGFS Papers, no 55, January 2016. US Treasury, A financial system that creates economic opportunities: banks and credit unions, June 2017, suggests a higher threshold. "Factbox: Fed lists foreign banks that may fall under new rule", Reuters, 20 February 2014. Letters from the Board of Governors to Sheldon Goldfarb, General Counsel, RBS Americas, 11 December 2014, and to Slawomir Krupa, CEO, Société Générale Americas, 6 July 2016. Another of the five banks, Mizuho, expected to set up an IHC in the future according to the Board letter to Frank Carellini, Deputy General Manager, Mizuho Bank (USA), 18 February 2016. Deutsche Bank, Annual Report, 2011 and 2012, notes on subsidiaries; S Nasiripour and B Masters, "Bank regulators edge towards 'protectionism'", Financial Times, 12 December 2012.