Lael Brainard: What can we learn from the pandemic and the war about supply shocks, inflation, and monetary policy?

Speech by Ms Lael Brainard, Member of the Board of Governors of the Federal Reserve System, at the 21st BIS Annual Conference "Central banking after the pandemic: challenges ahead", Bank for International Settlements, Basel, 24 June 2022.

Accompanying charts of the speech

Policymakers and researchers have begun reassessing certain features of the economy and monetary policy in light of recent experience. After several decades in which supply was highly elastic and inflation was low and relatively stable, a series of supply shocks associated with the pandemic and Russia's war against Ukraine have contributed to high inflation, in combination with a very rapid recovery in demand. The experience with the pandemic and the war highlights the challenges for monetary policy in responding to a protracted series of adverse supply shocks. In addition, to the extent that the lower elasticity of supply we have seen recently could become more common due to challenges such as demographics, deglobalization, and climate change, it could herald a shift to an environment characterized by more volatile inflation compared with the preceding few decades.

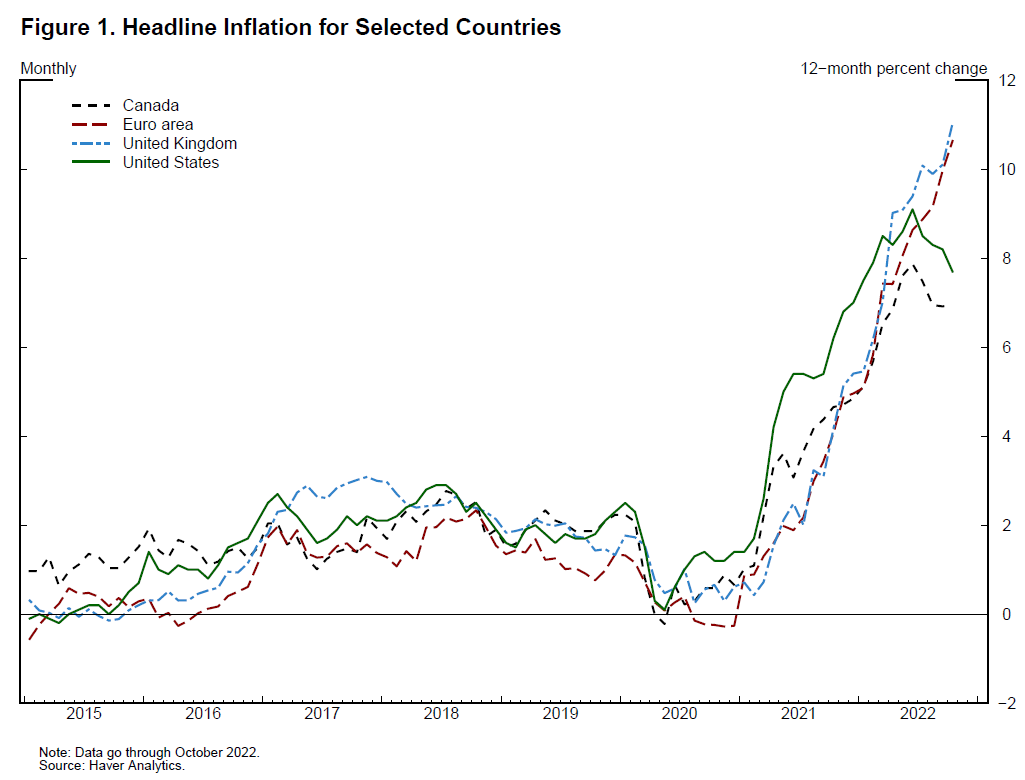

Inflation in the United States and many countries around the world is very high (figure 1). While both demand and supply are contributing to high inflation, it is the relative inelasticity of supply in key sectors that most clearly distinguishes the pandemic- and war-affected period of the past three years from the preceding 30 years of the Great Moderation. Interestingly, inflation is broadly higher throughout much of the global economy, and even jurisdictions that began raising rates forcefully in 2021 have not stemmed the global inflationary tide.

{kind=link}