CCPs and bank risk

(Extract from pages 66-67 of BIS Quarterly Review, December 2015)

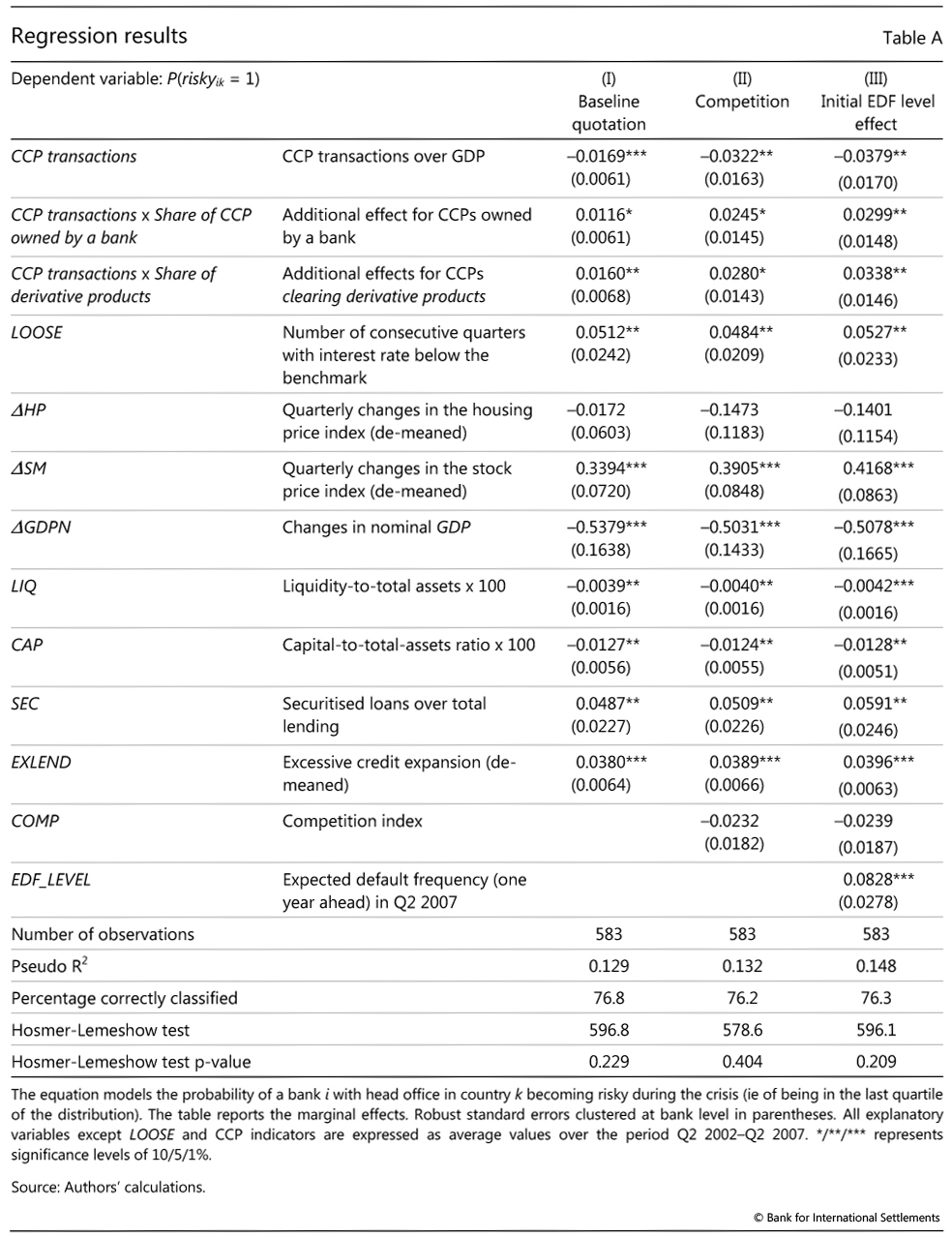

In this box, we present evidence on how the probability of a bank becoming risky during the Great Financial Crisis was affected by the characteristics of the CCPs with which it was operating. Using a sample of 583 banks, we first create a binary variable ("risky") that takes the value of 1 if the bank is in the top quartile of the distribution in terms of changes in its one-year expected default probability in the Q2 2007-Q2 2009 period, and 0 otherwise.

we first create a binary variable ("risky") that takes the value of 1 if the bank is in the top quartile of the distribution in terms of changes in its one-year expected default probability in the Q2 2007-Q2 2009 period, and 0 otherwise.

A bank's probability of belonging to the riskier group is then modelled as a function of a combination of factors, all measured pre-crisis. We relate this likelihood to a set of country-level macro variables (Y) and bank-specific characteristics (X). The vector Y includes: the number of consecutive quarters in which the real interest rate remained below the estimated natural rate as a measure of monetary policy looseness (LOOSE), the annual growth rate in nominal GDP (GDPN) and quarterly changes in housing and stock market returns de-meaned from their long-run average (∆HP and ∆SM). The vector X includes four bank-specific characteristics that could influence bank risk-taking: liquid assets over total assets (LIQ), the Tier 1 capital-to-assets ratio (CAP), securitisation activity (SEC) and excessive loan growth (EXLEND).

the annual growth rate in nominal GDP (GDPN) and quarterly changes in housing and stock market returns de-meaned from their long-run average (∆HP and ∆SM). The vector X includes four bank-specific characteristics that could influence bank risk-taking: liquid assets over total assets (LIQ), the Tier 1 capital-to-assets ratio (CAP), securitisation activity (SEC) and excessive loan growth (EXLEND).

To identify the impact of central clearing, we include the value of CCPs' transactions divided by nominal GDP (CCPT) and interaction terms that multiply CCPT by a vector (Z) containing two variables related to CCP characteristics: (i) the share of transactions conducted - in a given country - through a CCP owned by a bank; and (ii) the share of CCPs' overall activity that was in derivative products.

and interaction terms that multiply CCPT by a vector (Z) containing two variables related to CCP characteristics: (i) the share of transactions conducted - in a given country - through a CCP owned by a bank; and (ii) the share of CCPs' overall activity that was in derivative products.

The baseline empirical model is given by the following probit equation:

where P is the probability, Φ is the standard cumulative normal probability distribution, Y is a vector of regressors that include the macro variables of country k where bank i has its head office and X is a vector of bank-specific characteristics of the same bank i over the five years prior to the crisis (Q2 2002-Q2 2007). CCPs' transactions and characteristics are measured in 2007. This approach limits endogeneity problems by taking most of the right-hand variables from the pre-crisis period. The probit model is estimated by maximum likelihood.

Consistent with the existence of an "insulation" effect at the outbreak of the crisis, the CCP transaction variable has a negative coefficient (Table A). This suggests that banks operating in a system where a larger portion of transactions were cleared by CCPs were less likely to suffer a significant deterioration in solvency when the crisis broke out. The coefficients on the interaction terms between CCPT and CCP-specific characteristics indicate that banks operating in systems in which the CCP was owned by a bank became riskier. The findings further suggest that, if the CCPs operated in derivatives, the insulation effect was lower.

The findings further suggest that, if the CCPs operated in derivatives, the insulation effect was lower.

The results also show that liquid and well capitalised banks suffered less erosion of their solvency during the 2007-09 financial crisis. This is in line with Beltratti and Stulz (2009) and Detragiache and Merrouche (2010), who find that banks with more Tier 1 capital and more liquid assets performed better in the initial stages of the crisis. In line with Jiménez et al (2014) and Altunbas et al (2014), we find that a "too accommodative" monetary policy led to additional risk-taking by banks prior to the crisis.

We estimated the same model accounting for the initial level of the bank's expected default frequency (EDF) prior to the crisis and a bank competition variable, COMP (Boyd and De Nicolò (2005), Matutes and Vives (2000), Maddaloni and Peydró (2011)). However, the results remain unchanged (columns II and III).

The sample includes banks headquartered in the European Union (EU 15) and the United States. For a full description of the characteristics of the database and variable definitions, see Altunbas et al (2012, 2014). This measure considers the number of consecutive quarters in which the difference between the real short-term and "natural" interest rate, calculated using the Hodrick-Prescott filter, is negative. Similar results are obtained using different measures of the Taylor rule. For more details, see Altunbas et al (2014). We compute a bank-specific measure for credit expansion by subtracting from each bank's lending growth the average expansion in bank lending for the whole banking industry in that country. Data are taken from the CPMI Red Book and are corrected for the number of domestic participants. In particular, to compute a proxy for the volume of cleared products in a given banking industry, we have multiplied the total volume of the CCP operating in that country by the ratio of domestic participants (domestic participants/total participants). For some countries not reporting to the Red Book, the volume cleared by the national banking industry has been proxied by the total volume of the foreign CCPs mostly used by the domestic banks to clear outright transactions. In the case of a user-owned CCP (ie a bank that owns a CCP), the main objective for the owners is to lower the margins (costs) for the participants and to maintain a homogenous, high-quality participation base because more user capital is at risk in the event of a participant's default. In this case, the stability of the CCP is more strictly dependent on the financial resources (including capital) of the users (ie banks), and the fragility of this configuration could increase during a global financial crisis when banks too are directly hit.