Is the unthinkable becoming routine?

Abstract

Globally, interest rates have been extraordinarily low for an exceptionally long time, in nominal and inflation-adjusted terms, against any benchmark. Such low rates are the most remarkable symptom of a broader malaise in the global economy: the economic expansion is unbalanced, debt burdens and financial risks are still too high, productivity growth too low, and the room for manoeuvre in macroeconomic policy too limited. The unthinkable risks becoming routine and being perceived as the new normal.

This malaise has proved exceedingly difficult to understand. The chapter argues that it reflects to a considerable extent the failure to come to grips with financial booms and busts that leave deep and enduring economic scars. In the long term, this runs the risk of entrenching instability and chronic weakness. There is both a domestic and an international dimension to all this. Domestic policy regimes have been too narrowly concerned with stabilising short-term output and inflation and have lost sight of slower-moving but more costly financial booms and busts. And the international monetary and financial system has spread easy monetary and financial conditions in the core economies to other economies through exchange rate and capital flow pressures, furthering the build-up of financial vulnerabilities. Short-term gain risks being bought at the cost of long-term pain.

Addressing these deficiencies requires a triple rebalancing in national and international policy frameworks: away from illusory short-term macroeconomic fine-tuning towards medium-term strategies; away from overwhelming attention to near-term output and inflation towards a more systematic response to slower-moving financial cycles; and away from a narrow own-house-in-order doctrine to one that recognises the costly interplay of domestic-focused policies. One essential element of this rebalancing will be to rely less on demand management policies and more on structural ones, so as to abandon the debt-fuelled growth model that has acted as a political and social substitute for productivity-enhancing reforms. The dividend from lower oil prices provides an opportunity that should not be missed. Monetary policy has been overburdened for far too long. It must be part of the answer but cannot be the whole answer. The unthinkable should not be allowed to become routine.

Full text

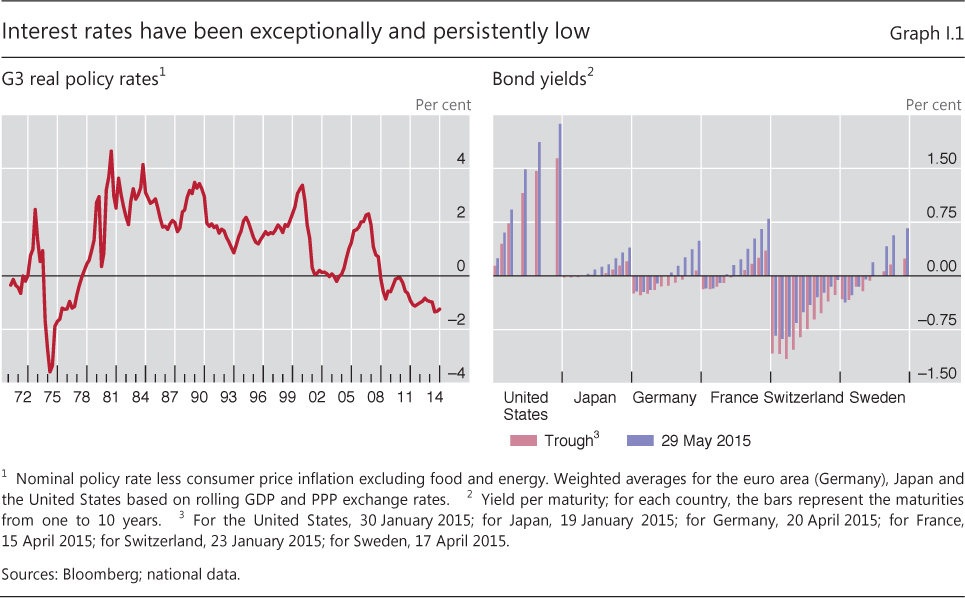

Interest rates have never been so low for so long (Graph I.1). They are low in nominal and real (inflation-adjusted) terms and low against any benchmark. Between December 2014 and end-May 2015, on average around $2 trillion in global long-term sovereign debt, much of it issued by euro area sovereigns, was trading at negative yields. At their trough, French, German and Swiss sovereign yields were negative out to a respective five, nine and 15 years. Such yields are unprecedented. Policy rates are even lower than at the peak of the Great Financial Crisis in both nominal and real terms. And in real terms they have now been negative for even longer than during the Great Inflation of the 1970s. Yet, exceptional as this situation may be, many expect it to continue. There is something deeply troubling when the unthinkable threatens to become routine.

Such low rates are only the most obvious symptom of a broader malaise, despite the progress made since the crisis. Global economic growth may now be not far from historical averages but it remains unbalanced. Debt burdens are still high, and often growing, relative to output and incomes. The economies hit by a balance sheet recession are still struggling to return to healthy expansion. In several others, financial imbalances show signs of building up, in the form of strong credit and asset price increases, despite the absence of inflationary pressures. Monetary policy has taken on far too much of the burden of boosting output. And in the meantime, productivity growth has continued to decline.

This malaise has proved exceedingly hard to understand. Debates rage. Building on last year's analysis, this Annual Report offers a lens through which to interpret what is going on. The lens focuses on financial, medium-term and global factors, whereas the prevailing perspective focuses more on real, short-term and domestic factors.

We argue that the current malaise may to a considerable extent reflect a failure to come to grips with how financial developments interact with output and inflation in a globalised economy. For some time now, policies have proved ineffective in preventing the build-up and collapse of hugely damaging financial imbalances, whether in advanced or in emerging market economies (EMEs). These have left long-lasting scars in the economic tissue, as they have sapped productivity and misallocated real resources across sectors and over time.

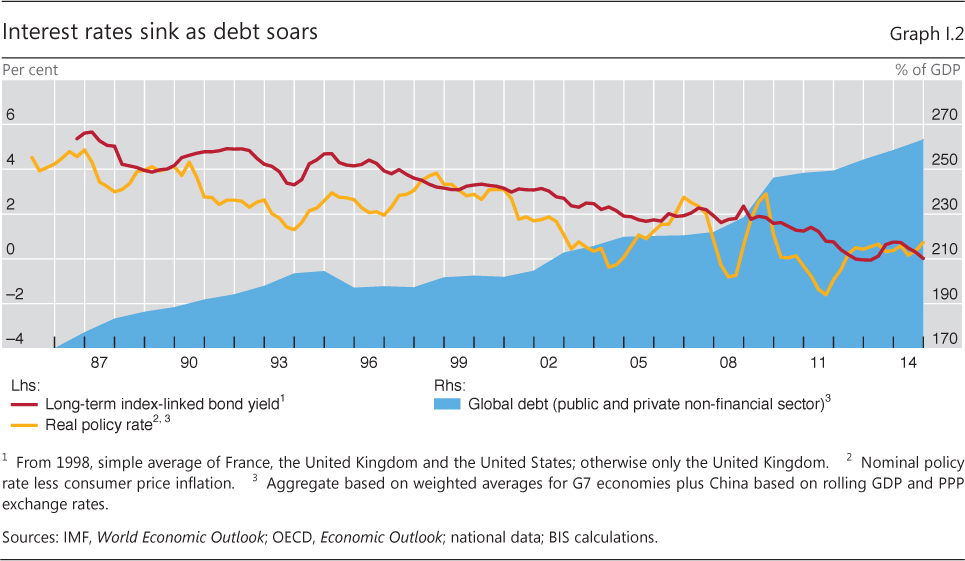

Our lens suggests that the very low interest rates that have prevailed for so long may not be "equilibrium" ones, which would be conducive to sustainable and balanced global expansion. Rather than just reflecting the current weakness, low rates may in part have contributed to it by fuelling costly financial booms and busts. The result is too much debt, too little growth and excessively low interest rates (Graph I.2). In short, low rates beget lower rates.

There is a domestic and an international dimension to all this. Domestic policy regimes have been too narrowly concerned with short-term output and inflation stabilisation, losing sight of slower-moving but more costly financial cycles. And the international monetary and financial system (IMFS) has exacerbated these shortcomings. This has been most evident post-crisis. As monetary policy in the core economies has pressed down hard on the accelerator but failed to get enough traction, pressures on exchange rates and capital flows have spread easy monetary and financial conditions to countries that did not need them, supporting the build-up of financial vulnerabilities. A key manifestation has been the strong expansion of US dollar credit in EMEs, mainly through capital markets. The system's bias towards easing and expansion in the short term runs the risk of a contractionary outcome in the longer term as these financial imbalances unwind.

The right response is hard to implement. The policy mix will be country- specific, but its general features are not. What is required is a triple rebalancing in national and international policy frameworks: away from illusory short-term macroeconomic fine-tuning towards medium- term strategies; away from overwhelming attention to near-term output and inflation towards a more systematic response to slower-moving financial cycles; and away from a narrow own-house-in-order doctrine to one that recognises the costly interplay of domestic-focused policies.

In this rebalancing, one essential element will be to rely less on demand management policies and more on structural ones. The aim is to replace the debt-fuelled growth model that has acted as a political and social substitute for productivity-enhancing reforms. The dividend from lower oil prices provides an opportunity that should not be missed. Monetary policy, overburdened for far too long, must be part of the answer, but it cannot be the whole answer.

The rest of the chapter digs further into the problem in a quest to unearth its possible solution. The first section reviews the global economy's evolution in the past year and assesses the prospects and risks ahead. The second provides the suggested lens through which to understand the forces that have been shaping, and will continue to shape, that evolution. The third considers the policy implications.

The global economy: where it is and where it may be going

Looking back: recent evolution

Where did we leave the economy at this point in time last year? Output growth was not far away from historical averages; and advanced economies (AEs) were gaining momentum even as EMEs had lost some. Except in a few EMEs, inflation was low, in some notable cases below central bank targets. Subdued risk-taking in the real economy contrasted with aggressive risk-taking in financial markets: anaemic investment coexisted with buoyant asset prices and unusually low volatility. Market performance seemed to hinge on extraordinary monetary accommodation as stock and bond indices responded to central bankers' every word and deed. As bank balance sheets in crisis-hit economies were slowly healing, market-based finance was surging. The balance sheets of the non- financial private sector were evolving along a clear divide: in crisis-hit countries the sector was deleveraging at varying but slow speeds; elsewhere it was leveraging up, sometimes uncomfortably fast. Fiscal policy was generally under strain, with debt-to-GDP ratios continuing to rise even as several AEs consolidated their finances. As a result, global private plus public sector debt-to-GDP ratios were edging up. Monetary policy was testing what, at the time, appeared to be its outer limits.

Since then, there have been two major developments. First, the oil price has fallen sharply, with lesser declines for other commodities. The drop of around 60% from July 2014 to March 2015 was the third largest in the last half-century, after those following the Lehman default and the OPEC cartel breakdown in 1985. The price has only partially recovered since then. Second, the US dollar has appreciated strongly. Over the same period, the dollar's trade-weighted exchange rate rose by around 15% - one of the sharpest appreciations on record within a similar window. The shift has been especially large vis-à-vis the euro.

Much ink has been spilled on the oil price. But, like that of any other asset, the price of oil is driven by a combination of market expectations about future production and consumption, risk attitudes and financing conditions (Chapter II). This time, a key factor was the realisation that OPEC had become more concerned about market share and would no longer restrict production as in the past - a true game changer. This explanation better fits the timing and steepness of the price drop than do worries about weakening global demand. In addition, hedging activity by highly indebted individual producers may have played a role.

Regardless of its drivers, the oil price drop has already provided, and will continue to provide, a welcome boost to the global economy (Chapter III). A fall in the price of a key input in global production is bound to be expansionary. This will be all the more visible to the extent that it does not reflect a fall in global demand. Even so, there will be obvious gainers and losers, and the interaction of oil price trends with financial vulnerabilities bears watching (see below).

The sharp dollar appreciation has multiple causes and uncertain effects. It started when firming expectations of divergent macroeconomic conditions and central bank policies made US dollar assets relatively more attractive. It became entrenched once the ECB surprised markets with its large-scale asset purchase programme. The impact of the appreciation through trade is mainly redistributional but welcome to the extent that it has shifted growth momentum from stronger to weaker economies. But the ultimate impact will depend on its imprint on financial vulnerabilities and on how policies, not least monetary policies, in turn react to currency movements. Here, the large stock of dollar debt run up by non-US residents looms large (see below).

Together, the oil price drop and dollar appreciation help explain, and in part reflect, the further plunge of short- and long-term interest rates. They help explain it to the extent that a lower oil price has added to global disinflationary pressures. They reflect it to the extent that exceptionally easy monetary policy in some jurisdictions prompts easing elsewhere. Just think of the Swiss National Bank's or the Danish central bank's decision to test the limits of negative interest rates as the exchange rates came under huge pressure.

Where has this left the world? On the surface, perhaps, not far from where we left it last year. Global growth is little changed, and the rotation from EMEs to AEs has continued. Inflation is somewhat lower, due mainly to temporary and positive supply side factors (Chapter IV). Financial markets have shown mixed signals: volatility has normalised somewhat and risk-taking in corporate debt markets has eased, especially in EMEs. Yet equity prices have soared further and markets still seem to take their cue from central bank policies (Chapter II). US monetary policy normalisation appears closer, but the timing is still uncertain. Banks have continued to heal, although doubts remain, and this has further boosted market-based finance (Chapter VI). Private sector balance sheets have evolved further in the same direction, with some countries deleveraging and others leveraging up, but little has changed overall (Chapter III).

Beneath the surface, though, the medium-term risks and tensions have increased, inherent as they are in a faulty debt-fuelled global growth model. And it is to these risks and tensions that we now turn.

Looking ahead: risks and tensions

To understand the main medium-term risks, it is useful to divide countries into two groups: those that were badly hit by the Great Financial Crisis, and those that were not. For, almost a decade on, the long shadow of the crisis is still with us (Chapter III).

In the least affected countries, the main risk is that of peaking domestic financial cycles, often coupled with external vulnerabilities. This group includes some AEs, notably commodity exporters, and many EMEs, notably some of the largest. In these economies, prolonged domestic credit booms have taken private sector debt-to-GDP ratios to new heights, often in tandem with strong increases in property prices. And in a number of them, as in the past, external sources of credit expansion, especially in foreign currency, have played a role. For example, US dollar credit to non-banks in EMEs has almost doubled since early 2009, to exceed $3 trillion. Especially at risk are commodity exporters, buoyed by a commodity "supercycle" and turbocharged by exceptionally easy global funding conditions. No wonder that estimates for potential growth rates have already halved in Latin America. China plays a pivotal role in all this: it is a huge economy and commodity importer that has slowed considerably under the weight of its pervasive financial imbalances.

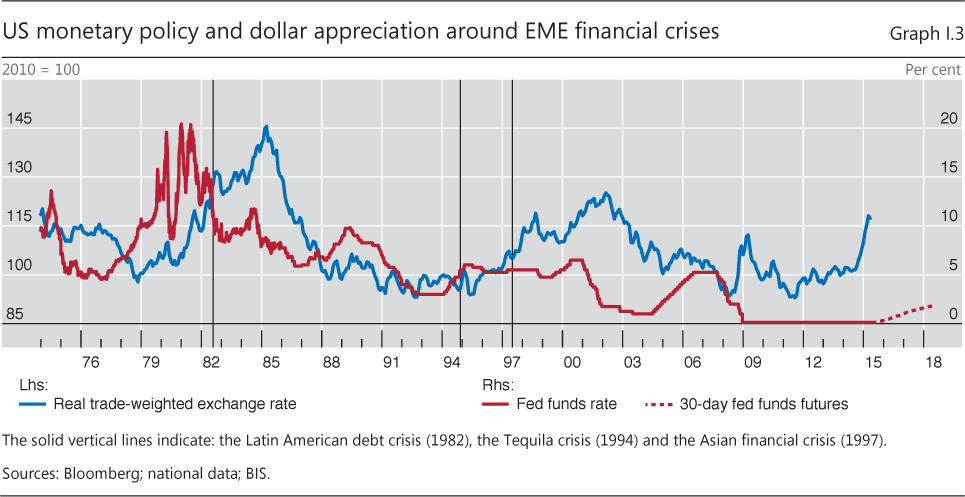

In several respects, EMEs are in better shape than in the 1980s and 1990s, when tighter monetary conditions in the United States and an appreciating dollar triggered crises (Graph I.3). Macroeconomic frameworks are stronger and exchange rates more flexible. The financial system infrastructure is more robust, and prudential regulation, not least the macroprudential setup, is tighter. For instance, despite the eye-catching US dollar figures, foreign exchange debt as a percentage of GDP is not as high as in the past. Indeed, that was the aim of developing local currency bond markets - to put an end to "original sin". And foreign exchange reserves are now much larger.

Even so, caution is called for. A seemingly solid performance in terms of growth, low inflation and fiscal probity did not insulate Asian economies in the 1990s. Foreign exchange exposures are now concentrated in the corporate sector, where currency mismatches are harder to measure. There are limits to how far official reserves can be mobilised to plug private sector funding liquidity shortfalls or to defend currencies. And it remains to be seen how the shift from banks to asset managers will influence asset price dynamics: the size asymmetry between suppliers and recipients of funds has not got any smaller, and markets could react violently if pressures became one-sided - liquidity will certainly evaporate in the heat of a rush for the exits. The 2013 "taper tantrum" was only an incomplete test: it reflected traditional balance of payments and macroeconomic concerns, but did not coincide with any more damaging unwinding of domestic financial imbalances.

One thing is for sure: gone are the days when what happened in EMEs largely stayed there. The EMEs' heft in the global economy has soared since the Asian crisis, from about one third to almost half of global GDP in purchasing power terms. And in some cases, their external financial exposures can be quite large from a global perspective, even if small in relation to the domestic economy. Take, in particular, China. At end-2014, it was the world's eighth largest borrower in terms of the $1 trillion in cross-border bank claims - double the amount outstanding just two years before - or the 11th largest on the more than $450 billion its nationals had borrowed in international debt securities markets by end-March 2015.

Different risks attend the countries most affected by the crisis, which are still deleveraging or starting to releverage. Three are worth highlighting.

The first relates to the medium-term costs of persistent ultra-low interest rates. These can inflict serious damage on the financial system (Chapters II and VI). Such rates sap banks' interest margins and returns from maturity transformation, potentially weakening balance sheets and the credit supply, and are a source of major one-way interest rate risk. Ultra-low rates also undermine the profitability and solvency of insurance companies and pension funds. And they can cause pervasive mispricing in financial markets: equity and some corporate debt markets, for instance, seem to be quite stretched. Such rates also raise risks for the real economy. In the shorter term, the plight of pension funds is just the most visible reminder of the need to save more for retirement, which can weaken aggregate demand. Over a longer horizon, negative rates, whether in inflation-adjusted or in nominal terms, are hardly conducive to rational investment decisions and hence sustained growth. If the unprecedented journey towards lower negative nominal interest rates continues, technical, economic, legal and even political boundaries may well be tested.

The second risk relates to the prolonged reliance on debt as a substitute for productivity-enhancing reforms. It is always tempting to postpone adjustment, even though the drag that high public debt can exert on growth has been well documented. Ageing populations compound this challenge in at least two ways. Economically, they make the debt burden much harder to bear. Politically, they heighten the temptation to boost output temporarily through demand management policies: the tyranny of headline growth figures, unadjusted for demographics, contributes to this. For example, it is not remarked often enough that, in terms of its working age population, Japan's growth has outpaced that of many of its advanced economy peers, not least the United States. On that basis, in 2000-07, Japan grew at a cumulative rate of 15%, almost twice as fast as the United States (8%) - the reverse of what headline growth rates show (10% and 18%). The difference is even bigger if the post-crisis years are also considered.

The third risk relates to the Greek crisis and its impact on the euro area. In some respects, developments in Greece, and in the euro area more generally, are akin to the broader global challenges but amplified by institutional specificities - a toxic mix of private and public debt and too little commitment to badly needed structural adjustments. As a result, monetary policy, seen as a quick fix to buy time, has borne the brunt of the burden. On strictly economic grounds, the euro area seems better placed to cope with contagion than when the crisis first broke out. Yet uncertainty lingers, and the potential for political contagion is even harder to assess.

Not included in this list is the risk of persistently low inflation or outright deflation. True, the risk depends on country-specific factors. But the current policy debate tends to overplay it (Chapter IV). First, it is sometimes not stressed enough that recent price declines largely reflect the fall in oil and other commodity prices. Their transient impact on inflation should be superseded by the longer-lasting boost to expenditure and output, especially in energy-importing countries. Second, there is a tendency to draw general conclusions from the Great Depression - a unique episode that may have had more to do with the large drop in asset prices and with banking crises than with deflation per se. In general, the longer historical record reveals that the link between deflation and growth is a weak one. Finally, the evidence also suggests that the real economic damage has so far stemmed from the interplay of debt with property prices, and not so much with goods and services prices, as the latest recession confirms. At the same time, policy responses should also take into account our still limited understanding of the inflation process.

The resulting picture is that of a world that has been returning to stronger growth but where medium-term tensions persist. The wounds left by the crisis and subsequent recession are healing, because balance sheets are being repaired and some deleveraging has taken place. Recently, the strong and unexpected boost from energy prices has helped too. In the meantime, monetary policy has done its utmost to support near-term demand. But the policy mix has relied too much on measures that, directly or indirectly, have entrenched dependence on the very debt-fuelled growth model that lay at the root of the crisis. These tensions manifest themselves most visibly in the failure of global debt burdens to adjust, the continued decline in productivity growth and, above all, the progressive loss of policy room for manoeuvre, both fiscal and monetary.

The deeper causes

Why has this happened? One possible answer lies in a blend of politics and ideas. The natural bias of political systems is to encourage policies that buy short-term gain at the cost of risking long-term pain. The reasons are well known and need no elaboration here. But, as ideas influence policy, their effect becomes all the more insidious because of that bias. Thus, the pressing question is whether prevailing economic paradigms are sufficiently good guides for policy.

Ideas and perspectives

Once the crisis broke out, there was widespread agreement that the dominant macroeconomic perspectives had failed to ward off the crisis because they ruled it out. To simplify somewhat, the presumption was that price stability was sufficient for macroeconomic stability and that either the financial system was self-stabilising or that its failure could not be very damaging.

Unfortunately, progress in tackling these shortcomings has been disappointing. Financial factors still appear to be hovering at the periphery of macroeconomic thinking. True, huge efforts have been made to bring them closer to the core: economists have worked hard to develop models that can accommodate them. But these efforts have not yet permeated deeply enough into the policy debate: macroeconomic stability and financial stability remain uncomfortable bedfellows.

If one strips the prevailing analytical view of all its nuances and focuses on how it is shaping the policy debate, its basic logic is simple. There is an excess or shortfall of final demand for domestic production (an "output gap") that determines domestic inflation, not least by underpinning inflation expectations. Aggregate demand policies are then used to eliminate that gap and so achieve full employment and stable inflation; fiscal policy affects spending directly, and monetary policy indirectly, through real (inflation-adjusted) interest rates. The exchange rate, if allowed to float, permits the authorities to set monetary policy freely in line with domestic needs and will, over time, also balance the current account. If each country adjusts its monetary and fiscal levers so as to close the output gap period by period, everything will be fine, domestically and globally.

Of course, to varying degrees, financial factors do make their appearance. For instance, in some cases too much debt is seen as widening the demand shortfall. In others, the possibility of financial instability is fully recognised. But then, at the end of the day, when all is said and done, the basic conclusions do not change. All demand shortfalls should be treated equally, ie through standard aggregate demand policies. And financial instability should best be addressed separately, through prudential policy, albeit with a stronger systemic (macroprudential) orientation. Following a tidy separation principle, monetary and fiscal policies are best left free to address standard macroeconomic concerns, very much as before. From this perspective, we are back in the familiar pre-crisis world. It feels oddly like Groundhog Day.

Last year's Annual Report offered a different analytical lens that brought different policy conclusions into view. That lens seeks to bring financial factors back to the core of macroeconomics, and stresses the medium term over the short term and the global over the domestic. Three basic elements, developed further in this year's Report, are essential.

First, the behaviour of inflation may not be a fully reliable guide to sustainable (or potential) output. This is because financial imbalances often build up when inflation is low and stable, declining or even negative. The hallmarks of these imbalances are booming credit and asset prices, particularly property prices, and signs of aggressive risk-taking in financial markets, such as low credit spreads and falling volatility. When these financial booms finally collapse, they can cause devastating and long-lasting economic damage. This was clearly true of the Great Financial Crisis. But that episode simply replayed a recurrent historical pattern, from the pre-Great Depression financial boom in the United States - prices actually fell for part of the roaring 1920s - to the crisis in Japan in the early 1990s and those in Asia in the mid-1990s.

If financial booms have common characteristics, it should be possible to identify some of the danger signals in advance. And the evidence does indicate that proxies for such financial booms can provide useful information about the risks ahead as events unfold (in "real time"). Such indicators would have helped establish that output was running above its sustainable, or potential, level ahead of the most recent crisis in the United States - something that typical estimates used in policymaking, partly distorted by subdued inflation, have done only ex post, as they rewrite history based on new information (Box IV.C). This is the reason why, for the United States, knowledge of the deviations of the debt service ratio and leverage from their long-term values in the mid-2000s would have helped project the behaviour of output during the subsequent recession and recovery (Box III.A). And it explains why the behaviour of credit and property prices during the boom, or that of the debt service ratio or even that of credit growth alone, has proved a useful indicator of future banking distress and costly recessions across countries.

Why is inflation an insufficiently reliable signal of sustainability, contrary to what the prevailing paradigm suggests? There are at least two possible reasons.

One has to do with the type of credit expansion involved. Instead of financing the purchase of newly produced goods or services, which lifts expenditures and output, strong credit growth may simply be paying for existing assets, either "real" (eg housing or companies) or financial (eg simple assets or more complex forms of financial engineering). Neither of these impinges directly on inflationary pressures.

The other has to do with what explains (dis)inflation. Supply-driven disinflations tend to boost output while providing fertile ground for the build-up of financial imbalances. Examples include forces such as the globalisation of the real economy (eg the entry of former communist countries into the world trading system), technological innovation, greater competition, and falling prices for key production inputs such as oil. The difference between supply- and demand-driven disinflations may well explain the historically weak empirical link between deflation and growth.

Second, the busts that follow financial booms do much more damage, and are less amenable to traditional aggregate demand policies. Growing empirical evidence indicates that the corresponding recessions are deeper, subsequent recoveries weaker, output potential permanently lost, and post-recession growth rates possibly lower. Indeed, the post-crisis experience has followed a similar pattern, despite the unprecedented monetary stimulus and initial fiscal expansion.

The reasons have to do with the strong undercurrents that the boom leaves in its wake. The financial sector is broken. Households and/or companies face large debt overhangs and asset quality problems. And, importantly, financial booms interact perversely with productivity growth. They can mask its secular decline, eroded by structural deficiencies, behind an illusory feel-good factor (see the 84th Annual Report). They can also undermine it more directly, by causing long-lasting resource misallocations, in both capital and labour (Box III.B). Taking cross-country estimates at face value, the impact can be quite large, up to nearly 1 percentage point per year during the boom and much larger after a crisis breaks out.

Under these conditions, and once the acute financial crisis phase is over, aggregate demand policies are pushing on a string. Undercapitalised financial institutions restrict and misallocate credit. Overindebted borrowers pay back debt. And misallocated resources cannot respond to an indiscriminate stimulus. In other words, not all output gaps are born equal, amenable to identical remedies; and post-crisis their size may not be as large as it appears. Thus, unless the underlying problems are addressed head-on, short-term gain may be purchased at the price of long-term pain: debt does not come down sufficiently, the policy room for manoeuvre shrinks further and the seeds are sown for the next financial bust. None of this, however, means higher inflation. Paradoxically, an easing bias in the short term may end up being contractionary longer-term.

Third, when the exchange rate becomes the point of least resistance, problems can be exacerbated globally. Since after a financial bust monetary policy has only limited traction on expenditures through domestic channels, the responsiveness of inflation and output to the exchange rate is stronger. Currency depreciation has a more immediate, mechanical effect on prices. And to the extent that it diverts demand away from other countries, it can boost output. But if, as argued below, exchange rates fail to insulate countries sufficiently from external influences, the appreciations will be resisted and the end result will be competitive depreciations and a looser monetary policy stance globally. Thus, if, on balance, policies are already too loose for lasting financial and macroeconomic stability, because of an unbalanced policy mix, the outcome will be worse. Once more, short-term gain may result in long-term pain.

Excess financial elasticity

It is now possible to put these various pieces together and diagnose what may be wrong with the functioning of the global economy. In this view, policies have been unable to constrain the build-up and collapse of damaging financial booms, ie the global economy exhibits "excess financial elasticity" - think of an elastic band that can be stretched out further and further until, eventually, it snaps back more painfully. This reflects three shortcomings: in the interplay between financial markets and the economy; in domestic policy regimes; and in the interaction of these regimes through the IMFS. Take each in turn.

By now, there is a keen appreciation that self-equilibrating forces in the financial system are weak, and that this can amplify business fluctuations. There is a mutually reinforcing feedback between loosely anchored perceptions of risk and value, on the one hand, and weak financing constraints, on the other. For a (long) while, asset valuations soar, risk-taking increases and financing becomes easier until, at some point, the process goes into reverse. Thus, the financial system is said to be "procyclical". The crisis revealed this once more, and with a vengeance.

The degree of procyclicality, or the system's elasticity, hinges on domestic policy regimes, and their evolution has increased it. First, financial liberalisation back in the 1980s eased financing constraints and made funding easier and cheaper to obtain. Meanwhile, prudential safeguards have lagged behind. Second, the emergence of monetary policy regimes focused on near-term inflation control has meant that policy would be tightened during financial booms only if inflation increased but would then be loosened aggressively and persistently during busts. Third, fiscal policy has failed to recognise the hugely flattering effect that financial booms have on fiscal accounts and the limited effectiveness of untargeted measures during busts. Taken together, these developments have resulted in an easing bias that allows financial booms to grow bigger, last longer and collapse more violently.

Importantly, the current IMFS has further increased this excess elasticity through the interaction of monetary and financial regimes (Chapter V).

The interaction of monetary regimes has spread the easing bias from the core economies to the rest of the world. This happens directly, because key international currencies - above all, the US dollar - are extensively used outside the issuing country's borders. Thus, the core countries' monetary policies directly influence financial conditions elsewhere. More importantly, an indirect effect works through the aversion of policymakers to unwelcome exchange rate appreciation. As a result, policy rates are kept lower and, if countries resort to foreign exchange intervention, yields are further compressed once the proceeds are invested in reserve currency assets.

The interaction of financial regimes, through the free mobility of capital across currencies and borders, reinforces and channels these effects. Freely mobile capital adds a key external source of funding during domestic booms. And it makes exchange rates subject to "overshooting" for exactly the same reasons as domestic asset prices are, ie loosely anchored perceptions of values, risk-taking and ample funding. Think, for instance, of popular strategies such as momentum trading and carry trades; or of the self-reinforcing feedback between exchange rate appreciation, lower foreign currency debt burdens and risk-taking. More generally, free capital mobility generates surges in risk-taking across countries, regardless of their specific conditions, inducing strong co-movements in long-term yields, asset prices and financing flows. Again, the stronger and more long-lasting these surges are, the more violent the subsequent reversal. Global liquidity, or the ease of financing in international markets, moves in irregular but powerful waves.

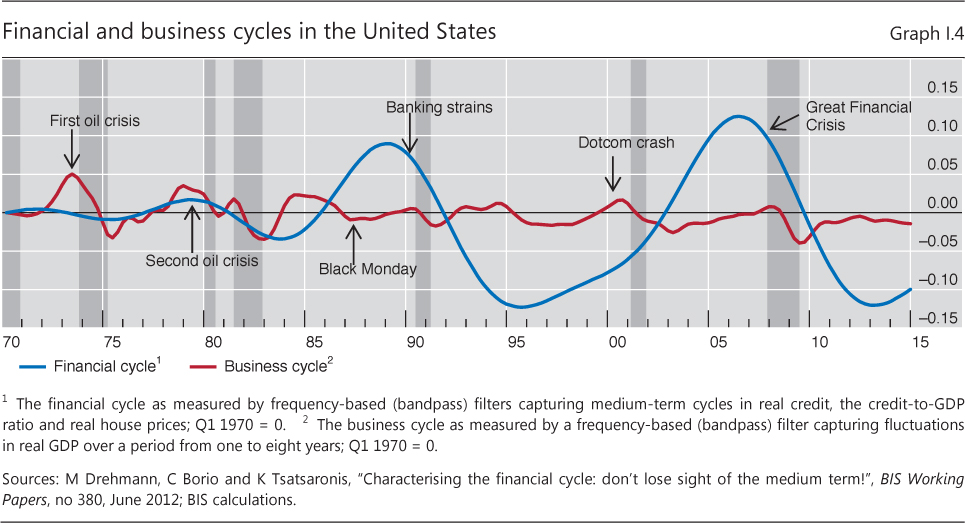

The historical evidence is broadly consistent with these observations. The lens helps explain why the scale and duration of financial booms and busts (financial cycles) have increased since the early 1980s (Graph I.4) - a development also supported by the progressive globalisation of the real economy, as trade barriers have come down and new countries have joined in, boosting global growth prospects while generating disinflationary pressures. It helps explain why, globally, inflation-adjusted interest rates have trended down and appear quite low regardless of benchmarks and why foreign exchange reserves have soared. It helps explain why, post-crisis, US dollar credit has surged outside the United States, directed largely towards EMEs. And it helps explain why we have been seeing signs of the build-up of financial imbalances in EMEs as well as in some advanced economies less affected by the crisis and highly exposed to international influences.

Note that, in this story, current account imbalances do not figure prominently. Current account deficits need not coincide with the build-up of financial imbalances. In fact, some of the most damaging financial imbalances in history have occurred in surplus countries - most spectacularly in the United States before the Great Depression and Japan from the late 1980s. And strong financial booms have recently occurred, or are now taking place, in several surplus countries, including China, the Netherlands, Sweden and Switzerland. The relationship between current accounts and financial imbalances is more nuanced: a reduction in the surplus or increase in the deficit tends to reflect the build-up of those imbalances. This has policy implications to which we will return.

Why are interest rates so low?

All this raises the fundamental question that lies at the heart of the current policy debate: Why are market interest rates so low? And are they "equilibrium (or natural) rates", ie are they where they should be? How are the market and equilibrium rates determined? The prevailing analytical perspective and the one proposed in this Report come up with different answers.

Most holders of either view would agree that market interest rates are determined by the interplay of central banks' and market participants' decisions (Chapter II). Central banks set the short-term policy rate and influence long-term rates through signals about how they will set short-term rates and, increasingly, through large-scale purchases along the maturity spectrum. Market participants set deposit and loan rates and, through their portfolio choices, help determine longer-term market rates. Their decisions will reflect many factors, including risk appetite, views about profitable investments, regulatory and accounting constraints and, of course, expectations about what central banks will do (Chapter II). In turn, actual inflation determines ex post inflation-adjusted rates and expected inflation ex ante real rates.

But are the interest rates that prevail in the market actually equilibrium rates? Take first the short-term rate, which central banks set. When we read that central banks can have only a transitory impact on inflation-adjusted short-term rates, what is really meant is that, at some point, unless central banks set them at their "equilibrium" level, or sufficiently close to it, something "bad" will happen. Exactly what that "bad" outcome is will depend on one's view of how the economy works.

In the prevailing view - one embedded in the popular "savings glut" and "secular stagnation" hypotheses - the answer is that inflation will rise or fall, possibly even turn into deflation. Inflation provides the key signal, and its behaviour depends on the degree of economic slack. The corresponding equilibrium rate is also known as the "Wicksellian" natural rate: it equates output with its potential, or saving and investment at full employment. To be sure, in practice policymakers also consider economic slack independently. But, in the final analysis, since slack is very hard to measure, they tend to revise its estimate based on what happens to inflation. For example, if unemployment falls below its presumed "equilibrium" level but inflation does not increase, they will infer that there is still slack in the economy.

In the view proposed here, inflation need not reliably signal that rates are at their "equilibrium" level. Rather, the key signal may be the build-up of financial imbalances. After all, pre- crisis, inflation was stable and traditional estimates of potential output proved, in retrospect, far too optimistic. If one acknowledges that low interest rates contributed to the financial boom whose collapse caused the crisis, and that, as the evidence indicates, both the boom and the subsequent crisis caused long-lasting damage to output, employment and productivity growth, it is hard to argue that rates were at their equilibrium level. This also means that interest rates are low today, at least in part, because they were too low in the past. Low rates beget still lower rates. In this sense, low rates are self-validating. Given signs of the build-up of financial imbalances in several parts of the world, there is a troubling element of déjà vu in all this.

Shifting the focus from short-term to long- term rates does not change the picture. There is no reason to presume that these long-term rates will be at their equilibrium level any more than short-term rates are. Central banks and market participants fumble in the dark, seeking either to push rates towards equilibrium or to profit from their movement. After all, long-term rates are just another asset price. And asset prices often do follow unsustainable and erratic paths, as when they are at the root of financial instability.

Policy implications

What are the policy implications of this analysis? The first is that monetary policy has been overburdened for too long, especially post-crisis. The second, more general one, is the need to rebalance policies away from aggregate demand management to initiatives that are more structural in character. True, this is politically difficult. But there is no other way to sustainably raise output and productivity growth and to shake off debt addiction. The specific blend of measures will naturally be country- specific, but it will generally involve improving the flexibility of product and labour markets, providing an environment conducive to entrepreneurship and innovation, and boosting labour force participation. This would also help relieve the huge pressure that has been placed post-crisis on fiscal and, above all, monetary policy. The oil dividend provides a tailwind for implementing such reforms and should not be wasted. The analysis is also a wake-up call for commodity exporters that may be tempted to avoid painful adjustments as their revenues fall sharply.

Beyond this, there are questions about how best to adjust policy frameworks, nationally and internationally, in order to take financial factors more systematically into account and about what to do at the current juncture.

Adjusting frameworks

As noted in last year's Annual Report, constraining the excess financial elasticity of individual economies calls for broad-based adjustments in domestic fiscal, prudential and monetary frameworks. The basic strategy would be to rein in financial booms more deliberately and to address financial busts more effectively. Compared with current ones, the resulting policies would be less asymmetrical over financial cycles, less procyclical and less biased towards easing over successive booms and busts. Take each type of policy in turn.

The priority for fiscal policy is to ensure that it behaves countercyclically and that it preserves sufficient room for manoeuvre during busts. This means, first and foremost, ensuring long-term sustainability - a daunting challenge in many jurisdictions (Chapter III). It also means exercising extra prudence during financial booms, so as not to overestimate the underlying solidity of fiscal positions: sustainable output and growth look rosy, fiscal revenues are bloated, and the contingent liabilities needed to deal with the bust remain hidden. During a bust, that fiscal space should ideally be used to speed up private sector balance sheet repair. This applies to banks - but only if private sector backstops prove insufficient - and non-banks alike. The range of options includes recapitalisation, temporary nationalisation and, for non-banks, outright debt relief. By tackling the root problem, this would be a more efficient use of public money than untargeted expenditures or tax cuts. More fundamentally, there is a strong case for eliminating the subsidy of debt over equity, so common in tax codes.

The priority for prudential policy is to strengthen its systemic or "macroprudential" orientation, so as to tackle procyclicality head-on. Basel III indeed moves in that direction with its countercyclical capital buffer, as does the implementation of full-fledged macroprudential frameworks in national jurisdictions. These deploy a range of instruments designed to strengthen the financial system's resilience and, ideally, to constrain financial booms (Chapter IV). Examples include maximum loan-to-value or debt-to-income ratios, proactive adjustments to capital requirements and provisioning, restrictions on non-core bank funding, and macroprudential (banking system- wide) stress tests.

At the same time, two big gaps remain (Chapter VI). One is how best to address the risks raised by the rapid growth of non-bank financial intermediaries. To be sure, insurance companies have always been regulated, although not so much from a systemic perspective. And work has been under way for some time on "shadow banks" - leveraged players active in maturity transformation. But attention has only recently turned to the asset management industry. Here the concern is not so much the failure of individual firms, but the impact of their collective behaviour on systemic stability through asset prices, market liquidity and funding conditions. Even when unleveraged, these investors are quite capable of generating leverage-like behaviour. The second gap is how best to address sovereign risk, including for banks. Several regulatory provisions and supervisory practices favour sovereign exposures. But sovereigns can be quite risky and, historically, have often been at the root of bank failures. Moreover, favouring them often comes at the expense of small and medium-sized enterprises, thereby stifling productive activities and employment. The right approach needs to be systemic and comprehensive, addressing the various types of exposure. The Basel Committee on Banking Supervision has recently taken up this challenge. That work should be pursued without delay or hesitation.

The priority for monetary policy is to ensure that financial stability concerns are incorporated more symmetrically during booms and busts (Chapter IV). The frameworks should allow for scope to tighten during financial booms even if near-term inflation is low and stable, and to ease less aggressively and persistently during busts.

While a number of objections have been raised to this proposal, none of them appears to be a show-stopper. Indeed, similar objections were levelled against adopting inflation targeting frameworks, which many regarded as a step in the dark.

A first objection is that there are no reliable indicators for the build-up of financial imbalances. But considerable progress has been made in this area, and macroprudential frameworks already actively rely on such assessments. Moreover, as noted, standard monetary policy benchmarks are unobservable and measured with great uncertainty, eg economic slack, potential output and equilibrium real interest rates. Even measuring the relevant inflation expectations is fraught with difficulties.

A second objection is that monetary policy has little impact on financial booms, and hence on credit expansion, asset prices and risk-taking. But these are key channels through which monetary stimulus influences aggregate demand. Indeed, this is the strategy that central banks have explicitly followed post-crisis to reanimate the economy. And, if anything, the evidence suggests that central banks have been very successful in influencing financial markets and financial risk- taking but less so in boosting risk-taking in the real economy and hence output.

The deeper question is how to reconcile such a strategy with inflation objectives. The strategy requires greater tolerance for persistent inflation deviations from target, especially when disinflation is driven by positive supply side forces. Are central banks prepared to accept them? And are the frameworks flexible enough? This will necessarily vary across central banks.

Arguably, some of the current frameworks already provide central banks with sufficient flexibility. Some arrangements, for instance, explicitly include the option to allow inflation to return to the long-run target only slowly over time, depending on the factors that drove it off track. This, of course, requires careful, and possibly quite challenging, explanation and communication. Two factors could in part explain why central banks may not have fully used this flexibility. One is their perception of the trade-offs involved. For example, they may see deflation as a kind of red line that, once crossed, triggers a self-reinforcing destabilising process. Another is the possibility of using macroprudential tools instead.

Even so, in a number of cases the frameworks and the mandates underpinning them may be seen as too restrictive. If so, adjustments could be made. These might even go as far as revisiting mandates, if necessary, such as by assigning greater weight to financial stability considerations. But, if chosen, this route would need to be travelled with great care. The revision process and final outcome could be unpredictable and might open the door to unwelcome political economy pressures.

On balance, the priority should be to use the existing room for manoeuvre to the full, and to encourage analytical perspectives that highlight the costs of failing to incorporate financial stability considerations into monetary frameworks. Building sufficient public support is critical. Mandates could then be revisited only as a last resort.

What about the IMFS? Putting one's own house in order, along the principles described, would already be a major step: it would greatly reduce the negative spillovers to the rest of the global village. But there is a need to go further (Chapter V).

This has long been recognised for the "financial" dimension of the system. The need for improvement has been the basis for increasingly tight cooperation in the development and implementation of commonly agreed prudential standards as well as in day-to-day supervision of banks. True, the journey has not been smooth, and momentum inevitably slows as the memories of a crisis fade. But the journey is continuing, particularly in the various initiatives under way under the aegis of the Basel Committee on Banking Supervision and the Financial Stability Board (see below). Progress requires unflagging commitment: the risk that national priorities and biases will gain the upper hand always lurks around the next corner.

By contrast, the recognition has been far less common for the "monetary" dimension of the system, at least since the breakdown of Bretton Woods. Here, it is worth distinguishing between crisis management and crisis prevention. In crisis management, cooperation has been long-standing, mainly through foreign exchange swap lines; in crisis prevention, which means in routine monetary policy settings, it has been much softer.

As regards crisis management, central banks have built on the successful cooperation during the Great Financial Crisis. Among the central banks of major currency areas, foreign currency swap lines exist or could be established quickly as needed. And there may be some room to strengthen these mechanisms further, even though risk management and governance issues loom large.

But international arrangements for emergency liquidity support cannot, and should not, substitute for cooperative efforts to prevent financial crises. They cannot, because the economic and social costs of a crisis are simply too large and unpredictable. And they should not, because of moral hazard and the tendency to overburden central banks.

Two factors have severely hindered monetary policy cooperation outside crises. The first has to do with diagnosis and hence the perceived need to act. As explained above, the prevailing view is that flexible exchange rates, combined with inflation-focused domestic regimes, can foster the right global outcomes. As a result, discussions on how to promote global coordination have centred on how to deal with current account imbalances, which are less amenable to monetary policy measures. Indeed, the terms "imbalance" and "current account imbalance" have been treated as synonymous. The second factor has to do with mandates and hence the incentive to act. National mandates raise the bar: actions must clearly be seen to promote the interests of one's own country. In other words, there is no perceived need and no incentive.

Yet neither factor should halt proceedings. The excess financial elasticity perspective highlights the need for cooperation: international spillovers and spillbacks are just too damaging. Moreover, it shifts the focus onto financial imbalances - the blind spot of present arrangements. Indeed, in this view, the exclusive focus on current account imbalances has sometimes been counterproductive. It has, for example, encouraged pressure on current account surplus countries to expand domestic demand even as financial imbalances were building up, as in the case of Japan in the 1980s or China post-crisis. As regards incentives, national mandates have not prevented tight cooperation in the prudential sphere.

How far could cooperation realistically go? At a minimum, enlightened self-interest, based on a thorough exchange of information, should be feasible. This would mean taking spillovers and spillbacks more systematically into account when setting policies. Large jurisdictions that are home to international currencies have a special responsibility. Cooperation could even extend to occasional joint decisions, on both interest rates and foreign exchange intervention, beyond those seen during crises. Unfortunately, a stronger sense of urgency and shared responsibility would be needed to develop new global rules of the game that would help instil greater discipline in national policies.

What to do now?

Room for manoeuvre in macroeconomic policy has been narrowing with every passing year. In some jurisdictions, monetary policy is already testing its outer limits, to the point of stretching the boundaries of the unthinkable. In others, policy rates are still coming down. Fiscal policy, after the post-crisis expansion, has been throttled back, as sustainability concerns have mounted. And fiscal positions are deteriorating in EMEs where growth is slowing. What, then, should be done now, besides redoubling reform efforts to strengthen productivity growth?

For fiscal policy, the overriding priority is to make sure that sovereign debt is on a sustainable path, which in many cases it is not (Chapter III). This is the precondition for lasting monetary, financial and macroeconomic stability. And it is also what defines the near-term room for manoeuvre. When longer-term growth prospects are in doubt, it would be highly imprudent to push for more expansionary fiscal policies - a mistake made often enough in the past. For countries that do have fiscal space and need to use it, the challenge is how to do so most effectively. This means, first and foremost, facilitating private sector balance sheet repair, supporting reforms that boost long-term productivity growth and a greater but judicious emphasis on investment at the expense of current transfers. The quality of public spending matters more than its quantity.

For monetary policy, there is a need to fully appreciate the risks to financial and hence macroeconomic stability associated with current policies. True, there is great uncertainty about how the economy works. But precisely for this reason it seems imprudent to push the burden of tackling financial stability risks entirely onto prudential policies. As always, the correct calibration will be country-specific. But, as a general rule, a more balanced approach would mean attaching more weight than hitherto to the risks of normalising too late and too gradually. And, where easing is called for, the same should apply to the risks of easing too aggressively and persistently.

Given where we are, normalisation is bound to be bumpy. Risk-taking in financial markets has gone on for too long. And the illusion that markets will remain liquid under stress has been too pervasive (Chapter II). But the likelihood of turbulence will increase further if current extraordinary conditions are spun out. The more one stretches an elastic band, the more violently it snaps back. Restoring more normal conditions will also be essential for facing the next recession, which will no doubt materialise at some point. Of what use is a gun with no bullets left? Therefore, while having regard for country-specific conditions, monetary policy normalisation should be pursued with a firm and steady hand.

All this naturally puts a premium on strengthening prudential safeguards (Chapter VI). Macroprudential tools should be applied with vigour, but without entertaining unrealistic expectations about what they can do on their own. Where appropriate, balance sheet repair should be pursued energetically, through loss recognition and recapitalisations. And the regulatory initiatives under way should be implemented promptly and comprehensively. In particular, the recalibration of the banks' leverage ratio is critical as a means of providing a reliable backstop for the risk-weighted minimum capital requirements. Likewise, it will be essential to set a tough standard for interest rate risk in the banking book at a time when nominal interest rates have been so exceptionally low for so long.

Conclusion

The global economy is growing again at rates not far from the historical average. Lower oil prices should boost it further in the near term even as they temporarily put further downward pressure on prices. But not all is well. Debt burdens and financial risks are still too high, productivity growth too low and room for manoeuvre in macroeconomic policy too limited. Global economic expansion is unbalanced. Interest rates that have been extraordinarily low for exceptionally long are the outward sign of this malaise.

Nothing is inevitable about this. The problems we face are man-made and can be solved by the wit of man. This chapter has provided one possible diagnosis out of the many on offer: our view is that the current plight reflects, to a considerable extent, the inability of policy frameworks to come to grips with the global economy's "excess financial elasticity" - its propensity to generate hugely damaging financial booms and busts. These leave enduring and deep wounds in the economic tissue that, unless properly treated, impede the economy's return to a healthy and sustainable expansion - one that does not set it up for the next disruptive cycle. In the long term, this risks entrenching instability and chronic weakness.

One may disagree with this diagnosis. It is harder, though, to disagree with the general principle of being prudent whenever diagnoses are uncertain. Prudence means following a treatment that allows for the possibility of error. From this perspective, current macroeconomic policy frameworks appear too one-sided. When all is said and done, they are still based on the presumption that inflation will suffice as a reliable gauge of sustainability or, if it will not, that financial stability risks can be adequately addressed through prudential policies alone. This is a familiar viewpoint: caveats aside, it harks back to the pre-crisis way of doing things.

A more balanced approach would have a number of features. It would seek to address financial booms and busts through a combination of policies - monetary, fiscal and prudential - rather than prudential policy alone. It would rebalance the mix away from demand management policies, especially monetary policy, towards structural measures. And it would not presume that, if one's own house is in order, the global village will be too.

Shifting the focus from the short to the longer term is more important than ever. Over the past decades, it is as if the emergence of slow-moving financial booms and busts has slowed down economic time relative to calendar time: the economic developments that really matter now take much longer to unfold. Meanwhile, the decision horizons of policymakers and market participants have shortened. Financial markets have compressed reaction times and policymakers have chased financial markets more and more closely in what has become an ever tighter, self-referential, relationship. Ultimately, it is this combination of slowing economic time and shorter decision horizons that helps explain where we are - and how, before we know it, the unthinkable can become routine. It should not be allowed to.