84th Annual Report, 2013/14 - Statistics associated with the graphs

Series description is to be found in the corresponding graph, that is linked in the right side column.

Download all statistics (zipped XLSX, 1.7 MB).

Graphs |

||

| Chapter I: data behind the graph (xlsx) | ||

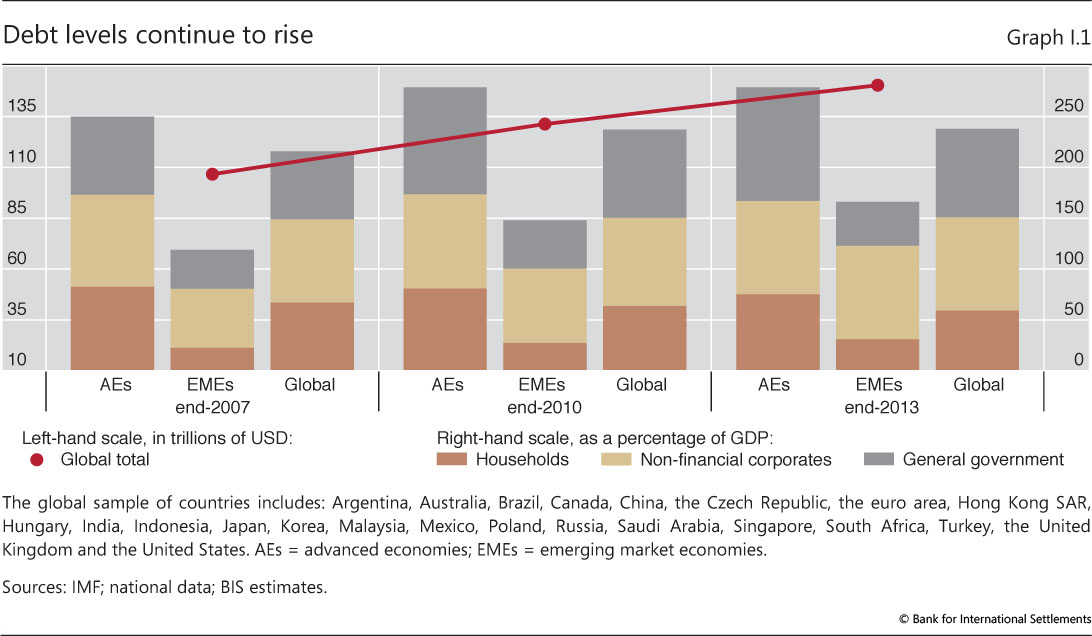

| I.1 | Debt levels continue to rise | p 10 |

| Chapter II: data behind the graphs (xlsx, 1.3 MB) | ||

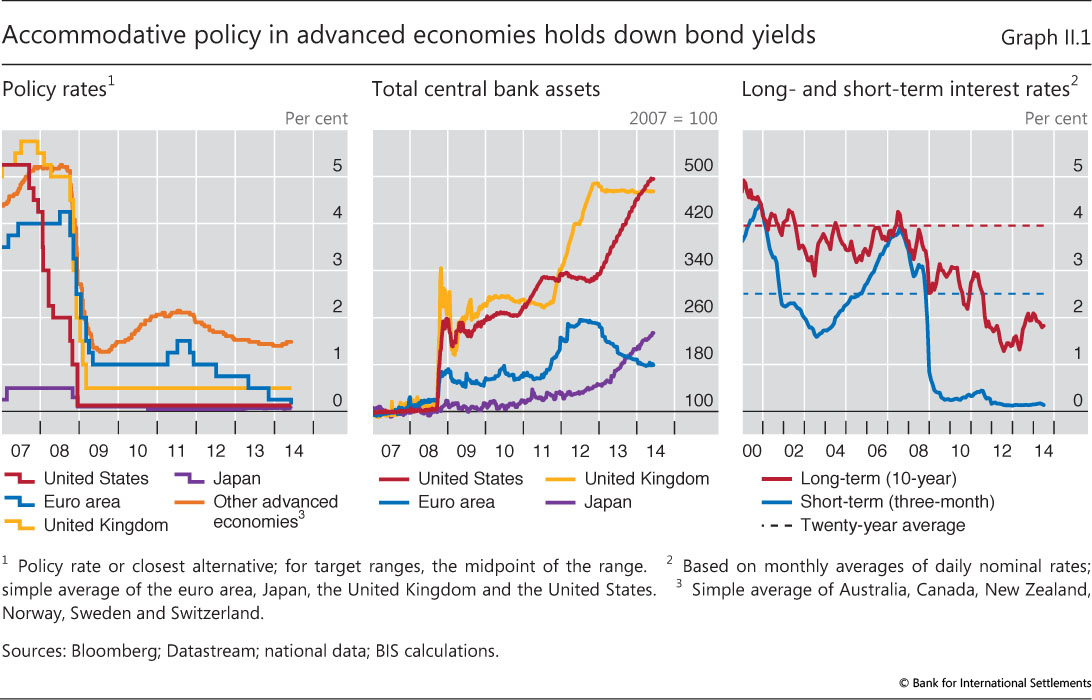

| II.1 | Accommodative policy in advanced economies holds down bond yields | p 24 |

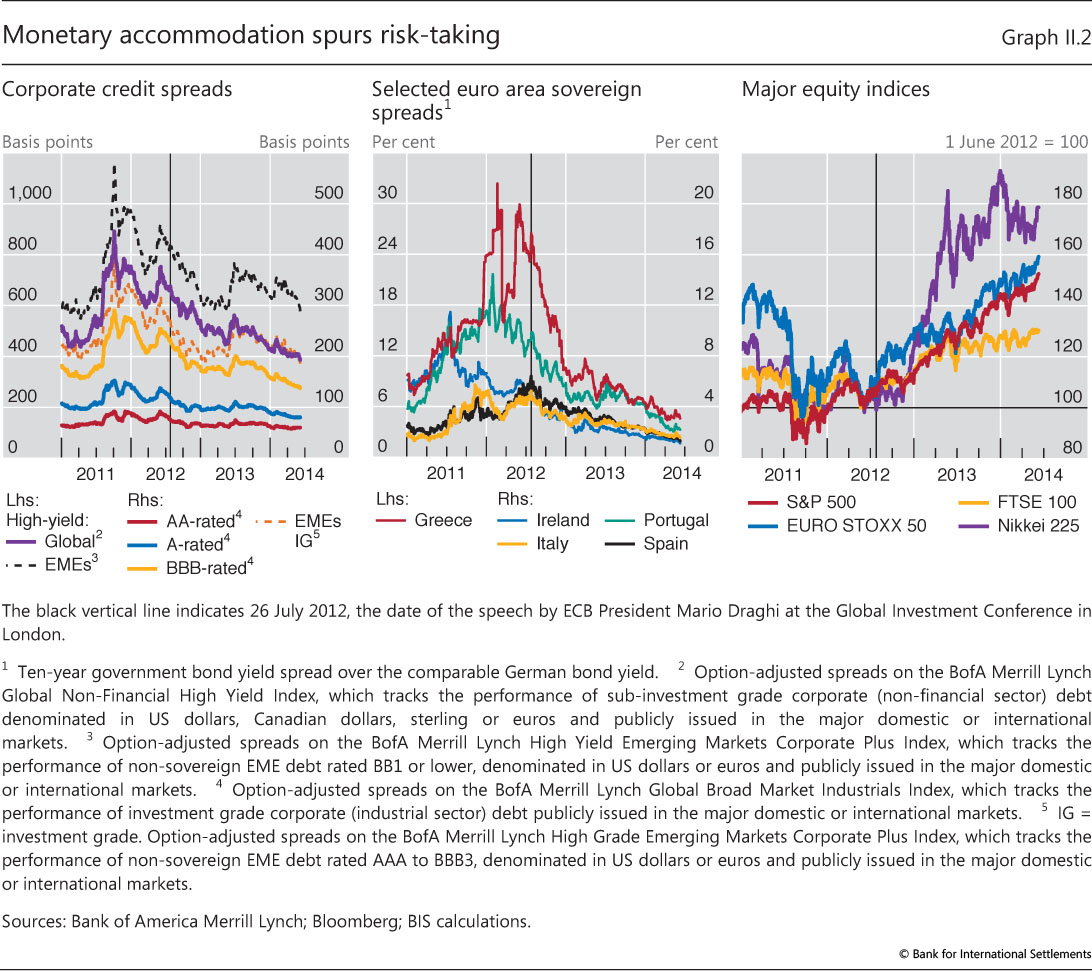

| II.2 | Monetary accommodation spurs risk-taking | p 25 |

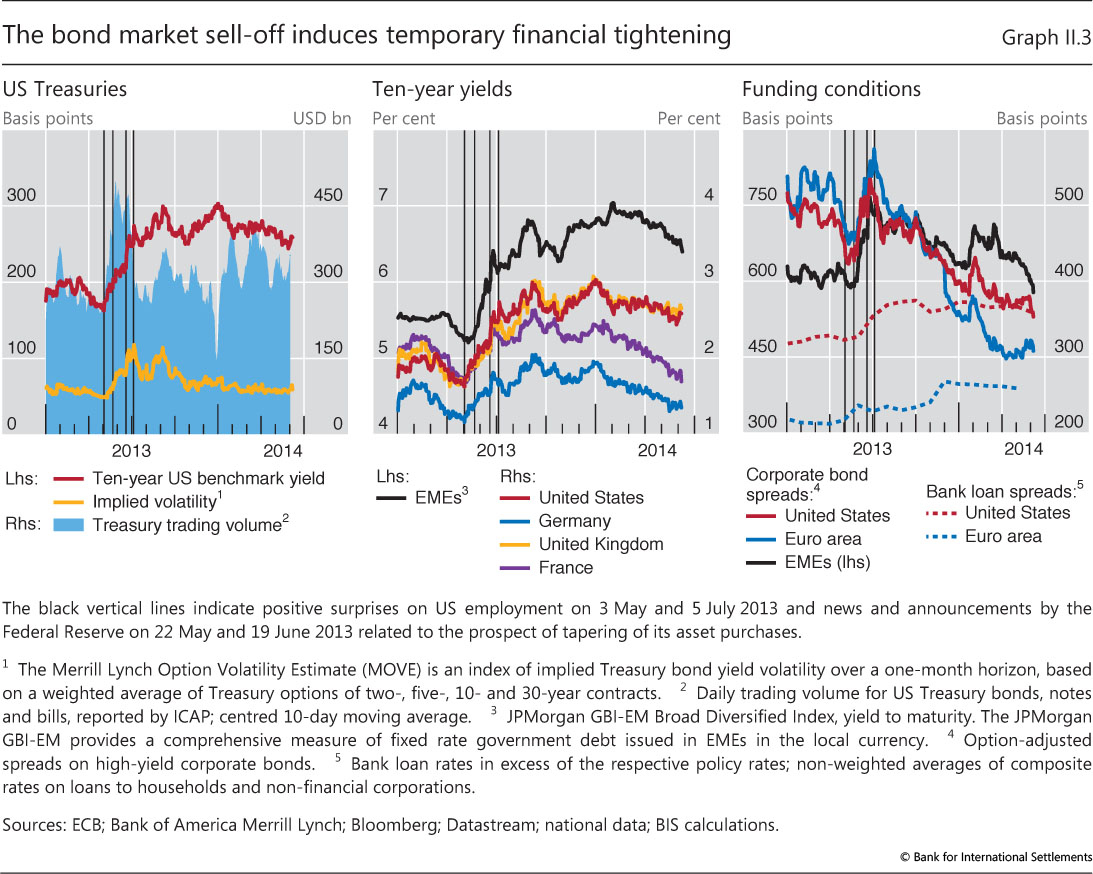

| II.3 | The bond market sell-off induces temporary financial tightening | p 26 |

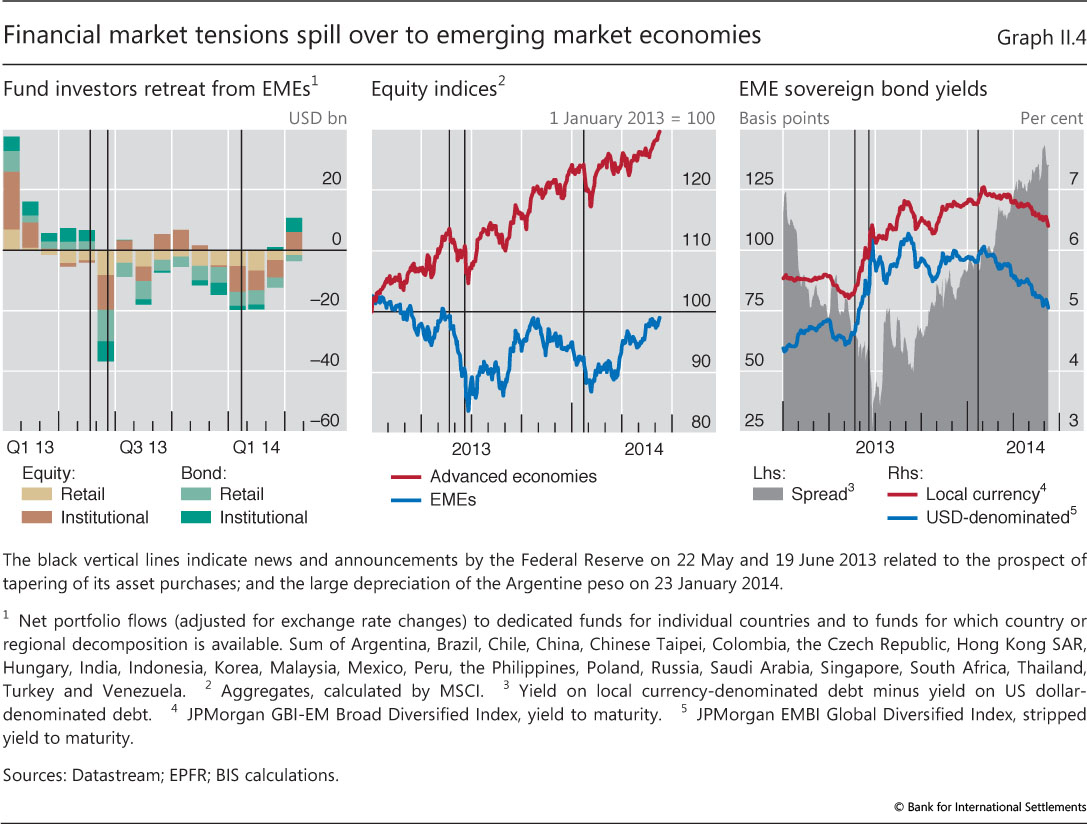

| II.4 | Financial market tensions spill over to emerging market economies | p 27 |

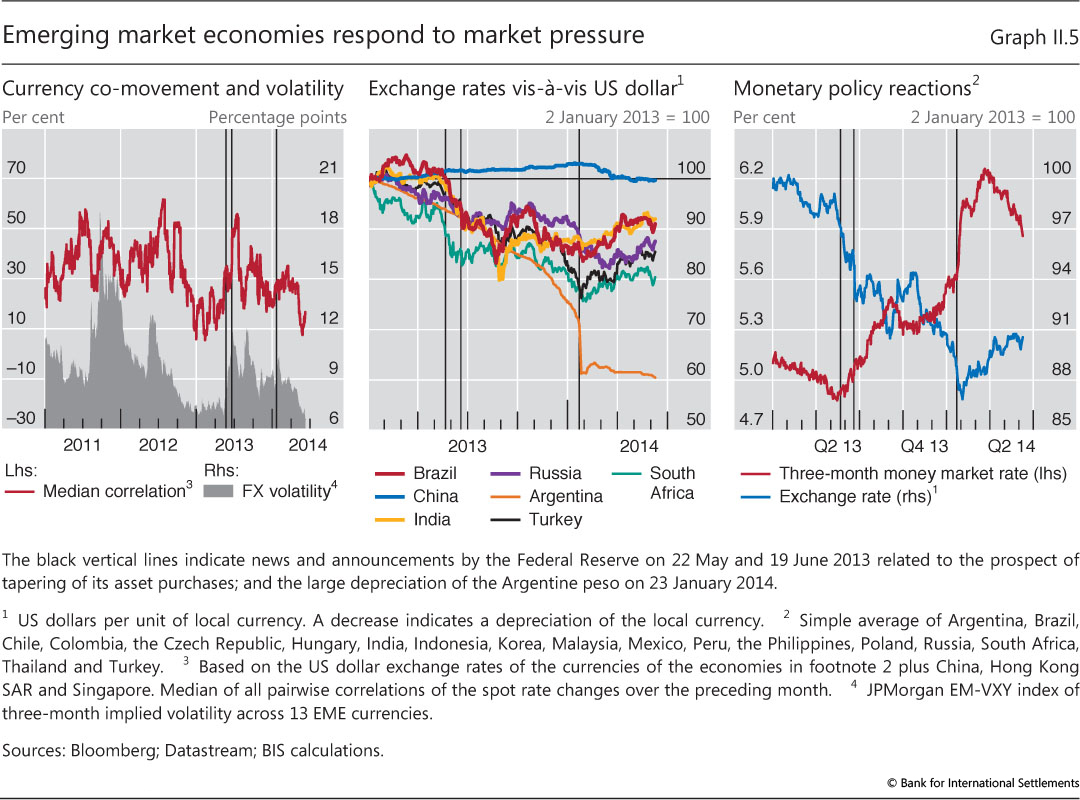

| II.5 | Emerging market economies respond to market pressure | p 28 |

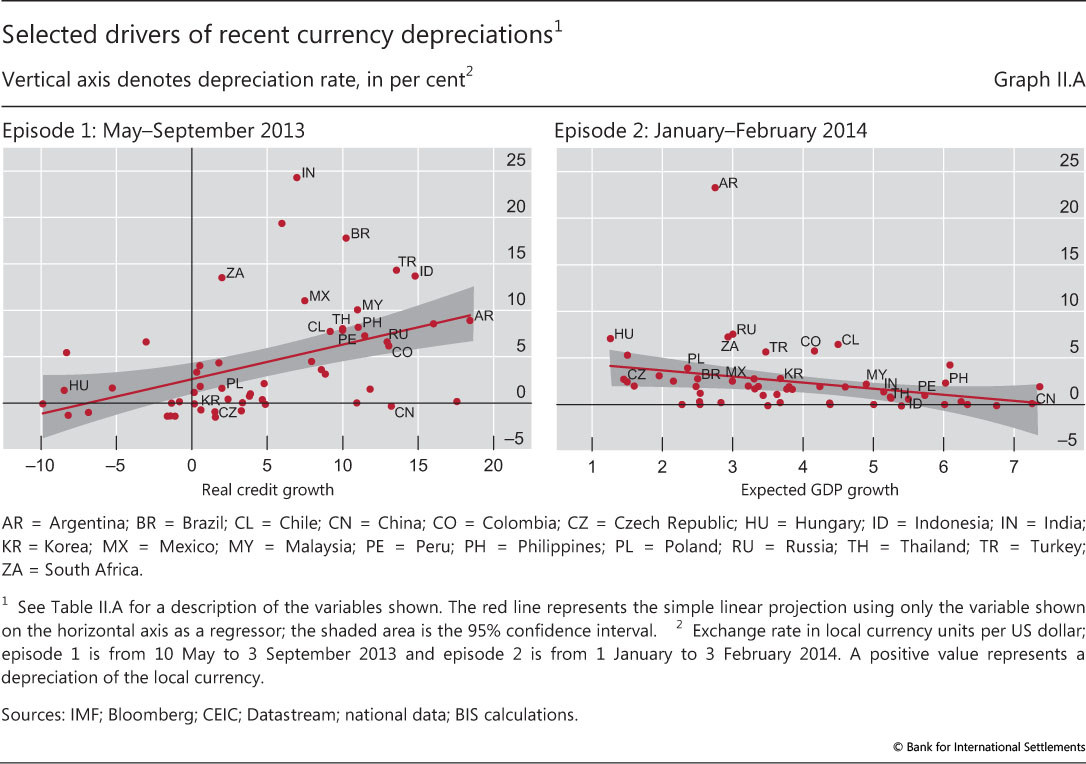

| II.A | Selected drivers of recent currency depreciations | p 29 |

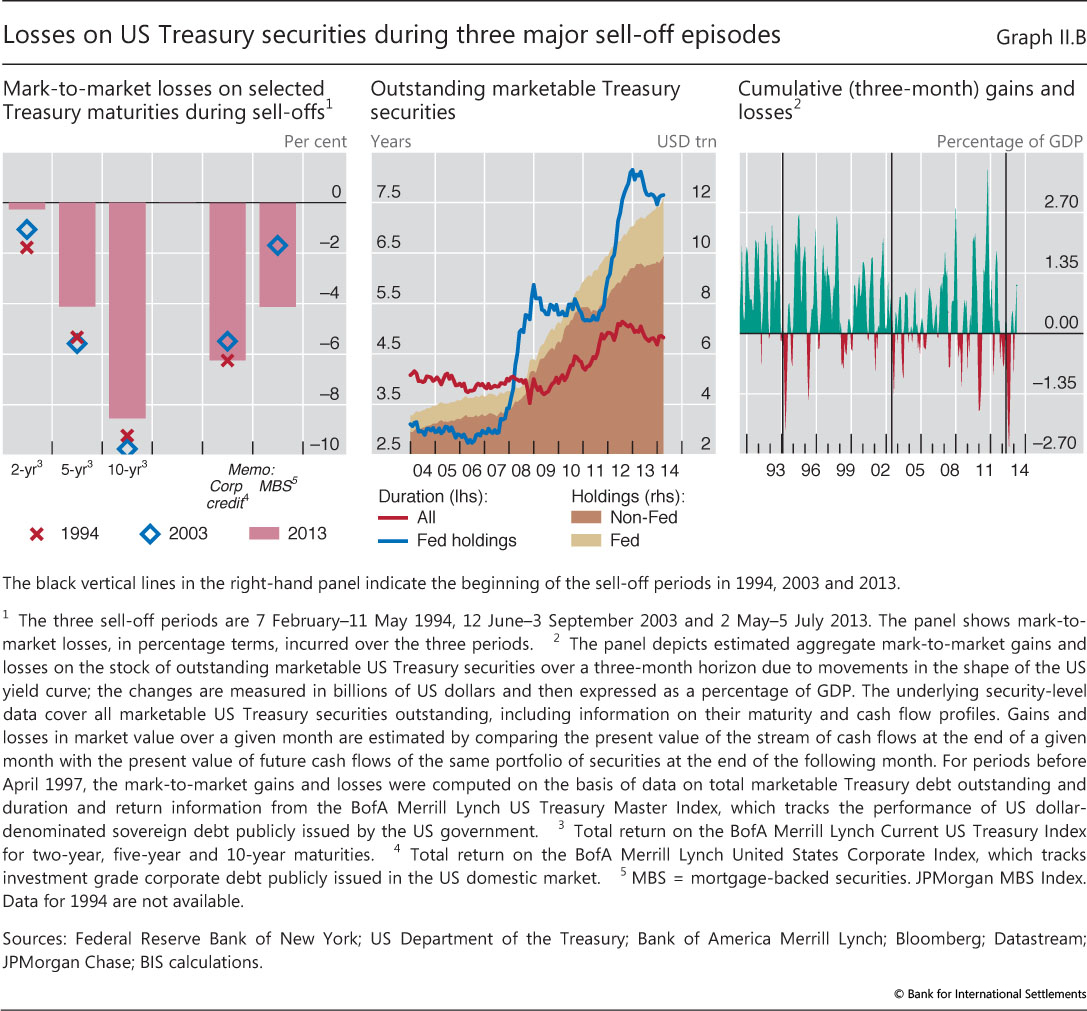

| II.B | Losses on US Treasury securities during three major sell-off episodes | p 33 |

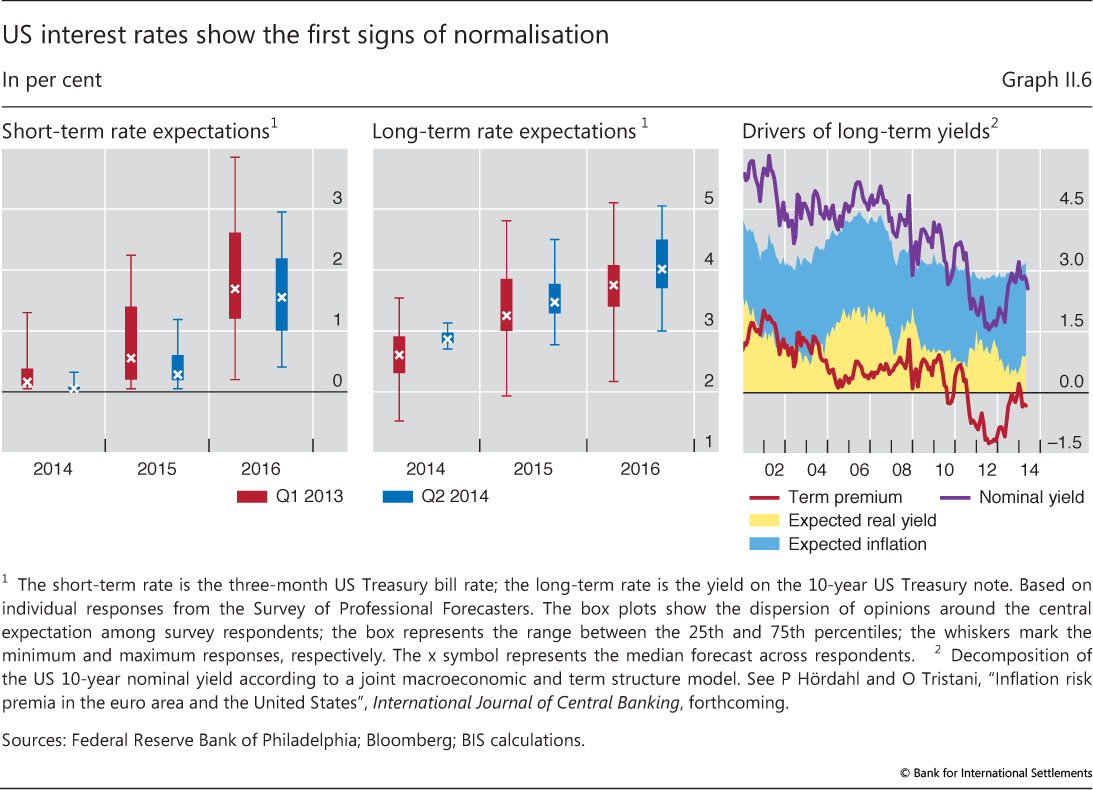

| II.6 | US interest rates show the first signs of normalisation | p 34 |

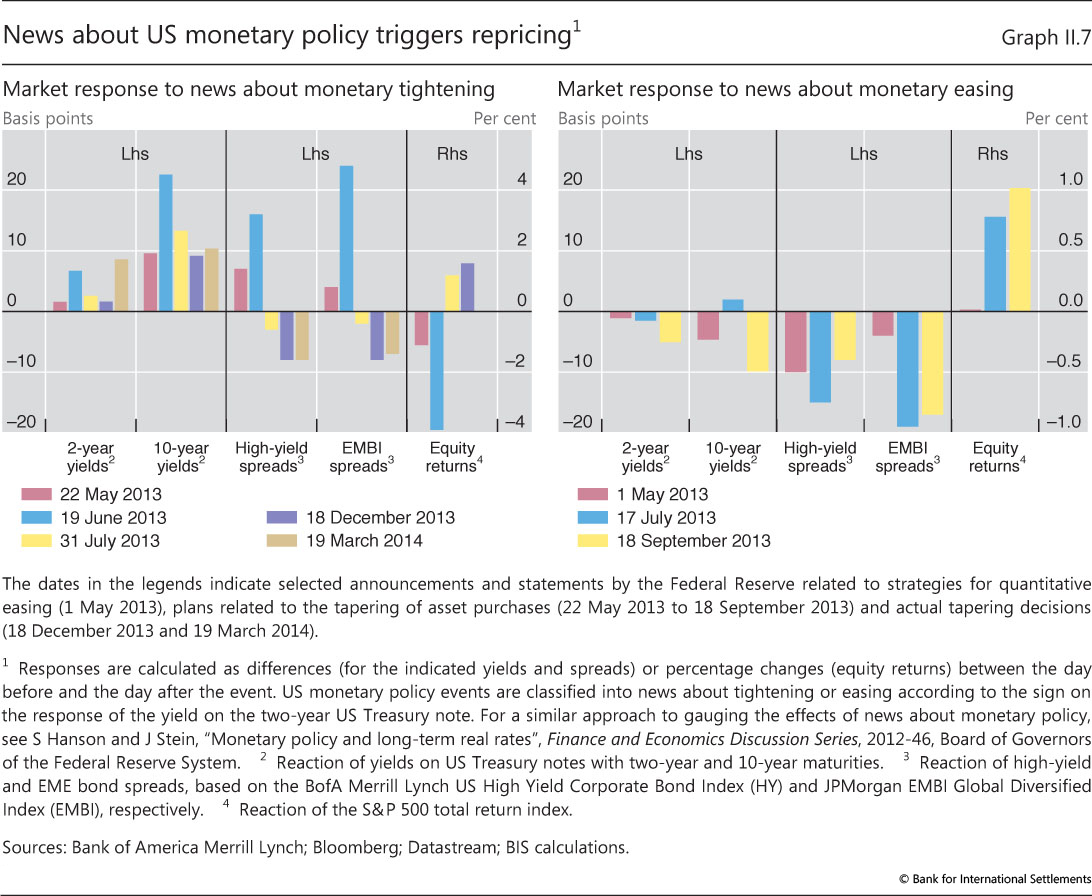

| II.7 | News about US monetary policy triggers repricing | p 35 |

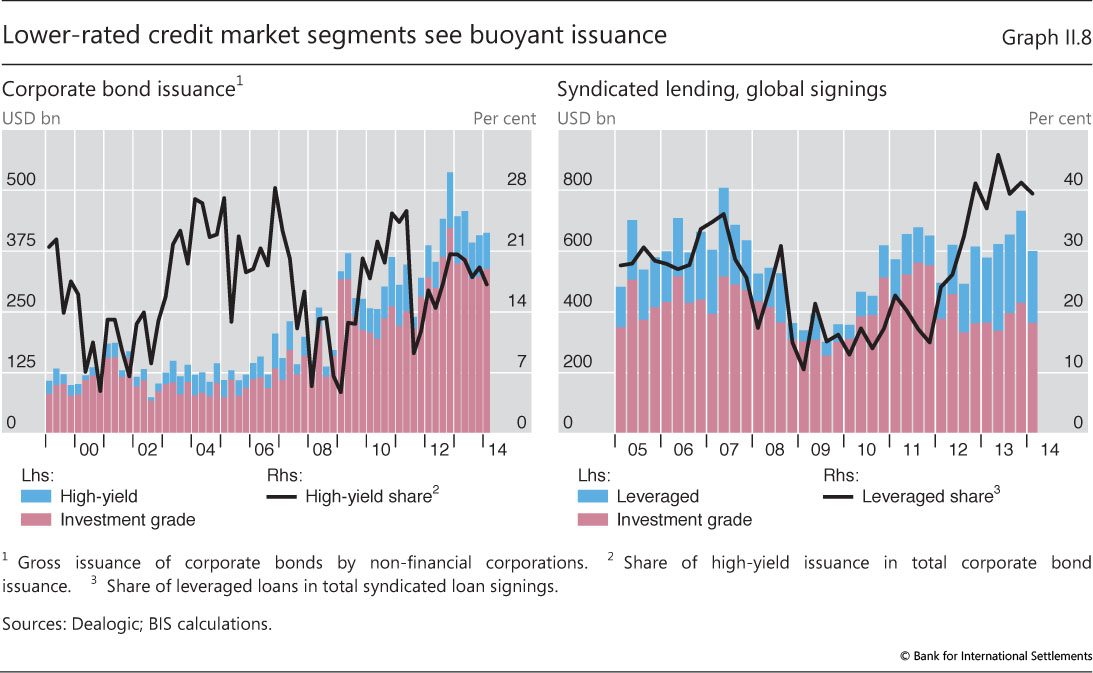

| II.8 | Lower-rated credit market segments see buoyant issuance | p 36 |

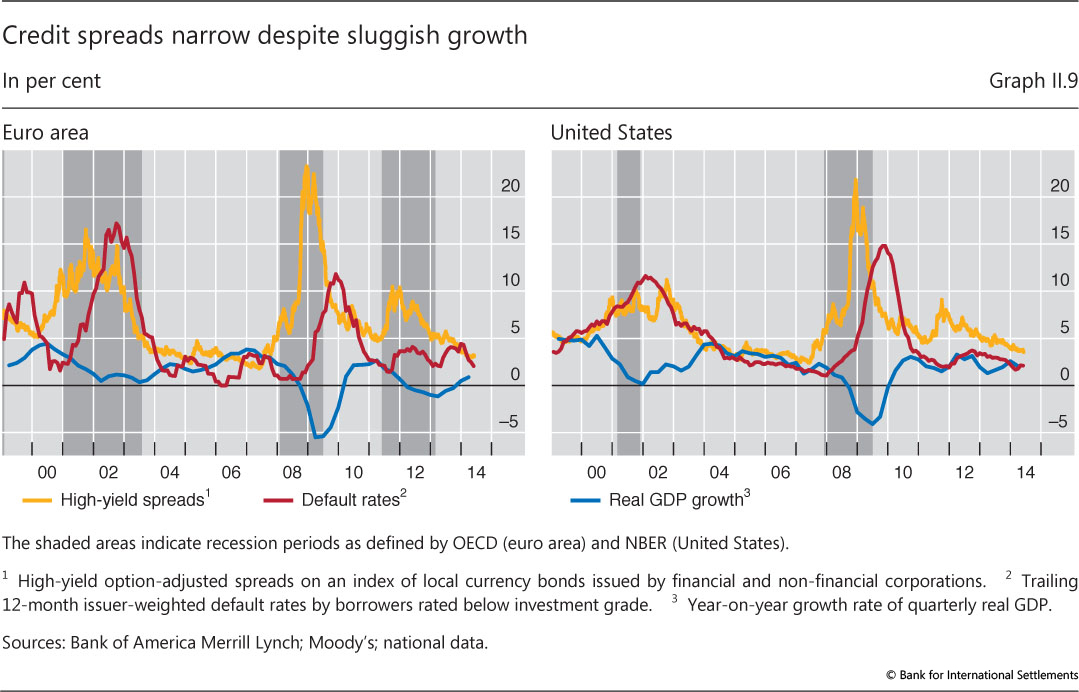

| II.9 | Credit spreads narrow despite sluggish growth | p 37 |

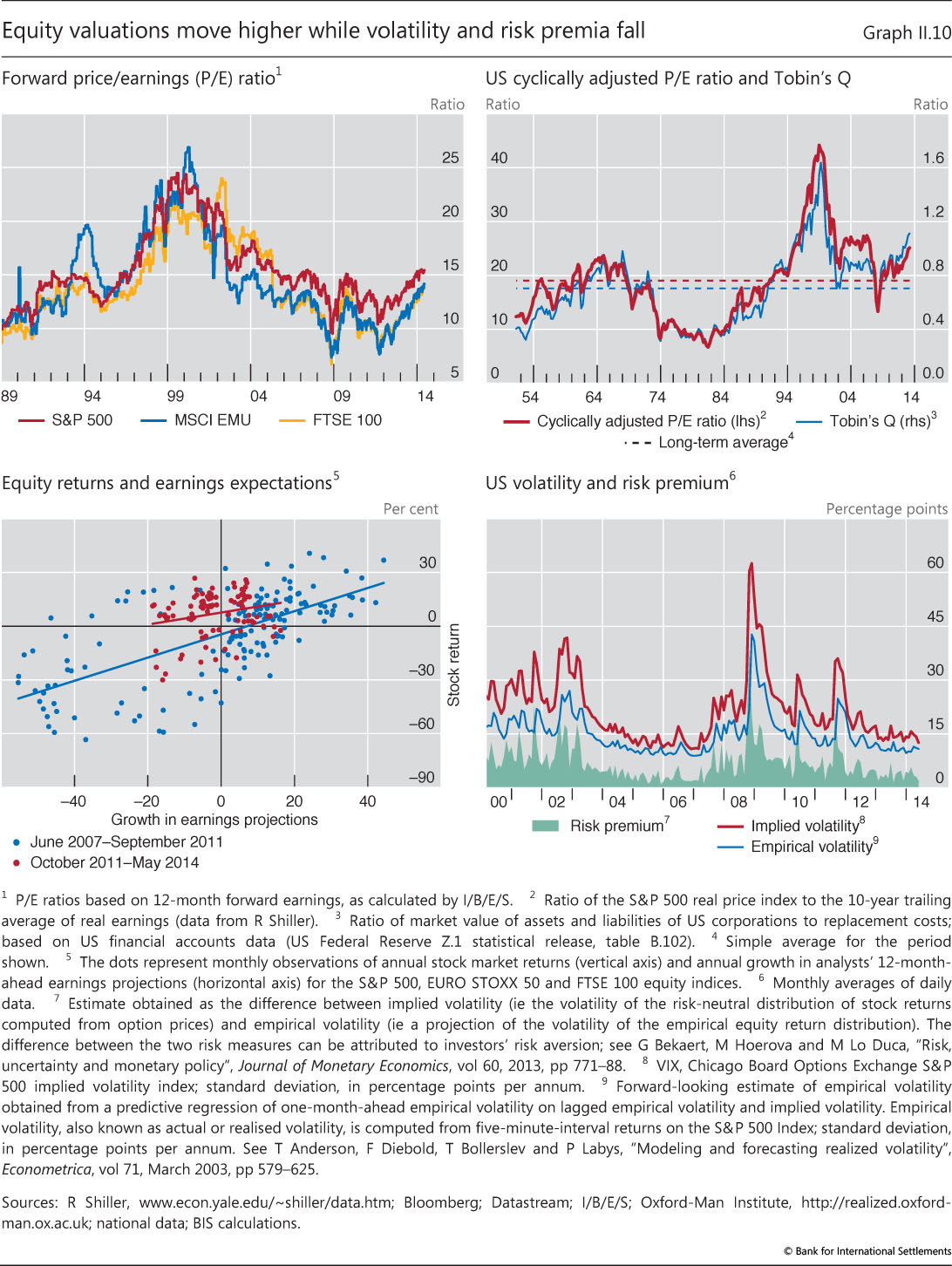

| II.10 | Equity valuations move higher while volatility and risk premia fall | p 38 |

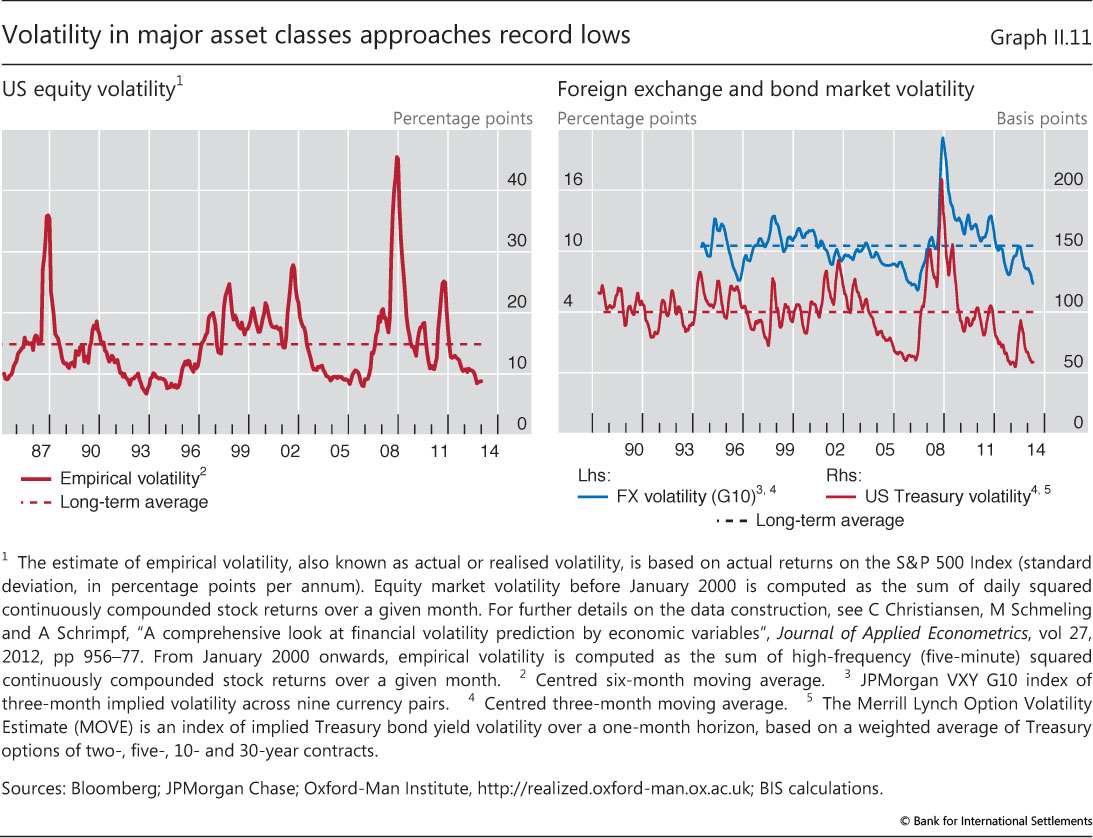

| II.11 | Volatility in major asset classes approaches record lows | p 39 |

| Chapter III: data behind the graphs (xlsx) | ||

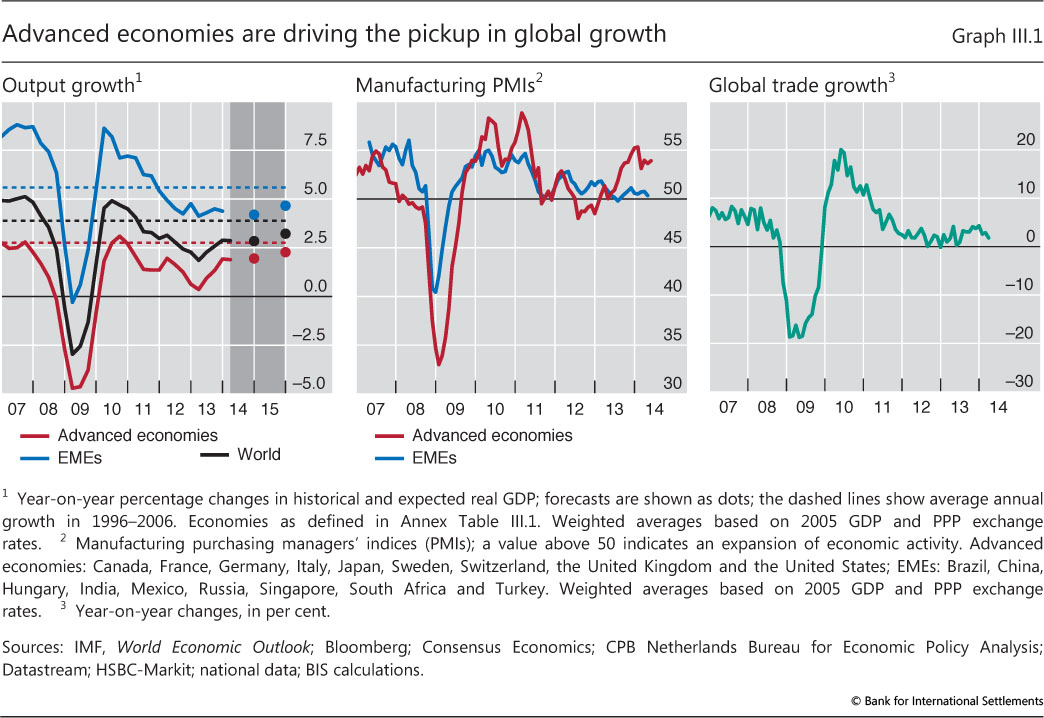

| III.1 | Advanced economies are driving the pickup in global growth | p 42 |

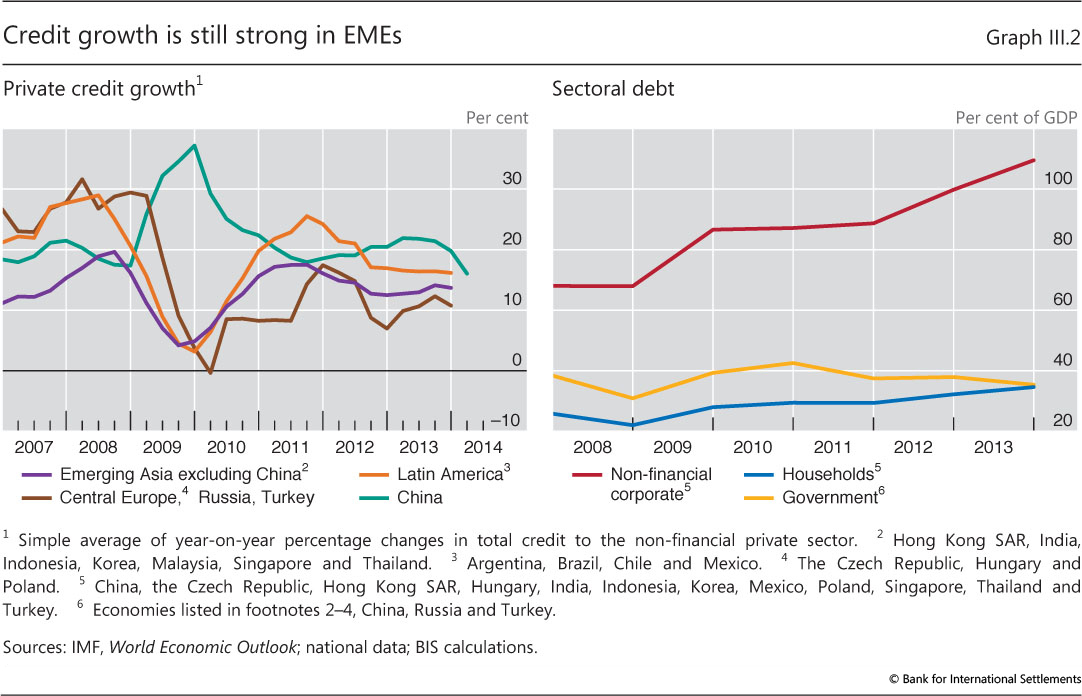

| III.2 | Credit growth is still strong in EMEs | p 43 |

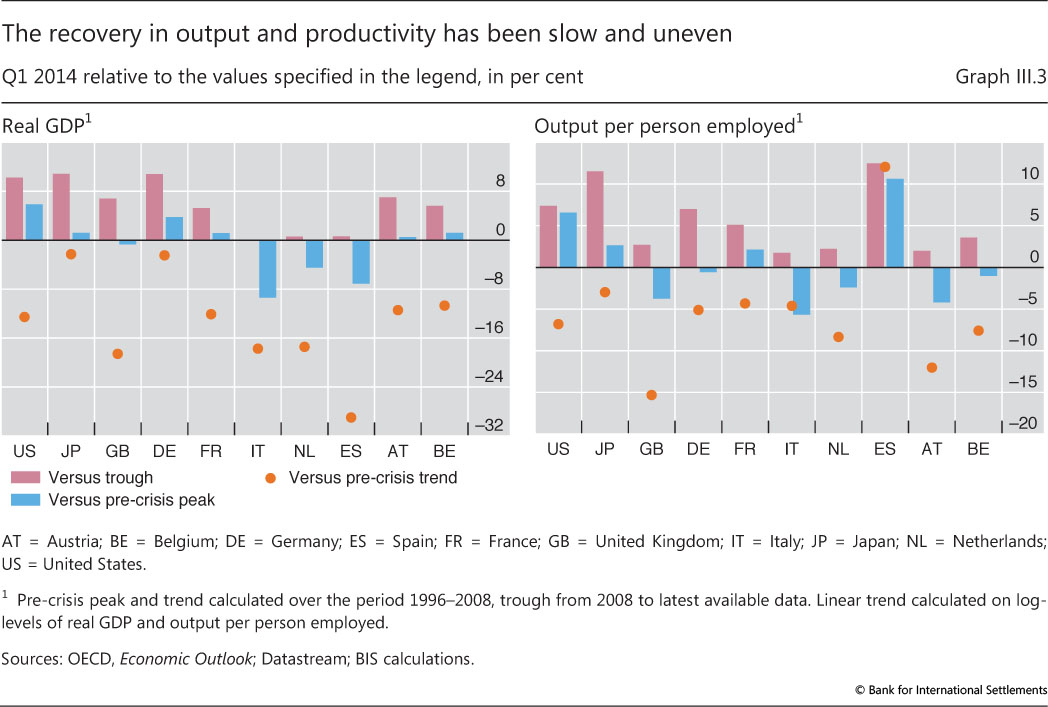

| III.3 | The recovery in output and productivity has been slow and uneven | p 44 |

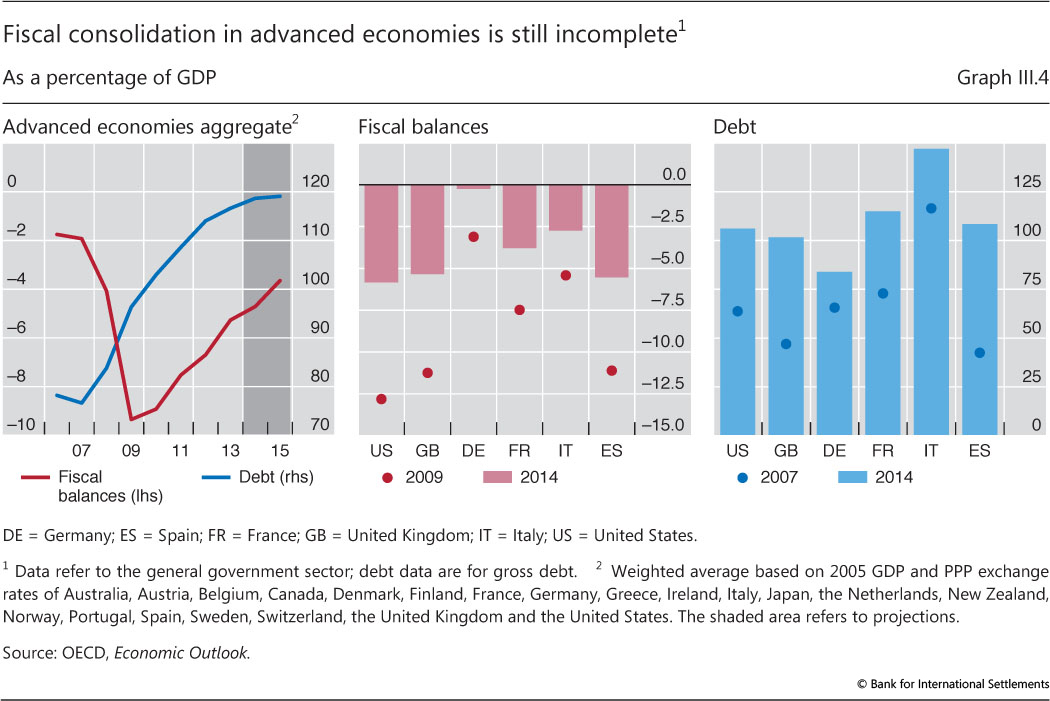

| III.4 | Fiscal consolidation in advanced economies is still incomplete | p 47 |

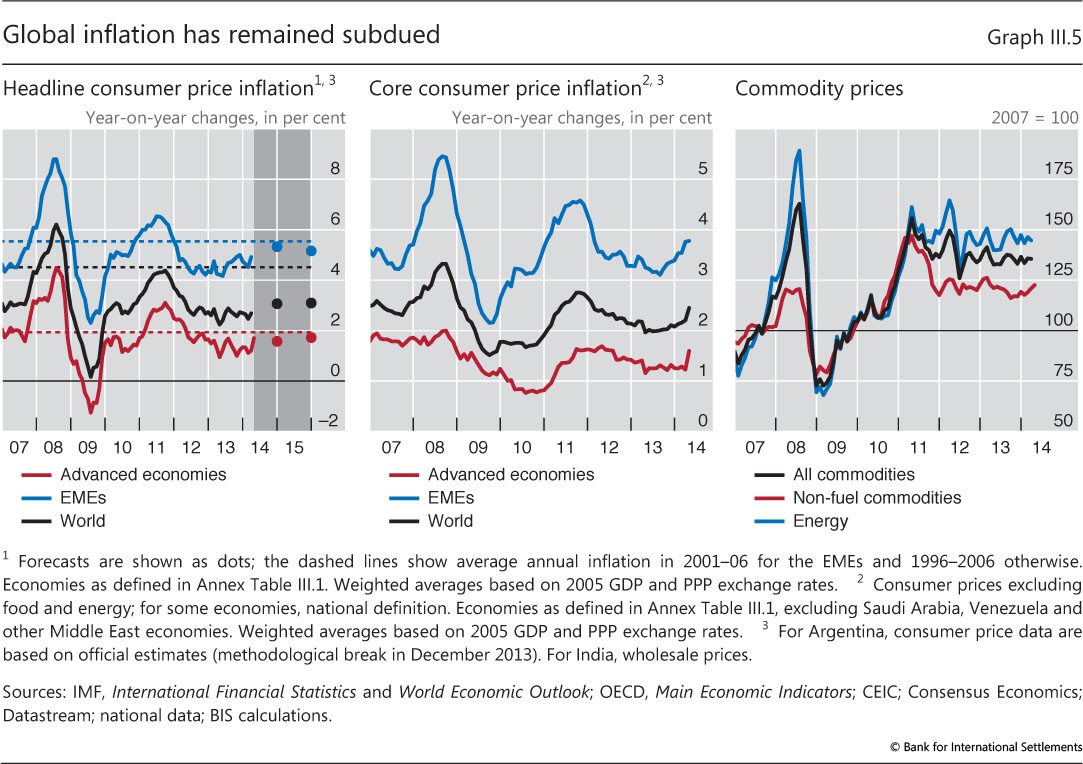

| III.5 | Global inflation has remained subdued | p 50 |

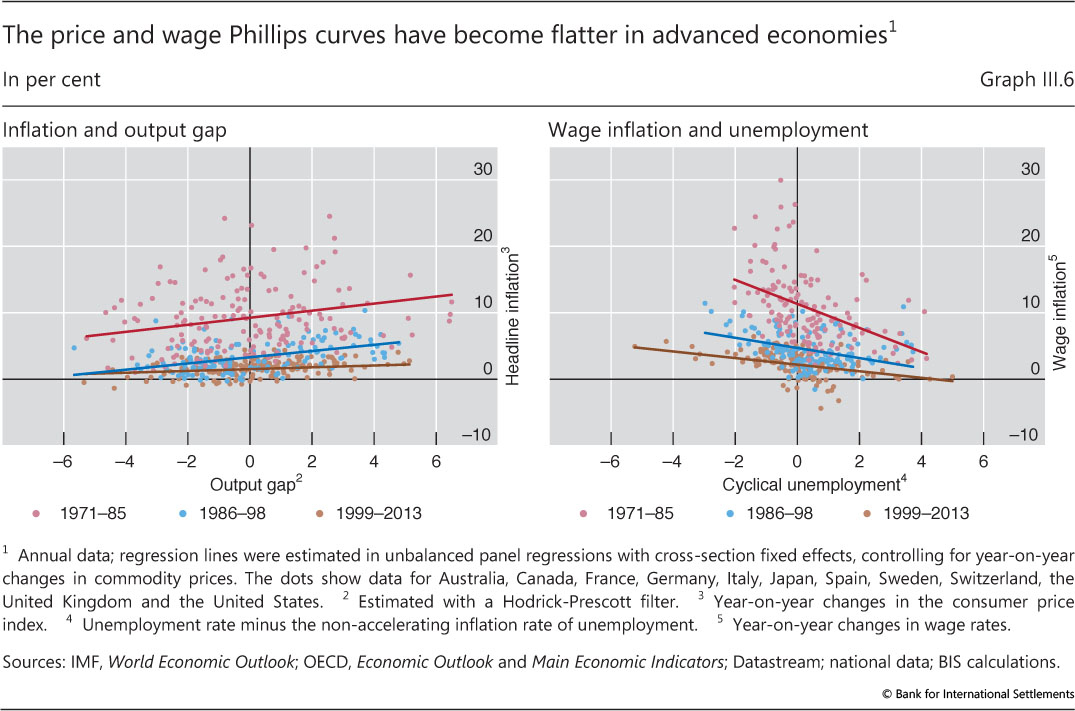

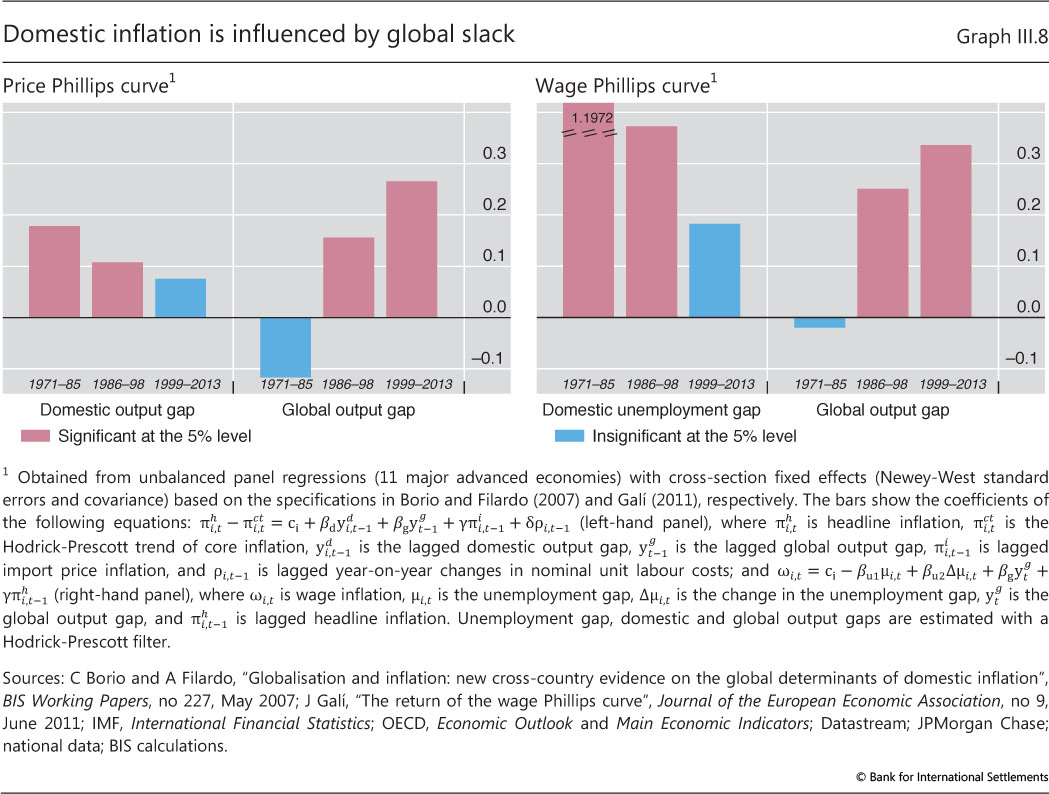

| III.6 | The price and wage Phillips curves have become flatter in advanced economies | p 51 |

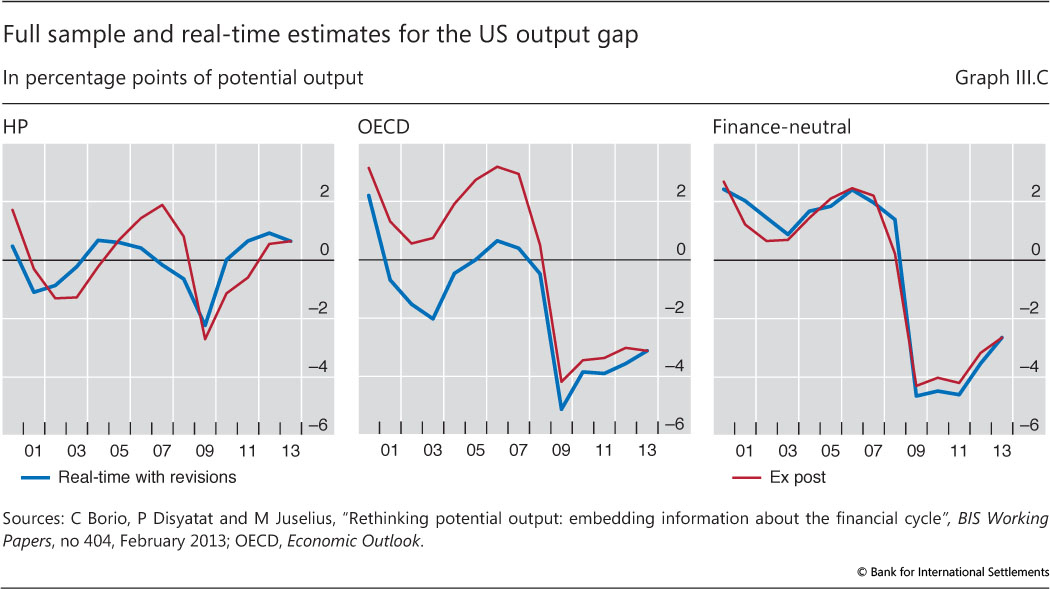

| III.C | Full sample and real-time estimates for the US output gap | p 52 |

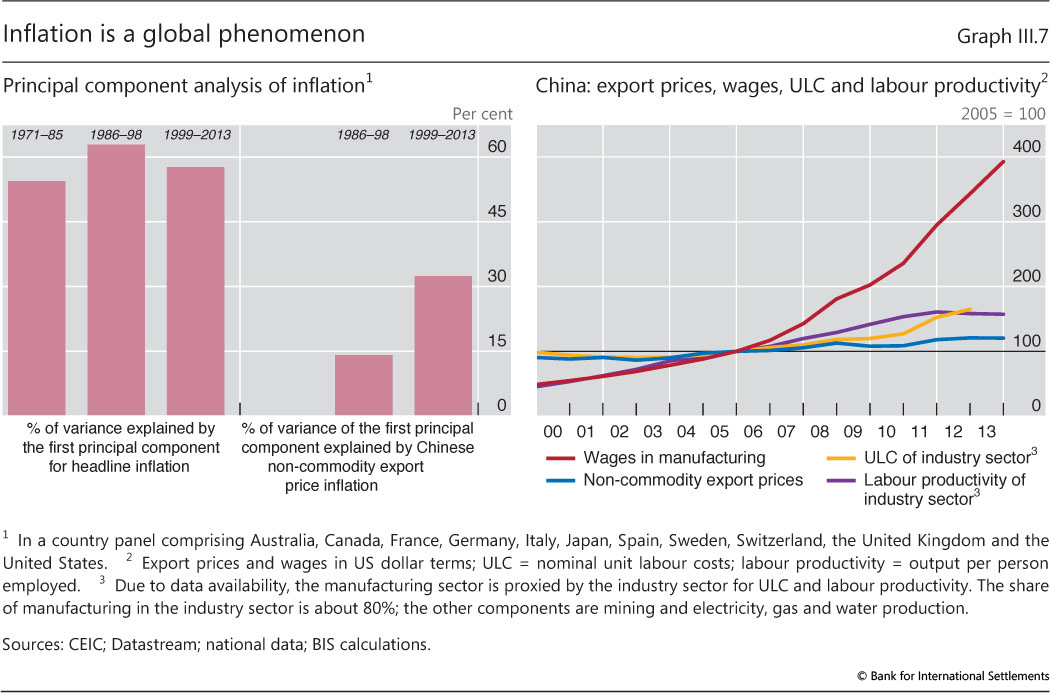

| III.7 | Inflation is a global phenomenon | p 54 |

| III.8 | Domestic inflation is influenced by global slack | p 55 |

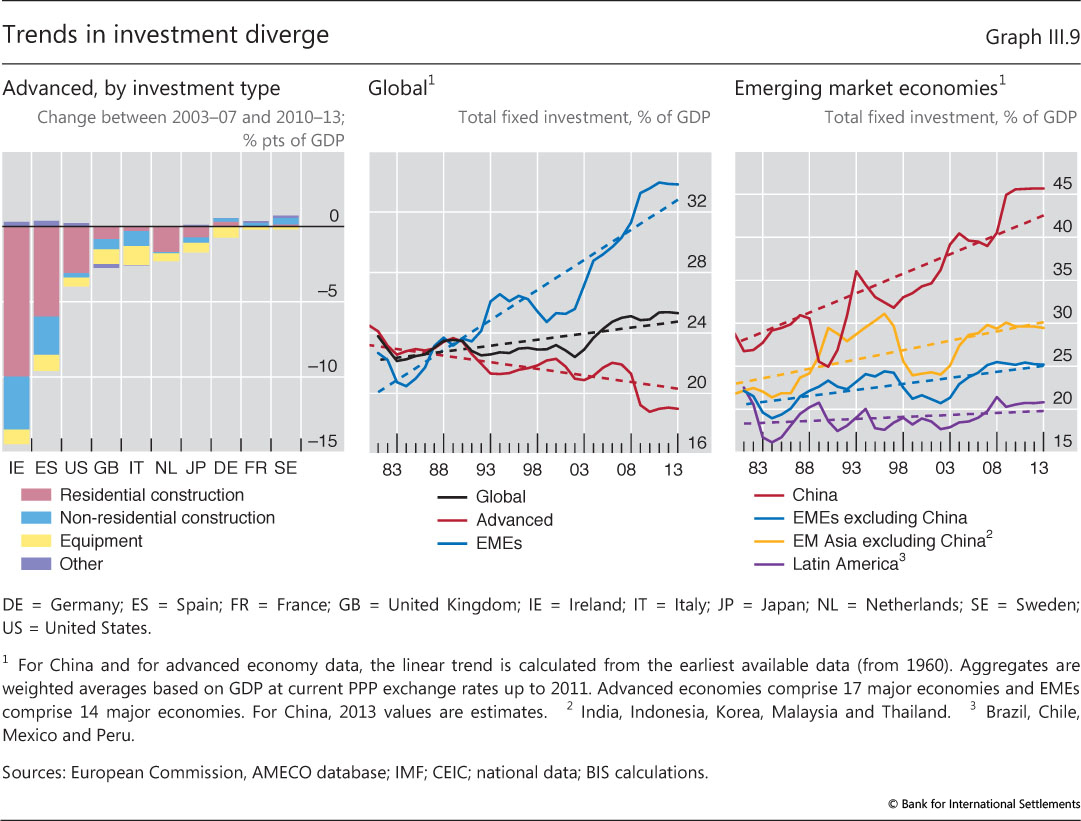

| III.9 | Trends in investment diverge | p 57 |

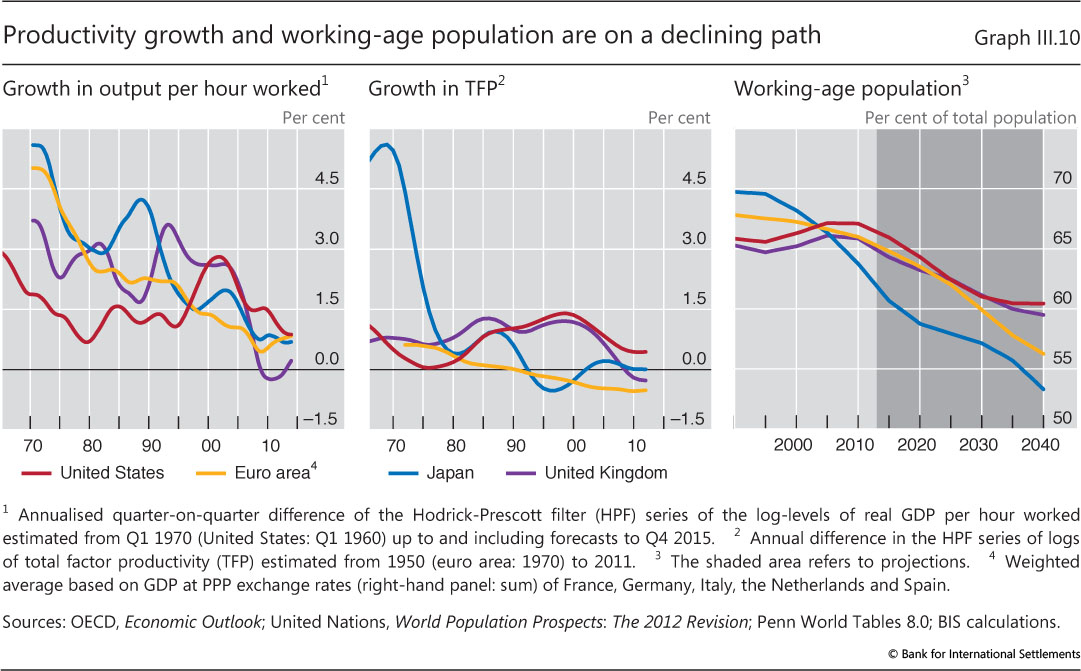

| III.10 | Productivity growth and working-age population are on a declining path | p 59 |

| Chapter IV: data behind the graphs (xlsx) | ||

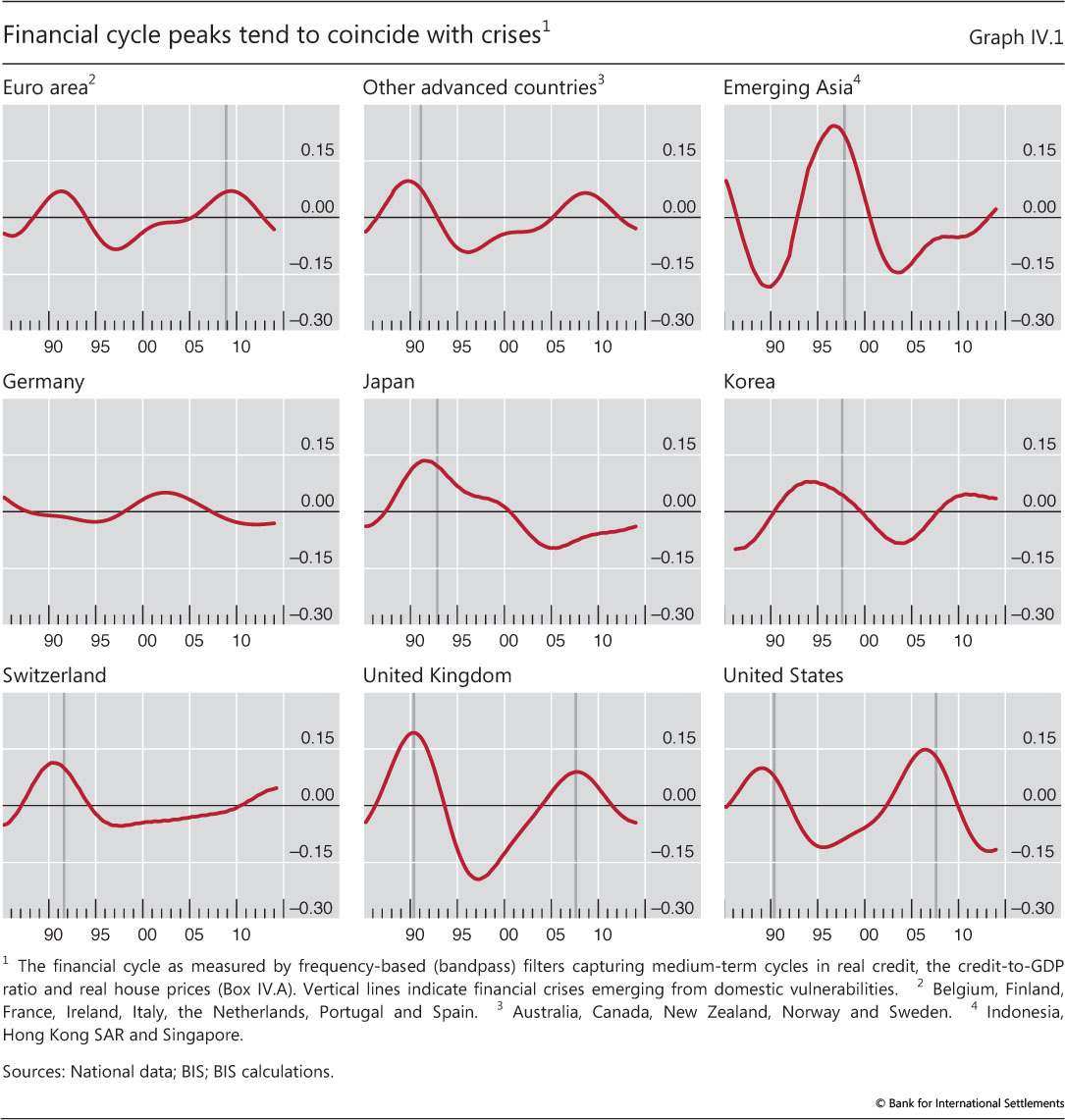

| IV.1 | Financial cycle peaks tend to coincide with crises | p 67 |

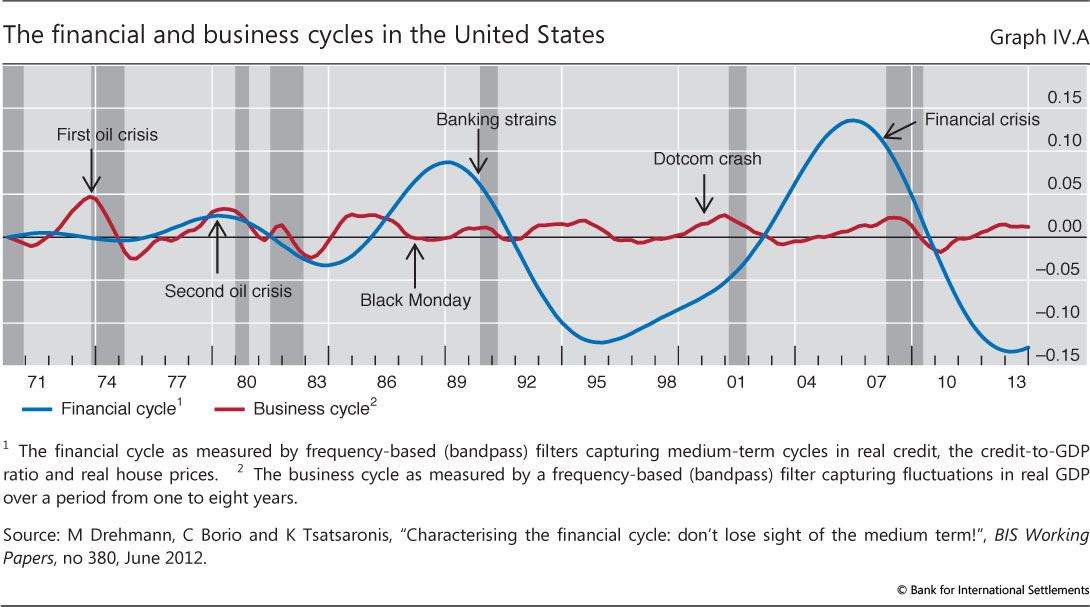

| IV.A | The financial and business cycles in the United States | p 68 |

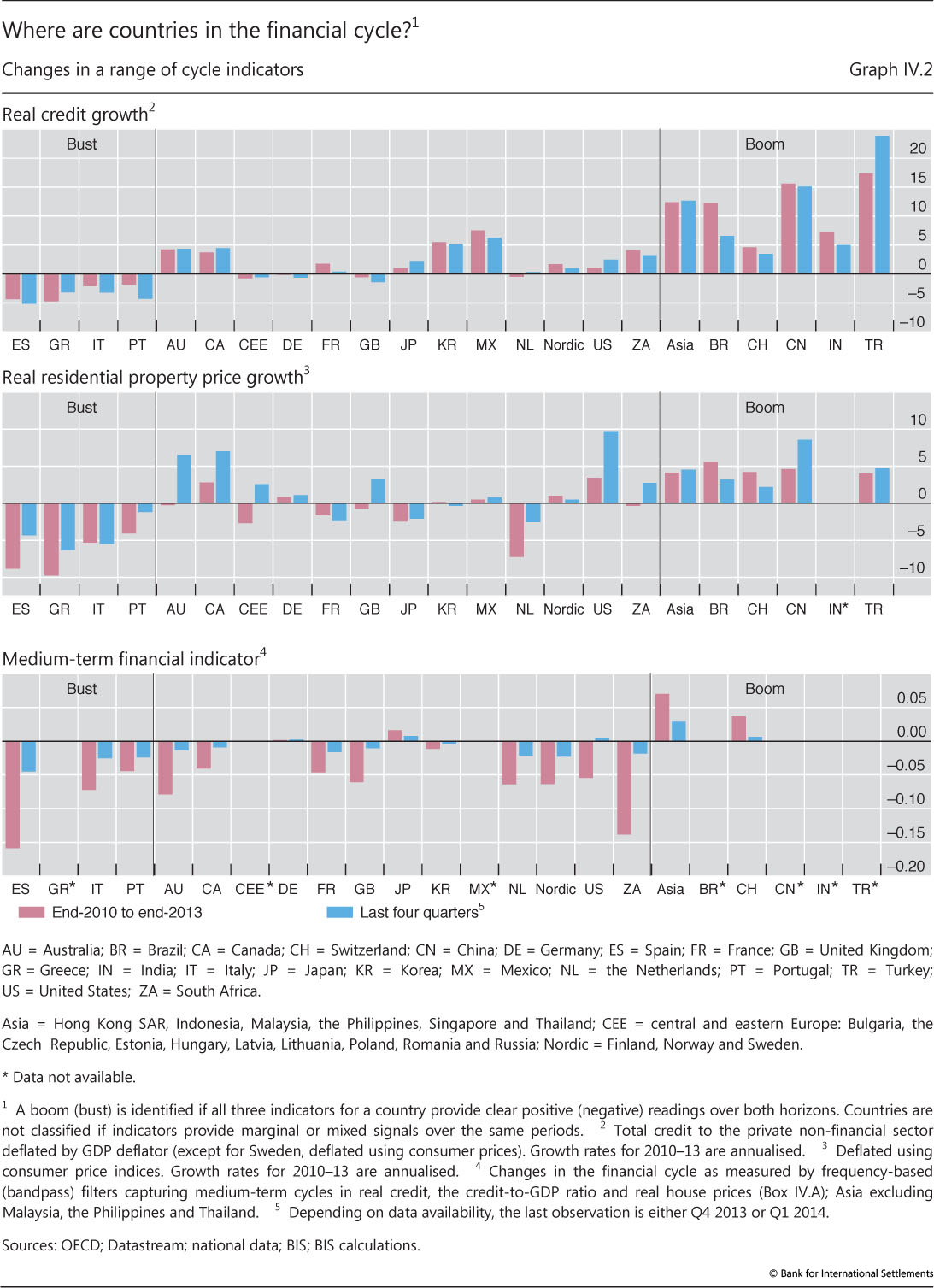

| IV.2 | Where are countries in the financial cycle? | p 70 |

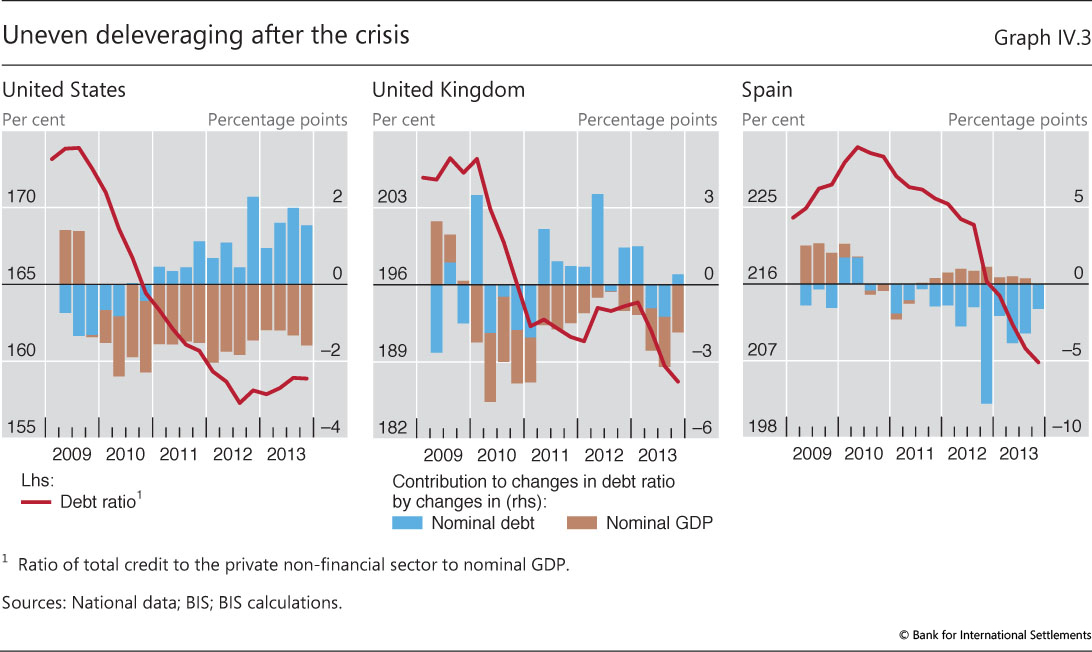

| IV.3 | Uneven deleveraging after the crisis | p 71 |

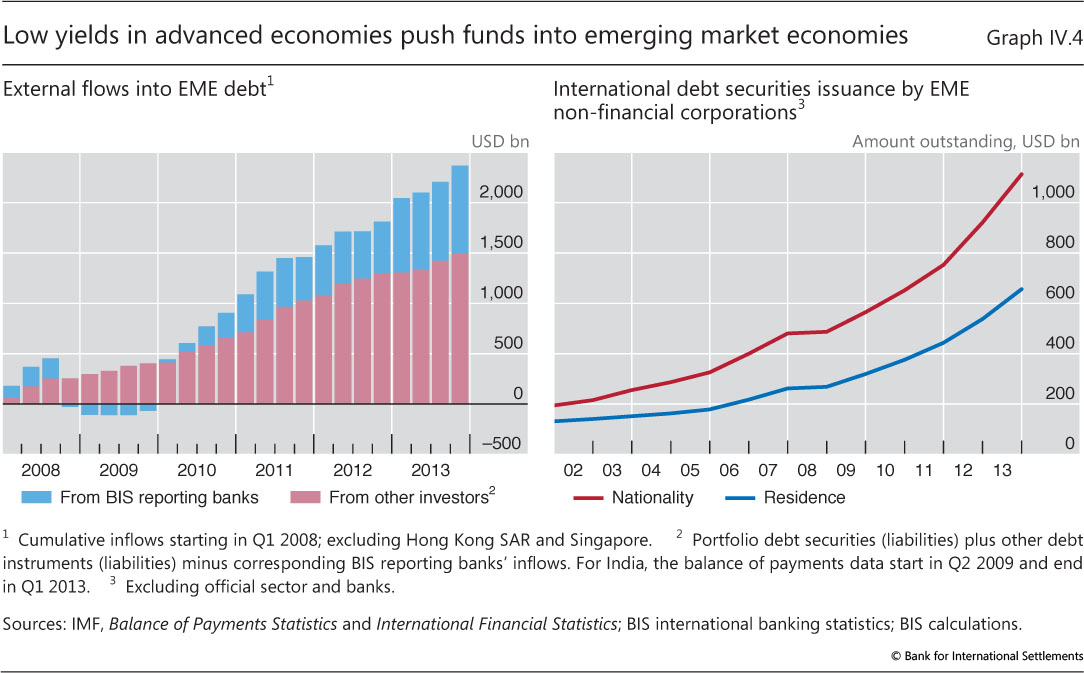

| IV.4 | Low yields in advanced economies push funds into emerging market economies | p 72 |

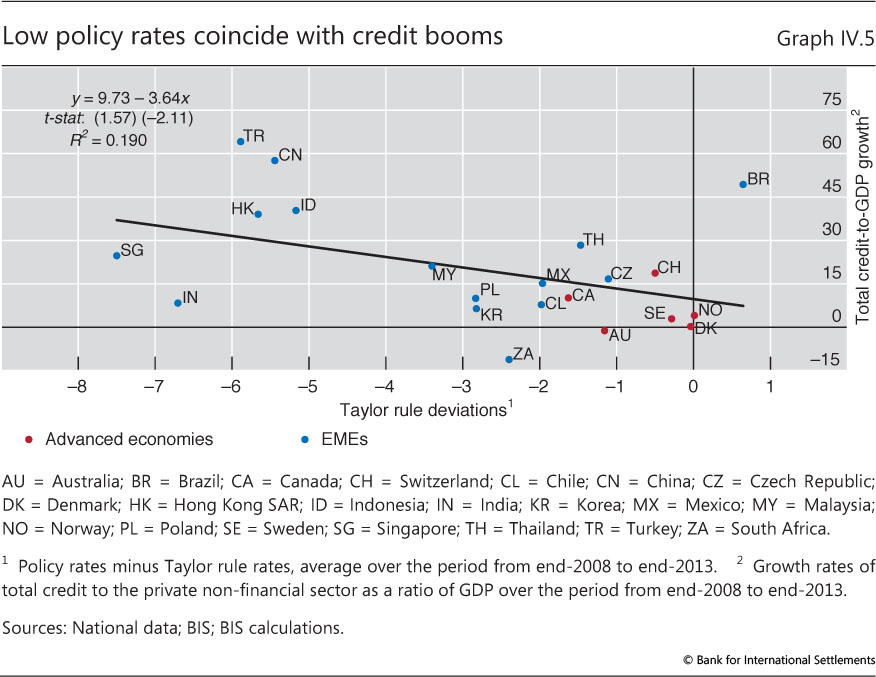

| IV.5 | Low policy rates coincide with credit booms | p 73 |

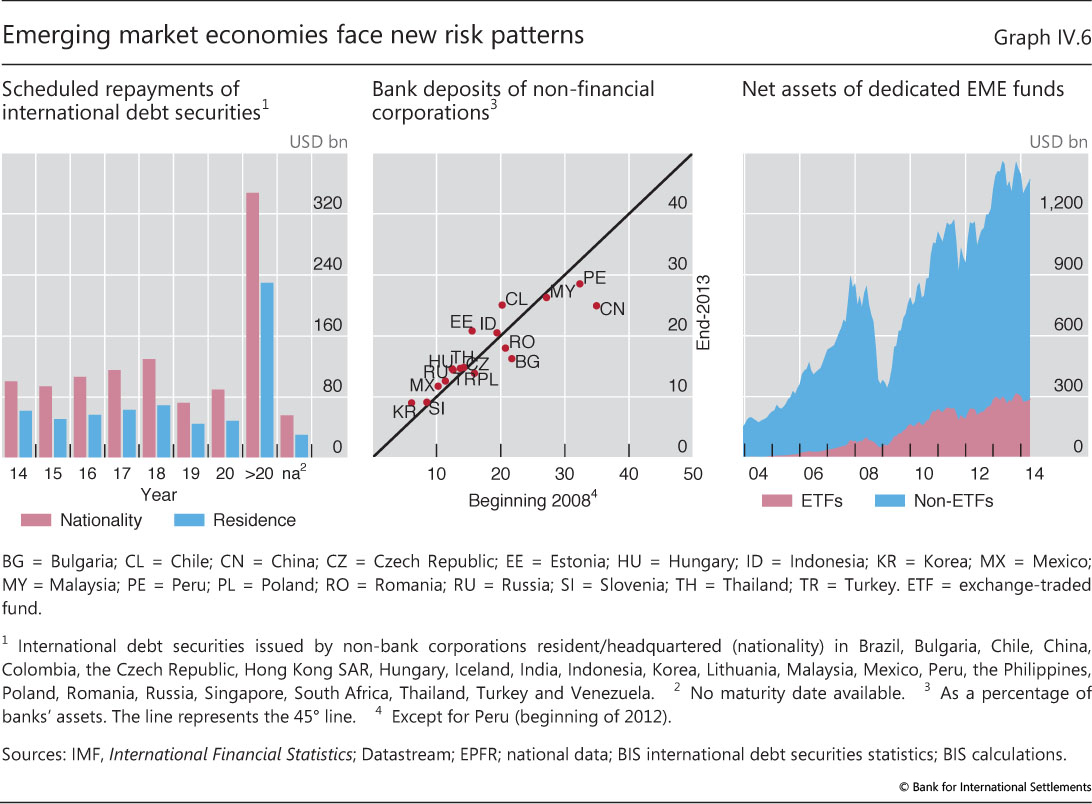

| IV.6 | Emerging market economies face new risk patterns | p 77 |

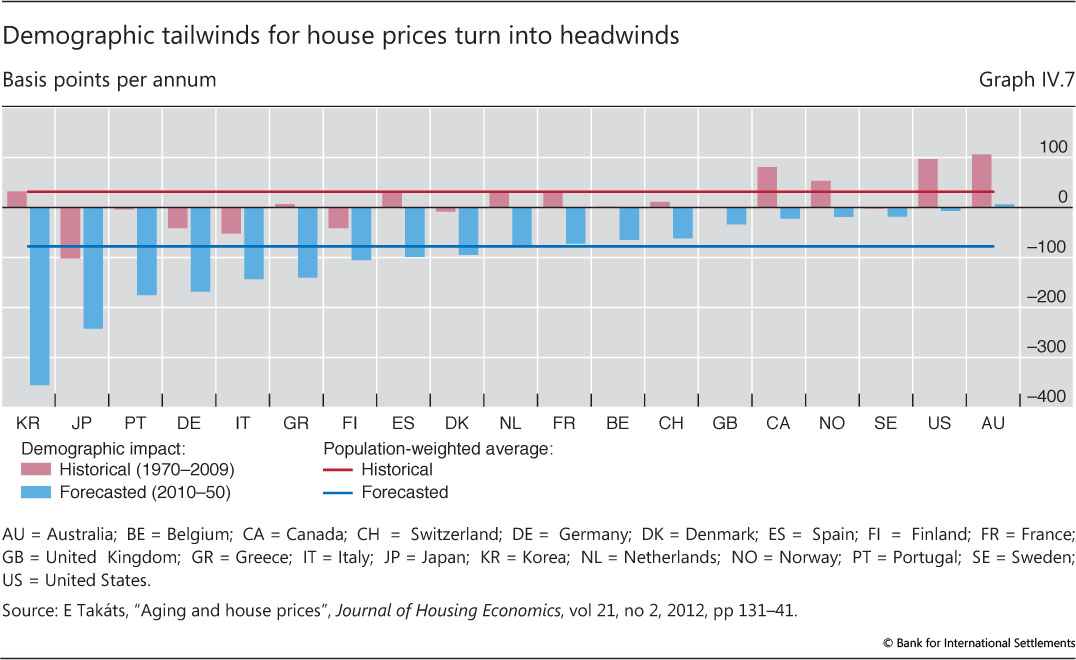

| IV.7 | Demographic tailwinds for house prices turn into headwinds | p 79 |

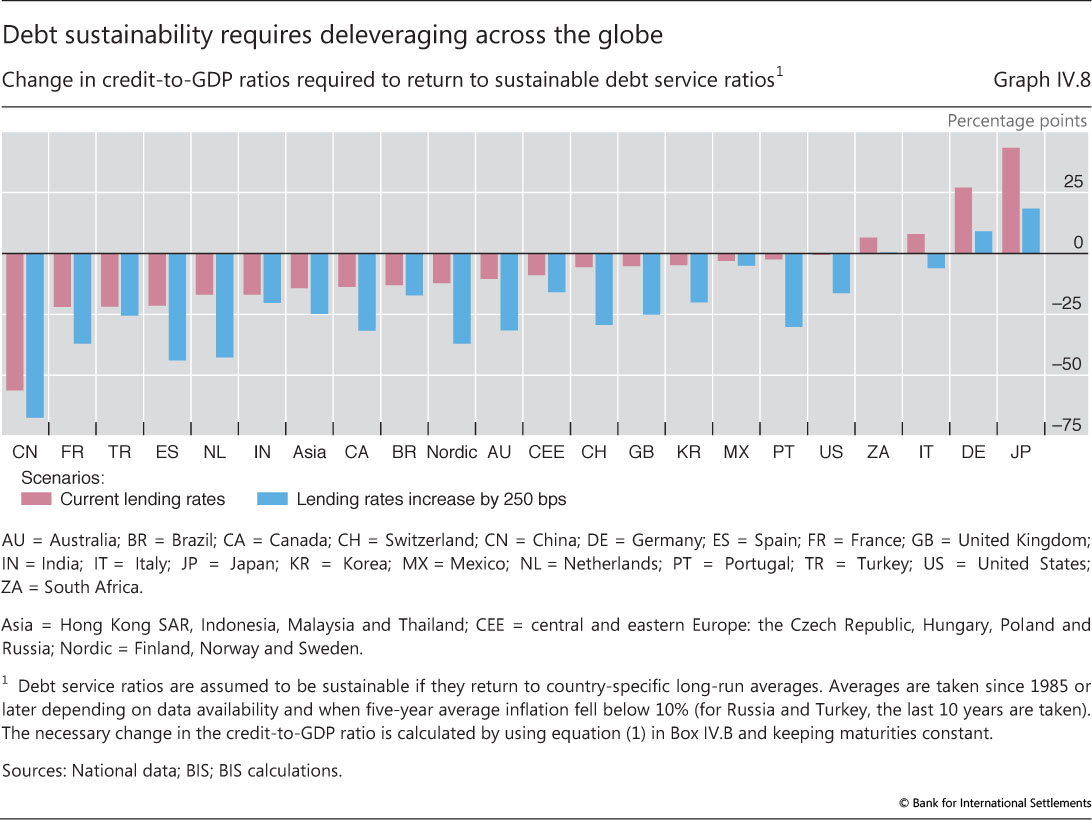

| IV.8 | Debt sustainability requires deleveraging across the globe | p 80 |

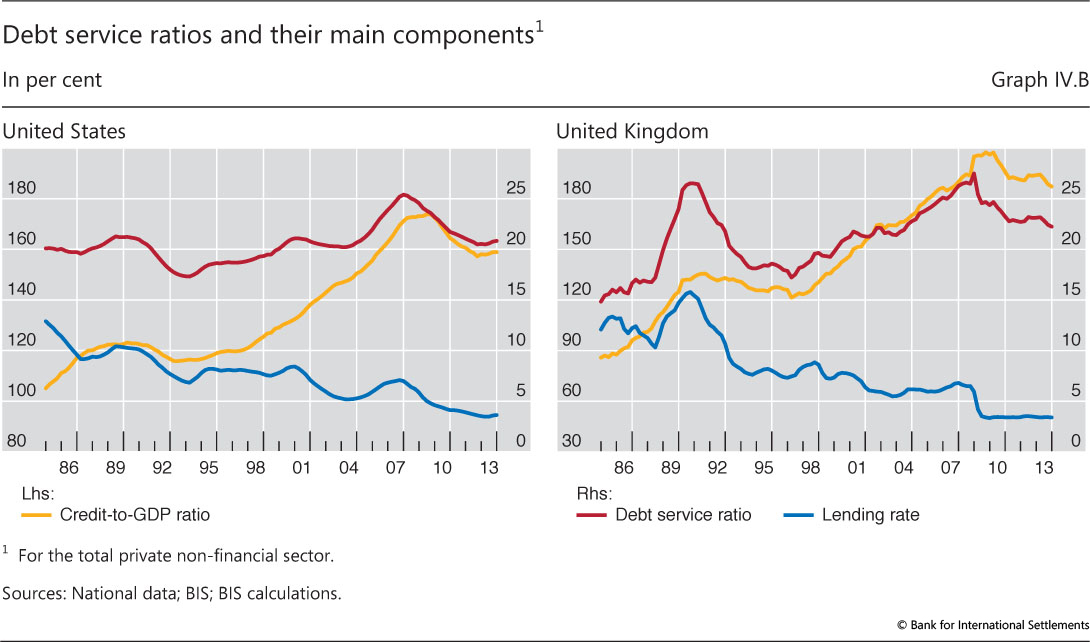

| IV.B | Debt service ratios and their main components | p 82 |

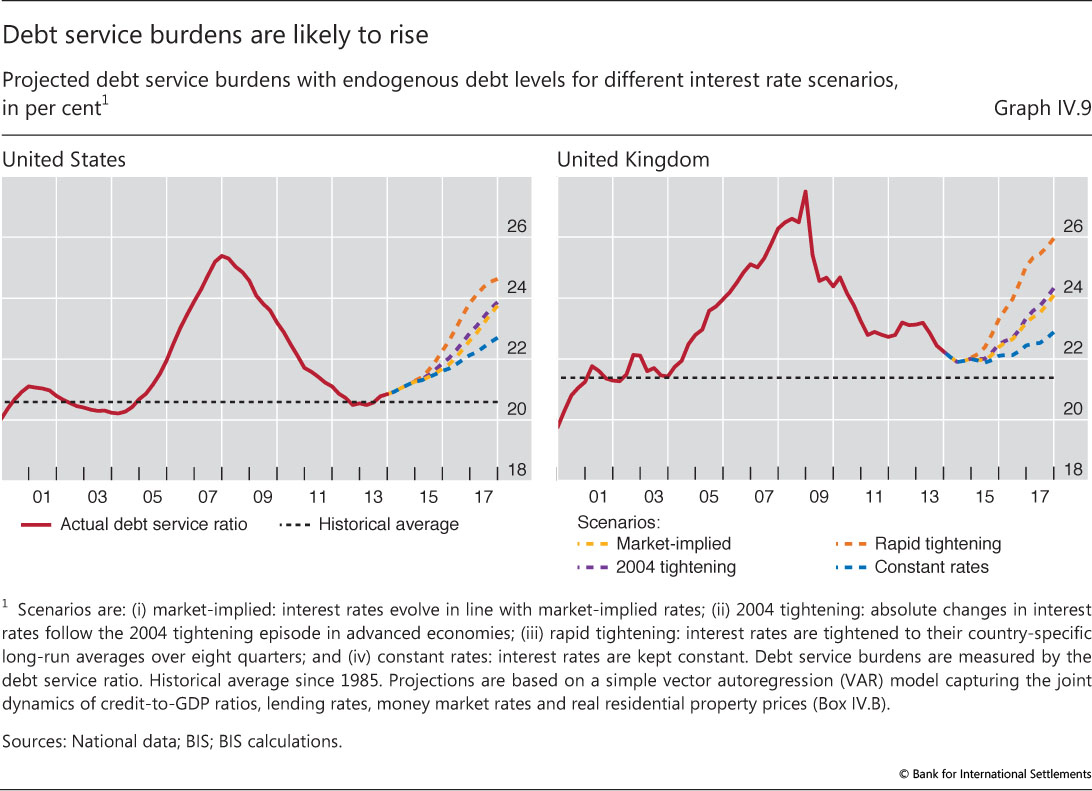

| IV.9 | Debt service burdens are likely to rise | p 83 |

| Chapter V: data behind the graphs (xlsx) | ||

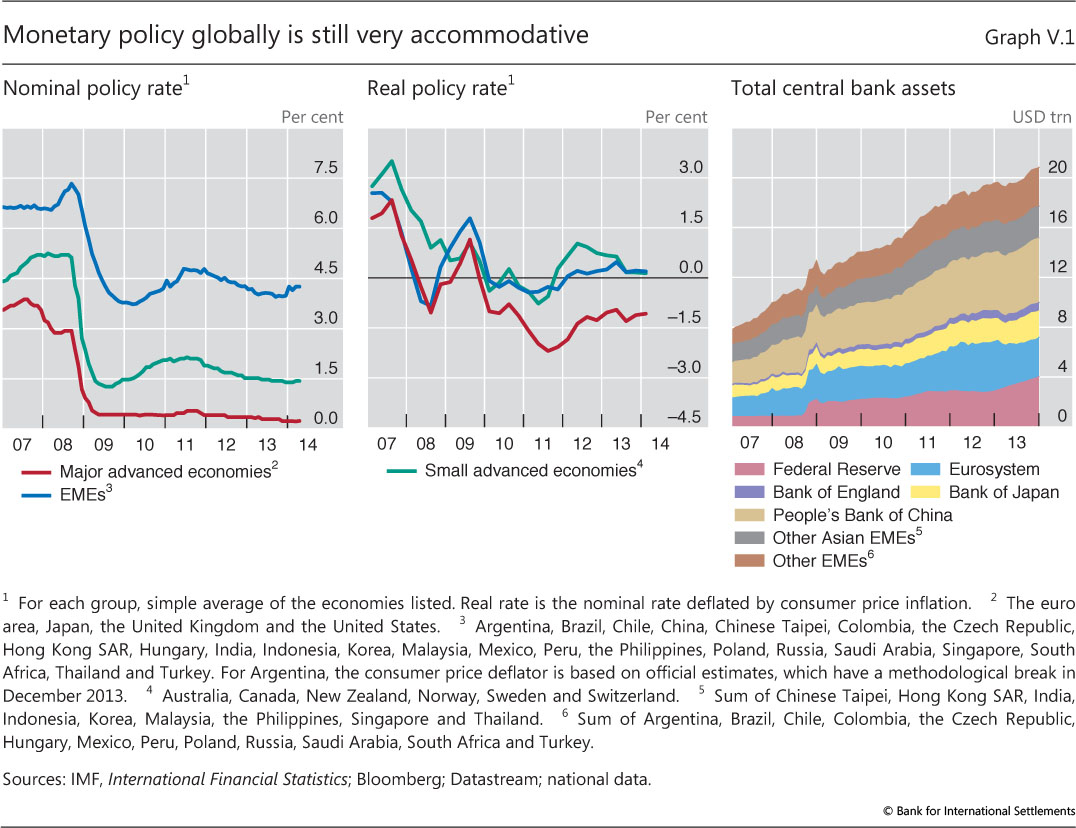

| V.1 | Monetary policy globally is still very accommodative | p 86 |

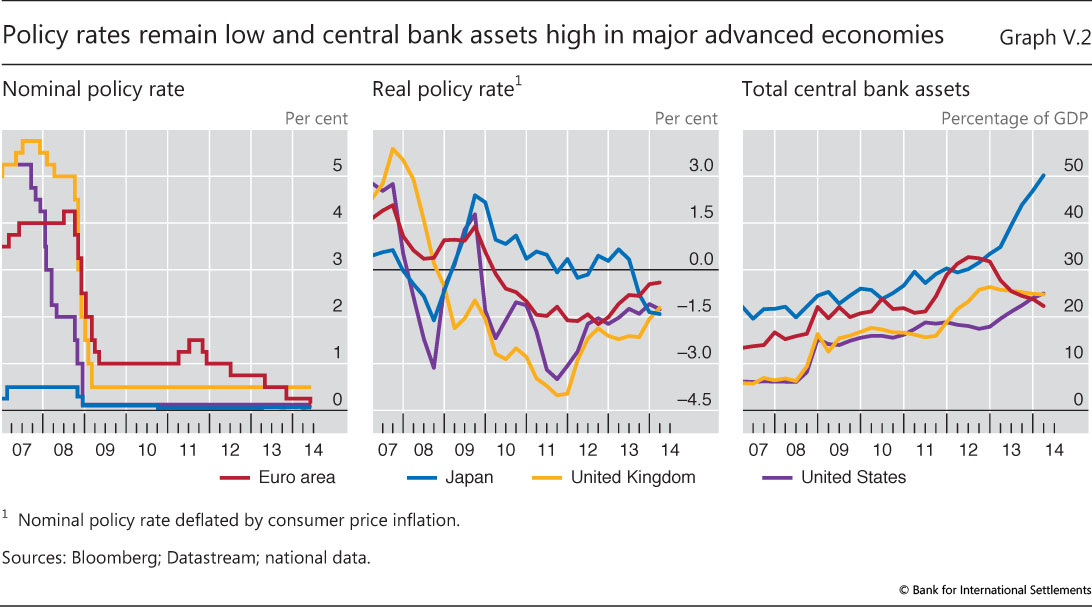

| V.2 | Policy rates remain low and central bank assets high in major advanced economies | p 87 |

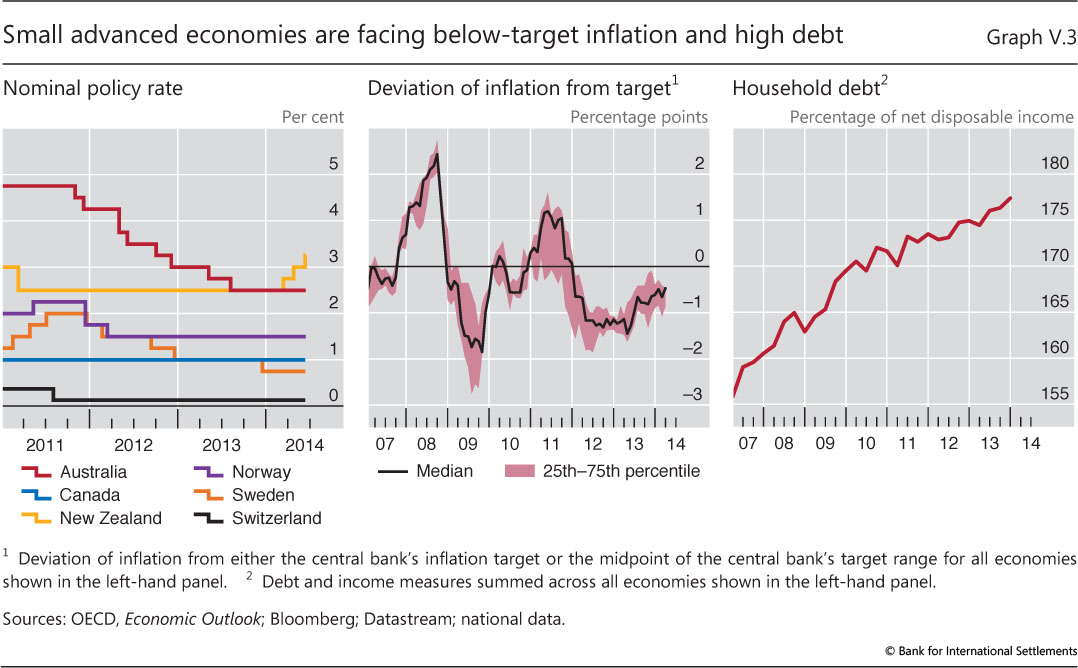

| V.3 | Small advanced economies are facing below-target inflation and high debt | p 88 |

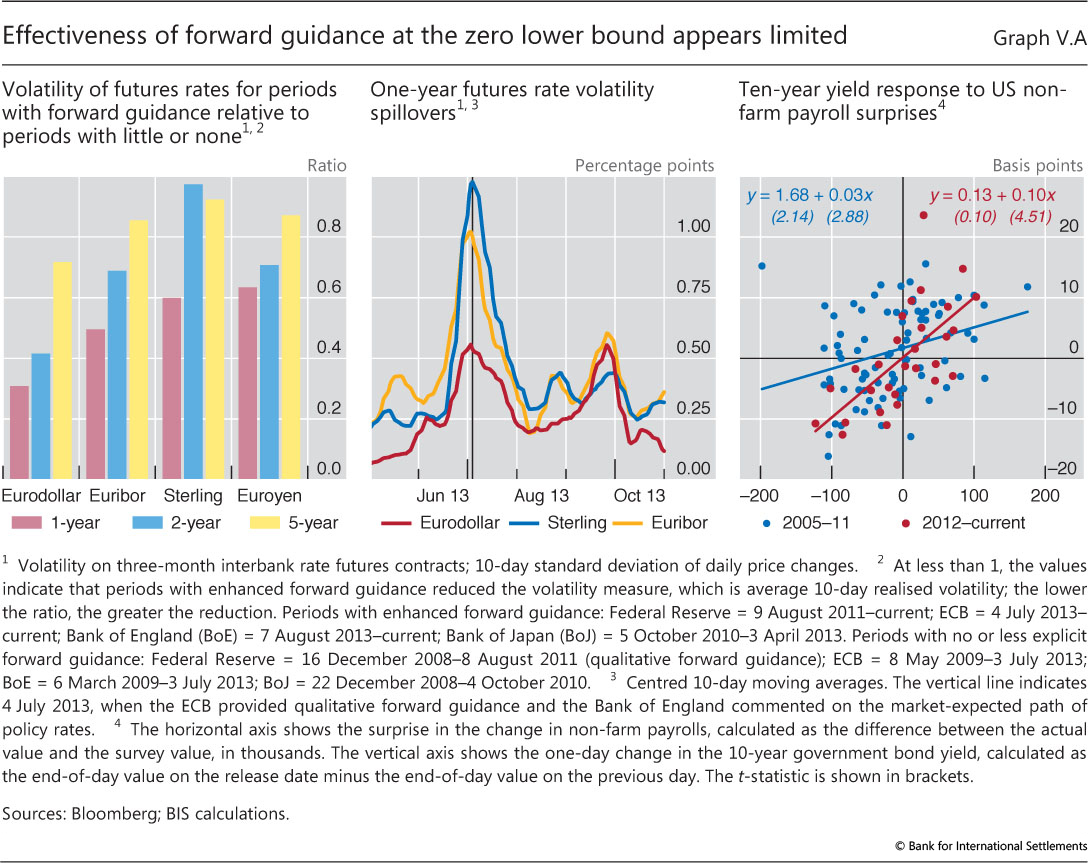

| V.A | Effectiveness of forward guidance at the zero lower bound appears limited | p 89 |

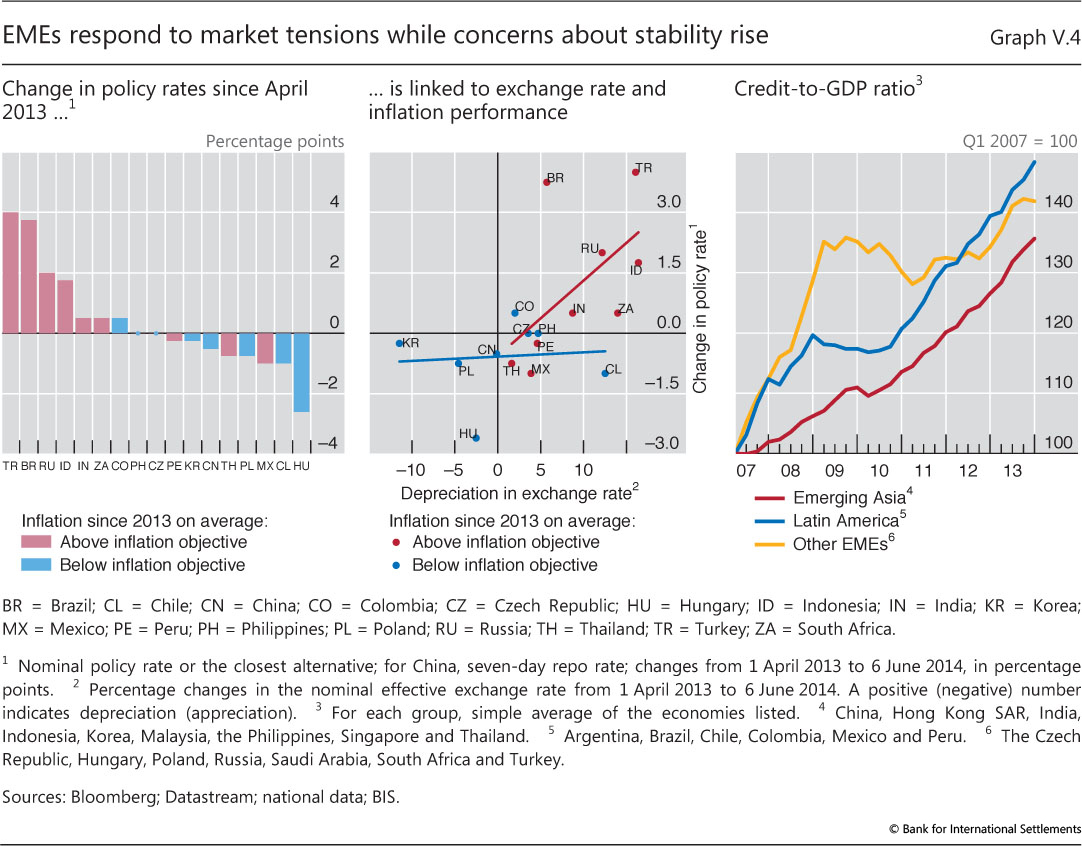

| V.4 | EMEs respond to market tensions while concerns about stability rise | p 91 |

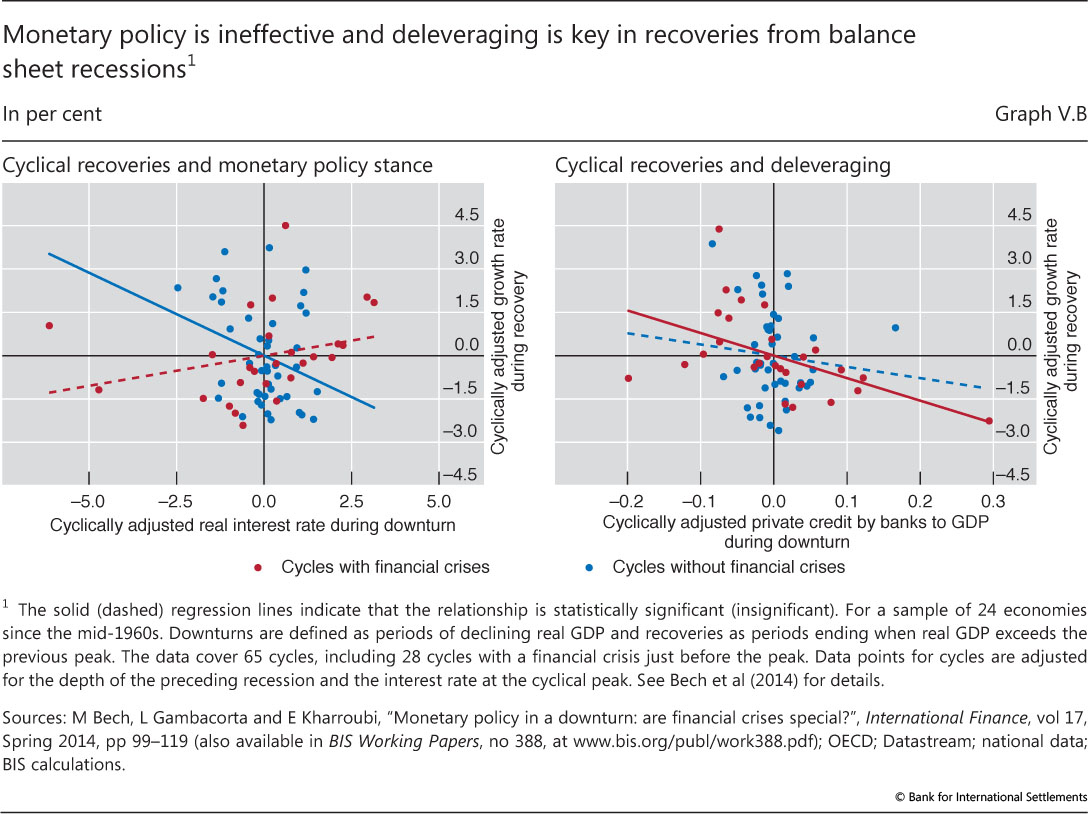

| V.B | Monetary policy is ineffective and deleveraging is key in recoveries from balance sheet recessions | p 93 |

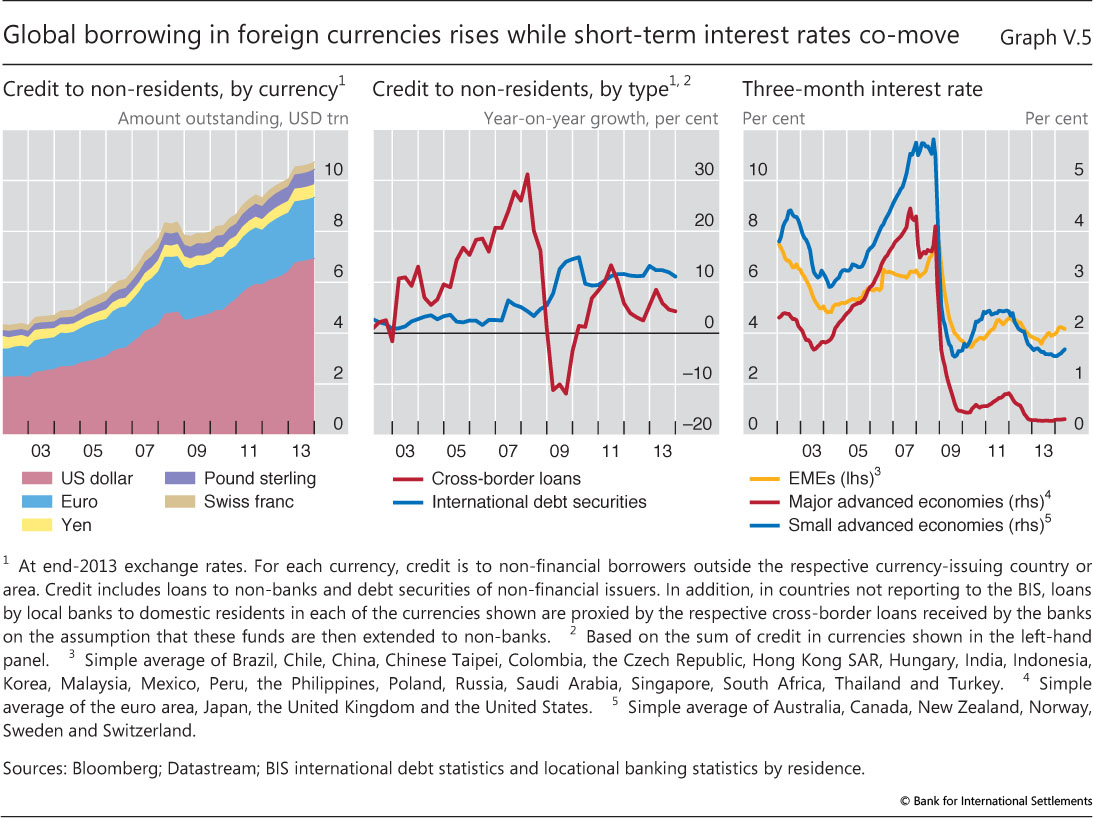

| V.5 | Global borrowing in foreign currencies rises while short-term interest rates co-move | p 94 |

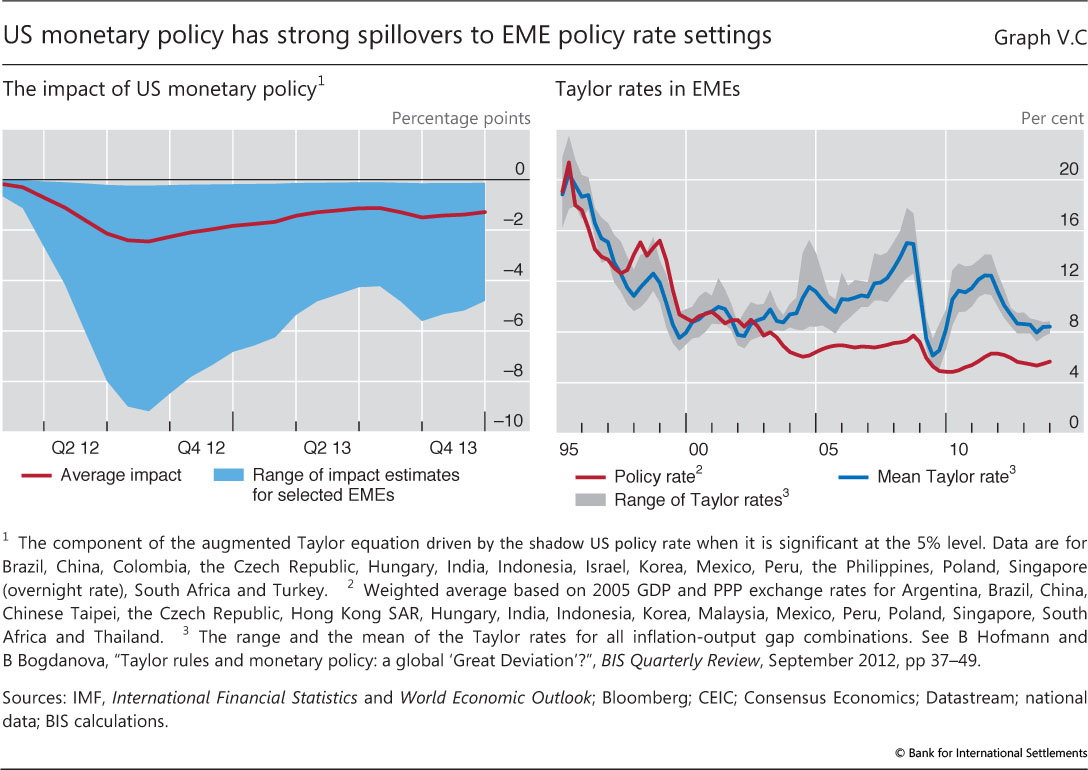

| V.C | US monetary policy has strong spillovers to EME policy rate settings | p 95 |

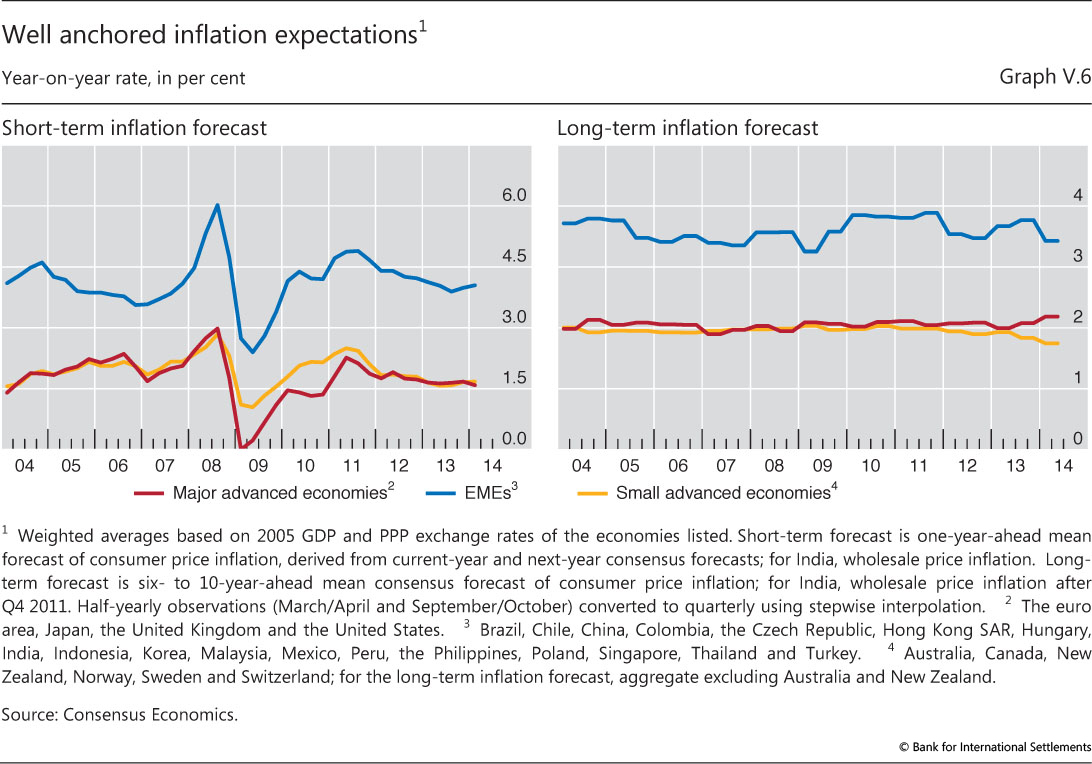

| V.6 | Well anchored inflation expectations | p 97 |

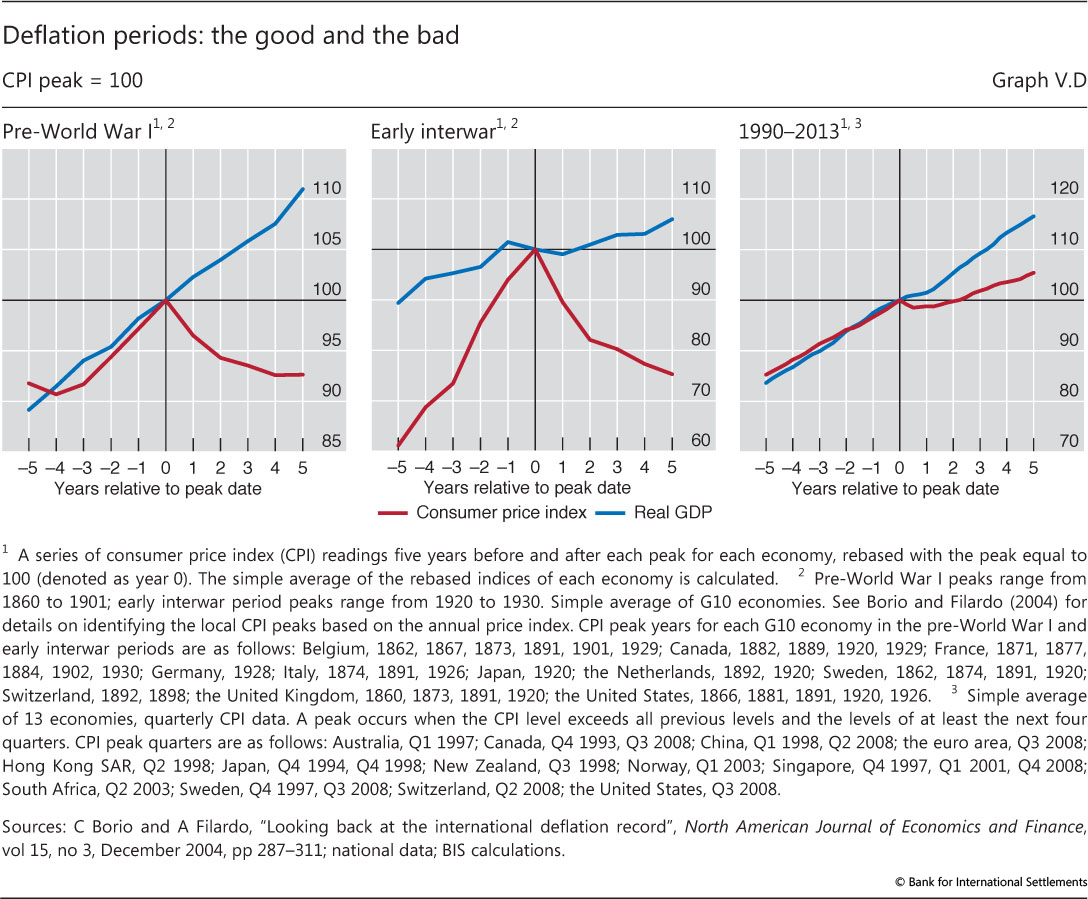

| V.D | Deflation periods: the good and the bad | p 98 |

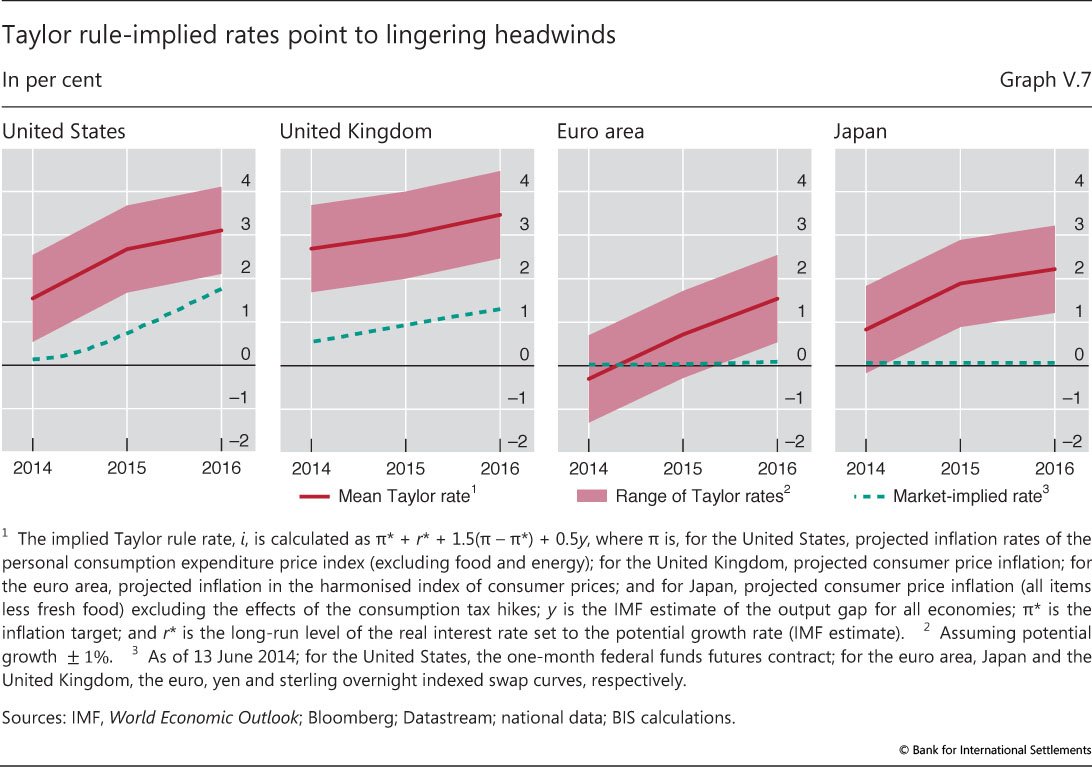

| V.7 | Taylor rule-implied rates point to lingering headwinds | p 101 |

| Chapter VI: data behind the graphs (xlsx) | ||

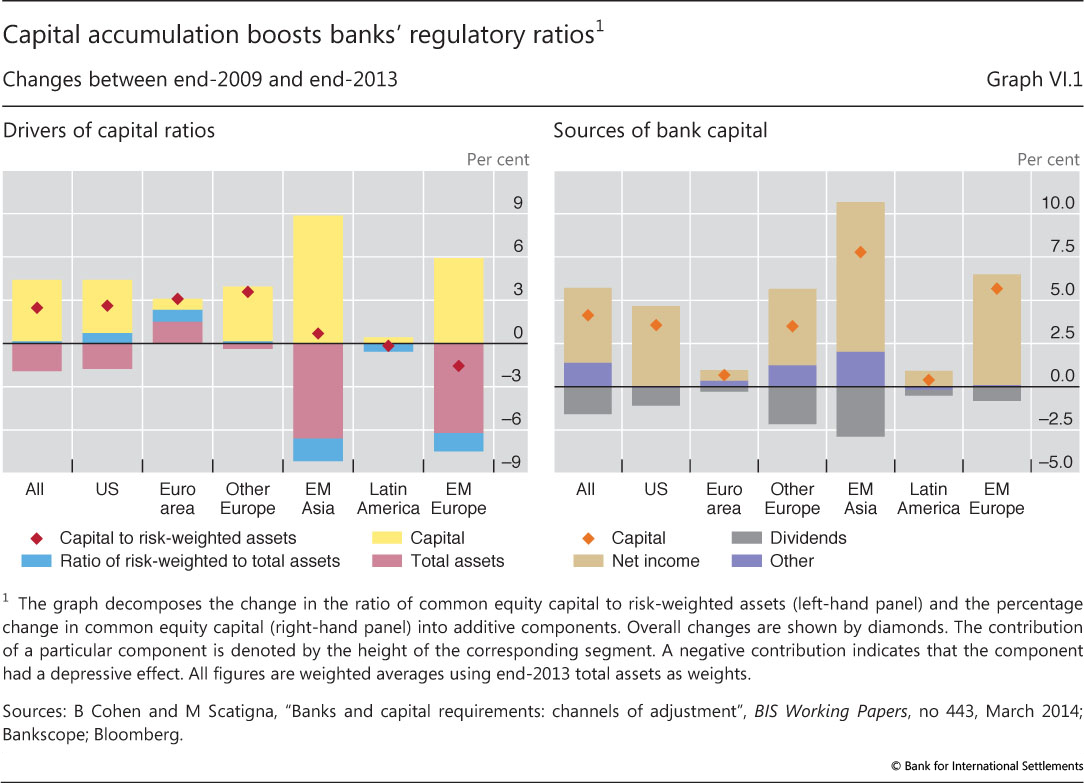

| VI.1 | Capital accumulation boosts banks' regulatory ratios | p 106 |

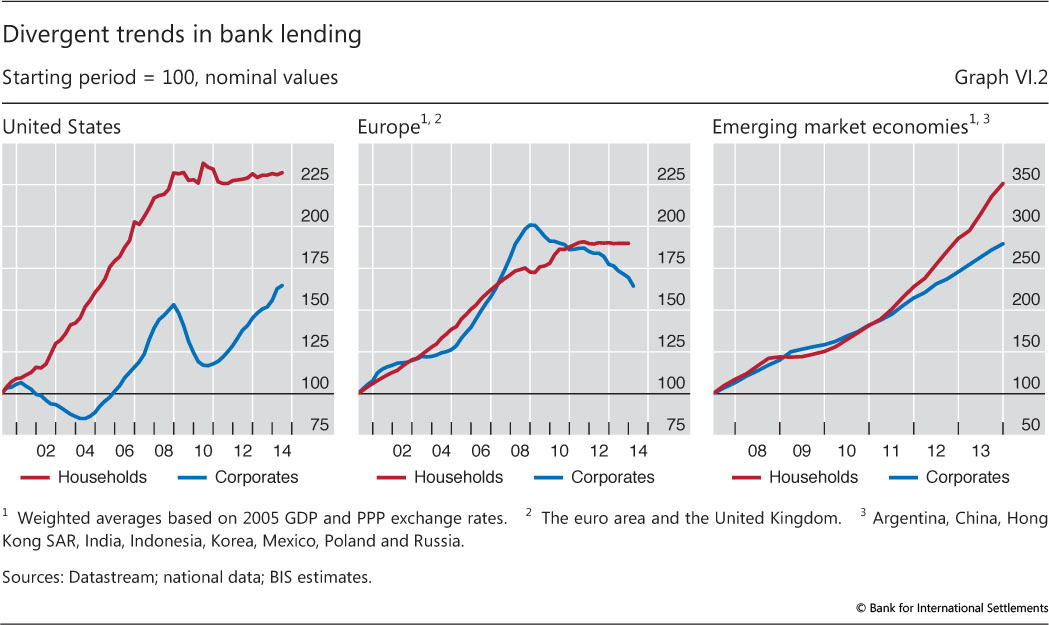

| VI.2 | Divergent trends in bank lending | p 110 |

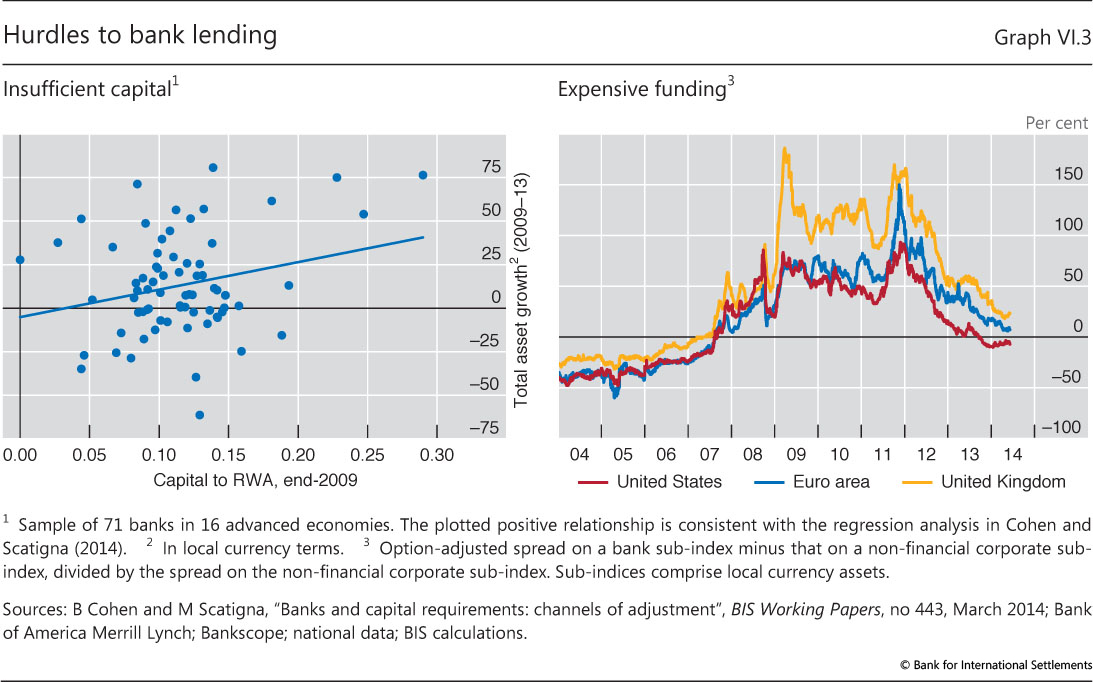

| VI.3 | Hurdles to bank lending | p 111 |

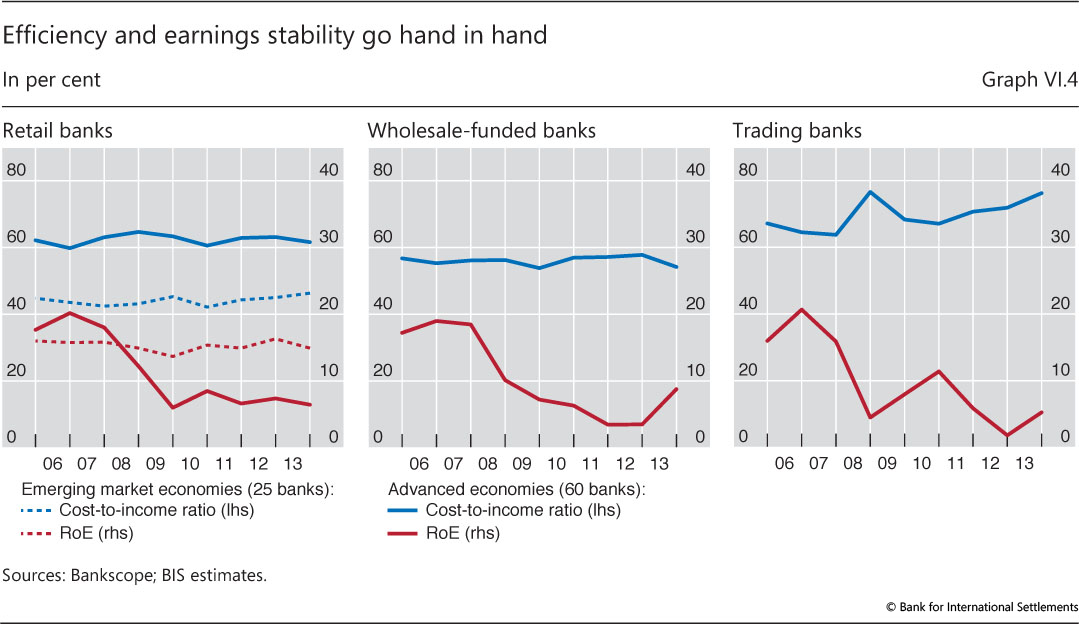

| VI.4 | Efficiency and earnings stability go hand in hand | p 112 |

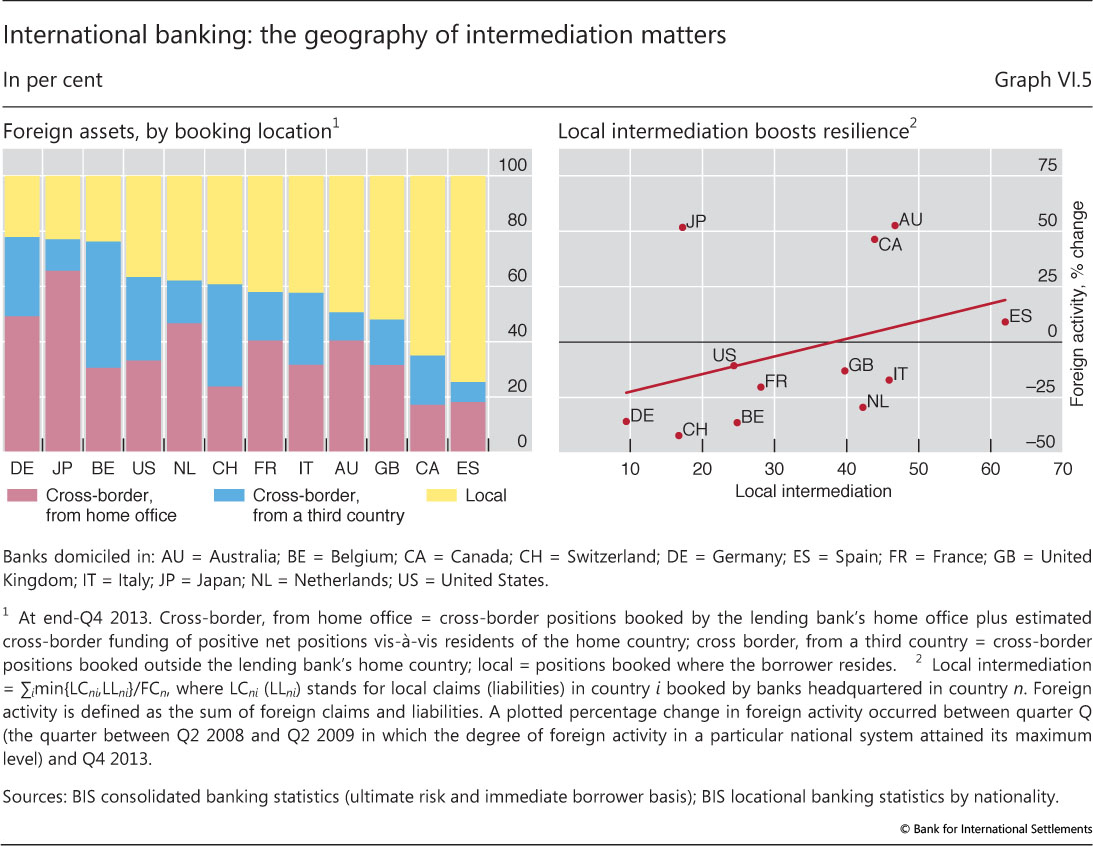

| VI.5 | International banking: the geography of intermediation matters | p 114 |

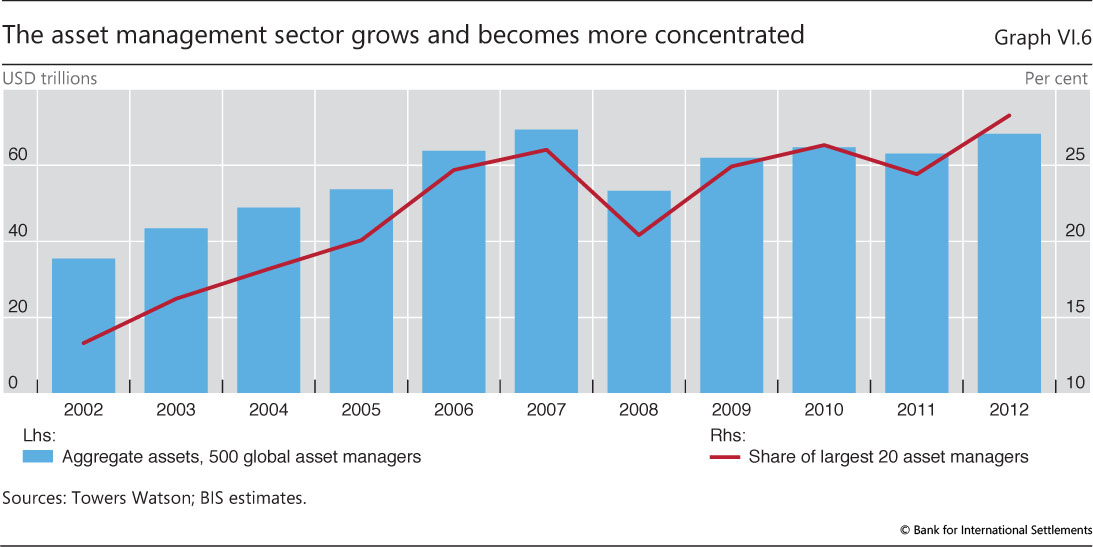

| VI.6 | The asset management sector grows and becomes more concentrated | p 115 |

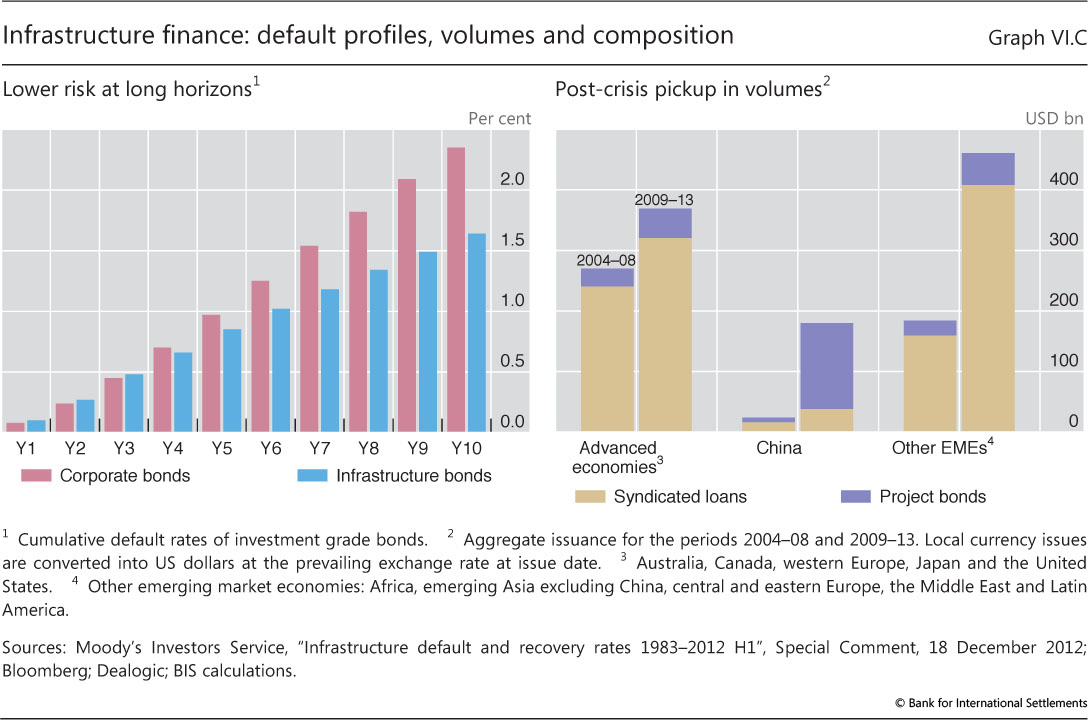

| VI.C | Infrastructure finance: default profiles, volumes and composition | p 116 |

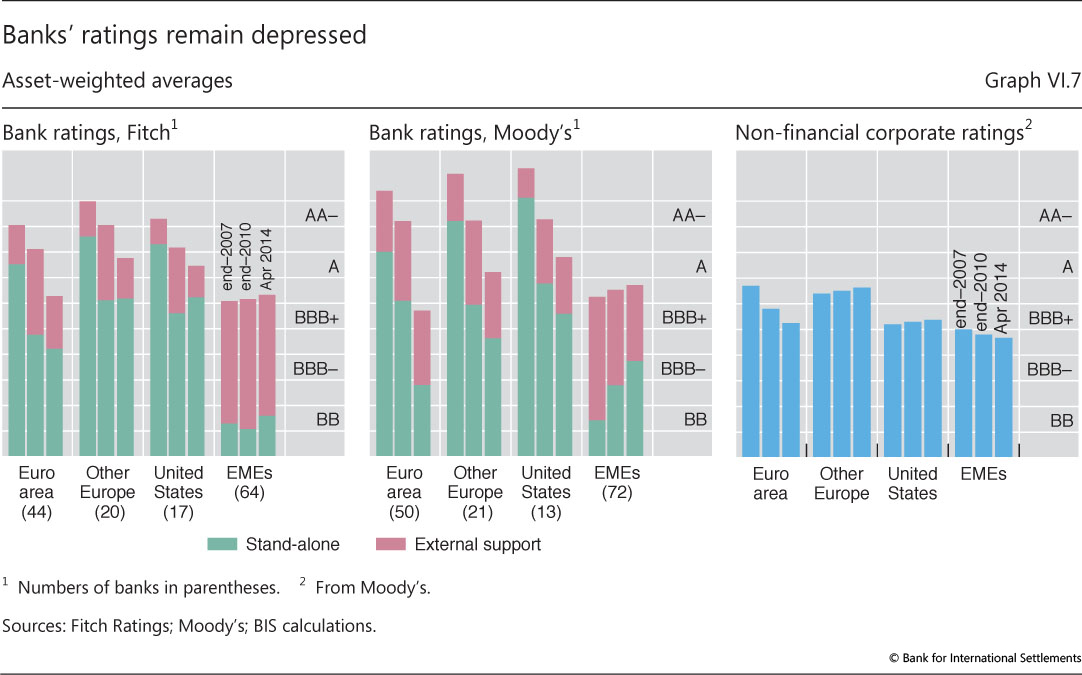

| VI.7 | Banks' ratings remain depressed | p 118 |

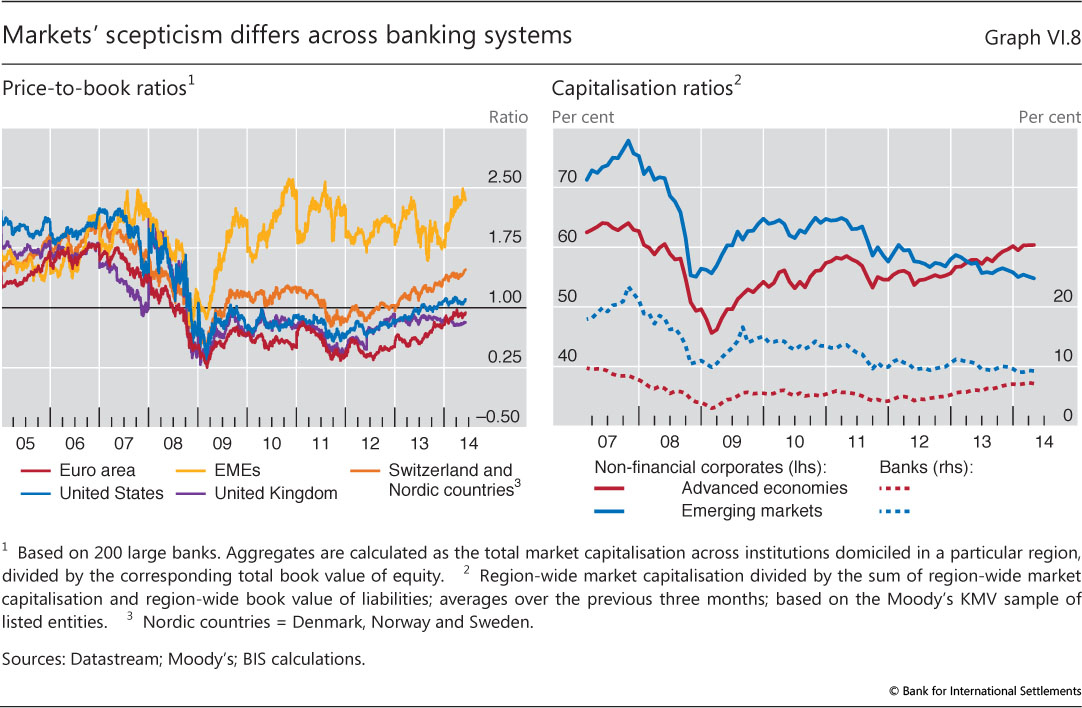

| VI.8 | Markets' scepticism differs across banking systems | p 118 |

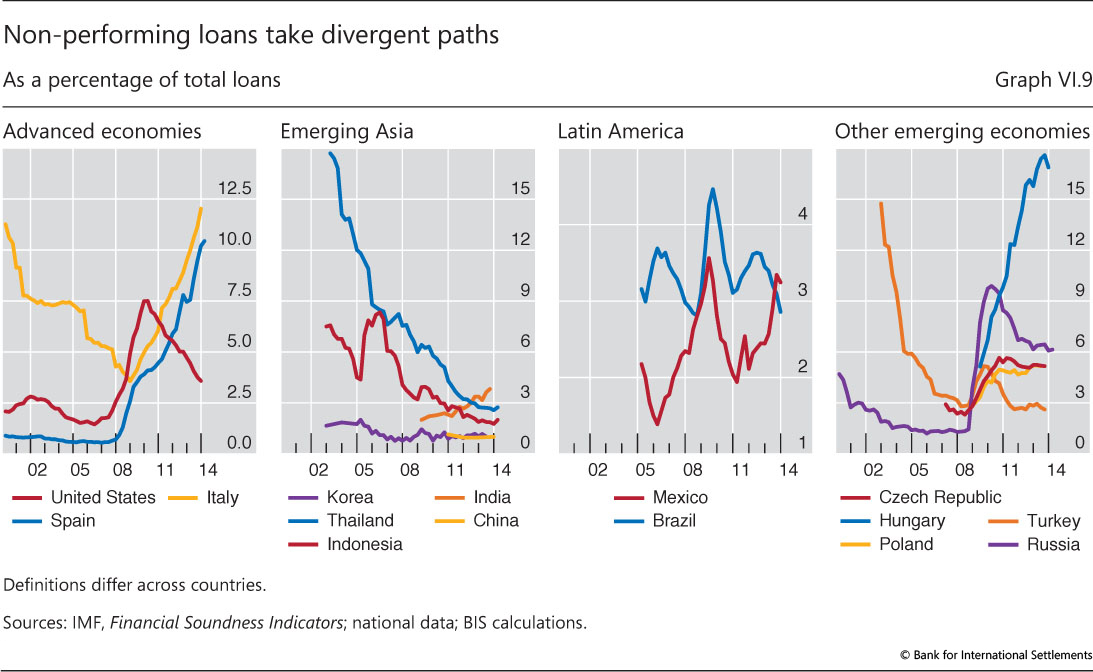

| VI.9 | Non-performing loans take divergent paths | p 119 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}