Post-Basel III: time for evaluation

Keynote address by Mr Pablo Hernández de Cos, Chairman of the Basel Committee on Banking Supervision and Governor of the Bank of Spain, at the 14th ASBA-BCBS-FSI High-level Meeting on Global and Regional Supervisory Priorities, Lima, 1 October 2019.

Introduction

Good morning, and welcome to the 14th high-level meeting jointly organised by the Association of Supervisors of Banks of the Americas, the Basel Committee and the Financial Stability Institute. Let me start by thanking our friends at the Superintendency of Banking, Insurance and Private Pension Funds of Peru for hosting this year's event. It is a pleasure to be in Lima.

The Basel Committee places great weight on its outreach programme with external stakeholders. Events organised by the FSI are a key channel for the Committee to engage directly with counterparts at central banks and supervisory authorities around the world to discuss financial stability issues with the aim of improving and strengthening their financial systems, and I am sure that this week's meeting will contribute to this objective.

As you probably know, the Committee's current work programme covers three broad themes: first, ensuring full, timely and consistent implementation of the Basel III reforms; second, assessing emerging risks and initiating targeted policy and supervisory developments; and third, evaluating and monitoring the impact of the post-crisis reforms.

Allow me to focus my initial remarks on this latter issue. Evaluating post-crisis reforms is one of the core safeguards to ensure that the Committee's work is guided by a medium-term perspective. But perhaps the goals and content of this evaluation work are not sufficiently known. So allow me to take this opportunity to describe this key component of our current work programme related to evaluating post-crisis reforms.

In addition, I will try to cover very briefly two of the topics included in today's agenda. First, one of our sessions will discuss coordination and cooperation among financial authorities, and I would like to comment on one aspect that affects the macro- and microprudential policy authorities. And, second, I will briefly comment on the issue of proportionality, which is the focus of another session and is another topical issue on the Basel Committee's agenda.

Evaluation of post-crisis reforms: an imperative for standard-setting bodies

Before I get into the specifics of the Committee's work programme on the evaluation of post-crisis reforms, I think it is helpful to take a step back and remind ourselves why the Committee is conducting these evaluations.

Let me start by emphasising what we are not doing: we are not re-opening previously agreed standards, rolling back or watering down reforms, or undertaking a "rubber stamping" exercise. Rather, this is a genuine, evidence-based analysis of the reforms, their impact and their interactions.

Our evaluation work programme is motivated by three broad necessities.

First, it is an imperative for standard-setting bodies - and indeed, any policymaking body - to evaluate the impact and effectiveness of any measure or reform it introduces. This is an integral part of the policymaking process. It enhances the intellectual rigour of standard setting by providing an ex post appraisal of the degree of success in attaining a policy objective, which complements the range of ex ante assessments conducted during the design stage. And such evaluation strengthens the accountability and credibility of policymakers by providing a transparent judgment on the impact of their reforms.

Second, the evaluation of post-crisis reforms is not being conducted in a vacuum. We will actively encourage and seek input from a broad range of stakeholders. Indeed, this is consistent with our approach to designing standards, which was recently described as "one of the most procedurally sophisticated" processes.1

Third, the work on evaluating post-crisis reforms is agnostic to the outcome. Our sole requirement is that any inputs to the evaluation be based on rigorous empirical analyses. As a result, I remain open-minded about our findings and any potential policy responses. Indeed, there may be as much a case to pursue additional measures or to address regulatory gaps as there may be a need to fine-tune aspects of our post-crisis framework.

Framework for evaluating post-crisis reforms

The Basel Committee approved a work programme for evaluating its post-crisis reforms towards the end of 2017. The programme covers three types of evaluations:

- Whether individual reforms, or a subset of reforms, have achieved their intended objectives. For example, to what extent has a specific reform delivered its intended outcome of, say, enhancing risk sensitivity, or have a subset of reforms been effective in reducing excessive variability of banks' risk-weighted assets (RWAs)?

- An evaluation of the interaction and coherence across different reforms. For example, are different measures mutually reinforcing or conflicting? Do different measures treat similar risks in a similar way? In principle, these could also include cross-sectoral interactions, ie interactions between the Committee's reforms and other post-crisis reforms.

- An assessment of any broader impact of the Committee's reforms, in aggregate or for a subset of reforms. For example, are there any structural impacts arising from the reforms? To what extent are these impacts desirable or undesirable?

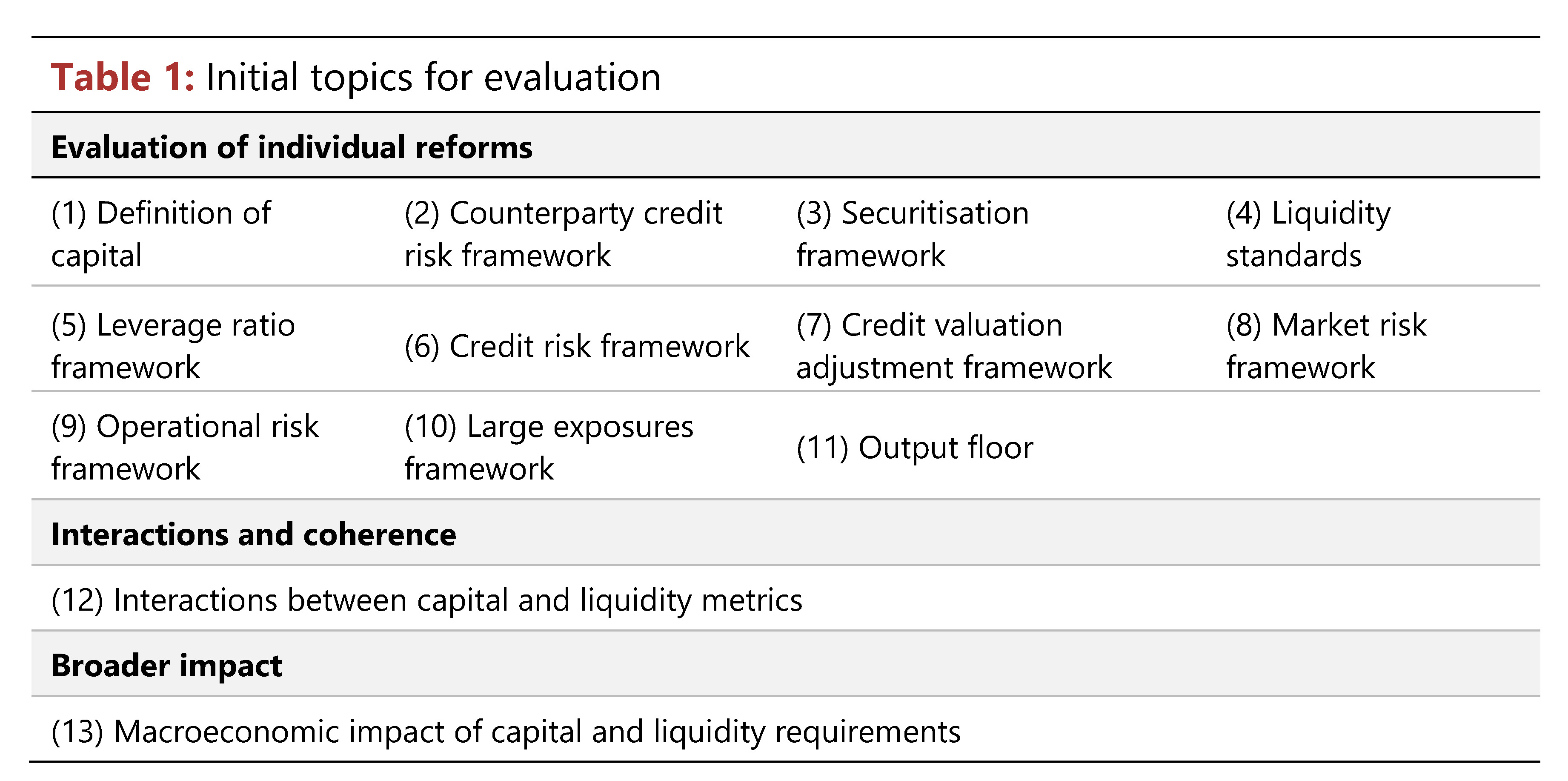

The Committee also agreed to an initial set of evaluations which relate to all three of these cases (Table 1). In addition, it is actively involved in cross-sectoral thematic evaluations alongside other standard-setting bodies and international forums such as the Financial Stability Board. This has included evaluations related to the effects of reforms on: (i) incentives to centrally clear over-the-counter derivatives; and (ii) infrastructure finance; while evaluations are ongoing in relation to (iii) small and medium-sized enterprise (SME) financing; and (iv) ending "too big to fail".2

An important feature of the Committee's evaluation work programme is its ex post nature. Put simply, we cannot fully evaluate the extent to which our standards have achieved their objectives until they are implemented. So our work on evaluating post-crisis reforms should not be seen as a reason to delay the implementation of Basel III among member jurisdictions. More than ever, it is important that Committee members adhere to the G20 Leaders' continued commitment for full, timely and consistent implementation of Basel III.

Given this ex post nature, our evaluation work programme is a multi-year initiative. For some of the topics - such as the Basel III definition of capital - the standards have been implemented and so our evaluation work is well under way. In other instances, such as the more recent Basel III standards - with an implementation date of January 2022, or January 2027 for some aspects of the framework - we are currently conducting preparatory analysis, including the design of our evaluation methodologies and the required data to support our empirical analysis.

There will be plenty of opportunities for the Committee to provide additional information on its evaluations as the work progresses. And we will be actively seeking input from all stakeholders to assist us.

Let me now briefly turn to the agenda for our high-level meeting this week, which includes a number of topics that could also benefit from additional analysis. I would like to offer a few personal reflections on a couple of them.

Macro- and microprudential policy: two sides of the same coin?

One of our sessions will cover coordination and cooperation among financial authorities, including the interactions between macro- and microprudential policy. During the session we will have the opportunity to discuss institutional and cooperation arrangements among different authorities, but let me say a few words about some of the potential dynamics of macro- and microprudential policy in the Basel Framework.

One of the most important elements of Basel III is the introduction of macroprudential instruments. These instruments seek to reduce the build-up of aggregate credit imbalances (eg the countercyclical capital buffer) and to ensure that loss-absorbing resources match the systemic risk profile of banks (eg the buffers for systemically important banks). They build on, and complement, the microprudential framework in Basel III.

A common feature of the Basel III macroprudential instruments is that they take the form of buffers: an additional layer of loss-absorbing resources above the regulatory minimum. Banks operating at levels below the buffers are subject to automatic restrictions on capital distributions, such as dividends and bonuses. When the restrictions are in effect, they limit the proportion of earnings that may be paid out.

The rationale for designing the macroprudential instruments as buffers is threefold. First, it gives banks flexibility to absorb losses in times of stress, thus enhancing their resilience. Second, it mitigates negative macroprudential externalities (eg related to fire sales or deleveraging). And third, it prevents imprudent depletion of capital resources, by setting constraints on the amount of capital distributions.

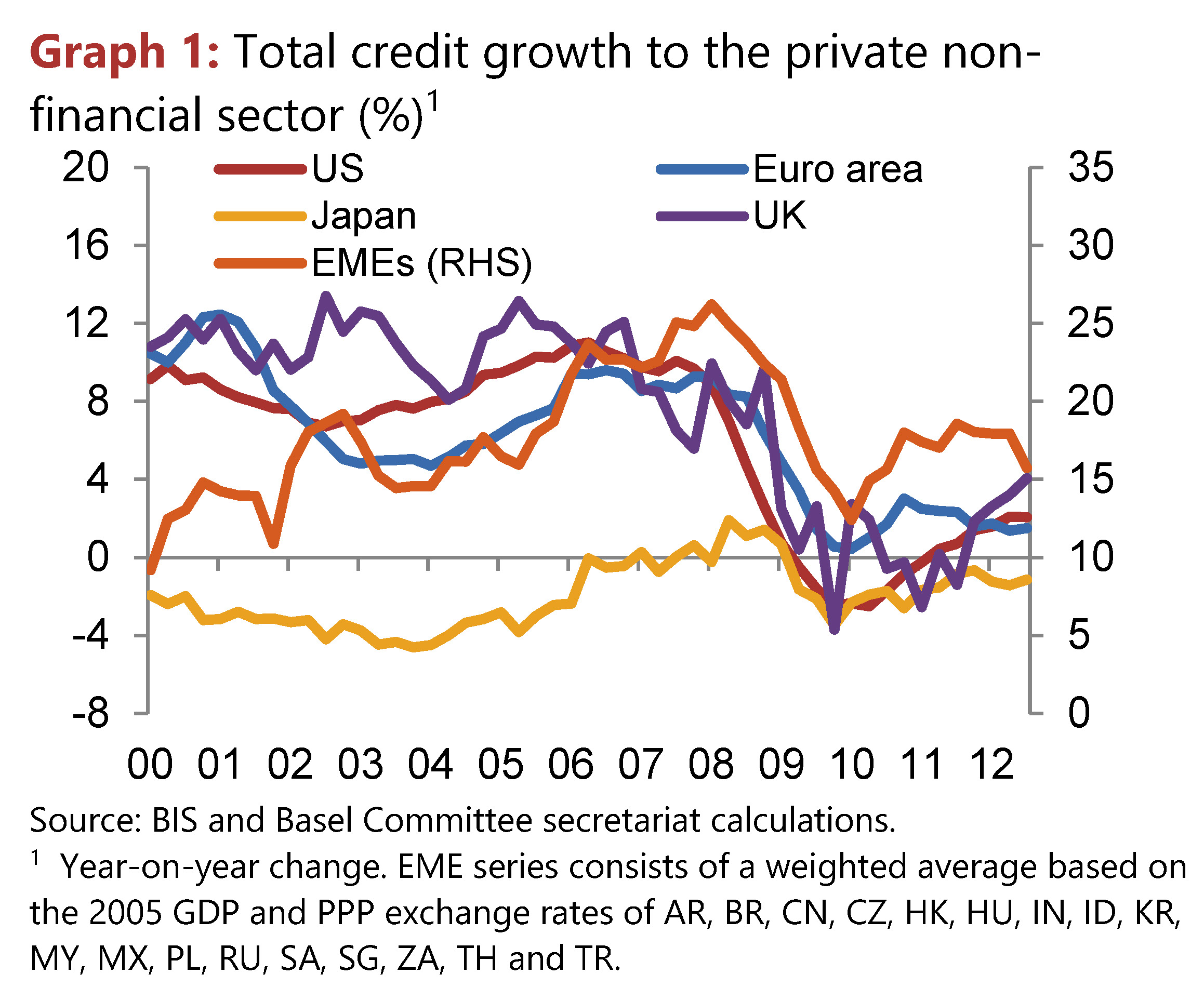

These interrelated objectives seek to directly address the outcome experienced during the Great Financial Crisis. Banks sharply cut back their lending to the real economy (Graph 1) due to a number of factors, one of which could have been to avoid breaching their capital requirements (although other factors, such as weak loan demand and funding difficulties, also played an important role). The incentive to deleverage should arguably be less pronounced in a situation where banks have a usable extra layer of capital resources - in the form of buffers - above minimum requirements.

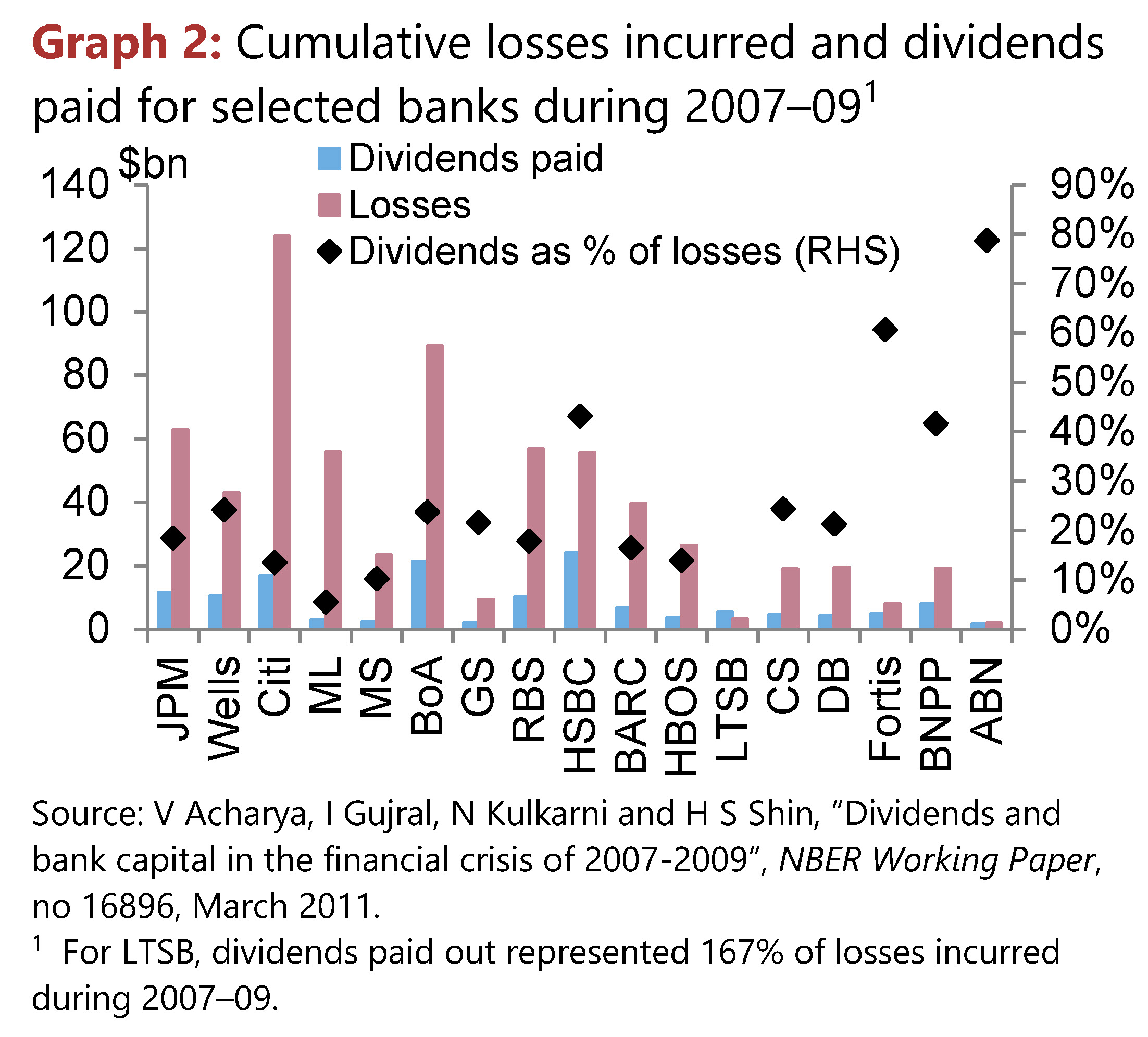

At the same time, some banks that incurred losses during the Great Financial Crisis continued to pay out dividends and even bonuses, with some of these payments increasing relative to the pre-crisis period (Graph 2). The automatic distribution restrictions in the buffer framework seek to prevent the imprudent outlay of capital resources and ensure that banks rebuild their capital strength in a timely and organic manner.

But will these macroprudential buffers operate as intended in practice, or could there be tensions between the macroprudential and microprudential objectives of the Basel Framework? These buffers have been largely untested in practice, especially in time of systemic stress, so it is not possible to provide a definitive answer at this stage.

However, one could envisage examples of potential conflicts between macro- and microprudential policy. For example, at a turning point in the credit cycle, the macroprudential perspective could call for distressed banks to draw down their capital buffers to absorb losses without abruptly cutting back on lending to the real economy. At the same time, the microprudential perspective may be more concerned with the resilience of distressed banks and the need for such banks to shore up their capital buffers. Both perspectives are understandable and legitimate, and highlight the importance of jurisdictions coordinating their macro- and microprudential policy regardless of their institutional setup.

More generally, the usability of capital buffers may also depend on the way in which banks perceive or anticipate any market reaction to a buffer drawdown. This also highlights the importance of an effective and coordinated communication strategy by macro- and microprudential authorities.

The Basel Committee will continue to monitor such developments and provide a forum for members to exchange their experiences in coordinating macro- and microprudential policy.

Proportionality and the Basel Framework

Another session for our meeting this week discusses the role of proportionality, which is another topical issue on the Basel Committee's agenda.

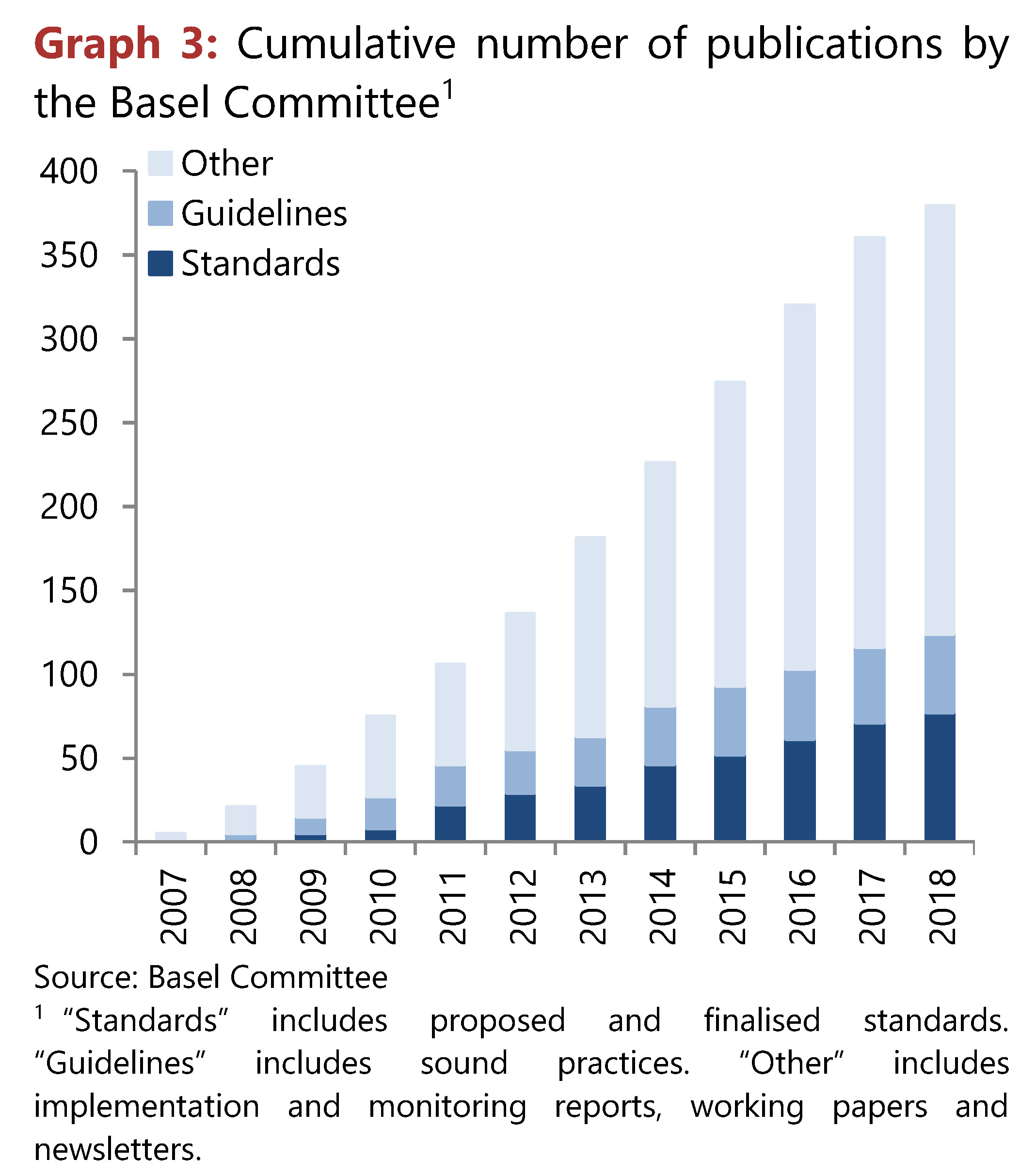

Over the past decade, the Committee has pursued a comprehensive and wide-ranging set of post-crisis reforms. While these reforms have strengthened the resilience of banks and enhanced global financial stability, they have also resulted in an increasingly voluminous and complex framework (Graph 3). This, in turn, could pose challenges for some banks and supervisory authorities in implementing and overseeing the Basel Framework. And it has raised questions about adequately balancing simplicity, comparability and risk sensitivity.

As you know, the Basel Framework is expected to be implemented in by Basel Committee member jurisdictions for internationally active banks. But the Core Principles for Effective Banking Supervision - which are relevant for all banks and jurisdictions around the world - embed the role of proportionality, including that "supervisory practices should be commensurate with the risk profile and systemic importance of the banks being supervised".

But the Committee also recognises that non-Committee jurisdictions may wish to implement some or all of the Basel III framework for a number of reasons. For example, they may wish to comply with the latest global banking standards which address fault lines in previous regulatory frameworks. In some instances, stakeholders such as market participants or credit rating agencies may also call for jurisdictions to implement the latest global standards.

The Committee recently conducted a stocktake of proportionality measures in place across jurisdictions, which highlighted that a majority of jurisdictions apply such measures.3

Yet how easy is it for such jurisdictions to implement Basel III in practice? On the one hand, the Basel Framework includes a number of standardised approaches in addition to internally modelled approaches. The former are in principle meant to be simpler to operate and implement than the latter, with both sets of approaches deemed to be equally acceptable options.

On the other hand, are the standardised approaches simple enough to be used in a proportionate regime for non-Basel Committee member jurisdictions? Or are there instances where some of the standardised approaches are too complex for both banks and supervisors to implement and oversee? This is a genuinely open question, and I look forward to hearing your views on this matter.

Conclusion

In conclusion, the Basel Committee will be devoting a substantive part of its agenda over the next few years to carefully evaluating the impact and effectiveness of its post-crisis reforms. This work will be grounded in rigorous empirical analysis, and will require the full implementation of our standards in order to arrive at an accurate assessment. We will be actively seeking stakeholders' views to support us in this work, and I am certain that our high-level meeting this week will serve as an important input.

1 A Viterbo, "The European Union in the transnational financial regulatory arena: the case of the Basel Committee on Banking Supervision", Journal of International Economic Law, vol 1, no 24, June 2019.

2 See the final evaluation reports on the incentives to centrally clear over-the-counter derivatives and on infrastructure finance; the consultation paper on SME financing, and the terms of reference for the evaluation of too-big-to-fail reforms.

3 Basel Committee on Banking Supervision (2019): "Proportionality in bank regulation and supervision - a survey on current practices", March.