Olli Rehn: Future proofing your bank? Digital transformation and regulatory reform in the financial sector

Closing keynote address by Mr Olli Rehn, Governor of the Bank of Finland, at The Financial Times Middle East Banking Forum, Dubai, UAE, 11 November 2018.

Your Excellencies, Ladies and Gentlemen,

Many thanks for the invitation to the FT Middle East Banking Forum, which has provided an excellent opportunity for substantive dialogue on the future of banking and finance. My task - both exciting and difficult - in this closing keynote is to discuss what future-proofing of your bank could mean, with the perspective of next 10 years.

Futurology is often associated mostly with technology. Yes, digital technology is quite profoundly changing the operating environment of banks. But it would still be a mistake to think the future is all digital, and nothing else. Future-proofing a bank is as much about a sound business model and the ability to adapt to a changing environment, as it is about utilising the best technologies available.

As we look at the next ten-year time horizon, there are three major forces challenging banks: digital technology, bank resilience, and climate change. Since my experience stems from Europe, I refer here to European banks, but this largely applies to banks in general.

Embracing digital technology is an essential part of future-proofing a bank. The financial industry is going through a major transformation, driven by the whole range of digital technologies and the explosive growth of data. Regulators, including central banks, are aiming at finding the right balance between regulation and innovation, so that consumers and businesses can benefit from new possibilities, while maintaining financial stability and a level playing field.

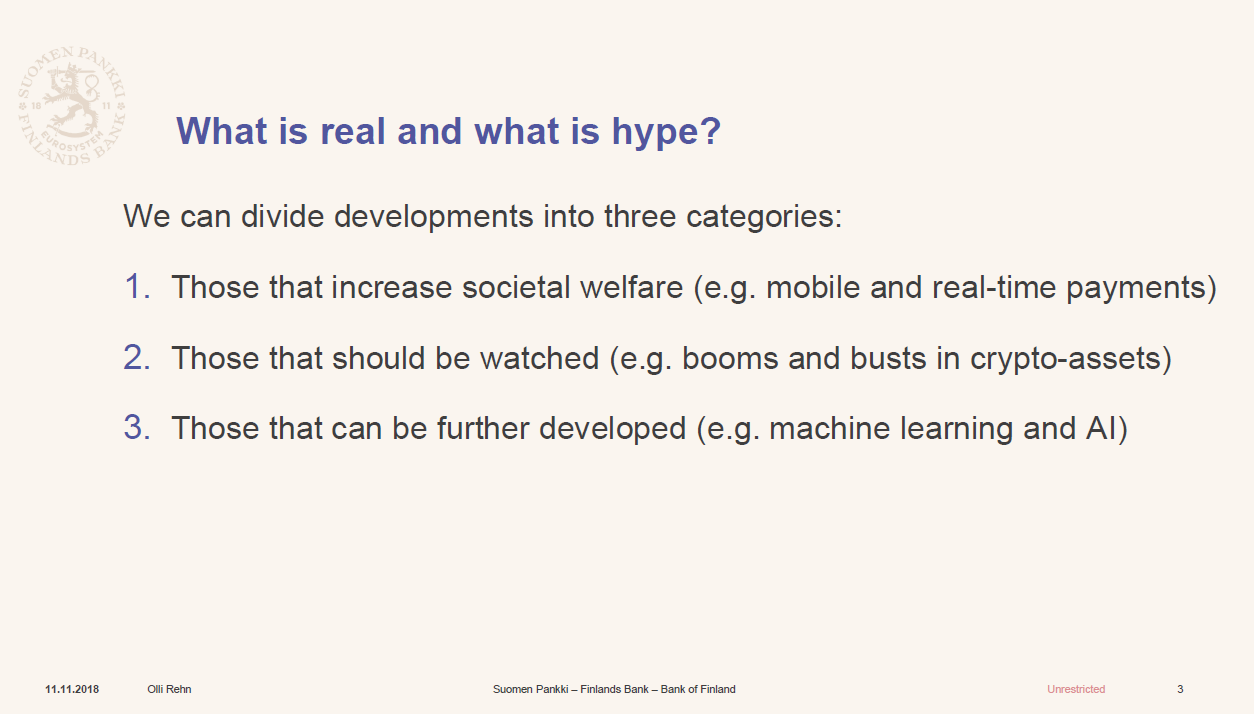

We want to make sure society remains inclusive. This requires us to look at digital transformation from the citizens' point of view. Therefore, we have to identify what is real and what is hype.

We can divide the developments in three categories:

- those that clearly increase societal welfare and should be benefitted from, such as mobile and real-time payments - as long as we also take care of enhancing financial literacy;

- those that should be watched, or even prevented, such as booms and busts related to crypto-assets; and

- those that can be further developed, such as machine learning and artificial intelligence.

Let me highlight two developments in the European banking sector, which may set an example for the rest of the world.

The first one is PSD2, and its related concept of Open Banking.

In the EU, the revised Payment Services Directive (PSD2) is an important regulatory framework to clarify payment legislation and make it better suited to a digitalising economy. The Directive aims at promoting competition, which will lead to better services and lower prices for consumers. It will open the payments market to third-party providers, and banks will be obliged to provide technical interfaces for accessing bank accounts. For some ears, this may sound daring - but the industry is currently working together with supervisors to make this as safe and secure as possible.

PSD2 is very much part of the broader trend of Open Banking. Banks all around the world are partnering with start-ups, and financial services are being rebuilt using the latest technology. In practice, it means that the customer experience can be provided by some party other than the bank itself, while the bank is providing the plumbing in the background.

The second development I would like to highlight is the instant payments system TIPS, which will be launched by the European Central Bank this month. TIPS will enable account-to-account transfers from one bank to another, in real-time, 24/7, every day of the year.

Why do I specifically want to highlight these two developments? Because when they work together, in synergy, they will have an impact which is greater than either would have on its own. Whereas PSD2 will help create a better payment experience for consumers, TIPS will make sure the money moves instantly. This will make the digital payments as close to cash as possible.

The second major force is the continuing work to make banks more resilient.

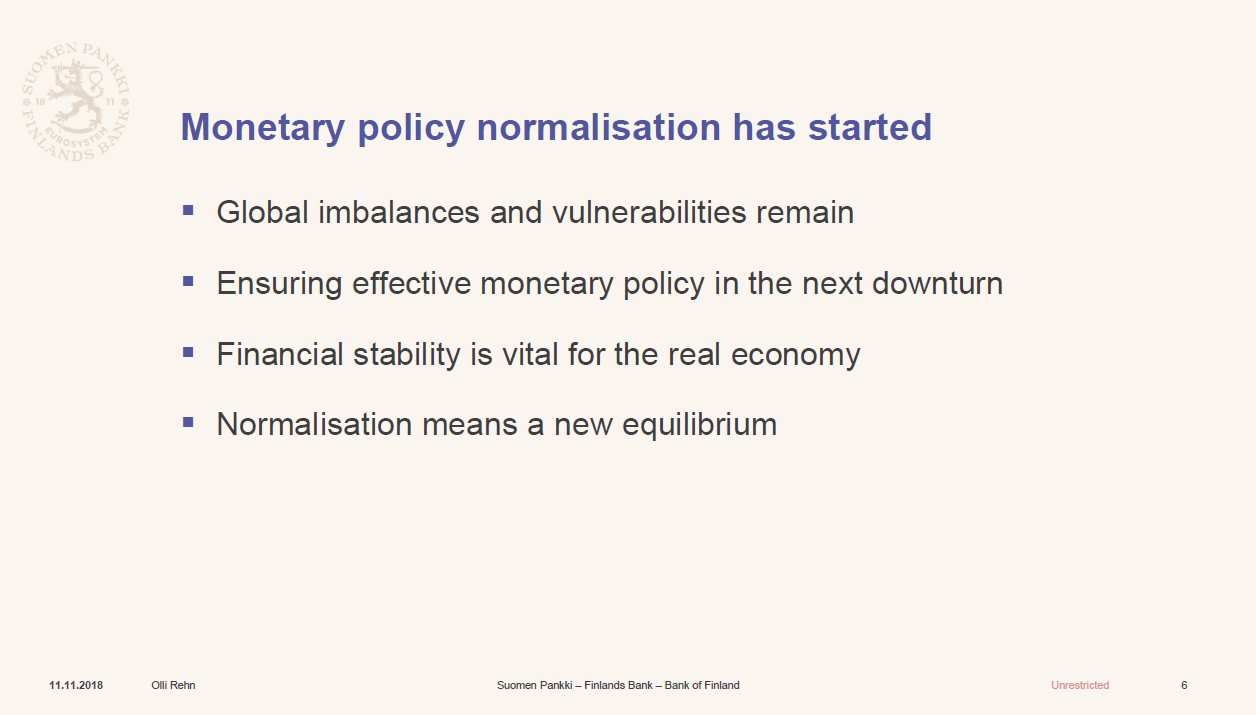

This is particularly important as we are also moving towards a normal monetary policy environment, although normalisation does not mean returning to a pre-2008 world. Instead, we are moving towards a new equilibrium.

Since some global imbalances and vulnerabilities remain, the European economy continues to need a degree of monetary policy support. This is a balancing act, since we must ensure the sustainable convergence of inflation to our definition of price stability, while simultaneously protecting the on-going recovery of employment and the repairing of balance sheets. An important lesson from the financial crisis is that the financial industry, including banks and other financial institutions, are special and have a huge impact on macroeconomic stability in the broad sense.

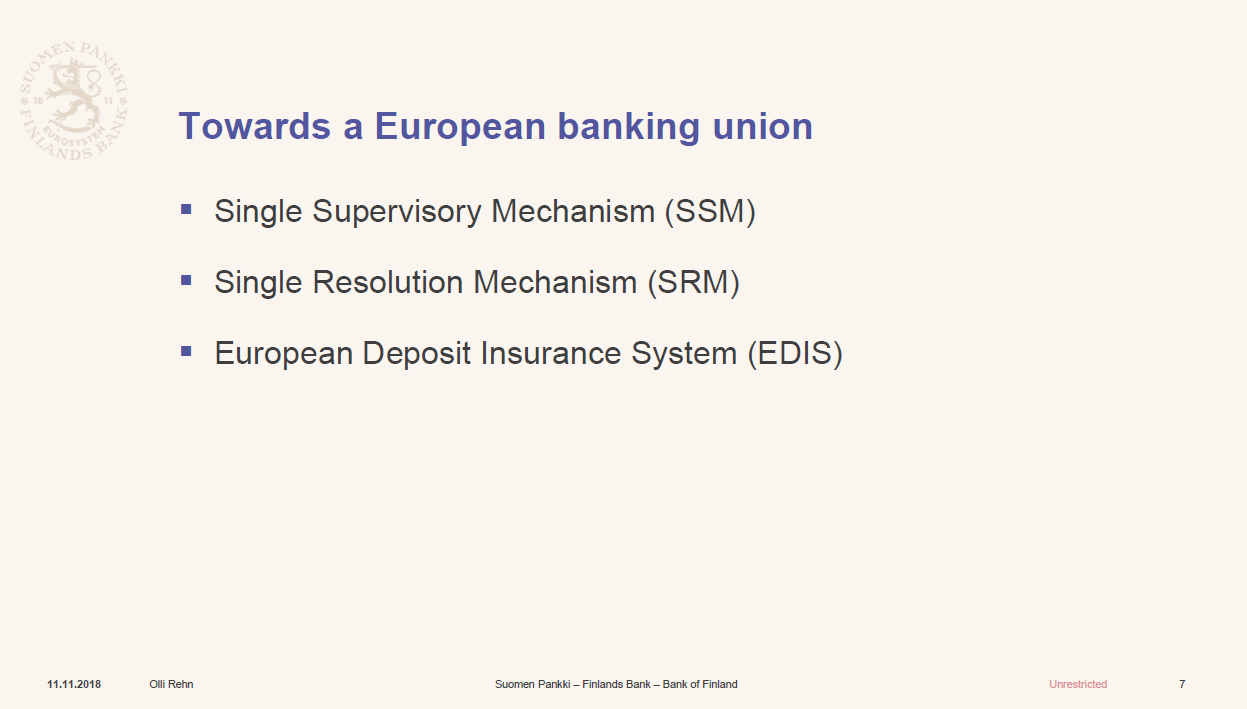

The most important regulatory steps taken in Europe to make the banking sector more resilient are the creation of the banking union and the development of a new macroprudential framework.

It may seem surprising that the development of the banking union only started as late as 2010-12, more than a decade after the founding of the euro. Today, the banking union makes a lot of sense, and it clearly strengthens the euro area - but regrettably it took a financial and debt crisis to really get the ball rolling.

Since 2014, the banking union consists of two main building blocks, the Single Supervisory Mechanism (SSM) and the Single Resolution Mechanism (SRM). However, the banking union is not yet complete. A third building block, the European Deposit Insurance System (EDIS), still needs to be implemented.

As for the macroprudential work, in 2010 the European Commission proposed a union-level body, with a mandate to oversee systemic risk in the financial system. A year later, the European Systemic Risk Board (ESRB) was founded and became responsible for the macroprudential oversight of the EU financial system.

Macroprudential policies are like taking away the punch bowl when the party is at its best. They help prevent the excessive build-up of risk, smoothen the financial cycle, and limit contagion. Some of the macroprudential tools are additional capital buffers, others are borrower-based tools, such as Loan-To-Value (LTV) caps. These have proven quite effective in many EU member states, e.g. by calming down the housing markets in Ireland, Norway and Sweden.

Now let me move to the third, and probably biggest challenge of all. How can we transform banking so that it contributes responsibly to an ecologically sustainable, yet growing and employing economy, in the face of climate change?

Let me be clear, climate change is very relevant for banks. That's because it is the biggest market failure of all times. Its impacts are already felt today, in the form of extreme weather events, hurricanes, flooding, and extended heat waves, leading to loss of lives as well as financial damages. Climate change is expected to increase their frequency and severity. The negative impact is further amplified by long-term effects, such as rising sea levels, changes in rainfall patterns, and potential mass migrations.

As the world moves from talk to action, climate policies start having an effect on the real economy. More stringent building regulation, subsidies for renewables, stricter emission standards - all these and many other measures will change the dynamics of economic growth.

For a financial institution, climate change poses two particular types of risks. There are physical risks, related to climate change itself, and transition risks, related to climate policies.

Physical risks lead to financial losses as a consequence of extreme weather events. To the extent that property is insured, this burden falls on insurers and re-insurers. Without insurance, it is the property itself that is suffering the loss. However, it is also possible that the debt servicing ability of a borrower, or the collateral for a loan, are damaged as a result of a weather event. In those cases it may be a bank that will book losses.

Financial losses from weather events can also extend beyond the initial damages, if the valuations of all properties near the damaged one are affected. We already have examples of this in some flood-prone areas, where insurance has become more expensive, and it has become more difficult to get a mortgage.

Transition risks materialise when a company with a carbon-intensive business model is unable to adjust quickly enough to new policies, competing technology, or changing customer preferences. Investors may also need to adjust their portfolios, leading to financial losses. Such losses are amplified if all investors act simultaneously.

The famous management scientist Peter Drucker is credited with the phrase "you can't manage what you can't measure", and the same applies here. Data plays a key role in managing these risks. Data is needed on businesses and their dependencies on carbon-intensive processes throughout the value-chain. We also need more data on the potential impact of extreme weather events. As of today, much of this data is incomplete.

Since climate change knows no borders, global efforts are needed. Regulators, central banks and supervisors around the world are starting to take action. First, on getting financial institutions to manage their own climate change related risks. The next step is to get them to adjust their balance sheets, and support a transition towards a more sustainable economy.

Ladies and Gentlemen,

As the excellent presentations and panels today have proven, banks are living in a time of change and transformation. Change in itself is inevitable, but transformation can be for the better - and by future-proofing our banks and perhaps also our personal choices - we can create not a grave but a braver new world, which is more inclusive, more responsible, more sustainable, and more prosperous.

Technology will provide the means, but a more liveable, sustainable planet will provide the purpose.

Thank you.