Debt weighted exchange rate indices

(Extract from pages 100-102 of BIS Quarterly Review, December 2016)

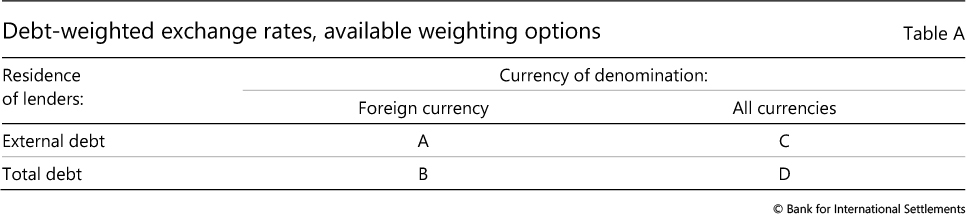

There are several possible ways of calculating debt-weighted exchange rate (DWER) indices, depending on what measure of debt is used to weight bilateral exchange rates. More concretely, the debt measure could vary along two main dimensions: the currency of denomination and the residence of lenders (Table A).

The first possible debt measure is foreign currency-denominated external debt (cell A in Table A). This is the narrowest of the four possible measures. It does not take into account the importance of external debt in total debt and the importance of domestic currency debt in external debt. Consequently, for countries whose foreign currency-denominated external debt is a modest share of total debt (eg the United States), even large swings of the index would have a minor impact on domestic financial conditions.

The second potential debt measure is total foreign currency-denominated debt (cell B in Table A). This is a more complete measure than the one in cell A since it incorporates local debt denominated in foreign currencies. That said, it still suffers from the problem that total foreign currency debt could be a relatively small share of total debt for certain economies (eg China).

The third possible debt measure is external debt denominated in all currencies (cell C in Table A). This measure, which is conceptually very close to the one constructed by Bénétrix et al (2015), is more complete than the one in cell B since it also incorporates information on external debt denominated in the local currency of the borrowing country. Nevertheless, it ignores any local debt, including local debt denominated in foreign currencies. Therefore, it could provide a misleading picture for countries in which a large portion of the domestic debt is denominated in foreign currencies (eg the Czech Republic, Hungary and Poland).

The final potential debt measure is total debt denominated in all currencies (cell D in Table A). This is the most comprehensive of the four measures since it includes total debt and a weight is given to debt in domestic currencies. Nevertheless, this measure tends to be too broad for addressing a large number of questions. For example, the value of the index is likely to be very close to 1 for countries in which the share of domestic debt in domestic currency is large (eg China). In theory, the "total debt" used for the construction of DWER indices should encompass the debt of only those entities that can actually choose their financing currency. In practice, however, this perimeter is not easily identifiable.

We opt to construct our benchmark DWER indices using the weights based on foreign currency-denominated total debt (ie cell B in Table A). While none of the above four measures is perfect, we select that particular one because it strikes the optimal balance between conceptual comprehensiveness and computability. Furthermore, it is the most direct counterpart to the trade-weighted exchange rate (NEER and REER) indices that are typically used in the existing empirical literature. That is, it captures the distribution of the foreign currency components of total debt (regardless of how large foreign currency debt is relative to debt in all currencies) in the same way that trade-weighted exchange rate indices capture the distribution of the foreign trade component of GDP (regardless of how large foreign trade is relative to GDP).

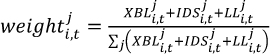

In more concrete terms, the DWER that we construct for each country is the geometric average of its bilateral exchange rates against each of the five major global funding currencies (US dollar, euro, Japanese yen, pound sterling and Swiss franc), weighted by the shares of these global funding currencies in that country's foreign currency debt. The weight of currency j at quarter t in the DWER index for country i is calculated using the following formula:

where: XBL = cross-border loans to non-banks denominated in foreign currencies (BIS LBS data)

data)

IDS = international debt securities statistics denominated in foreign currencies, issued by non-banks (BIS IDSS data)

data)

LL = local loans to non-banks denominated in foreign currencies (BIS LBS data)

Weights are calculated on a quarterly basis. For all days in a quarter, the end-of-quarter weights of the preceding quarter are applied (eg using end-Q3 2015 weights for all days in Q4 2015). When one of the five currencies is the home currency of a given country (eg the yen in Japan), only the remaining four currencies are used to calculate the DWER weights for the respective country. For countries that joined the euro after the currency's launch, the euro is treated as a foreign currency until the quarter in which the country joined the euro. For example, in the case of Estonia, the euro is treated as a foreign currency until Q1 2011.

The XBL and the LL series are taken directly from the BIS locational banking statistics (LBS). The IDS series are taken directly from the BIS international debt securities statistics data. When not available, we use one of the three following estimates:

- For countries which do not report data to the BIS LBS, local loans in foreign currency j are proxied by cross-border loans denominated in currency j to banks in the respective country. Since the United States does not report local loans in foreign currencies, this estimate is used for the United States as well.

- For countries that started reporting local loans in foreign currency after the sample period started, LL in currency j are proxied by multiplying cross-border loans to banks (in currency j) by the maximum of 1 and the average of the ratio of reported local claims on non-banks to cross-border claims on banks for the first eight reported quarters. When the ratio exceeds 1, the new-reporter estimate follows the same methodology as that of the non-reporter estimate.

- For China, local loans in foreign currencies are taken from national data and are assumed to comprise 80% USD, 10% EUR, 10% JPY, 0% GBP and 0% CHF, following a methodology similar to the one used by McCauley et al (2015).

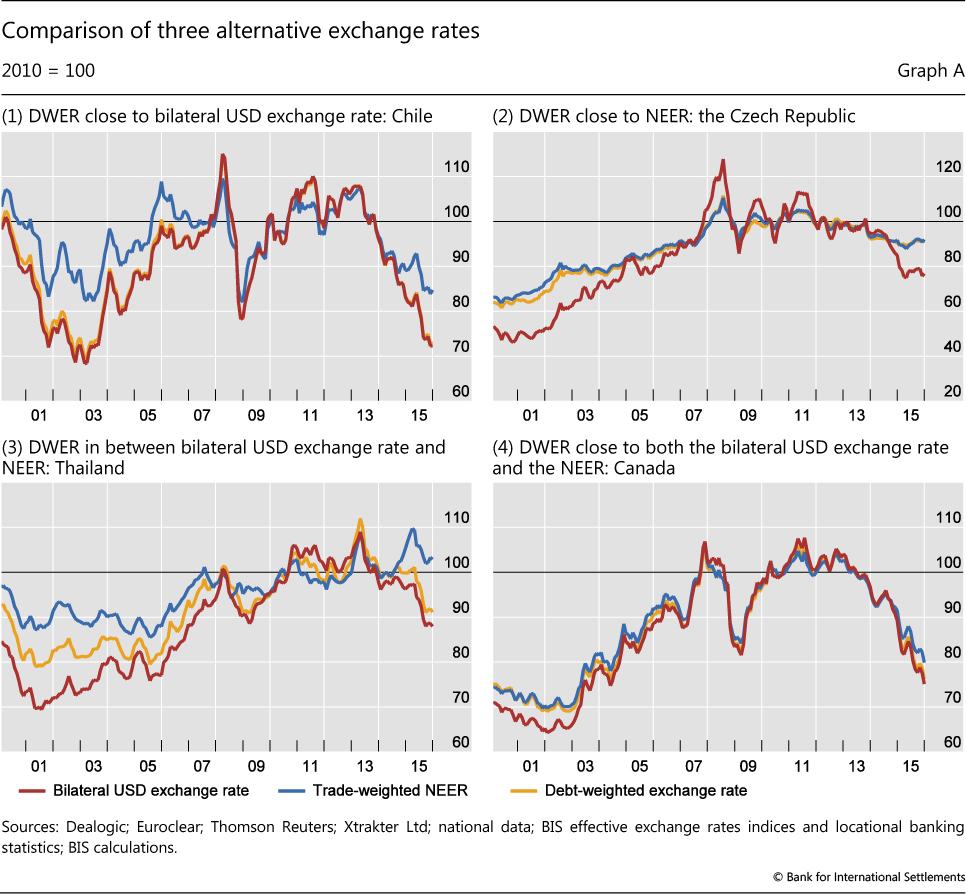

The 61 countries for which debt-weighted exchange rate indices were calculated can be roughly split into four groups:

1. Countries for which the DWER closely follows the bilateral US dollar exchange rate. This is, for example, the case for most Latin American countries, as illustrated by Chile in the upper left-hand panel of Graph A above. About 25% of the countries in the sample fall in this category.

2. Countries for which the DWER and the trade-weighted NEER index (as measured by the BIS effective exchange rate indices) are very similar. This is the case for several emerging European countries, as can be seen for the Czech Republic in the upper right-hand panel of Graph A, but is not very common in general (less than 10% of the sample falls into this category).

3. Countries for which the DWER falls between the bilateral US dollar exchange rate and the trade-weighted index. This is the case for more than half of the countries in the sample and is most prominent among euro area countries and several countries in emerging Asia. An example is Thailand, whose exchange rate is shown in the lower left-hand panel of Graph A.

4. Countries for which the DWER, the bilateral US dollar exchange rate and the trade-weighted NEER index are virtually the same, which is the case for slightly more than 10% of the sample. Often this involves countries that trade heavily with the United States, as Canada illustrates in the bottom right-hand panel of Graph A (the average trade weight of the United States in the NEER index for Canada was 62.6% between 1999 and 2013).

BIS locational banking statistics. BIS international debt securities statistics.