Christopher Kent: The limits of interest-only lending

Address by Mr Christopher Kent, Assistant Governor (Financial Markets) of the Reserve Bank of Australia, to the Housing Industry Association Breakfast, Sydney, 24 April 2018.

I would like to thank Michael Tran and Ben Jackman for help in preparing this material, and my colleagues Bernadette Donovan and Ben Shanahan from the Financial Stability Department for their helpful comments and suggestions.

Introduction

I'd like to thank the Housing Industry Association for the opportunity to speak to you about the role of interest-only loans.

Mortgages on interest-only terms have become an increasingly prominent part of Australian housing finance over the past decade. At their recent peak, they accounted for almost 40 per cent of all mortgages. While interest-only loans have a role to play in Australian mortgage finance, their value has limits.

Other things equal, interest-only loans can carry greater risks compared with principal-and-interest (P&I) loans. Because there's no need to pay down principal initially, the required payments are lower during the interest-only period. But when that ends, there is a significant step-up in required payments (unless the interest-only loans are rolled over). This owes to the need to repay the principal over a shorter period; that is, over the remaining term of the loan. Also, because the debt level is higher over the term of the loan, the interest costs are also larger.

For housing investors, the key motivation for using an interest-only loan is clear. By enabling borrowers to sustain debt at a higher level over the term of the loan, interest-only loans maximise interest expenses, which are tax deductible for investors. They also free up funds for other investments.

For those purchasing a home to live in, there are other motivations for an interest-only loan. They provide a degree of flexibility when it comes to repayment. They can assist households to manage a temporary period of reduced income or heightened expenditure. That might occur, for example, when a household wants to work less in order to raise children, cover the cost of significant renovations or obtain bridging finance to buy and sell properties. They can also appeal to households without a steady flow of regular income, such as the self-employed. So there are understandable reasons why borrowers have taken out interest-only loans.

During interest-only periods, disciplined borrowers will be able to provision for future repayment of principal. They can accumulate funds in an offset or redraw account, or build up other assets. With sufficient saving over the interest-only period, the health of their balance sheet need be no different than it would have been with a P&I loan.1

If, however, a borrower spends the extra cash flow available to them during the interest-only period (compared with the alternative of a P&I loan), they will need to make sizeable adjustments when that ends. They will have to either secure additional income by that time or reduce their consumption (or some combination of both). That will be more difficult and possibly come as a shock to the borrower if they haven't planned for it in advance.

If the borrower has made no provisions and is unable to make the necessary adjustment, they may need to sell the property to repay the loan. Therein lies an additional risk inherent in interest-only lending. Moreover, the borrower's ability to service the loan is not fully tested until the end of the interest-only period. If the borrower defaults, the potential loss for the lender will be larger than in the case of a P&I loan given that interest-only loans by design allow borrowers to maintain the debt at a higher level over the term of the loan.

That's why, when providing interest-only loans, prudent lenders will carefully assess the borrower's ability to make both interest and principal payments. Among other things, banks have to make their loan 'serviceability assessments' based on the status of the borrower's income and expenditure at the time of origination.2 To help manage risks, lenders also typically limit the maximum interest-only period to five years.3

The role of interest-only lending and its potential implications for financial stability have been of interest to the Reserve Bank for some time. The possible effects of the transition at the end of interest-only periods were discussed in the recent Financial Stability Review.4 I will come to that issue shortly, but first I want to review the regulatory responses to the strong growth of interest-only lending in recent years.

Tightening of lending standards

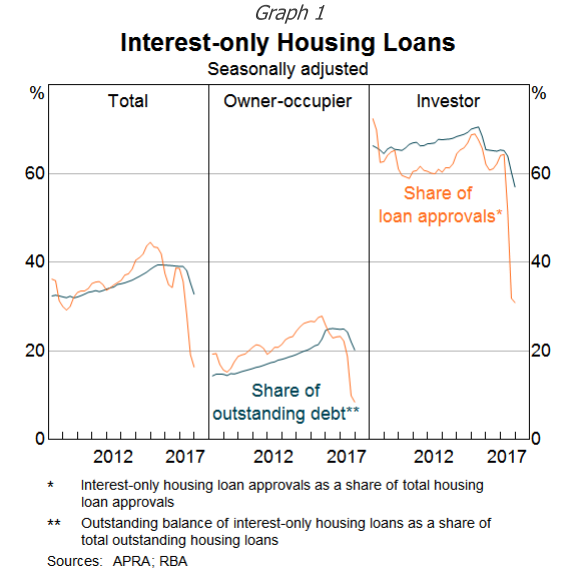

Interest-only loans had grown very strongly for a number of years in an environment of low mortgage rates and heightened competitive pressures among lenders. The share of housing credit on interest-only terms had increased steadily to almost 40 per cent by 2015 (Graph 1). The share of credit on interest-only terms has always been much higher for investors than owner-occupiers (consistent with the associated tax benefits for investors). But interest-only loans for owner-occupiers had also grown strongly.

In 2014, the Australian Prudential Regulation Authority (APRA) acted to tighten standards for interest-only loans, and mortgages more generally. APRA required serviceability assessments for new loans to be more conservative by basing them on the required principal and interest payments over the term of the loan remaining after the interest-only period. (Previously, some banks were assuming that the principal was being repaid over the entire life of the loan, which was clearly a lower bar for the borrower to meet.) At about the same time, APRA acted to ensure that the interest rate 'buffer' used in the serviceability assessments for all loans was at least 2 percentage points above the relevant benchmark rate (with an interest rate floor of at least 7 per cent). Also, that test was required to include other, existing debt (which is often substantial for investors). The application of such a buffer in serviceability assessments implies that borrowers should be able to accommodate a notable rise in required repayments.

When APRA tightened loan serviceability requirements, it also limited the growth of investor lending (to 10 per cent annually).5 The share of interest-only loans in total housing credit then stabilised for a time at around 40 per cent, having increased steadily up to that point.

In early 2017, in recognition that continued strong growth of interest-only loans was contributing to rising risks, APRA further tightened standards on interest-only lending. Among other things, banks were required to limit new interest-only lending to be no more than 30 per cent of new mortgage lending.6 Banks were also required to tightly manage new interest-only loans extended at high loan-to valuation ratios (LVRs).

The past year or so

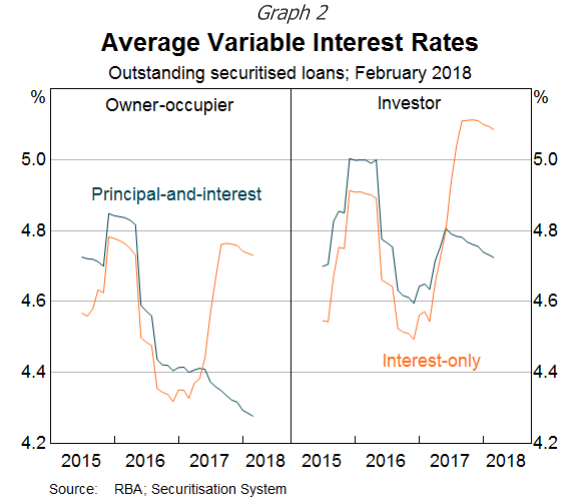

In response to those recent regulatory measures, the banks raised interest rates on investor and interest-only loans. From around the middle of 2017, the average interest rates on the stock of outstanding variable interest-only loans increased to be about 40 basis points above interest rates on equivalent P&I loans (Graph 2). Prior to that, there was little difference in interest rates on these loans.7

The higher interest rates contributed to a reduction in the demand for new interest-only loans. In addition, because banks had raised interest rates on all of their (variable rate) interest-only loans, existing customers had an incentive to switch their loans from interest-only to P&I terms before their scheduled interest-only periods ended. Many took up that option.8

The combination of higher interest rates and tighter lending standards contributed to the share of new loans that are interest-only falling comfortably below the 30 per cent limit. The stock of interest-only loans in total housing credit has also declined noticeably, from close to 40 per cent to almost 30 per cent.

This reduction in the stock of interest-only loans over the past year was substantial. It represented about $75 billion of loans (out of a total stock of interest-only loans of almost $600 billion in late 2016).

While many of the customers switching chose to do so in response to the higher rates on interest-only loans, there are likely to have been some borrowers who had less choice in the matter. Some borrowers may have preferred to extend their interest-only periods but may not have qualified in light of the tighter lending standards. We don't have a good sense of the split between those borrowers that switched voluntarily and those that switched reluctantly. However, our liaison with the banks suggests that most borrowers have managed the transition reasonably well. Also, the share of non-performing housing loans over the past year remains little changed at relatively low levels. Moreover, the growth of household consumption has been sustained; indeed it picked up a touch in year ended-terms over 2017.

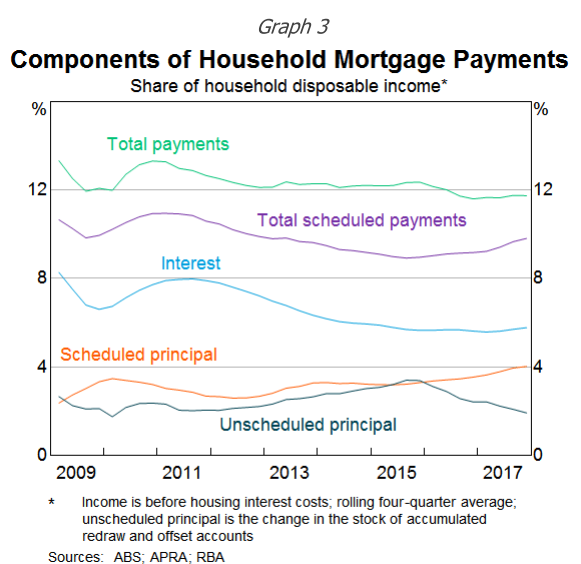

Given the large number of borrowers switching to P&I loans, it's not surprising that scheduled housing loan repayments have increased over the past year (Graph 3). Meanwhile, unscheduled payments have declined. With total payments little changed, the rise in scheduled payments has had no obvious implications for household consumption.

The next few years

So, many interest-only borrowers appear to have responded voluntarily to the pricing incentives and switched to P&I loans. This means that it is possible that the current pool of interest-only borrowers is a little more likely than usual to want to continue with their interest-only loans. For some of these borrowers, the decision not to switch to a lower interest rate P&I loan may reflect the higher required payments for such a loan.

Some commentators have gone so far as to suggest that when scheduled interest-only periods end, many borrowers will be forced onto P&I loans and will find it challenging to make the higher required payments.9 Commentators go on to suggest that such borrowers will either have to sell their property or reduce other expenditure significantly in order to service their loans.

In what follows, I'll explore these concerns by providing some estimates of the effect of borrowers switching to P&I loans in the years ahead. I'll focus my attention on the potential size of the change in households' cash flows as well as the effect on the household sector's consumption.

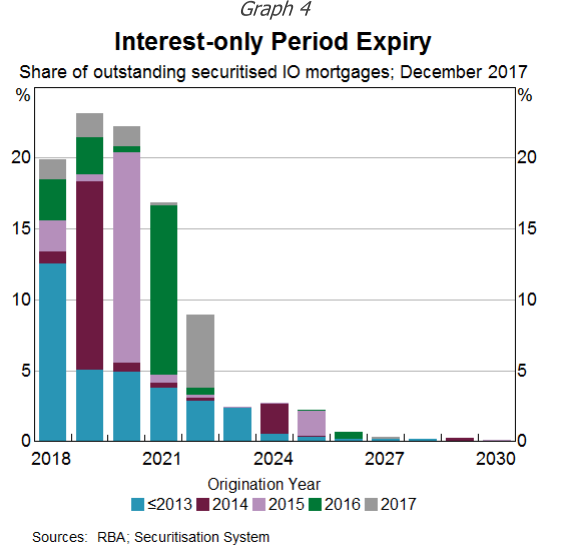

Around two-thirds of interest-only loans in the Reserve Bank's Securitisation Dataset are due to have their interest-only periods expire by 2020 (Graph 4).10 That is consistent with interest-only periods typically being around five years. Only a small share of loans have interest-only periods of 10 years (or longer), with very few loans on these terms having been written (and securitised) since 2015. This is in line with the earlier measures to tighten lending standards.

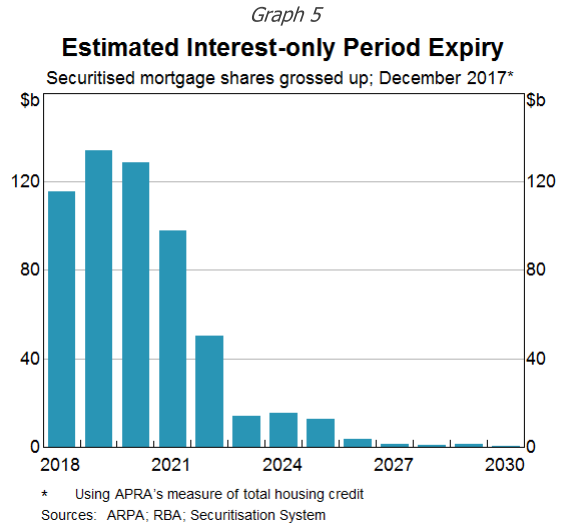

Applying this profile of expiries to the total value of all interest-only loans suggests that about $120 billion of interest-only loans is scheduled to roll over to P&I loans each year over the next three years (Graph 5). This annual figure is equivalent to around 7 per cent of the stock of housing credit outstanding.

While the value of loans scheduled to reach the end of the interest-only periods appears large, it is worth emphasising that expirations of this size are not unprecedented. At the end of 2016, a similar value of loans was due to have their interest-only periods expire in 2017. What is different now, however, is that many households have already switched willingly in 2017 in response to pricing differentials, and lending standards were tightened further in recent years. This could affect the ability of some borrowers to extend their interest-only periods or to refinance to a P&I loan with a longer amortising period so as to reduce required payments on the loan.

To estimate the effect of the expiry of interest-only periods, I'll consider the case where all of the interest-only periods expire as scheduled. While extreme, this provides a useful upper-bound estimate of the effect of the transition ahead.

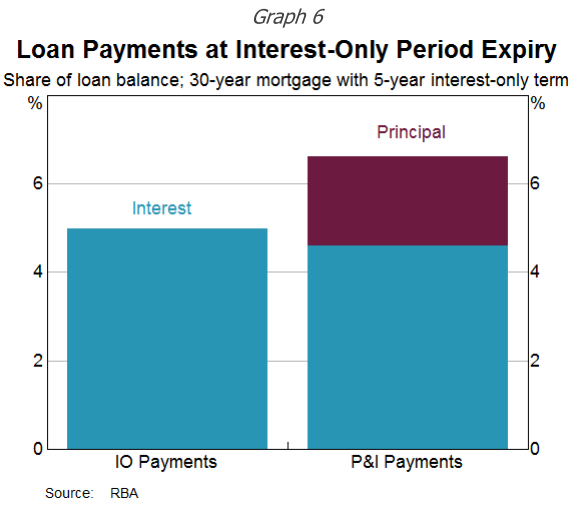

Consider a 'representative' interest-only borrower with a $400,000 30-year mortgage with a 5-year interest-only period.11 The left-hand side bar in Graph 6 shows the approximate interest payments (of 5 per cent) that such a borrower makes during the interest-only period. At the expiry of the interest-only period, required payments will increase by around 30-40 per cent (with an example shown in the bar on the right). (As shown in the graph, the interest rate applied to the loan is expected to be lower when it switches to P&I (by around 40 basis points) but this effect is more than offset by the principal repayments.)

The rise in scheduled payments amounts to about $7,000 per year for the representative interest-only borrower. This is a non-trivial sum for the household concerned.

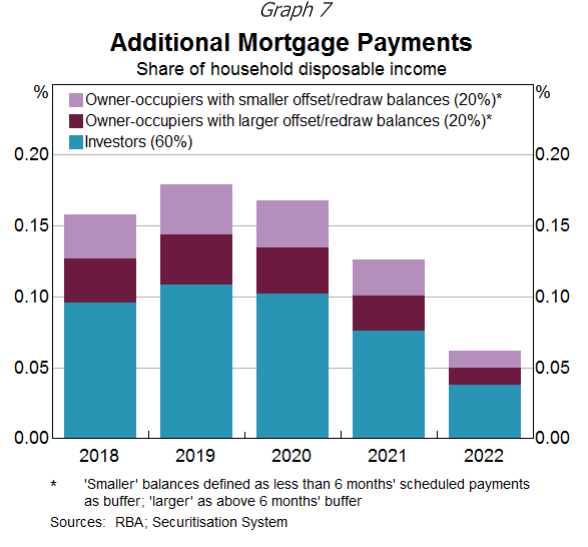

But how big is this cash flow effect when summed up across all households currently holding interest-only loans? Again, I adopt the extreme assumption that all interest-only periods expire as scheduled over the coming few years. As a share of total household sector disposable income, the cash flow effect in this scenario is estimated be less than 0.2 per cent on average per annum over each of the next three years (Graph 7).

For the household sector as a whole, this upper-bound estimate of the effect is relatively modest. Even so, there are a number of reasons why the actual cash flow effect is likely to be even less than this. More importantly, the actual effect on household consumption is likely to be lower still. So let me step through the various reasons.

Savings

Many borrowers make provisions ahead of time for the rise in required repayments. It is common for borrowers to build up savings in the form of offset accounts, redraw balances or other assets. They can draw upon these to cover the increase in scheduled payments or reduce their debt. Others may not even need to draw down on existing savings. Instead, they can simply redirect their current flow of savings to cover the additional payments. In either case, such households are well placed to accommodate the extra required payments without needing to adjust their consumption very much, if at all.

As shown in the chart above, about half of owner-occupier loans have prepayment balances of more than 6 months of scheduled payments. While that leaves half with only modest balances, some of those borrowers have relatively new loans. They wouldn't have had time to accumulate large prepayment balances nor are they likely to be close to the scheduled end of their interest-only period.

There are borrowers who have had an interest-only loan for some time but haven't accumulated offset or redraw balances of substance.12 Offset and redraw balances are typically lower for investor loans compared with owner-occupier loans. That is consistent with investors' incentives to maximise tax deductible interest. However, in comparison to households that only hold owner-occupier debt, there is evidence that investors tend to accumulate higher savings in the form of other assets (such as paying ahead of schedule on a loan for their own home, as well as accumulating equities, bank accounts and other financial instruments).13

Refinancing

Another option for borrowers is to negotiate an extension to their interest-only period with their current lender or refinance their interest-only loan with a different lender. Similarly, they may be able to refinance into a new P&I loan with a longer loan term, thereby reducing required payments. Based on loans in the Securitisation Dataset, a large majority of borrowers would be eligible to alter their loans in at least one of these ways.14

Any such refinancing will reduce the demands on a borrower's cash flows for a time. However, it is worth noting that by further delaying regular principal repayments, eventually those repayments will be larger than otherwise.

Extra income or lower expenditures

What about borrowers who have not built up savings ahead of time or are unable to refinance their loans? The Securitisation Dataset suggests that such borrowers are in the minority. More importantly, most of them appear to be in a position to service the additional required payments. Indeed, the tightening of loan serviceability standards a few years ago was no doubt helpful in that regard.

Some fraction of interest-only borrowers may have used the reduced demands on their cash flows during the interest-only period to spend more than otherwise. However, the available data, and our liaison with the banks, suggest that there are only a small minority of borrowers who will need to reduce their expenditure to service their loans when their interest-only periods expire.15

Sale of the property

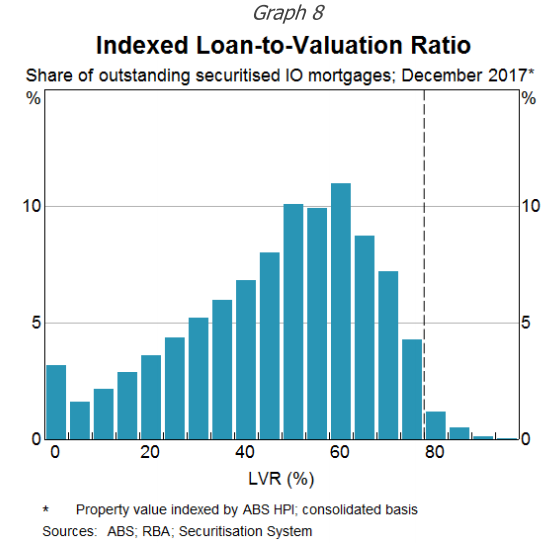

Finally, some interest-only borrowers may have to consider selling their properties to repay their loans. Difficult as that may be - most notably for owner-occupiers - doing so could free up cash flow for other purposes. It would also allow them to extract any equity they have in the property. The extent of that can be gauged by estimating LVRs from the Securitisation Dataset.16 The LVRs of almost all of those interest-only loans (both owner-occupier and investor) are below 80 per cent (based on current valuations and including offset balances) (Graph 8). This reflects the combined effects of loan serviceability tests and the increase in housing prices over recent years.

Some risks remain

While the various estimates I've provided suggest that the aggregate effect of the transition ahead on household cash flows and consumption is likely to be small, some borrowers may experience genuine difficulties when their interest-only periods expire. The most vulnerable are likely to be owner-occupiers, with high LVRs, who might find it more difficult to refinance or resolve their situation by selling the property.

Currently, it appears that the share of borrowers who cannot afford the step-up in scheduled payments and are not eligible to alleviate their situation by refinancing is small. Our liaison with the banks suggests that there are a few borrowers needing assistance to manage the transition. Over the past year, some banks have reported that there has been a small deterioration in asset quality. For some borrowers this has tended to be only temporary as they take time to adjust their financial affairs to cope with the rise in scheduled payments.17 For a small share of borrowers, though, it reflects difficulty making these higher payments. That share could increase in the event that an adverse shock led to a deterioration in overall economic conditions.

Conclusion

Today, I have discussed some of the risks associated with interest-only loans, which imply that their value as a form of mortgage finance has limits. I have also presented rough estimates of the likely effect of the upcoming expiry of interest-only loan periods. The step-up in required payments at that time for some individual borrowers is non-trivial. For the household sector as a whole, however, the cash flow effect of the transition is likely to be moderate. The effect on household consumption is likely to be even less. This is because some interest-only borrowers will be willing and able to refinance their loans. Also, many others have built up a sufficient pool of savings, or will be able to redirect their current flow of savings to meet the payments, or have planned for, and will manage, this change in other ways.

Indeed, the substantial transition away from interest-only loans over the past year has been relatively smooth overall, and is likely to remain so. Nevertheless, it is something that we will continue to monitor closely.

Finally, the observation that the transition is proceeding smoothly is not an argument that the tightening in lending standards on interest-only loans was unwarranted; far from it. The tightening in standards starting in 2014 has helped to ensure that borrowers are generally well placed to service their loans. And the limit on new interest-only lending more recently has prompted a reduction in the use of those loans during a time of relatively robust growth of employment and still very low interest rates. In this way, it has helped to lessen the risk of a larger adjustment later on in what could be less favourable circumstances.

1 This can be true even for investors today since (over a relatively long horizon) the benefit of the tax deduction can offset the cost of paying the higher interest rate on interest-only loans that now apply. Also, if the investor has attractive alternative investments, they may be willing to pay more for an interest-only loan.

2 The term 'bank' here refers to all authorised deposit-taking institutions, namely banks, building societies and credit unions, which are regulated by APRA.

3 Investors are sometimes given a clear option to extend into a second interest-only period, but that would normally proceed only after ascertaining that the borrower's financial position remains sound.

4 For more discussion of the risks associated with interest-only loans, see RBA (Reserve Bank of Australia) (2017), Financial Stability Review, April.

5 Strictly speaking, APRA imposed a 10 per cent benchmark on investor lending growth. If a lender breached that growth it would face higher capital charges and more scrutiny from APRA.

6 For details, see APRA (2017), 'APRA Announces Further Measures to Reinforce Sound Residential Mortgage Lending Practices', Media Release No 17.11, 31 March.

7 The gap between actual rates paid on interest-only loans and on P&I loans prior to 2016 largely disappears when we control for the differences between loan characteristics (such as loan size or LVR). For more details, see Kent C (2017), 'Some Innovative Mortgage Data', Address to Moody's Analytics Australia Conference 2017, Sydney, 14 August.

8 Indeed, lenders actively encouraged their existing interest-only borrowers to switch and allowed them to do so without penalty. Banks had an incentive to do so as their existing interest-only customers may otherwise have chosen to switch to a (lower rate) P&I loan with another lender.

9 For example, Shapiro J and Greber J (2017), The Australian Financial Review, 'Interest-only loans could be 'Australia's sub-prime', available at , 21 May; Hughes D (2018), The Australian Financial Review, 'Interest-only borrowers brace for mortgage crunch', available at , 17 January; and Kirby J (2018), The Australian, 'Interest-only crisis time bomb ticking as repayments rise', available at , 3 March.

10 The Reserve Bank collects detailed information on asset-backed securities it accepts as collateral in its domestic market operations. Most of the asset-backed securities in the dataset are underpinned by residential mortgages, covering around $400 billion of mortgages or about one-quarter of the total value of housing loans in Australia. Although the dataset is not representative of the entire mortgage market across all its dimensions, the aggregate share of interest-only loans in the Securitisation Dataset is similar to other measures that cover the broader housing market. For more details, Kohler M (2017), 'Mortgage Insights From Securitisation Data', Address to Australian Securitisation Forum, Sydney, 20 November.

11 This is based on the median loan size of interest-only loans from the Securitisation Dataset originated since 2013.

12 Fixed-rate loans do not allow substantial prepayments. Nevertheless, even those borrowers could be accumulating savings in other assets.

13 This is based on internal analysis using data from the survey of Household, Income and Labour Dynamics in Australia (HILDA).

14 To obtain these estimates, each borrower's maximum borrowing capacity is estimated using a measure aligned with APRA's prudential standards and conservative assumptions where possible (such as around minimum expenses). Also, borrowers who took out interest-only loans prior to 2015 are likely to have accumulated positive equity because of substantial price growth in recent years. This would help them to qualify for refinancing into a longer P&I term if they desired it.

15 The Australian Securities and Investment Commission has required eight lenders to provide remediation to borrowers that face financial stress as a direct result of poor lending practices related to interest-only lending. As yet, however, only a small number of borrowers have been identified as being eligible for such remediation action.

16 This is done by indexing property valuations (typically provided at the time a loan is originated) by a measure of housing prices and accounting for offset balances.

17 Banks can assist their borrowers experiencing temporary difficulties under their 'hardship programs', including by extending the interest-only period for brief period, for example.