Can CCPs reduce repo market inefficiencies?

(Extract from pages 13-14 of BIS Quarterly Review, December 2017)

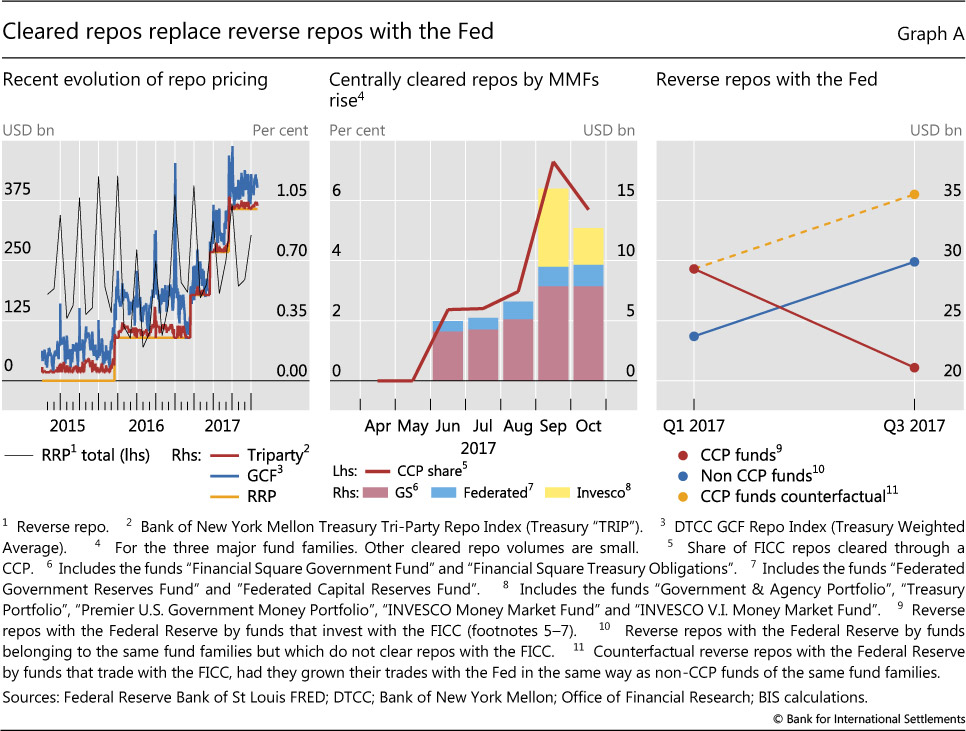

Repo markets have taken on an increasingly important role in global money markets since the Great Financial Crisis as unsecured borrowing has dwindled. But repo markets remain segmented. In the United States, there has been a persistent spread between general collateral financing (GCF) and triparty repo rates. Ultimate borrowers that cannot access the triparty market face higher costs. Money market funds (MMFs) that cannot access the delivery-versus-payment (DvP) or GCF markets to lend cash increase their take-up of the Federal Reserve's overnight reverse repurchase (ON RRP) facility, which pays a lower rate. Moreover, the retreat of dealers from repo markets at quarter-ends generates spikes in both prices and volumes: both GCF rates and the take-up of repos by MMFs under the ON RRP increase at quarter-ends (Graph A, left-hand panel).

Against this background, an important recent development is a rule change by The Depository Trust & Clearing Corporation (DTCC), approved by the Securities and Exchange Commission in May. This change allows DTCC's subsidiary, the Fixed Income Clearing Corporation (FICC), to expand the availability of clearing in the repo market to a broader set of institutional investors. Through this rule change, MMFs can provide cash or securities in the DvP markets through a dealer sponsor.

Some MMFs have already started clearing repos through the FICC. The total amount of centrally cleared repos stood at $13 billion at end-October 2017 (Graph A, centre panel). The volumes are still small compared with the total volumes in the triparty market or even compared with other funds belonging to the same fund family. But they have been growing rapidly. Centrally cleared repos made up close to 6% of the total repo volumes of the three fund families that cleared repos through the FICC in October 2017.

The initial response by the MMFs that clear repos through the FICC suggests that central clearing could potentially reduce market segmentation. There are already signs of convergence of prices, as centrally cleared repo trades earned up to 12 basis points more than the triparty rate index. Furthermore, funds that cleared trades through the FICC reduced their end-of-quarter take-up of the ON RRP compared with their peer funds (Graph A, right-hand panel). If these funds had instead increased their reverse repos with the Fed at the same rate as their peers, Fed RRPs at end-September 2017 would have been around $35 billion instead of the actual and much lower volume of $21 billion.

Furthermore, funds that cleared trades through the FICC reduced their end-of-quarter take-up of the ON RRP compared with their peer funds (Graph A, right-hand panel). If these funds had instead increased their reverse repos with the Fed at the same rate as their peers, Fed RRPs at end-September 2017 would have been around $35 billion instead of the actual and much lower volume of $21 billion.

Source: SEC N-MFP filings.