Jerome H Powell: Inflation - progress and the path ahead

Speech by Mr Jerome H Powell, Chair of the Board of Governors of the Federal Reserve System, at "Structural Shifts in the Global Economy", an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming, 25 August 2023.

Good morning. At last year's Jackson Hole symposium, I delivered a brief, direct message. My remarks this year will be a bit longer, but the message is the same: It is the Fed's job to bring inflation down to our 2 percent goal, and we will do so. We have tightened policy significantly over the past year. Although inflation has moved down from its peak-a welcome development-it remains too high. We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

Today I will review our progress so far and discuss the outlook and the uncertainties we face as we pursue our dual mandate goals. I will conclude with a summary of what this means for policy. Given how far we have come, at upcoming meetings we are in a position to proceed carefully as we assess the incoming data and the evolving outlook and risks.

The Decline in Inflation So Far

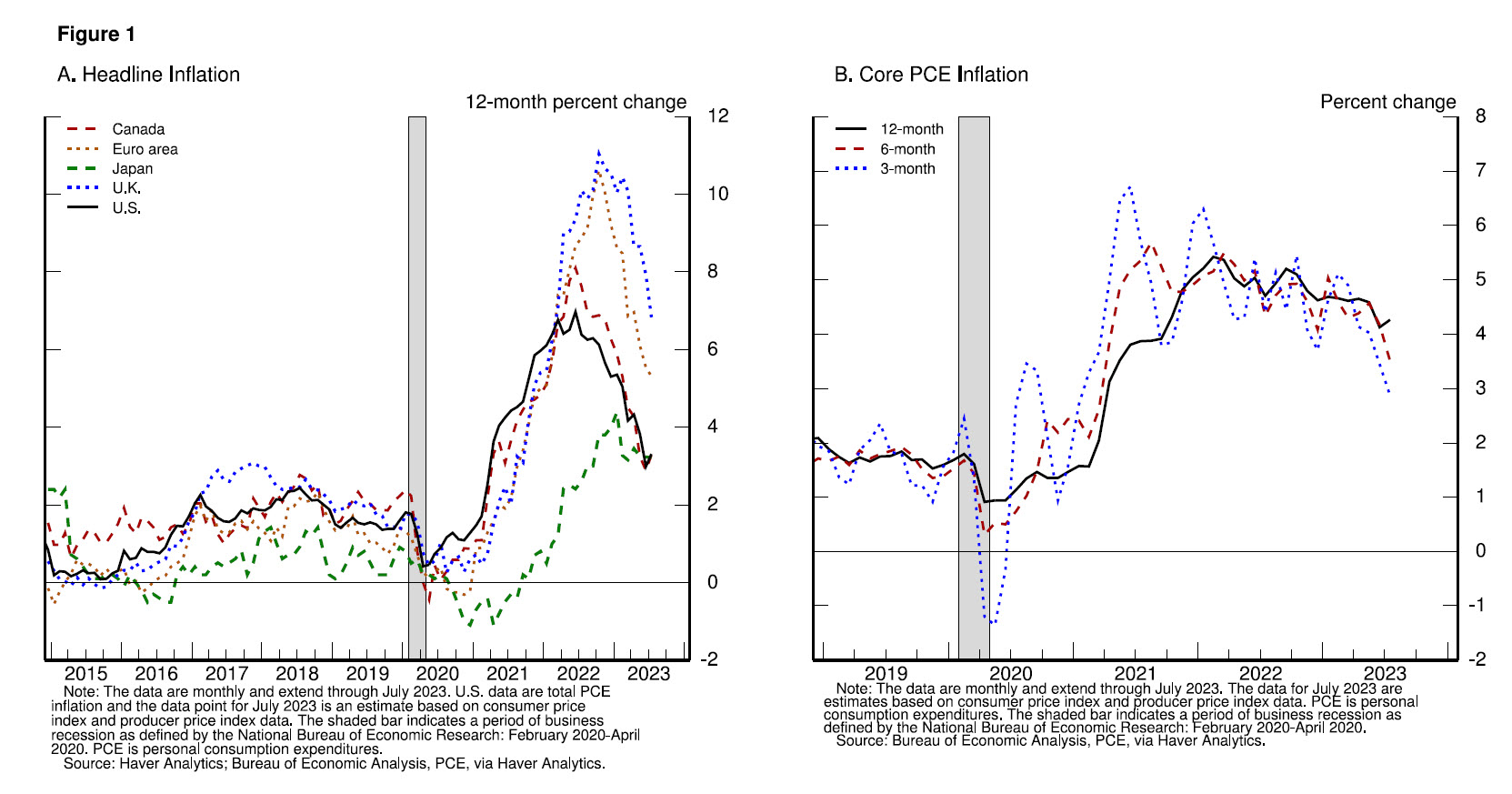

The ongoing episode of high inflation initially emerged from a collision between very strong demand and pandemic-constrained supply. By the time the Federal Open Market Committee raised the policy rate in March 2022, it was clear that bringing down inflation would depend on both the unwinding of the unprecedented pandemic-related demand and supply distortions and on our tightening of monetary policy, which would slow the growth of aggregate demand, allowing supply time to catch up. While these two forces are now working together to bring down inflation, the process still has a long way to go, even with the more favorable recent readings.

On a 12-month basis, U.S. total, or "headline," PCE (personal consumption expenditures) inflation peaked at 7 percent in June 2022 and declined to 3.3 percent as of July, following a trajectory roughly in line with global trends (figure 1, panel A).1 The effects of Russia's war against Ukraine have been a primary driver of the changes in headline inflation around the world since early 2022. Headline inflation is what households and businesses experience most directly, so this decline is very good news. But food and energy prices are influenced by global factors that remain volatile, and can provide a misleading signal of where inflation is headed. In my remaining comments, I will focus on core PCE inflation, which omits the food and energy components.

{kind=link}