Timothy Lane: Canada's economic expansion - a progress report

Remarks by Mr Timothy Lane, Deputy Governor of the Bank of Canada, to the Greater Vancouver Board of Trade, Vancouver, British Columbia, 8 March 2018.

I would like to thank Eric Santor and Garima Vasishtha for their help in preparing this speech.

Introduction

I am delighted to be spending International Women's Day here in Vancouver, a city that has long been a leader in fostering diversity, tolerance and inclusiveness.

Earlier today in Halifax, Governor Stephen S. Poloz and Finance Minister Bill Morneau unveiled the new $10 bank note, featuring a portrait of the late Viola Desmond.

Her story is an inspiring one. In 1946, Ms. Desmond, a Black Nova Scotian businesswoman, refused to leave a whites-only area of a movie theatre in New Glasgow and was jailed, convicted and fined.

She confronted this discrimination with grace and courage. And she made history, bringing forth the first known legal challenge against racial segregation by a Black woman in Canada. Her case was an inspiration for change and part of a wider set of efforts toward racial equality across the country.

The bank note will begin circulating later this year. I hope you'll agree that its imagery and symbols reflect the progress we have made as a nation-and the road still to be travelled-in the pursuit of human rights and social justice.

Now, I will turn from these lofty themes to the main topic of my speech today: Canada's continuing economic expansion, which has brought the Canadian economy close to its full potential. This is the setting for the monetary policy decision that we announced yesterday.

For those who may not know, we make eight decisions on the policy interest rate each year. Four of these come with the publication of our quarterly Monetary Policy Report, which provides a complete forecast and detailed explanation of how we see risks to our inflation outlook evolving. The Governor and Senior Deputy Governor hold a press conference the same day.

Until now, the other four decisions would come with only a press release-about one page long.

We've decided that, starting today, one member of the Bank's Governing Council will also give a public speech-an "economic progress report"-a day or so after each of these four interest rate announcements. The idea is to shed further light on how we see the economy evolving and the considerations that figured most prominently in our deliberations.

So, this speech kicks off a new initiative-another step in our ongoing efforts to help Canadians better understand our actions and decisions as Canada's central bank.

Now, let me begin.

Global and Canadian economic developments

The Canadian economy is progressing well. Following a decade of many setbacks, 2017 was a year of robust economic growth-3 per cent for the year as a whole.

After many years in which the growth was uneven, it has become more balanced.

The material slack that existed in the economy, and especially in the labour market, has been largely absorbed. Inflation is running close to our target rate of 2 per cent. While the future is subject to some notable uncertainties, which I'll discuss, trends over the past few quarters have been quite encouraging. The trends have been broad-based across regions and sectors, but these favourable economic conditions are particularly evident in some parts of Canada, including British Columbia.

Global developments

Of course, Canada is a very open economy, and its growth is supported by what is now a synchronous global expansion. This too is encouraging. We are now seeing solid growth not only in the United States and China but also in Europe, as well as in many other emerging-market economies.

The US economy has been on a path of mostly solid growth and job creation for a few years. At the beginning of 2018, the data indicated stronger momentum for the United States, and the tax cuts announced just before Christmas were expected to boost demand further. Developments since then have largely supported this story. US economic growth remained robust, at an annual pace of 2.5 per cent during the fourth quarter of 2017, and the US economy is essentially at full employment, with the jobless rate at a 17-year low. Wage growth has also edged up in recent months. Meanwhile, US business confidence remains high. And increases in government spending legislated in February are likely to provide a further boost in the next couple of years.

The US economic picture still has upside potential. The current expansion could create a virtuous circle, triggering "animal spirits" among businesses and consumers and driving even faster growth than expected. If that happened, stronger business investment and household spending in the United States would likely benefit our economy. So, as always, we are watching developments in the United States closely.

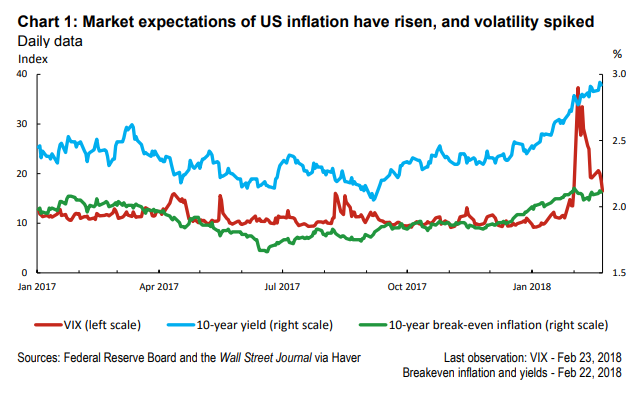

On that note, we saw some sharp movements in US and global stock markets a few weeks ago, ushering in increased market volatility (Chart 1). While these shifts were clearly amplified by technical factors-and, of course, markets are prone to overreaction-the repricing reflects a shifting economic outlook.

Market expectations about the path for inflation in some major advanced economies have been shifting upward-in the United States, for example, where inflation had persistently been running short of target. The shift in expectations about inflation and the strength of the global economy brings forward, to some degree, market expectations of less stimulative monetary policy. Over time, rising bond yields in the United States can be expected to put upward pressure on yields elsewhere, including in Canada. In effect, as markets digest what the changing dynamics could mean for central banks, markets themselves are bringing about some of the tightening that would be consistent with an improving world economy.

The rise in volatility came after a long period of exceptional calm in global financial markets-not just in stock markets but also in fixed-income markets. That tranquility reflected, at least in part, the influence of monetary policy: in many advanced economies, policy interest rates have been constrained by their effective lower bounds, and their central banks have relied on unconventional tools, including quantitative easing and forward guidance. As the global economic expansion becomes more secure, we may be reaching a turning point where the volatility-suppressing effects of monetary policy are diminishing and more normal levels of volatility are returning to markets.

At the same time, the global outlook remains subject to considerable uncertainty, notably around geopolitical developments and increasing protectionism. I'll talk more about this uncertainty a little later.

Canadian developments

Turning back to Canada, as I've said, 2017 was a year of robust growth for our economy.

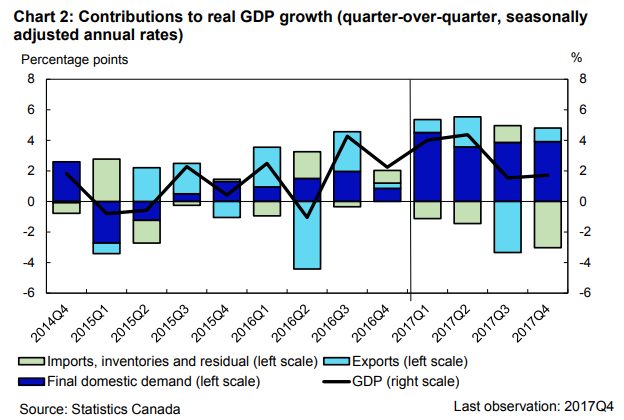

We were expecting growth to moderate to a more sustainable pace going into 2018, and the latest National Economic Accounts data confirm that it has. In fact, growth of real gross domestic product (GDP) during the fourth quarter of 2017 slowed more than we anticipated in our January forecast. Yet, even as the annual pace of growth came in at 1.7 per cent, under the 2.5 per cent pace in our projections, the underlying details suggest that the economy is progressing much as we thought it would. Specifically, what we economists refer to as "final domestic demand" increased at around a 4 per cent pace for a fourth consecutive quarter (Chart 2).

The slower-than-expected headline GDP growth number was largely due to higher imports, while exports made only a partial recovery from their third-quarter decline. The gain in imports mainly reflected stronger business investment, which adds to the economy's capacity. There were also some temporary factors influencing imports in the fourth quarter.

In addition, housing and government spending contributed more than expected to economic growth. On that note, we'll incorporate the implications of the recent federal budget for the outlook for growth and inflation in the Bank's April projection.

All that said, uncertainty about the North American Free Trade Agreement (NAFTA) and growing global trade tensions will need to be watched, for their possible impact on the outlook. Recent developments with respect to steel and aluminum, alongside increased protectionist rhetoric, carry potentially serious consequences. We do not know how or when the NAFTA talks or other trade disputes will conclude, and we do not know how industries, or governments, will react. The range of possibilities is wide, which means that trying to quantify any scenario in advance would not be useful for monetary policy purposes. For now, our working assumption is that existing trade arrangements will stay in place over our current two-year projection horizon. As and when concrete outcomes emerge, we will be in a better position to assess their impact on the Canadian economy.

But even with no changes in our trading arrangements, the uncertainty around them is affecting business investment decisions. The US tax reforms may further reduce the relative attractiveness of investing in Canada. For both these reasons, firms may decide to redirect some of their planned investment spending from Canada to the United States. Our economic projections have been incorporating the judgment that such effects are likely to dampen business investment-as discussed in January. As we prepare our April forecast, we'll assess whether the degree of caution we've applied is still appropriate. An important indicator will be our spring Business Outlook Survey (BOS), which we will publish on April 9.

There are a couple of additional points to note on the export and investment picture.

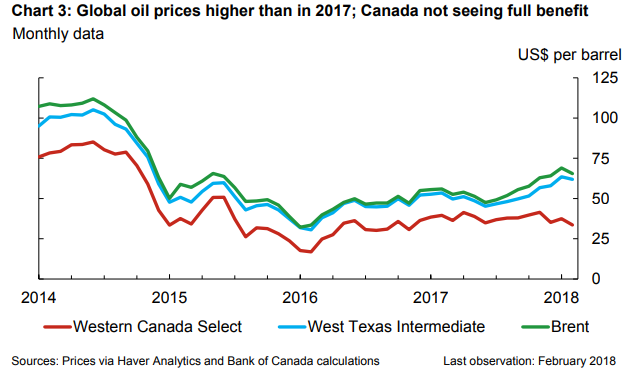

First, with respect to energy exports, spot prices for crude oil have fallen since we published our January forecast, but remain relatively high compared with 2017 (Chart 3). However, Canada is not seeing the full benefit of oil's recovery because of wider-than-average differences between benchmark global oil prices and prices for Canadian heavy oil. To the extent that these differences stem from ongoing transportation bottlenecks, we expect them to persist. This could have a dampening effect on investment in the energy sector.

In addition, although Canadian manufacturing activity has been solid in recent quarters, non-energy goods exports could disappoint, given ongoing competitiveness challenges. Indeed, in 2017, these challenges meant Canada was unable to benefit fully from a strengthening in global trade.

Another key element of our economic outlook is household spending-consumption and residential investment. In our January projection, this spending was expected to remain solid, while contributing less to growth as we go forward.

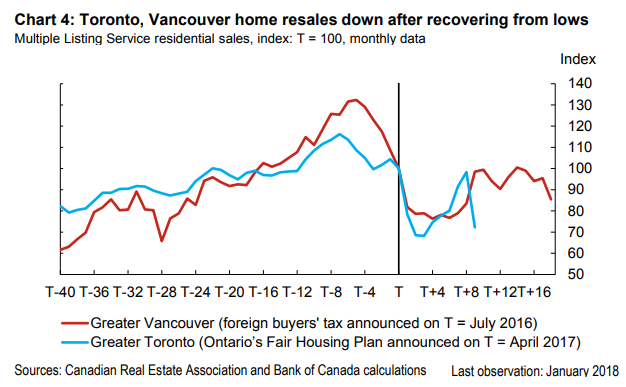

But there are a lot of moving parts. The effects of various provincial government measures in British Columbia and Ontario are still working their way through major housing markets. Federal authorities introduced new mortgage underwriting guidelines, which came into effect on January 1. And higher interest rates are also expected to dampen household spending. This effect is likely to be stronger than in the past, since the average household is now more heavily indebted.

The timing of these effects can vary and is hard to predict. For example, we expected that some home resale activity would be pulled forward into the last quarter of 2017 as buyers and sellers tried to book transactions before new underwriting guidelines took effect. The strong pace of resales late last year and the recent sizable drop (Chart 4) appear consistent with that pull-forward idea. But it's too early to tell how all these measures-not to mention measures that the BC government announced two weeks ago-will affect housing markets over the longer term.

We will continue to watch the data closely. We will also continue to assess how sensitive consumption is to higher interest rates, given high household debt. On that front, it's worth noting that household credit growth has been decelerating in recent months. It's still too early to firmly call it a trend, and credit data can be volatile, but it's what one would expect to see.

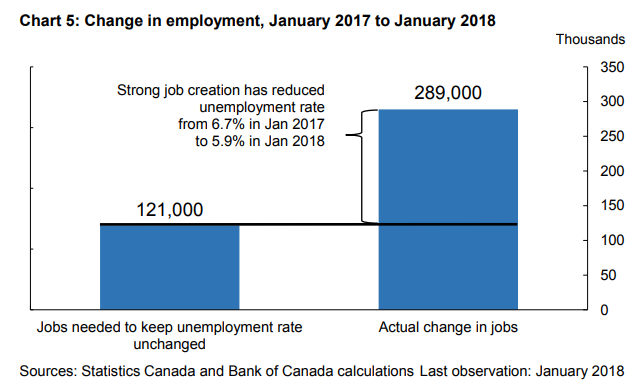

Turning to labour markets, despite a fall back in January, Canada has made considerable progress in job creation over the past year, notably with strong gains in full-time employment. The jobless rate is consequently near a historically low level (Chart 5). Wage growth has firmed, although it remains slower than would be typical in an economy with no labour market slack. Going forward, we will be monitoring the extent to which minimum-wage increases in key provinces may be affecting broader wage pressures. For now, it is a bit early to say. Meanwhile, even as regions such as British Columbia experience wage pressures and intensifying labour shortages, the elevated long-term unemployment rate and relatively low youth participation rate nationally suggest that there is still some slack in the Canadian labour market. Reflecting this, the Bank's composite labour market indicator-which is designed to capture broad labour market developments-has fallen by less than the unemployment rate.

Now, I'd like to go into a bit more detail about inflation, both globally and in Canada.

Global and Canadian inflation dynamics

I mentioned earlier that recent developments in global financial markets would seem to reflect shifting expectations about the path for inflation in some advanced economies.

Only a few months ago, the fact that inflation in advanced economies, including the United States, the euro area and Japan, was either slowing down or remaining weak, despite material slack being absorbed, caused some to question whether the inflationary process may have structurally changed.

At a global level, there are a number of possible explanations for why inflation has been slow to pick up. For instance, there may be more leftover economic slack. Inflation expectations may have drifted lower in response to persistently low inflation. The competitive effects of the rise of the digital economy and ongoing globalization may be playing a role in holding down prices. Or it may simply be a matter of time: inflation never picks up smoothly and does not follow a mechanical process.

Our staff have been working hard to assess these possible explanations. To date, they've found no compelling evidence that the underlying inflationary process has changed globally. That's not to say it hasn't-we need to continue to study this. But for now, our view remains that key relationships remain intact. Given the depths of the post-crisis recession and varying degrees of slack in different economies, inflation has taken longer in some countries than others to materialize on a sustainable basis.

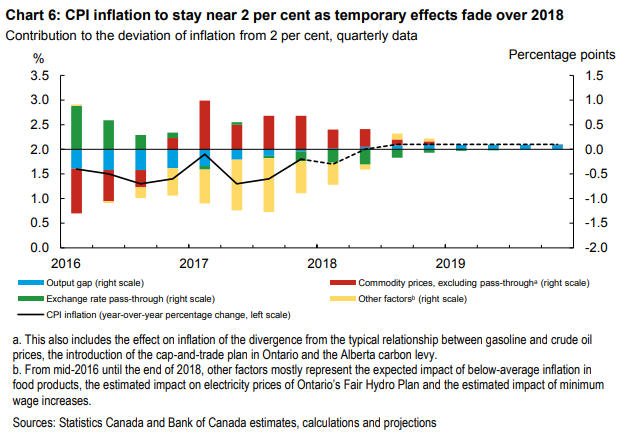

Meanwhile, here in Canada, inflation has lately been running close to our 2 per cent target. The Bank's core measures of inflation are also edging up, as we expected.

Still, inflation in Canada will be influenced this year by temporary factors related to gasoline, electricity and minimum wages. For example, we expected that inflation would drop temporarily below 2 per cent in January because of effects from gasoline prices a year earlier (Chart 6). But the decline in inflation, to 1.7 per cent, was a bit less than we had anticipated, reflecting a number of factors. Inflation is expected to climb back to around our target in the coming months as gasoline prices pick up on a year-over-year basis.

Our latest policy decision

That brings me to yesterday's decision to hold our policy rate, the target for the overnight rate, at 1.25 per cent.

This decision, as always, is grounded in our assessment of developments in the Canadian economy and what they mean for the outlook for inflation. In that regard, global and Canadian economic data have come in much as we expected. That confirmation gives us greater confidence that inflation will remain sustainably near our 2 per cent target.

Our decision yesterday also takes into account some important context. First, our policy rate remains appropriately below what we call the normal, or neutral, rate-the policy rate that would balance the economy in the longer run. We've estimated the neutral rate to be in the region of 2.5 to 3.5 per cent. I say it's appropriately below because accommodative monetary policy is working to offset several factors weighing on demand: persistent competitiveness challenges facing Canadian exports, the chilling effect of heightened uncertainty about future US trade policies, and the burden of high household debt levels.

The second piece of context is that, starting last summer, we increased our policy interest rate three times, for a total of 75 basis points. In these moves, we've been balancing the risk of undermining the economic expansion by moving too quickly with the risk of delaying too long and needing to raise rates sharply later to rein in inflation.

By moving gradually, we've been able to take in new data and conduct analysis on four key issues. First, when an economy is running close to full capacity, it can actually create more capacity as firms invest and discouraged workers are drawn back into employment. Second, as I've already discussed, inflation dynamics could be changing in the new economy, and it's important to understand those dynamics. Third, despite strong employment gains and an economy operating close to capacity, wage growth has been slower than would be expected. And, finally, with household debt at high levels, the economic effects of interest rate increases could be different than in the past.

In our deliberations for yesterday's decision, we took stock of recent developments related to these issues. As job creation has absorbed slack in the labour market, we have started to see wages pick up. With respect to the impact of higher interest rates on housing markets and the economy, although it is still too early to make a full assessment, we have seen a deceleration in household borrowing. And while it's also too early to tell how much additional potential output in the economy is being created, last week's strong investment figures are encouraging. We will be providing a fuller assessment of potential growth, as well as of the neutral interest rate, in our April Monetary Policy Report.

Conclusion

Allow me to conclude. All things considered, we decided yesterday that the current policy rate remains appropriate. While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target. My Governing Council colleagues and I will remain cautious in considering future policy adjustments, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.

Rest assured that, as always, the Bank of Canada will continue to do our part to ensure that we safeguard, and build on, the progress that has been made so far.