BIS international banking statistics at end-June 2020

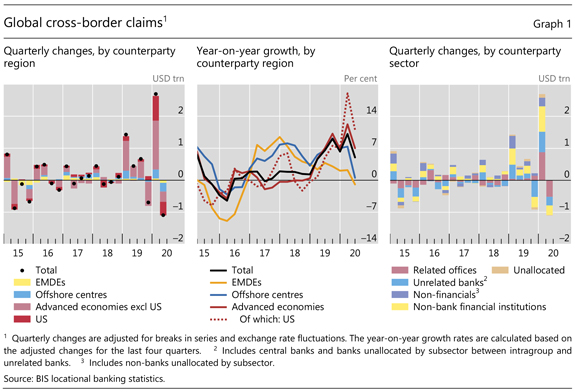

- Cross-border claims contracted by $1.1 trillion from Q1 to Q2 2020. The year-on-year growth rate dropped from 10% at end-March to 5% at end-June 2020. Interbank claims, which had surged in the first quarter, fell sharply, driving the overall contraction.

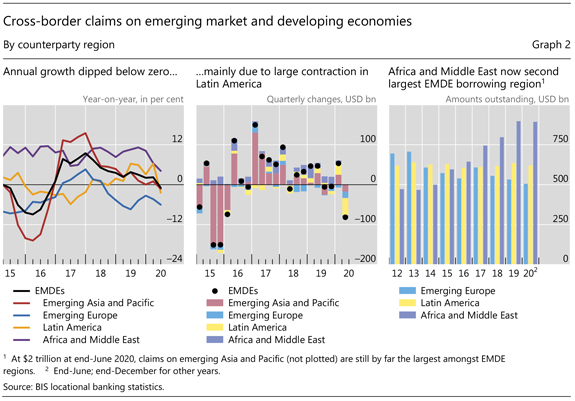

- Cross-border claims on emerging market and developing economies (EMDEs) fell year on year for the first time since 2016, mainly driven by a $43 billion contraction in claims on Latin America and the Caribbean.

- Banks have continued to rebalance their portfolios into government assets. Their consolidated foreign claims on the official sector globally rose to 29% of their total foreign claims in Q2 2020, up from 19% at end-2010.

Cross-border positions contracted in the second quarter of 2020

Cross-border claims contracted by $1.1 trillion from end-March to end-June, partly reversing the $2.7 trillion surge observed the quarter before. Consequently, the year-on-year (yoy) growth rate dropped from 10% to 5%. Like the Q1 surge, the Q2 contraction was driven by interbank positions; almost half of the quarterly change was the result of reduced inter-office positions (Graph 1, right-hand panel), as banks redistributed liquidity across their global operations amidst the pandemic. In particular, claims on counterparties located in the United States, which accounted for much of the expansion in the first quarter, fell the most in the second (left-hand panel).

The global contraction was uneven across regions. While cross-border claims on advanced economies contracted during the quarter, their annual growth rate remained strong at +7% yoy. The growth in claims on the United States in particular stayed high, at +11% yoy. In contrast, claims on offshore centres almost stalled (+1% yoy), and those on EMDEs fell (-1% yoy) for the first time since end-2016 (Graph 1, centre panel).

The contraction observed for EMDEs was relatively widespread. While claims on EMDE non-banks increased slightly (+3% yoy), this was more than offset by a big drop in interbank claims (-$93 billion or -5% yoy). Cross-border claims on all four EMDE regions dropped from Q1 to Q2 2020, with those on Latin America falling the most (-$43 billion; Graph 2, centre panel). Claims declined yoy for three of the four regions, resulting in negative yoy growth for EMDEs as a whole for the first time since end-2016 (left-hand panel). One exception to this general picture is the Africa and Middle East region: the annual growth in cross-border claims on its residents has remained positive (+4% yoy), extending the trend observed since 2014. As a result, claims on that region now surpass those on both emerging Europe and Latin America (right-hand panel).

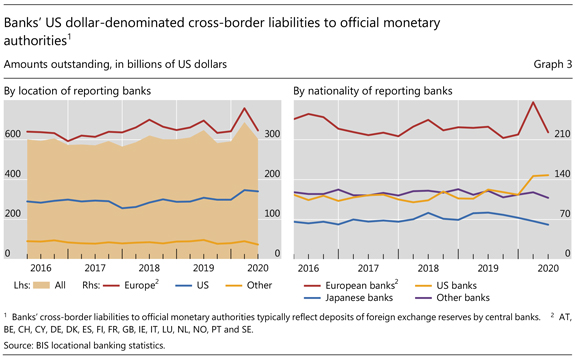

Banks reported fewer cross-border liabilities to official monetary authorities in Q2 2020, reversing the rise reported in the first quarter. These cross-border liabilities typically reflect deposits of foreign exchange reserves with commercial banks. US dollar-denominated deposits had surged in the course of Q1 2020 (+$97 billion) but then reverted in the second quarter by $84 billion (Graph 3, and Graph A.5 in the statistical annex). Commercial banks located in Europe and, to a lesser extent, the United States reported the largest fluctuations over the two quarters (Graph 3, left-hand panel). Ranked by bank nationality (right-hand panel), it was affiliates of European and US banks that saw the largest moves.

Shift in banks' portfolios into government assets

The BIS consolidated banking statistics (CBS), which track the globally consolidated positions of banks headquartered in a given country, also show a decrease in banks' claims in the second quarter. Overall, banks' foreign claims - ie cross-border claims and local claims booked by affiliates located abroad (excluding inter-office positions) - fell by $1.1 trillion from end-Q1 to end-Q2 2020.1

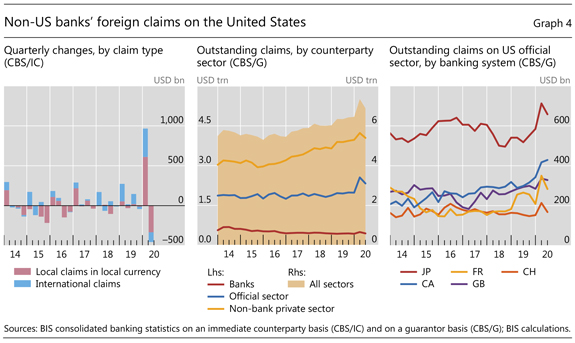

Most notably, non-US banks' foreign claims on the United States in the second quarter dropped by nearly half of the $950 billion surge they saw in the first (Graph 4, left-hand panel). Their local dollar claims on US residents accounted for much of this contraction (red bars).2 Non-US banks' foreign claims on the US official sector - which includes the US government and the Federal Reserve3 - fell by $223 billion (centre panel), partly reversing the jump in the first quarter when the pandemic escalated. French and Japanese banks accounted for the largest shares of this decrease, followed by Swiss banks (right-hand panel).

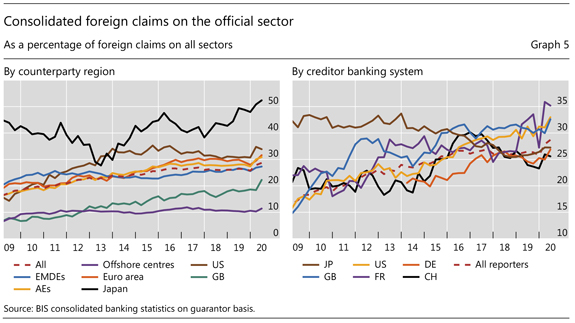

Despite the recent fluctuations in claims on the US official sector, an important long-term trend has been the increase in banks' consolidated claims on the official sector globally. Banks' public sector claims have risen from 19% of their foreign claims in 2010 to 29% at end-Q2 2020 (Graph 5, left-hand panel). This general trend applies to the official sector in both advanced economies and EMDEs. Amongst the former, banks' claims on the official sector in the euro area and Japan jumped from, respectively, 20% and 40% in 2010 to 32% and 52% at end-Q2. Amongst the large EMDE counterparties, the shares for China, Korea and the Czech Republic rose by 7, 6 and 26 percentage points, respectively.

Roughly half of all foreign claims on the official sector at end-Q2 were reported by just four banking systems: Japanese, US, UK and French banks. Of these, French banks saw the largest increase since 2010, with UK and US banks not far behind (Graph 5, right-hand panel).

1 Exchange rate-adjusted changes for the CBS are estimated using the currency breakdowns available in the LBS (since the CBS do not contain currency breakdowns).

2 This is consistent with Federal Reserve data showing that non-US banks' branches and agencies in the United States held $640 billion of reserves at the Federal Reserve at end-Q2 2020, down from $868 billion at end-Q1. Note that in the CBS, the official sector includes the central bank, and thus differs from the general government sector in the System of National Accounts.

3 The counterparty sector breakdown in the CBS on an immediate counterparty basis (CBS/IC) is available only for banks' international claims, and not for their local claims in local currency. By contrast, in the CBS on a guarantor basis (CBS/G), which allocates claims to the country and sector of the ultimate obligor after taking into account credit risk mitigants, the counterparty sector applies to all foreign claims, ie banks' local claims in local currency plus their international claims.