Lael Brainard: Bringing inflation down

Speech by Ms Lael Brainard, Member of the Board of Governors of the Federal Reserve System, at the Clearing House and Bank Policy Institute 2022 Annual Conference, New York City, 7 September 2022.

Speech charts and figures can be found here.

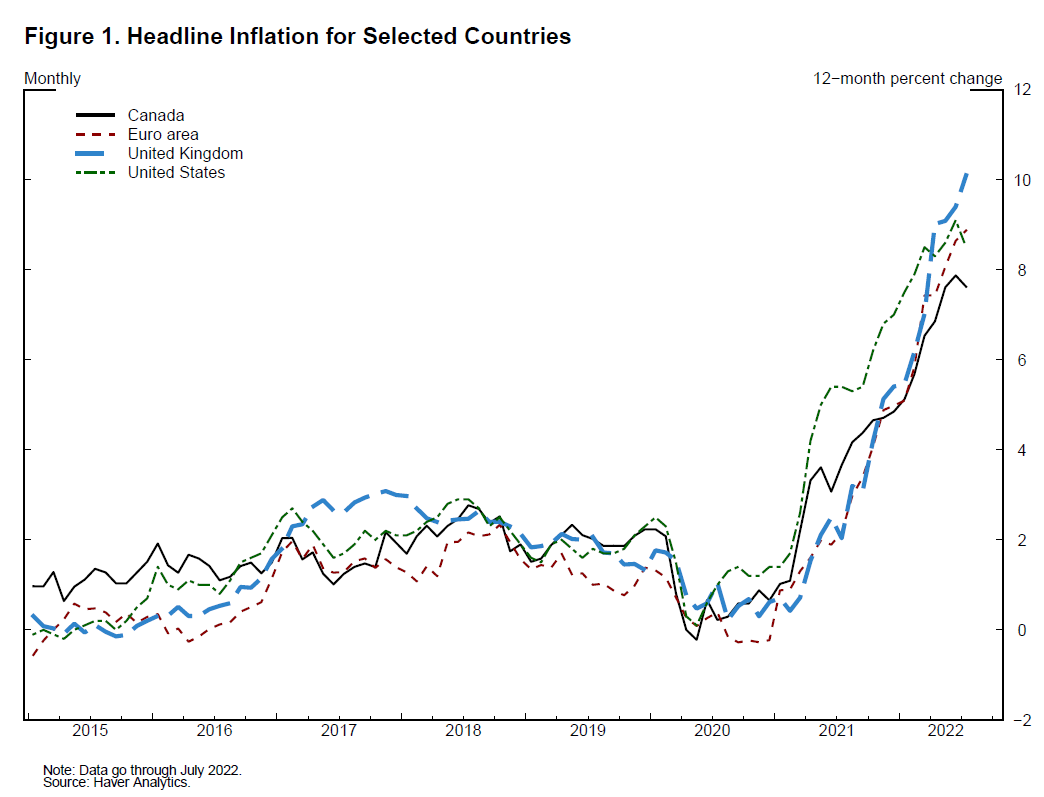

Over the past year, inflation has been very high in the United States and around the world (figure 1). High inflation imposes costs on all households, and especially low-income households. The multiple waves of the pandemic, combined with Russia's war against Ukraine, unleashed a series of supply shocks hitting goods, labor, and commodities that, in combination with strong demand, have contributed to ongoing high inflation. With a series of inflationary supply shocks, it is especially important to guard against the risk that households and businesses could start to expect inflation to remain above 2 percent in the longer run, which would make it much more challenging to bring inflation back down to our target. The Federal Reserve is taking action to keep inflation expectations anchored and bring inflation back to 2 percent over time.

{kind=link}

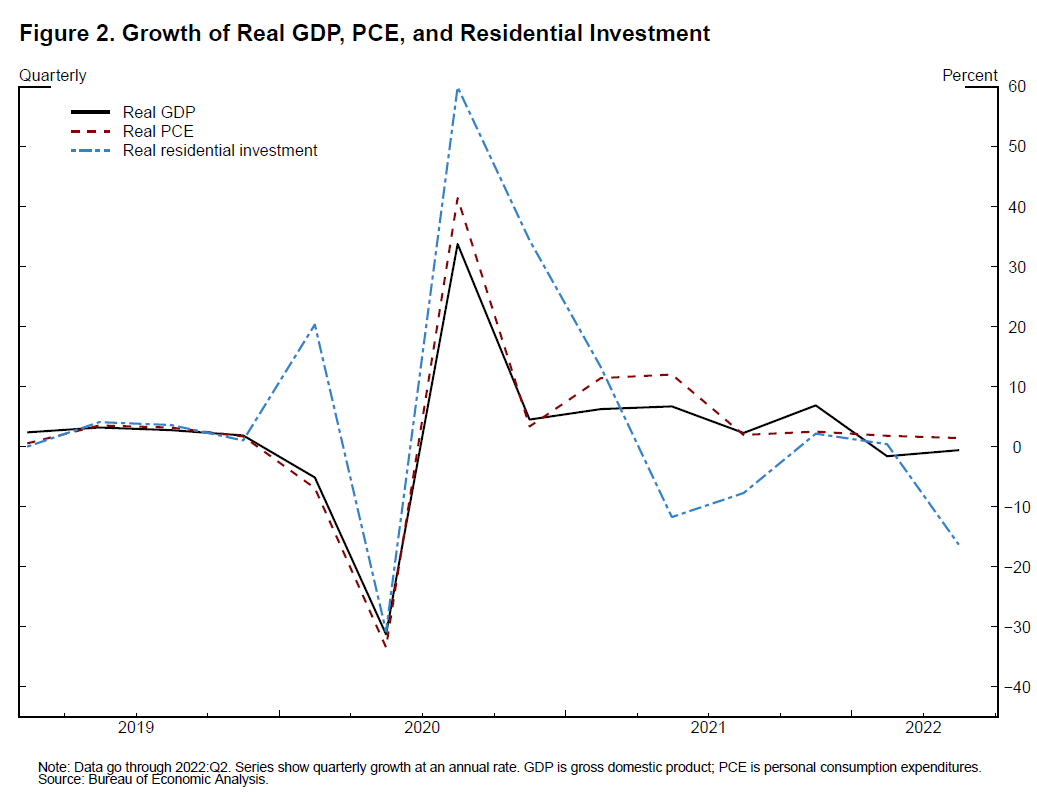

While last year's rapid pace of economic growth was boosted by accommodative fiscal and monetary policy as well as reopening, demand has moderated this year as those tailwinds have abated. A sizable fiscal drag on output growth alongside a sharp tightening in financial conditions has contributed to a slowing in activity. In the first half of 2022, real gross domestic product (GDP) declined outright, overall real consumer spending grew at just one-fourth of its 2021 pace, and residential investment, a particularly interest-sensitive sector, declined by 8 percent (figure 2).

{kind=link}

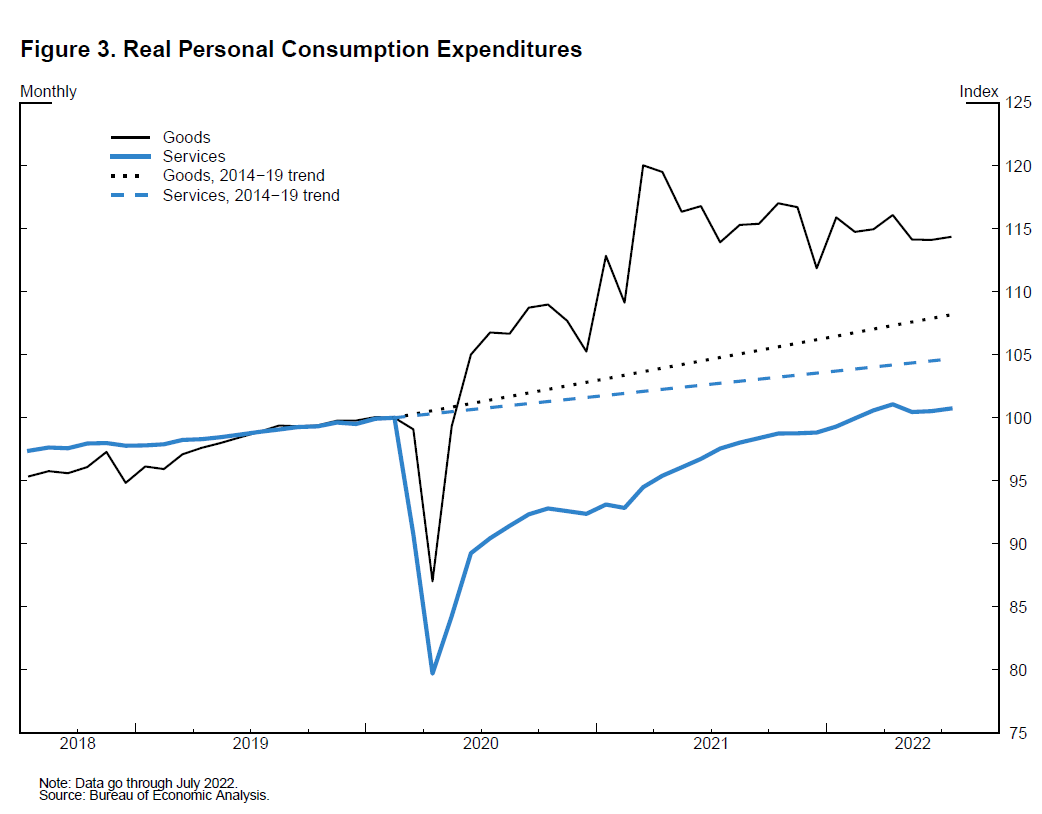

The concentration of strong consumer spending in supply-constrained sectors has contributed to high inflation. Consumer spending is in the midst of an ongoing but still incomplete rotation back toward pre-pandemic patterns. Real spending on goods has declined modestly in each of the past two quarters, while real spending on services has expanded at about half its 2021 growth rate. Even so, the level of goods spending remains 5 percent above the level implied by its pre-pandemic trend, while services spending remains 4 percent below its trend (figure 3).

{kind=link}