BIS global liquidity indicators at end-June 2020

- US dollar credit to non-bank borrowers residing outside the United States grew by 6% year-on-year, to reach $12.7 trillion at end-June 2020.

- In each of the three major currencies (USD, EUR, JPY), credit to non-residents grew more slowly than credit to residents of the respective currency areas in Q2.

- Dollar credit to emerging market and developing economies (EMDEs) expanded by 7% year-on-year, passing the $4 trillion mark. Issuance of debt securities remained the main driver of growth.

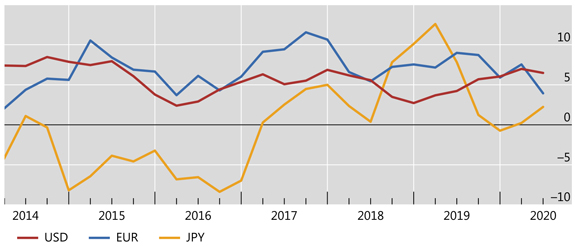

Growth in dollar credit outside the US remained robust

Graph 1: Year-on-year percentage change of US dollar-, euro- and yen-denominated credit to non-resident non-banks (interactive graph).

Source: BIS global liquidity indicators (Table E2.1, E2.2 and E2.3).

US dollar credit to non-bank borrowers outside the United States grew by 6% year on year (yoy) to reach $12.7 trillion at end-June 2020. Dollar credit remained robust throughout the period of market tensions in early 2020, sustaining the growth rates observed over the past decade.1

The growth in dollar credit in Q2 was driven by debt securities (+9% yoy). This is in contrast to Q1, when bank lending grew faster (Annex Graph A1). As a result, the share of debt securities in total dollar credit rose to 53% in Q2, up from 51% in the previous quarter and a continuation of the trend since the Great Financial Crisis (GFC) of 2007-09 (Annex Graph A4, left-hand panel, black line).

Credit in the other major currencies also expanded, although at a lower rate (Graph 1, blue and yellow lines). Euro credit to borrowers outside the euro area lost momentum in Q2 (+4% yoy), ending the quarter at €3.5 trillion (or $3.9 trillion). This contrasted with the past few years, when growth in euro credit outpaced that in dollar credit. Credit in Japanese yen outside Japan grew at 2% yoy in Q2, after zero growth in Q1.

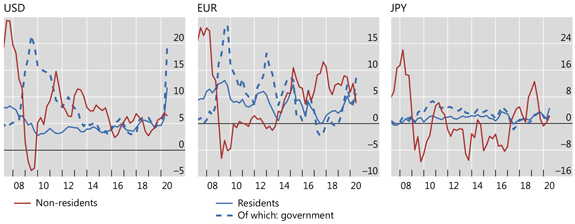

Credit to non-residents grew more slowly than credit to residents

Graph 2: Year-on-year percentage change of credit to non-residents (non-bank sector) and residents (non-financial sector) of the respective currency areas.

Source: BIS global liquidity indicators (Tables E2.1, E2.2 and E2.3).

For much of the post-GFC period, dollar and euro credit to non-resident borrowers has grown faster than credit to residents. For borrowers outside these currency areas, these liabilities are in a foreign currency and can thus be a source of vulnerability. However, in Q2 2020, credit to residents surged, outpacing credit to non-residents for all three major currencies (Graph 2). The increase in credit to residents was generally driven by government borrowing.

These developments were more pronounced for the United States. In particular, dollar credit to the US non-financial sector accelerated, pushing its growth rate to 12% yoy. This reflected a 19% surge in government debt, a pace comparable with that following the GFC (Graph 2, left-hand panel, dashed line).

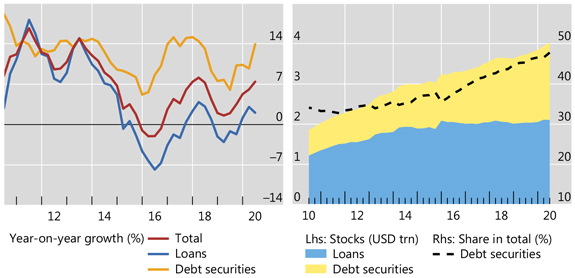

Debt securities continued to fuel growth in dollar credit to EMDEs

Graph 3: US dollar credit to non-bank borrowers in EMDEs.

Source: BIS global liquidity indicators (Table E2.1).

The component of global dollar credit directed to EMDEs grew by 7% yoy in Q2 2020, reaching $4 trillion (Graph 3). Consistent with the past few quarters, credit to Africa and the Middle East registered the highest growth rate, at 14%, driven by countries in the Middle East. Emerging Asia-Pacific also received dollar credit (+9%), while Latin America saw more modest growth (+5%). In contrast, dollar credit to emerging Europe continued to fall (-5%), extending the decline observed over the past six years. As a result, outstanding euro-denominated credit to the region has surpassed US dollar credit since early 2020.

Debt securities remained the driver of dollar credit to EMDEs. Strong issuance contributed to a brisk growth rate of 14% in Q2 2020 (Graph 3, left-hand panel, yellow line), slightly above the 12% average for the past decade. The share of debt securities in total credit continued to increase steadily, from 33% at end-2010 to almost half by Q2 2020 (right-hand panel).

1 For a discussion of the role of the dollar in international finance, see Committee on the Global Financial System, US dollar funding: an international perspective, CGFS Papers, no 65, June 2020.