Christopher J Waller: A hopeless and imperative endeavor - lessons from the pandemic for economic forecasters

Speech by Mr Christopher J Waller, Member of the Board of Governors of the Federal Reserve System, at the Forecasters Club of New York, New York City, 17 December 2021.

Accompanying figures:https://www.bis.org/review/r211219b_figures.pdf

Thank you, Mike, for the introduction. It is a privilege for me to address fellow macroeconomic forecasters, and I thought an appropriate subject would be the challenge of forecasting during the pandemic.1 First, a few remarks about my outlook. Then I will discuss some lessons learned from the pandemic-lessons about the economy's response to this unprecedented event relative to what forecasters, including myself, first thought.

In light of November's job report, I believe the economy is closing in on maximum employment. Though job creation was lower than expected last month, the number indicated another solid increase in jobs. Accounting for retirees leaving the workforce, I estimate that employment is only about 1-1/2 million jobs below its February 2020 level, when monetary policy was less accommodative and unemployment was at a 50-year low and below Federal Open Market Committee (FOMC) participants' estimates of the longer-run unemployment rate. The unemployment rate dropped to 4.2 percent in November, just a touch above the median of FOMC participants' longer-run level of 4 percent. The economy seems to be on track to grow at an annual rate of 6 to 7 percent this quarter and by nearly that much in the first quarter of 2022.

Turning to inflation, it is alarmingly high, persistent, and has broadened to affect more categories of goods and services, compared with earlier this year. Wages are rising, and business contacts are reporting in the Fed's Beige Book that they are comfortable passing on increases in input costs to their customers. I have argued for some time that there are upside risks to inflation, and with inflation exceeding the FOMC's 2 percent target for some time now, I strongly supported the Committee's decision this week to speed up the pace of the tapering of asset purchases. This action gives us increased flexibility to adjust monetary policy as needed in 2022.

Assuming this new pace of reductions in our monthly asset purchases continues, the FOMC will end purchases in March. The appropriate timing for the first increase in the policy rate, of course, will depend on the evolution of economic activity, something that I will be closely monitoring. But given my expectations for inflation and labor market conditions, I believe an increase in the target range for the federal funds rate will be warranted shortly after our asset purchases end.

One big uncertainty about this outlook, of course, is the Omicron variant. We still don't know how serious a public health threat it will be, so we don't know if it will slow the U.S. economy, as the Delta variant briefly did, or even possibly slow progress toward maximum employment. Cutting the other way, we also do not know if Omicron will exacerbate labor and goods supply shortages and add inflation pressure, derailing the moderation of inflation next year that is my baseline. Over the past couple of years, forecasters have gotten pretty used to sudden changes in the outlook, and my colleagues and I on the FOMC will adjust as needed.

The Perils of Forecasting

As I am speaking to the Forecasters Club of New York, I thought I would pontificate a bit on the nature of the forecasting business. Forecasting typically involves answering the following question: Given the data we see today, what will be the value of some variable, such as gross domestic product (GDP), some period into the future? If the only metric of success is the accuracy of the forecast, then one should use a purely statistical model that looks for the variables that have the best predictive power. In this world, no one asks why those variables have predictive power-they just do.

But that is not the only thing that a forecaster's clients want-they also want an explanation for why you are making this forecast. Using a recent example, in May 2021 inflation readings were over 4 percent. If your statistical model predicted that inflation would fall to 2 percent by the end of 2021, you would be asked why you are making that prediction. To answer this question, you need an economic model. But by resorting to an economic model, which is an abstract representation of the true economy, you are potentially making a tradeoff between the statistical accuracy of the forecast and the logic of an abstract economic model to explain that forecast.

On top of that, you must resort to a stochastic economic model, where future states of the world occur with probabilities of less than one. So not only do you need to specify future states of the world from an economic model, you also need to specify the probability for each possible state of the world. Unfortunately, God does not hand us the probability distribution for future states of the world, so we must come up with that on our own. We do that by looking at history and trying to tease out empirical estimates of those probabilities, hoping that history is a good guide to what will happen in the future. But one thing that history makes clear is that past behavior is not always a good predictor of future behavior. Thus, to forecast well, one needs a good economic model, knowledge about future states of the world, and an accurate probability distribution over those future conditions. Even if we believe we have all of these elements in our forecasting toolbox, we still face the daunting task of forecasting turning points and judging the effect of unusual shocks.

As a result, economic forecasting is a pretty hopeless endeavor. So why do we do it? Because of how much is riding on the outcome. All economic activity-every one of the billions of economic decisions that will be made today, and every day-is guided by a view of the future. It is based on assumptions about economic conditions down the line. If the view is that conditions will be prosperous, consumers will be more likely to buy that new, bigger TV, and business owners will be more likely to expand and hire. But if their views are that conditions will get worse, they will be more likely to save than spend. Without a set of beliefs about the future, no one would be able to decide to spend or invest. The cumulative effect of all those decisions determines whether the economy grows or contracts, whether a business thrives or fails, and whether families can pay their bills.

So, fully aware of the dismal prospects of getting a forecast right, we soldier on, in pursuit of the scintilla of understanding it may provide about a future that everyone is interested in. It is often said that, based on our performance, economic forecasters need to approach this work with humility, but I think it is exactly the opposite. It takes bravado and some chutzpah to stand up and express confidence in an economic forecast that will almost certainly be wrong. But we do it and take the hits when we are wrong, because so much depends on that view of where the economy is headed. Now, let us look at the forecasting community's performance over the past couple of years.

Two Years of COVID-19

It has been almost exactly two years since reports began to circulate of a novel virus in Wuhan, China. In March 2020, health experts in the United States and elsewhere were recommending social distancing, avoiding crowded public places, and maintaining at least six feet of distance from other people. At that time, many economies, and eventually much of the United States, instituted lockdowns that kept school kids and nonessential employees at home. The effect was a sudden and severe drop in economic activity and significant stress in the financial system, including a significant disruption in Treasury markets.

Unlike other severe economic shocks in the past century, such as the Global Financial Crisis (GFC), the COVID crisis was a health emergency. The response was a planned shutdown of key sectors of the U.S. economy-something that had never been done before. Obviously, the pandemic has been a great hardship for many people, and it was very challenging for anyone trying to forecast the effect of the virus on the economy. While we all knew that a recession was in the cards, forecasters lacked the historical analog to give us an idea of the severity of the recession. To say there was massive uncertainty in predicting the effect of the virus is an understatement.

While shutdowns and lockdowns were more severe in March and April 2020 in some parts of the country than in others, most of the country was affected, and the drop in employment and spending was larger and faster than the United States had ever experienced. Twenty-two million jobs were lost in March and April. The unemployment rate more than quadrupled from a 50-year low of 3.5 percent in February to 14.8 percent in April. Real GDP fell at an annualized rate of 31 percent in the second quarter of 2020, which was three times faster than ever recorded.2

Before the start of the pandemic, the top and bottom 10 respondents of the Blue Chip survey (meaning those with the highest and lowest forecasts) had an average forecast for 2020 GDP growth of 1.5 percent and 2.2 percent, respectively, which is a very tight range. Once the pandemic started, this range exploded, with GDP growth forecasts ranging from negative 1.1 to negative 7.4 percent. Pre-pandemic forecasts for the 2020:Q4 unemployment rate ranged from 3.2 to 4 percent. In April 2020, the forecast for the Q4 unemployment rate ranged from 5.4 to 13.7 percent. It is clear from these disparate forecasts that there was tremendous uncertainty regarding the future states of the world and the probabilities associated with those states of the world occurring, which impaired the effort to model that future.

Just as we lacked the background and experience to forecast the negative effects of the pandemic, we also lacked the experience to understand the extraordinary rebound that followed. GDP grew at a 33 percent annualized rate in the second quarter. Half of the jobs lost were regained in four months, and in seven months the unemployment rate had fallen to 6.7 percent. By comparison, after the GFC, it took more than two years to regain half of the jobs lost and more than four years to return unemployment to 6.7 percent.

So, given this unprecedented shock and the response of the economy to that shock, what are some lessons I learned from the pandemic for understanding the behavior of an economy, and how do those lessons affect my forecasts going forward?

Lesson 1: When the Shock Is Unique, Adapt Fast

I think a principal lesson from this experience is that forecasters have to consider the nature and the novelty of an economic shock and quickly adapt our models to new situations. Some adaptations will work well and others will not, but you must adapt and, through trial and error, sort out how to modify one's model to account for novel shocks.

At the onset of the pandemic, there was a lot of learning about the nature of the shock and how to adapt economic models. Economists had to quickly incorporate epidemiology models of disease transmission into their economic models to try to understand how the spread of the virus would affect the overall economy.3 As a simple example, how should we capture the economic effects of social distancing in models in which the concept of distance doesn't exist?

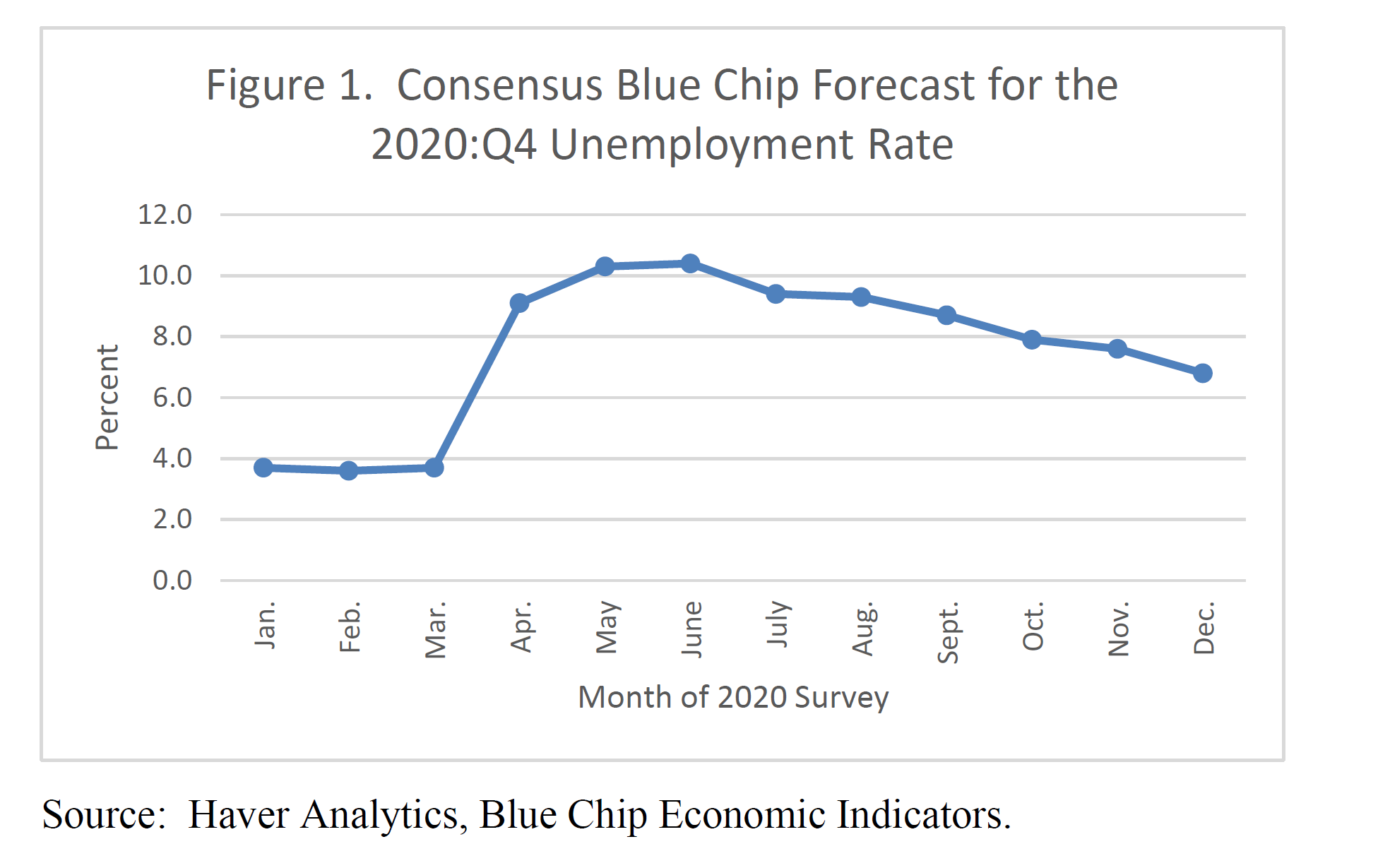

I cannot say how much forecasters relied upon their existing models or historical data to adjust their outlooks as 2020 progressed, but it was not enough to avoid large and persistent forecasting errors. For example,figure 1 shows the evolution of the Blue Chip summation of private forecasters' outlook for the average level of the unemployment rate in the fourth quarter of 2020. In March, like everyone else, these forecasters had no sense of what was coming; the consensus was for an unemployment rate of 3.7 percent near the end of the year. By April, there was a clear sense that the shock was bad. Forecasters adjusted their expectation for the unemployment rate to average near 9 percent in the fourth quarter of 2020. In May, with numbers in hand showing unemployment averaging around 14 percent for March and April, the consensus Blue Chip forecast then suggested a slowly declining unemployment rate that would average a bit over 10 percent in Q4. A slow decline in unemployment is what we experienced after the GFC, so it made sense to project a similar slow decline after the virus hit. But this time really was different.

{kind=link}

In fact, the unemployment rate dropped to 6.7 percent in November, and that is where it ended the year. Even after the dramatic economic rebound in May and June, the change in the consensus view for the unemployment rate later that year was extremely gradual. Something seemed to prevent forecasters-me included-from seeing the rapid improvement that was happening before our eyes.

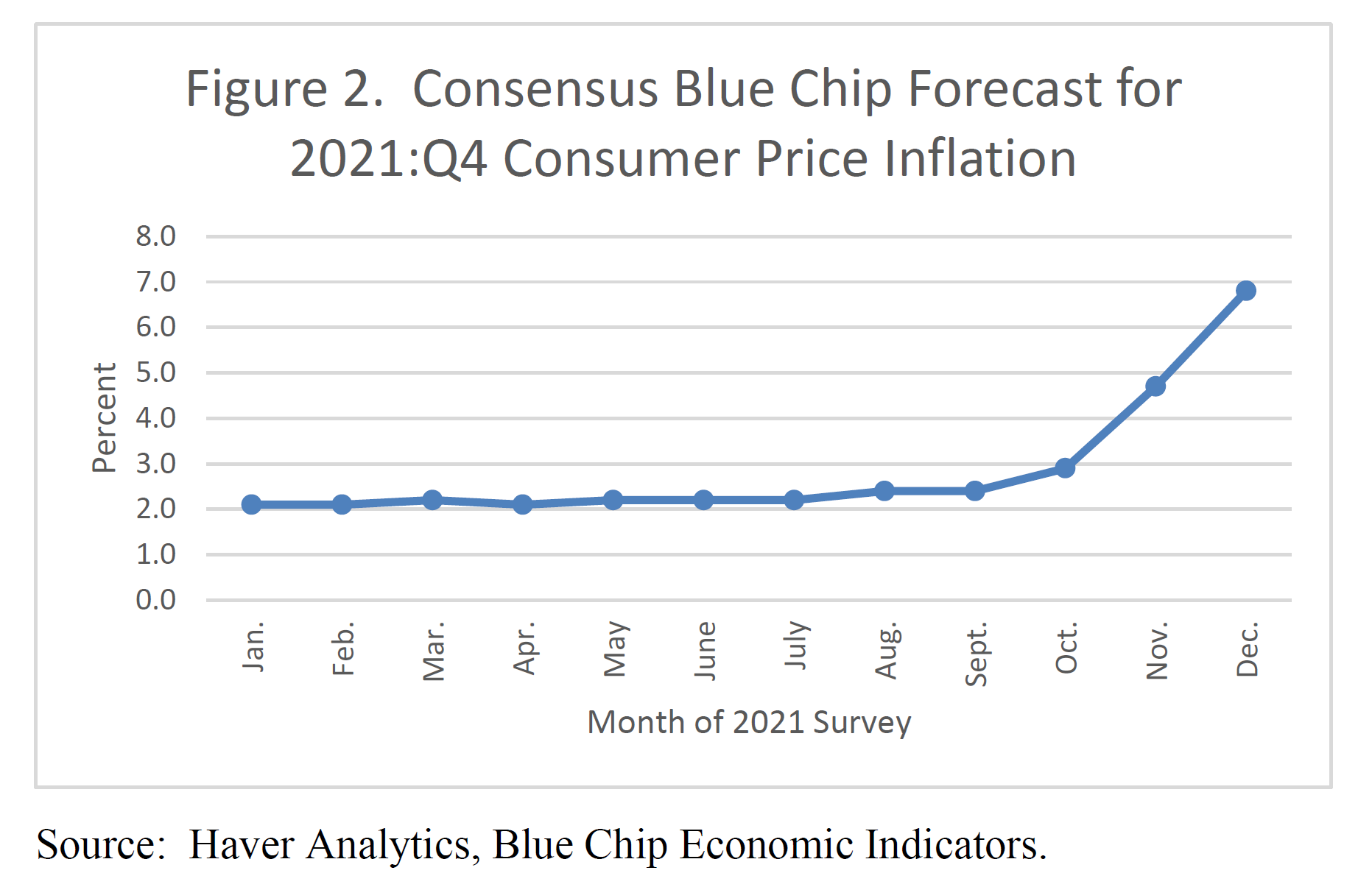

Same thing for the inflation forecast this year. As figure 2 shows, in January and February, the Blue Chip consensus was for consumer price inflation for Q4 to average about 2 percent. This forecast slowly ticked up to 2.4 percent through September. It was only in November that the consensus forecast moved above 4 percent and then jumped to 6.8 percent in the December survey. Just last Friday, November CPI inflation was reported at 6.8 percent for the 12 months ending November, the largest 12-month increase since mid-1982.

{kind=link}

I don't mean to single out private forecasters; my colleagues and I on the FOMC did no better forecasting during the pandemic. In June 2020, when the rebound in activity was under way, our median projection was for a drop in GDP that was more than twice as large as it turned out to be. Instead of an unemployment rate of 6.7 percent at year-end 2020, we predicted 9.3 percent. And even at the end of last year, nearly a year into the pandemic shock, we continued to have large forecast errors. We predicted that inflation based on personal consumption expenditures would be 1.8 percent this year, instead of the 5 percent it hit in October. Data suggest it will remain elevated through year-end.

Today at the Federal Reserve, we have learned from the COVID experience, and over the past two years we have improved our models and data collections in many ways.

One enhancement has been to supplement our models with additional high-frequency and microdata, such as data on school closures, airline passenger traffic, and mass transit ridership, to help us understand movements in various aspects of the economy. We gave more weight to weekly data on credit card purchases to supplement monthly retail sales reports. Both weekly paid employment and active employment from ADP have provided insight into the labor market ahead of when monthly employment numbers are released. We have also dug into very disaggregated data on prices to see where the upward and downward pressures are concentrated to help guide our thinking of how each of the sectors might adjust in the future. Another improvement in our approach to modelling is to incorporate epidemiological models to assist in thinking about the transmission of COVID over time and how vaccines have helped slow that spread and stabilize the economy.

The lesson from this experience is that economists need to continually adapt their models to the economic situation they are faced with, and when they are faced with a severe shock, they should ask themselves if they need to adapt their standard models and find other methods for forecasting the economy.

Lesson 2: Novel Shocks Can Produce Financial Stress in Unexpected Areas

Another lesson we learned was that unprecedented shocks, such as a pandemic, can generate unexpected and unfamiliar stress in the financial system. When the lockdowns and business closures started, it was reasonable to wonder whether banks would come under pressure, as they did during the Global Financial Crisis. As it turned out, banks were in pretty good shape and weathered the spring of 2020 pretty well, after a decade of effort by them and by government to strengthen regulation and supervision.4 On the other hand, probably the last thing that we expected to see was severe stress in the Treasury market, the most liquid and stable financial market in the world. But as it became clear that earnings and all sorts of payments could be disrupted to households, businesses, and state and local governments, there was a huge dash for cash and other liquid assets.5 Instead of flocking to Treasuries, people were trying to sell them into a rapidly deteriorating market. So we learned that even a Treasury security can become illiquid for certain types of shocks.

Lesson 3: The Fed Has Powerful Tools, Even When the Shock Is Unprecedented

We also learned that the Fed has potent tools to deal with even such an unfamiliar crisis. The Fed stepped in, lowered rates for discount window lending, revived lending facilities from the financial crisis, and created numerous new facilities to lend or support lending to households, small and large businesses, and state and local governments. In all, the Fed created 13 different lending facilities. In most cases, merely announcing these backstops succeeded in stabilizing markets, and, in fact, several facilities experienced very few requests for loans, which I consider a success.

So we learned that when the Fed acts quickly and decisively, our tools can quickly restore confidence, even when that loss of confidence is felt as widely as it was in the spring of last year. In addition, when the Fed makes it clear that it is prepared to act without hesitation as a backstop, that fact alone can be sufficient to stem a crisis.

Lesson 4: Globalization Is Fragile, and Inflation Ain't Dead

After two years of surprises, persistently elevated inflation is the biggest surprise for me, and I am carefully watching how this plays out in the next few months. High inflation is a heavy burden for households that have no choice about paying higher prices for groceries and other necessities. It hurts small business owners who have a harder time balancing their costs and the prices they charge for goods and services. One of the Federal Reserve's most important responsibilities is keeping prices stable and inflation under control.

Like most economists, after the performance of inflation over the past decade, it would have been hard for me to believe that it could run as high and as long as it has. I didn't expect it in 2020 as the pandemic took hold, and I was still in some doubt early this year. Likewise, I have been surprised at the persistence of the bottlenecks and other supply disruptions that have been a prominent source of elevated inflation. Like others, I expected that markets would adjust quickly and that these problems would be fixed, but that clearly isn't happening, and at this point, with COVID continuing to crimp supply, I don't know when it will. We are learning that the long and complex supply chains that have facilitated trade and driven down production costs in recent years are quite fragile and are taking longer to repair than I would have expected.

Similarly, I would have expected that labor supply shortages would have eased as the vaccine became widely available, unemployment benefits faded, and wages improved at the fastest rate in decades. Labor force participation increased last month, but I would have expected that more people would have joined the workforce after businesses and schools reopened. COVID has changed a lot of things, and we need to consider if it has persistently changed a significant number of people's desire to go back in the labor force.

This brings me back to my outlook for the economy in 2022, and the implications for monetary policy. The economy is set to continue growing very strongly through at least the first half of next year, and I expect employment to keep growing. With the unemployment rate at 4.2 percent in November, I believe we are very close to meeting the FOMC's maximum-employment goal. For inflation, as I said earlier, the next few months will be crucial in determining whether price increases will begin to moderate, as I still expect in my baseline outlook. However, I will be closely watching indicators of inflation expectations for signs that consumers and investors have come to expect high inflation well into the future, a development that could signal that the moderation in inflation I expect will not be coming soon. So, by choosing to speed up our reductions in asset purchases, the FOMC is providing flexibility for other adjustments to monetary policy, if needed, as early as spring to accommodate changes in the economic outlook. Omicron, as I said earlier, could slow the recovery or exacerbate inflation pressures, so we will have to be ready in the coming weeks to adjust as needed.

1 These views are my own and do not represent any position of the Board of Governors or other Federal Reserve policymakers. Return to text

2 The data here are from the Bureau of Economic Analysis, national income and product accounts. Since 1947, when quarterly measurement began, the previous record was an annualized drop of 10 percent in the first quarter of 1958. Return to text

3 For example, see Guillaume Vandenbroucke (2020), "The Mechanics of Individually- and Socially-Optimal Decisions during an Epidemic," Working Paper Series 2020-013B (St. Louis: Federal Reserve Bank of St. Louis, September); Andrew Glover, Jonathan Heathcote, Dirk Krueger, and Jose-Victor Ríos-Rull (2020), "Health versus Wealth: On the Distributional Effects of Controlling a Pandemic," NBER Working Paper Series 27046 (Cambridge, Mass.: National Bureau of Economic Research, September); Martin Bodenstein, Giancarlo Corsetti, and Luca Guerrieri (2020), "Social Distancing and Supply Disruptions in a Pandemic," Finance and Economics Discussion Series 2020-031 (Washington: Board of Governors of the Federal Reserve System, April); and Antoine Lepetit and Cristina Fuentes-Albero (2020), "The Limited Power of Monetary Policy in a Pandemic," working paper (September; revised November 2021). Return to text

4 See Randal K. Quarles (2020), "What Happened? What Have We Learned From It? Lessons from COVID-19 Stress on the Financial System," speech delivered at the Institute of International Finance, Washington, October 15. Return to text

5 In U.S. Treasury securities markets, for example, the difference between the prices offered to sell and buy some securities widened considerably, making it difficult for trades to occur. Return to text