The implications of passive investing for securities markets

The popularity of passive investing through index mutual funds and exchange-traded funds (ETFs) has grown substantially over recent years, displacing higher-cost active investment styles. A shift towards passive investing could affect securities markets in two key ways. First, it could result in higher correlation of returns and less security-specific price information. Second, it could affect aggregate investment fund flows and market price dynamics. In this context, active mutual funds exhibited persistent outflows in recent stress periods, whereas passive mutual fund flows were fairly stable. ETF flows were relatively volatile, although their link with underlying prices is less straightforward than for other fund types.1

JEL classification: G11, G12, G14, G23.

Passive portfolio management (or passive investing) is a strategy that tracks the returns of a price index, such as an established market benchmark. It is typically implemented by holding each of the indices' constituent securities in line with their representation in the index. Maintaining a passive investment strategy requires no trading in the absence of changes in index composition.

Passively managed funds are investment vehicles that offer diversified and low-fee portfolios. This contrasts with actively managed funds, which seek to earn higher returns than their chosen benchmark through discretionary security selection or trading in anticipation of market turning points. Doing so generates trading costs and requires compensation to active managers and investment in relevant information, which go hand in hand with higher fees.

Aside from the issue of the potential benefits and costs for individual investors, rapid growth of passively managed portfolios has generated debate about their possible impact on securities markets. One concern is that the mechanical investment rules of passive investing may give rise to distortions in the pricing of individual securities. At the aggregate level, there is also the question of whether it might add to destabilising price dynamics by amplifying investors' trading patterns.

This special feature provides a conceptual and empirical discussion of these issues. A key observation is that, despite their rapid growth, passive funds account for a relatively small fraction of outstanding securities. Even so, the available empirical evidence suggests that portfolio-wide trading of passive funds can still contribute to correlation across individual security prices. The mechanical way that passive funds manage their portfolios implies that their impact on aggregate security price dynamics will depend mostly on how end investors behave.2 Here, it is important to distinguish between the two main types of passive fund: index mutual funds and exchange-traded funds (ETFs). In this respect, we observe that investors in index mutual funds exerted a stabilising influence in recent periods of market stress relative to those using active mutual funds, while flows in and out of ETFs were relatively volatile.

The remainder of this feature is organised as follows. The first section provides an overview of the growth in passive funds across asset classes and countries. The second outlines the theoretical grounds for passive investing, and the third discusses factors behind its recent growth. The fourth considers the implications of greater passive investing for security prices and issuers, while the fifth examines the impact on aggregate fund flows and market price dynamics.

Recent growth in the passive fund industry

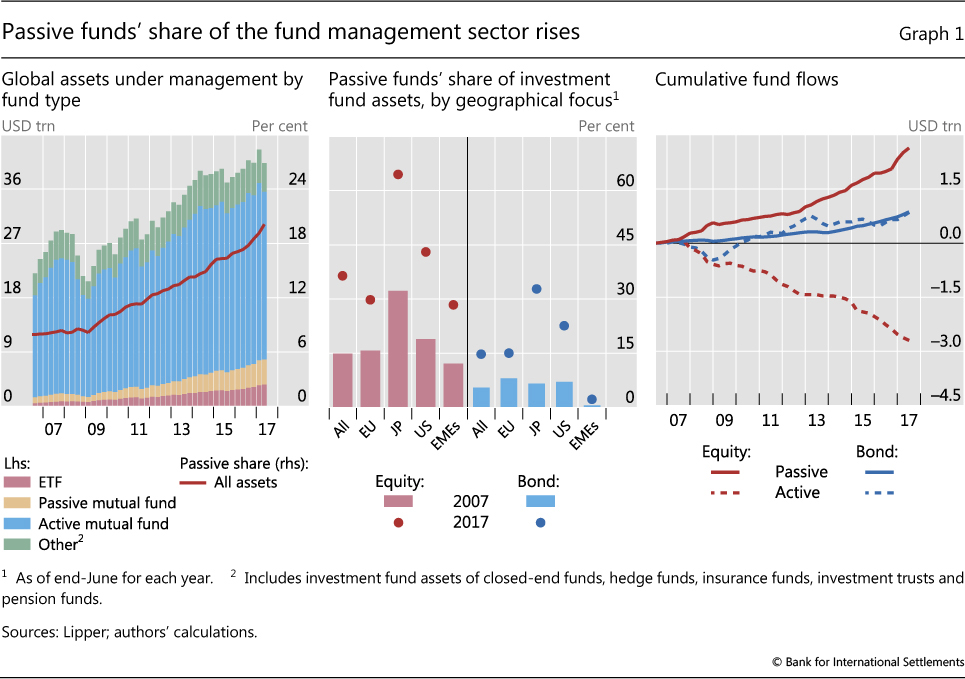

Passive fund assets have expanded rapidly over recent years and now represent a significant portion of the global investment fund universe. Measuring industry size by assets under management, passive funds managed about $8 trillion or 20% of aggregate investment fund assets as of June 2017, up from 8% a decade earlier (Graph 1, left-hand panel). Passive (or index) mutual funds, the traditional passive portfolio product, grew sharply over this period. ETFs, which allow intraday trading of shares in passive portfolios on a secondary market, grew even faster (Box B).3 ETFs' share of passive fund assets exceeded 40% in June 2017, compared with around 30% in 2007.

Growth in passive funds has been rapid for both equity and bond asset classes (centre panel). The rising popularity of passive equity funds has displaced investment in their active counterparts, which experienced outflows over the past decade (right-hand panel). Net outflows from active bond funds were concentrated in 2013 and 2015 - periods of bond market turbulence. Most of the remaining passive funds specialise in commodities.

Despite the rapid growth of passive bond funds, the majority of passive portfolios remain focused on equities. To some degree, this reflects the greater liquidity and exchange-traded nature of equities. In addition, constructing and tracking indices of equities is easier because they are perpetual securities, while the high correlation of interest rates may make holding broad market index bond portfolios less attractive (Fender (2003)).

Across countries, passive funds have gained most prominence in US equities. There, they have expanded to more than $4 trillion, or 43% of total US equity fund assets (Graph 1, centre panel). Although starting from a much lower base, passive funds have gained even more traction among Japanese equity funds, supported by the Bank of Japan's ETF purchases and the Government Pension Investment Fund's increased allocation towards equities over recent years.4 Sharp rises in the proportion of passive funds have also occurred for European and emerging market economy (EME) equity funds.

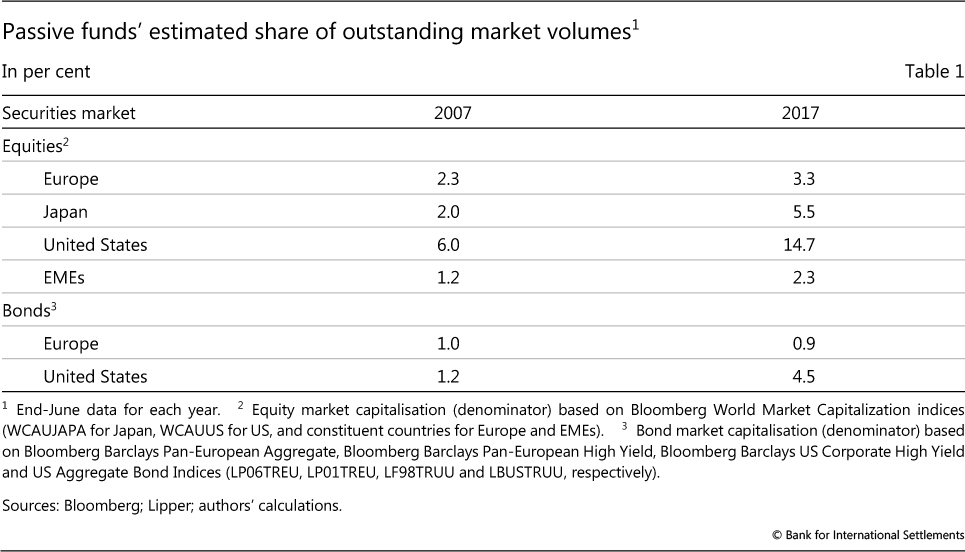

While passive funds have made substantial inroads into the universe of investment vehicles available to end investors, their holdings as a share of total outstanding securities remain at a relatively low level due to the sizeable holdings of other (non-fund) investors (Table 1). The share of securities held by passive fund portfolios is highest for the US equity market, but it still amounts to only around 15% of the total. Shares of passive funds in other equity markets are lower, at about 5% or less. The proportion of passive bond funds has risen to almost 5% of the US bond market.

Using assets managed by index tracking funds is a simple approach to measuring the extent of passive investing, but it is not without shortcomings. In practice, the distinction between passive and active fund strategies is fuzzy. The risk of outflows if they underperform their benchmark leads many active funds to avoid portfolios that deviate substantially from those of the market index. Cremers et al (2016) find that in many countries the share of "closet indexing" (where weights of securities in equity fund portfolios are not substantially different from those of the benchmark) is more or less the same as that of "explicit indexing", if not higher. Closet indexing is also prevalent among actively managed bond funds, particularly those investing in EMEs (Miyajima and Shim (2014)). Furthermore, other investors, such as pension funds and insurance companies, may implement passive investment strategies in their portfolios managed in-house or through investment vehicles other than mutual funds and ETFs. The rise of "smart beta" ETFs further blurs the distinction between passive and active fund management. Rather than track traditional market value-weighted indices, smart beta ETFs implement factor-weighting index strategies (such as those for value, volatility and dividend yield), the construction of which can be considered active in nature (Blackrock (2017)).

In sum, ascertaining the true extent of passive investing is challenging. Nonetheless, it seems clear that over recent years there has been a substantial shift towards passive portfolio management globally.

Theoretical grounds for passive investing

The end users' choice of investment vehicle depends on not only the track record of the fund manager but also how the manager's style accords with their preferences and risk appetite. There are several general considerations for individual investors in deciding whether or not to adopt a passive investment strategy (market-wide considerations are discussed further below).

From a theoretical perspective, the rationale for individual investors adopting a passive investment strategy is grounded in the notion of efficient markets. This theory holds that security prices rapidly incorporate all available information, implying that (excess) future returns are not predictable.5 A natural corollary is that there is limited room, if any at all, for active investment strategies to generate returns above those of the market. Limited scope for systematic outperformance raises doubt about the rationale of incurring management fees in excess of those necessary to maintain a diversified market portfolio.

Even if one rejects the notion of market efficiency (and thus the inability of managers to produce above-market returns over time), passive investing can still be considered an optimal strategy to the extent that outperformance of the market benchmark is a "zero sum game" (Sharpe (1991), Malkiel (2003)). Since passive investors' average return before costs should, by construction, equal the market return, the average return across all active investors must also equal the market return. Given that active investors are attempting to beat the market, any gains for some of these investors must be offset by the losses of others. Thus, after trading costs, the average return for active investors will be less than for passive ones.

In principle, investors could earn superior returns by selecting those active funds that outperform. But identifying such funds can be difficult in practice because it requires ex ante information about the incentives and skill of a manager. Adopting a strict index-based investment strategy therefore circumvents the main asymmetric information and agency problems arising from delegating authority for investment decisions to a fund manager (Vayanos and Woolley (2016)).

Notwithstanding the above arguments, there may still be a strong theoretical case for active management. First, informed active managers can earn above-market returns to the extent that the investor universe also includes active but uninformed investors whose aggregate portfolio underperforms the market. Second, while the zero sum game argument holds for a constant market portfolio, in reality passive fund managers must trade (albeit not frequently) to manage investor inflows and outflows and because indices themselves are not static (Pedersen (2018)). This means that, on average, informed active investors could outperform the benchmark by taking advantage of passive managers' predictable trading patterns, such as by trading in anticipation of adjustment to index membership or ahead of initial public offerings.

Drivers of recent growth in passive investing

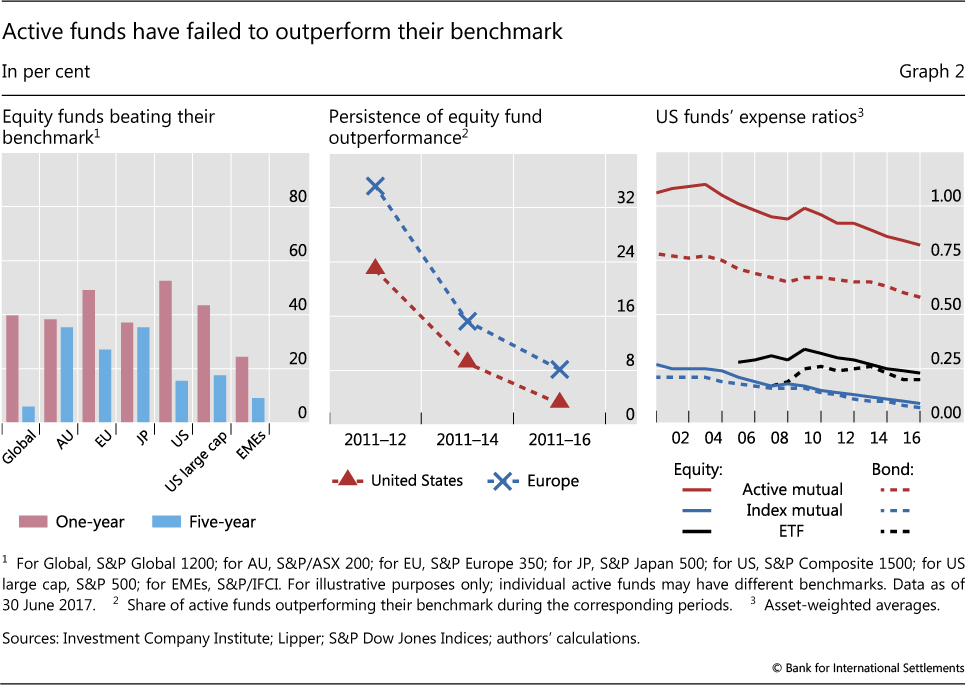

Various factors have contributed to the growing investor preference for passive funds in recent years. A key one has been the better performance record of passive funds over actively managed funds.

After fees and expenses, most active equity funds have failed to outperform the market benchmark in recent years (Graph 2, left-hand panel). Moreover, at least in major markets, funds that outperformed their benchmark have not done so consistently. For example, 35% of European equity funds outperformed during 2011-12, but only 8% outperformed over a longer horizon of six years (Graph 2, centre panel).

By and large, the findings of the empirical literature accord with recent experience; after fees and expenses, the average active equity fund underperforms the market portfolio over long horizons (eg Jenson (1968), Carhart (1997), Fama and French (2010), Busse et al (2014)). Although the literature is much less extensive, there are comparable findings of underperformance by active bond funds, on average, after adjusting for the riskiness of fund portfolios relative to the market benchmark (Blake et al (1993), Cici and Gibson (2012)).

The recent popularity of lower-cost passive funds has been supported by structural shifts in the financial advisory industry. These include: the rise of the so-called "robo advisors" (platforms offering low-fee automated investment management services); the introduction of fiduciary duty requirements; and a move away from commission-based remuneration. Regulators' greater focus on fee transparency has also played a role in some jurisdictions.6

The bulk of money flowing into passive funds over recent years has been directed to the largest fund managers, which tend to offer the lowest-cost funds. Since 2010, the three largest passive fund managers have received around 70% of cumulative inflows. This pattern of inflows can set in motion scale economies that help compress fees (Graph 2, right-hand panel).7 Greater fund size mechanically reduces funds' expense ratios and allows managers to further invest in cost reductions and new products, in turn helping them to attract more inflows. It also enables greater netting of inflows and outflows, as well as the negotiation of more favourable trading fees from brokers, thus reducing trading costs.

Greater use of information and computational technology is another factor underlying the development of the index industry and the rise of passive investing. There has been a marked expansion in the range of indices beyond traditional broad market benchmarks, opening up investment and diversification opportunities previously inaccessible to many investors.8

Lastly, the recent period of low volatility and associated high correlations within asset classes might have reduced the rewards to active security selection.

Implications for security pricing and issuers

The discussion in the previous two sections provided an individual-investor perspective on the rise of passive investing. The adoption of passive strategies by an increasing share of investors also has implications for security prices and issuers.

The efficiency of security price formation

Passive fund investment decisions are made at the portfolio level and not at the level of individual securities. Passive fund managers and investors naturally place emphasis on systematic (or common) factors affecting portfolio returns, such as expectations about monetary policy, inflation and other macroeconomic factors.

By contrast, passive portfolio managers have scant interest in the idiosyncratic attributes of individual securities in an index. They do not devote resources to seeking out and using security-specific information relevant for valuing individual securities. In effect, they free-ride on the efforts of active investors in this regard. Hence, an increase in the share of passive portfolios might reduce the amount of information embedded in prices, and contribute to pricing inefficiency and the misallocation of capital.9

An increase in passively managed portfolios could also affect the pricing of securities through greater portfolio-wide trading in the market. Passive managers buy and sell the entire basket of index constituents in response to fund inflows and outflows. This trading pattern can induce higher co-movement in the prices of the constituents of the index.10 It might also magnify any pricing differences with securities not included in the index (Wurgler (2010)).

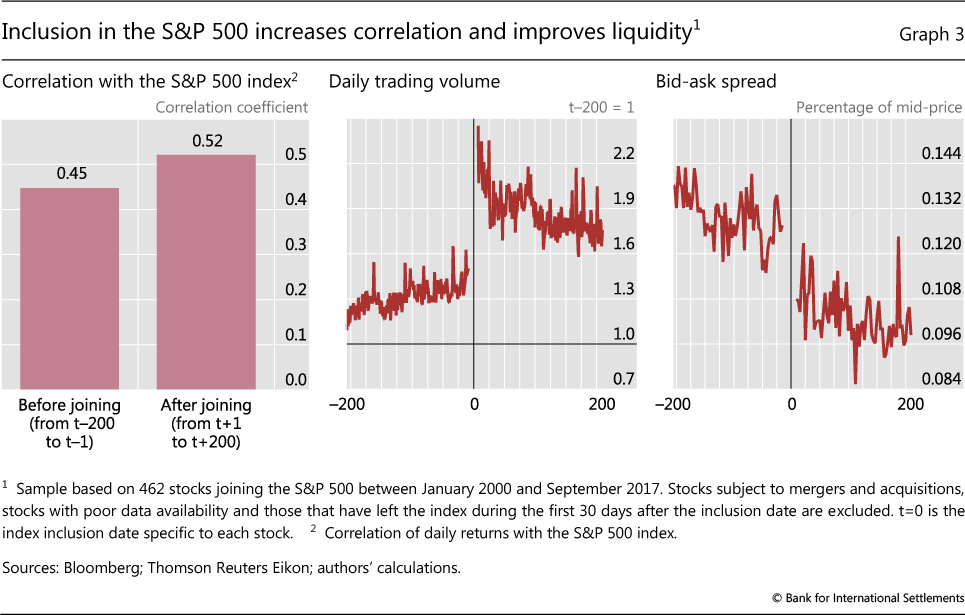

Numerous academic studies across a range of equity markets have identified co-movement, price pressures and other trading effects as securities are added to a benchmark index (eg Barberis et al (2005), Kaul et al (2002), Claessens and Yafen (2013)). Discernible effects are evident when individual stocks are included in the S&P 500 index: their correlation with the index increases, trading volume jumps and bid-ask spreads narrow (Graph 3). Research lends support to the view that index inclusion effects reflect "non-fundamental" investor demand shocks (Pruitt and Wei (1989), Greenwood (2008), Claessens and Yafen (2013)).11 The most obvious reason is the correlated behaviour of passive investors tracking an index, compounded by the behaviour of active investors that benchmark against an index. For ETFs specifically, there is recent evidence that trading and arbitrage activity contributes to the co-movement of S&P 500 stocks (Da and Shive (2018), Leippold et al (2016)).

It should be noted, however, that these effects also create counterbalancing forces. At some point, greater anomalies in individual security prices would be expected to increase the gains from informed analysis and active trading, and thus spur more active investment strategies.12 The ultimate balance between active and passive styles would depend on securities market characteristics, such as information costs, accessibility and overall market efficiency (Cremers et al (2016)). Thus, in markets that are already deep and efficient, the returns to active investors' information gathering should be relatively low and returns to scale from passive investing relatively high, all else equal. Evidence in support of this view might be found in the fact that passive funds have been able to secure a higher share of equity market capitalisation in advanced economies (AEs) than in EMEs (Table 1).

The perspective of security issuers

Going beyond the impact on the prices of individual securities, growth in passive funds might also influence the decisions and profile of security issuers.

A general consideration is that passive investing may alter the relationship between issuers and investors. By design, passive funds invest in all securities included in the index they track. Unlike active investors, they cannot express their disagreement with the decisions of individual issuers by selling their holdings. A higher share of passive investors could therefore weaken market discipline and alter the incentives of corporate and sovereign issuers to act in the interest of investors.13

Growth of passive bond funds, specifically, might encourage leverage by borrowers. Because inclusion in bond indices is based on the market value of outstanding bonds (that is, the face value of bond debt times its price), the largest issuers tend to more heavily represented in bond indices. As passive bond funds mechanically replicate the index weights in their portfolios, their growth will generate demand for the debt of the larger, and potentially more leveraged, issuers. From a financial stability perspective, there is a concern that this can act procyclically and encourage aggregate leverage. The analysis presented in Box A, which is based on a major global corporate bond index, suggests that passive bond funds do indeed obtain greater exposure to firm leverage than to firm size.

As passive funds grow, the mechanical trading impact of index inclusion or exclusion is likely to become more important for issuers. For instance, the higher the share of portfolios tracking an investment grade bond index, the larger the selling effect when a bond is removed from an index because of a credit rating downgrade.

Decisions around the country composition of indices can potentially have relatively large financial effects, given that they involve the combined weight of all securities from that country in the index. This is more so for smaller countries because the size of the fund asset base can be much larger than the underlying securities market. One example of a significant mechanical country trading effect is the reclassification in 2010 of Israel from emerging to developed market status by MSCI, an important provider of global benchmark equity indices. This reclassification resulted in about $2 billion of net equity fund outflows from Israel during the month in which the change came into effect. This occurred because Israel's new weight in the developed equities index was smaller than its previous weight in the emerging equities index, and the value of fund assets tracking these two indices was not very different (Raddatz et al (2017)). Reclassification could also result in spillovers to other countries if the country being removed (or added) has a large index weight, obliging index funds to rebalance their portfolios to accommodate the change.14

Box A

Corporate leverage and representation in a major bond index

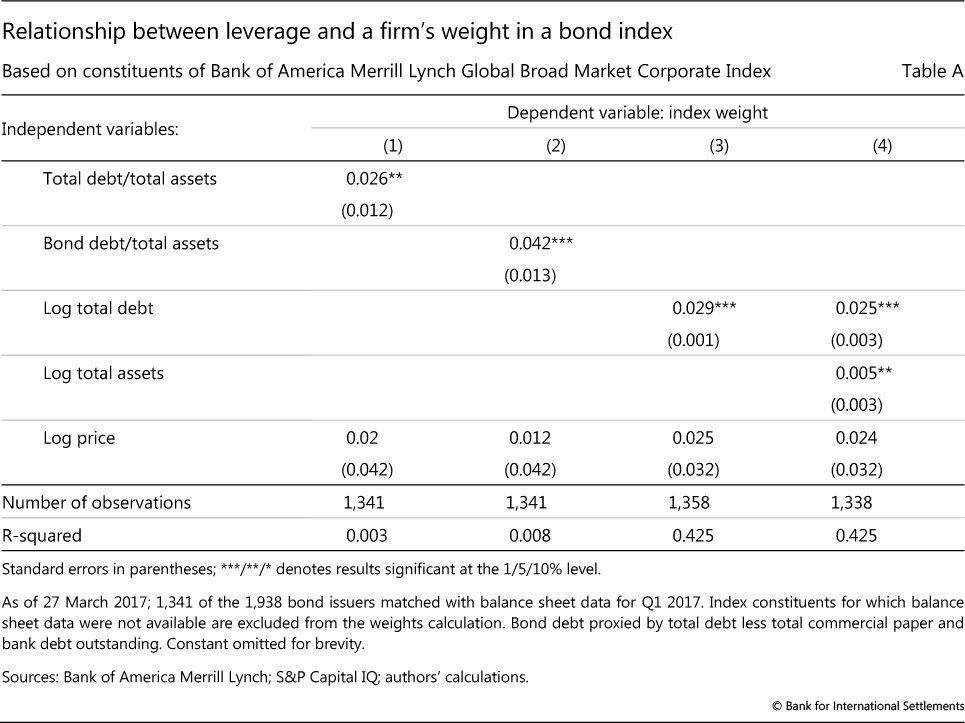

This box examines the relationship between a firm's leverage and its weight in a major corporate bond index, the Bank of America Merrill Lynch Global Broad Market Corporate Index. Data on corporate debt are matched with issuers in the index. A firm's weight in the index is then calculated as the sum of the market value of its individual bonds, divided by the market value for all issues where there is matching firm data.

Regression results confirm that there is a statistically significant positive relationship between a company's weight in the index and its leverage (based on either total debt or just bond debt; Table A, columns (1) and (2)), conditioned on the bond price. Although larger companies would be expected to have more outstanding debt, the coefficient on debt is about four times larger and more significant than the coefficient on total assets (column (4)). Specifically, a 1% increase in company debt is associated with a 0.025 percentage point increase in its weight in the index, compared with a 0.005 percentage point higher weight from a 1% increase in total assets.

Lack of data for some bond issuers could bias results if their leverage differs systematically from the average of the other issuers in the index. Since firm index weights are not normally distributed, we also run regressions using the log of the weight: the results are essentially the same.

Despite the above-mentioned concerns, the availability of benchmark indices may reduce issuance costs and improve issuance opportunities by supporting securities market development. For example, the development of a set of local currency bond indices in several major Asia-Pacific economies and the associated growth in passive funds have helped broaden and deepen Asian regional and local bond markets. Specific effects include the rise in bond issuance, increased market liquidity, institutional investors' greater participation, and lower barriers to non-resident investors (Chan et al (2012)).

Fund flows and aggregate price dynamics

The growth in passively managed portfolios also has implications for security price dynamics. A key question is whether passive funds have a stabilising or destabilising influence on aggregate prices.

Passive fund managers could exert a stabilising influence on prices in the absence of fund inflows and outflows. By design, the value of passive portfolios automatically rebalances in line with the index, and passive fund managers do not need to trade unless they receive investment or redemption orders from investors. In contrast, active fund managers have the discretion to adjust portfolio allocations in response to market events. For these reasons, passive funds might provide an offsetting force to any procyclical investment decisions of active funds.

On the other hand, passive funds could conceivably contribute to price overshooting if their fund flows are sizeable. As indices are typically weighted according to market values, the share of overvalued stocks or bonds in them tends to increase in a rising market and decline in a falling market (CGFS (2003)). Large flows into and out of passive funds could exacerbate these investment trends.

Given these considerations, the impact of passive fund growth on aggregate price dynamics will depend on two sets of factors. The first is how passive investment vehicles influence end investor fund flows. The stickiness of investor flows in times of market stress is an important aspect of this issue. The second is the strength of transmission from investor flows and trading to security prices. In assessing these factors, it is important to distinguish between the different types of passive funds, index mutual funds and ETFs, as their structures will have different implications.

Investor behaviour and fund flows

There are several reasons why index-tracking funds may be used by investors that themselves behave in a stable (or "passive") way with respect to their investments. For one, passive funds appear to be optimal vehicles for "buy-and-hold" investors seeking to minimise trading costs and fees. Second, the trading activity of some institutional investors, such as pension funds, can be limited by rigid asset allocation mandates and tax efficiency objectives. Third, the absence of fund manager discretion might make some investors less likely to shift their money in and out of the fund in response to fund performance.

At the same time, the unique structures of ETFs might allow, or even encourage, less stable investment behaviour by owners of these products. ETFs enable investors to trade index portfolios on an intraday basis at a transparent secondary market price. This contrasts with mutual funds, where trading usually occurs at the close of the trading day (Box B). The ability to trade ETFs frequently could attract high-turnover investors and investors pursuing shorter-term investment strategies, such as high-frequency trading (HFT) or dynamic market hedging. Based on this, one might expect ETF flows to be more volatile compared with those of index mutual funds.15

Box B

Trading mechanisms of ETFs compared with other fund types

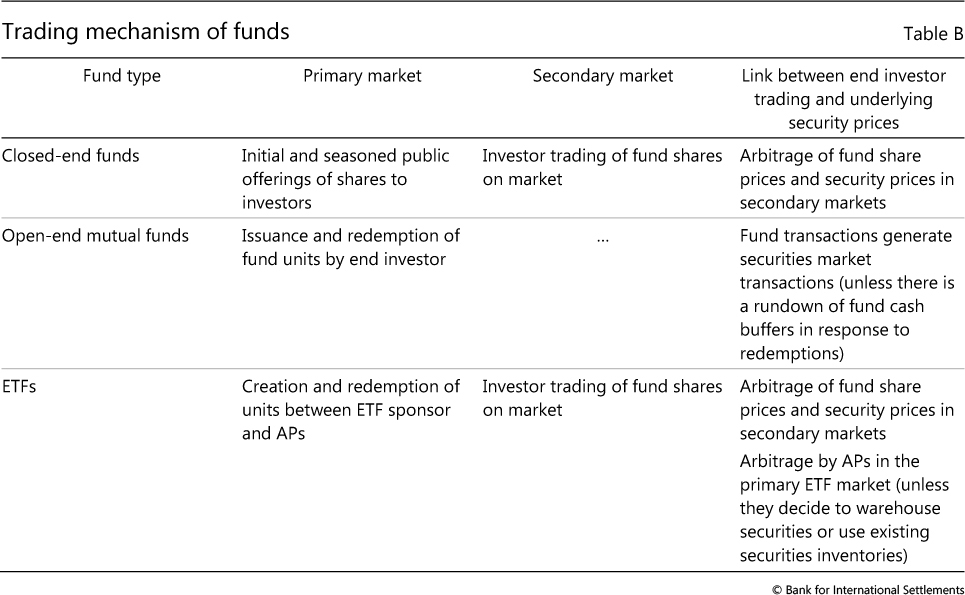

Like passive (index) mutual funds, exchange-traded funds (ETFs) seek to track the returns of a benchmark index. The key innovation of ETFs is a trading process that combines the characteristics of open-end mutual funds with those of closed-end funds. Variation in the number of ETF units arising from inflows or redemptions resembles the design of open-end mutual funds, while the ability to trade ETF shares throughout the day on a secondary market at a transparent price is a feature shared with closed-end funds. Trading of ETF shares on an exchange also allows market participants to place market, limit or stop orders, as well as to engage in short selling, which further boosts the ETFs' market liquidity.

ETFs' unique primary-secondary market trading mechanism is facilitated by registered intermediaries known as authorised participants (APs), typically broker-dealers or market-makers in the underlying securities. APs may trade the ETF shares on the secondary market like other investors, but they can also create and redeem ETF shares (known as "creation units") through direct transactions with the ETF sponsor at the current net asset value of the portfolio. The ability of APs to transact in both the primary and the secondary market incentivises profitable arbitrage of the ETF share price and the underlying assets. This, together with arbitrage by other market participants solely in the secondary market, underpins a key value proposition of ETFs for investors - near-immediate liquidity at a share price close to the value of assets underlying the price index. This can be contrasted with open-end mutual funds, where investors buy or redeem units directly at the fund's end-of-day net asset value.

For example, in the case of a material decline in the price of ETF shares below the value of the underlying assets, APs could purchase ETF shares and redeem these with the ETF sponsor in exchange for the underlying securities, which they then may sell on the market.

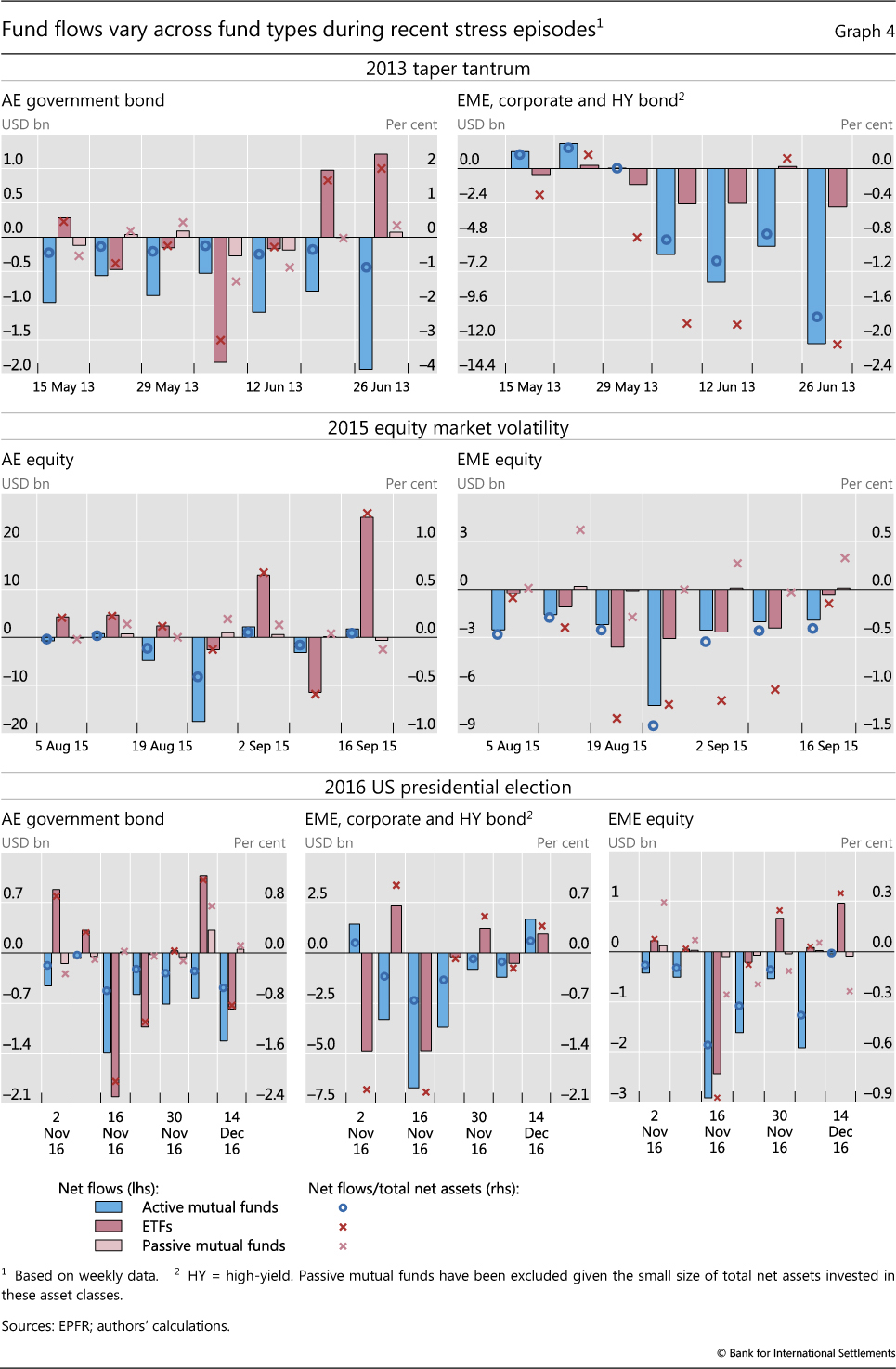

An analysis of recent stress episodes compares the stability of fund flows across passive fund types (index mutual funds and ETFs) and active mutual funds. We focus on three recent periods of stress: the 2013 taper tantrum (bond funds only); the 2015 bout of equity market turbulence (equity funds only); and the turbulence surrounding the 2016 US presidential election (bond funds and EME equity funds).16 Graph 4 shows weekly net flows for active mutual funds, passive mutual funds and ETFs in US dollar terms (absolute flows) on the left-hand scale, and net flows as a percentage of total assets (relative flows) on the right-hand scale.

Several patterns stand out. First, passive mutual funds' flows were the least volatile, in both absolute and relative terms, compared with those of both ETFs and active mutual funds. On this basis, index mutual fund investors do not appear to "rush for the exit" in times of stress.

Second, ETFs exhibited the largest inflows and outflows (ie fund flow volatility) relative to their asset size, although in some cases their flows offset each other over the weeks within an episode. The fact that fund flows were more volatile for ETFs than for passive mutual funds (and even active mutual funds in some instances) is consistent with ETFs being associated more with a wider array of investment and trading strategies.

Third, compared with both index mutual funds and ETFs, active mutual funds exhibited the most persistent outflows across asset classes in all three episodes. This tallies with well known active mutual fund procyclical effects arising from investor sensitivity to poor fund performance, as well as fund managers' discretionary sales (Shek et al (2018)).17 Active mutual fund flows also tend to be largest in terms of absolute dollar amounts, reflecting the sheer size of the assets managed by those funds.

Fund flows and trading in underlying securities

Variation in fund flow patterns during recent stress episodes points to a differential impact on securities market prices across fund types.

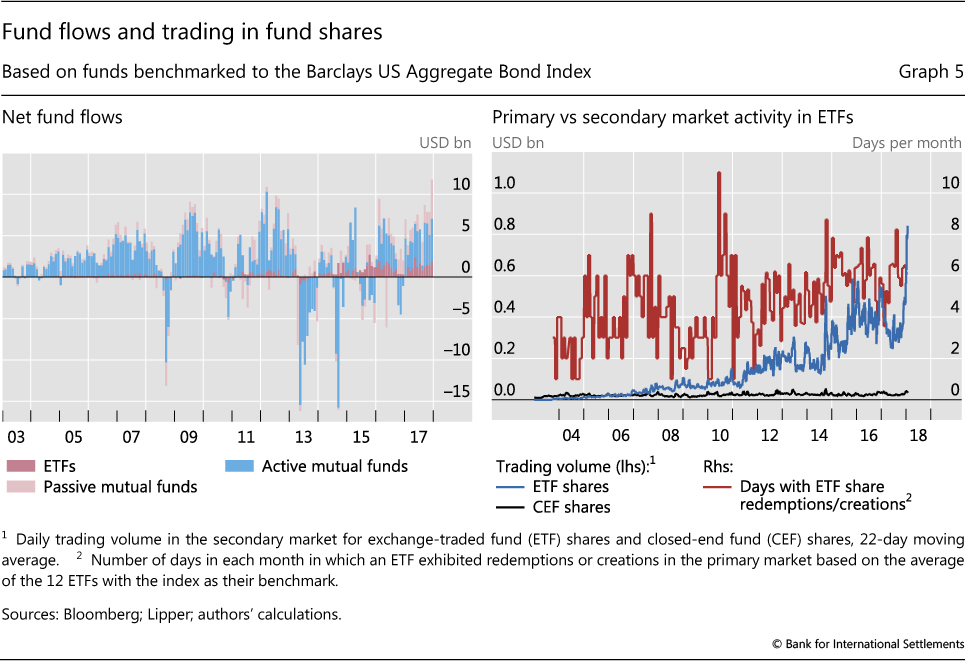

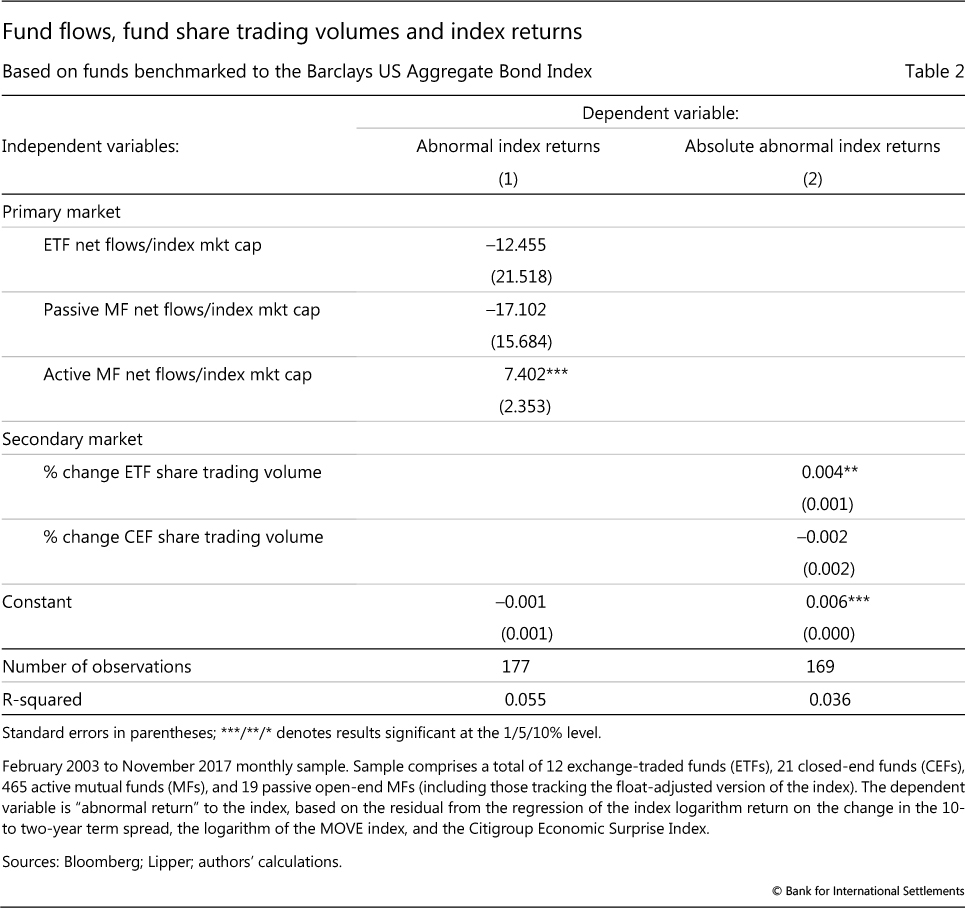

An examination of mutual funds and ETFs benchmarked to a major advanced economy bond index provides some evidence on the link between fund flows and security prices.18 Given their large size, active mutual fund flows should be important for the price dynamics of this index (Graph 5, left-hand panel). This is confirmed by the significant relationship of active mutual fund flows with the "abnormal returns" to the index - the component of index returns not explained by fundamental drivers (Table 2, column (1)).19 The regression results do not show a similar relationship for either index mutual fund or ETF flows.

The direct link between security prices and the flows of active mutual funds may also arise from the fact that mutual fund investors transact directly with the fund, which, in turn, trades directly in the underlying securities. For this reason, the buying or selling of fund shares by investors should be expected to result in the buying or selling of the underlying securities by the fund manager.20

By contrast, ETF investors trade fund shares in the secondary market with each other (similar to investors in closed-end funds). As a consequence, market-clearing prices in the secondary market will adjust to any demand/supply imbalances for ETF shares. In such a setting, the pass-through to the prices of the underlying securities will depend on arbitrage activity by various players in the secondary market for ETFs and in the underlying securities market - that is, investors taking long and short positions in the ETF shares and underlying securities portfolio. The importance of secondary market trading in ETFs for aggregate prices is confirmed by the result of a regression of the absolute value of the abnormal bond index return on ETF share trading volume (Table 2, column (2)).

Direct transactions with an ETF (ie fund flows) may be undertaken only by so-called authorised participants (APs; Box B), which can operate in both the primary and the secondary ETF market. But such ETF share creation and redemption appears to be fairly infrequent (Graph 5, right-hand panel). This is consistent with evidence that the vast bulk of ETF trading across various equity and bond classes clears in the secondary market (ICI (2015)). In addition, in the case of ETFs, the fund does not transact directly in the underlying securities, but rather relies on the AP. This too could dampen the effects of fund flows on securities markets. For example, after redeeming the ETF shares, APs can potentially warehouse the securities instead of immediately selling them in the secondary market (Box B, Table B). These two factors may help explain why ETF flows may have less of an impact on security prices than do active mutual funds flows.

In sum, the above analysis suggests that while active mutual fund flows have a direct impact on prices, ETF investor trading exerts a greater impact on underlying asset prices by generating the conditions for secondary market arbitrage.

Conclusion

The implications of the rapid expansion of passively managed funds have been hotly debated. At this point, the relatively small share of passive fund portfolios in total securities market holdings suggests that any effect on security prices and issuers may not be large. However, the effects could become significant if the passive fund management industry continues to expand.

This special feature discusses a number of possible securities market effects that warrant further consideration. Three issues are worth highlighting. First, it seems plausible that the portfolio-wide investing and trading of passive funds could bring about greater correlation of index securities and reduce the security-specific information contained in prices. Second, at an aggregate level, fund flow dynamics may change. In this respect, we observe that investors in index mutual funds exhibited a stabilising influence in recent stress episodes relative to active mutual funds. ETF flows were more volatile, in line with investors' ability to frequently trade these products. Third, the link between ETF trading and underlying security prices deserves further study. In particular, secondary market arbitrage of ETF shares appears to constitute an additional (and potentially more important) transmission channel to prices compared with that which works through fund flows.

References

Barberis, N, A Schleifer and J Wurgler (2005): "Comovement", Journal of Financial Economics, vol 75, no 2, pp 283-317.

Blackrock (2017): "Index investing supports vibrant capital markets", Viewpoints.

Blake, C, E Elton and M Gruber (1993): "The performance of bond mutual funds", The Journal of Business, vol 66, no 3, pp 370-403.

Busse, J, A Goyal and S Wahal (2014): "Investing in a global world", Review of Finance, vol 18, issue 2, April, pp 561-90.

Carhart, M (1997): "On persistence in mutual fund performance", The Journal of Finance, vol 52, no 1, pp 57-82.

Chan, E, M Chui, F Packer and E Remolona (2012): "Local currency bond markets and the Asian Bond Fund 2 initiative", BIS Papers, no 63, January.

Chernenko, S and A Sunderam (2016): "Liquidity transformation in asset management: evidence from the cash holdings of mutual funds", NBER Working Papers, no 22391.

Cici, G and S Gibson (2012): "The performance of corporate bond mutual funds: evidence based on security-level holdings", Journal of Financial and Quantitative Analysis, vol 47, no 1, pp 159-78.

Claessens, S and Y Yafen (2013): "Comovement of newly added stocks with national market indices: Evidence from around the world", Review of Finance, vol 17, issue 1, January, pp 203-27.

Committee on the Global Financial System (2003): "Incentive structures in institutional asset management and their implications for financial markets", CGFS Papers, no 21, March.

Cremers, M, M Ferreira, P Matos and L Starks (2016): "Indexing and active fund management: international evidence", Journal of Financial Economics, 120 (2016), February, pp 539-60.

Da, Z and S Shive (2018): "Exchange traded funds and asset return correlations", European Financial Management, vol 24, no 1, pp 136-68.

Fama, E and K French (2010): "Luck versus skill in the cross-section of mutual fund returns", The Journal of Finance, vol 65, no 5, pp 1915-47.

Fender, I (2003): "Institutional asset managers: industry trends, incentives and implications for market efficiency", BIS Quarterly Review, September, pp 75-86.

Feroli, M, A Kashyap, K Schoenholtz and H S Shin (2014): "Market tantrums and monetary policy", Chicago Booth Papers, no 14-09.

Fueda-Samikawa, I and T Takano (2017): "BOJ's ETF purchases expanding steadily - how long will the BOJ hold risky assets with no maturity?", Japan Center for Economic Research, July.

Goldstein, I, H Jiang and D Ng (2017): "Investor flows and fragility in corporate bond funds", Journal of Financial Economics, vol 126, no 3, pp 592-613.

Greenwood, R (2008): "Excess comovement and stock returns: evidence from cross-sectional variation in Nikkei 225 weights", Review of Financial Studies, vol 21, pp 1153-86.

Grossman, S and J Stiglitz (1980): "On the impossibility of informationally efficient markets", American Economic Review, vol 70, pp 393-408.

Investment Company Institute (2015): "The role and activities of authorized participants of exchange-traded funds", ICI Publications, March.

Jenson, M (1968): "The performance of mutual funds in the period 1945-1964", Journal of Finance, vol 23, pp 389-416.

Jung, J and R Shiller (2005): "Samuelson's dictum and the stock market", Economic Inquiry, vol 43, no 2, pp 221-8.

Kaul, A, V Mehrotra and R Morck (2002): "Demand curves for stocks do slope down: new evidence from an index weights adjustment", Journal of Finance, vol 55, pp 893-912.

Leippold, M, L Su and A Ziegler (2016): "How index futures and ETFs affect stock return correlations", University of Zurich working paper.

Malkiel, B (2003): "Passive investment strategies and efficient markets", European Financial Management, vol 9, no 1, pp 1-10.

Miyajima, K and I Shim (2014): "Asset managers in emerging market economies", BIS Quarterly Review, September, pp 19-34.

Morris, S, I Shim and H S Shin (2017): "Redemption risk and cash hoarding by asset managers", Journal of Monetary Economics, vol 89, pp 71-87.

Pedersen, L (2018): "Sharpening the arithmetic of active management", Financial Analysts Journal, 1-16, available online.

Pruitt, S and J Wei (1989): "Institutional ownership and changes in the S&P 500", The Journal of Finance, vol 44, no 2, June, pp 509-13.

Raddatz, C, S Schmukler and T Williams (2017): "International asset allocations and capital flows: the benchmark effect", Journal of International Economics, vol 108, pp 413-30.

Samuelson, P (1998): "Summing up on business cycles: opening address", in Beyond shocks: what causes business cycles, Federal Reserve Bank of Boston.

Sharpe, W (1991): "The arithmetic of active management", Financial Analysts Journal, no 47, vol 1, pp 7-9.

Shek, J, I Shim and H S Shin (2018): "Investor redemptions and fund manager sales or emerging market bonds: how are they related?", Review of Finance, vol 22, issue 1, February, pp 207-41.

Sushko, V and G Turner (2018): "What risks do exchange-traded funds pose?", Bank of France, Financial Stability Review, forthcoming.

Vayanos, D and P Woolley (2016): "The curse of the benchmarks", Paul Woolley Centre Financial Markets Group Discussion Papers, no 747, March.

Wurgler, J (2010): "On the economic consequences of index-linked investing", NBER Working Papers, no 16376, September.

1 This special feature draws on material prepared for the Committee on the Global Financial System in consultation with Kevin Henry (Federal Reserve Bank of New York), Fuminori Niwa (Bank of Japan), Edith Siermann (Netherlands Bank) and Jonathan Witmer (Bank of Canada). The authors also thank Claudio Borio, Benjamin Cohen, Stijn Claessens, Hyun Song Shin and Kostas Tsatsaronis for valuable comments, and Giulio Cornelli and Tania Romero for excellent research assistance. The views expressed are those of the authors and do not necessarily reflect those of the BIS.

2 Indeed, it is important to emphasise that the "passive" or "active" designation refers to the investment approach of the fund manager that acts as an agent for end investors. The investment strategies of end investors can differ from that of the fund manager. As a result, there may be significant variation in the stability of balances across investors in a given passive or active fund.

3 Around 2% of total ETF assets do not seek to track an index, but rather offer investors an active investment strategy designed to deliver absolute returns or high returns relative to a benchmark. Given the small share of active ETFs, we treat all ETFs as passive funds in this special feature.

4 The Bank of Japan holds approximately 60% of outstanding Japanese equity ETFs as part of its asset purchase programme (Fueda-Samikawa and Takano (2017)), while the share of the Government Pension Investment Fund (GPIF) equity investment allocation to passive investment vehicles exceeded 80% by 2016, according to published GPIF data.

5 There are several versions of the efficient markets hypothesis that differ in the strength of their assumptions around "all available information". The relevant version here is the semi-strong form, which states that the stock price includes all publicly available information regarding the prospects of the firm issuing it.

6 A recent example is the transparency-driven regulations embodied within the Markets in Financial Instruments Directive (MiFID) II that came into effect in the European Union in January of this year.

7 Active funds' expense ratios have also been declining in recent years, at least in the United States.

8 The proliferation of indices is evident in the fact that, as of early February 2018, around 350,000 equity indices and 80,000 bond indices were covered by Thomson Reuters Datastream.

9 It is possible that a rise in passive investing could lead to more resources being devoted to market-wide pricing factors. But efficiency might still deteriorate; there is an argument that pricing is less efficient for the market as a whole than for individual securities (Samuelson (1998)). Jung and Shiller (2005) provide supporting evidence, showing that individual US firms' price/dividend ratios have predictive power for future growth rates in real dividends, but when the firms are aggregated into an index the predictive power disappears or obtains a wrong sign.

10 Greater co-movement of securities in an index implies a reduction in the potential benefit of holding the diversified portfolio.

11 A different interpretation of the price pressures and increased stock co-movement is that they reflect better diffusion of available information (Barberis et al (2005)). For example, common return factors may be more quickly incorporated into prices given lower trading costs and higher liquidity for securities included in indices. In this case, greater passive investing would not reduce pricing efficiency.

12 The need for incentives to informed active investing underpins the argument of Grossman and Stiglitz (1980) that markets are likely to be mostly, but not completely, efficient.

13 Of course, there are potentially other ways in which passive funds can influence issuer behaviour, such as through their voting on board composition and executive remuneration. Concentration among passive fund providers might be a factor increasing the influence of individual passive funds.

14 Raddatz et al (2017) also examine the impact of the removal of Qatar and the United Arab Emirates from the MSCI Frontier Markets Index in 2014. These two countries together represented 40% of that index, so their removal resulted in large passive equity fund inflows to the smaller remaining countries, as their portfolio weights rose.

15 While not the focus of this article, ETF flow volatility could also stem from investor expectations of high liquidity and a possible impairment of authorised participant intermediation in times of stress. For a discussion of this issue and other risks posed by ETFs, see Sushko and Turner (2018).

16 The period May-June 2013 was characterised by a broad decline in fixed income markets as investors responded to expectations of monetary policy tightening by the US Federal Reserve. In August 2015, global equity markets experienced falling prices and bouts of volatility as investors focused on growing EME vulnerabilities following a plunge in China's equity prices. November 2016 was characterised by a sell-off in fixed income and EME assets as investors revised their expectations following the outcome of the US presidential election. For an overview of market developments during these episodes, see, for example, the Overview chapter in the September 2013, September 2015 and December 2016 issues of the BIS Quarterly Review.

17 Because investor redemptions from mutual funds affect the next-period net asset value of remaining investors' holdings, they can create a first-mover advantage. This effect is more pressing for less liquid asset classes, such as corporate bond funds (Goldstein et al (2017)). Feroli et al (2014) find evidence of such feedback outflows by fixed income mutual fund investors during the 2013 taper tantrum, when global bond markets were unusually turbulent.

18 We focus on the Barclays US Aggregate Bond Index, which is shown to have been the advanced economy bond benchmark most widely used by fund managers (Miyajima and Shim (2014)). The index represents about 8,200 fixed income securities with a total value of about $20 trillion, or more than 40% of the total US bond market.

19 The dependent variable is the "abnormal return" on the index, defined as the residual from the regression of the index log return on the change in the 10- to two-year term spread, the log of the MOVE index (a measure of bond market volatility) and the Citigroup Economic Surprise Index.

20 Although funds could meet redemptions by first drawing on any cash (or liquid asset) buffers, studies conclude that cash holdings of mutual funds are not sufficiently large to mitigate the price impact of fund flows (eg Chernenko and Sunderam (2016)). There is also evidence that fund managers increase cash hoarding in response to redemptions, which would amplify fire sales (Morris et al (2017)).