Guy Debelle: The outlook for the Australian economy

Opening keynote speech by Mr Guy Debelle, Deputy Governor of the Reserve Bank of Australia, at the CFO Forum, Sydney, 15 May 2018.

Thanks to Lynne Cockerell for her help in preparing this speech.

Today I would like to talk about the Bank's outlook for the economy. We published this in the Statement on Monetary Policy (SMP) earlier this month.1 This set of forecasts was little changed from the previous set of forecasts we released three months earlier. This is because the economy, both domestically and globally, has been evolving generally in line with our expectations.

When reading through the Bank's forecasts, I think it is useful to avoid false precision. An important question to ask is: are these revisions to the Bank's outlook consequential for the monetary policy decision? Similarly you can ask, do I think these changes affect my own decisions about my household or my business? A tenth or two of a percentage point here or there on the outlook for GDP or inflation is unlikely to matter that much for any of those decisions. Often, these revisions reflect the new information that has come to hand over the previous quarter. This leads us to reassess the starting point for our forecasts of where the economy is then likely to go. In making this assessment, we ask whether the incoming data have been view-changing or view-validating. Over the previous three months (and, indeed, the three months before that too), the data have generally been view-validating.

The forecasts that are published can best be characterised as the modal forecast for the economy. That is, they are the path for the economy which we think is most likely to occur. But there are a number of risks to that outlook. The SMP talks about some of those uncertainties too. Today I will also spend some time drawing out some of the issues around those uncertainties.2

The central forecast

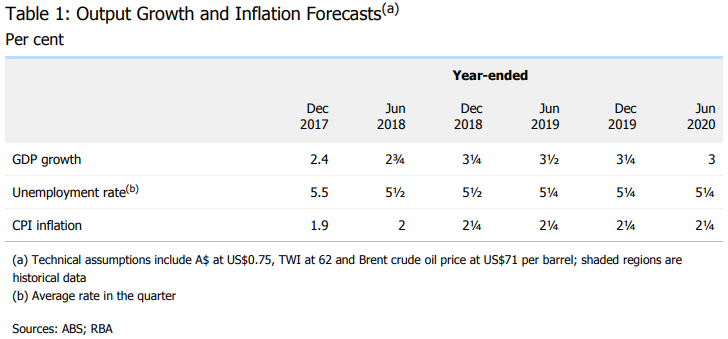

As I just said, the forecasts we have just published are little changed from those we published in February. Table 1 shows the Bank's outlook for GDP growth, the unemployment rate and inflation until June 2020. This is generally the time horizon that is relevant for the Board's deliberations on monetary policy.

The forecasts embody a number of technical assumptions. These include that the cash rate evolves broadly in line with the market expectations. Currently the market assumes that the cash rate is likely to remain unchanged for at least the next 12 months, and then rise only very slowly beyond that. The forecasts also assume that the exchange rate and oil prices remain at their current levels. Historically, we have found that assuming those variables remain constant is at least as good as any other forecast, while recognising that they are highly likely to change. In saying that, it is worth noting that the exchange rate has moved within a fairly narrow range over the past two years. These small variations have probably not been a major factor in your decision-making as CFOs. In contrast, I would expect that the 20 per cent depreciation of the Australian dollar in 2014-2015 did have a material impact on decision-making at any business with an export or import-competing focus.

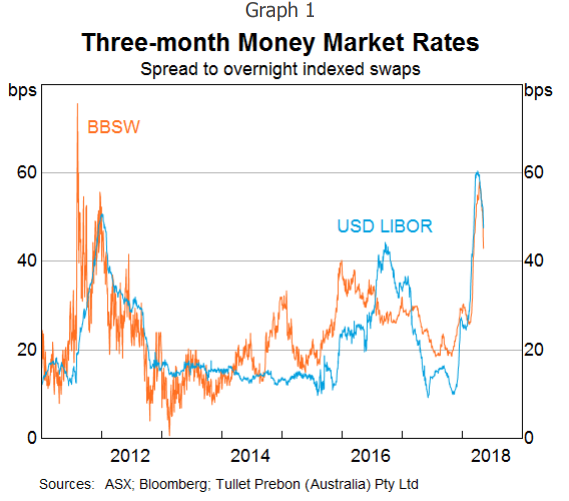

Other developments in financial conditions can affect the forecasts too. One example is developments in money market rates. In the SMP, we document the recent rise in money market interest rates in the US, particularly LIBOR (Graph 1). There are a number of explanations for the rise, including a large increase in bill issuance by the US Treasury and the effect of various tax changes on investment decisions by CFOs at some US companies with large cash pools.3 This rise in LIBOR in the US has been reflected in rises in money market rates in a number of other countries, including here in Australia. This is because the Australian banks raise some of their short-term funding in the US market to fund their $A lending, so the rise in price there has led to a similar rise in the cost of short-term funding for the banks here; that is, a rise in BBSW.4 This increases the wholesale funding costs for the Australian banks, as well as increasing the costs for borrowers whose lending rates are priced off BBSW, which includes many corporates.

However, the effect to date has not been that large in terms of the overall impact on bank funding costs. Thus far, it has not been a consequential development from a forecasting point of view. It is not clear how much of the rise in LIBOR (and hence BBSW) is due to structural changes in money markets and how much is temporary. In the last couple of weeks, these money market rates have declined noticeably from their peaks. We will continue to monitor how this unfolds in the period ahead.

The outlook for the economy in 2018 and 2019 is expected to be a little stronger than occurred in 2017. GDP growth is expected to pick up from around 2½ per cent currently to be around 3¼ over the next couple of years.

What is driving that pick-up in growth?

One part of the answer is that the global conjuncture is constructive. We have been witnessing the most synchronised pick-up in the global economy for quite some time. The US economy is doing well. Europe is doing better than it has been for the past decade. The Japanese economy has recorded its longest period of quarterly growth in almost three decades. The global conjuncture has been reflected in a pick-up in global industrial production and trade that is particularly beneficial to the east Asian region, which is leveraged to the global cycle.

China stands a little in contrast to these developments, though. Growth in China has moderated somewhat, in part because the authorities are pursuing other policy objectives to address pollution and financial stability risks. But the easing in growth has been small. It remains to be seen just how much tolerance the Chinese authorities would have to any significant slowing in growth.

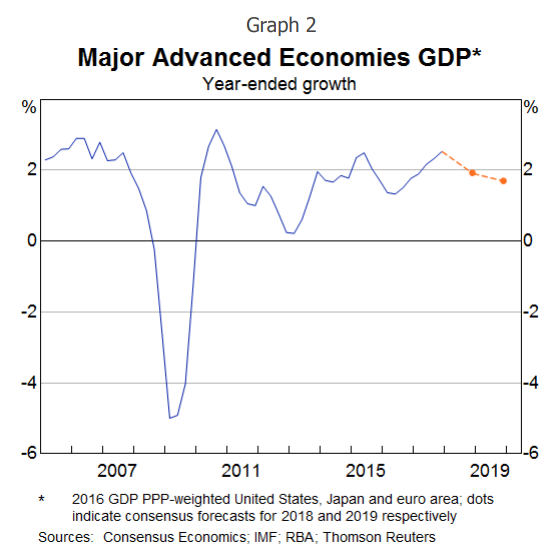

One interesting point about the global conjuncture is that while the recovery is synchronised, to date we haven't seen it accelerate in any meaningful way. Historically, synchronised growth cycles have tended to be self-reinforcing, leading to a continuing pick-up in growth. Today, growth in most economies is good, often a little above trend. But no economy is growing that much above trend. Forecasts for global growth in 2018 and 2019 are below the outcome for 2017, notwithstanding some upward revisions to those forecasts (Graph 2).

Why aren't we seeing a further pick-up in global growth? I think part of the explanation is that the global financial crisis has left long-lasting scars. For a number of years, risks to the outlook have generally been characterised as being on the downside by both policy-makers and business people. In contrast, in previous synchronised global upswings, the risks have generally had an optimistic slant to them. Even though we have seen a pick-up in business sentiment right around the world, a sizeable degree of caution and scepticism has accompanied that improvement in sentiment. We may be close to a tipping point where we see that tendency for pessimism swing to optimism.

That pessimism filter has been reflected in the focus on restraint in investment decisions in the decade after the financial crisis. It is also evident in the focus on cost-cutting and contributes to the subdued outcomes for wages and prices we have seen in many countries.

The current, more positive, pace of global growth is predicated on the stimulatory settings of monetary policy in place in most countries. That is, these policy settings have been necessary to deliver these growth outcomes. They have countered the headwinds that have been present in the global economy over the past decade. The headwinds have abated but it is not clear they have yet switched to be tailwinds.

One potential exception to this is the US. The fiscal stimulus that is in train this year and next is being delivered in an economy with limited spare capacity. Historically, such as in the late 1960s/early 1970s, such episodes have generally led to stronger growth but also higher inflation. I will come back to that in my discussions of some of the uncertainties around the outlook in a few minutes.

This constructive global outlook provides a solid backdrop for domestic developments. It is underpinning growth in our exports. Exports have also been bolstered by the additional capacity coming on stream in LNG. We expect that the additions to capacity in our main resource exports - iron ore, LNG and coal - will be largely complete by the end of the year.

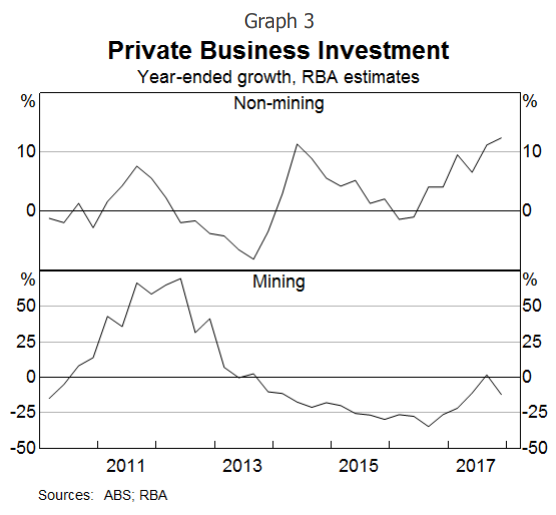

That also means that we are close to the end of the decline in mining investment. That has been a major drag on economic growth over the past several years (Graph 3). The absence of that negative is a positive, particularly when one factors in the associated export growth that has resulted from the investment.

The decline in mining investment also has had negative spillovers to the non-mining sector, particularly in the resource-intensive states.5 That now is largely past. Moreover, the increase in public infrastructure spending is creating positive spillovers.6 And importantly, the rise in business sentiment globally is also evident in Australia. All of these factors are reflected in the pick-up in investment in the non-mining sector we have seen over the past four years.

Turning to consumption, we have had more validation of our outlook with recent data revisions. We had been concerned that our forecast may have been a little optimistic, but are now more confident in it. In statistical terms, the weight on the modal forecast has risen. But uncertainties remain around the outlook for consumption, which I will discuss shortly.

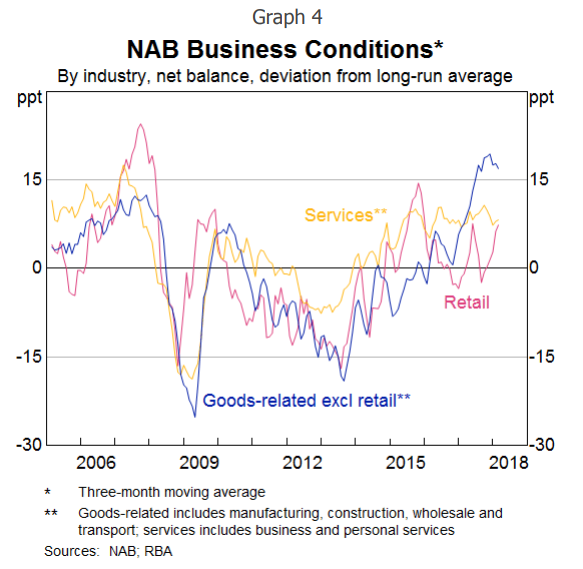

It is worth noting that domestic demand growth has outstripped growth in GDP, running at around 3¼ per cent. This gives us confidence in our forecast of GDP growth a little above trend over the next couple of years. That is, that GDP growth is likely to have a 3 in front of it. The surveys of business conditions very much support that assessment with conditions in many parts of the economy assessed to be well above average (Graph 4).

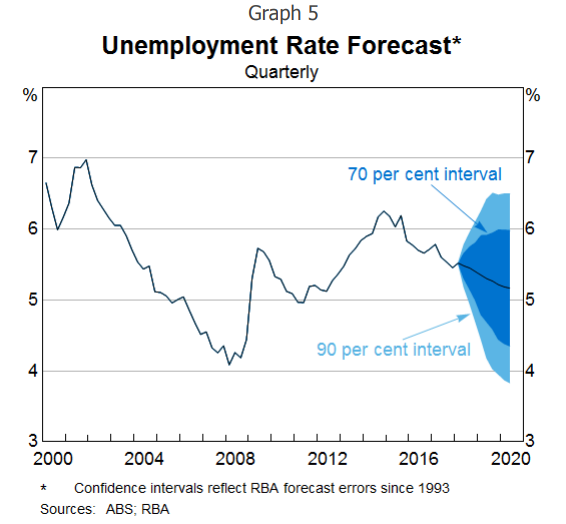

That pace of growth, should it transpire, will eat gradually into the spare capacity in the economy. Hence we expect the unemployment rate to gradually decline from here. The unemployment rate declined by a ¼ percentage point over the past year; we are expecting something similar over the year ahead.

The reduction in the unemployment rate has stalled for some months. I find the unemployment rate is the most useful single statistic to assess the state of the labour market. The unemployment rate has remained steady in an environment where employment growth has been measured to be particularly strong. Labour supply has risen strongly alongside it. Part of the explanation for this is an increase in female participation and older workers remaining in employment longer than previously.7 The strong employment growth has reduced unused capacity, which is a positive development, but not in a way that has lowered the unemployment rate.

Forward indicators in terms of vacancies and hiring intentions remain positive. GDP growth is expected to pick up. This gives me reasonable confidence that the unemployment rate will resume its gradual downward trend (Graph 5).

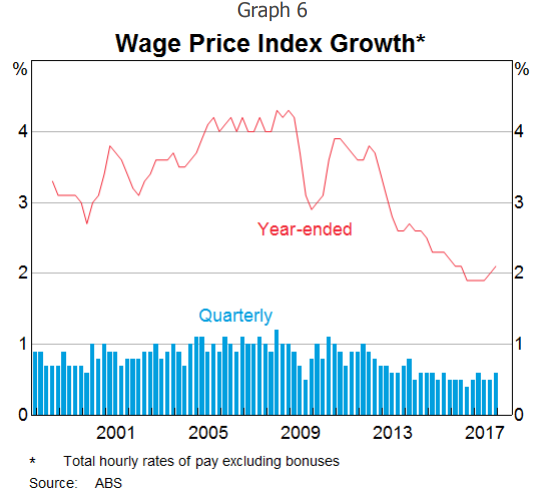

The gradual decline in spare capacity is expected to lead to a gradual pick-up in wages growth. A critical question is: when will wages start to rise in a meaningful way?

Recent data on wages provides some assurance that wages growth has troughed. The majority of firms surveyed in the Bank's liaison program expect wages growth to remain broadly stable over the period ahead. Over the past year, there has been a pick-up in firms expecting higher wage growth outcomes. Some part of that is the effect of the Fair Work Commission's decision to raise award and minimum wages by 3.3 per cent. Talking to businesses, such as yourselves, suggests that there are pockets where wage pressures are more acute. But, while those pockets are increasing gradually, they remain fairly contained at this point (Graph 6).

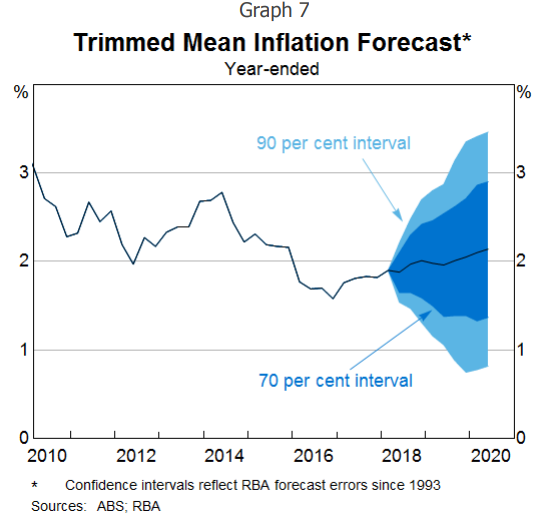

The most recent inflation data were also consistent with our forecasts. The data show that inflation remains low but stable. Domestic price pressures remain subdued. Inflation is very close to 2 per cent: 1.9 per cent on a CPI basis, marginally below the bottom of our inflation target. We expect upward pressure on prices over the next couple of years, but again this is expected to be quite a gradual process (Graph 7).

As you might have gathered by now, the key word in this discussion of the outlook is gradual. Further progress on both inflation and unemployment is expected over the period ahead, but it is expected to be only gradual. For some time the Reserve Bank Board's view has been that holding the cash rate steady at 1½ per cent would assist that progress, with steady monetary policy promoting stability and confidence. If the economy continues to evolve as expected, higher interest rates are likely to be appropriate at some point. Notwithstanding this, the Board does not currently see a strong case for a near-term adjustment in the cash rate.

Having talked about the central forecast, I will now talk about some of the uncertainties around this central forecast.

Uncertainties

One uncertainty relates to the global inflation outlook. We have experienced low inflation globally for a long period of time. There are signs of inflation starting to pick up. The global economy is close to full capacity, particularly in the advanced economies. The US fiscal stimulus is still to have its full effect in an economy that, as I said earlier, is very close to full capacity. This is a similar situation to that in the late 1960s and could lead to more inflation in the US than currently anticipated. In turn, that could lead to more tightening in monetary policy than currently expected. While markets expect some tightening, they don't expect too much more at this point. Moreover, in such circumstances, you might also expect the neutral policy rate to rise, albeit gradually.

Such a rise in growth and inflation offshore could lead to a depreciation of the Australian dollar, given that the Australian economy appears currently to have more spare capacity than some other advanced economies. If this were to occur, we would expect it to boost domestic output and lead to a faster rise in inflation than currently assumed, but somewhat later than in other economies.

There is also a significant risk to the global economy from the current tensions around trade policy. While the effect of the measures announced thus far has been modest, there is clearly the potential for this to escalate. Australia has benefited from an open, inclusive and rules-based international system. We have as much at stake as any other country in the continuation of this system.

The SMP has for some time highlighted the uncertainties around the outlook for China. I won't discuss them today, as the Governor will talk about them in depth in a speech next week.

Turning to uncertainties around the domestic outlook, one important uncertainty relates to household balance sheets. Australian households have a relatively large amount of mortgage debt. This means that they are more likely to be sensitive to changes in income and interest rates. This poses risks to the outlook for the largest component of spending, household consumption.

One reason why I think debt remains high relative to income has been because income growth has been unexpectedly low. In past decades, one of the easiest ways to pay down your mortgage was through inflation. Higher inflation was accompanied by higher wages growth. Because the mortgage is fixed in nominal terms, the debt level declined quite rapidly relative to a household's income when incomes were growing quickly. Household income growth has been subdued for a number of years, which means that a number of households may be carrying a larger mortgage for longer than they expected when they took out the loan. While they can service the mortgage, it has consumed a larger share of their income for longer than they might have intended.

Over recent years, a number of steps have been taken by regulators that have helped to strengthen resilience in household balance sheets. It is worth remembering that lending standards have been tightened for a number of years now. From 2014, APRA and ASIC have strengthened their focus on lending practices. This has included ensuring that lenders' serviceability tests for new borrowers must use an interest rate of at least 7 per cent. That is, households should be able to afford a mortgage rate well more than 2 per cent higher than it is currently (and remember, many households took out their loans when rates were higher than today). More recently, APRA has also been focused on ensuring that lenders assess borrowers' income appropriately. While the Royal Commission has highlighted a number of cases where this has not been the case, an important consideration from a macroeconomic perspective is how widespread this has been, and whether it is consequential for the ability of most households to afford to service their loans.

I take some comfort from the fact that arrears rates on mortgages remain low. Even in Western Australia, where there has been a marked rise in unemployment and where house prices have fallen by around 10 per cent, arrears rates have risen to around 1½ per cent, which is not all that high compared with what we have seen in other countries in similar circumstances and earlier episodes in Australia's history.

We have provided some information in the latest SMP on interest rate resets on interest-only loans. These can see the required mortgage payments rise by nearly 30-40 per cent for some borrowers. There are a number of these loans whose interest-only periods expire this year. It is worth noting that there were about the same number of loans resetting last year too. Our assessment is that there are quite a few mitigants which will allow these borrowers to cope with this increase in required payments, including the prevalence of offset accounts and the ability to refinance to a principal and interest loan with a lower interest rate. While some borrowers will clearly struggle with this, our expectation is that most will be able to handle the adjustment so that the overall effect on the economy should be small.8

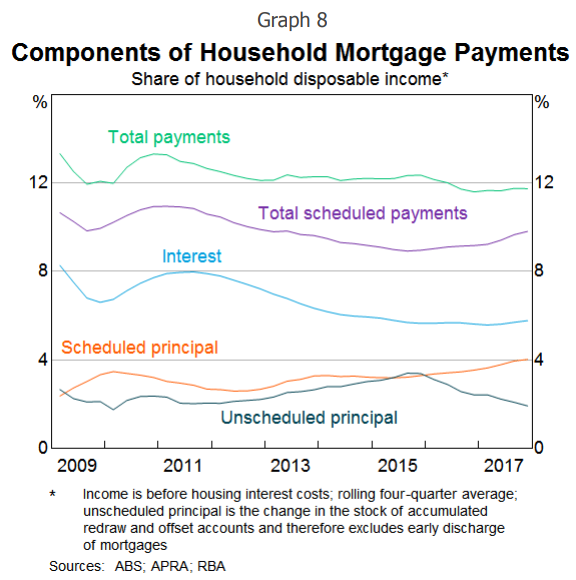

This switch away from interest-only loans should see a shift towards a higher share of scheduled principal repayments relative to unscheduled repayments for a time. We are seeing that in the data (Graph 8). It also implies faster debt amortisation, which may have implications for credit growth.

There is a risk of a further tightening in lending standards in the period ahead. This may have its largest effect on the amount of funds an individual household can borrow, more than the effect on the number of households that are eligible for a loan. This, in turn, means that credit growth may be slower than otherwise for a time. To me, that has more of an implication for house prices, than it does for the outlook for consumption.

Finally, in thinking about the resiliency of household balance sheets to higher interest rates, it is important to think about the environment in which interest rates would be rising. That environment is highly likely to be one where wages and household incomes are also growing faster than currently, improving the ability of households to afford higher mortgage repayments.

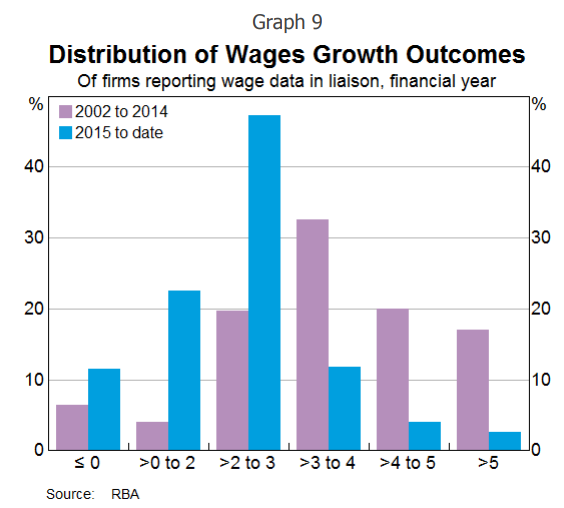

One final risk that I would like to touch on is the related risk stemming from low wages growth. How much longer is wages growth going to remain at its current low rates? The experience of other countries with labour markets closer to full capacity than Australia's is that wages growth may remain lower than historical experience would suggest. In Australia, 2 per cent seems to have become the focal point for wage outcomes, compared with 3-4 per cent in the past.9 Work done at the Bank shows the shift of the distribution of wages growth to the left and a bunching of wage outcomes around 2 per cent over the past five years or so (Graph 9). As I said earlier, while there are signs of wage pressure emerging, they remain localised for now. There is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2 per cent focal point evident in many wage outcomes today.

These are some of the uncertainties that the Board discusses in its monetary policy deliberations. They are not the central case, but they are some of the risks around it. Should these risks come to pass, then they are likely to have a material effect on the Bank's outlook for the economy. In turn, it is quite possible that such revisions would be consequential for the Board's assessment of the appropriate stance of monetary policy. But it is important to remember to think about the context in which these risks materialise. As is often the case, they may not materialise in isolation. Some of them may materialise at the same time or the actual manifestation of them may be different from the form I have discussed here.

Conclusion

Monetary policymaking, just like the business decisions that you make as CFOs, is about decision-making under uncertainty. I have highlighted some of these uncertainties around the Bank's central forecast for the economy.

That central forecast is for the economy to grow a little faster in 2018 and 2019 than in 2017. That should see the unemployment rate resume its gradual decline. It should also see wages growth and inflation gradually pick up. In time, should that central forecast come to pass, higher interest rates are likely to be appropriate. But the Board does not see a strong case for a near-term adjustment in the cash rate and holds the view that by holding the cash rate steady, it can best assist the achievement of the desired economic outcomes.

1 RBA (Reserve Bank of Australia) (2018), Statement on Monetary Policy, May.

2 I spoke about uncertainties in forecasting at the 7th Warren Hogan Memorial Lecture last year. See Debelle G (2017), 'Uncertainty', 7th Warren Hogan Memorial Lecture, Sydney, 26 October.

3 Note that the rise is not attributable to increased concerns about the global banking system as was the case in 2008 and 2009.

4 The rise in LIBOR has also resulted in higher money market rates in Hong Kong, New Zealand and the UK. But there has been less of an effect on European or Japanese rates. This is because while European and Japanese banks also raise funds in the US money markets, they do so to fund $US assets, rather than assets in their own currencies.

5 Debelle G (2017), 'Business Investment in Australia', Speech at UBS Australasia Conference, Sydney, 13 November.

6 See RBA (2018), 'Box C: Spillovers from Public Investment', Statement on Monetary Policy, February, pp 40-42.

7 See RBA (2018), 'Box B: The Recent Increase in Labour Force Participation', Statement on Monetary Policy, May, pp 33-34.

8 See RBA (2018), 'Box C: The Expiry of Interest-only Loan Terms', Statement on Monetary Policy, May, pp 45-48. Also Kent C (2018), 'The Limits of Interest-only Lending', Address to the Housing Industry Association Breakfast, Sydney, 24 April.

9 Bishop J and N Cassidy (2017), 'Insights into Low Wage Growth in Australia', RBA Bulletin, March, pp 13-20.