Central clearing: trends and current issues

Central clearing of standardised financial instruments, as promoted by the G20 Leaders, addresses some of the financial stability risks that materialised during the Great Financial Crisis. Its rapid evolution since 2009 may have changed the linkages between central counterparties and the rest of the financial system. Against the backdrop of these trends, this article discusses how, and through which mechanisms, central clearing might have affected systemic risk.1

JEL classification: G01, G14, G18, G28.

The shift to central clearing is a key element of financial system reforms in the aftermath of the Great Financial Crisis. To reduce the systemic risks resulting from bilateral trading, the G20 Leaders agreed at the 2009 Pittsburgh Summit that all standardised derivatives contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties (CCPs). CCPs had, indeed, proved resilient during the crisis, continuing to clear contracts even when bilateral markets had dried up.

Since then, central clearing has evolved. The share of centrally cleared transactions has increased significantly; CCPs have expanded; the industry has remained highly concentrated; and the range of banks and other financial institutions that channel their transactions through CCPs has broadened. As a consequence, more and more connections in the global financial system run through CCPs. This growing interconnectedness raises the question whether CCPs might spread losses in the case of defaults, or intensify deleveraging pressures in ways that add to systemic stress.

Global standard setters have devoted considerable effort to strengthening the resilience of individual CCPs. They have required more stringent CCP risk management, with a focus on stress events. And they have adjusted the relative levels of capital and margin requirements for centrally cleared and non-centrally cleared products, so as to ensure that bank capital and liquidity requirements appropriately cover the risks associated with bank exposures to CCPs while maintaining incentives for central clearing. More recently, the focus has also turned to the issue of CCP recovery and resolution planning.

While progress in these vital areas has been impressive, the interaction between CCPs and the rest of the financial system remains, at best, imperfectly understood. This special feature discusses the evolution of central clearing since the Great Financial Crisis of 2007-09 and explores possible implications for systemic risk. The expansion of centrally cleared transactions and the horizontal integration in terms of both products and geographical reach may have altered the characteristics of systemic risk and crisis propagation mechanisms. Further analysis of the implications of central clearing for the behaviour of the financial system in normal and stressed conditions should help authorities to consider a macroprudential perspective to the regulation and supervision of financial systems that rely on central clearing.

The remainder of this article is organised as follows. The first section explores the functioning of a CCP, while the second describes some recent trends in central clearing. The third section analyses the main propagation channels through which central clearing could affect systemic risk. The last section concludes.

Central clearing in the financial system

A CCP is an entity that interposes itself between the two counterparties in a financial transaction. After the parties have agreed to a trade, the CCP becomes the buyer to every seller and the seller to every buyer. In doing so, the CCP reduces counterparty credit and liquidity risk exposures through netting. It also provides standardised and transparent risk management.

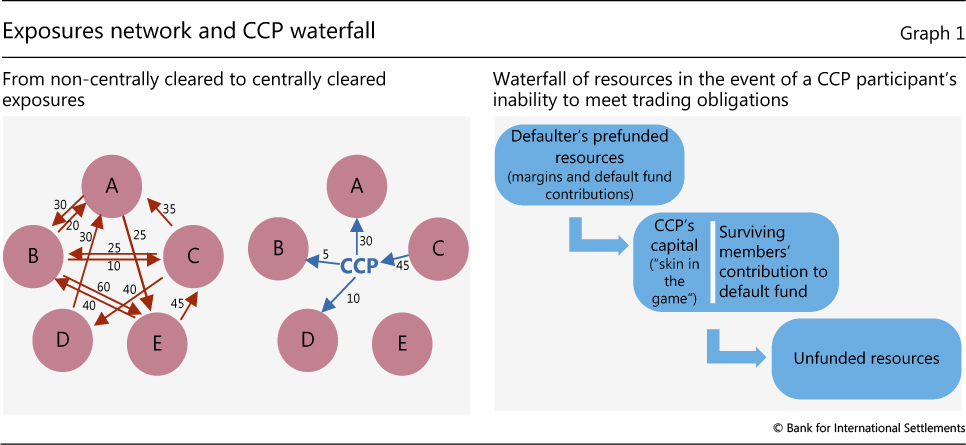

Central clearing fundamentally alters the linkages and exposures in the financial system. It replaces bilateral trading exposures between market participants with a centralised network of exposures between clearing participants and the CCP (Graph 1, left-hand panel). This implies that:

- the CCP combines the exposures to all clearing members on its balance sheet. If all clearing members can meet their obligations, the CCP runs regularly matched books. But if a participant defaults, it assumes the rights and obligations of the failed clearing participant; and

- instead of being subject to multiple exposures to a range of counterparties, each market participant maintains just a single trading exposure to the CCP. Because of multilateral netting, the size of this exposure is equivalent to the net position vis-à-vis all other clearing members.2

The network centre: CCP risks and risk management

The concentration of trading exposures in CCPs involves specific risks. One set of risks relates to the functioning of the CCP itself, including those risks stemming from the management of its activities (general business and operational risk). Another set arises from the possibility that a participant is unable to meet its trading obligations. This may give rise to liquidity risk, if the CCP has to advance payments that a participant cannot make, and to counterparty credit risk, if the participant is unable to cover losses on its positions because of its default.

To mitigate the risks resulting from a participant's default, a CCP marks positions to market and requires participants to settle losses and profits at least once a day by calling or paying "variation margins" (and in this way it runs regularly matched books). Should a participant be unable to meet its obligations, a CCP has a clear process in place either to transfer the participant's positions to other participants or to liquidate them ("close out"). The segregation of a participant's proprietary positions from those of its clients ("indirect CCP participants") makes it possible to transfer clients' positions to other participants ("portability").

If a clearing participant defaults, a CCP typically has three lines of defence to cover the resulting losses: (i) margins (initial and variation);3 (ii) default fund contributions; and (iii) the CCP's own financial resources (capital). The size of the aggregate margin fluctuates on a day-to-day basis depending on prices and participants' positions. In contrast, the contributions to the default fund are defined less frequently, typically via stress testing. These amounts are therefore more stable and less volatile, but at the same time less risk-sensitive, than margin payments.

The sequence of resources to be used in the case of losses follows a predefined "waterfall" (Graph 1, right-hand panel). It typically starts from the participant's own contributions: first the margins, then the default fund. Then, if necessary, the CCP turns to others' resources: the contributions to the mutualised default fund and the CCP's own capital, with a sequence that depends on each CCP's internal rules. In the extreme case that prefunded resources are not sufficient to cover losses, the CCP calls on pre-agreed unfunded contributions. These resources are ring-fenced in order to keep them available even if contributors default.

The design of these three lines of defence has important implications for the functioning of a financial system in which central clearing is prominent. In particular, their design affects the incentives of clearing participants and the CCP itself. The mix of the provision for own exposures through margin payments, the mutualisation of losses among participants through default fund contributions and the "skin in the game" of CCP owners is intended to limit moral hazard and reduce asymmetric information problems.4 At the same time, such measures create linkages between CCPs and banks (and other financial institutions) that go beyond the simple trading network described in the left-hand panel of Graph 1.

The network periphery: linkages with CCPs and associated risks

The links between CCPs and financial institutions take different forms, and create several layers of interconnection.

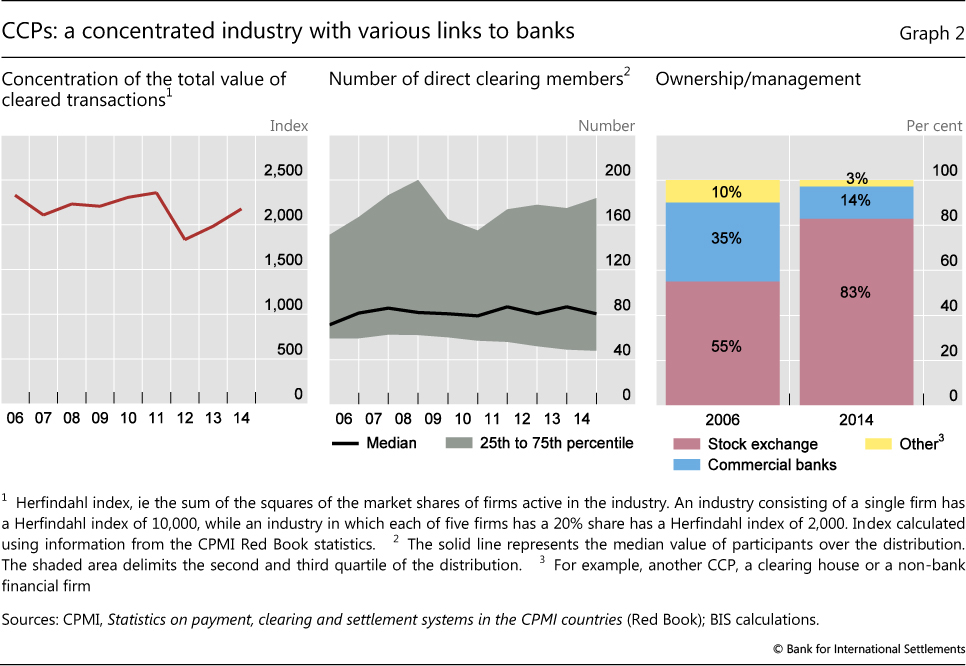

First, at the most basic level, banks are CCP participants, namely users of central clearing services. Every systemically important bank participates in many CCPs, often in multiple jurisdictions. The overall number of direct participants in CCPs has been quite stable in recent years, although it varies considerably between CCPs (Graph 2, centre panel). The large CCPs that clear most of the available over-the-counter (OTC) derivatives have a relatively small number of clearing members, and fewer still that offer clearing to their clients. However, many small domestic CCPs, especially those operating in Asia, have a large number of direct participants. Broad direct access to CCPs facilitates expansion of central clearing and increases the scope for multilateral netting, but at the same time it multiplies interlinkages with banks. A larger number of firms with access may also mean a wider variation in the creditworthiness of a CCP's participants, increasing its exposure to a sudden deterioration in credit quality in a particular segment of the financial system.

Second, banks are key providers of financial resources to CCPs. As direct clearing participants, they supply default fund contributions. Banks also supply liquidity lines or other backup facilities. If the ones that have committed to provide liquidity lines fail to do so, CCPs may be exposed to liquidity risk.

Third, banks are key providers of financial services to CCPs. For instance, CCPs typically rely on major banks to manage cash margins (mostly in repo transactions), and a CCP might need a custodian bank (or alternatively an operator of securities settlement systems) in order to deposit financial instruments posted as margin or as default fund contributions.

Finally, banks may also be the owners of CCPs. At the end of 2014, 14% of CCPs were directly owned or managed by commercial banks (Graph 2, right-hand panel). The ownership structures could affect risk behaviour. In the case of a user-owned CCP, the main objective for the owners is to reduce the cost for users and to maintain a homogeneous and high-quality participation base. Conversely, the main objective for a non-user-owned CCP is to maximise profits and increase participation (CPSS (2010)).

Recent trends in central clearing

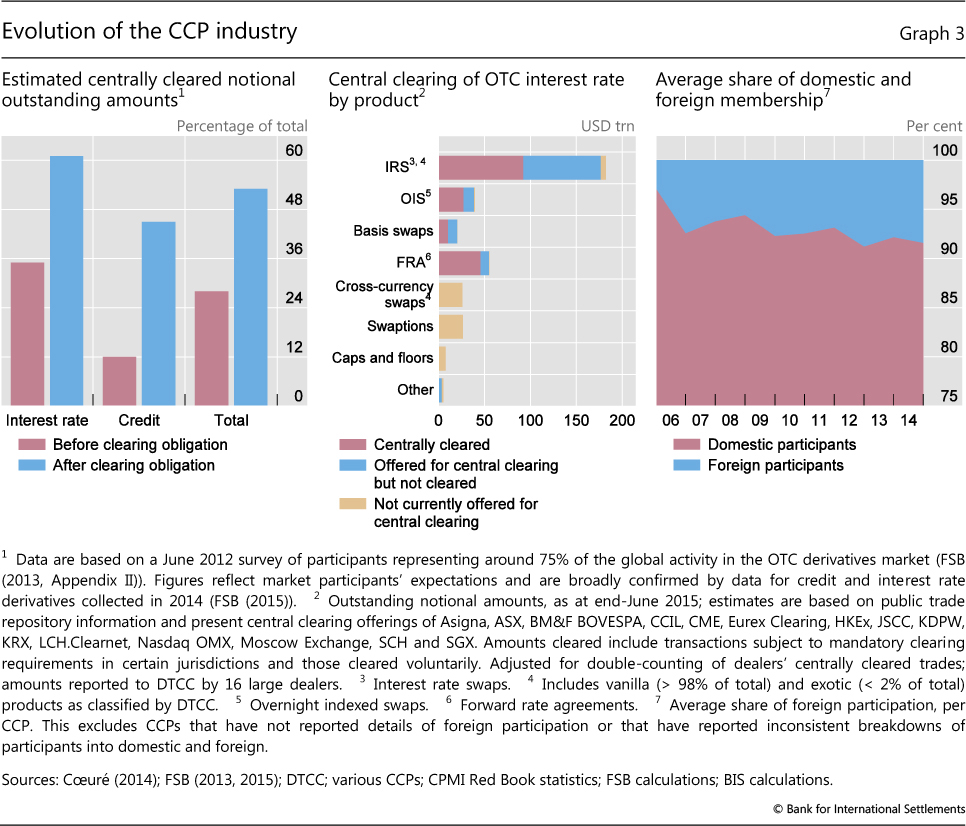

Since the 2009 Pittsburgh Summit declaration, central clearing has grown significantly. In 2014, more than half of the notional amount outstanding of derivatives transactions was centrally cleared, almost double the percentage in 2009 (Graph 3, left-hand panel). This trend is likely to continue in the near future, boosted by the implementation of further clearing obligations in the European Union (Rahman (2015)).

There seems to be ample room for the further expansion of central clearing. A recent study by the FSB (2015) finds that, for most of the plain vanilla interest rate contracts, the amount centrally cleared (Graph 3, centre panel, red bars) could increase significantly in the next few years (blue bars). Even larger increases could potentially take place for other contracts such as credit default swaps, for which the centrally cleared volume is currently quite low.

Economies of scale create incentives for concentration and vertical integration in central clearing. The scope for netting increases with the range of cleared instruments and markets, and high fixed costs also favour larger CCPs. At the end of 2014, two CCPs accounted for nearly 60% of the total volume of cleared transactions reported to the Red Book,5 a publication that compiles statistics covering centrally cleared transactions reported by members of the Committee on Payments and Market Infrastructures (CPMI).6 And the Herfindahl index suggests a constant high degree of concentration (Graph 2, left-hand panel). CCPs are typically part of groups that include exchange and trading platforms and, in certain instances, central security depositories. In 83% of the cases, CCPs are directly owned or managed by the company operating the stock exchange (Graph 2, right-hand panel).

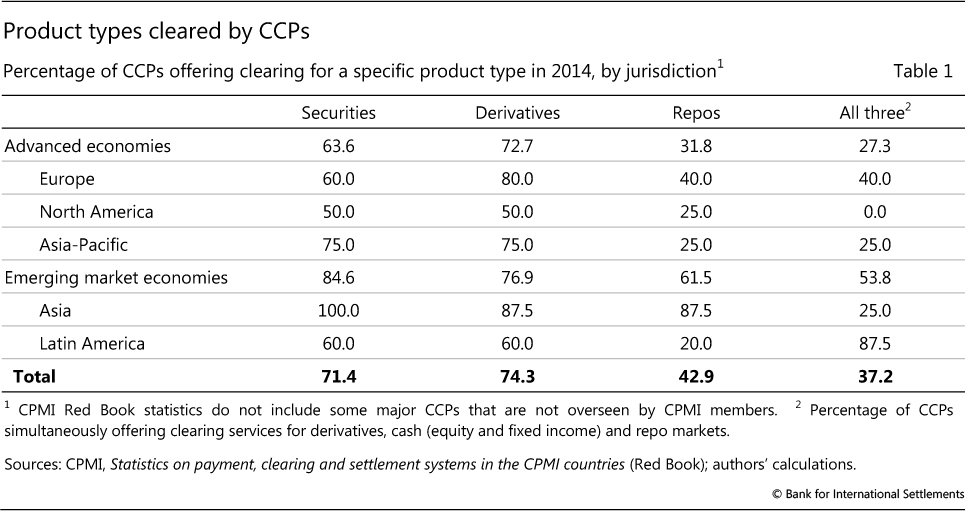

The market for central clearing is also more horizontally integrated than pre-crisis, in terms of both products and geographical reach. At the end of 2014, almost 40% of CCPs simultaneously offered clearing services for derivatives, cash and repo markets (Table 1) and average foreign participation reached 8% (Graph 3, right-hand panel). These percentages were, respectively, 20% and 4% in 2006.7 Horizontal expansion brings economies of scale and scope and, by providing some cross-product netting benefits, could reduce the need for collateral. Duffie et al (2015) find that, while mandatory central clearing increases collateral needs by about 30% as compared with the pre-reform case, it reduces collateral needs when CCPs offer more than one product in multiple markets.

Another evolving feature of central clearing is that, while the number of direct participants has remained quite stable, indirect participation in CCPs is growing (Cœuré (2014)). Because of fixed CCP participation costs, many small banks or financial intermediaries with limited activity in centrally cleared markets typically choose indirect access to comply with clearing obligations. In this tiered participation structure, the small number of direct clearing members that offer client clearing play an especially important role: non-clearing member firms in many cases are required to clear their OTC derivatives transactions centrally and otherwise would not be able to trade in those markets.

CCPs and systemic risk

The push towards central clearing is motivated by the experience of the Great Financial Crisis. After the Lehman Brothers default in September 2008, central counterparties continued to function smoothly despite abnormally high market volatility (Cecchetti et al (2009)). Within a short time frame, the positions of Lehman clients were either transferred to other, non-defaulting, CCP participants or liquidated. Moreover, preliminary econometric evidence (Box 1) suggests that banks operating in systems where a larger portion of transactions were cleared by CCPs were less likely to suffer a significant deterioration of solvency when the crisis hit.

Over the past few years, however, the financial system has evolved in ways that may affect the impact of central clearing on systemic risk. For example, better bank capitalisation is likely to have reduced default and counterparty credit risk. Greater reliance on collateral in wholesale financial markets may have altered liquidity dynamics in the financial system. And, finally, as described above, central clearing itself has evolved. This section discusses the relationship between central clearing and systemic risk in the light of these trends.

Propagation mechanisms

Clearing though a CCP creates a centralised network of trading exposures. Conceptually, this may influence systemic risk in two main ways. First, central clearing may affect the propagation of an (exogenous) shock through domino effects: the losses deriving from a counterparty default could trigger further defaults and spread the shock through the system. Second, central clearing, and the associated risk management practices, may affect the likelihood and impact of endogenous "run and deleveraging" mechanisms even in the absence of an initial default. While, in practice, both mechanisms may interact, considering them separately helps us to understand possible changes in the nature of systemic risk.

Box 1

CCPs and bank risk

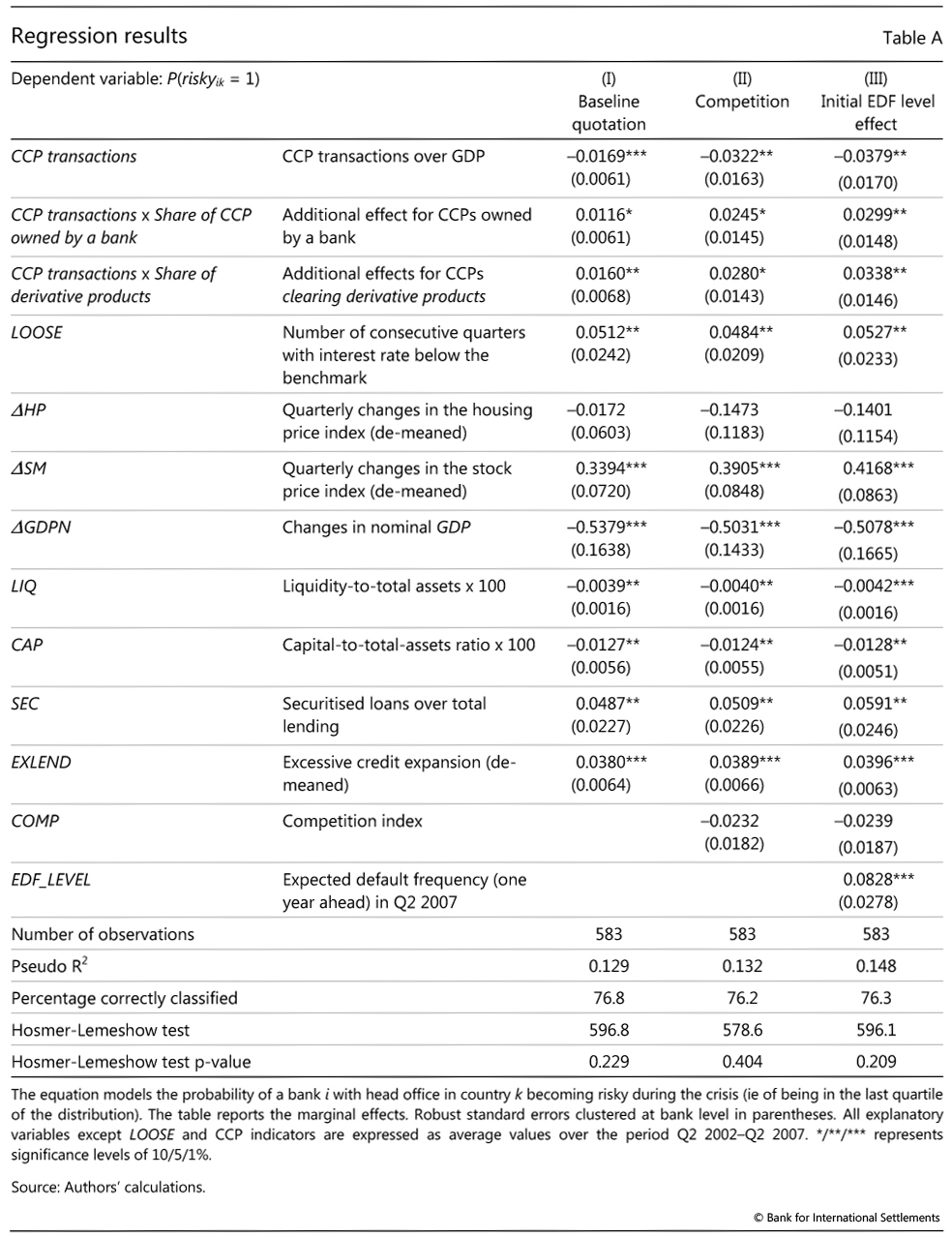

In this box, we present evidence on how the probability of a bank becoming risky during the Great Financial Crisis was affected by the characteristics of the CCPs with which it was operating. Using a sample of 583 banks, we first create a binary variable ("risky") that takes the value of 1 if the bank is in the top quartile of the distribution in terms of changes in its one-year expected default probability in the Q2 2007-Q2 2009 period, and 0 otherwise.

we first create a binary variable ("risky") that takes the value of 1 if the bank is in the top quartile of the distribution in terms of changes in its one-year expected default probability in the Q2 2007-Q2 2009 period, and 0 otherwise.

A bank's probability of belonging to the riskier group is then modelled as a function of a combination of factors, all measured pre-crisis. We relate this likelihood to a set of country-level macro variables (Y) and bank-specific characteristics (X). The vector Y includes: the number of consecutive quarters in which the real interest rate remained below the estimated natural rate as a measure of monetary policy looseness (LOOSE), the annual growth rate in nominal GDP (GDPN) and quarterly changes in housing and stock market returns de-meaned from their long-run average (∆HP and ∆SM). The vector X includes four bank-specific characteristics that could influence bank risk-taking: liquid assets over total assets (LIQ), the Tier 1 capital-to-assets ratio (CAP), securitisation activity (SEC) and excessive loan growth (EXLEND).

the annual growth rate in nominal GDP (GDPN) and quarterly changes in housing and stock market returns de-meaned from their long-run average (∆HP and ∆SM). The vector X includes four bank-specific characteristics that could influence bank risk-taking: liquid assets over total assets (LIQ), the Tier 1 capital-to-assets ratio (CAP), securitisation activity (SEC) and excessive loan growth (EXLEND).

To identify the impact of central clearing, we include the value of CCPs' transactions divided by nominal GDP (CCPT) and interaction terms that multiply CCPT by a vector (Z) containing two variables related to CCP characteristics: (i) the share of transactions conducted - in a given country - through a CCP owned by a bank; and (ii) the share of CCPs' overall activity that was in derivative products.

and interaction terms that multiply CCPT by a vector (Z) containing two variables related to CCP characteristics: (i) the share of transactions conducted - in a given country - through a CCP owned by a bank; and (ii) the share of CCPs' overall activity that was in derivative products.

The baseline empirical model is given by the following probit equation:

where P is the probability, Φ is the standard cumulative normal probability distribution, Y is a vector of regressors that include the macro variables of country k where bank i has its head office and X is a vector of bank-specific characteristics of the same bank i over the five years prior to the crisis (Q2 2002-Q2 2007). CCPs' transactions and characteristics are measured in 2007. This approach limits endogeneity problems by taking most of the right-hand variables from the pre-crisis period. The probit model is estimated by maximum likelihood.

Consistent with the existence of an "insulation" effect at the outbreak of the crisis, the CCP transaction variable has a negative coefficient (Table A). This suggests that banks operating in a system where a larger portion of transactions were cleared by CCPs were less likely to suffer a significant deterioration in solvency when the crisis broke out. The coefficients on the interaction terms between CCPT and CCP-specific characteristics indicate that banks operating in systems in which the CCP was owned by a bank became riskier. The findings further suggest that, if the CCPs operated in derivatives, the insulation effect was lower.

The findings further suggest that, if the CCPs operated in derivatives, the insulation effect was lower.

The results also show that liquid and well capitalised banks suffered less erosion of their solvency during the 2007-09 financial crisis. This is in line with Beltratti and Stulz (2009) and Detragiache and Merrouche (2010), who find that banks with more Tier 1 capital and more liquid assets performed better in the initial stages of the crisis. In line with Jiménez et al (2014) and Altunbas et al (2014), we find that a "too accommodative" monetary policy led to additional risk-taking by banks prior to the crisis.

We estimated the same model accounting for the initial level of the bank's expected default frequency (EDF) prior to the crisis and a bank competition variable, COMP (Boyd and De Nicolò (2005), Matutes and Vives (2000), Maddaloni and Peydró (2011)). However, the results remain unchanged (columns II and III).

The sample includes banks headquartered in the European Union (EU 15) and the United States. For a full description of the characteristics of the database and variable definitions, see Altunbas et al (2012, 2014). This measure considers the number of consecutive quarters in which the difference between the real short-term and "natural" interest rate, calculated using the Hodrick-Prescott filter, is negative. Similar results are obtained using different measures of the Taylor rule. For more details, see Altunbas et al (2014). We compute a bank-specific measure for credit expansion by subtracting from each bank's lending growth the average expansion in bank lending for the whole banking industry in that country. Data are taken from the CPMI Red Book and are corrected for the number of domestic participants. In particular, to compute a proxy for the volume of cleared products in a given banking industry, we have multiplied the total volume of the CCP operating in that country by the ratio of domestic participants (domestic participants/total participants). For some countries not reporting to the Red Book, the volume cleared by the national banking industry has been proxied by the total volume of the foreign CCPs mostly used by the domestic banks to clear outright transactions. In the case of a user-owned CCP (ie a bank that owns a CCP), the main objective for the owners is to lower the margins (costs) for the participants and to maintain a homogenous, high-quality participation base because more user capital is at risk in the event of a participant's default. In this case, the stability of the CCP is more strictly dependent on the financial resources (including capital) of the users (ie banks), and the fragility of this configuration could increase during a global financial crisis when banks too are directly hit.

Domino effects

Whether, and under what conditions, central clearing absorbs or spreads losses depends on the size of the shock and on CCPs' financial resources. As long as the negative shocks are sufficiently small, a more densely connected financial network enhances financial stability (Acemoğlu et al (2015)): a properly resourced CCP would act as shock absorber. Ideally, losses would be fully covered with the defaulter's own prefunded resources, leaving other clearing members unaffected. However, once losses exceed the CCP's prefunded resources, the same features that make a financial system more resilient may become sources of instability. As a consequence, financial networks may be "robust-yet-fragile" (Haldane (2009)).

For example, the size of a shock would matter for systemic risk to the extent that defaults inflict a liquidity shortage on a CCP. If one or more clearing members fail to meet their clearing obligations, the CCP itself must provide liquidity in order to make timely payments to the original trading counterparties. The CCP's own liquid assets and backup liquidity lines made available by banks may provide effective insurance against liquidity shocks resulting from the difficulties of one or a few clearing members. But they can hardly provide protection in the event of a systemic shock, when a large number of clearing participants - potentially including the providers of liquidity lines - become liquidity-constrained, thereby triggering domino effects.

More generally, the activation of a CCP's unfunded liquidity arrangements or other recovery instruments may impose financial strains on clearing participants. The resulting unexpected liquidity demands could impose stress on other clearing members and, in an extreme case, trigger a cascade of defaults. Heath et al (2015) simulate the distribution of losses if a CCP limits or stops paying variation margin gains because prefunded resources have been exhausted. While the authors find little evidence of contagion, the spillover of stress depends on a number of factors, including the distribution and direction of positions among participants, the magnitude of price changes across product classes and their co-movement, and the overall financial position of participants at the time of the shock.

Ultimately, if the (exogenous) shock is so big that losses exceed the CCP's prefunded and callable resources, a CCP could be forced into resolution and fail. Such a failure may have system-wide effects: clearing participants might find it difficult to manage positions if a CCP fails; and all clearing participants would have to find alternative ways of closing trades, at a time when there might be heightened uncertainty about the value of the underlying exposures and the associated market and counterparty risk.

From an international perspective, risks can be correlated across CCPs in several jurisdictions. Given the overlapping memberships of many CCPs, liquidity problems at one CCP may well coincide with similar issues at others. A participant bank unable to meet obligations - possibly defaulting and entering resolution - could be a global player active in many centrally cleared financial markets and could therefore be a participant in several CCPs. In the extreme case, the default of common clearing members could threaten the resilience of several CCPs at the same time. This, in turn, would impose strains on the surviving clearing members, propagating systemic risk.

Deleveraging and runs

A centralised structure of trading exposures may also affect the likelihood and nature of endogenous shocks in the form of forced deleveraging, fire sales and runs. The critical issue in this regard is the interaction between CCPs' risk management practices and those of clearing participants. On the one hand, if stringent risk management by a CCP replaces lax counterparty risk management in bilateral markets, central clearing would tend to reduce the risk of such procyclical behaviour. On the other hand, an unexpected tightening of CCP risk management could still lead to liquidity pressures on participants that could ultimately trigger fire sales and a self-reinforcing deleveraging (Morris and Shin (2008)).

One key determinant of possible procyclicality is the margining practices of CCPs (see eg Borio (2004)). Brunnermeier and Pedersen (2009) show that margins can be destabilising if lenders raise them when price volatility is expected to increase. A request for additional resources from a CCP in difficult times could put pressure on participant banks and indirectly affect the rest of the system. Even though regulation already requires CCP margins not to be "overly" procyclical, margin models based on value-at-risk methodologies could still understate the risk in calm conditions and amplify them in times of market stress (Abruzzo and Park (2014), Murphy et al (2014)).

A large decline in the market value of collateral could also trigger procyclical behaviour. A collateral squeeze, particularly if accompanied by high volatility in collateral markets, would reduce the value of initial margins posted to the CCP (also in a non-linear fashion) and trigger requests to members to replenish this value by posting additional collateral. This could force members to deleverage and potentially lead to fire sales precisely when the rest of the system is under stress.8 The risk of such liquidity strains and deleveraging could be anticipated by the market, triggering "runs" on participants perceived as vulnerable and stoking expectations that become self-fulfilling (Diamond and Dybvig (1983)).

These mechanisms place a particular onus on ensuring that CCP risk management is robust to shifts in the prices of cleared instruments. A sudden increase in risk premia or an abrupt price realignment within specific asset classes could invalidate the assumptions underlying CCPs' risk management models and procedures. For example, the assumptions used in CCPs' risk management models about correlations among different portfolio exposures might break down under stress. In the same vein, an unexpected "freezing" of trading activity in some financial markets could make it impossible for the CCP to fulfil default management procedures, such as the sale of non-cash collateral to cover losses stemming from a participant's inability to meet its obligations.9

Post-crisis trends and systemic risk assessments

The discussion of the general mechanisms above suggests that the impact of central clearing on systemic risk depends on a range of factors. These include the financial strength of clearing participants and CCPs, the robustness of CCP risk management and the interaction of CCP margining and collateral practices with liquidity and volatility conditions in broader markets. Assessing the significance of these factors with any precision would require a thorough understanding of existing financial linkages and exposure between CCPs and clearing participants, and within the financial system more generally. Without such information, it is only possible to make general, often ambiguous, inferences about how recent trends may have influenced systemic risk.

Consider the risk of domino effects (or deleveraging pressures) because of defaults. On the one hand, banks' capital positions have strengthened significantly since the Great Financial Crisis. Basel III has introduced more stringent capital regulation, which is reflected in the increase in bank capital ratios (BCBS (2011)). Moreover, capital surcharges for global systemically important banks (G-SIBs) take into account systemic risks resulting from interconnectedness. The Basel III capital framework has also strengthened banks' capital requirements in relation to their CCP exposures (Box 2). And, as a greater share of transactions is cleared through CCPs, multilateral netting reduces exposure to counterparty risk.

By the same token, central clearing may increase scope for taking on leveraged positions by freeing up collateral. The net effect of central clearing on collateral demand depends on two developments that seem to work in opposite directions. On the one hand, the migration of previously uncollateralised bilateral positions to CCPs increases the need for collateral. Indeed, CGFS (2013) estimates that the shift of bilateral contracts to CCPs will increase collateral demands on aggregate by up to $1 trillion. On the other hand, multilateral netting reduces collateral needs. Heller and Vause (2012) estimate that a CCP that cleared all asset classes would require only 74% of the initial margin collateral that would be demanded by separate CCPs for each asset class.10 The growing horizontal integration of CCPs, as discussed in the previous section, is likely to have added to these effects.

Questions also remain as to what combination of CCP financial resources and bank capital would provide the most effective protection against systemic risk. A trade-off exists between CCP prefunded resources, which represent self-insurance for the CCP and a cost for clearing members, and the reliance on unfunded liquidity provisions, which could put providers (whether participants or not) under pressure. Moreover, the capital of CCPs tends to be quite modest compared with their other prefunded resources, their gross exposures and the scale of their potential losses. The size of this capital cushion within the waterfall is typically a percentage of the total capital and is uncorrelated with the risks incurred by the CCP should one or more participants fail to meet their trading obligations. A recent study by Albuquerque et al (2015) indicates that the capital held by the five biggest CCPs in swaps is equivalent to just 2.6% of the sum of margin requirements and the default fund.11

Box 2

Regulatory responses to CCP-related risks

In recent years, regulatory efforts to address the risks connected to central clearing have proceeded along two main lines: (i) strengthening the resilience of CCPs; and (ii) strengthening banks' capital requirements in relation to their CCP exposures. Work to further strengthen resilience of CCPs and banks' CCP exposures is still ongoing.

Strengthening the resilience of CCPs

The regulatory approach to strengthening the resilience of individual CCPs reflects three features of central clearing.

The first is the critical role of sound risk management. This explains why regulation in recent years has increased the requirements for sound CCP risk management practices, namely through the Principles for Financial Market Infrastructures (PFMI) (CPSS-IOSCO (2012a)). The bar has been raised on how CCPs manage credit and liquidity risks - for example, by requiring CCPs that are exposed to particularly high risks (ie when operating in multiple jurisdictions or clearing complex products) to have financial resources to cover losses from the simultaneous default of at least the two largest participants. More demanding standards on transparency and the management of operational and general business risks have further strengthened CCPs (CPSS-IOSCO (2012b)).

The second feature that regulation has addressed is the importance of continuity in the provision of clearing services for systemic stability and - if this is not possible - of an orderly resolution of CCPs. Because even sound risk management may not prevent a CCP's default in extreme circumstances, emphasis has been placed on the need to develop robust recovery and resolution regimes for CCPs (CPSS-IOSCO (2012a), CPMI-IOSCO (2014), FSB (2014a)). The challenges in this respect are to define tools that take into account CCPs' specific characteristics (business model, liability structure) and to assess the extent to which tools that are already built into CCPs' risk management (eg bail-in tools) can also serve as recovery tools.

The third feature is the diversity of CCPs' organisational structures, functions and designs. Because of this, standard-setting bodies have introduced broad international principles rather than detailed quantitative requirements, supported by strong CCP governance and oversight arrangements, also at cross-border level. The CPMI and IOSCO are currently assessing the implementation of these standards across jurisdictions, such as the compliance and consistency outcomes of existing CCP stress testing, margin frameworks, prefunded loss absorption capacities and recovery planning.

Enhancing capitalisation of banks' exposures to CCPs

The bar has also been raised on how individual banks are required to cope with CCP-related risks. In particular, minimum capital requirements have been introduced - as part of the Basel III framework - to cover bank exposures to CCPs, which include both trade exposures and default fund contributions. The same items are included in the denominator of the Basel III leverage ratio. Liquidity commitments that banks provide to CCPs are included among the obligations that need to be covered by liquid assets through the Liquidity Coverage Ratio (LCR).

Margin requirements for OTC derivatives (BCBS-IOSCO (2015)) and minimum haircuts on securities financing transactions such as repos (FSB (2014b)) seek to introduce positive margins for non-centrally cleared transactions in order to create or to preserve incentives for the banks to shift to central clearing.

Together with the CPMI, IOSCO and the BCBS, the FSB is pursuing a coordinated work plan in four areas: (i) CCPs' resilience; (ii) CCPs' recovery; (iii) CCPs' resolution; and (iv) achieving a better understanding of the linkages between banks and CCPs. Banks' trade exposures to qualifying CCPs are risk-weighted by 2% (BCBS (2014a)). The latter also includes off-balance sheet items converted using the standardised risk-weight factors subject to a floor of 10%. To avoid double-counting of exposures, a clearing member's trade exposures to qualifying central counterparties associated with client-cleared derivatives transactions may be excluded when the clearing member does not guarantee the performance of a qualifying central counterparty (QCCP) to its clients (BCBS (2014b)).

The competitive dynamics in the CCP industry may work against a strengthening of capital buffers. Most CCPs are for-profit entities - typically vertically integrated with other financial market infrastructures, such as exchanges - that are strongly motivated to generate revenues by expanding their product offering and capturing market share. However, new products could bring incremental risk, which clearing members may end up bearing if the CCP does not increase its capital commensurately.

Turning to the risk of endogenous deleveraging, the assessment of the impact of post-crisis trends is similarly ambiguous. The fact that an increasing share of trading positions is subject to daily variation margin payments has arguably reduced the risk that counterparties are confronted with sudden big losses, as was for instance the case with AIG. However, the shift towards the centralised risk management of trading positions, including collateralisation and high-frequency margining, is also likely to affect market-wide liquidity dynamics. For example, extreme price movements in cleared financial instruments could result in large variations in the exposure of clearing members to the CCPs and therefore in the need for some of them to make correspondingly large variation margin payments. Such payments can be large, even if margin requirements remain unchanged. But they may be exacerbated if the CCP increases initial margins and/or tightens collateral standards in the face of unusually large price movements.

The interaction of such sudden and large shifts in collateral flows with the wider financial system is untested. The financial system as a whole has become much more reliant on high-quality collateral, increasing the risk that some market players could become collateral-constrained if risk premia rise sharply across the market. The demands and dispositions of CCPs could lead to big shifts in collateralised markets, adding to risk aversion and increasing pressure to reduce leverage in a procyclical manner. For example, CCPs are now huge players in reverse repo markets. ICE (one of the largest clearers of credit default swap contracts) held some $68 billion in collateral at end-2014, of which approximately $40 billion was in cash (Intercontinental Exchange Inc (2015)). LCH.Clearnet Ltd held comparable sums, amounting to $76 billion and $30 billion, respectively (LCH.Clearnet Group (2015)).

There is a consensus that the first line of defence against procyclical effects from central clearing consists in transparent, sound and robust CCP risk management practices. The CPSS-IOSCO Principles for financial market infrastructures (PFMI) have raised the bar for how CCPs manage credit and liquidity risks - for example, by requiring CCPs that are exposed to particularly high risks (ie when systemically important in multiple jurisdictions or when clearing complex products) to have financial resources to cover losses from the simultaneous default of at least the two largest participants (Box 2). Moreover, the PFMI require margin models not to be "overly" procyclical.

Certain challenges stand in the way of designing and implementing sound CCP risk management. One is that CCPs may underestimate the initial margins for participants who are clearing members in multiple CCPs for the same product. For instance, large internationally active banks may split their positions across several CCPs. Limited information on the total centrally cleared positions of its members in a specific product could induce the CCP to underestimate initial margins needed to appropriately cover liquidity costs in the liquidation process. Since liquidity costs tend to increase in a non-linear way with the size of the portfolio, the simultaneous liquidation of the larger aggregated position will have a market liquidity cost that is higher than one which the individual CCPs may have factored into initial margins (Glasserman et al (2015)).

Moreover, intense competition between CCPs may result in weaker risk management standards. In addition to broadening the range of products that they clear, as mentioned above, CCPs may directly compete via their margin requirements. In fact, Abruzzo and Park (2014) find that differences in margin requirements for futures between two major CCPs are, all things equal, one important variable in explaining margin cuts, implying that margin-setting may reflect competitive pressures.

Conclusions

The shift to central clearing has started to mitigate the risks that emerged in non-centrally cleared markets before and during the Great Financial Crisis. It has reduced financial institutions' exposure to counterparty credit risk shocks through netting, margining and collateralisation. And it has placed the focus on the need for sound risk management in trading markets more generally.

But central clearing may give rise to other forms of systemic risk. In particular, the concentration of the risk management of credit and liquidity risk in the CCP may affect system-wide market price and liquidity dynamics in ways that are not yet understood. A large body of research has analysed the structure and behaviour of financial networks, but lack of data and, much more fundamentally, our incomplete understanding of the post-crisis financial system prevent us from assessing how exactly central clearing might affect systemic risks. The multifaceted linkages between banks and CCPs add to these difficulties. It is possible that CCPs can buffer the system against relatively small shocks, at the risk of potentially amplifying larger ones.

Global standard setters have concentrated on strengthening the resilience of individual CCPs and, more recently, on ensuring the continued provision of clearing services if a CCP goes into recovery or resolution. Future efforts to understand the implications of central clearing for the behaviour of the financial system in normal and stressed conditions should help authorities to consider a stronger macroprudential perspective in the regulation and supervision of financial systems that rely on central clearing.

References

Abruzzo, N and Y H Park (2014): "An empirical analysis of futures margin changes: determinants and policy implications", Board of Governors of the Federal Reserve System, Finance and Economics Discussion Series, no 86, October.

Acemoğlu, D, A Özdağlar and A Tahbaz-Salehi (2015): "Systemic risk and stability in financial networks", American Economic Review, vol 105(2), pp 564-608.

Albuquerque, V, C Perkins and M Rafi (2015): "CCPs need thicker skins - Citi analysis", Risk.net, 3 August.

Altunbas, Y, L Gambacorta and D Marqués-Ibáñez (2012): "Do bank characteristics influence the effect of monetary policy on bank risk?", Economics Letters, no 117, pp 220-2.

--- (2014): "Does monetary policy affect bank risk?", International Journal of Central Banking, vol 10(1), pp 95-135.

Basel Committee on Banking Supervision (2011): Basel III: a global regulatory framework for more resilient banks and banking systems, June.

--- (2014a): Capital requirements for bank exposures to central counterparties.

--- (2014b): Basel III leverage ratio framework and disclosure requirements.

Basel Committee on Banking Supervision and International Organization of Securities Commissions (2015): Margin requirements for non-centrally cleared derivatives.

Beltratti, A and R Stulz (2009): "Why did some banks perform better during the credit crisis? A cross-country study of the impact of governance and regulation", NBER Working Papers, no 15180.

Biais, B, F Heider and M Hoerova (2012): "Clearing, counterparty risk, and aggregate risk", IMF Economic Review, vol 60(2), pp 193-222.

Borio, C (2004): "Market distress and vanishing liquidity: anatomy and policy options", BIS Working Papers, no 158, July.

Boyd, J and G De Nicolò (2005): "The theory of bank risk-taking and competition revisited", Journal of Finance, vol 60(3), pp 1329-43.

Brunnermeier, M and L Pedersen (2009): "Market liquidity and funding liquidity", Review of Financial Studies, vol 22(6), pp 2201-38.

Cecchetti, S, J Gyntelberg and M Hollanders (2009): "Central counterparties for over-the-counter derivatives", BIS Quarterly Review, September, pp 45-58.

Cœuré, B (2014): "Risks in central counterparties (CCPs)", speech at the conference "Mapping and monitoring the financial system: liquidity, funding and plumbing", Washington DC.

Committee on the Global Financial System (2013): Asset encumbrance, financial reform and the demand for collateral assets, May.

Committee on Payment and Settlement Systems (2010): Market structure developments in the clearing industry: implications for financial stability.

Committee on Payment and Settlement Systems and International Organization of Securities Commissions (2012a): Principles for financial market infrastructures, April.

--- (2012b): Principles for financial market infrastructures: disclosure framework and assessment methodology, December.

Committee on Payments and Market Infrastructures and International Organization of Securities Commissions (2014): Recovery of financial market infrastructures, October.

Detragiache, E and O Merrouche (2010): "Bank capital: lessons from the financial crisis", World Bank Policy Research Working Papers, no 5473.

Diamond, D and P Dybvig (1983): "Bank runs, deposit insurance and liquidity", Journal of Political Economy, vol 91(3), pp 401-19.

Duffie, D, M Scheicher and G Vuillemey (2015): "Central clearing and collateral demand", Journal of Financial Economics, vol 116(2), pp 237-56.

Duffie, D and H Zhu (2011): "Does a central clearing counterparty reduce counterparty risk?", Review of Asset Pricing Studies, vol 1(1), pp 74-95.

Financial Stability Board (2013): OTC derivatives market reforms. Fifth progress report on implementation, April.

--- (2014a): Key attributes of effective resolution regimes for financial institutions, October.

--- (2014b): Regulatory framework for haircuts on non-centrally cleared securities financing transactions, October.

--- (2015): OTC derivatives market reforms. Ninth progress report on implementation, July.

Glasserman, P, C Moallemi and K Yuan (2015): "Hidden illiquidity with multiple central counterparties", Office of Financial Research, Working Papers, no 15-07, May.

Haldane, A (2009): "Rethinking the financial network", speech at the Financial Student Association, Amsterdam, April.

Heath, A, K Gerard and M Manning (2015): "Central counterparty loss allocation and transmission of financial stress", Reserve Bank of Australia, Research Discussion Papers, no 2015-02, March.

Heller, D and N Vause (2012): "Collateral requirements for mandatory clearing of over-the-counter derivatives", BIS Working Papers, no 373, March.

Intercontinental Exchange Inc (2015): Form 10-K, February.

Jiménez, G, S Ongena, J Peydró and J Saurina (2014): "Hazardous times for monetary policy: what do twenty-three million bank loans say about the effects of monetary policy on credit risk-taking?", Econometrica, vol 82(2), pp 463-505.

LCH.Clearnet Group Ltd (2015): Consolidated financial statements for the year ended 31 December 2014.

Lewandowska, O (2015): "OTC clearing arrangements for bank systemic risk regulation: a simulation approach", Journal of Money, Credit and Banking, vol 47(6), pp 1177-203, September.

Maddaloni, A and J Peydró (2011): "Bank risk taking, securitization, supervision, and low interest rates: evidence from lending standards", Review of Financial Studies, vol 24(6), pp 2121-65.

Matutes, C and X Vives (2000): "Imperfect competition, risk-taking, and regulation in banking", European Economic Review, vol 44(1), pp 1-34.

Miglietta, A, C Picillo and M Pietrunti (2015): "The impact of CCPs' margin policies on repo markets", BIS Working Papers, no 515, October.

Morris, S and H S Shin (2008): "Financial regulation in a system context", Brooking Papers on Economic Activity, Fall, pp 229-74.

Murphy, D, M Vasios and N Vause (2014): "An investigation into the procyclicality of risk-based initial margin models", Bank of England, Financial Stability Papers, no 29, May.

Rahman, A (2015): "Over-the-counter (OTC) derivatives, central clearing and financial stability", Bank of England, Quarterly Bulletin, Q3, vol 55(3), pp 283-95.

Wendt, F (2015): "Central counterparties: addressing their too important to fail nature", IMF Working Papers, no 15/21, January.

1 The views expressed are those of the authors and do not necessarily reflect those of the BIS. We thank Claudio Borio, Ben Cohen, Mathias Drehmann, Klaus Löber and Hyun Song Shin for helpful comments, and Tracy Chan and Anamaria Illes for excellent research assistance.

2 For example, as shown in the left-hand panel of Graph 1, participant E has bilateral exposures to participant A equal to +25, to B equal to +20 (60 - 40 = +20), and to C equal to -45. After multilateral netting, participant E's exposure to the CCP is zero.

3 Margins include both initial margins - a fixed, predetermined amount of cash or non-cash collateral posted to the CCP by each party in a transaction - and variation margins, which are payments arising as a result of changes in the value of positions. For an analysis of the impact of clearing on collateral requirements, see Duffie and Zhu (2011), Heller and Vause (2012) and Duffie et al (2015).

4 CCPs' partial rather than full insurance against counterparty risk limits moral hazard and adverse selection (Biais et al (2012)).

5 CPMI, Statistics on payment, clearing and settlement systems in the CPMI countries, www.bis.org/cpmi/publ/d135.htm, September 2015.

6 www.bis.org/cpmi/membership.htm.

7 A large proportion of OTC derivatives activity takes place outside the home jurisdiction of the CCP clearing the relevant market, and involves at least one overseas participant. Rahman (2015) shows that 60% of initial margin requirements at UK CCPs was accounted for by clearing members not located in the United Kingdom themselves, with the vast majority based outside the European Economic Area.

8 This contagion process could be amplified by the fact that initial margin requirements are based (largely) on market risk indicators, and so may be expected to rise in times of market stress. Liquidity risk might also play a role, especially when there is a need to liquidate large volumes of offsetting positions.

9 Even in the absence of market distress, CCPs' risk management measures could affect the underlying financial markets. For example, the cost of funding could rise following a margin increase on repo transactions (Miglietta et al (2015)). Also, prices could fall and market volatility rise as an effect of the CCPs' management of the defaulter's position, which is likely to involve closing out the position and selling the defaulter's non-cash margins to cover losses (Wendt (2015)).

10 Lewandowska (2015) finds that, in the case of CCPs that clear all asset classes and have a high number of direct clearing members and no indirect ones, (i) central clearing maximises netting efficiency and thereby reduces replacement cost risk, which represents the cost for the clearing members if they are forced to replace the contract with a defaulting party at the current market value; and (ii) central clearing mitigates the concentration of liquidation costs, improving the loss allocation across the CCP's participants. The lower the concentration of liquidation costs, the more widely distributed are the replacement costs (the cost of replacing the contracts of a defaulting member), reducing the burden on any single counterparty.

11 Their approach implies an average "skin in the game" contribution for a CCP that trades interest rate swaps of 8.1% over the long term, while a clearing house that trades credit derivatives would contribute 11.4%.