How large are FX dealers' trade internalisation ratios?

(Extract from pages 45-46 of BIS Quarterly Review, December 2016)

Internalisation refers to the process whereby dealers seek to match staggered offsetting client flows on their own books instead of immediately hedging them in the inter-dealer market. Until now, solid data on this phenomenon have been scarce. Analysis has often relied on soft information obtained via market contacts. The 2016 Triennial aimed to address this information gap with a supplementary question on trade internalisation.

Until now, solid data on this phenomenon have been scarce. Analysis has often relied on soft information obtained via market contacts. The 2016 Triennial aimed to address this information gap with a supplementary question on trade internalisation.

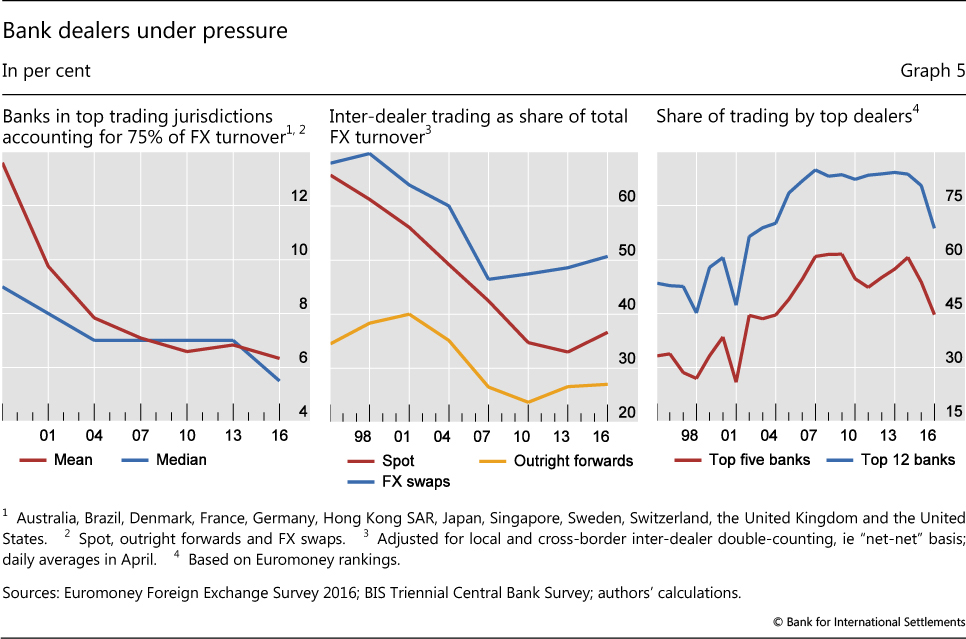

The bifurcation of liquidity provision described in the main text has meant that only a small number of bank dealers have retained a strong position as flow internalisers. This small set of global banks has increasingly faced competition from sophisticated technology-driven non-bank liquidity providers, some of which have also morphed into internalisers. As these large internalisers effectively become deep liquidity pools, their need to manage inventory via hot potato trading has fallen, contributing to a decline in turnover on venues such as EBS and Reuters. The declining share of inter-dealer trading observed between 1995 and 2013 (Graph 5, centre panel) has also been partly ascribed to a rise in trade internalisation. Yet while internalisation is known to have had a strong imprint on market structure, there have hardly been any numerical data on this crucial market phenomenon.

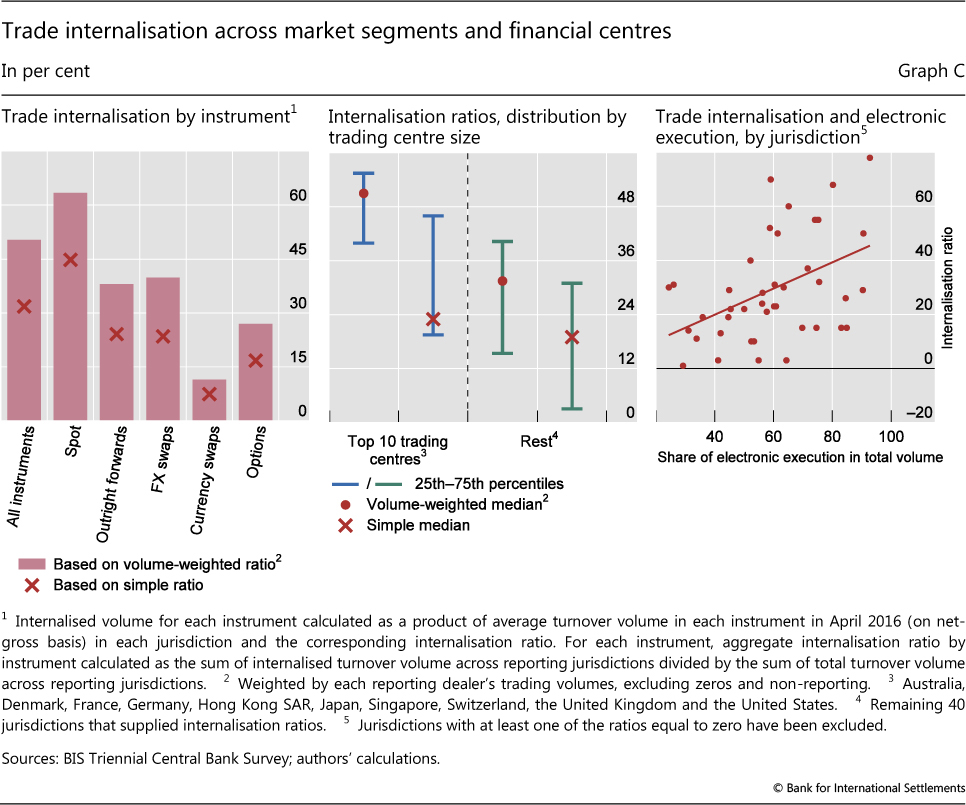

It is not surprising that, according to the Triennial, internalisation ratios are highest for spot, at 63% (Graph C, left-hand panel). Spot trading is the most standardised instrument and the segment of the foreign exchange market with the deepest penetration of electronic trading. However, these aggregate figures mask a high degree of heterogeneity across banks and jurisdictions. Internalisers with a large e-FX business can have much larger internalisation ratios (even above 90% in some major currency pairs). The extent to which the ability to internalise is a feature of large dealing banks can be gleaned by the much lower internalisation ratios when these are not weighted by reporting banks' trading volumes (left-hand and centre panels). While internalisation is most significant for spot, other important FX instruments also feature fairly high internalisation ratios (approximately 40% for both outright forwards and FX swaps).

{kind=link}

A locational breakdown suggests that internalisation ratios overall tend to be higher for larger FX trading centres (Graph C, centre panel). A large and diverse set of clients is key to a successful business model based on internalisation, and such a client base is most easily served via a major FX trading hub. From a risk management perspective, a business model based on internalisation is easier to operate when the bank's e-trading desk attracts a large client flow. Therefore, as one might expect, a cross-jurisdictional comparison shows that the internalisation ratio of FX dealers is positively correlated with the proliferation of e-trading (right-hand panel).

Bank and non-bank liquidity providers running an internalisation model benefit from access to large volumes of order flow originating from a diverse set of clients. Rather than immediately offloading inventory risk accumulated from a customer trade via the inter-dealer market, flow internalisers may hold open inventory positions for a short time (often not more than a few minutes) before matching against the flow of another customer. By internalising trades this way, they can benefit from the bid-ask spread without taking much risk, as offsetting customer flows come in almost continuously.