Philip N Jefferson: Is this time different? Recent monetary policy cycles in retrospect

Speech by Mr Philip N Jefferson, Vice Chair of the Board of Governors of the Federal Reserve System, at the Peterson Institute for International Economics, Washington DC, 22 February 2023.

Charts and figures to the speech

Thank you, Adam, and thank you to Peterson for the opportunity to speak to you today.

Before I begin, let me remind you that the views I will express today are my own and are not necessarily those of my colleagues in the Federal Reserve System.

I will take this opportunity to share with you my outlook on the U.S. economy and some upside and downside risks to which I am paying special attention. Also, I will review past monetary policy cycles and discuss what lessons we may learn from them. With that, let me turn to my outlook for the U.S. economy.

Aggregate Economic Activity

Growth in real gross domestic product in 2023 came in much higher than expected by most professional forecasters, buoyed by strength in consumer spending. Toward the end of 2023, however, household balance sheets began to weaken, as indicated by higher delinquency rates and a further decline in savings. These developments lead me to expect slower growth in spending and output in 2024. Even so, without a clear understanding of why consumer spending has been so resilient, I see continuing strength in spending as an important upside risk to my forecast. One possible explanation is that consumers do not want to give up previous levels of consumption, perhaps because of habit formation as described by Robert Pollak (1970) and an optimistic view of future income prospects. Another possibility is the one raised in pioneering work by James Duesenberry (1949) 75 years ago and later developed in the context of modern macroeconomics by Jordi Gali (1994). Socially motivated consumption-or "keeping up with the Joneses"-could cause individuals to consume more than what is predicted by models that only consider household wealth and income.

The Labor Market

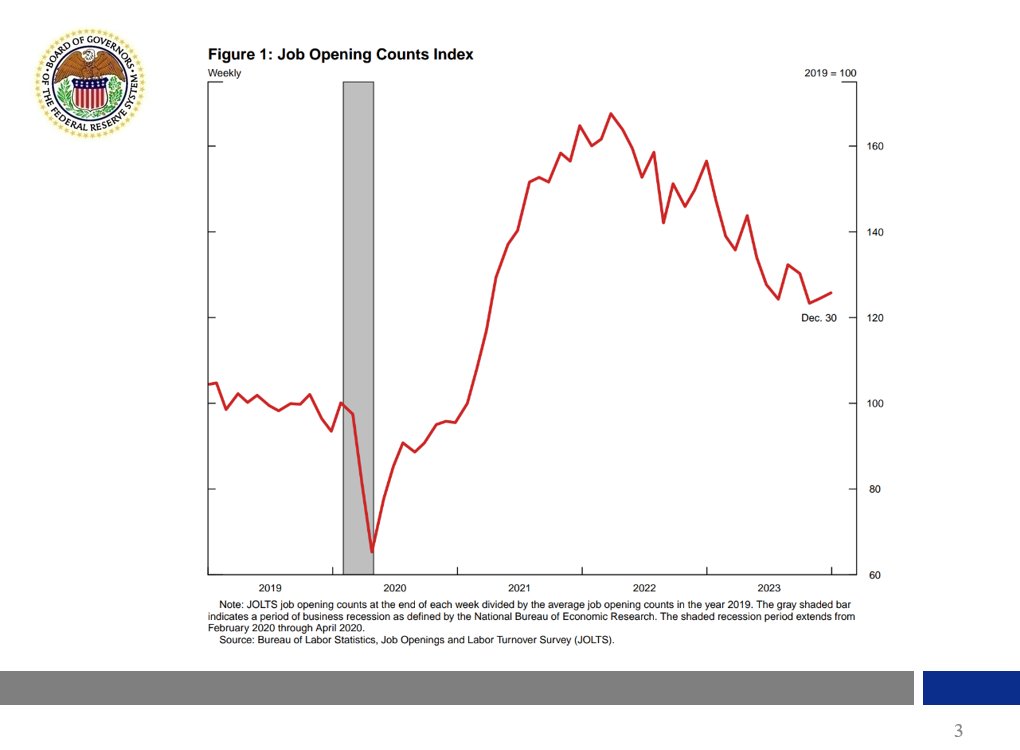

The imbalance between labor demand and labor supply has narrowed, as labor demand has cooled while labor supply has improved. There is evidence of cooling labor demand, such as the decline in job openings by 3 million from their peak in March 2022. Nevertheless, the labor market remains tight and job openings remain about 20 percent above their pre-pandemic level, as shown in figure 1. At the same time, layoffs have remained very low, and the pace of payroll employment gains remains strong, with nonfarm payroll monthly job gains in the past three months averaging 289,000. The unemployment rate in January was 3.7 percent, a level that is still near historical lows. The fact that the unemployment rate and layoffs have remained low in the U.S. economy over the past year amid disinflation suggests that there is a path to restoring price stability without the kind of substantial increase in unemployment that has often accompanied significant tightening cycles.

{kind=link}

The Inflation Outlook

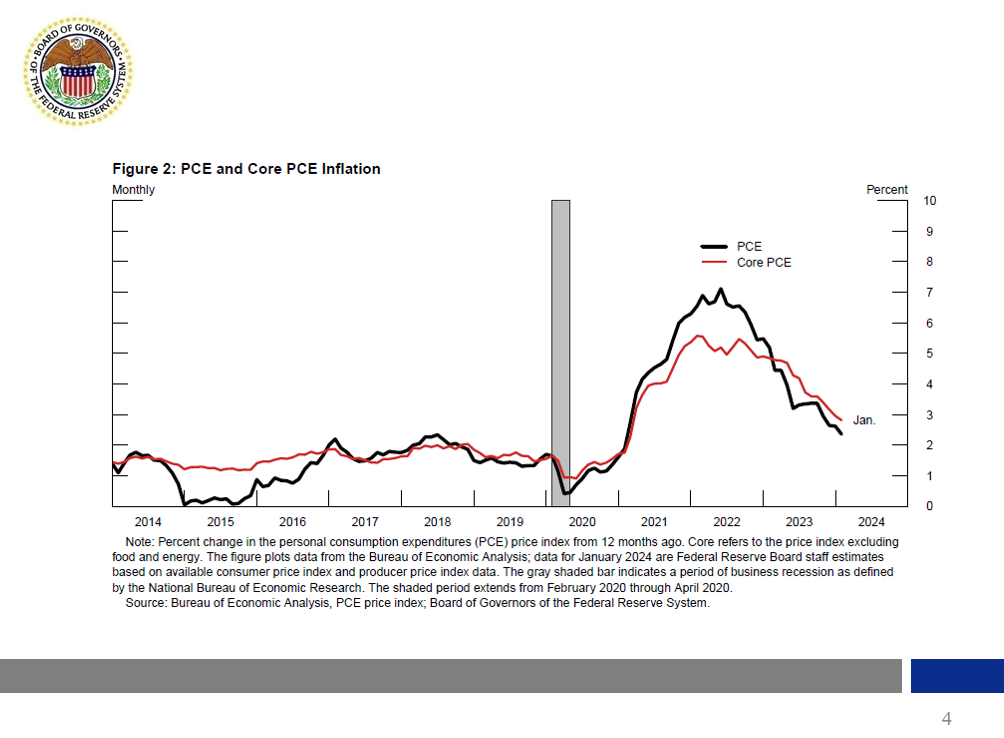

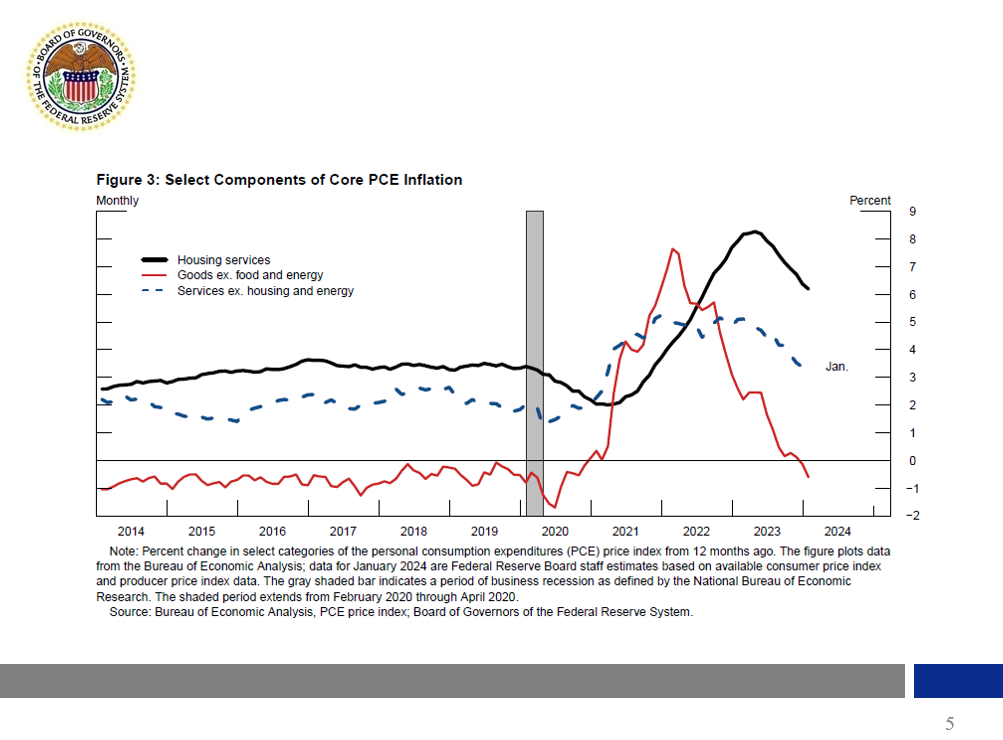

Inflation made clear progress over 2023 toward the Federal Open Market Committee's (FOMC) 2 percent inflation objective. I believe that this progress reflects both the unwinding of pandemic-related supply and demand distortions in the economy as well as restrictive monetary policy, which has cooled strong demand and given the supply side of the economy time to catch up. As shown in figure 2, over the 12 months ended in January, the Federal Reserve's staff estimates that total personal consumption expenditures (PCE) prices rose 2.4 percent, down from 5.5 percent over the preceding 12 months. Core PCE prices, which excludes energy and food prices, rose 2.8 percent, down from 4.9 percent. The figures for January are estimates that incorporate the somewhat larger consumer price index (CPI) increase we saw last month. That disappointing CPI reading highlights that the disinflation process is likely to be bumpy. The January data notwithstanding, the slowing in core inflation has been especially pronounced in recent months, as the 3- and 6-month changes in core PCE prices through January, at 2.5 percent and 2.4 percent, respectively, clearly remain below the 12-month change shown in figure 2. The most striking moderation has been in core goods prices, as shown in figure 3, which have declined outright over the past year. Inflation in core services, both in its housing component and nonhousing services, has also slowed, but not as much. I believe that as the labor market continues to cool, core services price increases will continue to moderate. Of course, I remain attentive to other possibilities.

{kind=link}

{kind=link}

A Longer-Term Perspective on Monetary Policy Cycles

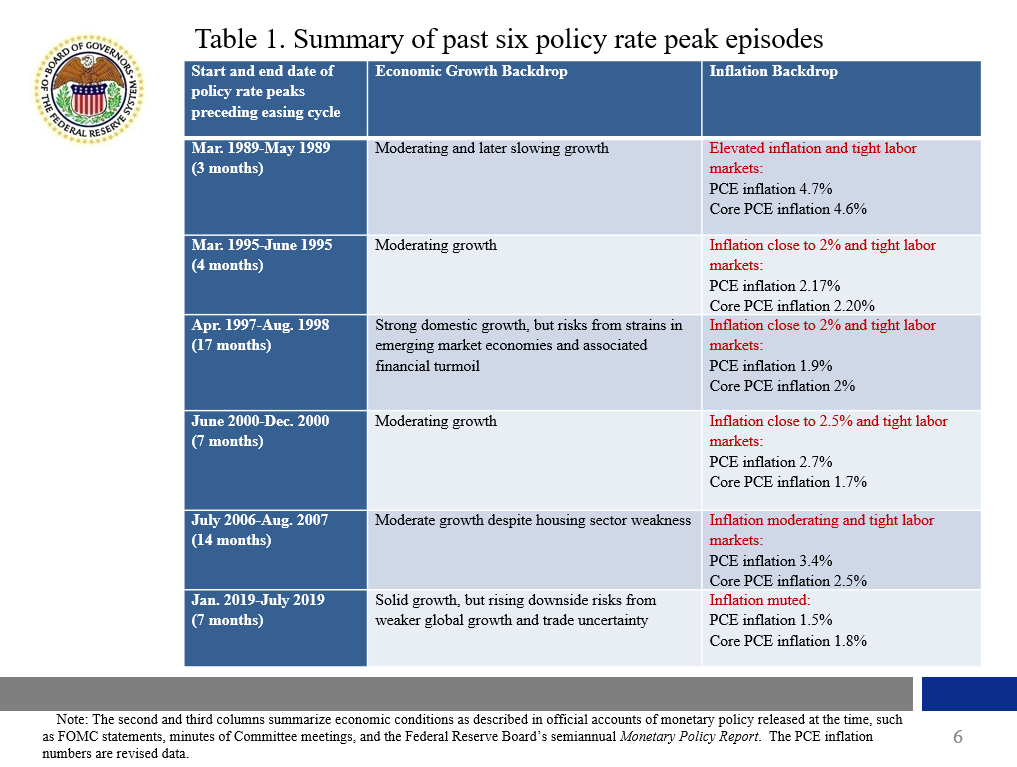

Next, I would like to highlight key aspects of past monetary policy cycles and what lessons we may learn from these past experiences. For exposition purposes, my review focuses on easing cycles and their preceding peak-rate episodes that extend back to 1989; however, I also will make some comments on an important episode prior to 1989.1 As of our last meeting in January, my colleagues on the FOMC and I believe that our policy rate is likely at its peak for this tightening cycle and that, if the economy evolves broadly as expected, it will likely be appropriate to begin dialing back policy restraint at some point this year. I will therefore start with a description of economic conditions during past peak-rate episodes, given where we are today.

The first column of table 1 lists the dates of the latest six peak-rate episodes preceding easing cycles, defined as a sequence of rate cuts without rate hikes in between. The second and third columns summarize economic conditions as described in official accounts of monetary policy released at the time, such as FOMC statements, minutes of Committee meetings, and the Federal Reserve Board's semiannual Monetary Policy Report. The table also records inflation at the time of the peak rate as measured by the 12-month percent change in headline and core PCE price indexes.2

{kind=link}

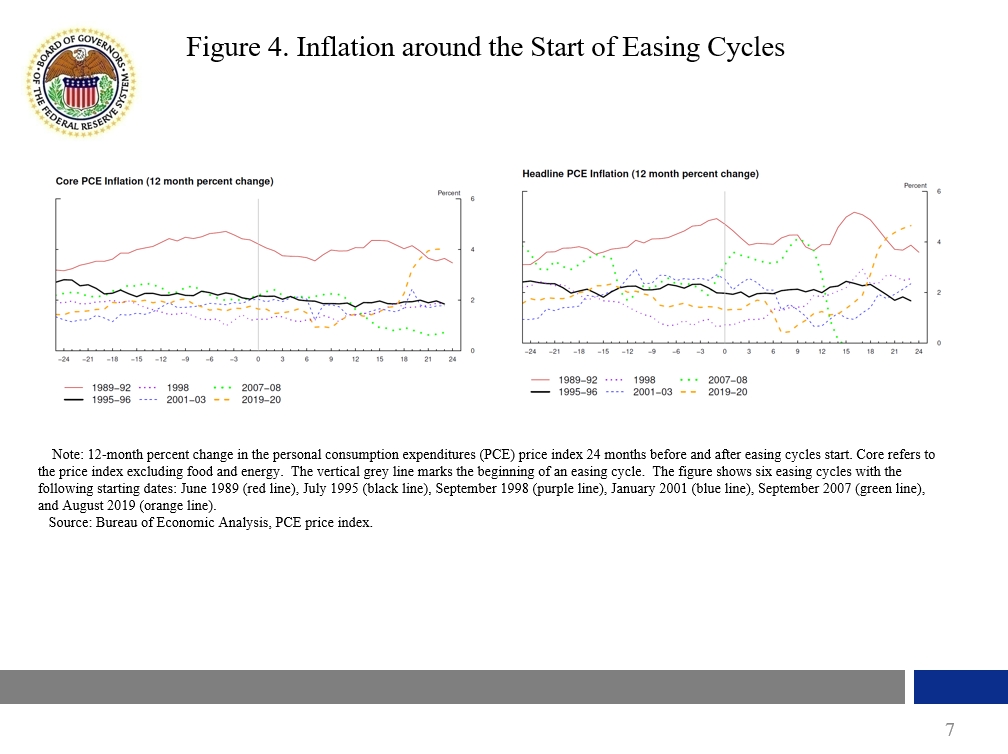

My main inference is that most of the time, in five out of the six episodes, the peak rate is reached once inflation is contained, albeit in some cases with risks still present. There is only one exception in this sample, the March 1989 to May 1989 peak-rate episode, when inflation was elevated-noted in the first row of the table. The easing cycle following this particular peak-rate episode began as core and headline PCE inflation were starting to come down from an elevated level, as illustrated in figure 4. 3 This figure shows headline and core inflation two years before and after the start date of each of the six easing cycles. The red line, which corresponds to the March 1989 peak-rate episode, stands out, with core PCE inflation at 4 percent at the beginning of the easing cycle, while all the other easing cycles show core PCE inflation at about 2 percent at commencement. Our situation today is closer to the norm during these episodes than to the exception, as PCE inflation is closer to 2 percent than to 4 percent.

{kind=link}

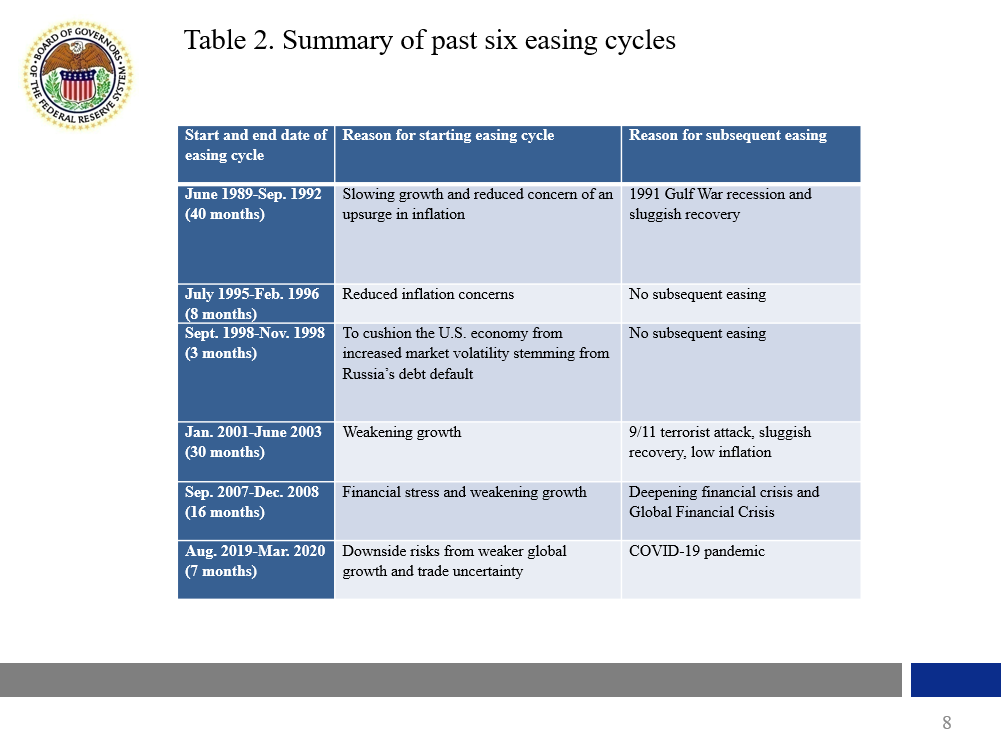

Table 2 summarizes the reasons given in Federal Reserve documents at the time to explain the rationale for easing policy. When studying monetary policy cycles, it is important to recognize the often-multistage nature of cycles and, because of this, table 2 distinguishes between the reasons underpinning the start of the easing cycle, listed in column 2, and those underpinning subsequent easings, listed in column 3. One clear example of a cycle with different phases and involving more than one reason for easing is the most recent easing cycle-the one listed in the last row-which took place between August 2019 and March 2020. The initial 75 basis points of easing in this cycle were a result of downside risks to the U.S. economy due to weaker global growth and high trade uncertainties. The subsequent easings in this cycle were due to the disruptions to the economy resulting from the COVID-19 pandemic.

{kind=link}

Looking at table 2, two facts stand out. First, most easing cycles start because of concern about slowing economic growth. In table 2, the one exception is the easing cycle that started in July 1995 and is associated with what Alan Blinder (2023) has labeled a "perfect soft landing" example.4 That particular easing cycle started predominantly because of reduced inflation concerns. All the other easing cycles started because either there was a concern about slowing economic growth, or, in one case, because there was a concern about slowing economic growth and there were reduced inflation concerns.

The second fact that stands out is that history is replete with events that complicate monetary policy decisions. The third column in table 2, which notes the reasons for subsequent easings, demonstrates this point. It shows that four out of the six easing cycles had multiple "easing phases," with later phases triggered by events like the 1991 Gulf War, the 9/11 terrorist attack, the Global Financial Crisis, and the pandemic. These events required policymakers to take a different course of policy easing from the course they may have anticipated earlier in the cycle. Specifically, because these events contributed to the contraction of economic activity, policymakers may have accelerated policy easing. The main messages that I see emerging from this review of the record are that policymakers need to remain vigilant and nimble, in case of adverse shocks hitting the economy, and that policymakers need some good luck.

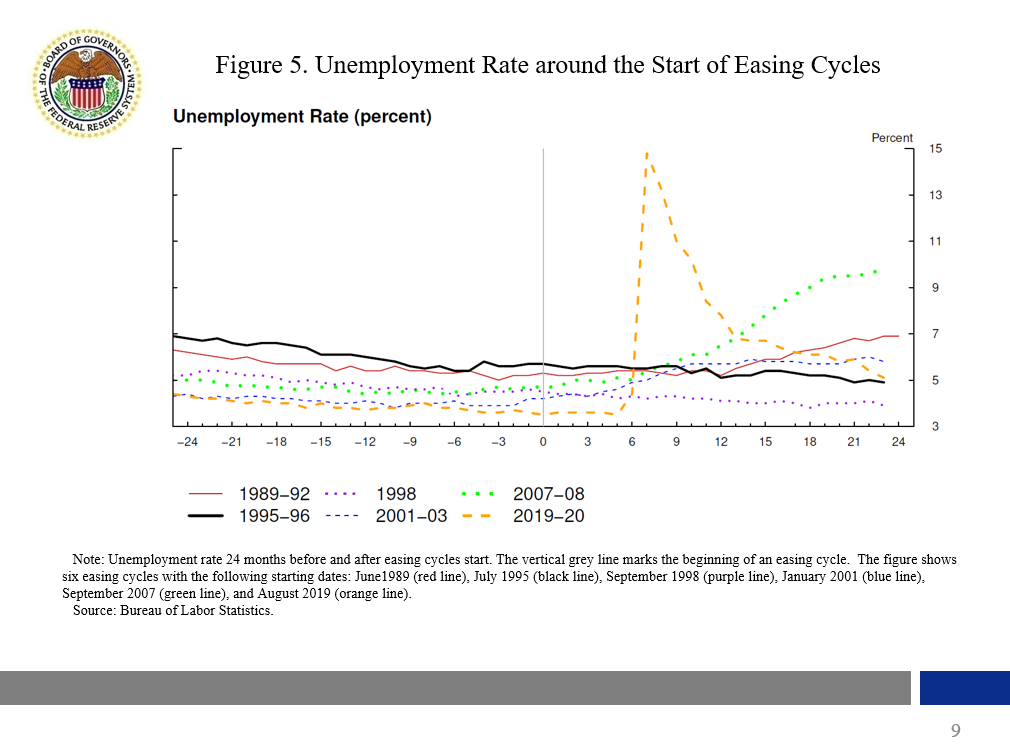

The lesson that policymakers need to remain vigilant and nimble is further illustrated in figure 5, which shows the unemployment rate around the start of each easing cycle. As can be seen from this chart, in some easing cycles-for example, the easing cycles that began in January 2001, shown in blue, and September 2007, shown in green-the unemployment rate ramps up quickly, shortly after the easing cycle began. In both these cases, the economy weakened rapidly.

{kind=link}

In the easing cycle that began in January 2001, moderating growth over the second half of 2000 gave way abruptly to sluggish growth around the end of the year. Economic weakness spread and intensified over the first half of 2001 and-as shown by the blue line-a year after the easing cycle began, the unemployment rate had increased just short of 2 percentage points.

In the easing cycle that began in September 2007, the macroeconomic data were not showing much weakening at the time of the cycle's first couple of rate cuts, although financial markets were exhibiting heightened and broad-based volatility and short-term funding markets were significantly impaired. It was only in December 2007 that incoming data started to show more significant spillovers of the housing downturn to other parts of the economy, while several financial firms also began to report larger-than-expected losses. As the green line in the chart shows, the unemployment rate was around 4-1/2 percent at the start of the 2007–08 easing cycle-having remained broadly stable around that level in 2006-but then rapidly rose to 6 percent within a year of the first easing. My motivation for discussing these two episodes is to highlight how quickly economic activity can weaken.

Another reason why policymakers need to watch all available information and be nimble in their decisionmaking is that developments concerning inflation can likewise change rapidly. This was highlighted recently by Russia's invasion of Ukraine in March 2022. The invasion compounded the effects of post-pandemic supply constraints on inflation. In addition, we always need to keep in mind the danger of easing too much in response to improvements in the inflation picture. Excessive easing can lead to a stalling or reversal in progress in restoring price stability. Former Fed Chair Paul Volcker stressed this danger in a 1981 speech, when he pointed to 1967 as a year when monetary policy eased in response to concerns about slowing economic growth and reduced inflation concerns, yet inflation subsequently turned back up.

Finally, another observation from reviewing past episodes is that careful easing in the July 1995 easing cycle allowed the FOMC to assess incoming data and other information to make sure that inflation was under control. As I noted earlier, the July 1995 easing cycle is associated with the so-called perfect soft landing. In this particular easing cycle, the FOMC started to ease as it observed a lessening in inflation concerns, left rates unchanged for three meetings as it waited for more information, and then continued to ease.

Lessons for Current Monetary Policy

With the knowledge of past experiences in hand, let me say a few words about the current monetary policy cycle and the extent to which future policy is likely to resemble, if at all, past experiences. Between March 2022 and July 2023, the FOMC raised the target range for the federal funds rate 5-1/4 percentage points. Our strong actions have moved our policy rate well into restrictive territory, and our restrictive stance of monetary policy is putting downward pressure on economic activity and inflation. If the economy evolves broadly as expected, it will likely be appropriate to begin dialing back our policy restraint later this year.

Getting back to the title of my talk today: Will this time be different? My answer is, of course it will. Every time is different. But we can still learn from past episodes. We cannot know if there will be unanticipated exogenous shocks that require a policy response different from what will be envisaged at the beginning of the easing cycle. All we can do is assess the risks as best we can, given the available information and our best forecasts. In the absence of unanticipated exogenous shocks, policymakers can weigh multiple factors, including keeping policy restrictive enough to tamp down a possible resurgence of inflation due to the strength of aggregate demand or easing sooner to avoid an undue increase in unemployment. Unfortunately, the history that I have reviewed today suggests that we should not be surprised if some kind of unanticipated shock occurs. Given that we must accept that uncertainty is present, we consider the risks that can affect our outlook and forecasts.

Looking ahead, I see at least three key risks. First, as I mentioned at the beginning, consumer spending could be even more resilient than I currently expect it to be, which could cause progress on inflation to stall. Second, employment could weaken as the factors supporting economic growth fade. Third, geopolitical risks could remain elevated, and a widening of the conflict in the Middle East could have greater effects on commodity prices, such as oil, and on global financial markets.

I remain cautiously optimistic about our progress on inflation, and I will be reviewing the totality of incoming data in assessing the economic outlook and the risks surrounding the outlook and in judging the appropriate future course of monetary policy.

References

Blinder, Alan S. (2023). "Landings, Soft and Hard: The Federal Reserve, 1965–2022," Journal of Economic Perspectives, vol. 37 (Winter), pp. 101–20.

Duesenberry, James S. (1949). Income, Saving, and the Theory of Consumption Behavior. Cambridge, Mass.: Harvard University Press.

Galí, Jordi (1994). "Keeping up with the Joneses: Consumption Externalities, Portfolio Choice, and Asset Prices," Journal of Money, Credit and Banking, vol. 26 (February), pp. 1–8.

Lindsey, David (2003). "A Modern History of FOMC Communication: 1975–2002 (PDF)," memorandum, Board of Governors of the Federal Reserve System, Division of Monetary Affairs, June 24.

Pollak, Robert, A. (1970). "Habit Formation and Dynamic Demand Functions," Journal of Political Economy, vol. 78 (4, part 1), pp. 745–63.

Stigum, Marcia, and Anthony Crescenzi (2007). Stigum's Money Market, 4th ed. McGraw-Hill.

Volcker, Paul (1981). "Dealing with Inflation: Obstacles and Opportunities," speech delivered at the Alfred M. Landon Lecture Series on Public Issues, Kansas State University, Manhattan, Kansas, April 15.

1 The start date of 1989 is motivated by the fact that this was the earliest cycle in which the FOMC was viewed as considering monetary policy actions in terms of discrete 25 basis point, 50 basis point, etc., rate moves in the federal funds rate target and, as such, is more comparable to today. See Stigum and Crescenzi (2007) for a discussion of the FOMC's increased focus on federal funds rate targeting in the late 1980s as well as Lindsey (2003), who describes the FOMC's further shift toward targeting the federal funds rate in 1989 by discontinuing the practice of targeting borrowed reserves.

2 The PCE inflation numbers in table 1 are revised data, which means the data that policymakers were reviewing at the time-the so-called real-time data-could have been different. In addition, for some of these cycles, policymakers focused on CPI inflation more than PCE inflation. Also, note that while the table frequently references inflation relative to a 2 percent rate, it was only for the last peak-rate episode for which the FOMC had established a 2 percent rate of inflation to be most consistent over the longer run with its price-stability goal, per its first "Statement on Longer-run Goals and Monetary Policy Strategy" adopted in January 2012.

3 The data shown in figure 4 are revised data.

4 Blinder (2023) labels the July 1995 episode as the "perfect soft landing" and identifies other "softish" landings (see his Table 1, page 119). Blinder (2023) defines a softish landing as an outcome in which real GDP declines by less than 1 percent or there is no NBER recession for at least a year after an FOMC tightening cycle.