NDF trading during the August 2015 renminbi volatility

(Extract from page 90 of BIS Quarterly Review, December 2016)

Using DTCC and Triennial data, this box explores how renminbi market developments in August 2015 spilled over into emerging FX markets. This analysis using newly available turnover data sheds new light on international spillovers from China's currency markets, heretofore identified through prices (Shu et al (2016)).

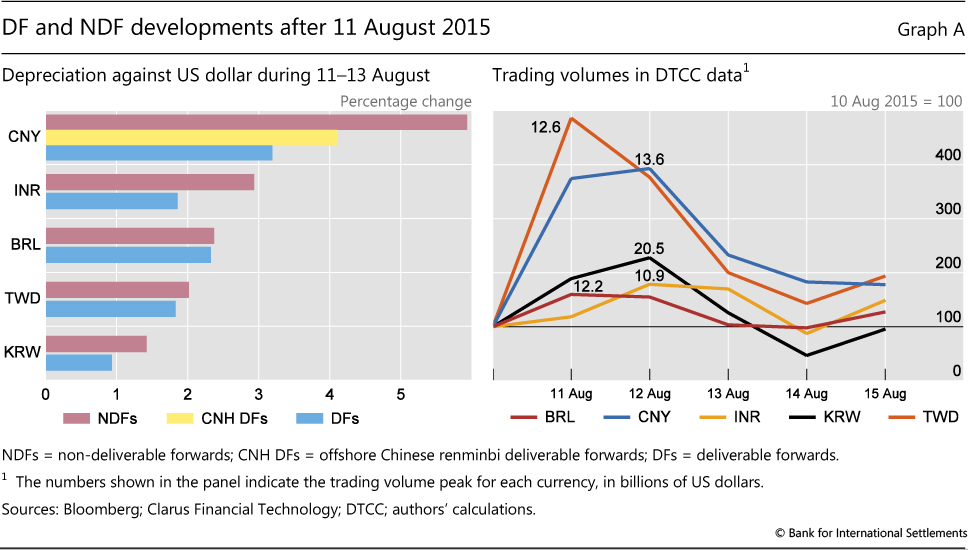

On 11-12 August 2015, the renminbi daily fixing was set successively 1.9% and then 1.6% lower than the previous day, and fears of a steep CNY depreciation led to widespread pressure on forwards of EME currencies (Graph A, left-hand panel). The INR three-month NDF and DF depreciated by 2.9% and 1.9% against the US dollar, respectively, in three days. The BRL DF and NDF both depreciated by 2.3-2.4%. The Korean won and New Taiwan dollar depreciated less, but, like the rupee, moves were larger for NDFs than DFs. These two currencies' NDF rates switched from implying a smaller depreciation than their DF counterparts before 11 August, to a greater depreciation after.

The volume response was bigger in the currencies of China's neighbouring economies. The DTCC data show that KRW and TWD NDF trading involving US counterparties saw larger rises in volumes, even though the INR and BRL rates depreciated more (Graph A, right-hand panel). On 11 August, renminbi NDF trading almost quadrupled to $13 billion. Given the ratio of DTCC turnover to global turnover in April, this implies around $40 billion in global CNY NDF turnover, four times the April 2016 level. CNY NDF turnover rose further on the following day before falling back. TWD NDF trading surged even more on 11 August, to 486% of the previous day's volume, or an estimated 3.7 times the April volume. While KRW NDF turnover only doubled, its increase of $10 billion was the largest response of the five currencies. In terms of volume, the responses of the INR and BRL NDFs were the smallest. Similar increases in NDF trading occurred during a bout of CNY turbulence in January 2016. On this evidence, it appears that, even though the CNY NDF turnover is fading, renminbi developments are boosting Asian NDFs.

Observations for three countries with daily data on domestic trading suggest that the NDF's share of trading increased in China and India in this episode, but not in Brazil. For the renminbi, the daily onshore spot trading through the China Foreign Exchange Trade System (CFETS) rose by 50% on average in the five days after 11 August, a modest increase compared with that of NDF trading registered with the DTCC. On 11 August when NDF trading peaked, the ratio of NDF trading in DTCC data to onshore spot trading (CFETS) rose to 50%, well above the ratio of 42% for the global NDF trading to onshore spot trading reported by the April 2016 Triennial. Data from the Reserve Bank of India show that increases in spot trading volumes in the initial days after the devaluation were comparable to those of the NDF trading reported in the DTCC data, but onshore DFs showed lower increases. Spot trading rose by more than that of NDFs over a five-day period in the case of the real, according to the Central Bank of Brazil.