Dollar credit to emerging market economies

We profile the US dollar debt incurred by borrowers in a dozen prominent emerging market economies (EMEs). These countries account for the bulk of total US dollar debt owed by EMEs. We measure the dollar borrowing of non-banks resident in these economies as well as that of their affiliates offshore, and relate these items to commonly used debt measures. We also discuss the limitations of our data. These data fail to assign bank debt to the right home country if firms have obtained dollar bank loans through offshore affiliates. And they understate dollar debt when firms borrow dollars indirectly through foreign exchange forwards.1

JEL classification: E43, E51, F34, G21, G23.

Since 2008, dollar credit has grown more rapidly outside the United States than inside. Although there is only one dollar yield curve, the two stocks of dollar credit behave differently. Dollar credit to non-US residents grew faster owing not only to more rapid growth in emerging market economies (EMEs) over the last six years. Dollar credit also expanded owing to its substitution for local currency credit given favourable dollar interest rates and exchange rate expectations (Bruno and Shin (2015a,b)) as EME firms leveraged up (IMF (2015)).

Dollar credit to non-banks outside the United States reached $9.8 trillion at end-Q2 2015. Borrowers resident in EMEs accounted for $3.3 trillion of this amount, or over a third. EME nationals resident outside their home countries (for instance, financing subsidiaries incorporated in offshore centres) owed a further $558 billion.2

Dollar bonds issued by EME non-banks' offshore affiliates have surged over the past six years, as have dollar bank loans obtained by non-banks within the home country. Since high overall dollar debt can leave borrowers vulnerable to rising dollar yields and dollar appreciation, dollar debt aggregates bear watching. Standard measures of residents' external debt do not include bonds issued by affiliates outside the home country or dollar bank debt incurred in the home country. Multinational firms' balance sheets are not neatly confined within national borders, and the domestic currency may not account for all domestic intermediation (Avdjiev et al (2015)), so a dollar debt measure that looks beyond and within national borders can indicate vulnerabilities missed by external debt measures.

Which EMEs borrow dollars? In what form do they borrow them? To what extent do they borrow dollars from banks at home or sell bonds through offshore affiliates? How big is dollar debt relative to all debt?

This special feature first describes the construction of measures of dollar credit to emerging economies, drawing attention to their relationship to external debt and to domestic debt aggregates, and to the limitations of the underlying data. It then expands on Borio et al (2011) and McCauley et al (2015) by profiling recent dollar credit growth for a dozen EMEs that accounted for almost three quarters of the US dollar credit to all EME non-bank borrowers.3

For this dozen, we find that underneath the rapid growth of dollar credit lies a variety of forms and channels of dollar borrowing that can make for different vulnerabilities. Some countries rely on bank loans, others more on bonds. Some rely on bank loans booked by banks at home, others not. Some issue dollar bonds not out of headquarters at home, but from their offshore affiliates. Some of these differences bear the footprint of policy.

The feature first takes up measurement issues and then makes comparisons with other debt aggregates. Then it draws out the themes of similarity and differences across the 12 cases for dollar bank loans and dollar bonds. The last section concludes. A box addresses the frequent question of why firms borrow dollars.

What we measure: dollar credit aggregates

Viewed from the debtor perspective, dollar credit to non-banks outside the United States represents about 17% of non-US GDP. Viewed from the creditor side, non-US borrowers owe remarkably little of their dollar debt to banks or investors that reside in the United States.4 It is thus understandable that dollar credit to non-US residents has not, until recently, appeared on US radar screens.

The ideal versus the practical

The baseline aggregate of dollar credit to non-banks resident in a particular country comprises outstanding bank loans and bonds. Non-banks include non-financial corporations, non-bank financial institutions, households and governments.5 For bank loans, we sum dollar loans to non-banks (including non-bank financials) booked both locally (within the respective economy) and cross-border.6 For bonds, we sum outstanding dollar obligations of non-bank borrowers resident inside the country. Combined, these elements provide an estimate of the total dollar credit to non-banks resident in the country.

Ideally, we would complement this residence-based measure with a corresponding consolidated one that respects the cross-border span of corporate balance sheets. That is, we would like a measure that includes dollar credit to offshore affiliates of non-banks headquartered in the country while excluding dollar credit to foreign-owned entities inside the country. For instance, Brazilian firms have sold many dollar bonds out of their financing subsidiaries in the Netherlands Antilles. Similarly, Chinese firms have borrowed significant dollar amounts from banks in Hong Kong SAR, using affiliates incorporated outside China. None of this debt shows up in residence-based credit measures for the countries concerned, but all would be included in an ideal consolidated measure based on corporate balance sheets rather than national borders.

Uses of US dollar funding

A frequently asked question is: why do firms (and some households) outside the United States borrow in US dollars? Some of the answers to this question simply invoke the dollar's broad international role in trade and investment, and the need to hedge the currency exposures that arise from these activities. Other motivations are better explained as an attempt to profit from interest rate differentials or currency movements, potentially leading to liabilities that can leave firms' financial soundness vulnerable to dollar appreciation.

Firms engaged in international trade borrow dollars to finance dollar-invoiced transactions. However, a back-of-the-envelope calculation shows that trade finance can explain only a small portion of offshore US dollar credit. About half of the $23.4 trillion per year in international trade is dollar-invoiced (Ito and Chinn (2015)). Assuming three-month financing terms, dollar credit of roughly $3 trillion (= $23.4 trillion x 0.5 x 0.25) finances dollar-invoiced trade. Subtracting the one ninth US share in world trade leaves about $2.7 trillion of US dollar trade credit to non-US residents, decidedly less than $9.7 trillion.

Firms can also use dollar credit to fund holdings of inventory and fixed assets at home. To the extent that these are in the traded goods sector, currency mismatches need not arise. Such risks do arise when firms in the non-traded goods sector at home borrow dollars, especially in leveraged real estate. This type of dollar borrowing is often motivated not only by lower interest rates but also by the ability to borrow at longer maturities.

Firms can borrow dollars to fund productive assets held by affiliates outside the home country, ie foreign direct investment. EME firms accounted for a record 35% of all foreign direct investment in 2014 (UNCTAD (2015)). In some EMEs, the largest dollar borrowers are also some of the largest direct investors abroad. Firms hedge some of the dollars borrowed for these purposes, but in general it is not possible to say how much. Inferences drawn from stock price responses to currency movements (see eg Acharya et al (2015) on India) require that investors know about these hedging strategies on the basis of scant disclosures by firms.

Finally, firms may also borrow dollars to accumulate financial assets, including those in the domestic currency. The combination of debt in the US dollar and a long position in domestic currency (a form of "carry trade") is difficult to document, given the opacity of corporate reporting. Bruno and Shin (2015c) find that dollar bonds are issued when carry trade incentives are attractive, and are associated with increases in corporate cash holdings. While such accumulated cash may reflect opportunistic front-loading of funding on the back of low US dollar yields, it may also fund corporate holdings of higher-yielding domestic assets, such as wealth management products or investment fund shares (Chui et al (2014)).

A further desideratum would be to measure dollar debt net of off-balance sheet hedges, including dollar credit obtained indirectly through forward dollar sales. For instance, Korean manufacturers effectively borrow dollars by selling forward dollars in exchange for won (see below). Such dollar debt is not at all captured by our measure.

Data limitations preclude the ideal measure, and allow only a partial shift from a strictly residence-based measure to a consolidated one that takes into account off-balance sheet positions. The dollar bond data do include information about both the nationality and the location of the issuer, so that we can use them, for example, to measure Brazilian firms' overall dollar debt rather than the dollar debt of firms in Brazil.7 Economy-level aggregates discussed below thus include these offshore dollar bonds, although they are identified separately in each graph and table to preserve the residence-based measure.

Otherwise, the possible falls short of the ideal. First, the dollar loan data reveal the borrower's location but not its nationality. Thus, neither loans to offshore national affiliates nor those to foreign entities inside the country can be identified. Second, data about off-balance sheet positions in general or indirect dollar credit via forward dollar sales in particular are unavailable for any country. Below, we discuss partial data from Hong Kong and Korea that bear on these lacunae.

Dollar debt versus other debt aggregates

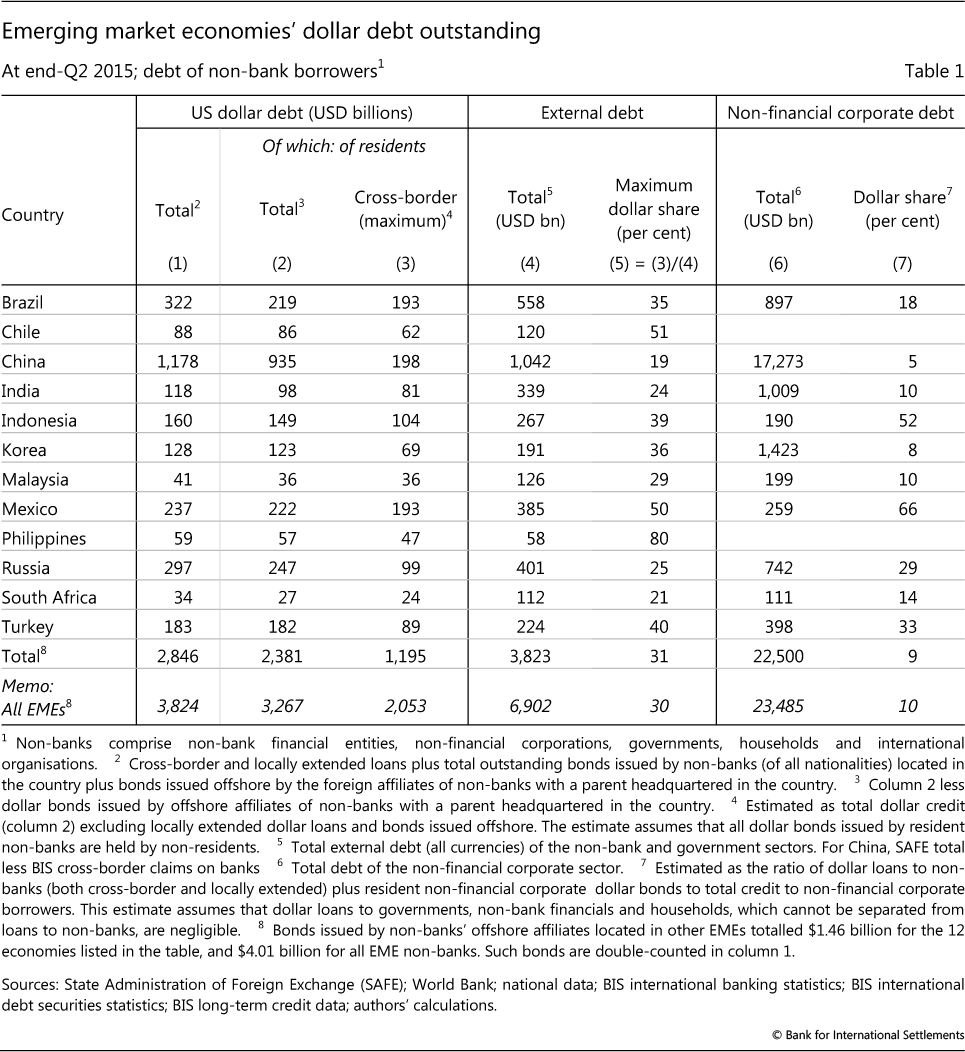

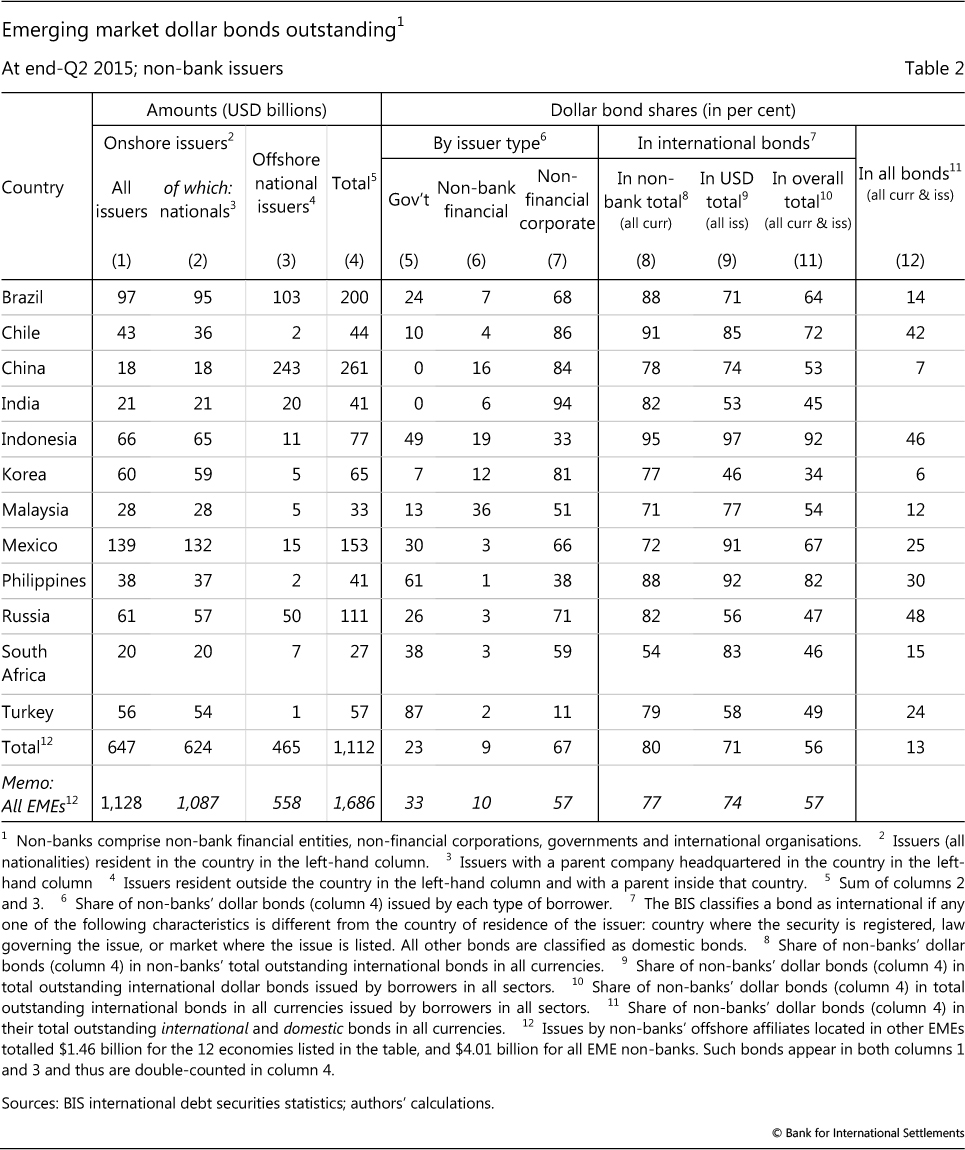

Table 1 juxtaposes, for 12 EMEs, dollar credit and other credit aggregates at end-Q2 2015. Column 1 reports the broadest aggregate, namely the hybrid that includes dollar credit to non-bank residents in each country and the dollar bonds issued by domestically headquartered non-banks' offshore affiliates (the time series are presented below). Across all EMEs, total dollar credit exceeded $3.8 trillion (last row), with the 12 EMEs detailed in the table accounting for $2.8 trillion, or 70%. Column 2, in turn, reports only the dollar debt of non-bank borrowers resident in each country (ie excluding offshore dollar bonds), which can be compared with other credit aggregates in the rest of the table.

Data limitations again hamper the assessment of how dollar credit from banks and bond investors contributes to non-banks' external debt in all currencies (column 4). In this case, the problem is the lack of data on domestic holdings of international dollar bonds issued by home firms and governments. However, on the extreme assumption that all dollar bonds issued by non-bank residents sit in the portfolios of non-resident investors, then column 3 provides an upper-bound estimate of the total cross-border portion of dollar credit in column 1 to non-bank borrowers in each country. On this assumption, such cross-border dollar credit accounted for much of total external debt in most of the 12 (column 5).

Columns 6 and 7 take the further step of juxtaposing the resident dollar credit aggregates to credit aggregates that include both cross-border and locally extended credit in all currencies. Here, we use the total credit figures (column 6) for non-financial firms only (see BIS website). Given granular bond data, we exclude from the numerator dollar bonds issued by governments and non-bank financial firms (included in column 2). Ideally, we would exclude dollar loans to these two sectors and to households. In practice we cannot, but if dollar loans to governments and non-bank financial firms are not large, then the most upwardly biased ratio would be for an economy with substantial dollar household mortgages. The admittedly imperfect ratios suggest that dollar-denominated borrowing accounts for double-digit shares in total corporate debt for eight economies considered here, with Mexico, Indonesia and Turkey registering the highest shares.

Dollar bank loans

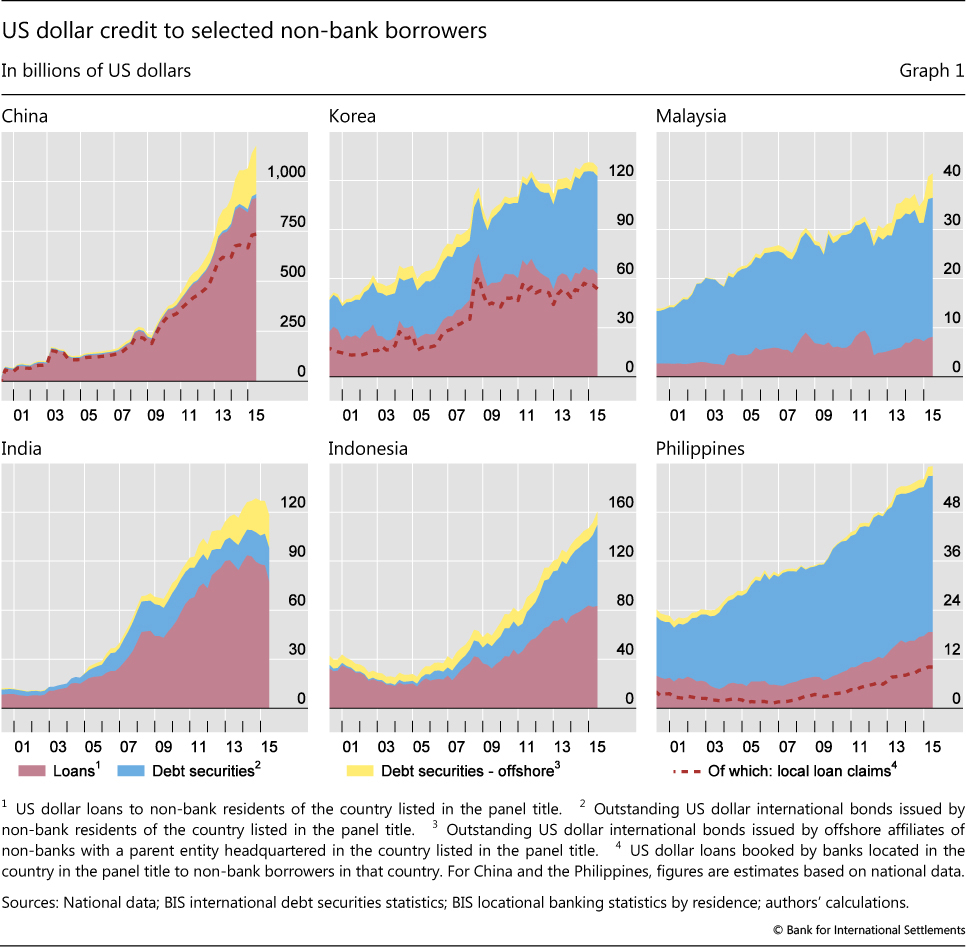

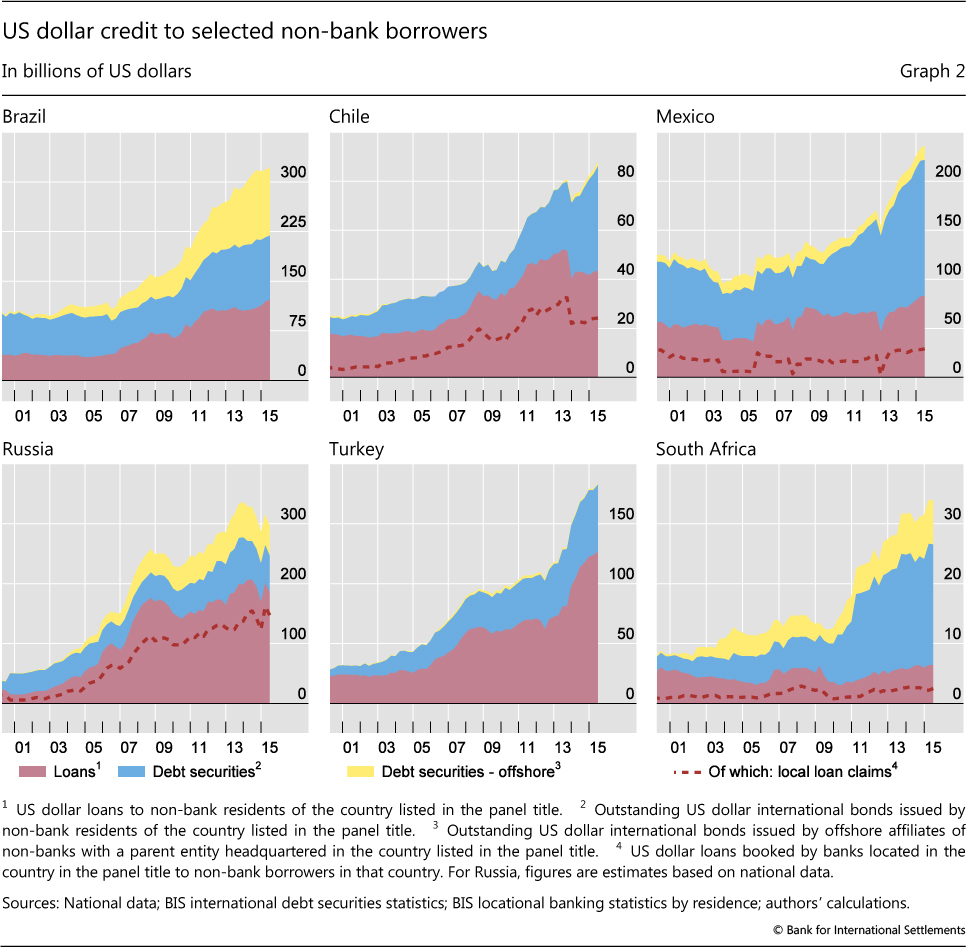

In aggregate, dollar bank loans remained larger than dollar bonds even as rapid bond issuance drove the doubling of the stock of dollar debt of non-bank borrowers in selected major EMEs between Q1 2009 and Q2 2015. Yet the composition of the dollar credit varies widely across the 12 cases, with dollar bank loans substantially larger than bonds only in China, India, Russia and Turkey (the different categories of dollar debt are illustrated in Graph 1, for the six Asian economies, and Graph 2 for the others).

In China, Russia and Turkey, the bulk of the dollar bank loans are booked at resident banks. Only in India's case do cross-border bank loans constitute most of the dollar loans.

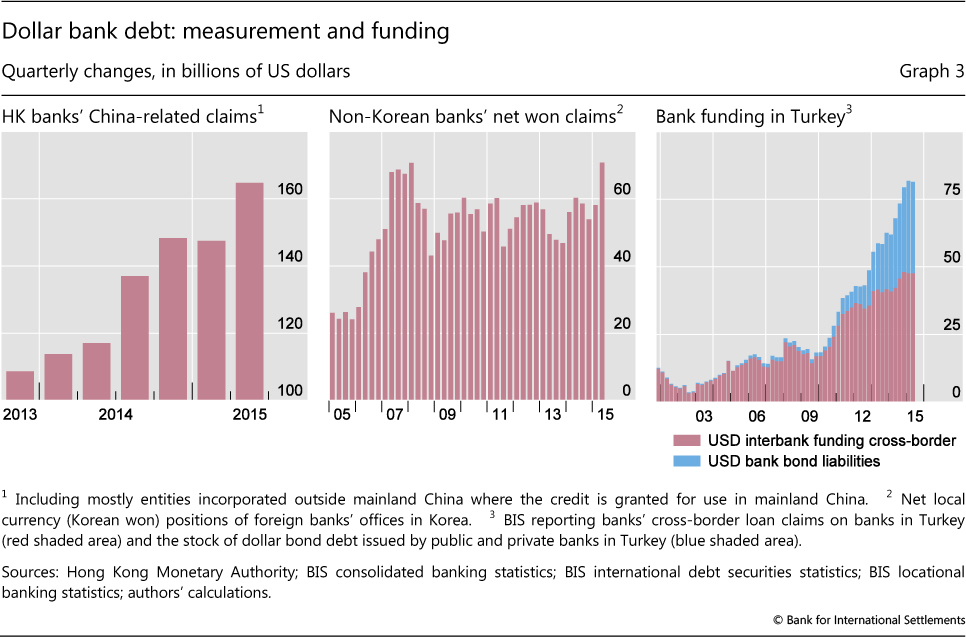

Recall that the split between dollar funding through bank loans and bonds is imprecise because data on bank loans are only available by residence. According to data published by the Hong Kong Monetary Authority (HKMA) on mainland-related lending in the territory to entities incorporated outside the mainland (Graph 3, left-hand panel), China's reliance on bank funding is even more disproportionate than that shown in the top left-hand panel of Graph 1 (Yuen (2014)).8

Chinese and Hong Kong data suggest that the third quarter of 2015 may have marked an inflection point in the growth of mainland-related dollar credit. Chinese domestic banking data show a $70 billion decline in foreign currency lending in the August-October 2015 period. Similarly, foreign currency loans fell in Hong Kong in September 2015.

Our measure of dollar debt in general, and the share accounted for by banks in particular, may be biased downwards. This is because of our inability to take account of forward sales of dollars that are in effect dollar bank loans. Taking into account forward positions would represent a net addition to our measure of dollar debt. For Korea, He and McCauley (2013) treat virtual dollar credit through dollar/won forwards as dollar credit and estimate its volume based on BIS data (Graph 3, centre panel). This would suggest another $60 billion in dollar bank debt in Korea, about half of which is owed by exporters (non-financial) and half by mutual funds (financial) (Chung et al (2015)). Looking at the same data for 23 EMEs in Q2 2015, $585 billion in additional virtual dollar debt (including Korea's $60 billion) might be inferred, some of which is owed by non-bank financials and some by non-financial firms. On this view, non-bank EME dollar debt could easily be some 10% larger than our estimated $3.8 trillion.

The economies most dependent on dollar bank loans differ in the sourcing of the dollars. In particular, banks in China and Russia, according to national sources, rely to a considerable extent on domestic dollar deposits to fund dollar loans at home. (Similarly, banks in Indonesia and the Philippines (another country where we rely on national data) draw on domestic dollar deposits to a considerable extent.) These economies may be said to have partially dollarised banking systems, with the result that external debt statistics can understate vulnerability to dollar interest rate rises or dollar appreciation. In contrast, banks in Turkey issue dollar bonds and raise dollar funding from banks abroad to fund domestically booked dollar loans (Graph 3, right-hand panel),9 although they also have domestic dollar deposits.

Dollar bonds

As noted in Shin (2013) and McCauley et al (2015), dollar bonds outstanding have grown faster than dollar loans since 2009. In part, this reflects the retrenchment of global banks, which suffered losses on their cross-border credits during the Great Financial Crisis of 2008-09 and which have since come under pressure from shareholders and supervisors. But it also reflects the very favourable yields for global borrowers that resulted from the Federal Reserve's large-scale bond buying.

These developments drove a surge in issuance by both long-standing issuers and new ones (Mizen et al (2012)).10 Petrobras, among the largest issuers, exemplifies the former. To pay the development costs for offshore oil in the face of cash flows weakened by low domestic administered energy prices, this partially state-owned Brazilian oil company ramped up its dollar debt in 2009-14, with multi-tranche offerings of no less than $8 billion and $6 billion highlighting the ready supply of institutional funds.11 Many African sovereigns exemplify the new issuers. Would-be underwriters courted them, mindful that pension funds and mutual funds sought to diversify away from the sovereign debt of the major economies in their portfolios. Ghana, Kenya, Rwanda and Zambia all found ready markets.

At the time of writing, deals are still going through even for non-investment grade sovereign issuers. Ghana, Pakistan, Sri Lanka and Zambia all issued in 2015, albeit in smaller amounts or at higher spreads than they desired or had previously achieved. Ethiopia debuted at end-2014, while Angola did so in November 2015.

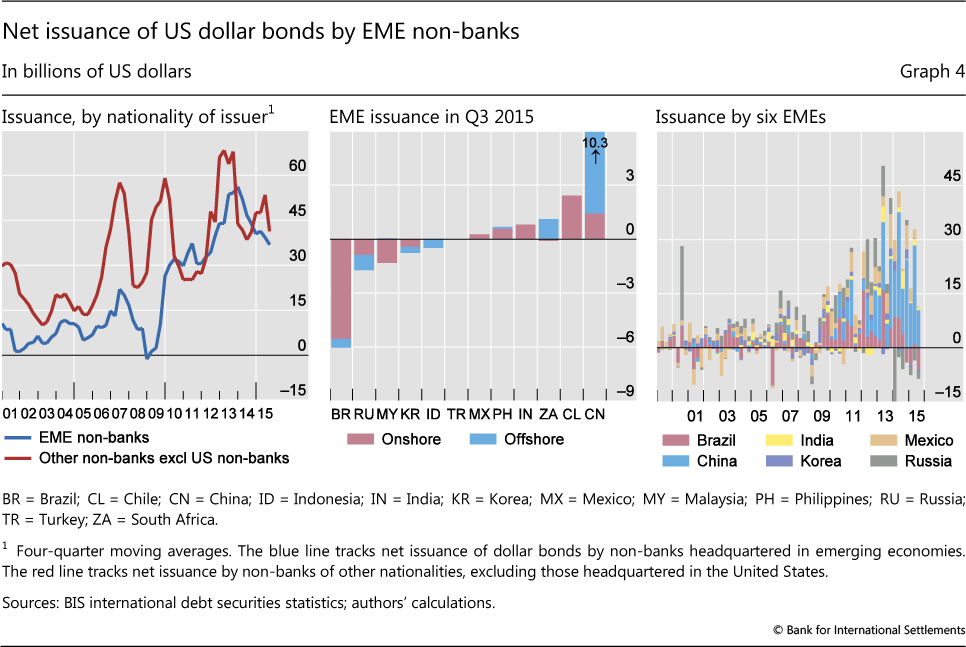

Nevertheless, dollar bonds outstanding have grown more slowly in 2015 than in 2013 and 2014. The largest Brazilian borrower and the main Russian borrowers have not been issuing owing to governance issues and international sanctions, respectively. Indeed, Q3 2015 data signal a steep decline in net issuance by the 12 (from $41 billion in Q2 to $5 billion in Q3), following the market turbulence in August in many EMEs (Graph 4; see also BIS (2015)). China's net issuance fell to $10.3 billion in Q3 but remained well above that of its peers (centre panel). But for five of the 12 EMEs that we study here, net dollar bond issuance by non-banks turned negative in Q3 2015.

A closer look at bond issuance

Table 2 summarises the outstanding dollar bonds issued by non-banks in the 12 countries discussed above. They totalled $1.1 trillion at end-Q2 2015 (column 4), or two thirds of the $1.7 trillion issued by non-banks in all EMEs (last row).12

Non-banks in most of these EMEs tended to issue dollar bonds as residents (column 2) rather than through offshore affiliates (column 3). We discuss the exceptions below. In principle, resident issuers of dollar bonds could include local affiliates of multinationals headquartered elsewhere. Column 2 demonstrates that there is very little such issuance. Thus, the sum of columns 2 and 3 yields a consolidated dollar bond aggregate that respects the cross-border span of domestic firms' balance sheets, as opposed to the residence-based aggregate in column 1 that is confined by national borders. (As noted, this shift in perspective is not possible for dollar loans.) Ignoring the offshore components of dollar credit raises the risk of missing potential threats to the ability to service this debt.

Corporate bonds bulk large (column 7). Government issues predominated only in Turkey and the Philippines (column 5). And only in four of the 12 economies - China, Indonesia, Korea and Malaysia - did non-bank financial institutions' dollar bonds contribute significantly. For the remaining eight economies, such issues accounted for single-digit shares of total dollar bonds issued by all non-banks.

Columns 8-12 in Table 2 demonstrate the prominence of non-banks' dollar bonds in various bond aggregates for these countries. For most countries, dollar bonds predominated in non-banks' total outstanding international bonds in all currencies (column 8). Moreover, non-banks' dollar bonds accounted for the bulk of total international dollar bonds, including those issued by banks (column 9). Only in Korea did banks issue a significant amount of dollar bonds. Non-banks' dollar bonds even accounted for a large share of total bond issuance, including domestic bonds, in some countries, notably Chile, Indonesia, and Russia (column 12).

Dollar bond issuance from the home country vs offshore affiliates

Chinese, Indian, Brazilian, Russian and South African firms use offshore subsidiaries to issue dollar bonds (Table 2, column 3). For this reason, external debt statistics can understate vulnerability to dollar yields or appreciation. The largest stock of such bonds, at $243 billion as of Q2 2015, is issued by affiliates of China's non-banks.

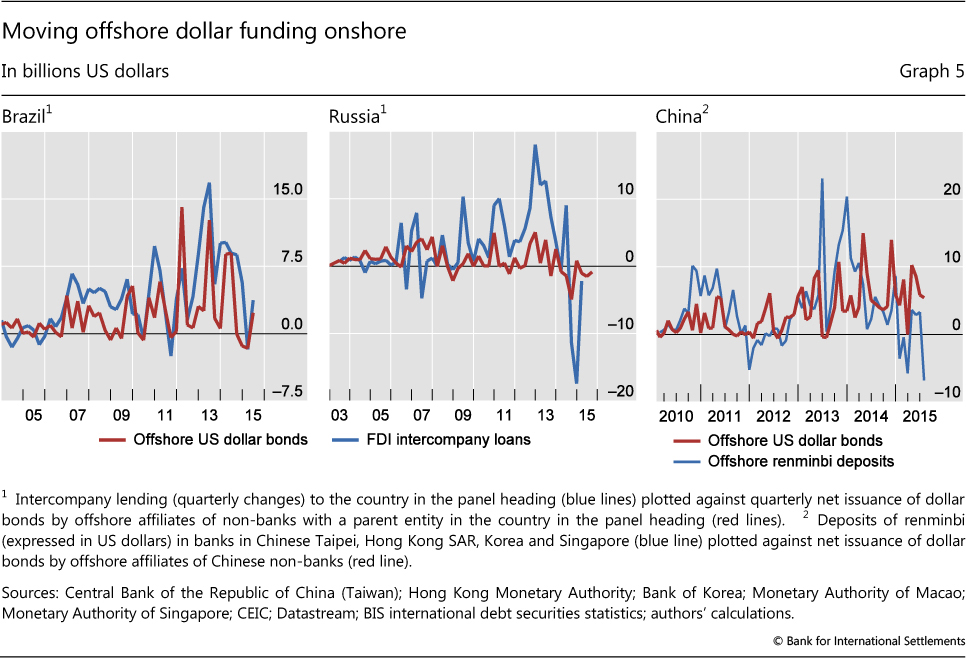

The repatriation of bond proceeds from offshore affiliates leaves a trail in the intercompany cross-border direct investment flows in the balance of payments (Avdjiev et al (2014)). According to Brazilian data, for example, intercompany loans tripled, from $67 billion to $206 billion between Q1 2009 and Q1 2015 (Graph 5, left-hand panel). Brazilian offshore dollar bonds outstanding also tripled then, from $34 billion to $107 billion, accounting for approximately half of the intercompany loans in Brazilian gross foreign direct investment. Hence, up to half of intercompany direct investment inflows into Brazil may represent the substitution of low-yielding dollar debt for higher-yielding domestic currency debt.

In China's case, there is a positive relationship between dollar issues by the offshore affiliates of Chinese non-banks and changes in offshore renminbi deposits in jurisdictions such as Hong Kong, Chinese Taipei and Singapore (Graph 5, right-hand panel). To some extent, Chinese firms may have used the proceeds of dollar bonds to accumulate offshore renminbi (which might show up in China's balance of payments as a renminbi deposit held by a non-resident bank). This would be consistent with the observation of Bruno and Shin (2015c), who uncovered evidence that dollar bond issuance responds to the same interest rate and exchange rate incentives that motivate the accumulation of offshore renminbi deposits.

Similarly to Brazil, intercompany lending by Russian firms tends to co-move with offshore US dollar issuance (Graph 5, centre panel), but the net issuance amounts to a much smaller fraction of intercompany lending flows. For example, only about half of the rise in intercompany flows is explained by offshore bond issuance in Q4 2010 and less than a third in Q4 2012. One reason for the difference with Brazil is that, while Brazilian firms issue bonds out of their own offshore subsidiaries, Russian firms have also relied on the services of banks elsewhere in Europe (at least prior to the sanctions). German and other banks were used to issue debt securities in Ireland or Luxembourg, backed by a loan participation note from a Russian firm's offshore affiliate, which then channelled the funds onshore. Hence, offshore US dollar funding raised indirectly via foreign banks supplemented US dollar bonds issued directly offshore by Russian firms.

The point to stress is that offshore dollar bond issues can show up in external debt statistics in a variety of ways. To the extent that dollar debt is obscured, corporate vulnerabilities can be understated.

Policy footprints

Policy measures can shape the composition of dollar credit: that is, whether loans are preferred to bonds; whether onshore loans are preferred to cross-border or offshore bank loans; and whether resident issuance is preferred to offshore bond issuance.

In Korea, policy discouraged dollar bank loans and thereby encouraged dollar bonds. A macroprudential levy was adopted in 2010 (operationalised in 2011) that, along with previous restrictive measures, raised the cost of dollar funding for banks in Korea. As a result, the growth of dollar loans in Korea slowed. Bruno and Shin (2014) find that the levy was associated with a decline in cross-border claims on Korea as compared with a control panel.13 The shift from US dollar bank loans to US dollar bond issuance boosted bonds to approximately half of the $128 billion in the US dollar debt of Korean non-banks, including both residents and offshore (Graph 1, top centre panel). This could be considered a case of regulatory arbitrage, but it could be more appropriately seen as an intended outcome. The bonds have a longer maturity than interbank deposits, reducing the risk of sudden massive outflows such as those experienced by Korea in Q1 1998 and Q4 2008.

Working in the opposite direction have been international sanctions on Russia. These deny some Russian firms and banks access to bond markets. The effect can be seen in the decline in the blue and yellow shaded areas in Graph 2, bottom left-hand panel, and a consequent shift towards reliance on dollar bank loans.

In China, the authorities' restricted foreign banks' ability to bring dollars into China. This was followed by a rapid increase in direct cross-border loans by banks outside China to non-banks in China (a divergence between the dotted red line and the top of the red area in the top left-hand panel of Graph 1). In addition, Chinese firms' offshore affiliates borrowed dollars from banks, as discussed above.

The Reserve Bank of India has eased restrictions on Indian firms' issuance of international bonds out of their offshore subsidiaries (Acharya et al (2015)). The yellow shaded area in the bottom left-hand panel of Graph 1 has accordingly grown in recent years.

Conclusion

We find that, underlying the generally rapid growth of dollar credit, the sheer variety of forms and channels for dollar borrowing can make for different vulnerabilities. Some countries rely on bank loans, others more on bonds. Some rely on bank loans booked by banks at home, others on cross-border loans. Some issue dollar bonds as obligations of headquarters at home, others as obligations of their offshore affiliates. Some of these differences bear the footprint of policy. Until recently, currency trends and interest rate differentials vis-à-vis the US dollar rewarded EME firms for substituting dollar borrowing for domestic currency borrowing. Policy measures helped to determine where and how this substitution took place.

The most recent data on foreign exchange loans in China and Hong Kong, as well as net issuance of US dollar bonds by EMEs, raise the question of whether dollar borrowing outside the United States will continue to expand. Changing macroeconomic and financial conditions - in particular, a shift in relative funding costs that might emerge from a tightening of US monetary policy - could lead dollar borrowers to repay dollar debt, and dollar creditors to seek repayment. This in turn could lead to a re-evaluation of the policy measures that have helped to shape these flows.

References

Acharya, V, S Cecchetti, J De Gregorio, S Kalemli-Özcan, P Lane and U Panizza (2015): Corporate debt in emerging economies: a threat to financial stability?, Committee for International Policy Reform, Brookings Institution.

Avdjiev, S, M Chui and H S Shin (2014): "Non-financial corporations from emerging market economies and capital flows", BIS Quarterly Review, December, pp 67-77.

Avdjiev, S, R McCauley and H S Shin (2015): "Breaking free of the triple coincidence in international finance", BIS Working Papers, no 524, October.

Bank for International Settlements (2015): "Highlights of the international banking statistics", BIS Quarterly Review, December.

Borio, C, R McCauley and P McGuire (2011): "Global credit and domestic credit booms", BIS Quarterly Review, September, pp 43-57.

Bruno, V and H S Shin (2014): "Assessing macroprudential policies: the case of South Korea", The Scandinavian Journal of Economics, vol 116(1), January, pp 128-57.

--- (2015a): "Capital flows and the risk-taking channel of monetary policy", Journal of Monetary Economics, vol 71, pp 119-32.

--- (2015b): "Cross-border banking and global liquidity", Review of Economic Studies, vol 82(2), April, pp 535-64.

--- (2015c): "Global dollar credit and carry trades: a firm-level analysis", BIS Working Papers, no 510, August.

Central Bank of the Republic of Turkey (2015): Financial Stability Report, May, p 25.

Chui, M, I Fender and V Sushko (2014): "Risks related to EME corporate balance sheets: the role of leverage and currency mismatch", BIS Quarterly Review, September, pp 35-47.

Chung, K, H Park and H S Shin (2015): "Mitigating systemic spillovers from currency hedging", in K Chung, S Kim, H Park, C Choi and H S Shin (eds), Volatile capital flows in Korea, Palgrave Macmillan, pp 217-44.

Fuertas, A and J Serena (2015): "How firms borrow in international bond markets: securities regulation and distribution of credit risks", mimeo.

He, D and R McCauley (2013): "Transmitting global liquidity to East Asia: policy rates, bond yields, currencies and dollar credit", BIS Working Papers, no 431, October.

International Monetary Fund (2015): "Corporate leverage in emerging markets - a concern?", Global Financial Stability Report, Chapter 3, October.

Ito, H and M Chinn (2015): "The rise of the redback: evaluating the prospects for renminbi use in invoicing", in B Eichengreen and M Kawai (eds), Renminbi internationalization: achievements, prospects, and challenges, Brookings Institution Press and the Asian Development Bank Institute, pp 111-58.

McCauley, R, P McGuire and V Sushko (2015): "Global dollar credit: links to US monetary policy and leverage", Economic Policy, vol 30(82), April, pp 187-229; also BIS Working Papers, no 483, January.

Mizen, P, F Packer, E Remolona and S Tsoukas (2012): "Why do firms issue abroad? Lessons from onshore and offshore corporate bond finance in Asian emerging markets", BIS Working Papers, no 401, December.

Shin, H S (2013): "The second phase of global liquidity and its impact on emerging economies", speech at the Federal Reserve Bank of San Francisco, November.

United Nations Conference on Trade and Development (2015): World Investment Report 2015, 25 June, p 5.

Yuen, A (2014): "Mainland-related exposures", Hong Kong Monetary Authority, inSight, 15 April.

1 This article expresses the views of the authors and not necessarily those of the BIS. Emerging market economies refer to "developing economies" in the BIS statistical tables. The authors thank Pablo García-Luna and Jeff Slee for research assistance and Claudio Borio, Ben Cohen and Hyun Song Shin for comments.

2 This includes $66 billion of bonds sold through affiliates located in the United States, which is excluded from the $9.8 trillion. There is (very minor) double-counting of debt issued by EME nationals as residents of another EME. Since the perspective here is on dollar credit to particular EMEs, these bonds are included in the measures discussed throughout this feature.

3 Data for these EME borrowers are available on the BIS website.

4 These US-based creditors extended only about a quarter of dollar credit to non-US non-bank borrowers. See Figure 3 in McCauley et al (2015).

5 In classifying bonds by sector, we look through the immediate borrower (eg Petrobras International Finance Company) to the ultimate borrower (in this case, Petrobras, an energy company). Thus, Petrobras issues are included in column 7 of Table 2 (non-financial corporates) and a non-financial aggregate can be constructed by excluding column 6 (non-bank financials). We exclude bonds issued by a bank, either as an ultimate issuer or as an immediate issuer (even a bank with a non-bank parent).

6 Most of the data are from the more than 40 jurisdictions that report to the BIS international banking statistics. For non-reporting countries (other than China, the Philippines and Russia), we proxy locally booked dollar loans to non-banks in these countries with cross-border loans to banks in these countries. For China, the Philippines and Russia, proxies are based on national data.

7 As discussed below, bonds issued by foreign entities resident in these economies contribute little, ie generally less than 5% of total bonds outstanding; see Table 2.

8 The HKMA survey was not intended to complement the residence-based bank loan data. As a result, some loans included in Graph 3 double-count cross-border claims on mainland residents.

9 Central Bank of the Republic of Turkey (2015) reports a sharp rise in net foreign currency liabilities of non-financial firms (from $63 billion to $150 billion) between 2009 and 2014.

10 Large established firms issuing global bonds are subject to full US Securities and Exchange Commission (SEC) disclosure rules, but Fuertas and Serena (2015) find that EME firms often opt for the lighter disclosure for bonds marketed to US institutional investors (under SEC rule 144A) or in eurobond markets. Lighter regulation attracts firms with poorer credit quality.

11 Figures from Bloomberg.

12 Dollar bond issuance tends to be concentrated among a few issuers in each country; the top five issuers account for over half of outstanding bonds in all but the larger economies. Non-banks' dollar bonds are overwhelmingly long-term.

13 As in the case of on-balance sheet dollar loans, virtual dollar debt through forward dollar sales (see above) has not grown much, constrained as it is by the macroprudential levy and other measures.